XGBoost Learning of Dynamic Wager Placement for In-Play Betting on

an Agent-Based Model of a Sports Betting Exchange

Chawin Terawong and Dave Cliff

a

Department of Computer Science, University of Bristol, Bristol BS8 1UB, U.K.

Keywords:

Agent-Based Models, Sports Betting Exchanges, In-Play Betting, Dynamic Wager Placement,

Machine Learning, XGBoost.

Abstract:

We present first results from the use of XGBoost, highly effective machine learning (ML) method, within the

Bristol Betting Exchange (BBE), an open-source agent-based model (ABM) designed to simulate a contem-

porary sports-betting exchange with in-play betting during track-racing events such as horse races. We use

the BBE ABM and its array of minimally-simple bettor-agents as a synthetic data generator which feeds into

our XGBoost ML system, with the intention that XGboost discovers profitable dynamic betting strategies by

learning from the more profitable bets made by the BBE bettor-agents. After this XGBoost training, which

results in one or more decision trees, a bettor-agent with a betting strategy determined by the XGBoost-learned

decision tree(s) is added to the BBE ABM and made to bet on a sequence of races under various conditions

and betting-market scenarios, with profitability serving as the primary metric of comparison and evaluation.

Our initial findings presented here show that XGBoost trained in this way can indeed learn profitable betting

strategies, and can generalise to learn strategies that outperform each of the set of strategies used for creation

of the training data. To foster further research and enhancements, the complete version of our extended BBE,

including the XGBoost integration, has been made freely available as an open-source release on GitHub.

1 INTRODUCTION

Like many other long-standing aspects of human cul-

ture, despite its five-thousand-year history, gambling

activity and opportunities were transformed by the

rise of the World-Wide-Web in the dot-com boom of

the late 1990s. One particular technology innovation

from that time subsequently proved to be a seismic

shift within the gambling industry: this was the ar-

rival of commercial web-based betting exchanges.

In much the same way that financial markets such

as stock exchanges offer platforms where potential

buyers and potential sellers of a stock can interact to

buy and sell shares, with buyers and sellers indicating

their intended prices in bid and ask orders, which are

then matched to compatible counterparties by the ex-

change’s internal mechanisms, so betting exchanges

are platforms where potential backers and potential

layers can interact and be matched by the exchange,

to find one or more people to take the other side of a

bet. In the terminology of betting markets, a backer

is someone who places a back bet, i.e. a bet which

a

https://orcid.org/0000-0003-3822-9364

will be paid if a specific event-outcome does occur;

and a layer is someone who places a lay bet, i.e. a

bet that’s paid if the specific event-outcome does not

occur. The revolutionary aspect of betting exchanges

is that they operate as platform businesses: the ex-

change does not take a position as either a layer or

a backer, it simply serves to match customers who

want to back at a particular odds with other customers

who want to lay at those same odds, and the exchange

makes its money by taking a small fee from each cus-

tomer’s winnings. In contrast, traditional bookmakers

(or “bookies”) are the counterparty to each customer’s

bet, and lose money if they miscalculate their odds.

The first notably commercially successful sports

betting exchange was created by British company

BetFair (see www.betfair.com), a start-up which

grew with explosive pace after its founding in 2000,

and by 2006 was valued at £1.5billion. In 2016 Bet-

fair merged with another gambling company, Paddy

Power, in a deal worth £5bn, and the Betfair-branded

component of the merged company (now known

as Flutter Entertainment PLC) remains the world’s

largest online betting exchange to this day; at the time

of writing this paper in late 2023, Flutter’s market

Terawong, C. and Cliff, D.

XGBoost Learning of Dynamic Wager Placement for In-Play Betting on an Agent-Based Model of a Sports Betting Exchange.

DOI: 10.5220/0012487500003636

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 16th International Conference on Agents and Artificial Intelligence (ICAART 2024) - Volume 1, pages 159-171

ISBN: 978-989-758-680-4; ISSN: 2184-433X

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

159

capitalization is £22.5billion. For further discussion

of BetFair, see e.g. (Davies et al., 2005; Houghton,

2006; Cameron, 2009).

Creating an online exchange for matching layer

and backer bettors was not the only innovation that

BetFair introduced. They also led in the develop-

ment of in-play betting, which allowed bettors to con-

tinue to place back and lay bets after a sports event

had started, and to continue betting as the event pro-

gressed, until some pre-specified cut-off time or sit-

uation occurred, or the event finished. This is in

contrast to conventional human-operated bookmak-

ers, who ceased to take any further bets once the event

of interest was underway: because Betfair’s betting

exchange system was entirely automated, it could pro-

cess large numbers of bets while an event is underway,

operating in real time with flows of information that

would overwhelm a human bookie.

Just as most stock-exchanges publish real-time

summary data of all the bids and asks currently seek-

ing a counterparty, often showing the quantity avail-

able to be bought or sold at each potential price for a

particular stock, so a betting exchange publishes real-

time summary data for any one event E showing all

the currently unmatched backs and lays, the odds (or

“price”) for each of them, and the amount of money

available to be wagered at each price – in the termi-

nology of betting exchanges, this collection of data is

the “market” for event E.

During in-play betting, the prices in the market

can shift rapidly, and while some types of events such

as tennis matches might last for hours, allowing for

hours of in-play betting to endure for a single match,

for other types of event such as horse-racing the event

may only last a few minutes. The exploratory work

that we describe in this paper is motivated by the hy-

pothesis that it may be possible to use machine learn-

ing (ML) methods to process the rapidly-changing

data on a betting-exchange market for short-duration

events such as horse races, and for the ML system to

thereby produce novel profitable betting strategies.

For the rest of this paper, without loss of gener-

ality, we’ll limit our descriptions to talking only of

betting on horse races because this is a very widely

known form of sport on which much money is wa-

gered, because the duration of most horse races is

only a few minutes, and also because it is reasonably

easy to create an appropriately realistic agent-based

model (ABM), a simulation of a horse race, where

each agent in the model represents a horse/rider com-

bination, and where during the race each agent has

a particular position on the track, is travelling at a

specific velocity, and may or may not be blocked or

otherwise influenced by other horses in the race. Ex-

actly such a simulation of a horse race was introduced

by Cliff (Cliff, 2021), as one component of the Bris-

tol Betting Exchange (BBE), an agent-based simula-

tor not only of horse races, but also of a betting ex-

change, and also of a population of bettor-agents who

each form their own private opinion of the outcome

of a race, and then place back or lay bets accordingly.

Various implementations of BBE have been reported

previously by (Cliff et al., 2021) and at ICAART2022

by (Guzelyte and Cliff, 2022), but to the best of our

knowledge ours is the first study to explore use of XG-

Boost (Chen and Guestrin, 2016) on in-play betting

data to develop profitable betting strategies.

The bettor-agents in the BBE ABM each form

their own private opinion on the outcome of a race

on the basis of their own internal logic, i.e. their own

individual betting strategy, and the original specifica-

tion of BBE in (Cliff, 2021) included a number of

minimally simple strategies, described in more detail

in Section 2.3 below, and the BBE ABM usually oper-

ates with a bettor population having a heterogeneous

mix of such betting strategies. As the dynamics of

a simulated race unfold, so the bettor-agents react to

changes in the competitors’s pace and relative posi-

tions by making and/or cancelling in-play bets, alter-

ing the market for that race. The BBE ABM records

every change in the market over the duration of a race,

along with the rank-order positions of the competitors

at the time of each market change (i.e., which com-

petitor is in first place, which is in second, and so on):

this we refer to as a race record.

In the work described here, we typically run 1000

race simulations, gathering a race record from each.

The set of race records then go through an automated

analysis process to identify the actions of the most

profitable bettors in each race. That is, for each race,

we look to see which bettors made the most profit

from in-play betting on that race, and we then work

backward in time to see what actions those bettors

took during the race, and what the state of the mar-

ket and the state of the race was at the time of each

such action. This then forms the training and/or test

data for XGBoost: for any one item of such data, the

input to XGBoost is the state of the market and the

state of the race, and the desired output is the action

that the bettor took.

