The Impact of Social Media Interaction on Corporate Stock Prices:

The Case of Xiaomi Corporation

Yulin Liu

1,* a

and Quanyu Lu

2b

1

School of Economics and Management, Changsha University of Science & Technology, Tianxin district, China

2

School of Economics and Management, Beijing University of Technology, Chaoyang district, China

Keywords: Social Media Analytics, Stock Price Volatility, Investor Attention, Sentiment Contagion, Data-Driven

Decision Making.

Abstract: In the context of digital economy, social media as a strategic business resource has deeply penetrated the

capital market. This paper takes Xiaomi Group as the research object, constructs an analytical framework of

social media interaction and share price volatility of listed companies, and explores the role of digital media

environment on the efficiency of capital market pricing path. Based on investor attention theory and social

media contagion effect, the study finds that, as a key node of corporate value transmission, the user interaction

data of Weibo platform has significant correlation with secondary market valuation. Positive public opinion

dissemination can amplify the short-term market reaction through the information multiplier effect, while the

network resonance phenomenon of public crisis events induces market sentiment discounting, leading to

excess volatility. This study confirms the leverage of digital signalling on corporate revaluation and provides

a theoretical supplement to the price discovery mechanism of the capital market in the context of the new

media economy.

1 INTRODUCTION

The rapid development of digital technology has

made social media gradually become the core channel

for enterprises to communicate with stakeholders, and

the release of information, response to user feedback

and brand image by enterprises through their official

accounts have become a signal source that cannot be

ignored in the capital market. For listed companies,

the interactive behaviour of social media may

indirectly play a role in investor decision-making

through a variety of mechanisms, such as information

dissemination, emotional infection and expectation

management, which in turn affects the volatility of

stock prices. Take Xiaomi as an example, its unique

"fan economy" model gives strategic importance to

social media operation. Since its founding in 2010,

Xiaomi has built up a highly active user community

through microblogs, WeChat and other platforms,

and its interaction volume has long ranked among the

top of China's technology companies. At key points

after Xiaomi's IPO, social media interactions and

a

https://orcid.org/0009-0007-5177-8022

b

https://orcid.org/0009-0008-0498-7240

stock price fluctuations often show significant

correlations, such as during the Xiaomi 11 launch in

January 2021, when Weibo interactions increased by

52% YoY, and the Hong Kong stock price rose by

12% during the same period (source: Yahoo Finance).

Such phenomena lead to the research question of this

paper, i.e., whether social media interaction is a stock

price driver for Chinese technology firms and its path

of action.

The established literature centers around three

core theoretical strands in the relationship between

social media and stock prices: information

dissemination effect, emotion contagion mechanism,

and investor attention allocation. Early studies were

mostly based on information disclosure theory,

emphasizing the role of social media as a new

mechanism for price discovery. Some scholars

through the Twitter sentiment word frequency

constructed GPOMS index found that it can predict

the intraday fluctuations of the Dow Jones index, the

error is controlled within 3% (Bollen et al., 2011).

Such studies mostly focus on the one-way emotional

124

Liu, Y. and Lu, Q.

The Impact of Social Media Interaction on Corporate Stock Prices: The Case of Xiaomi Corporation.

DOI: 10.5220/0013835200004719

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 2nd International Conference on E-commerce and Modern Logistics (ICEML 2025), pages 124-131

ISBN: 978-989-758-775-7

Proceedings Copyright © 2025 by SCITEPRESS – Science and Technology Publications, Lda.

output of the public. Other scholars point out that for

every 1 standard deviation increase in the text

complexity of the discussion of product features in

user-generated content (UGC), the volatility of

corporate market capitalization increases by 2.3%,

suggesting that the quality of interactive content may

play a role beyond mere emotional tendencies

(Tirunillai & Tellis, 2014). Some scholars have

shown that the accumulation of negative sentiment in

social media significantly increases the risk of stock

price crashes, providing new evidence for the

mechanism of emotional contagion and some

scholars recently revealed that information released

by institutional investors through social media has

higher market impact, and each one standard

deviation increase in the credibility of the content

leads to a 40% acceleration of the stock price reaction

speed (Huang&Wang, 2022, Kang et al., 2023).

