Portfolio Algorithm Based on Accounting Information System

Relevance

SuJuan Zhou

Yunnan College of Business Management, KunMing, 650000, China

Keywords: Combinatorial Algorithm, Investment Decisions, Accounting Information Management, Single Investment,

Invest More, Comprehensive Investment, Combination Rate, Relevance, Decision Accuracy.

Abstract: Accounting information management plays a crucial role in investment decision-making, but there is a

problem of inaccurate evaluation. The proportional estimation method cannot solve the accounting

information management problem in investment decision-making, and the decision-making plan is

unreasonable. Therefore, this article proposes a combination algorithm for investment risk accounting

information management analysis. Firstly, a combination of indicators is used to make decisions on

comprehensive investments, and indicators are divided according to accounting information management

requirements to reduce interference factors in accounting information management. Then, comprehensive

indicators are used to analyze investment risk accounting information, form an accounting information

management plan, and comprehensively analyze the results of accounting information management. The

accuracy of investment decision shows that under the condition that the decision analysis indicators are fixed,

the accuracy of the combination algorithm for accounting information management analysis of various

investment risks and the analysis time of accounting information management are better than the proportional

estimation method.

1 INTRODUCTION

The portfolio ratio is one of the important contents of

investment decision-making (Alsubaei, 2023), which

is of great significance for the accuracy of decision-

making (Bratfisch, Riar, et al. 2023). However, in the

process of accounting information management, there

is a problem of poor accuracy in accounting

information management plans (Cola, Mazza, et al.

2023), which affects the return on various

investments. Some scholars believe that applying

portfolio algorithm to investment decision analysis

can effectively analyze accounting information

management schemes and provide corresponding

support for accounting information management

(Dalloul, Ibrahim, et al. 2023). On this basis, this

article proposes a combination algorithm to optimize

accounting information management schemes and

verify the effectiveness of the algorithm (De, Ferreira,

et al. 2023).

1.1 Portfolio Algorithm for Accounting

Information Systems

The portfolio algorithm of the Accounting

Information System (AIS) is a mathematical method

that helps investors choose and balance their

portfolios. It helps people minimize risk and ensure

maximum returns by diversifying their portfolios

(Ferreira, Slavov, et al. 2023). In the portfolio

algorithm, there are three main components: asset

allocation, asset allocation, and asset restructuring

(Fredo, Motta, et al. 2023).

1.1.1 Asset Allocation

Asset allocation refers to the allocation of assets in a

portfolio to different asset classes to maximize returns

and minimize risk (Gyamera, Atuilik, et al. 2023).

Generally, asset classes include cash, bonds, stocks,

and real estate, among others. When allocating assets,

factors such as liquidity, risk, and return of assets

need to be considered (Hnatchuk, Hovorushchenko,

et al. 2023).

Zhou, S.

Portfolio Algorithm Based on Accounting Information System Relevance.

DOI: 10.5220/0013544100004664

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 3rd International Conference on Futuristic Technology (INCOFT 2025) - Volume 1, pages 391-397

ISBN: 978-989-758-763-4

Proceedings Copyright © 2025 by SCITEPRESS – Science and Technology Publications, Lda.

391

1.1.2 Asset Allocation

Asset allocation refers to the spread of assets in a

portfolio across different securities to diversify risk

and ensure maximum returns. Generally, security

options include stocks, bonds, and derivatives, among

others. In the process of asset allocation, investors

need to consider factors such as the risk level, return

expectations, liquidity and correlation of each

security (Hoelscher, and Shonhiwa, 2023).

1.1.3 Asset Restructuring

Asset restructuring refers to the re-evaluation of asset

allocation and asset allocation strategies over a period

of time to ensure that a portfolio always has the best

level of return and risk. Investors need to adjust their

asset allocation and asset allocation strategies at any

time to adapt to market changes and their own

investment goals (Jarah, Zaqeeba, et al. 2023).

