A Cost-Sensitive Method for Credit Card Default Prediction

Yiqi Zhou

a

Department of Mathematics, The Ohio State University, 281 W. Lane Avenue, Columbus, Ohio 43210, U.S.A.

Keywords: Credit Card Default, Cost-Sensitive, Tuning Threshold, Gradient Boosting, Financial Risk.

Abstract: With an increasing number of credit cards being issued, financial institutions must predict credit card default

to minimize bad debts and remain profitable. Traditional machine learning approaches typically emphasize

maximizing overall accuracy but neglect the higher cost of missing actual defaulters (false negatives, FNs).

This research introduces a cost-sensitive framework that involves robust data cleaning, multi-model

comparisons, and threshold tuning. Based on a University of California, Irvine (UCI) dataset containing

30,000 records and 25 features, the procedure merges anomalous categories, removes duplicates, and

standardizes skewed numeric columns. Benchmarking three popular algorithms—Logistic Regression,

Random Forest, and eXtreme Gradient Boosting (XGBoost)—reveals that XGBoost attains the highest Area

Under the Curve (AUC) and recall for credit defaulters. Building on these findings, the XGBoost decision

threshold is further adjusted by assigning heavier penalties to FNs than to false positives (FPs). Experimental

results indicate that without such an intervention, potential bad debt nears 877,900 (or 11.58 percent of the

total), whereas the cost-sensitive approach reduces it to approximately 432,400 (or 5.64 percent), highlighting

the limits of raw accuracy metrics. This paper concludes with a discussion of interpretability, advanced

hyperparameter tuning, and deployment considerations in real-world finance, reflecting data up to October

2023.

1 INTRODUCTION

Credit card lending remains a major revenue source

for banks, yet it can also involve default risks that

erode profits and jeopardize long-term stability.

Expanding consumer credit access around the globe

has made the effective identification of potential

defaulters increasingly vital. Machine learning has the

potential to reinforce and automate credit risk

decisions, sometimes outperforming conventional

models in both speed and predictive power. Brown

and Mues (2012) indicate that ensemble methods

often handle imbalanced credit scoring more

effectively than older techniques, while Yeh and Lien

(2009) show that data mining approaches frequently

surpass standard statistical models in identifying

defaulters. These findings illustrate the promise of

advanced algorithms—such as gradient boosting or

cost-sensitive classification—for leveraging large-

scale finance data and achieving more accurate,

efficient predictions than standard solutions.

However, existing methods tend to focus on metrics

a

https://orcid.org/0009-0000-1834-8521

like accuracy or AUC without investigating how

misclassifications differently influence institutional

outcomes.

Cost asymmetry, if ignored, may result in

suboptimal performance. A missed defaulter (FN) can

entail a far higher cost than a false alarm (FP), because

lenders risk losing the entire unpaid balance plus fees,

whereas a wrongly flagged customer experiences only

minor inconvenience or limited credit access

(Bahnsen, Aouada, & Ottersten, 2015; He & Garcia,

2009). Certain studies address class imbalance

through oversampling or weighting, but often

overlook actual monetary losses. Meanwhile, data

quality issues—such as “filler” categories, duplicates,

and skewed numeric fields (credit limit, bill

amounts)—can distort modeling results. Merging

anomalous labels, removing repeated records, and

normalizing columns helps mitigate these challenges

(Li, Zhao, & Wu, 2019). Another key concern is

interpretability: although complex ensembles like

gradient boosting yield strong predictive performance,

they often appear opaque to loan officers or regulators

who seek transparency in decision-making.

516

Zhou, Y.

A Cost-Sensitive Method for Credit Card Default Prediction.

DOI: 10.5220/0013701200004670

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 2nd International Conference on Data Science and Engineering (ICDSE 2025), pages 516-520

ISBN: 978-989-758-765-8

Proceedings Copyright © 2025 by SCITEPRESS – Science and Technology Publications, Lda.

A cost-sensitive framework is introduced to

manage these problems, combining enhanced data

preprocessing on the UCI dataset (merging rare labels,

removing duplicates, and scaling skewed features)

with threshold-based penalization of FNs in XGBoost.

Small threshold adjustments can substantially reduce

potential losses, thereby bridging standard

classification metrics and the real-world economic

landscape. This perspective raises credit modeling

beyond routine data cleansing, aligning machine

learning decisions more closely with the financial

realities of default risk.