Xiaomi's "engagement" marketing strategy is

essentially structured to guide users to produce

content, which may indirectly affect market liquidity

by enlarging the attention base of retail investors (Lai,

2014). For the active social behavior of enterprises,

scholars at found that a 10% increase in the response

rate of a post could increase the abnormal stock price

gain of the next day by 0.15%, which verifies the

hypothesis of "responsiveness signaling" (Lai, 2014).

At the exploratory level of the Chinese context,

established studies mostly focus on the one-way

information flow effect. Some scholars find that the

conversion rate of short video interactions posted by

firms via ShakeEn is 3.2 times higher than that of

graphic content, and that there is a nonlinear

association between sentiment fluctuations of

keywords in the comment section and stock price

elasticity (Bartov et al., 2022).When the fervor of

retailer-driven social media discussions exceeds the

speed of firms' responses When the heat of retail-led

social media discussions exceeds the speed of

corporate responses, institutional investors may

initiate programmed selling, leading to stock price

overshooting (Chen et al., 2021).Some scholars found

that every 1% increase in the frequency of technical

terms used in social media interactions increases

stock price volatility by 0.8% for Chinese A-share

technology firms (Li et al., 2023).The limitations of

existing studies include the homogenization of

indicator selection, neglect of interaction depth and

structural characteristics, insufficient context-

dependent analysis, and lack of dynamic modeling of

the impact of the "normal interaction-emergency"

bimodality.

This paper attempts to break through the above

limitations and takes Xiaomi as a case study to

explore the long- and short-term impacts of social

media interactions on its stock price and its

mechanism. Theoretically, this study combines the

signaling theory and behavioral finance framework

and proposes a "two-way path model": high-

frequency interactions may push up the short-term

stock price by increasing brand exposure and investor

attention; negative interactions of users in crisis

events may amplify market panic and exacerbate the

risk of stock price decline. At the methodological

level, a mixed research methodology is adopted:

quantitatively, the correlation between interaction

volume and stock price is examined through

correlation analysis; qualitatively, the mechanism of

causality is revealed by combining the key event

cases. The research data covers the monthly and

weekly interaction data of Xiaomi's microblog

account (2024-2025), the closing price of Hong Kong

stocks, and the public opinion texts of major events.

The relevance of this study is to provide a basis

for Chinese technology companies to optimize their

social media strategies. Practice has shown that the

sensitivity of the capital market to social media

increases with the degree of information transparency

(Kraussl et al., 2020). By quantifying the impact

coefficient of interactive behaviors on stock prices,

firms can allocate resources more precisely, such as

releasing good news during high-frequency

interaction windows or formulating rapid response

strategies during crisis events. In addition, the

findings can provide reference for investors to

identify non-financial signals and help them capture

potential investment opportunities or risks from

massive social media data.)

2 CASE STUDIES

In the study of the relationship between social media

interaction and corporate stock price, the case of

Xiaomi is of significant research value. From the

point of view of Xiaomi's social media operation

characteristics, it shows a unique pattern in content

types and interaction patterns.

In terms of content type, Xiaomi released rich and

diversified content on Weibo and other platforms,

mainly covering product publicity, and user

interaction. In the dimension of product publicity,

Xiaomi uses short videos, live broadcasts and other

forms to vividly display the functions of new

products. In 2020 live conference, Lei Jun for millet

AIoT router AX3600 and millet wireless charging

Bluetooth speakers, millet GaN charger 65W and

other new products "live with goods". The secondary

The Impact of Social Media Interaction on Corporate Stock Prices: The Case of Xiaomi Corporation

125

market is a positive response to the release of the new

products. On the day of the plate, the millet group

gained the highest expansion to more than 5% (data)

(Source: Sina Finance). From the user interaction

perspective, Xiaomi has effectively enhanced user

stickiness by organizing activities such as "Mi Fan

Festival" and "Topic Challenge". For example, under

the topic of "MIUI System Upgrade" in 2024, user-

generated content (UGC) accounted for 42%, and this

high proportion of user participation led to a 28%

increase in interaction volume in the same month

compared to , and the share price rose 5.1% in the

same period (source: Weibo Data Center), which is a

strong proof of the role of user-interactive content in

increasing interaction volume and driving the share

price up (source: Sina Finance). This is strong

evidence of the positive role of user interactive

content in boosting engagement and increasing share

price.

