Refining Medical Insurance Cost Predictions with Advanced Machine

Learning Models

Sheying Shen

a

School of Business, Nanjing University, Nanjing, Jiangsu, China

Keywords: Medical Cost, Insurance Prediction, Algorithms, Machine Learning.

Abstract: This paper employs diverse machine learning algorithms to enhance the accuracy of medical insurance cost

predictions. With the increasing complexity of healthcare costs and the need for fair and sustainable pricing

strategies, improving predictive accuracy is essential for both insurers and policyholders. Traditional methods

often fail to capture the intricate relationships between various factors and medical costs, leading to

suboptimal pricing. To address this, this paper leverages advanced machine learning techniques, including

ensemble methods like XGBoost and Random Forest, to analyse real-world data. These methods not only

improve prediction accuracy but also provide valuable insights into the key drivers of medical costs, such as

lifestyle behaviours and health indicators. Results show ensemble methods like XGBoost and so on excel in

predictive accuracy and generalization as well as offer insights into feature impacts, highlighting the

substantial influence of behavioural and health indicators on pricing. The research concludes that these

advanced techniques can significantly improve prediction precision, aiding insurers in refining their pricing

strategies. It also underscores the role of model interpretability in financial risk management.

1 INTRODUCTION

Predicting medical insurance costs is very important

for creating fair pricing strategies. In the past,

insurance companies mostly used simple linear

models or basic rules to estimate costs. These

methods were easy to use but often missed important

patterns in the data. As a result, insurers sometimes

had trouble finding the right balance between keeping

costs low for customers and making sure they could

cover their expenses. This could lead to pricing that

wasn't as accurate or effective as it could be.

Machine learning has changed this situation.

Unlike traditional methods, machine learning can

handle a lot of different variables and find

connections that were hard to see before. This helps

insurers understand what drives medical costs better,

so they can set prices more accurately and manage

risks more effectively. This not only helps insurance

companies stay financially stable but also makes

healthcare more accessible for everyone.

Recent studies have explored various machine

learning algorithms to make relevant predictions. For

instance, Orji and Ukwandu (2024) implemented

a

https://orcid.org/0009-0004-2936-8535

ensemble models like Extreme Gradient Boosting

(XGBoost), Gradient Boosting Machine (GBM), and

Random Forest (RF) to forecast medical insurance

expenses. Their findings indicated that XGBoost

achieved superior performance, while RF balanced

accuracy and computational efficiency. Similarly,

Cenita et al. (2023) evaluated Linear Regression,

Gradient Boosting, and Support Vector Machine

(SVM) models. Their results demonstrated that

Gradient Boosting outperformed the other models,

achieving an R² of 0.892 and the lowest Root Mean

Square Error (RMSE) of 1336.594. Billa and Nagpal

(2024) conducted a comparative analysis of different

machine learning algorithms for medical insurance

price prediction. Their study highlighted the

effectiveness of ensemble methods over traditional

regression models, suggesting that ensemble

approaches provide better predictive performance.

Effective feature selection is crucial for enhancing

the performance of machine learning models in

healthcare cost prediction. Panay and Baloian (2020)

developed a method using Weighted k-Nearest

Neighbours (k-NN) and Evidential Regression to

select relevant features for predicting healthcare

Shen, S.

Refining Medical Insurance Cost Predictions with Advanced Machine Learning Models.

DOI: 10.5220/0013702200004670

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 2nd International Conference on Data Science and Engineering (ICDSE 2025), pages 573-580

ISBN: 978-989-758-765-8

Proceedings Copyright © 2025 by SCITEPRESS – Science and Technology Publications, Lda.

573

costs. Their transparent model performed comparably

to Artificial Neural Networks and Gradient Boosting,

achieving an R² of 0.44. Additionally, Singh et al.

(2022) reviewed various feature selection methods

and their impact on machine learning algorithms in

healthcare applications. They emphasized the

importance of selecting appropriate features to

improve model accuracy and generalization.

While existing studies have applied various

machine learning models and feature selection

methods to make prediction, there is a lack of

research focusing on the interpretability of these

models. Understanding the influence of individual

features on predictions is essential for stakeholders to

make informed decisions.

This paper explores how machine learning can

help predict costs more accurately. It looks at the

problems with older methods and shows how

machine learning can be a better solution. By

analyzing real data and using advanced algorithms,

this paper aims to provide useful insights for insurers

to develop better pricing strategies in the future.