To accomplish this, we modified the existing

source-code of the most recent version of BBE, which

is the multi-threaded BBE integrated with Opin-

ion Dynamics Platform used in Guzelyte’s research

(Guzelyte, 2021b; Guzelyte and Cliff, 2022), hosted

on Guzelyte’s GitHub (Guzelyte, 2021a), to incorpo-

rate the XGBoost betting agent. After the integra-

tion of XGBoost, we conduct experiments to train and

ICAART 2024 - 16th International Conference on Agents and Artificial Intelligence

160

evaluate the XGBoost bettor-agent’s performance in

different market scenarios.

A surprising result we present here is that although

XGBoost is trained on the profitable betting activity

of a population of minimally simple betting strategies,

the betting strategy that it then learns can outperform

even the best of those simple strategies. That is, XG-

Boost generalises over the training data sufficiently

well that the profitability of XGBoost-enabled bettor-

agents can eventually be better than those of the non-

learning bettors whose behaviors formed the training

data for XGBoost.

Our work described here is exploratory: we use

the BBE agent-based model (ABM) as a synthetic

data generator to create the training data needed for

XGBoost, and then we take the XGBoost-trained bet-

tor agent and test it in the BBE ABM. We are doing

this in an attempt to answer the research question of

whether the multidimensional time series of data from

the in-play betting market for horse races can in prin-

ciple be fed into a machine learning system such as

XGBoost and result in a learned profitable automated

betting system. What we develop here is a proof-of-

concept, and as we show in Section 4 our results thus

far do show some promise, but we strongly caution

against any readers of this paper actually gambling

with real money on the basis of the system we de-

scribe here: a lot of further development work and

much more extensive testing would be required before

we would ever want to deploy this system live-betting

with our own money.

Section 2 gives further background information,

and then our experiment design is described in Sec-

tion 3. Section 4 presents our results, followed by

discussion of future work in Section 5.

2 BACKGROUND

2.1 BBE Race Simulator

Guzelyte’s research (Guzelyte, 2021b; Guzelyte and

Cliff, 2022), relies heavily on Keen’s thesis (Keen,

2021) and Cliff’s original paper (Cliff, 2021) to create

the Bristol Betting Exchange (BBE) race-simulator.

BBE isn’t designed to perfectly mimic a real track

horse-race, but rather to generate convincing data re-

sembling real race dynamics: the changes in pace and

rank-order position that occur within real races.

In every race simulation, competitors are selected

from a pool and placed on a one-dimensional track

of a fixed length. Each competitor’s position on

the track at a given time is represented as a real-

valued distance. The race begins at t = 0 and con-

cludes when the last competitor crosses the finish

line. The progress of each competitor is calculated

using a discrete-time stochastic process which pro-

vides for modelling of individual differences in pace

(e.g., some might start the race at a fast pace but sub-

sequently slow down; others might instead hold back

in the early stages of the race and then speed up at

the end) and for inter-competitor interactions such as

a competitor being blocked and hence slowed by an-

other competitor immediately in front, or a competi-

tor being “hurried” by another competitor closing on

to its rear. Full details of the race simulator were first

published in (Cliff, 2021) to which the reader is re-

ferred for more information

2.2 BBE Betting Exchange

The Bristol Betting Exchange (BBE) uses a matching-

engine that tracks all of the bets that are placed. The

details of the bets of each bettor (time of bet, amount

of bet, etc) is recorded for every race. If a bet hasn’t

been matched with a counterparty, it can be cancelled,

but once it’s matched, it can’t be. When it comes to

matching bets, older bets are prioritized if the odds

are the same. To create the market for a race, for each

competitor BBE collects all back and lay bets at the

same odds, calculating the total money bet. After a

race finishes, the money from losing bets is gathered

and given to the winners. BBE earns by taking a small

commission from the winnings. BBE’s matching-

engine is designed to implement exactly the same pro-

cesses as are used in real-world betting exchanges, so

in this sense it can be argued that the BBE’s exchange

module is not just a simulation, but an actual instance

of a betting exchange.

2.3 BBE Betting Agents

BBE has a variety of bettor-agents each utilizing a

unique approach. These bettors’ strategies range from

the wholly irrational Zero Intelligence (ZI) strategy,

where choice of bets is made entirely at random; to

wholly rational, where the best available information

guides their decisions. The most rational strategy in

BBE at present is the Rational Predictor (RP), which

makes its race outcome predictions based on a series

of simulated “dry-runs” of the race: at the start of the

race, an RP bettor runs n independent and identically

distributed (IID) private (i.e., known only to that RP

bettor) simulations of the entire race from time t = 0

to whatever time the last horse crosses the finish-line,

using the same race simulator engine as is used to im-

plement the actual ‘public’ race that all BBE bettors

are betting on; then at various times t = t

i

during the

XGBoost Learning of Dynamic Wager Placement for In-Play Betting on an Agent-Based Model of a Sports Betting Exchange

161

race, the RP bettor will run another fresh set of n IID

simulations of the current race, running the simula-

tion forwards from the current positions of the horses

at time t

i

forward to the end of the race, and then may

then make a fresh in-play bet if the most frequent win-

ning horse in those n simulations is different from

whatever horse it had previously bet on. In (Cliff,

2021), the behavior of an RP agent was defined as

being determined primarily by the hyperparameter n,

how many IID simulations it runs each time it reeval-

uates the odds, and so these agents were denoted as

RP(n) bettors. Other authors who have worked with

BBE since the publication of (Cliff, 2021) have found

it useful to also be explicit about the time interval be-

tween an RP(n) bettor’s successive sets of n IID sim-

ulations: this can be captured by two additional hy-

perparameters, ∆

t:min

and ∆

t:max

, such that the wait (in

seconds) until the next set of n IID simulations is con-

ducted by an RP bettor is given by a fresh draw from

a uniform distribution between ∆

t:min

and ∆

t:max

] (de-

noted by U[∆

t:min

, ∆

t:max

]) as that bettor concludes its

current set of IID simulations. For this reason, an RP

bettor is fully denoted by RP(n, ∆

t:min

, ∆

t:max

).

The computational costs of simulating any one

RP(n, ∆

t:min

, ∆

t:max

) bettor agent over the duration of

an entire race manifestly rises sharply as n increases

and/or as the expected value E(U[∆

t:min

, ∆

t:max

])

falls. Authors such as (Keen, 2021; Guzelyte,

2021b) have concentrated on using the relatively low-

computational-cost instance of RP(1,10,15), which —

because this type of bettor is in receipt of privileged

information — has come to be referred to as the Priv-

ileged bettor strategy. In the work presented here, we

follow their convention and also use Privileged bettors

as our form of RP agent.

There are several other types of BBE bettor strate-

gies. The Linear Extrapolator (LinEx) employs a

strategy of estimating competitor speed and predict-

ing the outcome based on linear extrapolation. The

Leader Wins (LW) bettor operates on the assumption

that the leading competitor will maintain their posi-

tion and win the race. The Underdog strategy (UD)

supports the second-placed competitor as long as they

are within a certain threshold of the lead. The Back

The Favourite (BTF) bettor, on the other hand, aligns

their predictions with the market’s favourite.

The Representative Bettor (RB) is a unique agent

designed to mimic real-world human betting be-

haviours. It factors in betting preferences such as

an inclination towards certain stake amounts, often

seen in human bettors who prefer multiples of 2, 5, or

10. This bettor also exhibits the well-known favorite-

longshot bias, reflecting the tendencies of human bet-

tors to bet disproportionately on the favourite or the

longshot, regardless of the actual odds.