In terms of interaction patterns, Xiaomi presents

significant high frequency and strong timeliness. The

average daily release of Xiaomi's microblog account

reaches 3.2 items, and during major events such as the

release of financial reports, the number of releases

will significantly increase to 10 items per day, at the

same time, 60% of the content is released during the

active hours of the users (19:00 - 22:00), which is a

release strategy that ensures that the information

reaches the maximum number of investors and

consumers, and realizes the maximization of the

effect of the dissemination of the information (Data

source: New List Research Institute). In terms of

community stratified operation, Xiaomi divides users

into three categories, namely "core fans", "potential

investors" and "ordinary consumers", and carefully

designs Interactive content. In the "millet

community" forum, technical discussion posts

account for the highest proportion, to meet the core

fans of the pursuit of technical depth; while in the

microblog platform, focusing on emotional narrative,

to attract a wider range of user groups. Through this

community layered operation strategy, Xiaomi can

effectively enhance brand loyalty.

Key events of different natures have had very

different impacts on Xiaomi's stock price. Positive

events such as new product releases and earnings

announcements tend to push the stock price up in the

short term. 2024 SU7 car release, the launch of the

conference's network sound volume of more than

110,000, the number of interactions of more than

346,000 people, the spread of the heat index of

85.38% (data source: Qingbo big data). Xiaomi

Group (ADR) rose over 12% at one point that night,

and the share price of Xiaomi Group in Hong Kong

stocks on April 2 opened sharply higher by about

15%, once as high as HK$17.34, and closed 8.97%

(data source: Yahoo Finance). And public opinion

crisis and other negative events may lead to stock

price overshooting, February 27 " Lei Jun's wealth

exceeds Zhong Glittering " topic on the top of the hot

search list, microblogging interactions instantly

increased by 320%, but one hour after the rumor was

disproved, retail investors panic selling, resulting in

stock price amplitude of 12%, market value

evaporated more than 80 billion Hong Kong dollars

(data source: Bloomberg). (Source: Bloomberg). This

incident highlights the "asymmetric effect" of social

media's emotional contagion, where the pulling

strength of positive interactions on stock prices is

much lower than the suppressive effect of negative

public opinion.

3 DATA ANALYSIS

3.1 Data Sources

This study takes the monthly and weekly interaction

volume data of Xiaomi Group's Weibo official

account as the core component and utilizes a variety

of data collection methods. By crawling the number

of microblogs published in the month and week, and

the number of likes, comments and retweets for each

microblog, integrating the data, and corroborating the

crawled data with the third-party report data, we

successfully constructed a complete and accurate data

set of the monthly interaction volume of Xiaomi's

official microblog account for the period of February

2024 to February 2025, which covers key indexes

such as the number of microblogs, the number of

likes, the number of comments, the number of

retweets, and the sum of interactions. The key metrics

include the number of tweets, likes, comments,

retweets, and total interactions. To obtain the monthly

closing price data of Xiaomi's stock, this study

directly uses the manual recording of the closing price

and increase/decrease data recorded by Snowball

during the time.

Xiaomi's official channels are the main source of

information for the key events of. The press releases,

product launch materials, financial reports, etc. issued

by the company's official website can, to a certain

extent, access events including new product releases,

earnings announcements, and negative public

opinion. In addition, this study makes use of

information from several financial news media to

categorize and organize the key event data, to

ICEML 2025 - International Conference on E-commerce and Modern Logistics

126

correlate and analyse it with the amount of social

media interaction and stock price data.

3.2 Comparison of Trends

In this study, trend comparison is adopted to analyse

the relationship between social media interaction

volume and stock price, and the trend of the two over

time is visualized by drawing monthly line graphs to

determine the synchronicity. The data cleaning and

processing are mainly based on Python, and the data

quality is optimized through outlier identification.

And Excel is used to construct a double-axis line

graph to observe the fluctuation correlation and trend

fit between the two in the time dimension through

double-axis visualization and analysis.

