The Impact of Psychological Factors on Luxury Stock Prices:

Empirical Analysis of Paris Market

Yuanyuan Gan

1,+ a

, Xiaoyue Liang

2b

and Enshuo Yan

3c

1

Wuhan Britain-China School, No. 10 Gutian Ce Road, Wuhan, China

2

Department of Finance, Beijing University of Financial Technology, No.1 Songzhuang Nan Road, Beijing, China

3

Department of Finance Engineering, Southern University of Science and Technology,1088 Xueyuan

Avenue, Shenzhen, Guangdong, China

*

Keywords: Luxury Stock Market, Behavioural Economics, Psychological Factors, Market Volatility, Investor Sentiment.

Abstract: With the luxury market's rapid growth and increasing integration into global financial systems, understanding

its stock dynamics has become critical for investors and policymakers. This study focuses on the luxury stock

market, examining the impact of psychological factors on luxury stock prices from the perspective of

behavioural economics. Based on empirical analysis and qualitative event studies, we analyse data from six

luxury companies (e.g., LVMH, Hermès, Dior) listed on the Paris open market from January 2020 to

December 2024. The research investigates correlations among market volatility (VIX Index), investor

sentiment, and economic policy uncertainty. Key findings reveal a significant negative correlation between

market volatility and stock prices of certain brands, a positive influence of investor sentiment on most stock

valuations, and heightened irrational price fluctuations due to economic policy uncertainty. These results

underscore the importance of psychological factors in luxury stock pricing, provides theoretical support for

investment strategies, and advocate for future research integrating social media sentiment data and multi-

factor models.

1 INTRODUCTION

Contemporarily, with the considerable development

of people's living standard, the market of luxury is

more and more mature and gradually taking up larger

share of consumption. Considering that the luxury

industry is having a greater status which leads to the

development of the luxury stock market, the

researches on the factors influencing the changes of

luxury stocks is essential. In the process, researchers

have studied the luxury stocks and luxury stock

pricing based on the researches about luxury industry

before, using methods of market research and

quantitative research. They have got several research

achievements in related fields that can be used by

follow-up further research.

Then, it comes to the process of background

investigation. Research on the pricing of luxury

goods stocks has yielded several relevant findings

a

https://orcid.org/0009-0001-5956-536X

b

https://orcid.org/0009-0005-6888-5620

c

https://orcid.org/0009-0003-9661-8322

from previous researchers. According to the previous

articles, luxury goods can be distinguished from non-

luxury goods based on the unique combination of

their functionalism, experientialism and symbolic

interactionism across these three important

dimensions. This theory provides a fundamental

theoretical framework and empirical support for

research in the field of luxury marketing. Recent

years, researches related to relevant topics have also

made some progress. Talukdar found that the high

volume of tweets from luxury brands can sometimes

dilute their excellent image previously established,

which can have a negative impact on stock prices

(Talukdar, 2020). In contrast, carefully selected and

meaningful digital communications can increase

consumer engagement and make brand equity better.

In 2012, scholars analysed psychological antecedents

of luxury consumption, which demonstrates the

motivation of consuming luxury and provides more

38

Gan, Y., Liang, X. and Yan, E.

The Impact of Psychological Factors on Luxury Stock Prices: Empirical Analysis of Paris Market.

DOI: 10.5220/0013832300004719

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 2nd International Conference on E-commerce and Modern Logistics (ICEML 2025), pages 38-43

ISBN: 978-989-758-775-7

Proceedings Copyright © 2025 by SCITEPRESS – Science and Technology Publications, Lda.

information about psychology for relevant topics

(Kastanakis & Balabanis, 2012). Other findings from

reveal two aspects of psychological factors

influencing luxury stock (Wen, 2024). External

shocks, including events such as the COVID-19, the

Russia-Ukraine war and the China-United States

trade war, have introduced significant uncertainties

into the luxury market. Similarly, corporate internal

decisions also reflect the psychological foundation of

investor behaviour. Other articles that may not be so

relevant to our topic are also have useful information

to our research. Han indicated that the need for brand

salience depends on the consumption strategies of

different consumer groups (Han et al., 2010).