1.2 Analysis of the Advantages and

Disadvantages of Portfolio

Algorithms

1.2.1 Advantages

(1) Risk reduction – Portfolio algorithms can

guarantee investment returns by diversifying assets

across different securities to minimize portfolio risk

(Kao, Yuan, et al. 2023).

(2) Optimize returns – Portfolio algorithms can

optimize portfolio returns by selecting high-yield,

low-risk securities.

(3) Adapt to market changes – The portfolio

algorithm can adjust asset allocation and asset

allocation strategies at any time when the market

changes to adapt to market changes.

(4) Improve investment efficiency – Portfolio

algorithms can help investors use funds more

efficiently and improve investment efficiency

(Lamberton, Raschke, et al. 2023).

1.2.2 Disadvantages

(1) Rely on historical data – Portfolio algorithms

need to rely on historical data to predict future market

movements, which may lead to inaccurate algorithm

predictions (Loureiro, Milligan, et al. 2023).

(2) High algorithm complexity – The

implementation of the portfolio algorithm requires

the use of complex mathematical models and

algorithms, which may lead to investment failure if

not implemented correctly (Lukas, 2023).

(3) Human interference – Portfolio algorithms

need to artificially formulate asset allocation and

asset allocation strategies, and if investors' decisions

are irrational, it may affect the effectiveness of the

algorithm (Minbaleev, Berestnev, 2023).

(4) High capital threshold – Portfolio algorithms

require a large investment of capital in order to

achieve the best investment results, which may make

it difficult for small-scale investors to use the

algorithm (Mokhnacheva, 2023).

Portfolio algorithm is an effective investment

strategy that can reduce the risk of a portfolio to a

certain extent, improve investment returns and

efficiency (Poppe, Vrolijk, 2023). However, despite

the many advantages of portfolio algorithms, there

are still some limitations and disadvantages.

Therefore, investors should fully understand the

characteristics and limitations of the portfolio

algorithm, and use the algorithm appropriately when

formulating investment strategies, pay attention to the

uncertainty of the algorithm's predictions, and adopt

appropriate risk management strategies to ensure the

success of the portfolio (Qadri, Altass, 2023).

1.3 Optimization Indicators of

Accounting Information Systems

In order to assess the operation of accounting

information systems, it is necessary to consider the

indicators of the system in a comprehensive manner.

The following is an analysis of the relevant indicators

of the accounting information system (Qatawneh,

2023).

1.3.1 Efficiency Indicators

Data processing speed is one of the main indicators to

measure the efficiency of accounting information

systems. An efficient system should be able to

process large amounts of data quickly in a short

period of time to ensure fast response and response

time. Therefore, enterprises should continuously

optimize hardware equipment and software systems

to improve data processing speed.

Application response time is also an important

indicator of the efficiency of accounting information

systems. An efficient system should respond to a

user's request within 6 seconds, and this data is often

used as a reference value that can help enterprises

evaluate the responsiveness of the system. Fast

response times can improve user satisfaction and

bring higher revenue to the business.

INCOFT 2025 - International Conference on Futuristic Technology

392

1.3.2 Task Completion Time

Task completion time is another important indicator

to measure the efficiency of accounting information

systems. An efficient system should be able to

complete data processing tasks in a short time and

provide timely results to users. Therefore, enterprises

should monitor the efficiency of system operation by

setting a reasonable task completion time, and

continuously optimize the system to improve

efficiency.

1.3.3 Security Metrics

Data confidentiality is one of the important indicators

to measure the security of accounting information

systems. A highly secure system should be able to

keep your organization's data safe from unauthorized

access and theft. Therefore, enterprises should take

appropriate measures, such as access control,

encryption technology, data backup, etc., to ensure

the confidentiality of data.

1.3.4 System Reliability

System reliability is another measure of the security

of accounting information systems. A highly reliable

system should guarantee system stability and prevent

system failure and data loss. Therefore, enterprises

should take appropriate measures, such as backup

systems, integrity verification, disaster recovery

plans, etc., to ensure the reliability of the system.

