Auditor Competency to Conduct Remote Audits

Robiur Rahmat Putra, Kiko Armenita Julito, Sihar Tambun and Anjeli Frisilia

Universitas 17 Agustus 1945 Jakarta, Jl. Sunter Permai Raya, North Jakarta, Indonesia

Keywords: Auditor Competency, NVivo, Remote Audit.

Abstract:

This research aims to obtain concepts and information about what competencies are needed by an auditor, if

you want to become an auditor with remote audit skills. The research data sources are online news, YouTube

and research articles for 3 years, specifically from 2021 to 2023. Data sources are selected based on credibility

and suitability of the data to the problem being studied. Data processing uses NVivo 12 Plus software. There

are four stages of data processing, the data input process, coding process, visualization process, and conclusion

determination process. Coding validity was evaluated using a triangulation approach. The research results

obtained seven competency points needed for auditors with remote audit skills. Firstly, two-way

communication competency during the audit process. Second, master audit procedures in general. Third, have

an attitude of professionalism. Fourth, be able to extract audit evidence from information and communication.

Fifth, have IT-based audit certification. Sixth, master digital technology. Seventh, understand management

information systems. The implications of the research results can be used by auditors or prospective auditors

in the future. If you want to work as an auditor with remote audit skills, it is recommended that you master

these seven competencies. For students who are prospective auditors, these seven competencies can be

equipped and prepared now. With these seven competencies, it is hoped that they can become capital to

become superior auditors in the era of digitalization in the future.

1

INTRODUCTION

In early October 2023, Ziprecruiter noted that Auditor

work in the field of remote audit is one of the jobs

with a high average salary in the United States. The

annual salary of an auditor in the remote audit field is

$65,762 to $118,317. This salary is higher than the

average salary for auditors in other fields.

Ziprecruiter also reports that there are very few

vacancies for professional auditors in the remote audit

field in various cities in the world, such as in Jakarta

(Ziprecruiter, 2023). The demand for the auditor

profession in the field of remote audit is very high in

developed countries such as the United States

(Crucean & Hategan, 2023). Meanwhile in

developing countries, the demand for auditors in the

field of remote audit emerged after the Covid 19

pandemic (Baatwah & Al-Ansi, 2022; Castka &

Searcy, 2023). This fact is very interesting to observe,

considering that the direction of world development

is towards digitalization and high technology.

Information on the facts and phenomena described

above must be utilized. Auditors and prospective

auditors must compete to be able to compete in this

profession. Paying attention to phenomena and facts

in the field raises a very important research question

to study, what competencies are needed by auditors to

carry out remote audits.

Previous research achievements related to the

problems studied, there are several things that have

been achieved. Bhattacharjee et al. (2020)explained

that remote audits can still maintain audit quality

because supervision can be carried out through the

audit software used. Supervisors play an important

role in maintaining the quality of the audit process.

Remote audits can also trigger auditors' creativity in

solving problems encountered during audits.

Furthermore, Fan et al., (2020) stated that remote

audits use more efficient costs. This audit system will

cut a lot of operational costs. Large costs will depend

on creating a system for remote audits that is adequate

and integrated with artificial intelligence technology.

The difference between this research and previous

research lies in the differences in the problems

studied and the resulting research recommendations.

Research was conducted to produce a systematic

concept about the competencies needed to become an

auditor with remote audit skills. No previous research

304

Putra, R., Julito, K., Tambun, S. and Frisilia, A.

Auditor Competency to Conduct Remote Audits.

DOI: 10.5220/0012581100003821

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 4th International Seminar and Call for Paper (ISCP UTA ’45 JAKARTA 2023), pages 304-310

ISBN: 978-989-758-691-0; ISSN: 2828-853X

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

has done this. There are no professional accounting

bodies or auditor professional bodies in various

countries that have this competency standard. There

are no standardized competency standards in the form

of professional standard books. This research carries

out a coding process from various sources, combines

coding in one visualization model, and determines

conclusions using the principle of triangulation. This

research model is still new and has not been carried

out by many researchers.