Olorenshaw put forward a theory claiming that the

conspicuous consumption reveals the fact that the

demand curve for luxury goods is likely to grow as

prices rise (Olorenshaw, 2011). Kessous and Valette-

Florence pointed out that self-success and symbolic

value have great effect on luxury markets (Kessous &

Valette-Florence, 2019). Chang et al., used the

example of energy to analyse the herd effect of the

stock market (Chang et al., 2020). Moreover,

Dhaliwal et al. introduced an overview of luxury

consumption behaviour (Dhaliwal et al., 2020).

However, the researchers are not enough to cover

all the guiding theories about luxury pricing. The

factors that have impact on luxury pricing are much

more complex in many aspects (Loranger & Roeraas,

2022; Savelli, 2012; Lewis et al., 2025). There are

still some research gaps on the psychological factors

affecting luxury pricing that should be ascertained to

provide more investment information on luxury

stocks. In this article, we consider the previous

researches and create our own methods to conduct our

study. Given that researches on the luxury pricing

have research gap, our study analysed the influence

of psychological factors on the luxury stock market

from the perspective of behavioural economics as

supplementary. This paper examines the data from

the Paris open market, which contains daily closing

prices and returns for several luxury brands, including

EPA: MC, EPA: RMS, EPA: CDI, EPA: KER, EPA:

SMCP, and EPA: DPT, over a period from January

2020 to December 2024, a period marked by

significant market fluctuations due to the COVID-19

pandemic. The analysis will focus on identifying

patterns and potential correlations between market

returns and psychological factors such as market

volatility, investor sentiment, and economic

uncertainty.

2 METHODOLOGIES

This research collected the closing prices of six major

luxury brands in the Paris public market from 2020 to

2024. These six companies are Moët Hennessy Louis

Vuitton Group, Hermès International SCA, Christian

Dior SE, Kering Group, SMCP Group, and S.T.

Dupont, ranked in descending order of market

capitalization. The research methods include

descriptive statistics, correlation analysis, CAPM fit

test, and multiple linear regression modelling. These

methods are chosen to provide a comprehensive

understanding of the relationships between the

variables.

We begin by calculating basic descriptive

statistics (mean, median, standard deviation) for the

daily returns of each luxury brand. This provides an

initial overview of the data and helps identify any

outliers or anomalies. Subsequently, we compute the

correlation coefficients between the daily returns of

each luxury brand and various psychological factors.

These factors include market volatility (measured by

the Volatility Index), investor sentiment (proxied by

the Google Trends and France Sentiment Index), and

economic uncertainty (proxied by the Europe Policy

Uncertainty Data – France News Index). Correlation

analysis helps identify the strength and direction of

the relationships between these variables. The linear

relationship between the returns of luxury companies

and the Dow Jones France Index has been tested first

in the study. A high positive correlation suggests that

the company's returns move in tandem with the

market, indicating a strong market influence. It is also

possible to examine to what extent the CAPM model

conforms to the changes in stock prices:

E(R

i

) = R

f

+ β

i

(E(R

m

) - R

f

) (1)

where E(R

i

) is the expected rate of return of asset i;

R

f

is the risk-free rate of return, usually represented

by the yield of government bonds; β

i

is the systematic

risk coefficient of asset i, indicating the sensitivity of

the rate of return of the asset to changes in the market

rate of return; E(R

m

) is the expected rate of return of

the market portfolio, that is, the average rate of return

of Dow Jones France Index; (E(R

m

) - R

f

) is the market

risk premium, indicating the portion by which the

expected rate of return of the market portfolio

exceeds the risk-free rate of return.

