Practical Research on the Transformation of Financial Accounting

Electro-Algorithms into Management Accounting Electro-Algorithms

Jingkui Shao

School of Accounting and Finance, Beijing Institute of Technology, Zhuhai, China

Keywords: Computer Theory, Management Accounting Algorithm, Electronic Computer.

Abstract: The use of computers plays an important role in management accounting, but there is a problem of inaccurate

evaluation of results. The financial accounting algorithm cannot solve the problem of the use of electronic

computers in management accounting work, and the analysis is unreasonable. Therefore, this paper proposes

an electrical algorithm for management accounting and analyzes the use of electronic computers. First of all,

computer theory is used to analyze the management accounting work, and the indicators are divided according

to the requirements of the use of electronic computers to reduce them Interference factors in the use of

electronic computers. Then, the use of electronic computers by computer theory in management accounting

work forms an electronic computer use scheme and the use of electronic computers as a result Conduct a

comprehensive analysis. AICPA simulation shows that under certain analysis criteria, management

accounting algorithms are used in management accounting work The accuracy of the use of electronic

computers and the use time of electronic computers are better than financial accounting algorithms.

1 INTRODUCTION

With the rapid development of information

technology, electronic data processing technology

has become an important part of enterprise financial

management (ZHENG, WANG, et al. 2022).

Computerized technology provides more powerful,

accurate and timely data support for enterprise

management accounting, making the analysis and

decision-making of enterprise management

accounting more scientific and accurate. This article

will explore the optimization of management

accounting practices by computerized accounting and

how these optimizations can promote the

development of enterprise management accounting

(Waymond, Salem, et al. 2020).

1.1 Application of Accounting

Computerization Method in

Enterprise Management

Accounting

1.1.1 Financial Information Systems

The financial information system is the core system

of enterprise financial management, which can

effectively manage and statistically various financial

data of the enterprise (Zhang,, Bai, et al. 2020). It

includes general ledger, accounts receivable and

payable, inventory accounts, cost accounting, fixed

asset management and other modules, which can

facilitate the management of enterprises to query and

analyze. At the same time, the data of the financial

information system can also be integrated with other

business systems to realize the automatic processing

of business data (Scheffson, 2018).

1.1.2 Cost Accounting and Management

Cost accounting and management is an important task

of enterprise management accounting. Through

computerized technology, enterprises can automate

the processing of various cost information, including

direct costs, indirect costs, allocation costs, etc., so as

to achieve accurate cost calculation and management.

At the same time, enterprises can also monitor and

optimize product costs and production efficiency

through cost accounting and management systems

(Zhong, 2016).

398

Shao, J.

Practical Research on the Transformation of Financial Accounting Electro-Algorithms into Management Accounting Electro-Algorithms.

DOI: 10.5220/0013544200004664

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 3rd International Conference on Futuristic Technology (INCOFT 2025) - Volume 1, pages 398-404

ISBN: 978-989-758-763-4

Proceedings Copyright © 2025 by SCITEPRESS – Science and Technology Publications, Lda.

1.1.3 Budget Management

Budget management is another important job in

business management accounting. Through

accounting computerization technology, enterprises

can automatically process various budget

information, including sales budget, production

budget, cost budget, etc., so as to achieve accurate

budget formulation and management. At the same

time, enterprises can also monitor and optimize the

budget through the budget management system.

1.1.4 Decision Analysis

Decision analysis is an important part of enterprise

management accounting, through computerized

technology, enterprises can automatically process a

variety of financial and non-financial information,

including revenue, cost, profit, market, marketing and

other data, so as to achieve a comprehensive analysis

of enterprise operations and decision-making. At the

same time, through various data visualization tools,

enterprise managers can more intuitively understand

the operation status and trends of enterprises, so as to

make more accurate decisions (Al-Bukhrani, Al-

Matari, et al. 2023).

