Investment Financial Risk Assessment in Fuyao Glass'

Internationalization Process

Zitao Wang

School of Accountancy, Tianjin University of Commerce, Guangrong Road 409, Beichen District Tianjin, China

Keywords: Fuyao Glass, Investment Risk, Multinational Enterprises, Manufacturing Industry.

Abstract: This study investigates the financial risk management challenges faced by Fuyao Glass during its international

expansion, with a focus on its U.S. investments from 2014 to 2020. By analyzing the company's financial

data, the research highlights two major risks: exchange rate volatility and structural market risks, which

significantly impacted Fuyao's profitability. The findings reveal large fluctuations in foreign exchange gains

and losses (ranging from ¥459 million in profits to ¥422 million in losses), underscoring the company's

exposure to currency risks despite its growing overseas revenue (55–65% of total income). The study applies

Miller's (1996) risk classification framework to assess Fuyao's strategies, demonstrating that while the

company successfully transitioned from trade to local manufacturing, its risk mitigation measures, particularly

in financial hedging, remained underdeveloped. Based on these insights, the paper proposes an integrated risk

management approach combining strategic financial tools, dynamic asset-liability matching, and specialized

team training. This research contributes to the understanding of financial risks in emerging-market

multinationals and offers practical recommendations for manufacturing firms expanding globally.

1 INTRODUCTION

1.1 Risk Identification Research

Scholars have developed a systematic theoretical

framework for classifying cross-border investment

risks. Miller (1996) pioneered a risk classification

system based on three dimensions: macro-

environmental risks, industry-specific risks, and

internal corporate risks, laying the foundation for

subsequent studies. Xu Hui and Yu Juan (2007)

expanded on Miller's framework by incorporating 15

key risk factors through empirical analysis, defining

investment risk as the potential losses arising from

uncertainties in cross-border operations, including

economic setbacks or investment failures. Chen Ning

(2011) further refined the classification logic by

proposing a "macro-meso-micro" three-dimensional

risk analysis model, enhancing the theoretical

inclusivity of risk categorization. This evolution

reflects the deepening academic understanding of

cross-border investment risks.

In macro-level research, scholars have focused on

political, legal, and financial risks in host countries.

Usher (1965) was among the first to highlight the

impact of political instability on foreign investments.

Liu Hongxia (2006) expanded this perspective by

categorizing political risks into three dimensions:

regulatory and service risks, overseas protection risks,

and investment environment risks, thereby extending

the analysis to include both home and host country

dynamics.

In the economic risk domain, Pantzalis et al. (2001)

explored the relationship between multinational

enterprises' geographic dispersion and risk exposure,

finding that broader subsidiary distribution reduces

exchange rate risk. Liao Wangke (2011) introduced

the concept of "country risk," emphasizing unique

challenges in cross-border economic activities. Yang

Da (2020) further classified risks into economic and

non-economic categories, demonstrating the

significant impact of RMB exchange rate fluctuations

on Chinese outbound investments.

At the meso level, scholars like Liang Yingying

(2014) and Cai Chengbin (2019) examined industry-

specific risks, particularly tax rates and cost structures.

Micro-level research, represented by Zhang Youtang

and Huang Yang (2011), highlighted internal risks

such as unfamiliarity with foreign financing policies

and overlooked factors like corporate social

Wang, Z.

Investment Financial Risk Assessment in Fuyao Glass’ Internationalization Process.

DOI: 10.5220/0014350500004718

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 2nd Inter national Conference on Engineering Management, Information Technology and Intelligence (EMITI 2025), pages 259-265

ISBN: 978-989-758-792-4

Proceedings Copyright © 2025 by SCITEPRESS – Science and Technology Publications, Lda.

259

responsibility and environmental standards (Zhu

Xinglong, 2016).

1.2 Risk Mitigation Measures

After identifying risks, effective mitigation strategies

are crucial. Scholars have proposed approaches

ranging from risk early-warning systems to tailored

policies for different investment stages.

Tyebjee and Bruno pioneered a combination of

qualitative analysis and quantitative research to first

identify key risk factors, and then used a

questionnaire survey method to construct a risk

project evaluation model suitable for the US market.