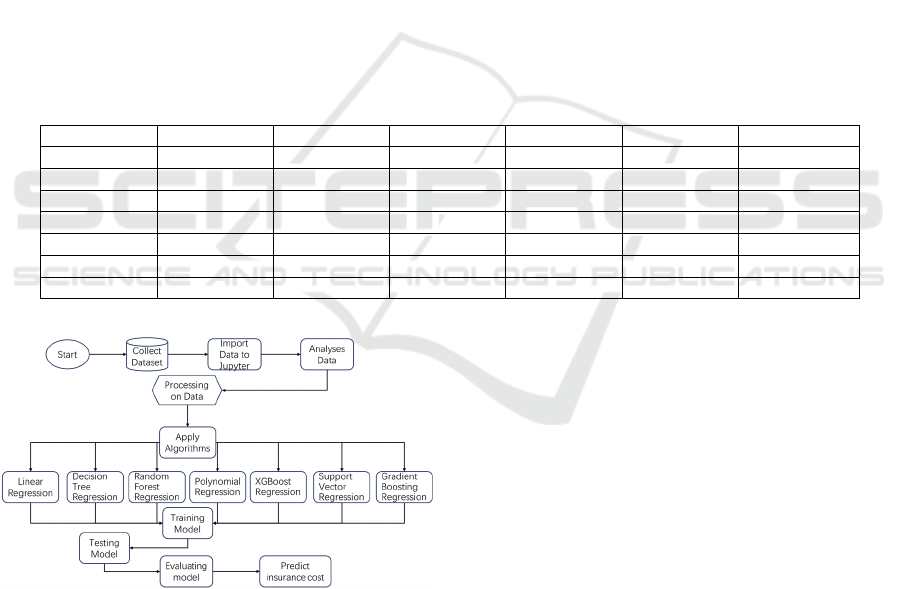

2 METHODOLOGIES

This paper collects medical insurance data from

Kaggle. The data includes 7 features, 4 of which are

numerical and 3 categorical. The focus is on

predicting the exact price of medical insurance based

on these 7 features (Table 1). This section briefly

describes the research process depicted in Figure 1.

The study followed five main stages: data

preprocessing, exploratory data analysis (EDA),

model training and evaluation, overfitting analysis,

and feature contribution analysis. The dataset was

cleaned and prepared, followed by EDA to

understand data distributions. Multiple machine

learning models were then trained and evaluated

using key metrics such as R² and RMSE. Overfitting

was assessed, and feature contributions were analysed

using SHAP values.

Table 1: Part of dataset

Age Sex Bmi Children Smoker Region Charges

19 Female 27.900 0 yes Southwest 16884.92400

18 Male 33.700 1 No Southeast 1725.55230

28 Male 33.000 3 No Southeast 4449.46200

33 Male 22.705 0 No Northwest 21984.47061

32 Male 28.880 0 No Northwest 3866.85520

31 Female 25.740 0 No Southeast 3756.62160

46 Female 33.440 1 No Southeast 8240.58960

Figure 1. Detailed Flowchart for Predicting Medical

Insurance Costs (Picture credit: Original)

2.1 Data Preprocessing

The data preprocessing stage focused on preparing

the dataset for analysis and modeling. Firstly, the

dataset used in this study had no missing values.

Categorical variables, including gender, smoking

status, and region, were encoded into numerical

representations using mapping dictionaries. This

transformation was essential to enable machine

learning models to process these features effectively.

Initially, numerical features such as age, BMI, and

charges were not standardized. These features were

first examined in their raw form and utilized in the

initial phase of algorithm development. It was only

during subsequent stages of algorithm optimization

that these features underwent standardization to

ensure that differences in feature scales would not

bias the model training process. These preprocessing

steps collectively ensured the dataset was clean,

consistent, and ready for further analysis.

