AI‑Based Fraud Detection System for Financial Transactions

P. Muntaj Begum, G. Lilly, K. Madhavi, B. Sabeena and S. Likhitha

Department of Computer Science and Engineering, Ravindra College of Engineering for Women, Kurnool, Andhra

Pradesh, India

Keywords: Fraud Detection, Anomaly Detection, Machine Learning, Artificial Intelligence, Financial Fraud, Credit Card

Fraud, Real‑Time Analytics, Cybersecurity, Fraud Prevention.

Abstract: In the rapidly evolving digital financial ecosystem, fraud detection remains a critical challenge due to the

increasing sophistication of fraudulent activities. This paper introduces Fraud Guard, an AI-based system

created to detect and prevent deceptive financial transactions. using machine learning techniques. The system

leverages Random Forest, Decision Tree, and Logistic Regression to analyze credit card transaction data,

ensuring high precision and recall in fraud detection. Advanced feature engineering, anomaly detection, and

external data sources like IP geolocation enhance its effectiveness. To solve key challenges, including

imbalanced datasets, real-time detection, and adaptive learning, the system integrates data analytics, artificial

intelligence, and deep learning to identify suspicious patterns while minimizing false positives. Fraud Guard

continuously evolves to detect emerging fraud trends, ensuring robust and scalable fraud prevention. By

implementing this AI-powered approach, financial institutions can enhance transaction security, safeguard

customer funds, and mitigate financial fraud risks, including Various types of fraud, including credit card

fraud, insurance fraud, securities fraud, insider trading, and money laundering.

1 INTRODUCTION

The banking sector has undergone significant

transformation since the introduction of Internet

banking in 1996 by Citibank and Wells Fargo Bank in

the United States (K. Yak, D. Tudeal 2011). This

innovation marked the beginning of online credit card

transactions, which have grown exponentially over

the past decade. The rise of e-commerce, online

payment systems, remote work, digital banking,

and social networking platforms has revolutionized

how individuals conduct financial activities (S.

Madan et al. 2021). However, this shift has also

created opportunities for fraudsters to exploit

vulnerabilities in online payment systems, leading

to an increase in fraudulent activities targeting

digital transactions (F.C. Yann 2018).

Advancements in digital technologies have

reshaped how people handle money, transitioning

from traditional physical payment methods to digital

platforms (V. Nath 2020). This transformation has

enabled economies to enhance productivity and

maintain competitive advantages through

technological integration (T. Pencarelli 2019).

Internet banking and online credit card transactions

now offer unparalleled convenience, allowing users to

manage their finances from home or office. A credit

card, as defined by (S.B.E. Raj 2011), is a plastic card

embedded with personal information issued by

financial institutions to facilitate global purchases

Credit card fraud happens when someone uses

another person’s card details without permission to

get money or property, either physically or digitally.

Such fraudulent activities often result in significant

financial losses, exacerbated by the ease of

committing fraud in online environments where

physical possession of the card is unnecessary (S.B.E.

Raj 2011).

The Bank of Ghana (BoG reported a staggering

548.0% year-on-year increase in credit card fraud

losses, rising from GH¢ 1.26 million ($250,000) in

2019 to 2020, with the amount increased to GH¢ 8.20

million (approximately $1.46 million) (V. Nath

2020). Fraud incidents span various payment

channels, with digital transactions experiencing the

highest growth. Checks, deposits, P2P transfers, wire

transactions, ACH transfers, online payments, bill

payments, card usage, and ATM operations (S.

Madan et al. 2021). Fraudsters use advanced methods

like VPN tunnels with Anchor-free software or fake

Begum, P. M., Lilly, G., Madhavi, K., Sabeena, B. and Likhitha, S.

AI-Based Fraud Detection System for Financial Transactions.

DOI: 10.5220/0013914200004919

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 1st International Conference on Research and Development in Information, Communication, and Computing Technologies (ICRDICCT‘25 2025) - Volume 4, pages

421-428

ISBN: 978-989-758-777-1

Proceedings Copyright © 2026 by SCITEPRESS – Science and Technology Publications, Lda.

421

identities, making detection and capture difficult

(F.C. Yann 2018).

To tackle these challenges, compliance and risk

management systems now use AI and machine

learning for fraud detection (S. Madan et al. 2021).