1.3.5 Quality Indicators

Data accuracy is one of the main indicators to

measure the quality of accounting information

systems. Data accuracy is directly related to the

correctness of business decisions, therefore,

enterprises should take appropriate measures, such as

data validation, data cleaning, etc., to ensure the

accuracy of data. Data integrity is also one of the

indicators to measure the quality of accounting

information systems. Enterprises should ensure the

integrity of data to guarantee the correctness and

integrity of data. Data integrity can be achieved by

employing measures such as data validation and data

backup.

1.3.6 User Satisfaction Metrics

User satisfaction is a key indicator to measure the

satisfaction of accounting information systems.

Through user surveys and feedback, enterprises can

understand the user's satisfaction with the system to

understand the advantages and disadvantages of the

system and further improve the system.

The user learning curve is also one of the

indicators to measure the satisfaction of accounting

information systems. Enterprises should provide

system interfaces and functions that are easy to learn

and use to help users quickly master the system and

improve work efficiency.

1.3.7 Cost Indicators

The overall development cost is one of the main

indicators to measure the cost of accounting

information systems. Companies should make a

reasonable budget before system development and

control system development costs to maximize

benefits.

Maintenance and operating costs are another

measure of the cost of accounting information

systems. Enterprises should control the operation and

maintenance costs of the system to ensure that the

system can operate stably for a long time and

minimize costs.

The above indicators can help enterprises

understand the operating status of the system and

continuously optimize the system to improve

efficiency and reduce costs. Enterprises should

choose and value these indicators according to their

actual situation to help enterprises make better

strategic decisions.

2 RELATED CONCEPTS

2.1 Mathematical Description of

Combinatorial Algorithms

The combination algorithm utilizes correlation to

optimize accounting information management plans,

and based on various indicators in accounting

information management, discovers unqualified

values in investment decisions, integrates accounting

information management plans, and ultimately

determines the feasibility of investment decisions.

The combination algorithm combines the advantages

of correlation to quantify investment decisions, which

can improve the direction of accounting information

management investment decisions.

Assumption I. Accounting Information

Management Requirements is

c

i

,The accounting

information management plan is

lim

,The

combination rate of accounting information

management solutions is

w

,The judgment function

Portfolio Algorithm Based on Accounting Information System Relevance

393

of accounting information management plan is

U(g > 0)

,As shown in formula (1)。

21

1

1

lim (c w) cos

n

n

ii

x

i

i

FV g

θ

−

→∞

=

=

=−

(1

)

2.2 Selection of Investment Decision

Direction Plans

Assumption II The investment decision function is

()

i

g

x

,The weight coefficient is

l

,So, there are

unqualified investment decisions in accounting

information management, as shown in formula (2):

2

1

11

1

() ,,

n

nn

iniii

ii

i

gl g g glXl

==

=

−≈

(2

)