Their research results indicate that a company's

operational management capabilities and risk

resilience significantly influence the expected level of

risk (Tyebjee & Bruno, 1984). Huang Li and Li

Wanchao adopted case study and statistical analysis

methods, selecting eight industrial enterprises as

research samples. They screened out eight core

financial indicators, including the quick ratio and

equity ratio, using a significance T-test, and

successfully constructed an enterprise financial early

warning system using principal component analysis

(Huang Li & Li Wanchao, 2003). These studies

demonstrate the methodological evolution from

qualitative identification to quantitative modeling,

providing diversified analytical tools for assessing

risks in cross-border investments.

(1) Preventive measures based on different

investment stages

Zhang Liulu innovatively divides the cross-border

investment process into three key stages and proposes

differentiated risk management strategies tailored to

the characteristics of each stage: During the

investment decision-making phase, the focus is on

conducting a systematic analysis of project feasibility

and risk sources to provide a basis for investment

evaluation; during the investment implementation

phase, the emphasis is on dynamically adjusting

investment strategies based on actual operational

performance; and during the investment recovery

phase, the primary focus is on political risk factors,

conducting a comprehensive assessment of project

sustainability and ensuring the safe recovery of

investment costs (Zhang Liulu, 1997). The

introduction of this phased risk management

framework not only enhances the theoretical

framework of transnational investment risk

management but also provides enterprises with

comprehensive risk prevention and control guidance

throughout the entire lifecycle of cross-border

investment decisions in practice.

1.3 Research Objectives

This study aims to analyze the financial risks

involved in Fuyao Glass's internationalization

process, with a focus on the impact of exchange rate

fluctuations and market structure risks on its cross-

border investments. By evaluating Fuyao's financial

data from its investments in the United States

between 2014 and 2020, the study identifies

shortcomings in its risk management system and

proposes an integrated risk management framework

combining strategic planning, financial tool

application, and organizational optimization. This

framework provides theoretical insights and practical

recommendations for the globalization practices of

Chinese manufacturing enterprises.

2 FUYAO GLASS INVESTMENT

CASE STUDY

2.1 About Fuyao

Fuyao Glass Industry Group Co., Ltd. (hereinafter

referred to as Fuyao Glass) was established in Fuzhou,

Fujian Province, China in 1987. It is mainly engaged

in the manufacture of automotive glass, float glass,

and other industrial glass, and provides a full range of

services including research and development, design,

manufacturing, sales and distribution, and after-sales

service. It is currently the largest global glass

manufacturing enterprise in China.

2.2 History of Investment in the United

States

As shown in Table 1, in terms of investment scale, the

combined registered capital of all subsidiaries reached

US$173 million in 2014. The actual operational scale

expanded even more significantly: the total revenue of

the three companies reached RMB 233 million in 2014,

surged to RMB 1.3 billion in 2015 due to the

commencement of operations at Fuyao USA, and

stabilized at around RMB 1.5 billion thereafter.

Among these, Fuyao America contributed the

majority of revenue (977 million RMB), while the

North American subsidiary also achieved rapid

growth (from 174 million RMB to 522 million RMB).

This development trajectory reflects Fuyao's strategic

upgrade from exploratory trade to deep localization in

manufacturing, achieving internationalization through

substantial capital investment to establish a complete

domestic supply chain system in the United States.

EMITI 2025 - International Conference on Engineering Management, Information Technology and Intelligence

260

Table 1: Balance of Fuyao Glass’ long-term equity investment in U.S. subsidiaries(in millions of dollars)