The presence of these various bettors, each with

different parameters, within BBE gives rise to an en-

gaging and complex dynamic in the in-play betting

market. For full details and implementation notes on

each of these bettor strategies, see (Cliff, 2021; Keen,

2021; Guzelyte and Cliff, 2022).

2.4 XGBoost Model Training

XGBoost, an abbreviation for eXtreme Gradient

Boosting, introduced by (Chen and Guestrin, 2016),

is an ML technique celebrated for its speed, precision,

and flexibility. The algorithm operates on the gra-

dient boosting framework, sequentially crafting deci-

sion trees that progressively enhance prediction accu-

racy. XGBoost has proven its effectiveness by fre-

quently being used in winning solutions to interna-

tional data science competitions, particularly on Kag-

gle, a competitive data science platform (Adebayo,

2020). Moreover, its real-world use extends to dif-

ferent fields like predictive modelling and recommen-

dation systems, demonstrating its versatility. With its

combination of computational power and predictive

capability, XGBoost continues to drive advancements

in machine learning.

Gradient boosting is a technique utilized in ma-

chine learning for both regression and classification

problems. It operates by iteratively combining a se-

ries of simple predictive models, typically decision

trees. Each subsequent model is designed to rectify

the residual errors of its predecessor, thus enhancing

accuracy incrementally (Friedman, 2001).

The technique gets its name from Gradient De-

scent, an optimization method used to minimize the

chosen loss function. Every new model reduces the

loss by moving in the direction of the steepest de-

scent. It does this by incorporating a new tree that

minimizes the loss most effectively, which is the

essence of gradient boosting (Friedman, 2001). Un-

like other boosting algorithms such as AdaBoost (Fre-

und and Schapire, 1997), gradient boosting identifies

the weaknesses of weak learners via gradients in the

loss function, while AdaBoost does so by examining

high-weight data points.

XGBoost (Chen and Guestrin, 2016) is designed

to be highly scalable and parallelizable, making it

suitable for handling large-scale datasets. The algo-

rithm effectively manages sparse data and missing

values without additional input. Additionally, XG-

Boost includes a regularization term into its objective

function. This regularization term helps control the

model complexity and avoid overfitting, a common

problem found with other gradient boosting algorithm

ICAART 2024 - 16th International Conference on Agents and Artificial Intelligence

162

(Friedman, 2001).

Space limitations prevent us from giving here

full details of the XGBoost algorithm, for which

the reader is instead referred to (Chen and Guestrin,

2016). For the purposes of this paper, it is sufficient to

treat XGBoost as a “black-box” learning method that

produces a set of decision trees that can be used as a

betting strategy. We used the XGBoost Python library

(Chen, 2023) which provides a flexible interface with

the scikit-learn API (Pedregosa et al., 2011).

XGBoost’s performance can be further improved

with a technique called parameter tuning. The algo-

rithm’s parameters and hyperparameters are divided

into three types: general parameters, booster parame-

ters, and learning task parameters (Chen, 2023). Gen-

eral parameters control the overall function, booster

parameters influence individual boosters, and learn-

ing task parameters oversee the optimization pro-

cess. Example of hyperparameters include: max-

imum tree depth (max depth); step size shrinkage

(learning rate), number of trees (n estimators);

minimum loss reduction (gamma); minimum sum

of instance weight (min child weight); and the

subsample ratio of training instances (subsample).

Through the adjustment and tuning of these param-

eters, XGBoost can be adjusted to efficiently address

a broad range of machine learning tasks.

2.5 Tuning and Cross Validation

Hyperparameter Tuning Using Grid Search. In

machine learning, hyperparameters are important

configurations that pre-determine the algorithm’s

training process which influences the model’s final

performance on prediction accuracy (Nyuytiymbiy,

2020). In particular, within the scope of this research

involving the XGBoost algorithm, key hyperparame-

ters such as the learning rate and the maximum depth

of the decision trees can significantly affect the model

performance. The optimization of these hyperparam-

eters is core to achieving the highest model predic-

tion ability. A widely recognized technique to find the

best set of hyperparameters is called ‘Hyperparameter

Tuning’. Among the variety of methods available for

this purpose, ‘Grid Search’ emerges as particularly

robust. Grid Search conducts a methodical explo-

ration of all potential combinations of hyperparam-

eter values within a predefined boundary (list). This

is for finding the combination of hyperparameters that

offers optimal model performance (Malato, 2021).

Cross Validation (K-Fold Cross-Validation). K-

fold cross-validation is a technique to determine the

performance of a machine learning model. It involves

partitioning the dataset into k equally-sized subsam-

ples. Each iteration uses one subsample for validation

and the remaining k − 1 for training. The model un-

dergoes k evaluations, with each subsample serving

once as the validation set. The outcomes from the

k tests are averaged to obtain a consolidated perfor-

mance metric. This approach ensures every data point

contributes to both training and validation, preventing

overfitting of the model (Scikit-Learn, 2023a).

GridSearchCV. The GridSearchCV module from the

scikit-learn library (Scikit-Learn, 2023b) integrates

grid search and cross-validation, offering a stream-

lined mechanism for hyperparameter tuning. To use

it, one provides a model (like XGBoost), a param-

eter grid defining the hyperparameter value combina-

tions to test, a scoring method, and a number of k-fold

cross-validations. GridSearchCV then systematically

explores these combinations using cross-validation,

where the dataset is partitioned into subsets and each

subset is iteratively used for validation. Leveraging

GridSearchCV with the XGBoost algorithm not only

saves effort but also ensures the identification of op-

timal hyperparameters, enhancing model robustness

and performance on unseen data.

3 EXPERIMENT DESIGN

3.1 Overview

The primary objective of this experiment is to inte-

grate the XGBoost betting agent into the existing suite

of agents in the BBE system. The agent will leverage

a trained XGBoost model to make informed decisions

on whether to ‘Back’ or ‘Lay’ a bet, predicated on the

input data.