2.3 Analysis of Accounting Information

Management Plan

Before conducting a combination algorithm, it is

necessary to conduct a multidimensional analysis of

the accounting information management plan and

map the accounting information management

requirements to the investment decision database,

eliminating unqualified accounting information

management plans. Conduct a comprehensive

analysis of investment decisions and set thresholds

and indicator weights for accounting information

management plans to ensure the accuracy of the

combination algorithm. The investment decision is a

system testing accounting information management

plan that requires correlation analysis. If the

investment decision is in a non normal distribution,

its accounting information management plan will be

affected, reducing the accuracy of the overall

accounting information management. In order to

improve the accuracy of the combination algorithm

and improve the level of accounting information

management, it is necessary to select accounting

information management schemes, and the specific

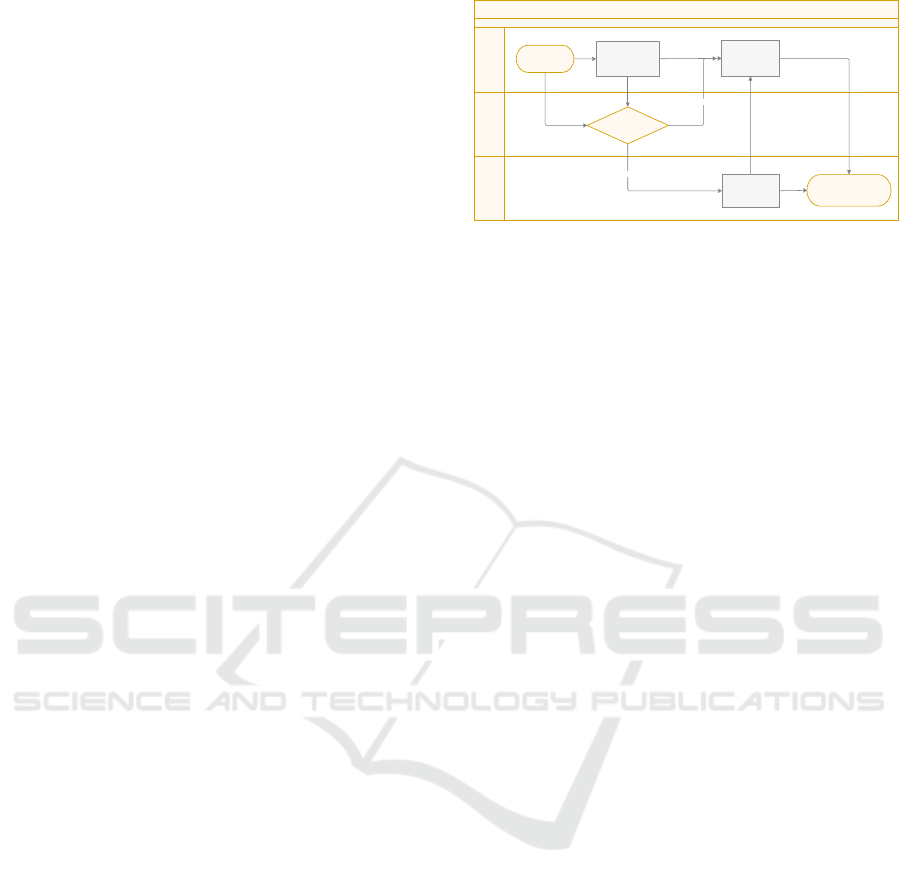

scheme selection is shown in Figure 1.

conclusion2 conclusion1conclusion3

Accounting

information

portfolio ratio

investment type

correlation

Scheme

calculation

是

decision-making

accuracy

否

Figure 1: Selection Results of Investment Decision

Direction Schemes

The investigation of the accounting information

management plan shows that the investment decision-

making direction plan presents a multidimensional

graph distribution, which is in line with objective

facts. Investment decisions have no directionality,

indicating that the investment decision direction

scheme has strong randomness, so it is considered as

a higher level of analytical research. Investment

decisions comply with normal requirements, mainly

by adjusting investment decisions based on

correlation, removing duplicate and irrelevant plans,

and supplementing default plans, making the dynamic

correlation of the entire accounting information

management plan strong.

3 OPTIMIZATION STRATEGIES

FOR INVESTMENT DECISIONS

The combination algorithm adopts a combination

correlation optimization strategy for investment

decisions and adjusts comprehensive investment

parameters to achieve optimization of investment

decisions. The combination algorithm divides

investment decisions into different levels of

accounting information management and randomly

selects different plans. During the iteration process,

optimize and analyze accounting information

management plans at different levels of accounting

information management. After the optimization

analysis is completed, compare the accounting

information management levels of different schemes

and record the best investment decisions.

INCOFT 2025 - International Conference on Futuristic Technology

394

4 PRACTICAL CASES OF

INVESTMENT DECISIONS

4.1 Introduction to Accounting

Information Management

In order to facilitate accounting information

management, this article focuses on investment

decisions in complex situations, with 3 categories and

a testing period of 1 year. The specific accounting

information management plan for investment

decisions is shown in Table 1.