2 METHODS

2.1 Dataset

The “Default of Credit Card Clients” dataset made

publicly available by Yeh and Lien (2009) in the UCI

Machine Learning Repository (Dua & Graff, 2019) is

employed. It contains 30,000 records and 25 features,

with each record representing a unique cardholder’s

demographic and financial attributes. The target label

specifies whether a cardholder is in default (1) or not

(0). According to Yeh and Lien (2009), around 22%

of cardholders default in the original data, whereas

78% do not. If further filtering or cleaning is

performed, the final distribution should be

reconfirmed, but in its default version the data

generally splits at approximately 22% default vs. 78%

non-default. This imbalance can motivate naive

models to prioritize the majority class if maximizing

accuracy alone is the objective.

2.1.1 Data Cleaning

Combining certain anomalous values in

EDUCATION (0,5,6) and MARRIAGE=0 into an

“other” category (such as EDUCATION=4,

MARRIAGE=3) prevents fragmentation arising from

extremely rare labels. Any duplicate entries are

eliminated to maintain unique records, given that

duplication can distort metrics if repeated samples are

uncommonly easy or difficult to classify. Numeric

columns such as LIMIT_BAL, monthly bill amounts,

and payment amounts can display significant

skewness, so standard scaling ((x − µ)/σ) is applied to

reduce outlier influence. Although alternative

transformations such as logs are feasible,

standardization aligns well with the pipeline setup.

2.1.2 Exploratory Analysis

A check of the distribution of default vs. non-default,

the range of numeric columns, and correlations across

features (for example, monthly billing correlated with

repayment) is carried out to identify whether any

derived features could be impactful. Despite these

examinations, the original columns remain in place

for the main modeling stage.

2.2 Models

Logistic Regression is a linear model that calculates

log-odds for the default class based on weighted

feature inputs. While it offers convenient

interpretability via its coefficients, it may overlook

significant nonlinearities in financial data unless

supplementary transformations are introduced.

Random Forest, in contrast, merges multiple decision

trees constructed via bootstrap aggregating, which

often delivers robust performance on tabular credit

data by modeling more complex relationships than

purely linear methods. Some interpretability is

retained through feature importance measures, yet the

model structure is inherently more opaque than

Logistic Regression. XGBoost applies a gradient

boosting strategy (Chen & Guestrin, 2016),

incrementally refining shallow trees through

advanced regularization and efficient handling of

missing data. Research by Brown and Mues (2012)

suggests that boosting algorithms frequently outdo

simpler ensembles in terms of AUC and recall when

dealing with credit scoring challenges, indicating that

XGBoost is likely to be either the top performer or a

strong benchmark for real-world default detection.

All models undergo identical transformations,

including standardized numeric columns, one-hot

encoded categorical variables (with merged “other”

categories), and an 80–20 split into train and test

subsets.

2.3 Experimental Setup

2.3.1 Train–Test Split

A random partition is carried out, with 80% of the

available records (24,000) dedicated to training and

20% (6,000) allocated to testing, while preserving the

proportion of defaulters in each subset. This approach

replicates the default and non-default distribution

encountered in the original dataset (Hand & Henley,

1997).

2.3.2 Performance Metrics

Before each model is trained, the standard

transformations mentioned above are applied, and

default hyperparameters are used unless noted

A Cost-Sensitive Method for Credit Card Default Prediction

517

otherwise. Evaluation includes accuracy, AUC, recall

(for defaulters), precision, and F1. Accuracy can be

deceptive under imbalanced conditions, while AUC

reflects how effectively the model ranks defaulters

over non-defaulters. High recall for defaulters is vital

in credit settings, since missed defaulters (false

negatives) impose considerable costs. Precision

measures how many predicted defaulters indeed

default, whereas the F1 score balances recall and

precision in a single index. Earlier findings (Brown &

Mues, 2012) imply that XGBoost tends to surpass

simpler baselines in terms of AUC and recall for

credit defaulters, thereby providing a stable basis for

further threshold calibration.

3 RESULT

Logistic Regression, Random Forest, and XGBoost

are trained and the metrics are collected in Table 1:

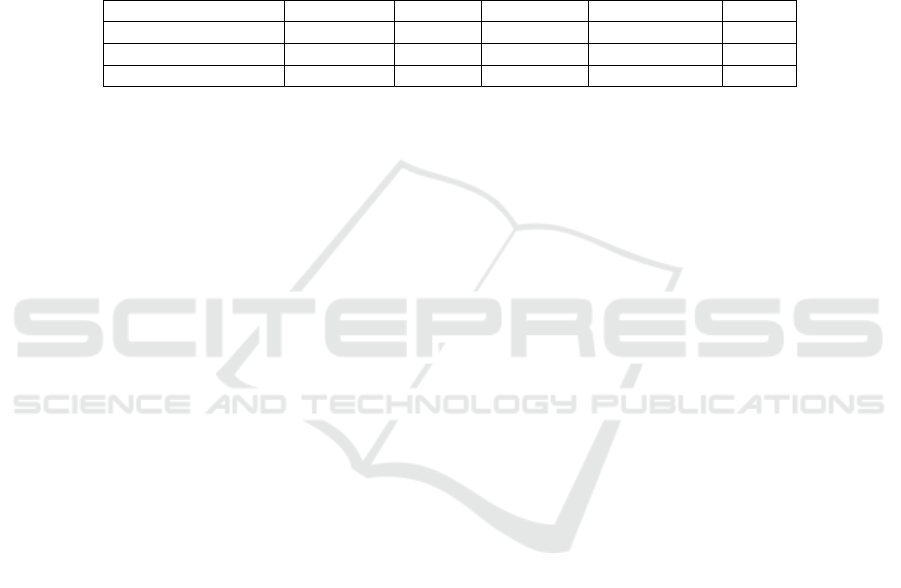

Table 1: Comparison of model performance indicators

Model

Accurac

y

AUC Recall(1) Precision(1) F1(1)

Lo

g

istic Re

g

ression 0.81 0.7062 0.25 0.69 0.37

Random Forest 0.81 0.7550 0.36 0.64 0.46

XGBoost 0.81 0.7588 0.36 0.61 0.45

All three perform at an accuracy of ~81%,

suggesting moderate separability of the dataset. But

XGBoost gives the highest AUC (0.7588) and the

same recall(1) (=0.36) as Random Forest. On the

contrary, the recall of Logistic Regression(1) is only

0.25, indicating that it misses more defaulters. For

institutions that give priority to capturing defaulters,

XGBoost is the best candidate before threshold tuning.

In standard classification, a threshold of 0.5 is

commonly employed: predicted probabilities greater

than or equal to 0.5 result in a “default” label.

However, as Bahnsen et al. (2015) suggest, the cost

of a missed defaulter (FN) in credit risk substantially

exceeds that of a false positive (FP), and failing to

account for these differences frequently leads to

suboptimal default detection. Consequently, the

approach here defines a cost function that imposes a

heavier penalty on FNs.

4 DISCUSSION

4.1 Comparison with Other Work

Many studies have highlighted advanced boosting or

ensemble methods for credit scoring but have

centered primarily on optimizing metrics such as

AUC or recall (Li et al., 2019). By systematically

scanning thresholds under an explicit cost function

and translating different error types into direct

monetary impacts, the present approach offers a

clearer understanding of how false negatives and false

positives each influence potential losses. This

perspective extends beyond basic imbalance handling

(He & Garcia, 2009) by identifying the precise cost

ratio that best aligns with real-world risk.

Consequently, the measure proposed here provides a

tangible metric of potential bad-debt reduction,

distinguishing it from methods that merely improve

top-line classification rates without clarifying

financial consequences.

4.2 Real-World Implementation

If the framework is to be deployed in an actual

banking environment, it must be established who

would revise the threshold and how frequently. One

possibility is to perform monthly updates to the ratio

of Cost_FN vs. Cost_FP, using default outcomes or

macroeconomic indicators observed within that

period. Such updates would then feed into the

production XGBoost scoring model, causing

acceptance rates for borderline applicants to fluctuate

depending on current risk conditions. Regulators

might question the equity or transparency of a

frequently shifting threshold, thus suggesting the

need for interpretability measures or disclaimers that

clarify the strategic selection of cost-based thresholds.

4.3 Managing Macroeconomic

Ambiguity

Credit default rates can rise and fall alongside broader

economic trends. When unemployment increases,

more borrowers might fail to repay their balances,

rendering a static threshold increasingly risky.

Adopting a dynamic threshold—one that lowers

automatically when default rates climb—may

mitigate some portion of potential damage. If

combined with advanced forecasting tools, this tactic

could guide lenders to tighten acceptance policies

before an expected recession. Still, implementing

ICDSE 2025 - The International Conference on Data Science and Engineering

518

real-time or frequent updates to the cost function may

become logistically complex, requiring additional

processes for data ingestion and threshold

recalibration.

4.4 Potential Extensions

One extension might involve incorporating hybrid

models that blend XGBoost with specialized anomaly

detection techniques, particularly for unusual

behavior in credit usage. Another possibility involves

deeper exploration of feature contributions, moving

beyond threshold scans to examine which attributes

drive cost outcomes most strongly. In some cases, a

time-series or sequence-based approach might be

pursued if payment patterns over multiple months can

be formulated as a sequence, thus applying RNN or

transformer architectures. Finally, methods such as

SHAP or LIME can clarify which features

consistently trigger a default label, thereby satisfying

stakeholders who need transparency (Zhang & Li,

2020).