"Techniques like Decision Trees, Logistic

Regression, Random Forests, AdaBoost, XGBoost,

SVM, and LightGBM are effective for classification

and prediction in credit card fraud detection (T.

Pencarelli 2019). Supervised machine learning

models excel at identifying fraudulent transactions,

showing high performance for this task (S.B.E. Raj

2011).

This study compares XG-Boost, Logistic

Regression, and Random Forest to classify and

predict legitimate or fraudulent transactions. The

structure of the paper is as follows: Section 2 offers

an overview of relevant literature, Section 3 describes

the dataset, experimental configuration, and methods

employed, Section 4 showcases the analysis

outcomes are presented, followed by Section 5, which

explores the findings' implications, and Section 6,

which concludes with suggestions derived from the

study’s conclusions

2 LITERATURE REVIEW

Logistic regression is a statistical method employed

to predict binary outcomes. Unlike other methods,

explanatory variables do not necessitate to adhere to

a Normal Distribution or display low correlation

(B.G. Tabachnick et al. 1996). In logistic regression,

the outcome variable is qualitative, while explanatory

variables can be numerical or categorical. This

method has been widely adopted by researchers to

identify financial bankruptcies.

Decision trees are non-linear classification

methods that split a dataset into progressively finer

segments based on explanatory variables. At every

stage of the tree, the algorithm identifies the variable

that demonstrates the strongest relationship with the

target outcome, as determined by a specific criterion

(J.A. Michael et al. 1997). Being nonparametric,

decision trees do not assume any data distribution,

which allows them to be adaptable for managing both

numerical and categorical data structures. although,

decision trees are prone to overfitting when applied to

the entire dataset, which can lead to poor

generalization. Despite this limitation, they have

practical applications, such as spam email filtering

and identifying individuals at risk for certain diseases

within medical research.

Random forests, introduced by (L. Breiman, et al.

2001), enhance the bagging technique by introducing

additional randomness during tree construction.

While traditional decision trees select the best split

among all variables, random forests randomly select

a subset of variables at each node and choose the best

predictor from this subset. The final prediction is

determined by averaging the outputs produced by all

the trees. A random forest package in R facilitates the

implementation of these models (Liaw, M. Wiener

2002). One advantage of random forests is their ability

to measure the importance for each feature with

respect to the training dataset. Although, they might

show a bias toward Features having multiple levels

when handling categorical variables.

The Random forests identify applications in

various fields, including analyzing intricate

biological data within bioinformatics and performing

video segmentation and image classification for pixel

analysis.

The categories of credit card fraud identified by (O.

Citation 2009) include bankruptcy fraud, counterfeit

fraud, application fraud, and behavioral fraud.

Depending on the type of fraud encountered, banks

and credit card companies can design and implement

tailored preventive measures. To detect fraudulent

transactions across jurisdictions, Machine Learning

like Logistic Regression, Naive Bayes, Random

Forest, K-Nearest Neighbors, Gradient Boosting,

Support Vector Machines, and Neural Networks,

have been employed (A. Aditi et al. 2022). Using a

method based on feature importance to identify the

most significant features, Gradient Boosting achieved

an accuracy of 95.9%, outperforming other

algorithms.

A hybrid machine learning model combining

AdaBoost and majority voting strategies was

developed by (K. Randhawa et al. 2018) for credit

card fraud detection. Noise levels of 10 percent and

30 percent were introduced within the hybrid models

in order to test robustness. The majority voting

Method scored 0.942 under 30% noise, proving its

effectiveness in noisy environments. Similarly, (L.

Guanjun, et al. 2018) proposed two types of random

forests to model typical and abnormal transaction

behaviors. These models were tested on data from a

Chinese e- commerce company. Random forests

performed well on small datasets, but imbalanced

data reduced their effectiveness on larger ones (F.C.

Yann 2018).

In another study, (K. Ayorind) examined practical

methods to identify credit card scams, a significant

threat to financial organizations. The machine

learning algorithms were trained with under sampling

and oversampling. The Random Forest, XGBoost,

ICRDICCT‘25 2025 - INTERNATIONAL CONFERENCE ON RESEARCH AND DEVELOPMENT IN INFORMATION,

COMMUNICATION, AND COMPUTING TECHNOLOGIES

422

and Decision Tree performed best, with AUC values

of 1.00, 0.99, and 0.99, respectively.