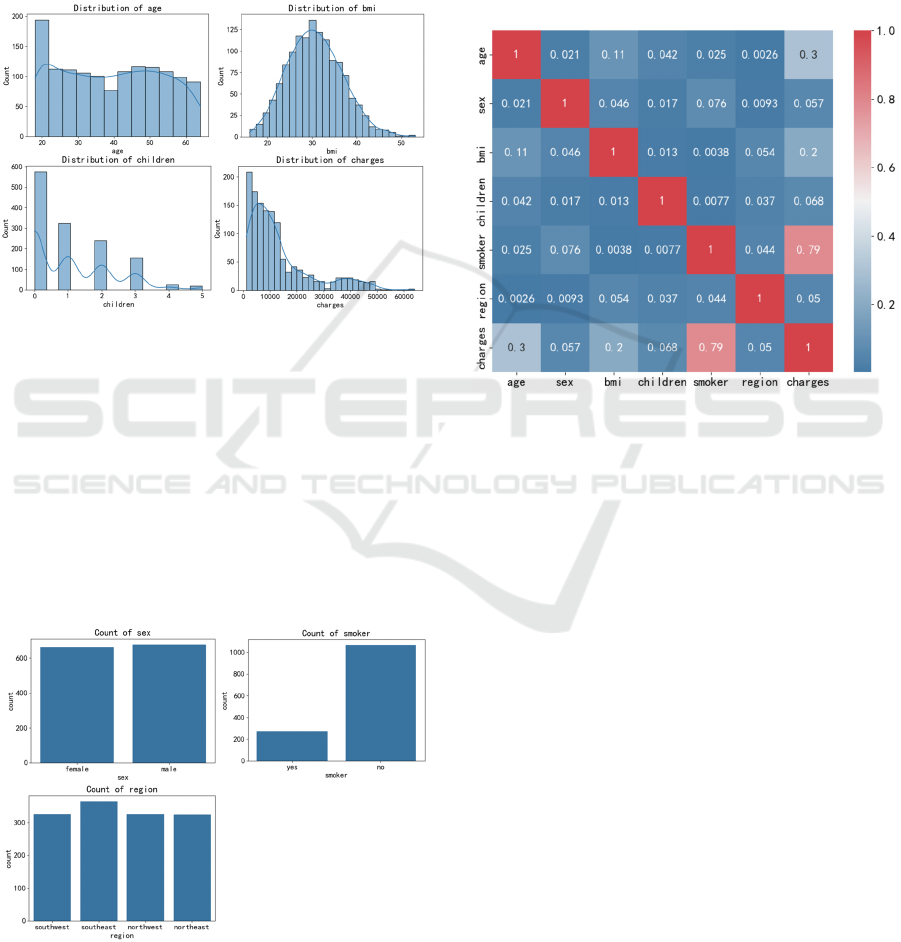

2.2 Exploratory Data Analysis (EDA)

To gain insights into the dataset, Exploratory Data

Analysis (EDA) was performed using visualization

techniques and summary statistics. The distribution

of numerical features was explored through

histograms and kernel density estimation (KDE)

plots. For example, Figure 2 illustrates the

ICDSE 2025 - The International Conference on Data Science and Engineering

574

distribution of numerical variables such as Age, BMI,

and Charges. The x-axis represents the value range of

each feature, while the y-axis indicates the frequency

or density of occurrences. The plot reveals that BMI

exhibits a right-skewed distribution, with most values

concentrated in the lower range. Medical charges, on

the other hand, show a wide variability, indicating

significant differences in insurance costs among

individuals.

Figure 2: Distribution of Numerical variables (Picture

credit: Original)

Figure 3 examines the distribution of categorical

variables, including Gender, Smoker, and Region.

Count plots were used to visualize the frequency of

each category. The x-axis denotes the categories (e.g.,

Male/Female, Yes/No for smoker status, and different

regions), while the y-axis shows the number of

occurrences. The analysis confirms a balanced

representation of genders and smoking statuses in the

dataset, with a relatively even distribution across

different regions.

Figure 3: Distribution of Categorical variables (Picture

credit: Original)

Figure 4 presents a heatmap of Pearson

correlation coefficients, visualizing the strength of

relationships between features. The x-axis and y-axis

both represent the features in the dataset, while the

color intensity indicates the magnitude of correlation.

The heatmap reveals strong positive correlations

between smoking status and medical charges, as well

as between BMI and medical charges. These findings

highlight the potential of smoking status and BMI as

significant predictors of insurance costs.

Figure 4: Pearson Correlation Heatmap (Picture credit:

Original)

Overall, this phase of EDA provided a solid

understanding of the dataset, setting the foundation

for model development. The visualizations and

statistical summaries helped identify key patterns and

relationships that would inform the selection and

training of machine learning models.

3 RESULTS

3.1 Model Training and Evaluation

Multiple machine learning models were trained to

predict insurance costs. The selected models included

Linear Regression, Decision Tree Regression,

Random Forest Regression, XGBoost Regression,

Support Vector Regression (SVR), Gradient Boosting

Regression, Polynomial Regression (degree=2) and

Polynomial Regression (degree=3). These models

were chosen to cover a spectrum of capabilities, from

simple linear predictors to complex ensemble

methods. The models were trained and tested on an

80-20 split of the dataset, and their performance was

evaluated using metrics such as R², mean squared

Refining Medical Insurance Cost Predictions with Advanced Machine Learning Models

575

error (MSE), and root mean squared error (RMSE).