Company/Time 2014 2015 2016 2017 2018 2019 2020

Fuyao America 71700 97704 97704 97704 97704 97704 97704

North American Package 17367 33074 33074 45657 52162 52162 52162

Fuyao North America 5885 5885 5885 5885 5885 5885 5885

ADD UP THE TOTAL 23258 120955 136662 149246 155751 155751 155751

Data source: Fuyao Glass Annual Report

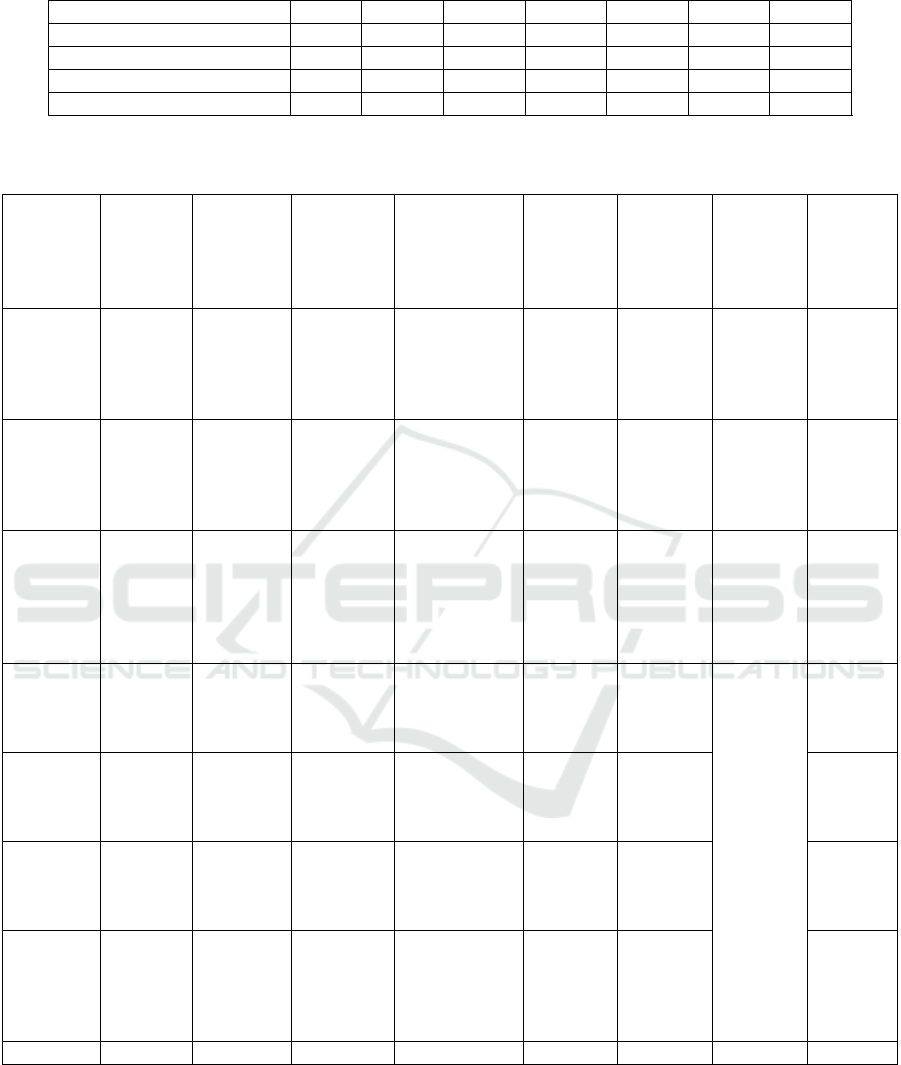

Table 2: Formation of Fuyao Glass U.S. subsidiaries.

NAME OF

SUBSIDIA

RY

ACRONY

MS

REGISTER

ED

CAPITAL

(US$

MILLION)

INVESTME

NT TIME

COMMISSION

ING TIME

MIAN

AREAS

OF

BUSINES

S

NATURE

OF

BUSINES

S

SERVICE ACQUISI

TI ON

METHOD

American

Green

Banyan

(liquidated

in 2010)

—— 426 1994 American commercia

l enterprise

Automotiv

e glass

sales

Investmen

t

establishm

ent

Fuyao

Northern

Glass

Industry

Co., Ltd.

Fuyao

North

290 2004 South

Carolina,

United

States

commercia

l enterprise

Automotiv

e glass

sales

Investmen

t

establishm

ent

Fuyao

Glass North

America

Co., Ltd.

North

American

accessories

600 2010 2011 Michigan,

USA

manufactur

ing

company

Automotiv

e glass

processing

and sales

Business

combinati

ons under

non-

common

control

Fuyao

Glass

America,

Inc.

Fuyao

USA

16000 2014 2016 Ohio,

United

States

manufactur

ing

company

Automotiv

e glass

manufactur

ing and

sales

Investmen

t

establishm

ent

Fuyao

Glass

Illinois,

Inc.