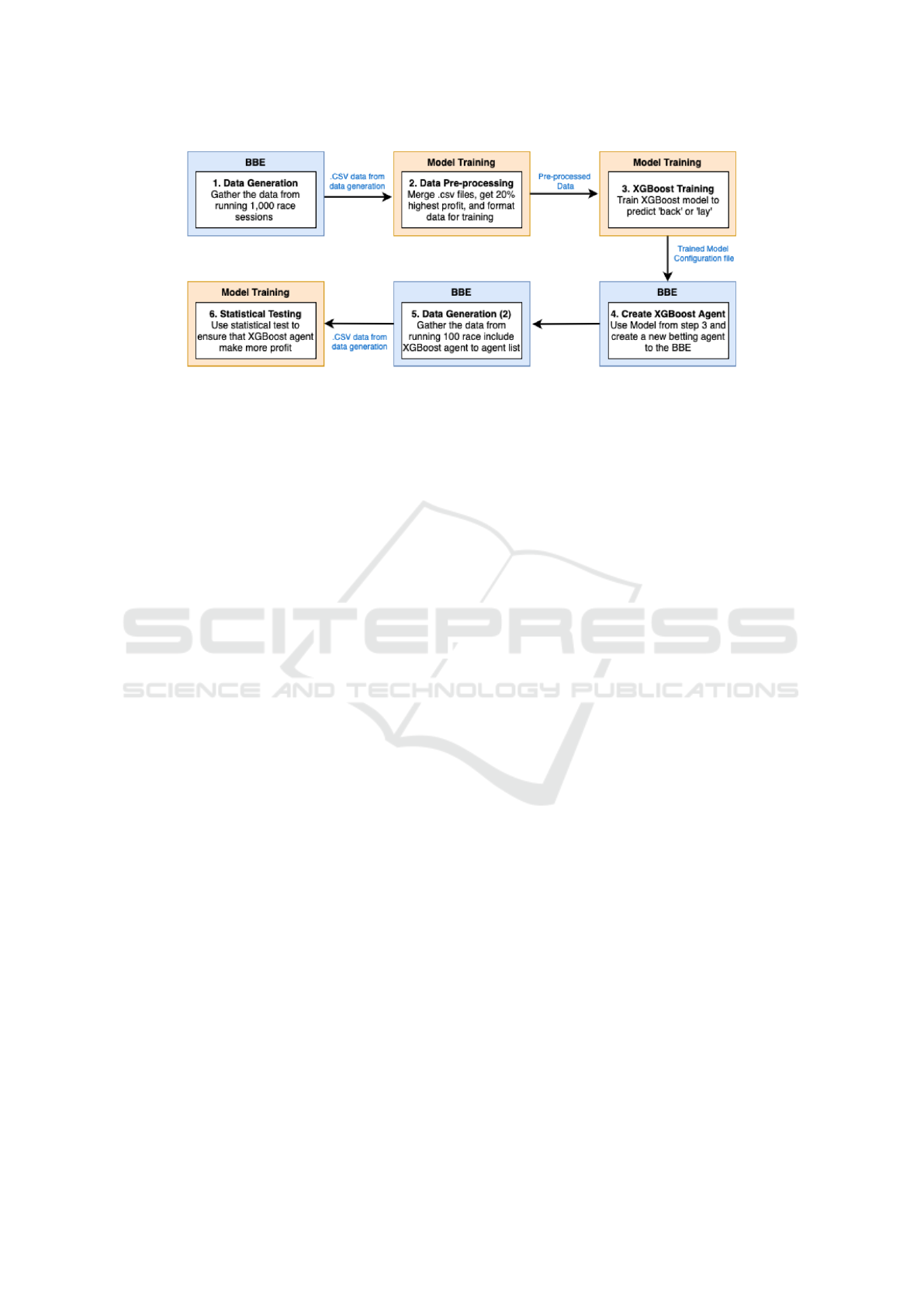

Figure 1 provides the high-level design of this ex-

periment. The first step is to gather the data from

BBE by running 1,000 race sessions. These race

records are then pre-processed, narrowing down the

data to the top 20 percent of the most significant trans-

actions (Back or Lay actions). This refined dataset

was then used for training with the XGBoost Python

library. By tuning the Hyperparameters and using

Cross-validation, the goal was to ensure the model

could perform well in many scenarios.

Once a trained XGBoost model is ready, it is

added as a new betting agent into the BBE system.

To further test its performance, various race scenar-

ios were run, each scenario with 100 races. This ap-

proach ensured we had enough data to assess how the

new agent compared to the existing ones. Lastly, the

collected data is used for statistical hypothesis tests to

validate if the new XGBoost agent is more profitable.

XGBoost Learning of Dynamic Wager Placement for In-Play Betting on an Agent-Based Model of a Sports Betting Exchange

163

Figure 1: High-level overview of the experiment and the data flow of the system.

3.2 Setup for Model Training

Here we outline the specific scenario used for the data

gathering process for XGBoost model training. Com-

plete further details details are available in (Terawong,

2023). We ran 1000 races, each of the same fixed dis-

tance so that the duration of each race was approx-

imately the same, and all races had 5 competitors.

The population of bettors in the ABM was made up

from 10 each of Guzelyte’s (Guzelyte, 2021b; Guze-

lyte and Cliff, 2022) “opinionated” versions of the ZI,

LW, BTF, LinEx, and Underdog strategies plus 5 of

Guzelyte’s Opinionated-Privileged strategy; and then

55 of the original un-opinionated versions of these

strategies, again split 10/10/10/10/10/5, for a grand

total of 110 bettors.

3.3 Setup for Profit Validation

After implementing the XGBoost agent into the BBE

system, data (including the data generated by the XG-

Boost agent) was gathered to evaluate whether the

XGBoost agent generates more profit than the other

agents. Two scenarios are created to experiment with

this new XGBoost agent.

• Scenario 1. The number of simulations is reduced

from 1,000 to 100, as this is only for profit testing

and not for model training. A total of 5 XGBoost-

trained bettor agents were added to the popula-

tion.

• Scenario 2. Everything remains the same as in

Scenario 1, except the number of agents is set to 5

for every agent type. This is for testing how the

XGboost agent performs when the environment

changes.

3.4 XGBoost Parameters

We used the scikit-learn XGBoost API instead of the

native XGBoost API. The native API of XGBoost

provides a highly flexible and efficient way to train

models, making it suitable for those experiment that

prioritize performance and more refined configura-

tion. On the other hand, the scikit-learn XGBoost

API is a wrapper around this native API that inte-

grates seamlessly with the widely used scikit-learn

Python Library. This compatibility is the primary rea-

son for selecting it in this research, mainly due to

its seamless connection with GridSearchCV. This tool

aids in hyperparameter tuning, an important aspect of

model optimization. Moreover, the scikit-learn XG-

Boost API offers a user-friendly interface that reduces

some complexities while still retaining robustness and

enough flexibility.

In the model training process, specific choices

shaped its direction. One crucial decision was the se-

lection of the model’s objective function. This func-

tion dictates what the model aims to achieve during

the learning process. In this work reported here the

objective chosen was binary:logistic. This objective

means the model is made to perform binary classifi-

cation, determining an output as one of two distinct

classes. The term logistic refers to the logistic func-

tion, mapping any input into a value between 0 and 1,

making it suitable for probability estimation in binary

decisions. Given the context of our betting decisions

being binary (Back or Lay), the binary:logistic objec-

tive was a proper selection (Chen, 2023).

For evaluating the effectiveness of the model, lo-

gistic loss (“logloss”) was chosen as the metric (Chen,

2023). In machine learning, the choice of evalua-

tion metric is crucial as it directly influences how the

model’s performance is estimated and how it learns

during training. The logloss is a measure for binary

classification that quantifies the accuracy of a classi-

fier by penalizing false classifications. It estimates the

ICAART 2024 - 16th International Conference on Agents and Artificial Intelligence