To further explore the impact of psychological

factors on share prices, we construct multiple

regression models. The dependent variable is the

monthly return of each luxury brand, while the

independent variables include market volatility,

investor sentiment, and economic uncertainty. This

allows us to quantify the impact of each

The Impact of Psychological Factors on Luxury Stock Prices: Empirical Analysis of Paris Market

39

psychological factor on share prices, controlling for

other factors. The regression model is specified as

follows:

Stock Price

i,t

= α + β

1

Market Volatility

t

+ β

2

Investor

Sentiment

t

+ β

3

Macroeconomic Uncertainty

t

+ϵ

it

(2)

where Stock Price it is the stock price of the luxury

company i at time t; Market Volatility t is measured

by the Volatility Index at time t; Investor Sentiment t

is measured by France Sentiment Index at time t;

Macroeconomic Uncertainty t is measured by the

Europe Policy Uncertainty Data – France News Index

at time t; α is the intercept; β

1

, β

2

, β

3

are the

coefficients to be estimated; ϵ

it

is the error term.

3 RESULTS AND DISCUSSION

3.1 Descriptive Statistics

The mean daily return for EPA: MC is 0.03%, with a

standard deviation of 0.019. This indicates relatively

stable returns with occasional fluctuations. EPA:

RMS shows a higher mean return of 0.1% and a

standard deviation of 0.018, suggesting slightly less

volatility. EPA: CDI, EPA: KER, EPA: SMCP and

EPA: DPT exhibit similar patterns, with mean returns

ranging from 0.02% to -0.08%, and standard

deviations between 0.02 and 0.05, indicating a

negative relationship: higher volatility is associated

with lower returns.

Table 1 shows that after calculating the average

return, due to the external shocks such as the COVID-

19 pandemic and geopolitical conflicts during this

period, the economy gradually recovered from 2020

to 2024, and the investment in the stocks of luxury

companies do not all brought positive returns.

However, there is no positive correlation between

volatility and return rate, but a positive correlation

with market capitalization.

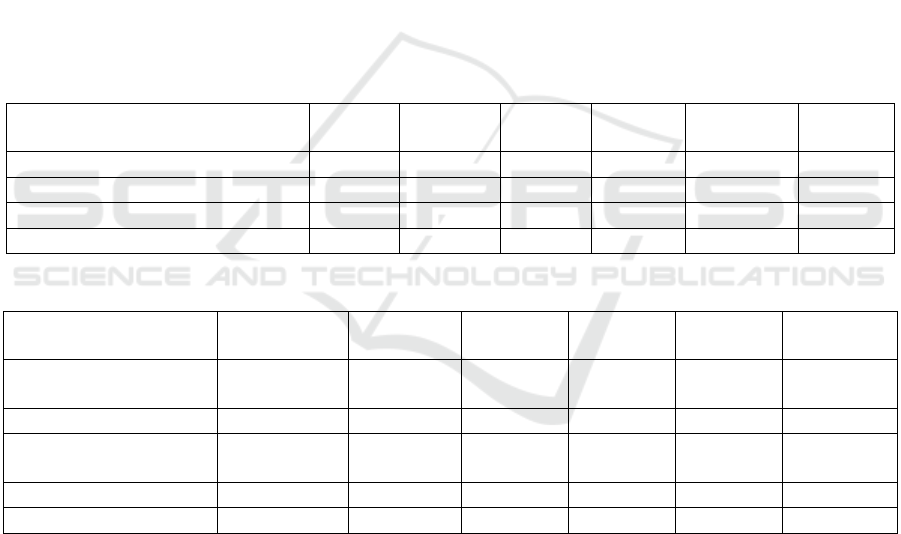

Table 1: Descriptive Statistics.

EPA: MC EPA: RMS EPA: CDI

EPA:

KER EPA: SMCP EPA: DPT

Expected return (dail

y

) 0.03% 0.01% 0.02% -0.07% -0.08% -0.02%

Expected return (annualized) 7.93% 24.22% 5.01% -18.05% -19.97% -4.46%

Expected volatilit

y

(dail

y

) 1.88% 1.78% 2.00% 2.12% 3.64% 5.15%

Expected volatilit

y

(annualized) 29.74% 28.12% 31.62% 33.49% 57.53% 81.39%

Table 2: Correlation Analysis.