1.2 Optimization of Enterprise

Management Accounting Practice

by Accounting Computerization

Method

1.2.1 Improve the Accuracy and Reliability

of Management Accounting Data

Through the establishment and operation of the

financial information system, various financial data

of the enterprise can be better managed and statistical,

and the accuracy and reliability of the data can be

improved. At the same time, automated processing

also avoids manual processing errors and loopholes,

ensuring data integrity and security (Alhawtmeh,

2023).

1.2.2 Improve the Scientificity and Accuracy

of Analysis and Decision-Making

Through the application of accounting

computerization technology, enterprise managers can

more intuitively understand the operation status and

trends of enterprises, so as to make more accurate

decisions. At the same time, through the application

of data visualization tools, data can be better analyzed

and understood, thereby improving the scientificity

and accuracy of analysis and decision-making

(Anggadini, Yahya, et al. 2023).

1.2.3 Improve Management Efficiency and

Management Level

Through the application of cost accounting and

management system, enterprises can better manage

and control costs, thereby improving the management

efficiency and management level of enterprises. At

the same time, the application of budget management

system can also assist enterprises to formulate and

manage budgets, thereby improving the management

level of enterprises (Appleton, Barckow, et al. 2023).

1.2.4 Promote the Modernization and

Informatization of Enterprise

Management

Through the application of accounting

computerization technology, enterprises can realize

modernization and information management, and

improve the core competitiveness of enterprises.

Through the establishment and operation of financial

information system and other management

accounting systems, enterprise managers can

formulate and manage business strategies and

policies of enterprises more scientifically, so as to

improve the comprehensive competitiveness of

enterprises.

1.3 The Impact of Computerized

Accounting Method on the

Optimization of Enterprise

Management Accounting Practice

The application of accounting computerization

method will have an important impact on the

optimization of enterprise management accounting

practice (Azzam, Alsayed, et al. 2023). First of all,

the application of accounting computerization

technology can improve the accuracy and reliability

of enterprise management accounting data, and make

enterprise decision-making more scientific and

accurate. Secondly, the application of accounting

computerization technology can improve the

management efficiency and level of enterprises, and

make the operation of enterprises more efficient and

refined. Finally, the application of accounting

computerization technology can promote the

modernization and informatization of enterprise

management and improve the core competitiveness of

enterprises.

Practical Research on the Transformation of Financial Accounting Electro-Algorithms into Management Accounting Electro-Algorithms

399

This paper discusses the optimization of

management accounting practice by computerized

accounting method, including financial information

system, cost accounting and management, budget

management, and decision analysis. These

optimizations improve the accuracy and reliability of

enterprise management accounting data, improve the

scientificity and accuracy of analysis and decision-

making, improve management efficiency and level,

and promote the modernization and informatization

of enterprise management. These optimizations are of

great significance to the operation and development

of enterprises (Bawono, and Handika, 2023).

In the future, with the continuous development of

information technology, the application of accounting

computerization method will be more extensive and

deep. For example, the use of big data and artificial

intelligence technology can improve the analysis and

inference ability of accounting data, help enterprise

managers better understand and use financial data; at

the same time, it is also necessary to pay attention to

the ethical and social impact of information

technology to ensure the sustainable development of

science and technology.

The use of computer software is one of the

important contents of management accounting work,

which is of great significance to the development of

the accounting industry . However, in the process of

using electronic computers, there is a problem of poor

accuracy in the use of electronic computers, which

adds certain obstacles to audit and audit. Some

scholars believe that the application of management

accounting algorithms to the analysis of management

accounting work can effectively analyze the use

scheme of electronic computers and provide

corresponding support for the use of electronic

computers . On this basis, this paper proposes an

electrical algorithm for management accounting,

optimizes the use scheme of electronic computer, and

verifies the effectiveness of the model.

2 RELATED CONCEPTS

2.1 Mathematical Description of the

Electrical Algorithm of

Management Accounting

The management accounting algorithm is to use

double-entry accounting to optimize the use of the

electronic computer, and according to the indicators

in the use of the computer

i

y

, find the unqualified

value in the management accounting work

i

z

, and

correct The use of the computer scheme is integrated,

and the feasibility of management accounting work is

(

iij

tol y x⋅ )

finally judged, and the calculation is

shown in Equation (1).