Also, after the first stage of algorithm training, some

models had poor prediction performance, so the

algorithm was optimized in the second stage. The

final results are shown in the Table 2. XGBoost,

Gradient Boosting, and Random Forest emerged as

the top-performing models, delivering high predictive

accuracy and robust generalization.

Table 2: Result of all the algorithms

Re

g

ression Models R s

q

uared MSE RMSE MAE

Linear Regression 0.78 34,011,470.00 5831.94 4211.92

Decision Tree Regression 0.76 37,916,750.00 6157.66 2798.95

Random Forest Regression 0.88 19,145,080.00 4375.51 2430.58

XGBoost Re

g

ression 0.88 18,013,380.00 4244.22 2383.64

SVR

(

Su

pp

ort Vector Re

g

ression

)

0.66 53,519,900.00 7315.73 3588.89

Gradient Boosting Regression 0.88 18,874,540.00 4344.48 2392.89

Polynomial Regression (degree=2) 0.87 20,558,010.00 4534.09 2722.62

Polynomial Regression (degree=3) 0.85 22,646,870.00 4758.87 2844.96

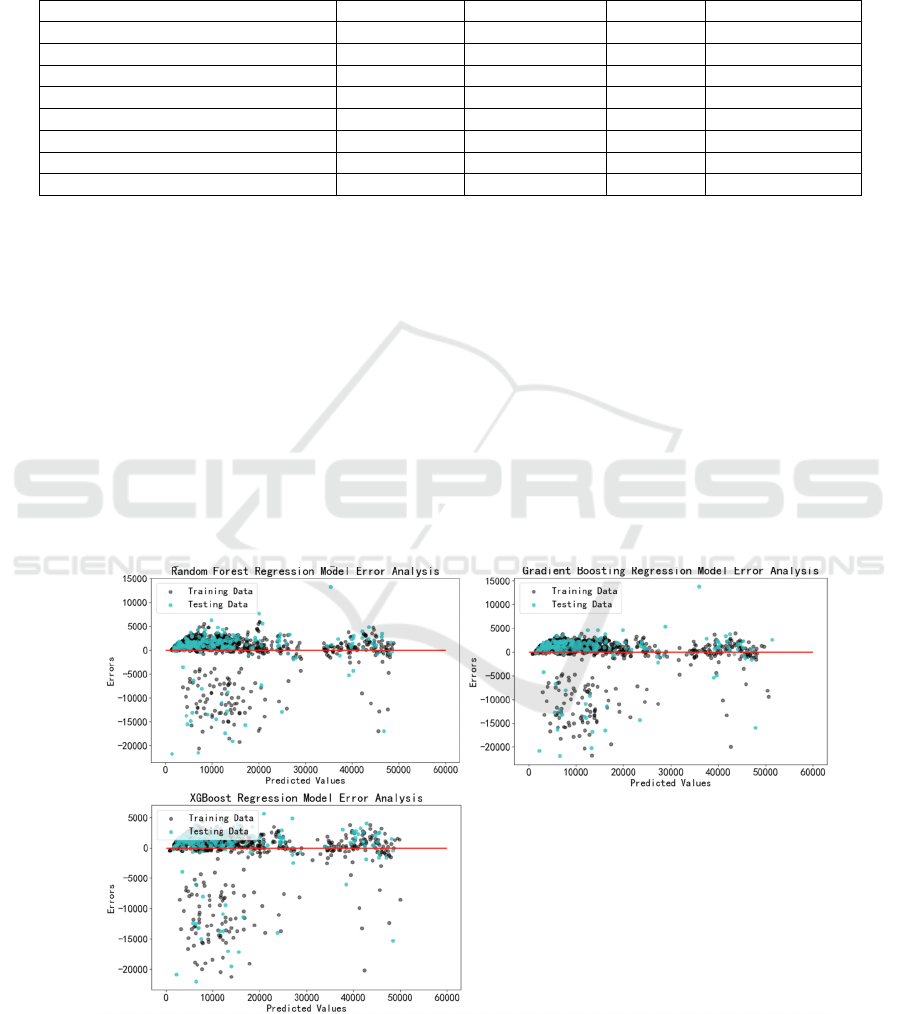

3.2 Model Training and Evaluation

In the realm of predictive modelling, overfitting is a

prevalent concern that can undermine the reliability

of a model's predictions on unseen data. To address

this, the paper conducted an analysis focusing on

three ensemble methods that demonstrated superior

performance in previous assessments: Random Forest

Regression, XGBoost Regression, and Gradient

Boosting Regression.