4.5 Limitations Revisited

Although this cost-sensitive approach unifies data

preprocessing, multi-model comparison, and

threshold optimization in XGBoost, several

constraints remain. First, the 1000:100 ratio is

heuristic and may not reflect actual institutional

practices. Different banks could adopt distinct scales

based on average credit limits or interest structures,

indicating that a tiered or dynamic cost matrix might

better capture genuine lending risks. Second, only a

basic version of XGBoost was tested here, and

advanced hyperparameter tuning or specialized cost-

sensitive objectives could further refine outcomes.

Third, the study hinges on one UCI dataset,

suggesting a need for external validation on

proprietary data to verify real-world performance.

Finally, threshold scanning occurs offline, whereas

continuous risk environments require pipelines for

frequent data ingestion, model retraining, and

threshold readjustment. Nonetheless, emphasizing

penalties for missed defaulters reduces estimated bad

debt from roughly 877,900 to 432,400, underscoring

how accuracy (or AUC) alone may conceal the severe

costs of high-risk borrowers. Future directions

include multitier cost ratios guided by credit lines,

deeper tuning of XGBoost, and integration of

interpretability tools such as SHAP or LIME for

regulatory approval. Online or dynamic thresholds

could also adapt to evolving economic signals,

ensuring that modeling keeps pace with real-world

lending operations (Zhou, 2012).

5 CONCLUSION

This study proposed a cost-sensitive framework for

credit card default prediction, which integrates

comprehensive data preprocessing, multi-model

comparison, and threshold optimization in the

XGBoost. Highlighting the imbalanced cost of

missing defaulters brought potential bad debt down

from around 877,900 to 432,400, pointing to the fact

that some metrics like accuracy or AUC can miss the

point in high-stakes finance contexts.

Discussion of these results emphasized how a

decision threshold adjustment, instead of just

maximizing standard measures, can better suit

classification to real-world lending goals. This insight

advances practice through cost-based threshold

tuning and overcoming missing sentiment, which will

improve risk management and profits.

Still, some limitations do exist. Decisions made

using the single-cost ratio present in this paper may

not generalize to all lenders, nor is it based on any

numerous datasets. Refining this approach with

multi-tiered cost frameworks or more sophisticated

hyperparameter searches would enhance its

robustness and adaptability. Moreover, the

interpretability issue is not solved in complex

ensemble approaches such as gradient boosting,

highlighting the need for explainable tools that can

help fulfill the requirements of transparency in

financial systems.

Therefore, in practice, this cost-sensitive strategy

can be implemented as part of the day-to-day decision

processes of banks and credit issuers that can update

their thresholds as market conditions change. Next

steps may be for models to become adaptive, updating

cost ratios in real time to further improve the risk

capture while maintaining a good balance with

overall portfolio performance.

REFERENCES

Bahnsen, A. C., Aouada, D., & Ottersten, B. 2015.

Example-dependent cost-sensitive logistic regression

for credit scoring. Expert Systems with Applications,

42(6), 2476–2486.

Brown, I., & Mues, C. 2012. An experimental comparison

of classification algorithms for imbalanced credit

scoring data sets. Expert Systems with Applications,

39(3), 3446–3453.

A Cost-Sensitive Method for Credit Card Default Prediction

519

Chen, T., & Guestrin, C. 2016. XGBoost: A scalable tree

boosting system. In Proceedings of the 22nd ACM

SIGKDD International Conference on Knowledge

Discovery and Data Mining, 785–794.

Hand, D. J., & Henley, W. E. 1997. Statistical classification

methods in consumer credit scoring: A review. Journal

of the Royal Statistical Society: Series A, 160(3), 523–

541.

He, H., & Garcia, E. A. 2009. Learning from imbalanced

data. IEEE Transactions on Knowledge and Data

Engineering, 21(9), 1263–1284.

Li, C., Zhao, K., & Wu, Y. 2019. Deep learning for credit

risk assessment: A review of challenges and solutions.

Expert Systems with Applications, 122, 206–220.

Thomas, L. C. 2009. Consumer credit models: Pricing,

profit, and portfolios. Oxford University Press.

Yeh, I.-C., & Lien, C.-H. 2009. The comparisons of data

mining techniques for the predictive accuracy of

probability of default of credit card clients. Expert

Systems with Applications, 36(2), 2473–2480.

Zhang, L., & Li, J. 2020. Cost-sensitive boosting trees for

financial risk assessment. IEEE Transactions on

Knowledge and Data Engineering, 32(5), 909–919.

Zhou, Z.-H. 2012. Ensemble methods: Foundations and

algorithms. Boca Raton, FL: CRC Press.

ICDSE 2025 - The International Conference on Data Science and Engineering

520