Fuyao

Illinois

0.1 2014 2015 Illinois,Uni

ted States

manufactur

ing

company

Investmen

t

establishm

ent

Fuyao

America C

Asset

Company

US C

Assets

0.08 2014 Illinois,Uni

ted States

commercia

l enterprise

Investmen

t

establishm

ent

Fuyao

America

Asset

Company

A

Asset A in

the United

States

0.08 2014 Ohio,

United

States

commercia

l enterprise

Investmen

t

establishm

ent

Total 17316.26

Data source: Fuyao Glass Annual Report Summary

As shown in Table 2, Fuyao Glass' investment

strategy in the U.S. market has followed a clear

evolutionary path and expansion trajectory. From an

investment perspective, the company has undergone

a transformation from trade to manufacturing through

three distinct phases since its initial entry into the U.S.

market in 1994: the initial phase (1994–2010) focused

primarily on establishing trading companies,

including the establishment of Fuyao North America

Glass

Industry Co., Ltd. with a registered capital of

Investment Financial Risk Assessment in Fuyao Glass’ Internationalization Process

261

Data source: Fuyao Glass Annual Report Summary

Figure 1: Fuyao Glass Foreign Operating Income Percentage,2016-2020

USD 2.9 million; the intermediate phase (2010–2014)

saw a shift toward production-oriented investments,

such as the establishment of North America

Supporting Company in 2010 through a corporate

merger with a registered capital of USD 6 million;

and the later phase (starting in 2014) marked the

entry into a large-scale capacity expansion phase,

with an investment of USD 160 million to establish

Fuyao Glass USA Co., Ltd. and the establishment of

production bases in Ohio and Illinois.

3 FUYAO COMPANY RISK

IDENTIFICATION AND

MANAGEMENT MEASURES

3.1 Risk Identification at Fuyao

Company

When beginning to analyze Fuyao's risk

identification, Fuyao's unique corporate

characteristics determine its specific risks. In line

with the theme of this article, this section will

analyze Fuyao's current risks from the perspective of

internal financial risks.

Fuyao Glass's financial data from 2016 to 2020,

as shown in Figure 1, reveals the significant

exchange rate risks and market structural risks it

faces in its cross-border operations. From the

perspective of revenue structure, although the

proportion of domestic revenue increased from 34.47%

in 2016 to 45.73% in 2020, domestic revenue

experienced a negative growth rate of 11.84% in

2020, reflecting the substantial impact of overseas

market fluctuations on the company's overall

revenue. More notably, exchange rate risk exposure

is highlighted. Figure 2 shows exchange losses of

388 million yuan and 422 million yuan in 2017 and

2020, respectively, with corresponding foreign

currency statement translation differences of -295

million yuan and -495 million yuan for the respective

years. This significant two-way volatility (foreign

exchange gains of 459 million yuan in 2016 and 259

million yuan in 2018) indicates that the company's

foreign exchange risk management system has room

for improvement. Notably, exchange rate

fluctuations and revenue regional structure form a

dual risk overlap—even when domestic revenue

accounted for nearly 50% (in 2019), the company

still faced financial performance instability caused

by exchange rate fluctuations, indicating that Fuyao's

internationalization strategy has not yet established

an effective exchange rate risk hedging mechanism.

This financial risk characteristic typifies the core

challenges faced by manufacturing multinational

corporations in their global expansion: while seeking

to expand overseas markets to achieve revenue

diversification, they must also address the resulting

currency mismatch and exchange rate volatility risks.

The magnitude of data fluctuations indicates that

exchange rate factors have substantively impacted

the

stability of corporate profits, necessitating

0

500000

1000000

1500000

2000000

2500000

2016 2017 2018 2019 2020

Total operating revenue (in ten thousand yuan) Revenue from overseas operations

EMITI 2025 - International Conference on Engineering Management, Information Technology and Intelligence

262

Data source: Fuyao Glass Annual Report Summary

Figure 2: Fuyao Glass Exchange Gains and Foreign Currency Financial Statement Translation Differences,2016-2020.

enhanced utilization of financial instruments such as

forward foreign exchange contracts and optimization

of currency matching in overseas asset-liability

structures.

3.2 Fuyao Company's Cross-border

Investment Risk Management

As a multinational corporation, Fuyao Glass is

susceptible to the impact of exchange rate and

economic fluctuations, and its foreign exchange risk

management strategy urgently needs systematic

optimization. Facing the new normal of two-way

fluctuations in the RMB exchange rate after 2014, the

company should improve its risk management system

from three aspects: dynamic monitoring, use of

financial instruments, and team building.