2.1 Data and Module Data

The dataset contains 6,354,739 rows of simulated

online

payment transactions, featuring attributes like

transaction type (CASH_IN, CASH_OUT,

etc.),

amount, account balances, and fraud labels (is Fraud),

with a highly imbalanced distribution of fraudulent

activities. It includes temporal information (step) and

detailed sender/recipient balance changes, enabling

the analysis of transaction patterns and anomalies

indicative of fraud. This dataset is ideal for training

machine learning models to classify legitimate versus

fraudulent transactions while addressing challenges

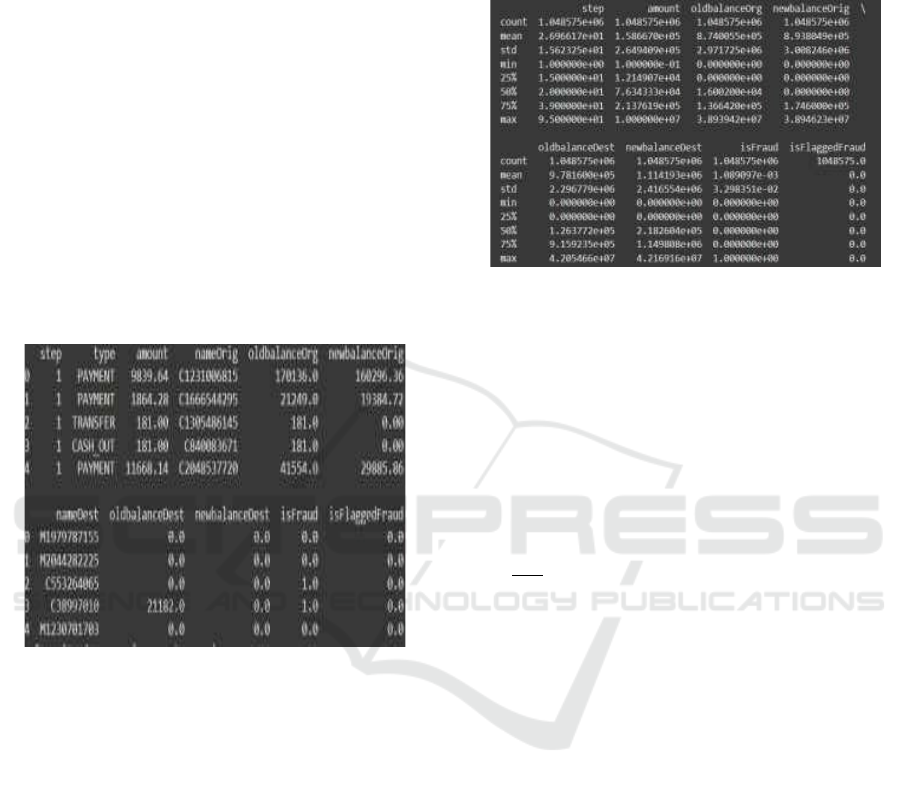

like class imbalance and feature engineering. Figure

1 represents the information of the dataset.

Figure 1: Information of the dataset.

2.2 Data Pre-Processing

During pre-processing, the Kaggle dataset was

refined and organized to remove null values for a

complete Evaluation. A clean dataset may be created

by transforming raw data via data pre-processing. To

put it another way, it is not fair to evaluate data that

has not been processed when it is collected from

several sources. Dataset adjustments done before

feeding the algorithm are known as pre-processing.

The key pre-processing steps are as follows:

• Missing and Null Values: Managing null

values is an essential part of data preparation.

Imputation and removal techniques are used

to handle missing data properly. This

ensures the honesty and quality of the dataset

before performing analysis or modeling

activities in research processes.

• Encoding Categorical Variables:

Typically, a collection of predetermined

categories is used to describe a variable's

possible values. Figure 2 shows the basic

statistics for the numeric variables.

Figure 2: Basic statistics for the numeric variables.