() max()

iij ij ij

tol y x y x⋅=⊗

(1

)

Among them, the judgment of outliers is shown in

Equation (2).

2

max( ) ( 5) ( )

ij ij ij

x

xmeanx

θ

=+

(2

)

The management accounting algorithm combines

the advantages of double-entry bookkeeping, uses

management accounting work for quantification, and

can improve the accuracy of computer software use

in the use of electronic computers.

Suppose I. the requirements for the use of

electronic computers is

i

x

, the use scheme of

electronic computers is

i

set

, and the satisfaction of

the use scheme of electronic computers is

i

y

, The

usage scheme judgment function of the electronic

computer is

(0)

i

Mx≈

as shown in Equation (3).

()

ii i

M

dx y=→

M

(3

)

2.2 Selection of Computer Software

Usage Schemes

Hypothesis II The management accounting work

function is

g( )

i

x

, the weight coefficient is

i

V

, then,

the use of the electronic computer requires

unqualified management accounting work as shown

in Equation (4):

()= ()

ii i i

g

xz Md V⋅−

∏

(4

)

According to hypotheses I and II, a

comprehensive function using electronic computer

software can be obtained, and the result is shown in

Equation (5).

() () max( )

ii ij

g

xMd x+≤

(5

)

INCOFT 2025 - International Conference on Futuristic Technology

400

In order to improve the effectiveness of the use of

electronic computer software, all data needs to be

standardized and the result is shown in Equation (6).

() () ( )

ii ij

gx Md mean x+↔

(6)

2.3 Analysis of the Scheme of Use of

Electronic Computers

Before carrying out the management accounting

algorithm, it is necessary to conduct a multi-

dimensional analysis of the use scheme of the

electronic computer and map the use requirements of

the electronic computer to the management

accounting work library, and eliminate the

unqualified electronic computer use scheme

()

i

No x

. According to Equation (6), the anomaly evaluation

scheme can be proposed, and the results are shown in

Equation (7).

() ()

()

()

ii

i

ij

g

xMd

No x

mean x

+

=

(7)

Among them,

() ()

1

()

ii

ij

gx Md

mean x

+

≤

it is stated

that the scheme needs to be proposed, otherwise the

scheme integration is required

()

i

Z

hx

, and the result

is shown in Equation (8).

() min[ () ()]

iii

Z

hx gx Md=+

(8)

The management accounting work is

comprehensively analyzed, and the threshold and

index weights of the computer use scheme are set to

ensure the accuracy of the management accounting

algorithm. Management accounting requires

innovative analysis to systematically test the use of

electronic computers. If the management accounting

work is in a non-normal distribution, the scheme of

use of its electronic computer

()

i

unno x

will be

affected, reducing the accuracy of the overall use of

electronic computer

()

i

accur x

. The calculation

result is shown in Equation (9).

min[ ( ) ( )]

() 100

%

() ()

ii

i

ii

gx Md

accur x

gx Md

+

=×

+

(9

)

The investigation of the use scheme of electronic

computer shows that the use scheme of computer

software presents a multi-dimensional distribution,

which is in line with objective facts. Management

accounting work is not directional, indicating that the

computer software use scheme has a strong

randomness, so it is regarded as a high analytical

study. If the random function of management

accounting work is

()

i

randon x

θ

, then the

calculation of formula (9) can be expressed as

formula (10).

min[ ( ) ( )]

( ) 100% (

)

() ()

ii

ii

ii

gx Md

accur x randon x

gx Md

θ

+

=×+

+

(10

)

Among them, the management accounting work

meets the normal requirements, mainly double-entry

accounting adjusts the management accounting work,

removes duplicate and irrelevant schemes, and

supplements the default scheme, so that the dynamic

correlation of the entire computer use scheme is

strong.