3.2.1 Establish a Dynamic Exchange Rate

Risk Monitoring System

Companies need to establish a real-time, efficient

foreign exchange risk monitoring mechanism.

Specifically, they should integrate multi-dimensional

data sources: obtain real-time exchange rate data

through professional foreign exchange trading

platforms such as Bloomberg and Reuters; track

macroeconomic indicators using international

financial data terminals such as Wind and CEIC; and

combine this with detailed data on foreign currency

assets and liabilities from the company's internal

financial system to ensure data comprehensiveness.

In terms of monitoring frequency, foreign currency

asset and liability scales should be updated daily, risk

exposure reports should be generated weekly, and

monthly analyses should be conducted using

economic reports from authoritative institutions such

as the IMF and central banks to scientifically predict

exchange rate trends and provide data support for

decision-making.

3.2.2 Strategies for the Refined Use of

Financial Instruments

Companies should select financial derivatives

appropriately based on the characteristics of their risk

exposure and develop differentiated operational

strategies. First, currency swaps can be used for

hedging the risks associated with long-term foreign

currency debt, such as long-term liabilities in

overseas project financing or cross-border mergers

and acquisitions. When implementing such strategies,

it is essential to select compliant counterparties (such

as international banks), negotiate terms including

principal amounts, exchange rates, and tenors, and

conduct regular cash flow exchanges. The advantage

lies in locking in long-term exchange rates to

effectively mitigate volatility risks; however, it is

important to note the drawbacks of higher transaction

costs and lower flexibility. Second, forward foreign

exchange contracts are suitable for future foreign

currency receipts and payments with known amounts,

such as import/export trade receivables. Companies

can enter into contracts with banks to agree on future

exchange rates and amounts, with settlement at the

contract rate upon maturity. Its advantages include

-60000

-40000

-20000

0

20000

40000

60000

2016 2017 2018 2019 2020

exchange gain converted difference

Investment Financial Risk Assessment in Fuyao Glass’ Internationalization Process

263

simplicity and lower costs, but businesses must be

vigilant about the risk of adverse market exchange

rate movements at contract maturity. Third, foreign

exchange option management. Foreign exchange

options are suitable for high-uncertainty foreign

currency receipts and payments, such as potential

income from bidding on overseas projects.

Businesses pay an option premium to purchase call or

put options, gaining the right, not the obligation, to

trade at the agreed-upon exchange rate. The primary

advantage is controllable risk (with losses capped at

the option premium), but the higher cost of options

must be balanced against this benefit.

3.2.3 Strengthen Professional Team

Building and Process Optimization

Companies should establish a professional foreign

exchange management team, with members holding

qualifications such as CFA or FRM, and undergo

regular training in derivatives operations and risk

management. Additionally, a comprehensive

assessment mechanism should be established: prior to

transactions, develop hedging strategies based on risk

exposure, clearly define tool selection and

proportions (e.g., hedging ratios not exceeding 80%);

during transactions, dynamically monitor market

changes and adjust positions in a timely manner; post-

transaction, conduct monthly assessments of hedging

effectiveness, utilize VaR models for quantitative

analysis, and continuously optimize strategies. By

leveraging currency matching, dynamically adjusting

risk exposure, and employing financial tools with

precision, Fuyao Glass can establish a three-pronged

foreign exchange risk management system to

effectively mitigate the impact of exchange rate

fluctuations on operational outcomes. This

optimization approach aligns with the practical needs

of multinational corporations while also aligning with

the macro trend of exchange rate marketization

reforms.

4 CONCLUSION

First, Fuyao Glass's internationalization development

path exhibits the typical three-stage characteristics of

“trade-led, manufacturing-rooted, and supply chain

integration.” This evolutionary process validates the

core tenets of the stepping-stone theory, which posits

that emerging market enterprises can achieve rapid

globalization through resource leverage and

continuous leaps. However, as internationalization

deepens, the financial risks faced by enterprises also

exhibit increasingly complex characteristics,

particularly the compounding effects of exchange rate

risks and market structural risks.