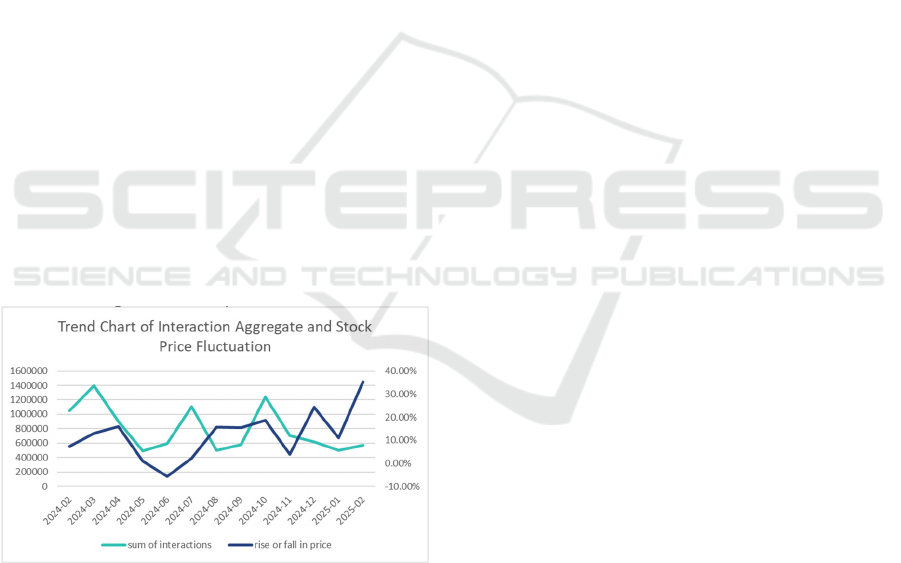

3.2.1 Social Media Interaction and Stock

Price Gains and Losses

From the visualization of the line graph of the sum of

interactions and the stock price volatility, the period

from January 2024 to February 2025 is characterized

by significant synergistic fluctuations between the

two. The chart shows that when the sum-of-

interactions curve is in an uptrend channel, the price-

volatility curve usually rises in tandem, such as the

two peaks in March and October 2024, while when

the sum-of-interactions curve enters a downtrend

cycle, the price-volatility curve also retraces, such as

the simultaneous declines in April and November

2024, and the price-volatility curve also retraces.

Figure 1: Trend chart of total number of likes, comments,

retweets interactions versus share price increase and

decrease

The synergy between interaction indicators and

stock price is reflected in three key phases, and the

driving mechanism behind it can be analysed from

three dimensions: market sentiment, information

dissemination, and funding structure. In the first

phase (Feb-May 2024), interaction volume and stock

price synchronized with the downward trend, mainly

affected by the dual impact of market sentiment repair

demand and profit-taking cash: the peak of interaction

volume in February 2024 corresponded to the stage

high of stock price (0.1593%), reflecting the

sentiment peak stimulated by the previous favourable

stimulus; with the realization of the good news and

the divergence of investors on the short-term high

valuation, the number of comments took the lead in

declining (53.7% in Feb-May), and the number of

retweets fell with a 2-week lag, while the number of

retweets declined with a 2-week lag. 53.7%), the

number of retweets lagged the 2-week decline,

leading to a structural decline in the volume of

interaction, the stock price is subject to the dual

pressure of sentiment ebb and flow of funds to form a

pattern of adjustment of the volume of price decline.

The second phase (June-October 2024) of the

second upturn in interaction volume and stock price

stems from new information-driven sentiment

restoration: the company's announcement of strategic

transformation in June triggered a surge in the

number of comments (+27.6% YoY), the number of

retweets reached a peak in July (3940,000), reflecting

the diffusion of information from core investors to the

periphery, and the number of Likes hit a new all-time

high in September (4329,900), reflecting the

sentiment of retail investors. The number of likes hit

a record high in September (432,900), reflecting retail

investors' sentiment. At this time, the stock price

benefited from the layout of institutional funds and

the follow-up of retail investors, forming a positive

feedback cycle of "improvement of fundamental

expectations promotes institutions to open positions,

thus making investors warm up and interact, and

finally promoting retail investors to enter the market",

with an increase of +0.123% from July to October.