164

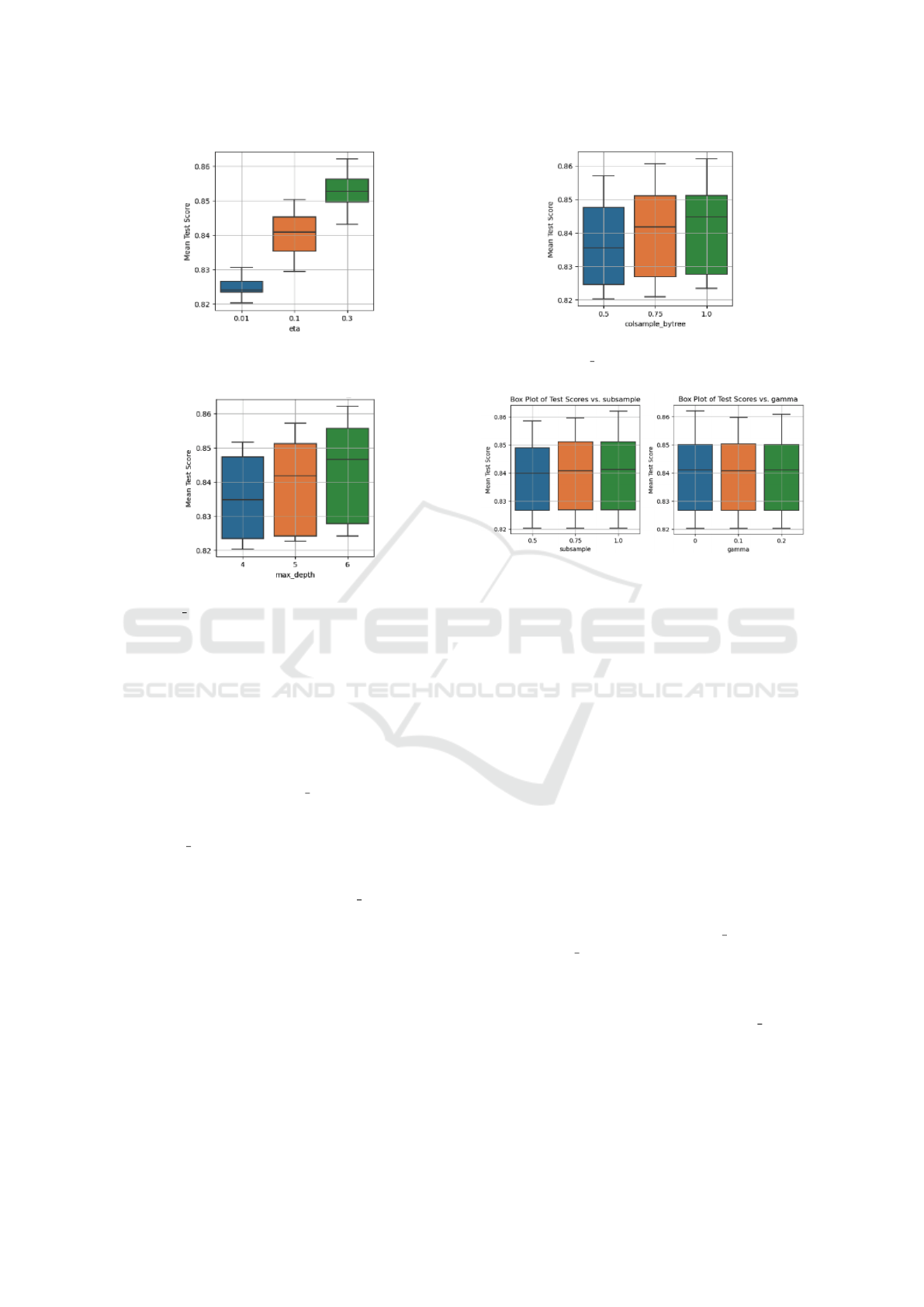

Figure 2: Box-plot of the influence of XGBoost hyperpa-

rameter eta on the mean test score.

Figure 3: Box-plot of the influence of XGBoost hyperpa-

rameter max depth on the mean test score.

probabilities associated with the accuracy of predic-

tions. The closer the predicted probability is to the

actual class, the lower the log loss.

Choice of hyperparameter values is crucial in

shaping model performance. Hyperparameter tun-

ing played a crucial role in the training, and we used

GridSearchCV. The parameters tuned in our work are

as follows: the learning rate eta which regulates

step-size during boosting; max depth, the maximum

depth of the decision tree; subsample, the fraction

of training data to be used in each boosting round;

colsample bytree, the fraction of features to be

used for constructing each tree; gamma, the minimum

loss reduction required to make a further partition of

a leaf node in the decision tree, and n estimators,

which indicates the number of boosting rounds or

trees to be constructed. This sequence is followed be-

cause n estimators influences training time. Identify-

ing the best hyperparameter set initially reduces the

training time on finding the appropriate n estimators.

For further details of the design and implementa-

tion of this extended version of BBE, see (Terawong,

2023).

Figure 4: Box-plot of the influence of XGBoost hyperpa-

rameter colsample bytree on the mean test score.

Figure 5: Illustration of the influence of ‘gamma’ and ‘sub-

sample’ on the mean test score, visualized using box plots.

Left: the effects of subsample. Right: the effects of gamma.

4 RESULTS

4.1 Evaluation of XGBoost Training

4.1.1 Evaluation of Hyperparameters

The metric for evaluating hyperparameter perfor-

mance in the experiment is the ‘accuracy’ score of the

classification. Figures 2 to 5 present results from a 5-

fold cross-validation combined with a hyperparame-

ter tuning using grid search on the training dataset for

the XGBoost model. Key insights are summarized as

follows:

• Hyperparameters Impacting Model Per-

formance. As shown in Figures 2 to 4,

the hyperparameters eta, max depth, and

colsample bytree significantly influence model

performance. An increase in the values of these

hyperparameters generally correlates with an im-

proved accuracy. Among them, eta demonstrates

a pronounced effect, whereas colsample bytree

exhibits a more subtle impact.

• Hyperparameters with Minimal Impact. Vari-

ations in hyperparameters like subsample and

gamma seem to have little to no effect on the

model’s performance according to Figure 5.

XGBoost Learning of Dynamic Wager Placement for In-Play Betting on an Agent-Based Model of a Sports Betting Exchange

165

Figure 6: Illustration of the learning process of the model.

It can be observed that the ‘LogLoss’ gradually decreased

when the number of boosting round increases.

Through the process of cross-validation and hy-

perparameter tuning on the training data using the

XGBoost machine learning algorithm, an optimal

model was derived with a specific set of hyperparam-

eters: colsample bytree=1.0; eta=0.3; gamma=0;

max depth=6, and subsample=1.0.

4.1.2 Evaluation of ‘n estimators’ Parameters

After identifying the optimal set of hyperparameters,

the next parameter under evaluation was n estima-

tors. This parameter indicates the number of boost-

ing rounds or trees that should be constructed. While

in the code n estimators was initially set to 1,000, im-

plying the intention to execute 1,000 boosting rounds,

the inclusion of early stopping rounds=10 ensures that

training halts if the validation metric doesn’t demon-

strate any enhancement over 10 successive boosting

rounds. The combined usage of n estimators and early

stopping rounds aids in mitigating both underfitting

and overfitting of the model.

As depicted in Figure 6, the ‘LogLoss’ consis-

tently decreases as the number of boosting rounds

increases. This suggests that the model continues

to learn and improve. The dashed line represents

the early stopping point, beyond which the model no

longer exhibits significant improvement. The model

halted at the 452nd boosting round, as indicated by

the early stopping mechanism. With these refine-

ments, an optimal model has been obtained.

4.1.3 Evaluation of Optimal XGBoost Model

The SciKitLearn XGBoost training function that we

use in this work provides insights into how different

features contribute to the model’s predictions using

the XGBoost F-score, which denotes the frequency

with which a feature is used to split the data across

all trees: this tell us the relative importance of each

feature. The three most important features in our XG-

Boost bettor were:

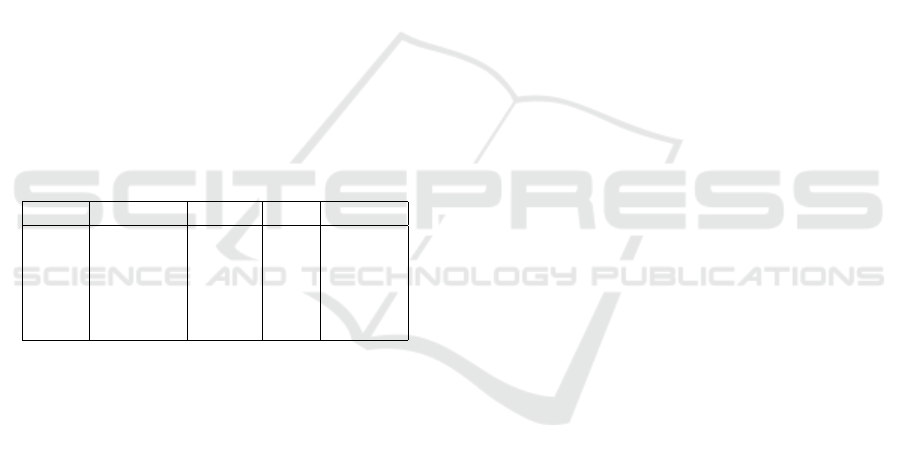

Table 1: Confusion Matrix from the XGBoost training.

Predicted Labels

lay back

True Labels

lay 72521 1197

back 9541 6730

1. Distance (F-score: 8680). As the most influen-

tial feature, ‘distance’ plays a central role in the

model’s decision-making, indicating its signifi-

cance in predicting the patterns the model iden-

tifies.