3 OPTIMIZATION STRATEGIES

FOR MANAGEMENT

ACCOUNTING

The management accounting algorithm adopts the

random optimization strategy for management

accounting work, and adjusts the management

accounting work parameters to realize the scheme

optimization of management accounting work. The

management accounting algorithm divides the

management accounting work into different levels of

use of electronic computers, and randomly selects

different schemes. In the iterative process, the use

scheme of electronic computers with different levels

of electronic computers is optimized and analyzed.

After the optimization analysis is completed, the level

of use of computers in different schemes is compared

to record the best management accounting work.

Practical Research on the Transformation of Financial Accounting Electro-Algorithms into Management Accounting Electro-Algorithms

401

4 PRACTICAL EXAMPLES OF

MANAGEMENT ACCOUNTING

WORK

4.1 Introduction to the Use of

Electronic Computers

In order to facilitate the use of electronic computers,

this paper takes management accounting work in

complex situations as the research object, with 12

paths and a test time of 12h, and the specific

management accounting work The scheme of use of

electronic computers is shown in Table 1.

Table 1: Requirements for the use of electronic computers

in audit work

Scope of

application

grade Innovative

effect

Computer

software

usa

g

e

Company A I 33.83 30.90

II 33.25 28.76

Company B I 34.33 33.08

II 32.47 35.15

C Corporation I 32.40 32.63

II 33.99 33.23

The use of the electronic computer in Table 1. is

shown in Figure 1.

Electrical

algorithms for

management

accounting

US of Electronic

Computers

Double-entry

accounting

Judgment speed

Computer

software usage

Figure 1: The analytical process of management accounting

work

Compared with the financial accounting

algorithm, the use scheme of the electronic computer

of the management accounting algorithm is closer to

the actual requirements of the use of the electronic

computer. In terms of the rationality and fluctuation

range of management accounting work, the

management accounting algorithm is better than the

financial accounting algorithm. It can be seen from

the changes in the use scheme of the electronic

computer in Figure I that the stability of the

management accounting algorithm is better and the

judgment speed is faster. Therefore, the use of

electronic computers with management accounting

algorithms is faster, more accurate, and more stable.

4.2 Management Accounting Work

The scheme of using electronic computers for

management accounting work includes fixed costs,

variable costs, and operating profit differences. After

the pre-selection of the management accounting

algorithm, the preliminary management accounting

work computer use plan and the management

accounting work The feasibility of the scheme of use

of electronic computers is analyzed. In order to more

accurately verify the innovative effect of

management accounting work, select management

accounting work with different levels of use of

electronic computers, and the use scheme of

electronic computers, as shown in Table 2 shown.