The aim of this research was to obtain concepts

and information about the competencies needed to

carry out remote audits. This concept really needs to

be obtained in detail, so that professional auditors and

candidates get a clear picture of this competency.

There is no systematic description or detailed

information in various literature. There is no

standardized concept regarding the competencies that

auditors must fulfill. Even the professional standards

for public accountants in Indonesia and in various

countries do not yet have this competency standard.

Remote audit competency standards have not been

standardized in the form of professional competency

standards. There are not many experts who

understand this field. This research was conducted to

formulate this concept and provide information for

administrators of professional bodies.

The benefits of the results of this research can be

used by practicing auditors and prospective auditors

in the future. Auditors and prospective auditors can

prepare themselves from now on by strengthening

competencies in accordance with remote auditing

needs. Accountant or auditor professional bodies can

utilize the information resulting from this research, as

a basis for preparing standardized competency

standards. Educational institutions or universities can

also utilize this information to develop learning

curricula for accounting students. The curriculum was

formed and structured to produce accounting

graduates with competency in the field of auditing,

specifically remote auditing. This is very important,

considering that the world is heading towards an era

of digitalization in various sectors, including the

accounting and auditing industries.

2

LITERATUR REVIEW

Competency is the work ability of each individual

which includes aspects of knowledge, skills and work

attitudes that are in accordance with the expected

standardization (Li et al., 2022). Another definition

states that competence is something related to an

individual's abilities and skills to achieve the expected

results (Basilotta et al., 2022). According to Spencer

& Spencer (2008), competence consists of five

characteristics. First, skills, the ability to plan,

thoroughness, leadership ability, ability to collaborate

in groups accompanied by abilities in accordance

with intellectual, emotional and social intelligence in

planning, leading with accuracy, ability to collaborate

in groups. Second, goal or motivation is something

where a person consistently thinks so that he takes

action. adding that motives are drives, direct and

select behavior toward certain actions or goals and

away from others. For example, someone who has

achievement motivation consistently develops goals

that provide a challenge to himself and takes full

responsibility for achieving these goals and expects

feedback to improve himself. Third, traits are traits

that make people behave or how someone responds to

something in a certain way. For example, self-

confidence, self-control, fortitude or endurance.

Fourth, attitude, the attitudes and values that a person

has. Attitudes and values are measured through tests

on respondents to find out the values a person has and

what interests someone to do something. Fifth,

knowledge, the information a person has for a

particular field. Knowledge is a complex

competency. Knowledge tests measure a participant's

ability to choose the most correct answer but cannot

see whether someone can do the job based on the

knowledge they have.

Remote audit is an audit that is carried out

partially or completely offsite. Audits will still cover

all areas but use digital technology to support

assessors where site visits are not possible (Ariyanto,

2022). Due to efficiency considerations, audit

procedures previously carried out via client visits

were also carried out remotely as a reaction to

increased activity (Febriyana et al., 2023). The

remote audit itself is carried out like a normal audit,

starting from planning or pre-audit, opening meeting,

audit implementation, closing meeting and reporting,

then post-audit follow up (Agha, 2022). Electronic

documents and data are shared via screen sharing.

Apart from that, remote audits can also be used for

online discussions, opening and closing audit

meetings, and in some cases site inspections

(Hermina, 2022)

3

METHODS

This research uses qualitative research methods using

a systematic literature review approach. The literature

studied does not only come from research articles, but

also from several sources obtained online. Sources of

Auditor Competency to Conduct Remote Audits

305

data processed come from YouTube, online news,

and research articles. The data source must come

from a credible source, whether YouTube channels,

online news, and other sources. Data is searched

using keywords that match the research question. The

consideration for using this data is due to the

availability of adequate data on the internet and it can

be accessed easily (Hafidhah & Yandari, 2021). The

selected data sample is data published during the last

three years, specifically 2021 to 2023. The data

processing uses NVivo 12 Plus software. This

software was chosen because it is able to produce

coding visualization images and the way to use the

software is very user friendly (Tambun & Sitorus,

2023).