Second, according to data analysis, Fuyao Glass's

exposure to exchange rate risks was relatively high

between 2016 and 2020, with fluctuations in foreign

exchange gains and losses reaching 880 million yuan

(from a gain of 459 million yuan to a loss of 422

million yuan), and fluctuations in foreign currency

statement translation differences reaching 860

million yuan. Such significant fluctuations not only

directly impact the stability of corporate profits but

also reflect the inadequacies of the current foreign

exchange risk management system. Notably, even as

domestic revenue accounted for over 45% of total

revenue, exchange rate fluctuations still significantly

impacted corporate performance, indicating that

business regional diversification alone cannot

automatically mitigate exchange rate risks. Third,

there are three key areas for improvement in risk

management: first, the use of financial derivatives is

relatively conservative, failing to fully leverage risk

hedging functions; second, the currency matching of

overseas assets and liabilities needs to be improved;

third, there is a lack of specialized foreign exchange

risk management teams and systematic risk

assessment mechanisms. These issues make it

difficult for companies to effectively respond to the

new normal of two-way fluctuations in the RMB

exchange rate.

Based on the above findings, this study

recommends that multinational manufacturing

enterprises should establish a “three-in-one” risk

management system: at the strategic level, establish a

risk preference framework aligned with the

internationalization process; at the operational level,

improve the combination of tools such as forward

contracts and currency swaps; and at the

organizational level, cultivate a specialized risk

management team. Additionally, it is particularly

important to integrate risk management into the entire

process of internationalization strategy to achieve

synergistic development between risk control and

business expansion. The theoretical value of this

study lies in combining traditional investment risk

theory with emerging market corporate practices,

thereby enriching the research perspective on cross-

border investment risk management. Practically, it

provides a referenceable risk management framework

for the globalization process of Chinese

manufacturing enterprises. Future research could

further explore the application of new risk

management tools in the context of the digital

economy, as well as the mechanisms through which

EMITI 2025 - International Conference on Engineering Management, Information Technology and Intelligence

264

geopolitical factors influence cross-border

investment risks.

REFERENCES

Cai, C. (2019). The impact of host country economic risks

on Chinese enterprises' overseas investment: An

analysis based on two dimensions of China's outward

direct investment and engineering project investment.

Macroeconomic Research, (04), 107-115.

Chen, N. (2011). Risk prevention in cross - border

operations of small and medium - sized enterprises from

the perspective of stakeholders. Modern Finance, (1),

54-59.

Huang, L., & Li, W. (2003). Application of principal

component analysis in empirical research on financial

forecasting. Statistics and Information Forum, (05), 83-

86.

Liang, Y. (2014). A study on the determinants and

strategies of China's outward direct investment. Nankai

University. (04), 93-95.

Liao, W. (2011). Response matrix analysis method for

transnational investment risk assessment. Technology

and Economy, (01), 56-63.

Liu, H. (2006). Research on the risks of Chinese overseas

investment and their prevention. Journal of Central

University of Finance and Economics, (03), 63-67.

Miller, K. D. (1996). A framework for integrated risk

management in the international business. Journal of

International Business Studies, (2), 311-331.

Pantzalis, C., Simkins, B., & Lluch, P. (2001). Operational

hedges and the foreign exchange exposure of U.S.

multinational corporations. Journal of International

Business Studies, 32(4), 793-812.

Tyebjee, T. T., & Bruno, A. V. (1984). A model of venture

capitalist investment activity. Management Science,

30(9), 300-330.

Usher, D. (1965). Political risk. Economic Development

and Cultural Change, 13(4).

Xu, H. (2004). Interactive research on risk perception and

international market entry strategy decision - making:

With a discussion on risk prevention in Chinese

enterprises' transnational operations. Exploration of

Economic Issues, (10), 10-12.

Xu, H., & Yu, J. (2007). A study on the identification of key

risks in enterprise internationalization. Nankai

Management Review, (04), 92-97.

Yang, D. (2020). The impact of RMB exchange rate

fluctuations on the risk of Chinese enterprises' outward

direct investment. Journal of Northeastern University

(Social Sciences Edition), 22(06), 24-30.

Zhang, L. (1997). Risks and prevention measures for

Chinese overseas investment. Journal of Henan

University (Social Sciences Edition), (03), 63 - 66+129.

Zhang, Y., & Huang, Y. (2011). Research on risk warning

and regional positioning of transnational investment by

enterprises. Accounting and Finance Bulletin, (31), 17-

20.

Zhu, X. (2016). Research on the risks of China's outward

direct investment and its prevention system. Wuhan

University. (06), 12-18.

Investment Financial Risk Assessment in Fuyao Glass’ Internationalization Process

265