Correlation Coefficien

t

EPA:MC EPA: RMS EPA: CDI

EPA:

KER

EPA:

SMCP EPA: DPT

France Consumer

confidence index -0.1367 -0.1599 -0.1037 0.4423 0.0303 -0.2714

France Sentiment index 0.3340 0.1057 0.3736 0.4256 0.3375 0.3299

France Economy

Uncertain Polic

y

Index -0.1244 0.1227 -0.1498 -0.391 -0.2284 -0.0057

VIX Volatilit

y

Index -0.6138 -0.6138 -0.6116 0.0867 0.0069 0.0439

Goo

g

le Trends 0.3680 0.7829 0.1865 -0.2826 0.2625 -0.1077

3.2 Correlation Analysis

Table 2 calculates the correlation coefficients

between stock prices and five indicators. It is found

that the VIX index is strongly correlated with the

stock prices of three brands - EPA: MC, EPA: RMS

and EPA: CDI. This indicates that higher uncertainty

is associated with higher returns, likely due to risk-

seeking behaviour during uncertain times. Google

Trends is only strongly correlated with the stock price

of RMS (r = 0.78), and as the only company among

the six with an annualized investment return

exceeding 20%, it indicates that digital

communication may have a significant impact on

investor decisions, and further research should be

conducted in combination with social media data

analysis tools.

ICEML 2025 - International Conference on E-commerce and Modern Logistics

40

3.3 Regression Modelling

Table 3 tests the fit of CAPM in actual financial data,

using the Dow Jones France Index as the market

expected return for regression. It shows that CAPM

can be used to predict the value of company stocks to

a certain extent, especially with a higher fit with

large-cap companies, with an R² of about 0.5,

reflecting market efficiency. However, the fit with

small-cap companies is poor. The following

regression model includes independent variables of

market volatility (measured by independent variable

3 VIX Volatility Index), investor sentiment

(measured by independent variable 2: France

Sentiment index) and economic uncertainty

(measured by independent variable 1: Economy

Uncertain Policy Index) TINV (0.05, 56) =

2.003240719. Table 4 selects three variables for

multiple linear regression, and the results show that

the French Investor Sentiment Index and the French

Economic Policy Uncertainty Index have significant

t-values in most companies, indicating that these

variables statistically have an impact on the stock

prices of companies.

The quantitative analysis reveals the following

findings. The VIX index is significantly negatively

correlated with the stock prices of Louis Vuitton,

Hermès, and Dior (correlation coefficient of -0.61),

which may reflect "risk aversion", that is, reducing

investment in stocks when market uncertainty

increases. The French Investor Sentiment Index is

weakly positively correlated with the stock prices of

all companies, and in multiple linear regression,

except for RMS, the t-values of its impact on stock

prices are significant, verifying the hypothesis of

"sentiment-driven valuation". The CAPM model has

obvious limitations in simulating the stock prices of

relatively small-cap companies, such as SMCP (0.243)

and DPT brands, with low R

2

values (0.004),

indicating that their stock prices are dominated by

non-market factors (such as psychological factors),

highlighting the necessity of a "multi-factor model".

The analysis reveals that psychological factors,

such as market volatility, investor sentiment, and

economic uncertainty, can influence the share prices

of luxury companies to some extent. Specifically,

higher market volatility and positive investor

sentiment are associated with higher prices, while

economic uncertainty are associated with lower

prices. These findings suggest that luxury companies

may benefit from strategies that capitalize on periods

of high uncertainty and positive sentiment, while

managing risks during gloomy economic conditions.

Table 3: CAPM Model.

EPA: MC EPA: RMS EPA: CDI EPA: KER EPA: SMCP EPA: DPT

Dail

y

Expected return 0.0003 0.0010 0.0002 -0.0007 -0.0008 -0.0002

Beta 1.1972 0.9655 1.2872 1.2258 1.4156 0.2481

R^2 0.6496 0.4722 0.6640 0.5371 0.2426 0.0038

Table 4: Multivariate Regression.