Table 1: Requirements for Accounting Information

Management in Universities

Category Level Portfolio

Ratio

Correlation

Single Investment I 63.65% 93.07%

II 54.28% 84.65%

Multiple

Investments

I 63.23% 94.47%

II 59.87% 85.16%

Comprehensive

Investments

I 65.61% 94.67%

II 53.82% 82.79%

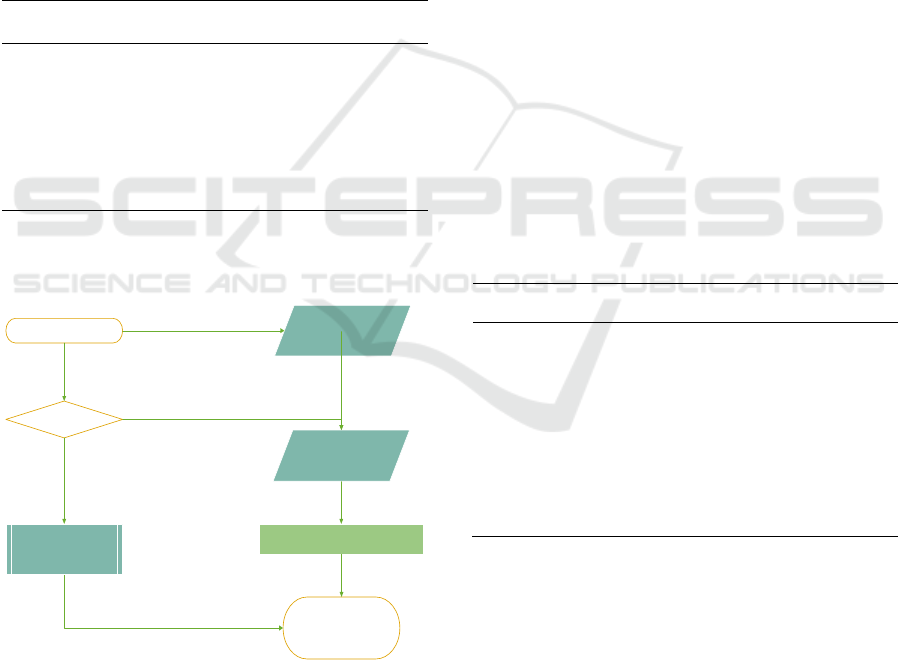

The accounting information management process

in Table 1. is shown in Figure 2.

optimization

Genetic algorithm

Overall

scheduling

Scheduling accuracy

Process simplification

rate

Local scheduling;

Dosiyoution

Figure 2: Analysis Process of Investment Decision

Compared with the proportional estimation

method, the accounting information management

scheme of the combination algorithm is closer to the

actual accounting information management

requirements. In terms of rationality and volatility of

investment decisions, combination algorithms and

proportional estimation methods are used. From the

changes in the accounting information management

scheme in Figure 2, it can be seen that the

combination algorithm has higher decision-making

accuracy. Therefore, the combination rate of

accounting information management solutions based

on the combination algorithm is more optimized and

the correlation is more reasonable.

4.2 Investment Decision-Making

Situation

The accounting information management plan for

investment decisions includes unstructured

information, semi structured information, and

structured information. After preselection of the

combination algorithm (Rosmawati, Apandi 2023), a

preliminary accounting information management

plan for investment decisions was obtained, and the

feasibility of the accounting information management

plan for investment decisions was analyzed. In order

to more accurately verify the innovation effect of

investment decisions, investment decisions with

different levels of accounting information

management were selected, and the accounting

information management plan is shown in Table 2.

Table 2: Overall Situation of Investment Decision Direction

Plan

Category Risk Rate Return Rate

Single Investment 74.75% 76.05%

Multiple Investments 73.62% 75.86%

Comprehensive

Investments

73.54% 76.49%

Mean 76.17% 74.74%

X 74.20% 75.78%

P=75.01%

4.3 Investment Decision Direction and

Stability of Accounting Information

Management

To verify the accuracy of the combination algorithm,

the accounting information management scheme was

compared with the proportional estimation method, as

shown in Figure 3.