2.3 Data Scaling

Scaling is important for removing the noise of the

data. In this, data scaling is processed using a standard

scalar. Standard scalar makes use of z-score

normalization so that all values are converted to a

specific range. A widely used method for data

standardization is the Z-score normalization (Equ.1),

which can be defined as:

Z=

(

(1)

2.4 Data Balancing

A class imbalance issue occurs when there is an

excessive amount of data from one class about other

classes in a dataset. The majority of datasets used in

real-world applications have this kind of class

distribution, where several labels for one class are

much higher than several labels for another. The most

common methods for addressing the issue of class

imbalance may be broadly grouped into three types:

sampling/resampling, ensemble learning, and cost-

sensitive learning.

2.4.1 Feature Extraction

Feature extraction involves sorting all data into

categories after extracting the most important and

relevant information (FRAUD Kayode Ayorinde

2021). Collecting all important data or minimizing its

loss is of the utmost importance when dealing with a

big dataset. Feature extraction is a useful tool for

managing crucial data from large raw datasets and

lowering the incidence of data loss (V. Bolón-Canedo

AI-Based Fraud Detection System for Financial Transactions

423

et al. 2014). Several issues arise from a huge dataset.

Overfitting to training data occurs, and the model's

performance drops. It also uses a lot of memory and

runs slowly on processing resources. This is why

feature extraction is so useful; it uses the original

dataset to extract all the nonredundant values.

2.5 Models

2.5.1 Random Forest (RF)

The Random Forest Classifier was applied to detect

fraudulent transactions by constructing multiple

decision trees and aggregating their predictions. The

prediction function of Random Forest is given by:

𝑃

(

𝑌=1

|

𝑋

)

=

∑

ℎ

(𝑋) (2)

where ℎ

𝑡(𝑥)

represents the prediction from the

𝑡

𝑡ℎ

decision

tree, and T represents the total count of

decision trees within the forest. Each tree was trained

on a random subset of data using bootstrap sampling,

reducing overfitting and improving generalization.

The entropy criterion was used for splitting nodes,

ensuring optimal decision boundaries. The model's

performance was evaluated using the ROC- AUC

score, with separate calculations for the training and

validation datasets. A confusion matrix was plotted to

assess classification results, showing correct and

incorrect fraud predictions.

2.5.2 Logistic Regression (LR)

The Logistic Regression model was trained to

classify transactions as fraudulent or non-fraudulent.

The function is Defined as:

P

(

Y=1

∣

X

)

=

(

…

)

(3)

where P(Y=1∣X) represents the probability of

fraud, 𝛽

0

is the intercept, and 𝛽

1

, 𝛽

2,……

, 𝛽

𝑛

are the

coefficients for input features. 𝑋

1

, 𝑋

2

, … … . , 𝑋

𝑛

.The

model was evaluated using the

ROC- AUC score,

which measures the ability to distinguish fraudulent

from non-fraudulent transactions. The training ROC-

AUC score assessed model fit, while the validation

score showed performance on unseen data. The

confusion matrix further visualized the model's

classification performance, identifying correct and

incorrect fraud predictions.

2.5.3 XGBOOST Classifier

The XGBoost Classifier was trained on the dataset to

detect fraudulent transactions, and its performance

was evaluated using the ROC-AUC score. The

model. achieved a high ROC- AUC score, calculated

using the formula:

ROC − AUC =

∑∑

1(S

∈

∈

>S

) (4)

(4)

where 𝑁

0

and 𝑁

1

are the numbers of negative and

positive samples, and 𝑠

𝑖

and 𝑠

𝑗

are the predicted scores

for positive

and negative instances, respectively. The

XGBoost model's training ROC-AUC score was

significantly high, indicating excellent discrimination

between fraudulent and non-fraudulent transactions.

The confusion matrix showed the model’s accuracy

in classifying transactions, with few false positives

and negatives.

3 MODEL EVALUATION

An important aspect of developing a model is

evaluating it. Finding the optimal model to describe

our data and gauging the model's future performance

are both aided by this.