EPA: MC EPA:

RMS

EPA:

CDI

EPA:

KER

EPA:

SMCP

EPA: DPT

R

2

0.5483 0.5414 0.5570 0.3526 0.1736 0.1462

t for VIX Volatility

Index

-0.5540 1.9907 -0.8166 -3.4027 -1.6965 0.1083

t for France Sentiment

Index

2.5572 0.1936 3.0273 3.8724 2.7502 2.8687

t for Economy

Uncertainty Policy

Index

-7.2857 -7.9100 -7.1489 2.0224 1.1871 1.5501

3.4 Analysis and Comparison

For Moët Hennessy Louis Vuitton Group, in 2024,

there was a decline in sales, affected by changes in

the macroeconomy and consumer habits. Investors

were concerned about its future development, and the

stock price fluctuated to a certain extent. Experts

believe that the slowdown in industry growth and

market competition are very important factors.

Similar events are that other luxury giants also face

The Impact of Psychological Factors on Luxury Stock Prices: Empirical Analysis of Paris Market

41

performance stress during economic downturns.

Literature points out that the luxury goods industry is

vulnerable to the impact of changes in the

macroeconomy and consumption trends. Investors

are affected by the herd effect. After seeing the news

of the slowdown in industry growth and the

company's performance decline, they blindly

followed the trend and sold stocks, leading to an

excessive decline in the stock price, ignoring the

long-term values such as LVMH's powerful brand

matrix and market competitiveness.

Regarding to Hermès International SCA. from

2019 to 2023, growth was driven by price increases,

and in 2025, the prices of its products were raised

globally. This is a tactic for the brand to consolidate

its high-end positioning. Investors' reactions were

relatively ignored, and the stock price was relatively

stable. Experts believe that this reflects the brand's

strong pricing power and market position. Similar

brands like Chanel also have price increase

behaviours. Relevant literature shows that price

increases of luxury brands are closely related to brand

value and market demand. Investors have an

anchoring effect. They rely too much on Hermès' past

brand performance and price strategies, have

insufficient understanding of the brand's value growth

potential after the price increase, and did not adjust

their expectations of the stock price in a timely

manner, so that the stock price failed to fully reflect

the possible value increase brought about by the price

increase.

As for Christian Dior SE, in January 2025, Kim

Jones, the men's artistic director of Dior, announced

his departure. This is an important personnel change

for the brand, which may influence the brand's

creativity and development direction. Since it is a

brand under LVMH, it affects investors' expectations

of LVMH to a certain extent. Experts believe that new

creativity is vital for the brand's future development.

Other brands also have situations where the departure

of a creative director affects performance. Relevant

literature emphasizes the value of creative talents to

fashion brands. Investors may have an overreaction

mentality. They are overly worried about the

departure of Kim Jones, magnify the negative impact

of this event on the brand's future development, and

then affect the investment decision-making regarding

LVMH, causing the stock price to fluctuate

irrationally.

For Kering Group, in 2024, the revenue of Kering

Group reduced by 12% year-on-year. As a core brand,

Gucci's performance in 2024 declined by 23%

throughout the year. This reflects the challenges the

brand faces in terms of market competition and

changes in consumer preferences. Investor

confidence was damaged, leading to a stock price

decline of more than 40%. Experts believe it is related

to Gucci's creative transformation not meeting

expectations, intensified market competition, and the

macroeconomic environment. Similar events include

other brands experiencing performance declines due

to creative and market strategy issues. Relevant

literature discussions emphasize the importance of

brand innovation and adapting to market changes for

luxury goods enterprises. Investors have a loss

aversion mentality. Seeing Gucci's continuous

performance decline, they worried that the group's

future performance would deteriorate further and sold

stocks one after another, resulting in an excessive

decline in the stock price. They did not fully consider

the possible positive changes brought about by brand

adjustment and transformation.

As for SMCP Group, in 2024, stores were closed

in the Chinese market, and performance declined.

This is a strategic adjustment by the brand to address

market issues. It may lead to a decrease in investors'

confidence in its stock price, and the stock price is

affected. Experts believe it is related to the previous

over-expansion in the Chinese market and changes in

the market environment. Other international brands

also have situations where they adjust their store

strategies in the Chinese market. Literature shows

that brand internationalization needs to adapt to

different market cultures and demands. Investors

have an overly pessimistic sentiment. Just because of

the store closures and performance decline in the

Chinese market, they are overly worried about the

company's future development prospects, ignoring

the brand's potential in other markets and the possible

improvements after the strategic adjustment, resulting

in an irrational decline in the stock price.