Figure 5 illustrates the residual plots for each of

the three models, showing how prediction errors are

distributed. In these plots, the x-axis represents the

predicted values, while the y-axis shows the residuals

(the difference between actual and predicted values).

Ideally, residuals should be randomly scattered

around zero without any discernible pattern. For

Random Forest Regression, the residuals exhibit

some clustering but are generally well-distributed.

XGBoost Regression shows an even more uniform

distribution of residuals, indicating minimal bias in

predictions. Gradient Boosting Regression also

displays a favourable pattern, with residuals closely

clustered around zero. These visual assessments

suggest that all three models generalize well to

unseen data.

Figure 5: Residual Plots of 3 Regression Models (Picture credit: Original)

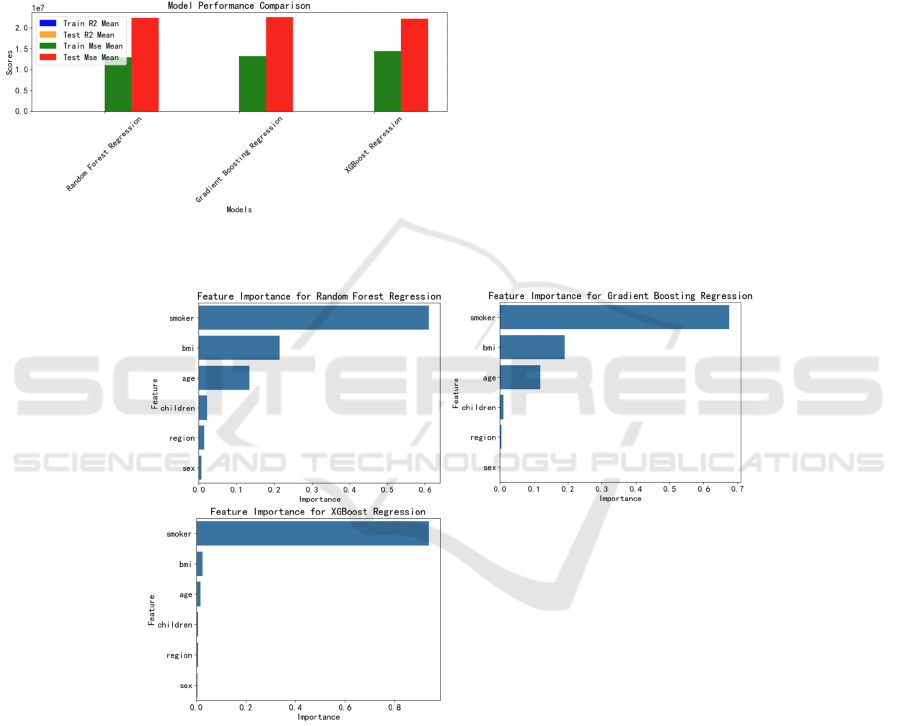

To further validate these observations, we

employed cross-validation, a technique that provides

a quantitative measure of model performance across

different subsets of data. Figure 6 presents the cross-

ICDSE 2025 - The International Conference on Data Science and Engineering

576

validated performance metrics for the three models.

The x-axis denotes the models, while the y-axis

shows the average R² score and Mean Squared Error

(MSE) from cross-validation. The results confirm that

all three models achieve high R² scores and low MSE

values, indicating strong predictive accuracy and

robust generalization. XGBoost Regression slightly

outperforms the others, with the highest R² score and

the lowest MSE, reinforcing its effectiveness in

capturing complex patterns in the data.

Figure 6: Cross-Validated Performance of 3 Regression

Models (Picture credit: Original)

3.3 Feature Contribution Analysis

This paper assesses the influence of various features

on predictive outcomes by computing feature

importance scores for tree-based models. This

method ranks variables based on their impact on

predictions, identifying the most influential features

in the model's decision-making process. The analysis

also includes SHAP values to provide a detailed

examination of each feature's contribution to

individual predictions, thereby enhancing model

interpretability.

Figure 7 displays the feature importance plots for

the three regression models. The x-axis represents the

feature importance scores, while the y-axis lists the

features. For all models, 'smoker' status and 'BMI' are

identified as the most influential features, followed by

'age' and 'number of children'. This ranking

underscores the significant impact of lifestyle and

health indicators on insurance costs.