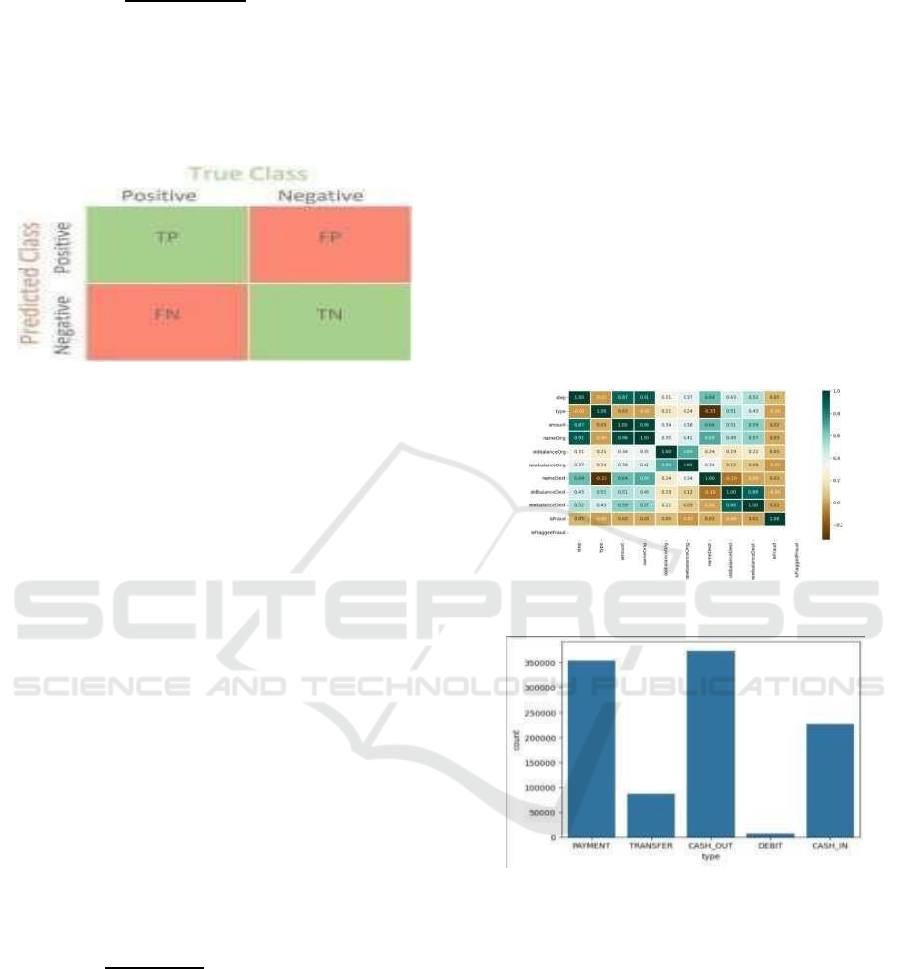

a) Confusion Matrix

The confusion matrix compares the actual classes

with the projected classes and displays the results in

tabular form. It shows how many samples were taken

from each quadrant. The model's projected True

Negatives, False Negatives,

3.1 Precision

Precision, also called positive predictive value, is the

ratio of true positives to all positive predictions.

𝑃𝑟𝑒𝑐𝑖𝑠𝑖𝑜𝑛 =

(5)

3.2 Recall

Equation 7 shows how to compute it by splitting a

proper positive number by the total number of

samples, which is a positive number.

𝑅𝑒𝑐𝑎𝑙𝑙 =

(6)

3.3 F1-Score

As shown, precision is determined by dividing the

total number of positive outcomes that were achieved

by the total number of positive results that were

predicted by the classifier.

ICRDICCT‘25 2025 - INTERNATIONAL CONFERENCE ON RESEARCH AND DEVELOPMENT IN INFORMATION,

COMMUNICATION, AND COMPUTING TECHNOLOGIES

424

𝐹1−𝑆𝑐𝑜𝑟𝑒=

∗∗

(7)

True Positives, and False Positives may be better

understood

with this information. This helps in

determining the model's accuracy in the classification

task. Figure 3 represented below is a confusion

matrix.

Figure 3: Confusion matrix.

• True Positive (TP): The number of

correctly detected with Np denoting an

amount of data at node Np and |Ni| denoting

an amount of data at node Ni, the data with

the 𝑗

𝑡ℎ

label as a percentage of the total data

at node Np is represented by Pj, and the

inequality 0 ≤ I ≤ c. indicates several positive

records are shown by TP.

• False Positive (FP): The FP proportion

represents the count of samples incorrectly

labeled as positive True Negative (TN): TN

displays the quantity of accurately identified

negative records. False Negative (FN): FN

refers to the count of positive samples

wrongly labeled as negative.