2. Time (F-score: 6642). The ‘time’ feature emerges

as the second most influential feature, though it

lags behind ‘distance’ by over 2000 points. Nev-

ertheless, its considerable F-score denotes its rel-

evance in the model’s predictions.

3. Rank (F-score: 1276). With a considerably lower

F-score compared to the other two features, ‘rank’

seems to h ave a more marginal impact on the

model’s decision process.

The confusion matrix of Table 1 summarizes the

performance of the classification model. The follow-

ing interpretations can be drawn:

• True Positive (6730). These instances correctly

identify a ‘back’ bet. This means the model cor-

rectly predicted 6,730 instances where one should

back a bet.

• True Negative (72521). These instances represent

cases where the model correctly predicted a ‘lay’

bet. In this context, it means the model accurately

identified 72,521 instances where one should not

back the bet.

• False Positive (1197). These instances represent

errors in prediction. The model mistakenly iden-

tified 1,197 bets as ‘back’ when they should have

been ‘lay’.

• False Negative (9541). This count represents in-

stances where the model wrongly classified bets

as ‘lay’ when they should have been ‘back’. These

could be seen as signifying areas where the model

could be improved for better accuracy since the

number is high.

According to this matrix, the model shows high

accuracy in predicting when to place a lay bet be-

cause the number of true negatives is high. However,

the number of false negatives indicates an area of po-

tential improvement for the model, highlighting the

potential to better recognise instances when the bettor

should place a back bet.

The classification report, summarized in Table 2,

provides in-depth metrics to assess the XGBoost

ICAART 2024 - 16th International Conference on Agents and Artificial Intelligence

166

model’s performance on the betting decision. Here,

Class 0 corresponds to lay and Class 1 to back:

Precision (Class 0: 0.88, Class 1: 0.85). Preci-

sion measures how accurate the model’s positive pre-

dictions are. For Class 0, a precision of 0.88 means

that out of all predicted lays, 88% were correct. For

Class 1, 85% of the model’s predictions were correct.

Recall (Class 0: 0.98, Class 1: 0.41). Recall as-

sesses the model’s ability to detect all actual positives.

For Class 0, the model identified 98% correctly. How-

ever, for Class 1, it was only 41%, showing room for

improvement here.

F1 Score (Class 0: 0.93, Class 1: 0.56). F1-Score

balances precision and recall. While it shows a high

score for Class 0 of 93%, it has a moderate score for

Class 1 of 56%.

Accuracy (0.88). The model correctly predicted

the outcome for 88% of the bets. Referring to Table 2,

it’s clear that the model performs well for Class 0 be-

cause precision and recall are high. For Class 1, while

precision remains high, recall drops, indicating chal-

lenges in detecting this class. However, the model’s

overall prediction accuracy is still high at 88%.

Table 2: Classification Report of the best model trained by

XGBoost: Class 0 is lays; Class 1 is backs; Acc. is Accu-

racy; MA is Macro Average; and WA is Weighted Average.

Class Precision Recall F1 Support

0 0.88 0.98 0.93 73718

1 0.85 0.41 0.56 16271

Acc. 0.88 89989

MA 0.87 0.70 0.74 89989

WA 0.88 0.88 0.86 89989

4.2 Hypothesis Testing

4.2.1 Scenario 1

Simulation Setup. The sessions were set at 100

rounds, incorporating various agents in predefined

quantities. Specifically, 10 agents each of types ZI,

LW, Underdog, BTF, and LinEx were introduced,

along with 5 each of XGBoost and Privilege agents.

This specific configuration was reminiscent of the one

used during the model training phase, albeit here with

the inclusion of the XGBoost agent.