Figure 7: Feature Importance Plot of 3 Regression Models (Picture credit: Original)

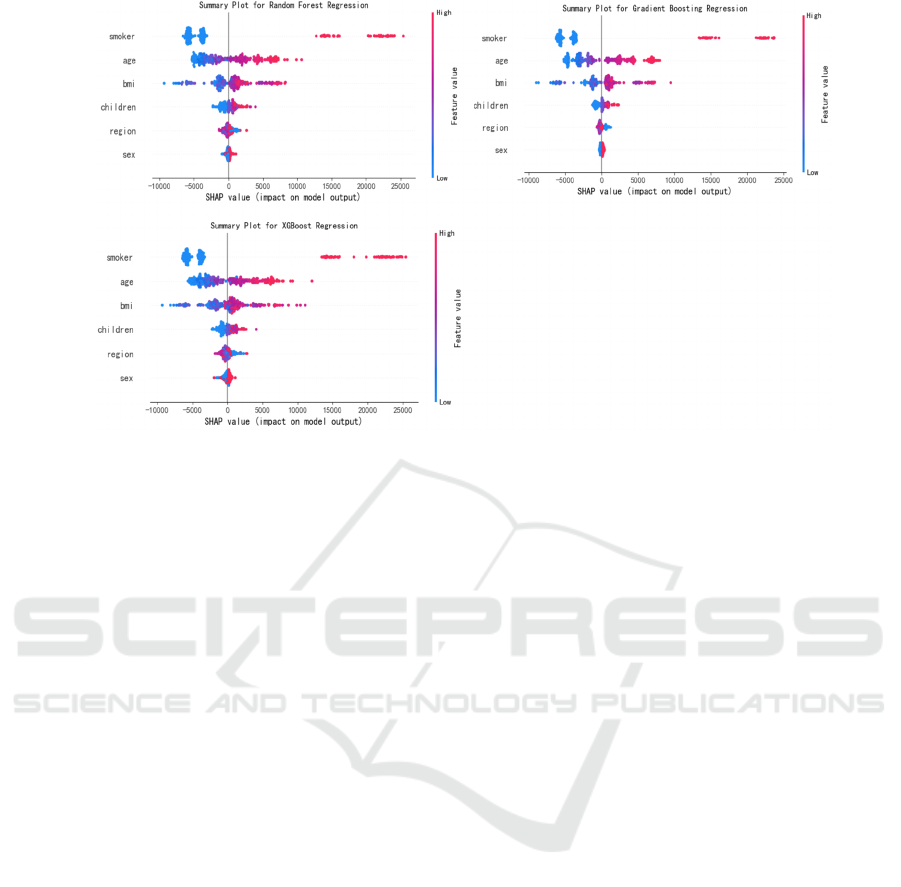

Figure 8 presents the SHAP summary plots for the

same models, offering a granular view of each

feature's contribution to individual predictions. The

x-axis shows the SHAP values, indicating the impact

of each feature on the model output, while the y-axis

lists the features, with the most important ones at the

top. The plots reveal that 'smoker' status has a

substantial positive impact on predicted charges,

while 'BMI' and 'age' also contribute significantly.

These findings align with the results from the

exploratory data analysis, highlighting the critical

role of these features in determining costs.

Refining Medical Insurance Cost Predictions with Advanced Machine Learning Models

577

Figure 8: SHAP Summary Plot of 3 Regression Models (Picture credit: Original)

Overall, the combination of feature importance

scores and SHAP values provides a comprehensive

view of feature contributions, confirming the

dominant influence of 'smoker' status, 'BMI', and 'age'

on insurance pricing. This analysis offers

transparency into the models' decision-making

processes and provides a clear basis for further

discussions on model implications.

4 DISCUSSION OF RESULTS

This study systematically evaluates the performance

of diverse machine learning algorithms in predicting

medical insurance costs and elucidates the underlying

factors driving these predictions. The following

sections provide an in-depth discussion of model

performance disparities, interpretability insights from

residual and SHAP analyses, limitations of the

current approach, and future research directions.

4.1 Model Performance and

Algorithmic Disparities

The superior performance of XGBoost and Random

Forest regression models (R² = 0.88) compared to

simpler methods like Linear Regression (R² = 0.78)

highlights the critical role of ensemble techniques in

capturing non-linear relationships and complex

feature interactions. XGBoost’s gradient-boosting

framework, which iteratively corrects errors from

previous trees, enables it to model intricate patterns in

healthcare data more effectively than shallow models

(Chen & Guestrin, 2016). In contrast, Linear

Regression, while computationally efficient, assumes

linearity and homoscedasticity — assumptions often

violated in healthcare cost datasets characterized by

skewed distributions and heteroscedasticity (Cenita et

al., 2023). Decision Tree Regression’s tendency to

overfit (training RMSE: 2798.95 vs. test RMSE:

6157.66) underscores the limitations of single-tree

models in generalizing to unseen data, a weakness

mitigated by ensemble methods through aggregation

and regularization (Biau & Scornet, 2016).