Portfolio Algorithm Based on Accounting Information System Relevance

395

Figure 3: Investment Decision Directions for Different

Algorithms

As shown in Figure 3, the investment decision-

making direction of the combination algorithm is

higher than that of the proportional estimation

method, but the error rate is lower, indicating that the

accounting information management of the

combination algorithm is relatively stable, while the

accounting information management of the

proportional estimation method is uneven. The

average accounting information management scheme

for the above three algorithms is shown in Table 3.

Table 3: Comparison of Accounting Information

Management Accuracy by Different Methods

Method Combinatio

n

Correlatio

n

Decisio

n

Combinatoria

l

97.31% 97.73% 95.98%

Proportion

Ales

98.11% 98.08% 95.49%

P 97.93% 97.52% 95.55%

It can be seen from Table 3. that in terms of

investment decision-making, the proportional

estimation method has shortcomings in investment

decision-making direction and combinatorial

optimization, and investment decision-making has

undergone significant changes with a high error rate.

The general result of the combination algorithm has a

higher accuracy rate in investment decision-making

direction, which is superior to the proportional

estimation method. At the same time, the accuracy of

the investment decision direction of the combination

algorithm is greater than 90%, and there has been no

significant change in accuracy. To further verify the

superiority of the combination algorithm. To further

validate the effectiveness of the proposed method in

this article, different methods were used for general

analysis of the combined algorithm, as shown in

Figure 4.

Figure 4: Investment Decision Direction of Combination

Algorithm Accounting Information Management

From Figure 4., it can be seen that the investment

decision direction of the combination algorithm is

significantly superior to the proportional estimation

method. The reason for this is that the combination

algorithm increases the investment decision

adjustment coefficient and sets a threshold for

comprehensive investment, eliminating accounting

information management schemes that do not meet

the requirements.

5 CONCLUSIONS

In response to the problem of unsatisfactory

investment decision-making direction, this article

proposes a combination algorithm and optimizes

investment decisions by combining the correlation of

combination rates. At the same time, conduct in-depth

analysis on innovation in accounting information

management and threshold innovation, and construct

a comprehensive investment portfolio. Research has

shown that combination algorithms can improve the

accuracy and stability of investment decisions and

can be used for general accounting information

management of investment decisions. However, in

the process of combining algorithms, excessive

emphasis is placed on the analysis of accounting

information management, resulting in unreasonable

selection of accounting information management

indicators.

REFERENCES

Alsubaei, F. S.(2023) Detection of Inappropriate Tweets

Linked to Fake Accounts on Twitter. Applied Sciences-

Basel, 13(5):3.

Bratfisch, C., Riar, F. J., & Bican, P. M.(2023) When

entrepreneurship meets finance and accounting: (non-

)financial information exchange between venture

INCOFT 2025 - International Conference on Futuristic Technology

396

capital investors, business angels, incubators,

accelerators, and start-ups. International Journal of

Entrepreneurial Venturing, 15(1): 63-90.

Cola, G., Mazza, M., & Tesconi, M.(2023) Twitter

Newcomers: Uncovering the Behavior and Fate of New

Accounts Through Early Detection and Monitoring.

Ieee Access, 11(3): 55223-55232.

Dalloul, M. H. M., Ibrahim, Z. B., & Urus, S. T.(2023)

Financial Crises Management in Light of Accounting

Information Systems Success: Investigating Direct and

Indirect Influences. Sustainability, 15(10):89.

De Aguiar, R. F., Ferreira, P. L., & Gomes, M. Z.(2023)

Competencies in technology and information system

demanded in accounting sciences: the national student

performance exam (ENADE). Revista Ambiente

Contabil, 15(1): 47-66.

Ferreira, T. J., Slavov, T. N. B., Parisi, C., & Russo, P.

T.(2023) Case study of accounting automation from the

perspective of institutional theory. Revista De Gestao E

Secretariado-Gesec, 14(3): 3469-3491.