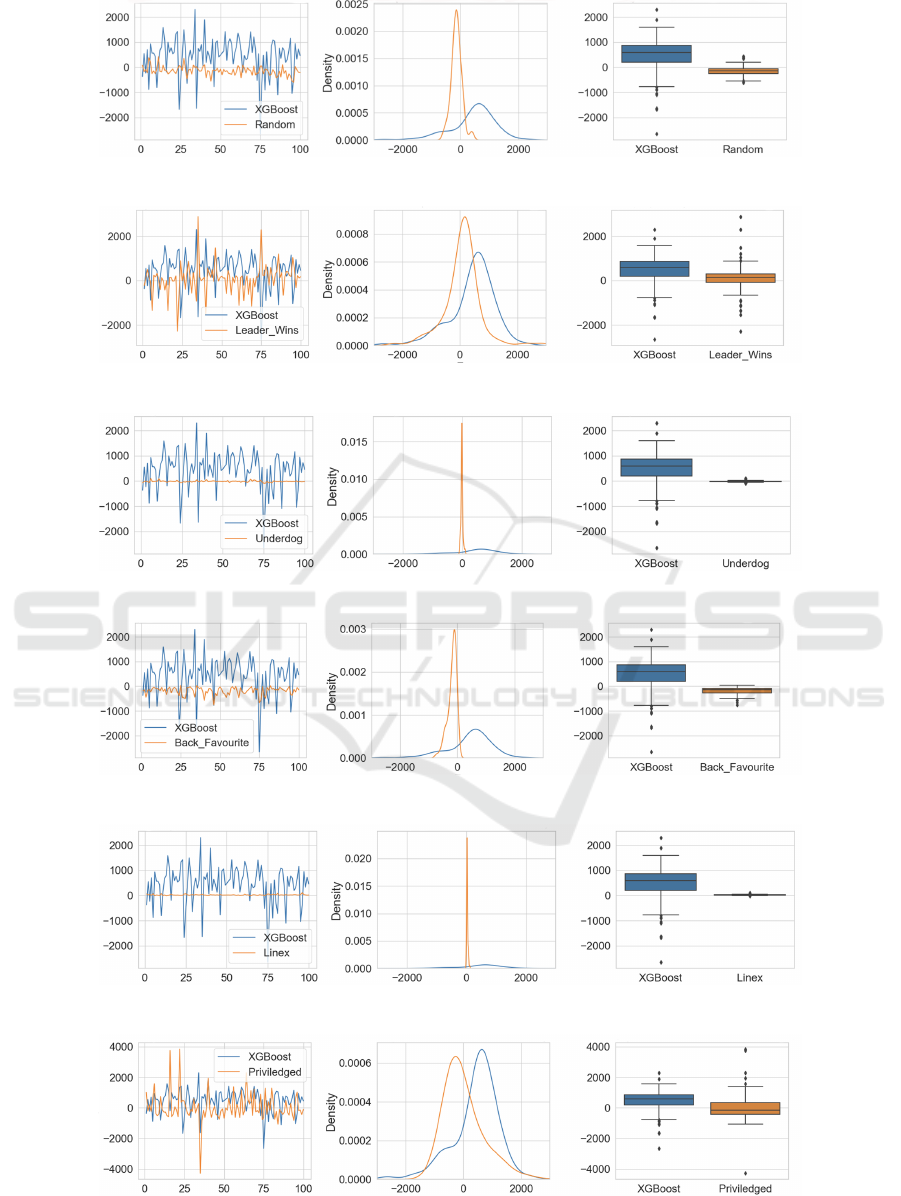

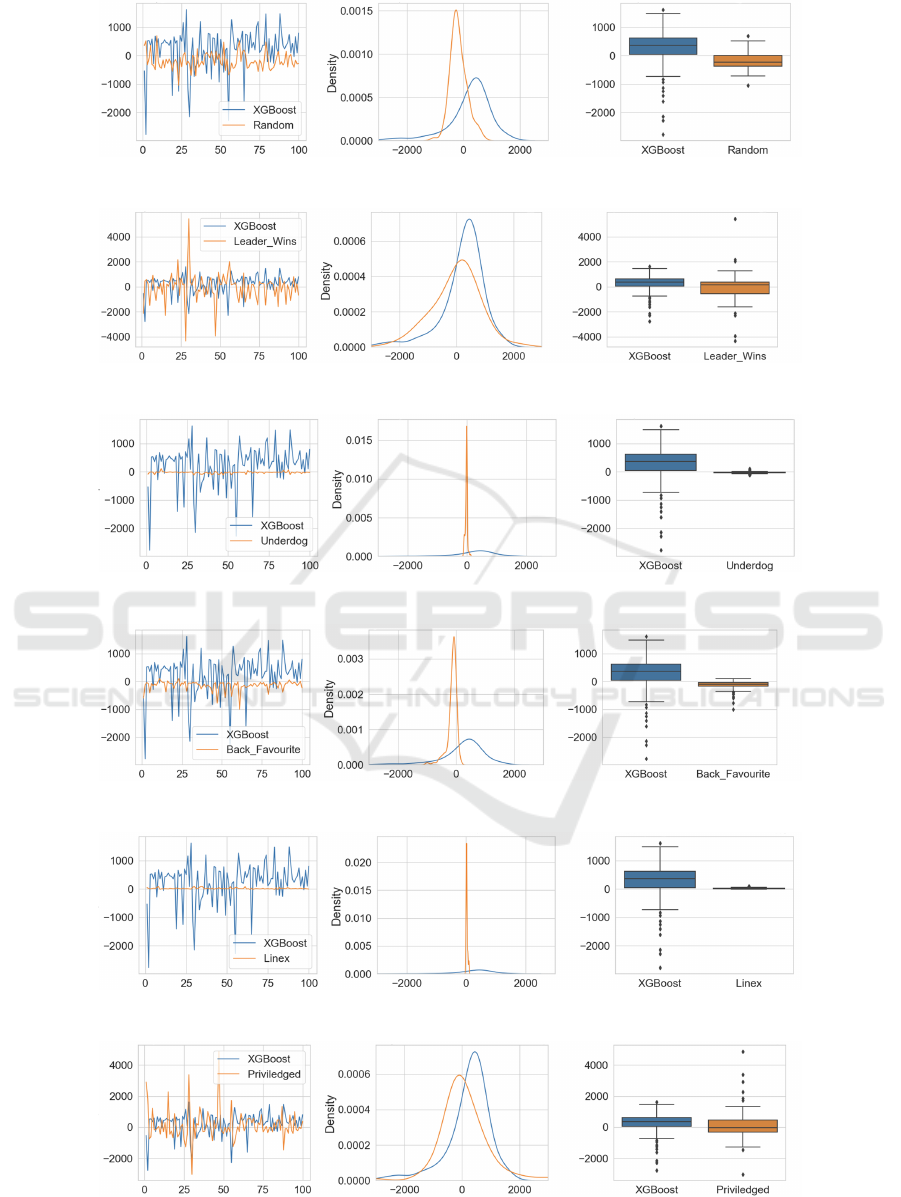

In Figures 7 through 12, a consistent layout is

used: the leftmost plot shows the average profit time-

series comparison between XGBoost and its counter-

part agent; the central plot exhibits the Kernel Density

Estimation (KDE) contrasting XGBoost and the cor-

responding agent; the rightmost plot shows a box plot

of this comparative data.

Statistical Examination. Visual inspection of the

Kernel Density Estimation (KDE) plots of Figures 7

through 12, indicated that the data distributions were

non-Normal, and in each case when we applied the

Shapiro-Wilks test, the test outcome confirmed non-

Normality. This prompted us to use the Wilcoxon-

Mann-Whitney U-Test to with null hypothesis that

there’s no difference in the profit averages between

the XGBoost agent and other agents, and alternate hy-

pothesis that the XGBoost agent is more profitable. In

all cases the null hypothesis is roundly rejected.

4.2.2 Scenario 2

Simulation Setup. Retaining the simulation ses-

sions at 100 rounds, a different composition of agents

was employed: 5 agents each for Random, Leader

Wins, Underdog, Back Favourite, Linex, XGBoost,

and Privilege.

Statistical Examination. Similar to Scenario 1, the

data’s non-normal distribution was confirmed in each

case by the Shapiro-Wilk test and this is confirmed

by visual inspection of the Kernel Density Estimation

(KDE) plots of Figures 13 through 18. Consequently,

the Wilcoxon-Mann-Whitney U test was used, and in

each case the results from the U-test led to the rejec-

tion of the null hypothesis (the largest p value, for

Privileged/XGBoost, was 0.0017), further emphasis-

ing the XGBoost agent’s performance.

Furthermore, from examination of the plots of

Figures 13 through 18 it’s also evident that the

XGBoost betting agent consistently outperforms its

peers, the same as in Scenario 1. The line graph

highlights XGBoost’s superior performance, with its

values often trending higher. Similarly, the box plot

emphasizes its strong placement, often residing in the

upper range of outcomes.

In conclusion, for both scenarios, the XGBoost

betting agent demonstrably outperformed its peers in

terms of profit generation. Given these consistent re-

sults across different scenarios, it’s obvious that the

XGBoost agent, as modelled and implemented, offers

a notable advantage in the context of this simulation.

5 FUTURE WORK

Numerous opportunities and potential areas remain

for further investigation, including:

Variability of Data Collection. BBE, being a com-

plex system, offers several scenarios and parame-

ters setting that can influence outcomes. Each race’s

length, the number of competitors, and the mixture of

participating agents all contribute uniquely to the fi-

XGBoost Learning of Dynamic Wager Placement for In-Play Betting on an Agent-Based Model of a Sports Betting Exchange

167

Figure 7: Profit generated from XGBoost compare with Random Betting Agent for Scenario 1.

Figure 8: Profit generated from XGBoost compare with Leader Win Agent for Scenario 1.

Figure 9: Profit generated from XGBoost compare with Underdog Agent for Scenario 1.

Figure 10: Profit generated from XGBoost compare with Back Favorite Agent for Scenario 1.

Figure 11: Profit generated from XGBoost compare with Linex Agent for Scenario 1.

Figure 12: Profit generated from XGBoost compare with Privileged Agent for Scenario 1.

ICAART 2024 - 16th International Conference on Agents and Artificial Intelligence

168

Figure 13: Profit generated from XGBoost compare with Random Betting Agent for Scenario 2.

Figure 14: Profit generated from XGBoost compare with Leader Win Agent for Scenario 2.

Figure 15: Profit generated from XGBoost compare with Underdog Agent for Scenario 2.

Figure 16: Profit generated from XGBoost compare with Back Favorite Agent for Scenario 2.

Figure 17: Profit generated from XGBoost compare with Linex Agent for Scenario 2.

Figure 18: Profit generated from XGBoost compare with Privilege Agent for Scenario 2.

XGBoost Learning of Dynamic Wager Placement for In-Play Betting on an Agent-Based Model of a Sports Betting Exchange

169

nal dataset. Currently, the data extraction from BBE

has been largely uniform. However, by introducing

more randomness or systematically varying these pa-

rameters, it’s possible to simulate a broader spectrum

of race scenarios. Gathering data from these diverse

conditions would likely provide a dataset with richer

contextual information.

Feature Engineering. The model currently relies on

four primary features is both a strength, for simplic-

ity, and a limitation, for depth of insight. While dis-

tance, rank, time, and stake are crucial, there exist

other features that might further refine the model’s un-

derstanding. For instance, the rate of change of rank

over time, interactions between distance and stake, or

even cyclic patterns in betting behaviour could be po-

tential features. Incorporating such sophisticated fea-

tures could refine the model’s decision boundaries and

offer more precise predictions.

Model Optimization and Evaluation Metrics. The

choice of the [binary:logistic] objective function has

been pivotal for the model’s current design, aiming

for binary classification. However, XGBoost offers

a large number of objective functions and evalua-

tion metrics tailored for different kinds of predic-

tive tasks. By experimenting with other objectives,

such as ‘multi:softmax’ for multiclass problems or

‘reg:squarederror’ for regression tasks, new insights

or even potential performance improvements could be

achieved. This could also lead to the development of

betting agents that can predict more than just binary

outcomes, potentially increasing the versatility of the

agent in different betting scenarios.