The robust generalization of ensemble methods is

further validated by residual analysis (Figure 5),

where errors for XGBoost and Random Forest are

symmetrically distributed around zero, indicating

minimal bias. In contrast, Linear Regression exhibits

systematic underestimation of high-cost cases

(residuals > 10,000), likely due to its inability to

account for multiplicative effects between variables

such as smoking and age. This aligns with findings by

Orji and Ukwandu (2024), who noted that linear

models often fail to capture interactions critical to

healthcare cost prediction.

Future improvements could explore hybrid

approaches, such as stacking ensemble models with

deep learning architectures (e.g., neural networks) to

further enhance predictive accuracy. Additionally,

incorporating domain-specific constraints (e.g.,

actuarial fairness principles) into model training

could address potential biases in risk assessment

(Sharma & Jeya, 2024).

ICDSE 2025 - The International Conference on Data Science and Engineering

578

4.2 Interpretability Insights: Smoking,

BMI, and Residual Patterns

The SHAP analysis (Figures 7–8) identifies smoking

status and BMI as the most influential predictors,

consistent with prior studies linking these variables to

chronic diseases and elevated healthcare utilization

(Panay et al., 2020). Smoking’s outsized impact

(SHAP value range: +5,000 to +20,000) reflects its

association with conditions such as lung cancer and

cardiovascular diseases, which incur high treatment

costs (Boodhun & Jayabalan, 2018). The positive

correlation between BMI and charges (SHAP range:

+1,000 to +8,000) may stem from obesity-related

comorbidities like diabetes and hypertension, which

drive long-term medical expenses (Jain & Singh,

2018). Notably, the interaction between smoking and

BMI—though not explicitly modeled—could amplify

risks, as smoking exacerbates metabolic dysfunction

in obese individuals (Vijayalakshmi et al., 2023).

Future work should incorporate interaction terms or

employ interpretable models like Generalized

Additive Models (GAMs) to disentangle these

effects.

Residual patterns further reveal that ensemble

methods minimize systematic errors for high-cost

cases, whereas simpler models struggle with outliers.

This aligns with the findings of Jain and Singh

(2018), who emphasized that tree-based models

inherently handle skewed distributions through

hierarchical partitioning, unlike linear models reliant

on Gaussian assumptions.

4.3 Limitations and Future Direction

While this study advances medical insurance cost

prediction, several limitations warrant attention. First,

the dataset (n=1,338) is relatively small and lacks

granular clinical variables (e.g., pre-existing

conditions, medication history), limiting the model’

s ability to capture nuanced health risks. Expanding

data sources to include electronic health records

(EHRs) or claims histories could improve predictive

granularity (Panda et al., 2022). Second, the study

focuses on tree-based models and polynomial

regression; alternative approaches like Bayesian

networks or transformer-based architectures remain

unexplored. Recent work by Ejiyi et al. (2022)

suggests that Bayesian methods excel in uncertainty

quantification, a valuable feature for risk-sensitive

applications like insurance pricing.

Finally, the ethical implications of using

behavioral features (e.g., smoking) for pricing require

careful consideration. While these variables improve

accuracy, they risk penalizing individuals for lifestyle

choices influenced by socioeconomic factors. Future

research should integrate fairness-aware machine

learning techniques to ensure equitable premium

calculations (Billa & Nagpal, 2024).

By addressing these limitations and building on

the interpretability frameworks established here,

subsequent studies can further bridge the gap between

predictive accuracy and ethical, transparent insurance

pricing.

5 CONCLUSION

This paper establishes a robust framework for make

predictions in medical insurance by harmonizing

advanced machine learning techniques with model

interpretability tools. Through systematic

comparisons of algorithms including XGBoost,

Random Forest, and polynomial regression, the

research demonstrates that ensemble methods

outperform traditional linear models in capturing

complex feature interactions, achieving an R² of 0.88.

Crucially, the integration of SHAP values provides

granular insights into the drivers of insurance costs—

notably smoking status and BMI—while residual

analysis validates the generalizability of these

models. By bridging predictive accuracy with

transparency, this work addresses a critical gap in

actuarial science, where interpretability is essential

for ethical pricing strategies and stakeholder trust.

This research validates the utility of machine

learning approaches, particularly ensemble methods

like XGBoost and Random Forest, in accurately

predicting insurance costs. By integrating SHAP

values, the study identifies significant predictors and

explains their impact on individual predictions

transparently. The findings highlight the importance

of behavioral factors, such as smoking status, in

determining insurance premiums, offering insights

into the complex interplay of health-related variables

and financial risk.