For S.T. Dupont, in 2025, the Jet Agile series of

casual shoes was launched, and there was a problem

of counterfeit lighters in 2023. The launch of new

products is a normal business expansion, and the

problem of counterfeits affects the brand image.

Investors did not show obvious reactions, and the

stock price did not fluctuate significantly. Similarly,

other brands also have troubles with counterfeits and

launches of new products. Literature emphasizes the

significance of brand protection and innovation for

enterprises. If investors focus too much on the

problem of counterfeits and turn a blind eye to

positive factors such as the launch of new products,

they will make inaccurate judgments about the

company's value due to cognitive biases, which may

cause the stock price to fluctuate irrationally and fail

ICEML 2025 - International Conference on E-commerce and Modern Logistics

42

to truly reflect the company's actual value and

development potential.

4 CONCLUSIONS

To sum up, this study validates the significant

influence of psychological factors on luxury stock

prices: market volatility suppresses valuations

through risk-averse behaviour, while investor

sentiment drives positive price movements.

Economic policy uncertainty exacerbates irrational

fluctuations, particularly in small- and mid-cap

companies. The research highlights the limited

explanatory power of the traditional Capital Asset

Pricing Model (CAPM) for small-cap brands,

emphasizing the need for multi-factor models (e.g.,

incorporating social media sentiment or ESG metrics)

to enhance predictive accuracy. Future research

should differentiate behavioural patterns between

retail and institutional investors and integrate real-

time social data (e.g., Twitter, Weibo) for deeper

insights. These findings provide a strategic

framework for the luxury industry to balance market

rationality and behavioural biases, offering practical

implications for investment decisions and corporate

governance.

AUTHOR CONTRIBUTION

All the authors contributed equally and their names

were listed in alphabetical order.

REFERENCES

Chang, C. L., Mcaleer, M., Wang, Y. A., 2020. Herding

behaviour in energy stock markets during the global

financial crisis, sars, and ongoing covid-19. Renewable

and Sustainable Energy Reviews, 134.

Dhaliwal, A., Paul, J., & Singh, P., 2020. The consumer

behavior of luxury goods: a review and research

agenda. Journal of Strategic Marketing, 3.

Han, Y. J., Nunes, J. C., Drèze, Xavier., 2010. Signalling

status with luxury goods: the role of brand prominence.

Journal of Marketing, 74(4), 15-30.

Kastanakis, M. N., Balabanis, G., 2012. Between the mass

and the class: Antecedents of the “bandwagon” luxury

consumption behavior. Journal of Business Research,

65(10), 1399–1407.

Lewis, J., Kim, J, H., Ozturk, A., 2024. Luxury

Conglomerate Strategy: A Comparative Case Analysis

of LVMH and Kering. Luxury, 1-21.

Loranger, D., Roeraas, E., 2022 Transforming luxury:

Global luxury brand executives’ perceptions during

COVID. Journal of Global Fashion Marketing, 14(1),

48-62.

Lou, X., Chi, T., Janke, J., Desch, G., 2022. How Do

Perceived Value and Risk Affect Purchase Intention

toward Second-Hand Luxury Goods? An Empirical

Study of U.S. Consumers. Sustainability, 14(18), 11730

Olorenshaw, R., 2011. Luxury and the recent economic

crisis. Vie & sciences de lentreprise, 188(2), 72.

Savelli, E., 2012. Role of Brand Management of the Luxury

Fashion Brand in the Global Economic Crisis: A Case

Study of Aeffe Group. Journal of Global Fashion

Marketing, 2(3), 170-179.

Talukdar, N., 2020. Luxury Connoisseurs and Twitter: An

Empirical Study of Relationship between Volume of

tweets from Luxury Brands and their Stock Price

Returns in the US. Marché et organisations, 37(1), 73–

97.

Wen, H., 2024. Analysis of Stock Price Fluctuation Factors

in Luxury Goods Industry Based on LVMH’s Stock

Price. Highlights in Business, Economics and

Management, 28, 234–239.

The Impact of Psychological Factors on Luxury Stock Prices: Empirical Analysis of Paris Market

43