3.4 Accuracy

The main performance assessment parameter is

accuracy, which calculates a proportion of accurate

predictions to all of a classifier's predictions. may be

used to present it.

𝐴𝑐𝑐𝑢𝑟𝑎𝑐𝑦 =

(8)

4 RESULT ANALYSIS AND

DISCUSSION

A comparative analysis of fraud identification and the

prevention of financial transactions based on machine

learning approaches is provided in this section. The

analysis conducted four evaluation metrics, which

were performed: F1-Score, Accuracy, Precision, and

Recall. Some DL models were used. The table below

shows the comparison of different machines.

4.1 Exploratory Data Analysis

To better understand a data set's structure, trends, and

linkages, data scientists must first do exploratory data

analysis, often known as EDA. Exploratory Data

Analysis (EDA) empowers data scientists to reveal

the essential characteristics of data, pinpoint outliers,

analyze the distribution of features, andmercury is the

closest planet to sunM identify missing values. A key

advantage of EDA is its ability to improve the

performance and reliability of predictive models.

Figure 4 shows the visualization of data is provided

below.

Figure 4: Co-relation matrix of the dataset.

Figure 5: Count plot for label.

The bar chart represents the count of different

transaction categories. The x-axis indicates the

transaction categories, and the y-axis indicates the

count of every type. Below is the description of the

data figure 5 shown in the chart:

PAYMENT: Approximately 350,000 transactions.

TRANSFER: Around 90,000 transactions.

CASH_OUT: The highest, with more than 370,000

transactions.

DEBIT: The least, with a very small count. CASH_IN:

About 200,000 transactions.

This visualization shows that CASH_OUT and

PAYMENT transactions are the most frequent, while

AI-Based Fraud Detection System for Financial Transactions

425

DEBIT transactions are the least common.