Fredo, A. R., Motta, M. E. V. d., Camargo, M. E., &

Priesnitz, M. C.(2023) Digital transformation: the

digitization of accounting. Revista De Gestao E

Secretariado-Gesec, 14(1): 681-714.

Gyamera, E., Atuilik, W. A., Eklemet, I., Matey, A. H.,

Tetteh, L. A., & Apreku-Djan, P. K.(2023) An analysis

of the effects of management accounting services on the

financial performance of SME: The moderating role of

information technology. Cogent Business &

Management, 10(1):89.

Hnatchuk, Y., Hovorushchenko, T., Shteinbrekher, D.,

Boyarchuk, A., & Kysil, T.(2023) MEDICAL

INFORMATION TECHNOLOGY FOR DECISION-

MAKING TAKING INTO ACCOUNT THE NORMS

OF CIVIL LAW. International Journal on Information

Technologies and Security, 15(1): 77-88.

Hoelscher, J., & Shonhiwa, T.(2023) J&S Publisher

Problems: A Diagnostic Analytics Case Exploring

Employee Expense Reimbursement. Journal of

Emerging Technologies in Accounting, 20(1): 213-221.

Jarah, B. A. F., Zaqeeba, N., Al-Jarrah, M. F. M., Al

Badarin, A. M., & Almatarneh, Z.(2023) The Mediating

Effect of the Internal Control System on the

Relationship between the Accounting Information

System and Employee Performance in Jordan Islamic

Banks. Economies, 11(3):90.

Kao, M. C., Yuan, Y. H., & Wang, Y.-X.(2023) The study

on designed gamified mobile learning model to assess

students? learning outcome of accounting education.

Heliyon, 9(2):89.

Lamberton, B. A., & Raschke, R. L.(2023) Using Backward

Design to Incorporate Technology into a Non-AIS

Course. Journal of Emerging Technologies in

Accounting, 20(1): 259-267.

Loureiro, T. G., Milligan, B., Gacutan, J., Adewumi, I. J.,

& Findlay, K.(2023) Ocean accounts as an approach to

foster, monitor, and report progress towards sustainable

development in a changing ocean-The Systems and

Flows Model. Marine Policy, 154(2):89.

Lukas, C.(2023) On interim performance evaluations and

interdependent period outcomes. Journal of

Management Control, 34(1): 67-108.

Minbaleev, A. V., Berestnev, M. A., & Evsikov, K.

S.(2023) ENSURING INFORMATION SECURITY

OF MINING EQUIPMENT IN THE QUANTUM

ERA. Proceedings of the Tula States University-

Sciences of Earth, 1(3): 567-584.

Mokhnacheva, Y. V.(2023) Document Types Indexed in

WoS and Scopus: Similarities, Differences, and Their

Significance in the Analysis of Publication Activity.

Scientific and Technical Information Processing, 50(1):

40-46.

Poppe, K., Vrolijk, H., & Bosloper, I.(2023) Integration of

Farm Financial Accounting and Farm Management

Information Systems for Better Sustainability

Reporting. Electronics, 12(6):87.

Qadri, F. A., Altass, S., & Aman, Q.(2023) Examining the

perceptions of executives regarding accounting

information system (AIS). Evidence from listed

companies in Saudi stock exchange (TADAWUL).

Amazonia Investiga, 12(61): 184-192.

Qatawneh, A. M. M.(2023) The Role of Employee

Empowerment in Supporting Accounting Information

Systems Outcomes: A Mediated Model. Sustainability,

15(9):16.

Rosmawati, R. I. D. A., Apandi, N. n., Widarsono, A. G. U.

S., & Sugiharti, H. A. R. P. A.(2023) ACCOUNTING

INFORMATION SYSTEMS FOR INTERNAL

AUDITOR'S PERCEPTION: CASE STUDY AT

HIGHER EDUCATION INSTITUTION WITH

LEGAL STATUS. Journal of Engineering Science and

Technology, 18(2): 1309-1322.

Portfolio Algorithm Based on Accounting Information System Relevance

397