Expanded Testing Scenarios. Here we have used

only two testing scenarios. However, the dynamic na-

ture of the betting domain suggests the potential ben-

efit of a more comprehensive evaluation, encompass-

ing a broader spectrum of conditions and parameters.

The performance and limitations of the XGBoost bet-

ting agent, in comparison to other available agents in

the system, could be further illuminated under an ar-

ray of diversified scenarios.

For instance, the impact of varying the number of

competitors in a race could provide insights into the

agent’s robustness across different competitive land-

scapes. Similarly, the distance of races can influence

outcome predictability, with certain agents potentially

excelling in short sprints while others might have an

edge in longer, more strategic races.

Furthermore, exploring races with different odds

ranges can unveil how well the XGBoost betting agent

navigates between high-risk, high-reward situations

versus more conservative betting scenarios. Extend-

ing the testing to these more diverse scenarios would

offer a richer, more comprehensive view of the XG-

Boost betting agent’s capabilities, strengths, and po-

tential areas for improvement

Online Learning and Feedback Loop Integration.

The field of online machine learning, where models

learn on the go, adapting to new data as it arrives,

offers a chance to improve the static nature of the cur-

rent implementation. Instead of periodic manual data

extraction and retraining, an integrated feedback loop

would allow the XGBoost agent to continuously re-

fine its strategies during every BBE session.

6 CONCLUSION

The primary contribution of this paper is the intro-

duction of XGBoost learning to the bettor-agents in

the BBE agent-based model, offering the opportu-

nity to use BBE as a synthetic data generator and

for XGBoost to then learn profitable betting strate-

gies from the data provided from BBE. Comparing

the XGBoost-learned betting strategy with the perfor-

mance of the minimally simple strategies pre-coded

into BBE demonstrates that XGBoost does indeed of-

fer a distinct advantage in adaptively learning in-play

betting strategies which are more profitable than any

of the strategies that were used to create the training

data. This serves as a proof-of-concept and in future

work we intend to explore application of the methods

described here to automatically learn betting strate-

gies that could be profitable if deployed in betting on

real-world races.

REFERENCES

Adebayo, S. (2020). How the Kaggle winners algorithm

XGBoost works. https://dataaspirant.com/xgboost-

algorithm.

Cameron, C. (2009). You Bet: The Betfair Story; How Two

Men Changed the World of Gambling. Harper Collins.

Chen, T. (2023). XGBoost Documentation.

https://xgboost.readthedocs.io/en/stable/index.html.

Chen, T. and Guestrin, C. (2016). XGBoost: A scalable

tree boosting system. In Proceedings of the 22nd

ACM SIGKDD International Conference on Knowl-

edge Discovery and Data Mining, KDD2016, pages

785–794.

Cliff, D. (2021). BBE: Simulating the Microstructural Dy-

namics of an In-Play Betting Exchange via Agent-

Based Modelling. SSRN 3845698.

Cliff, D., Hawkins, J., Keen, J., and Lau-Soto, R. (2021).

Implementing the BBE agent-based model of a sports-

betting exchange. In Affenzeller, M., Bruzzone, A.,

Longo, F., and Petrillo, A., editors, Proceedings of the

33rd European Modelling and Simulation Symposium

(EMSS2021), pages 230–240.

ICAART 2024 - 16th International Conference on Agents and Artificial Intelligence

170

Davies, M., Pitt, L., Shapiro, D., and Watson, R. (2005).

Betfair.com: Five technology forces revolutionise

worldwide wagering. European Management Journal,

23(5):533–541.

Freund, Y. and Schapire, R. (1997). A decision-theoretic

generalization of on-line learning and an application

to boosting. Journal of Computer and System Sci-

ences, 55(1):119–139.

Friedman, J. (2001). Greedy function approximation: A

gradient boosting machine. The Annals of Statistics,

29(5):1189–1232.

Guzelyte, R. (2021a). BBE OD: Threaded Bris-

tol Betting Exchange with Opinion Dynamics.

https://github.com/Guzelyte/TBBE OD.

Guzelyte, R. (2021b). Exploring opinion dynamics of

agent-based bettors in an in-play betting exchange.

Master’s thesis, Department of Engineering Mathe-

matics, University of Bristol.

Guzelyte, R. and Cliff, D. (2022). Narrative economics of

the racetrack: An agent-based model of opinion dy-

namics in in-play betting on a sports betting exchange.

In Rocha, A.-P., Steels, L., and van den Herik, J., edi-

tors, Proceedings of the 14th International Conference

on Agents and Artificial Intelligence (ICAART2022),

volume 1, pages 225–236. Scitepress.

Houghton, J. (2006). Winning on Betfair for Dummies. Wi-

ley.

Keen, J. (2021). Discovering transferable and profitable al-

gorithmic betting strategies within the simulated mi-

crocosm of a contemporary betting exchange. Mas-

ter’s thesis, University of Bristol, Department of Com-

puter Science; SSRN 3879677.

Malato, G. (2021). Hyperparameter Tuning, Grid Search

and Random Search. https://www.yourdata-

teacher.com/2021/05/19/hyperparameter-tuning-grid-

search-and-random-search/.

Nyuytiymbiy, K. (2020). Parameters and hyperpa-

rameters in machine learning and deep learn-

ing. https://towardsdatascience.com/parameters-and-

hyperparameters-aa609601a9ac.

Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V.,

Thirion, B., Grisel, O., Blondel, M., Prettenhofer,

P., Weiss, R., Dubourg, V., Vanderplas, J., Passos,

A., Cournapeau, D., Brucher, M., Perrot, M., and

Duchesnay, E. (2011). Scikit-learn: Machine learning

in Python. Journal of Machine Learning Research,

12:2825–2830.

Scikit-Learn, (2023a). Cross-validation: evaluating estima-

tor performance. https://scikit-learn.org/stable/mo-

dules/cross validation.html.

Scikit-Learn, (2023b). SKLearn model se-

lection: GridSearchCV. https://scikit-

learn.org/stable/modules/gen-erated/

sklearn.model selection.Grid-SearchCV.html.

Terawong, C. (2023). An XGBoost Agent Based Model of

In-Play Betting on a Sports Betting Exchange. Mas-

ter’s thesis, Department of Computer Science, Univer-

sity of Bristol, UK.

APPENDIX: GITHUB REPOS

The integration of the XGBoost machine learn-

ing algorithm into BBE has been separated

into two GitHub repositories, both of which are

freely available as open-source Python code from:

https://github.com/ChawinT/

Synthetic Data Generator

GitHub repo: XGBoost TBBE/tree/main

1. Data Collection. Enhancements were made to the

Bristol Betting Exchange (BBE) to facilitate an

efficient data acquisition process.

2. XGBoost Betting Agent. A new component,

named the XGBoost betting agent, was introduced

within the betting agent.py file. This serves as a

blueprint for embedding machine learning capa-

bilities into BBE.

3. Model Configuration. The model.json file encap-

sulates the trained XGBoost model utilized by the

agent for bet predictions.

This repository lays the foundation for data col-

lection and demonstrates a practical blueprint for in-

tegrating machine learning models into the BBE sys-

tem.

Model Training & Validation

GitHub repo. XGBoost ModelTraining

1. Model Training. Comprehensive training of the

XGBoost model has been conducted, supple-

mented with optimization techniques and visual-

ization tools.

2. Statistical Hypothesis Testing: Dedicated sections

have been allocated for rigorous statistical hy-

pothesis testing to validate the reliability of the

results.

Together, these repositories form a comprehensive

suite for introducing and harnessing the power of ma-

chine learning, specifically XGBoost, in the realm of

betting on the BBE platform.

XGBoost Learning of Dynamic Wager Placement for In-Play Betting on an Agent-Based Model of a Sports Betting Exchange

171