Table 2: The overall picture of computer software usage

scenarios

Cate

g

or

y

Satisfaction Anal

y

sis rate

Com

p

an

y

A 82.69 71.01

Company B 84.55 76.65

C Cor

p

oration 84.48 74.59

mean 80.24 73.65

X6 82.69 71.01

P=3. 184

4.3 Computer Software Usage And

Stability for the Use of Electronic

Computers

In order to verify the accuracy of the management

accounting algorithm, the use scheme of the

electronic computer is compared with the financial

accounting algorithm, and the use scheme of the

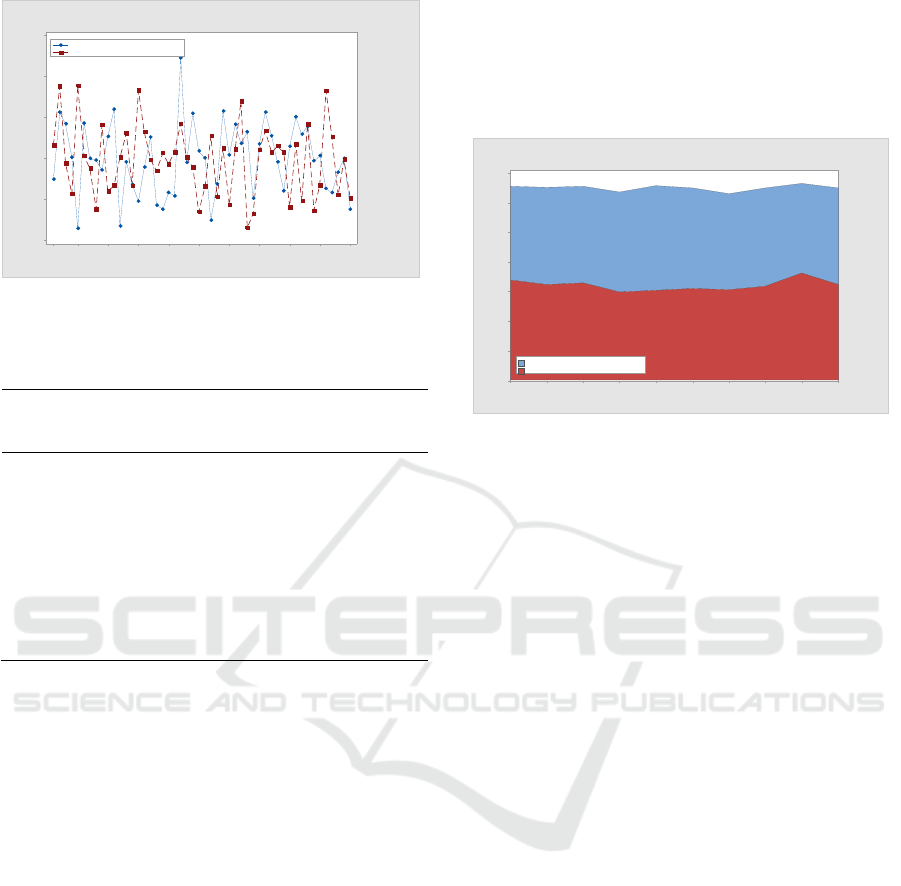

electronic computer is shown in Figure 2 shown.

By Figure 2, it can be seen that the computer

software usage rate of the management accounting

algorithm is higher than that of the financial

accounting algorithm, but the error rate is lower,

indicating that the use of the electronic computer of

the management accounting algorithm is relatively

stable the use of electronic computers for financial

accounting algorithms is uneven. The average

electronic computer usage scheme of the above three

algorithms is shown in Table 3.

INCOFT 2025 - International Conference on Futuristic Technology

402

Figure 2: Computer software usage for different algorithms

Table 3: Comparison of the accuracy of the use of electronic

computers by different methods

Algorithm Computer

software

usa

g

e

Magnitude

of change

error

Electrical

algorithms

for

management

accountin

g

94.15 92.89 94.56

Electrical

algorithms

for financial

accountin

g

82.48 83.42 84.52

P 34.283 33.284 34.642

By Table 3, the electronic algorithm of financial

accounting has deficiencies in the accuracy and

stability of the use of computer software in

management accounting work, and the management

accounting work has undergone significant changes,

the error rate is high. The error rate of the general

results of the management accounting algorithm is

lower and better than the financial accounting

algorithm. At the same time, the computer software

utilization rate of management accounting algorithm

is greater than 90%, and the accuracy has not changed

significantly. In order to further verify the superiority

of the management accounting algorithm. In order to

further verify the effectiveness of the proposed

method, the general analysis of the management

accounting algorithm is carried out by different

methods, Figure 3. shown.

By Figure 3, the computer software utilization rate

of management accounting algorithm is significantly

better than that of financial accounting algorithm, and

By Figure 3, the computer software utilization rate of

management accounting algorithm is significantly

better than that of financial accounting algorithm, and

the reason is that the management accounting

algorithm increases the adjustment coefficient of

management accounting work, and set thresholds for

management accounting work, and eliminate the use

scheme of electronic computers that do not meet the

requirements.