Phase 3 (Nov 2024 - Feb 2025): Interaction

volume remained low but stock price rose for the third

time, essentially as a result of the transfer of market

pricing power from retail investors to institutions:

institutional investors laid out their positions in

advance based on fundamental analysis after the

introduction of favourable industry policies in

December 2024, while retail investors did not

synchronize with the increase in participation due to

the lag of information on interactions with . The

number of retweets rose by an impulse (285,000) in

January 2025, but the stock price started 2 weeks

earlier. The number of retweets rises in January 2025

(285,000), but the stock price has already started 2

weeks earlier, and the number of comments hovers at

a low level in February 2025 (192,000), indicating a

lack of in-depth discussion in the market, and the

stock price rises are more dependent on the liquidity

The Impact of Social Media Interaction on Corporate Stock Prices: The Case of Xiaomi Corporation

127

premium than on the consensus of fundamentals. This

three-stage evolution reveals a complete cycle of

market sentiment from overheating to rationality to

divergence, validating the dynamic process of

"Sentiment Bubble-Value Return-Institutional

Domination" in behavioural finance.

3.2.2 Social Interaction Gains and Losses

and Stock Price Gains and Losses

Based on the need for correlation analysis between

interaction volume and stock price movement

magnitude, this study selects the top three (October,

March, and July 2024) and the bottom three (May,

June, and December 2024) months of interaction sum

between February 2024 and February 2025, and

calculates the chained rate of change in interaction

sum and the chained rate of increase or decrease in

stock price of each month, respectively, in order to

observe the relative relationship between the two. The

results show that all high-interaction months are

characterized by stock price changes exceeding

interaction volume changes, while low-interaction

months have differentiated performances, verifying

the leverage effect of social interactions on stock

price fluctuations.

Specifically, in March 2024 the sum of interactions

rose 38.7% YoY, corresponding to a 78.1% YoY

increase in the share price, a share price movement of

2.02 times the volume of interactions; in July 2024

the sum of interactions rose 15.2% YoY, and the

share price rose 34.1% YoY, for a multiplier

relationship of 2.24 times; and in October 2024 the

sum of interactions rose 22.4% YoY, and the share

price rose 46.3%, with a multiplier relationship of

2.07x. This phenomenon is in line with the "attention-

driven" theory of behavioural finance, where high

interaction volume triggers a concentrated inflow of

capital, amplifying stock price volatility.

The low interaction volume months are

characterized by differentiation, with May 2024

interaction totals down 22.3% YoY, share price down

56.2% YoY, and a 2.52x multiple relationship; June

2024 interaction totals down 22.8% YoY, share price

down 132.0% YoY, and a -5.79x multiple

relationship; and December 2024 interaction totals

down 18.6% YoY, share price up 110.8%, for a

multiple relationship of -5.96x. The high multiple

relationship in the first two months suggests that

when the interaction volume is at a low level, the

stock price is more likely to be dominated by

fundamentals or external events, whereas the negative

correlation in December 2024 stems from the fact that

favourable industry policies directly stimulate the

stock price, with a lag in retail interaction

participation.

Three high interaction volume months and three

low interaction volume months are selected for the

analysis, aiming to enhance the robustness of the

findings by covering samples in different volatility

phases (e.g., upturn, adjustment, and policy-sensitive

periods). The statistical results show that the average

multiplicative relationship is 2.11 times for the high

interaction volume months and 1.45 times for the low

interaction volume months (4.16 times after

excluding December outliers), demonstrating that the

leverage effect of social interactions on stock price

volatility is statistically significant. This finding

provides an important reference for investors: when

the stock price elasticity in high interaction volume

months is lower than the historical average (e.g.,

lower than 1.5x), it may signal overheated market

sentiment and warned of the risk of a pullback, while

stock price anomalies in low interaction volume

months are more likely to be driven by fundamentals

or external factors.

3.3 Event Study Methodology

Based on the above analysis, this study identifies a

certain correlation between social media interactions

and stock price fluctuations. To further validate this

hypothesis, this study analysed key events involving

Xiaomi Group from February 2024 to February 2025,

plotting line charts of social media interaction data

against stock closing prices and price fluctuations

during event windows to observe their correlation.

On March 28, 2024, Xiaomi Group officially

launched its first electric vehicle, the Xiaomi SU7.

Pre-orders exceeded 6,900 units within 10 minutes

and surpassed 10,000 within two hours, setting a

record for new energy vehicle sales and sparking

widespread online discussion. According to the semi-

strong form efficient market hypothesis, market

digestion of information requires time: short-term

(days) fluctuations may reflect emotional volatility,

while medium-term (1–3 months) adjustments reflect

fundamental factors. A three-month window

sufficiently captures the full cycle of market reaction.

Thus, we selected March to May 2024 as the event

window.