Financially, these findings have several

implications. Firstly, recognizing smoking status as a

critical cost driver underscores the need for insurers

to develop risk-adjusted premium structures that

reflect behavioral health risks adequately. This could

encourage healthier lifestyles among policyholders,

potentially reducing overall claims and enhancing the

financial sustainability of insurance portfolios.

Secondly, the study underscores the value of

advanced machine learning techniques in risk

assessment, offering insurers a tool to improve the

accuracy of their pricing strategies. Accurate cost

Refining Medical Insurance Cost Predictions with Advanced Machine Learning Models

579

predictions enable more competitive pricing,

allowing insurers to maintain market share while

minimizing financial risk.

Moreover, the use of SHAP values introduces a

level of interpretability crucial in the financial sector,

where decision-making often requires transparency to

gain stakeholder trust. By elucidating the contribution

of each feature, this research provides insurers with

actionable insights, enabling them to communicate

pricing decisions more effectively to customers and

regulators. For instance, the significant impact of

BMI and smoking status on premiums could serve as

evidence for targeted wellness programs or

differential pricing based on modifiable health

behaviors.

Additionally, this study contributes to the broader

discourse on financial risk management by

demonstrating how data-driven approaches can

optimize pricing strategies while maintaining fairness

and equity. The negligible influence of regional

factors in this dataset suggests that geographic pricing

discrimination may not be justified in certain

contexts, reinforcing the importance of evidence-

based decision-making in financial services.

In summary, this research bridges the gap between

advanced predictive modeling and practical financial

applications, offering a roadmap for insurers to

leverage machine learning for improved pricing

accuracy and risk assessment. It highlights the

potential for data-driven insights to drive innovation

in financial product design, ultimately contributing to

a more efficient and equitable insurance market.

REFERENCES

Billa, M.M., Nagpal, T., 2024. Medical insurance price

prediction using machine learning. Journal of

Electrical Systems, 20(7s), 2270-2279.

Boodhun, N., Jayabalan, M., 2018. Risk prediction in life

insurance industry using supervised learning

algorithms. Complex & Intelligent Systems, 4(2), 145-

154.

Cenita, J.A.S., Asuncion, P.R.F., Victoriano, J.M., 2023.

Performance evaluation of regression models in

predicting the cost of medical insurance. arXiv preprint

arXiv: 2304.12605.

Ejiyi, C.J., Qin, Z., Salako, A.A., et al., 2022. Comparative

analysis of building insurance prediction using some

machine learning algorithms.

Orji, U., Ukwandu, E., 2024. Machine learning for an

explainable cost prediction of medical insurance.

Machine Learning with Applications, 15, 100516.

Panay, B., Baloian, N., Pino, J.A., et al., 2020. Feature

selection for health care costs prediction using weighted

evidential regression. Sensors, 20(16), 4392.

Panda, S., Purkayastha, B., Das, D., et al., 2022. Health

insurance cost prediction using regression models. In:

2022 International Conference on Machine Learning,

Big Data, Cloud and Parallel Computing (COM-IT-

CON). IEEE, 1, 168-173.

Pudjihartono, N., Fadason, T., Kempa-Liehr, A.W., et al.,

2022. A review of feature selection methods for

machine learning-based disease risk prediction.

Frontiers in Bioinformatics, 2, 927312.

Sharma, A., Jeya, R., 2024. Prediction of insurance cost

through ML structured algorithm. In: 2024 IEEE

International Conference on Computing, Power and

Communication Technologies (IC2PCT). IEEE, 5, 495-

500.

Vijayalakshmi, V., Selvakumar, A., Panimalar, K., 2023.

Implementation of medical insurance price prediction

system using regression algorithms. In: 2023 5th

International Conference on Smart Systems and

Inventive Technology (ICSSIT). IEEE, 1529-1534.

Medical Cost Personal Datasets,

https://www.kaggle.com/datasets/mirichoi0218/insura

nce.

Biau, G., Scornet, E., 2016. A random forest guided tour.

Test, 25, 197-227.

Chen, T., Guestrin, C., 2016. XGBoost: A scalable tree

boosting system. In: Proceedings of the 22nd ACM

SIGKDD International Conference on Knowledge

Discovery and Data Mining, 785-794.

Jain, D., Singh, V., 2018. Feature selection and

classification systems for chronic disease prediction: A

review. Egyptian Informatics Journal, 19(3), 179-189.

ICDSE 2025 - The International Conference on Data Science and Engineering

580