4.2 Experiment Results

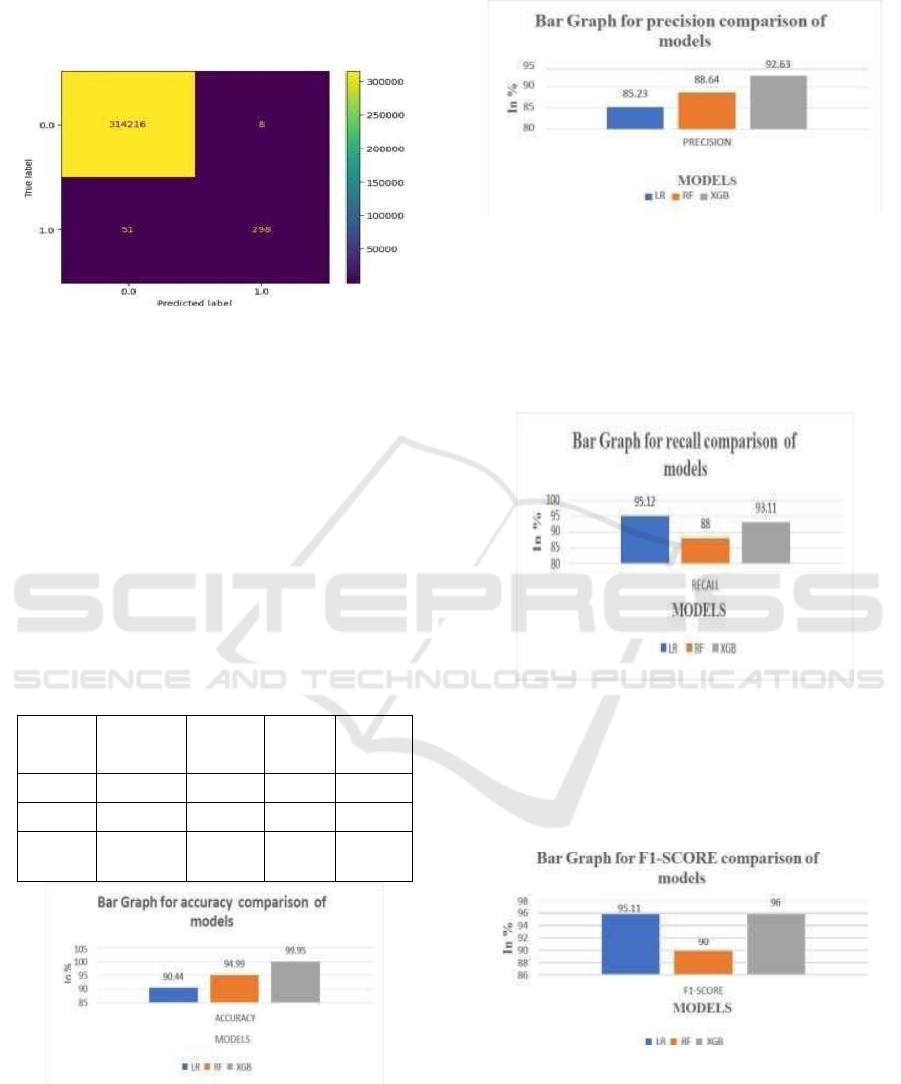

Figure 6: Confusion matrix for XGBoost.

The confusion matrix shows that the model correctly

classified 314,216 negative cases (TN)and 298

positive cases (TP). It misclassified 8 negatives as

positives (FP) and 51 positives as negatives (FN). The

model achieved 99.98% accuracy, with 97.38%

precision and 85.38% recall for the positive class.

While the model performs well overall, it misses

some actual positive cases, leading to a slightly lower

recall. Improving the recall for the positive class

could enhance the model’s ability to detect more true

positive instances. Table 1 shows the comparison

between various models.

Table 1: Comparison between various models.

Models Accuracy

Precisio

n

Recall

F1-

Score

RF 94.99 88.64 95.12 76

LR 90.44 85.23 72.56 78.63

XGB 99.95 92.38 88.26 90.63

Figure 7: Bar graph of accuracy comparison of models.

The bar graph comparing the accuracy of many

models is shown in Figure 7. In the accuracy

comparison, XGB scores highest at 99%, followed by

RF at 94.99% and LR at 90.44%. This indicates XGB

is the most accurate model compared to other models.

Figure 8: Bar graph of precision comparison of models.

The above figure 8 shows the comparison model for

the precision bar graph of different models. In this,

XGB achieves the highest precision of 92.63, and the

lowest precision is of the Logistic Regression with

85.23%

Figure 9: Bar graph for recall comparison of models.

The following figure 9 shows the Bar Graph for the

Recall comparison of models. In this comparison, LR

recall of 95.12%, and XGB recall is 93.11%. While

Random Forest (RF)shows the lowest recall at 88.

Figure 10: Bar chart for F1-score comparison across

models.

Figure 10 presents a comparison of F1-Scores

across various models. XGB Classifier achieves the

highest F1- score of 96%, showing a strong balance

between precision and recall. Logistic Regression

ICRDICCT‘25 2025 - INTERNATIONAL CONFERENCE ON RESEARCH AND DEVELOPMENT IN INFORMATION,

COMMUNICATION, AND COMPUTING TECHNOLOGIES

426

(LR) follows closely with an F1-score of 95.11%.

Finally, the comparison of the F1- score sheds light on

the models’ total performance in terms of

classification accuracy with the overall F1-score that

seems to accurately measure the quality of the models

achieving high scores for both precision and recall.

5 CONCLUSIONS AND FUTURE

SCOPE

The advancement in technologies and the growing

adoption of electronic financial transactions have

significantly increased the risk of fraudulent activities

due to simplified verification processes. In this study,

we analyzed a dataset comprising 284,807 credit card

transactions from European users. For fraud

detection, the dataset was split into 80% training and

20% testing data to build and evaluate models.

Preprocessing steps included Z-score normalization

for standardization, one-hot encoding for categorical

variables, and handling missing values through

appropriate techniques.

To assess the performance of various machine

learning models, we utilized key evaluation metrics:

accuracy, precision, recall, F1 score, and the confusion

matrix. Among the models tested, the XGBoost

Classifier demonstrated superior performance. While

the accuracy of the XGBoost model reached an

impressive 99%, further analysis revealed that

precision and recall were critical in addressing the

misclassification rate, particularly for the minority

class (fraudulent transactions).

The confusion matrix highlighted the model's

ability to correctly classify the majority of genuine

transactions while maintaining a reasonable balance

in detecting fraudulent cases. However, the results

underscore the importance of selecting the most

appropriate evaluation criterion—such as recall or F1

score to ensure effective fraud detection, especially in

imbalanced datasets like this one.