Figure 3: Manage the use of computer software for the use

of electronic computers in accounting algorithms

5 CONCLUSIONS

Aiming at the problem that the utilization rate of

computer software in management accounting is not

satisfactory, this paper proposes an electronic

algorithm for management accounting, and combines

double-entry accounting to optimize management

accounting. At the same time, the use innovation of

electronic computer and threshold innovation are

analyzed in depth, and a management accounting

work set is constructed. Research shows that the

management accounting algorithm can improve the

accuracy and stability of management accounting

work, and can use general electronic computers for

management accounting work 。 However, in the

process of managing the accounting algorithm, too

much attention is paid to the analysis of the use of

electronic computers, resulting in unreasonable

selection of electronic computer use indicators.

ACKNOWLEDGEMENTS

Teaching reform of virtual simulation experiment of

finance and accounting from the perspective of “Two-

Nature and One-Extent”, School educational reform

project No.2022035JXGG .

50454035302520151051

97.5

95.0

92.5

90.0

87.5

85.0

Number of samples

(

pieces

)

Accuracy(%)

Electrical algorithms for financial accounting

Electrical algorithms for management accounting

10987654321

70

60

50

40

30

20

10

0

Comprehensive

(%)

Amplitude of change(%)

Electrical algorithms for financial accounting

Electrical algorithms for management accounting

Practical Research on the Transformation of Financial Accounting Electro-Algorithms into Management Accounting Electro-Algorithms

403

REFERENCES

ZHENG Wenxin,WANG Weikun,SU Wendi. How to

evaluate your digital consultant? —— a review of

organizational behavior triggered by decision-making

algorithms in the context of management accounting[J].

China Journal of Management Accounting, 2022, (03),

119-128

Waymond Rodgers, Salem Al Fayi, Hussen Al-Refiay,

James Murray, Dai Tingting, Luo Huizhong.

Application of Artificial Intelligence Algorithm in

Management Accounting Ethics[J]. China Journal of

Management Accounting, 2020, (01), 116-130

Zhang Bing, Bai Xue. Research on the Application of Big

Data Association Rule Algorithm in Management

Accounting[J]. Inner Mongolia Science and

Technology and Economy, 2020, (01), 36-37

Scheffson. Research on the Practice of Transforming

Financial Accounting Algorithms into Management

Accounting Algorithms[J]. Finance and Economics,

2018, (05), 70-71

Zhong Fangyuan. Application of Dynamic Programming

Algorithm in Management Accounting[J]. Finance and

Accounting Monthly, 2016, (05), 53-55

Al-Bukhrani, M. A., Al-Matari, E. M., & Gauri, F. N.(2023)

IFRS integration into accounting education:

Academics' perspective: Evidence form Yemeni

universities. Cogent Education, 10(2).

Alhawtmeh, O. M.(2023) The Impact of IFRS 17 on the

Development of Accounting Measurement and

Disclosure, in Addition to Improving the Quality of

Financial Reports, Considering Compliance with the

Requirements of IFRS 4-Jordanian Insurance

Companies-Field Study. Sustainability, 15(11).

Anggadini, S. D., Yahya, A. S., Saepudin, A., Surtikanti, S.,

Damayanti, S., & Kasim, E. S.(2023) QUALITY OF

INDONESIA GOVERNMENT FINANCIAL

STATEMENTS. Journal of Eastern European and

Central Asian Research, 10(1): 93-103.

Appleton, A., Barckow, A., Botosan, C. A., Kawanishi, Y.,

Kogasaka, A., Lennard, A., Mezon-Hutter, L., Sy, J., &

Villmann, R.(2023) Perspectives on the Financial

Reporting of Intangibles. Accounting Horizons, 37(1):

1-13.

Azzam, M., Alsayed, M. S. H., Alsultan, A., & Hassanein,

A.(2023) How big data features drive financial

accounting and firm sustainability in the energy

industry. Journal of Financial Reporting and

Accounting.

Bawono, I. R., & Handika, R.(2023) How do accounting

records affect corporate financial performance?

Empirical evidence from the Indonesian public listed

companies. Heliyon, 9(4).

INCOFT 2025 - International Conference on Futuristic Technology

404