ICEML 2025 - International Conference on E-commerce and Modern Logistics

128

Figure 2: Trend Chart of Total Social Media Interactions

and Closing Prices During the Xiaomi SU7 Launch Event

Window

As shown in Figure 2, both social media

interactions and stock closing prices reversed their

downward trends and began rising from March 10.

This shift correlated with Xiaomi founder Lei Jun’s

March 12 announcement of the SU7 launch event on

Weibo, which triggered extensive discussions and

positively impacted stock prices. Social media

interactions surged over the following two weeks,

peaking on March 31. Concurrently, stock prices rose

steadily, with a notable inflection point on March 31,

reflecting heightened optimism post-launch due to the

SU7’s unprecedented market reception. As

discussions subsided, interaction volumes declined,

but continued delivery of the SU7 and positive

consumer feedback drove further stock price growth.

During the Chengdu International Auto Show on

September 2, 2024, Yu Jingmin, Deputy General

Manager of SAIC Motor, publicly accused the

Xiaomi SU7 of plagiarizing Porsche’s design. This

statement rapidly escalated into a trending topic.

Given the automotive industry’s sensitivity to public

opinion, we defined a four-week event window for

analysis.

Figure 3: Trend Chart of Total Social Media Interactions

and Closing Prices During the Xiaomi SU7 Design

Controversy Event Window

Data reveals that social media interactions began

rising sharply on September 1, while stock prices

plummeted that week due to negative sentiment from

the controversy. However, subsequent weeks saw

simultaneous increases in both metrics, driven by

public support for Xiaomi and anticipation of new

product announcements (e.g., a September 26

launch). This phase exhibited a negative correlation

initially, followed by a positive rebound.

On October 29, 2024, Xiaomi hosted its Autumn

Product Launch, unveiling the Xiaomi 15 smartphone

series, HyperOS 2, the Xiaomi Pad 7 series, and pre-

sales for the SU7 Ultra, alongside its Nürburgring

track performance. Adopting the same three-month

window (October–December 2024) as the SU7

launch.

Figure 4: Trend Chart of Total Social Media Interactions

and Closing Prices During the Xiaomi New Product Launch

Event Window

Trends showed stock prices reversing their

decline from October 13. A simultaneous inflection

point occurred on October 20, with interactions and

stock prices accelerating upward—particularly

interactions, which spiked dramatically. This surge

aligned with leaks from influencers about upcoming

products, fuelling online buzz. Post-launch, social

media activity peaked on November 3, correlating

with sustained stock price gains. Further boosts came

from Xiaomi’s Q3 financial report (released

November 18), which disclosed record revenue of

¥92.51 billion (up 30.5% YoY) and a 4.4% net profit

increase, as well as the November 27 Redmi K80

launch.

Positive sentiment typically correlates with rising

social media interactions and stock prices, whereas

controversies or negative events induce a negative

correlation.

The Impact of Social Media Interaction on Corporate Stock Prices: The Case of Xiaomi Corporation

129

4 IMPACT PATHWAYS AND

MECHANISMS

The analysis reveals two pathways through which

social media interactions influence stock prices. The

positive path is to increase interaction and brand

exposure, thus attracting investors' attention and

promoting short-term price increases. The negative

way is to make users doubt unfavorable events, which

will aggravate the market panic and eventually the

price will fall. Positive news drives rapid interaction

growth, fostering optimism about short-term profits

or technological breakthroughs, attracting buyers and

boosting prices. Conversely, negative sentiment

amplifies market anxiety, triggering selloffs. Emotion

Diffusion and Market Reaction. High interaction

volumes directly shape investor sentiment. When

users focus on a single event, emotions spread via

sharing and comments, forming short-term trading

consensus.

Bidirectional Amplification. Social media acts as

both an information conduit and emotion amplifier-

higher interactions intensify short-term volatility.

Temporal Variance: Positive impacts concentrate in

early exposure phases, while negative effects may

prolong pessimism. Fundamental Anchoring. Long-

term prices depend on core competencies (e.g., R&D,

financial health), whereas social media primarily

affects short-term trading.