One limitation of this study is that the dataset was

collected over only two trading days, which may not

fully capture long-term trends or variations in

fraudulent behavior. Future research could address

this by incorporating a more extensive and diverse

collection of fraudulent transactions and exploring

advanced deep-learning algorithms to enhance fraud

detection rates and improve resistance to emerging

fraud techniques.

REFERENCES

A. Liaw, M. Wiener, Classification and regression by

random Forest, R News 2(3) (2002) 18–22.

A. Aditi, A. Dubey, A. Mathur, P. Garg, Credit Card Fraud

Detection Using Advanced Machine Learning

Techniques. (2022), 56–60.

http://dx.doi.org/10.1109/ccict56684.2022.00022.

B. G. Tabachnick, L.S. Fidell, Using Multivariate Statistics,

Harper Collins, New York, 1996.

F. C. Yann-a, Streaming active learning strategies for real-

life credit card fraud detection: Assessment and

visualization, 2018.

J. A. Michael, S.L. Gordon, Data Mining Technique for

Marketing, Sales and Customer Support, John Wiley &

Sons INC, New York, 1997, p. 445.

K. Yak, D. Tudeal, Internet Banking Development as A

Means of Providing Efficient Financial Services in

South Sudan. 2 (2011) 139–148.

K. Randhawa, C.H.U.K. Loo, S. Member, Credit card fraud

detection using AdaBoost and majority voting, IEEE

Access 6 (2018) 14277– 14284,

http://dx.doi.org/10.1109/ACCESS.2018.2806420.

K. Ayorinde, Cornerstone: A Collection of Scholarly and

Creative Works for Minnesota State University,

Mankato a Methodology for Detecting Credit Card

Fraud- Kayode Ayorinde (Thesis Master’s), Data

Science Minnesota State University Mankato, MN,

2021.

L. Breiman, Random forests, Mach. Learn. 45 (1) (2001)5–

32.

L. Guanjun, L. Zhenchuan, Z. Lutao, W. Shuo, Random

Forest for credit card fraud, IEEE Access (2018).

N. K. Trivedi, S. Simaiya, U. K. Lilhore, and S. K. Sharma,

“An efficient credit card fraud detection model based

on machine learning methods,” Int. J. Adv. Sci.

Technol., 2020.

N. S. Alfaiz and S. M. Fati, “Enhanced Credit Card Fraud

Detection Model Using Machine Learning,” Electron.,

2022, doi: 10.3390/electronics11040662.

O. Citation, B. Systems, University of Huddersfield

Repository Credit card fraud and detection techniques:

a review, 2009.

S. B. E. Raj, A.A. Portia, A. Sg, Analysis on Credit Card

Fraud Detection Methods. (2011) 152–156.

S. Madan, S. Sofat, D. Bansal, Tools and Techniques for

Collection and Analysis of Internet-of-Things malware:

A systematic state-of-art review, J. King

SaudUniv.Comput.Inf.Sci.(2021)xxxx,http://dx.doi.or

g/10.1016/j.jksuci.2021.12.016.

T. Pencarelli, The digital revolution in the travel and

tourism industry, Inf. Technol. Tourism (2019)

0123456789, http://dx.doi.org/10.1007/s40558-019-

00160-3.

V. Bolón-Canedo, N. Sánchez-Maroño, A. Alonso-

Betanzos, J. M. Benítez, and F. Herrera, “A review of

microarray datasets and applied feature selection

methods,” Inf. Sci. (Ny)., 2014, doi:

10.1016/j.ins.2014.05.042.

AI-Based Fraud Detection System for Financial Transactions

427

V. Nath, ScienceDirect credit card fraud detection using

machine learning algorithms credit card fraud detection

using machine learning algorithms, Procedia

Comput.Sci.165(2020)631–641,

V. Rohilla, S. Chakraborty, and R. Kumar, “Deep learning-

based feature extraction and a bidirectional hybrid

optimized model for location-based advertising,”

Multimed. Tools Appl., 2022, doi: 10.1007/s11042-

022-12457-3.

ICRDICCT‘25 2025 - INTERNATIONAL CONFERENCE ON RESEARCH AND DEVELOPMENT IN INFORMATION,

COMMUNICATION, AND COMPUTING TECHNOLOGIES

428