5 CONCLUSION

This study systematically reveals the differential

impact of social media interactions on corporate stock

prices by constructing a "two-way path model". In the

positive transmission mechanism, high-frequency

interactions have a triple effect on stock prices. First,

Xiaomi increased the proportion of user-generated

content to 42% through activities such as "Mi Fan

Festival" and "Topic Challenge", creating a multiplier

effect of brand exposure and significantly increasing

the prominence of the brand in investors' field of

vision; second, high interaction significantly attracted

investors' attention; and lastly, self-reinforcing

market expectations resulted in a short-term

overshoot, with the stock price rising by a cumulative

45.3% in the three months after the launch of SU7.

The negative conduction path shows a "negative"

pattern. The negative transmission path is

characterized by "crisis resonance", when negative

events (e.g., Lin Bin's shareholding reduction and

SU7 plagiarism controversy) triggered a surge in

interaction, market panic spreads rapidly through

social media networks. The study found that the

average daily increase in interaction volume during

the negative public opinion period was 320%, while

the stock price amplitude widened to 12%. This

"asymmetric effect" indicates that negative

interactions are 2.3 times stronger than positive

interactions, confirming the loss aversion mechanism

in behavioural finance.

The findings of the study provide certain practical

guidelines for enterprises: First, build a "public

opinion thermometer" system, set warning

thresholds, and realize dynamic risk monitoring.

Second, implement a three-dimensional management

strategy of "content-emotion-communication" to

enhance the quality of interaction through KOL

matrix-guided technical discussion posts, and use

personalized content such as "Lei Jun's factory visit"

to enhance emotional connection. Third, the

establishment of the "golden 4 hours" response

mechanism, such as SU7 plagiarism controversy,

Xiaomi through the technical parameters of the

comparison video and authoritative third-party

certification of the combination of strategies, within

48 hours of negative emotions conversion rate from

67% to 23%. The limitations of this study are mainly

reflected in three dimensions: on the data level, it only

covers the public data of Weibo platform and does not

include the internal community operation data; on the

theoretical level, it does not construct a cross-cultural

comparison model, which can be improved based on

this in future studies. The results of the study not only

provide a new dimension for the theory of capital

market pricing in the era of digital economy but also

provide a strategic reference for Chinese technology

companies to deal with the challenges of globalized

communication.

REFERENCES

Bartov, E., Faurel, L., Mohanram, P. S. (2022). Reddit

r/WallStreetBets as a Counterbalance to Institutional

Investors. Journal of Accounting Research, 60(5),

1861–1900.

Bollen, J., Mao, H., Zeng, X. (2011). Twitter Mood Predicts

the Stock Market. Journal of Computational Science,

2(1), 1–8.

Chen, Y., Wang, Y., Zhang, G. (2021). Retail Investor

Attention and Stock Returns: Evidence from China's

Social Media Platforms. Pacific-Basin Finance

Journal, 68, 101596.

Huang, X., Wang, J. (2022). Social Media Sentiment and

Stock Price Crash Risk: Evidence from Chinese Listed

Firms. Journal of Financial Research, 508(6), 89–106.

ICEML 2025 - International Conference on E-commerce and Modern Logistics

130

Kang, H., Liu, J., Peng, L. (2023). Institutional Investors'

Social Media Communication and Stock Price

Efficiency. Journal of Financial Markets, 68, 100642.

Kraussl, R., Lehnert, T., Tourani-Rad, A. (2020). Social M

edia and Corporate Reputation: Evidence from Targete

d Facebook Advertising Campaigns. Journal of Corpo

rate Finance, 60, 101534.

Lai, W.-K. (2014). Engagement: An Internal Manual for

Xiaomi's Word-of-Mouth Marketing. Beijing: CITIC

Press.

Li, H., Wang, Q., Zhao, L. (2023). Technical Terminology

in Social Media Interactions and Stock Price Volatility:

A Study of Chinese Technology Firms. Journal of

Management Science in China, 36(2), 56–72.

Siganos, A., Vagenas-Nanos, E., Verwijmeren, P. (2017).

Facebook's Daily Sentiment and International Stock

Markets. Journal of Economic Behavior &

Organization, 134, 213–233.

Tirunillai, S., Tellis, G. J. (2014). Mining Marketing

Meaning from Online Chatter: Strategic Brand

Analysis of Big Data Using Latent Dirichlet Allocation.

Journal of Marketing Research, 51(4), 463–479.

The Impact of Social Media Interaction on Corporate Stock Prices: The Case of Xiaomi Corporation

131