There are four stages carried out in the data

processing process with NVivo, i.e. the data input

stage, coding stage, visualization stage and

conclusion stage (Sitorus & Tambun, 2023). The first

stage, data input uses two methods, internal data input

and external data. Internal data is data input to NVivo

without using an internet connection. This data is

usually data that is already available on the laptop,

such as research articles. Meanwhile, external data is

data that is input into NVivo using an internet

connection, the data input process uses the ncapture

for NVivo facility. Examples of external data

originating from the internet such as YouTube, online

news, and various social media. The second stage,

coding data according to the answers to the research

question. Coding is simple words or sentences that are

answers to research questions. At this stage, content

analysis is carried out, particularly the stage of

understanding the words or sentences in the research

data (Tambun, 2021). Specifically for the coding

process for YouTube data sources or social media

sources in video form, coding is carried out after there

is a transcript of the YouTube content or video.

Analysis was carried out by making transcripts, then

a coding process was carried out (Salahudin et al.,

2020). The third stage, create a coding visualization

image. Visualization coding is a collection of coding

that forms an image. Coding images are

interconnected with various data sources. This coding

image is analyzed in the process of drawing research

conclusions. The fourth stage, determining research

conclusions. Research conclusions are answers to

research questions. The answer can be seen from the

existing coding. Coding is considered to have strong

validity if the coding is confirmed from various data

sources. Coding validity is strong if it is confirmed at

least three times from various data sources. This

principle is a measurement of coding validity using

the triangulation method (Natow, 2020). Next, the

coding is sorted based on the most confirmations to

the coding with the fewest confirmations. These

codings are used as answers to research questions, as

well as as research conclusions.

4

RESULTS AND DISCUSSION

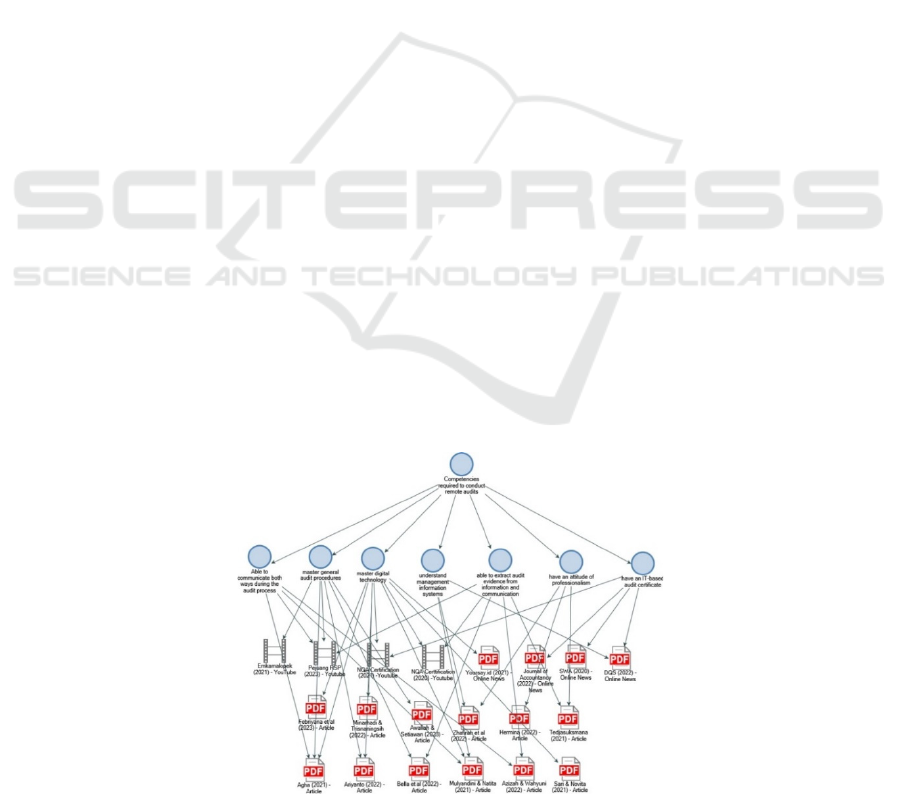

This research produced several references consisting

of: 4 YouTube, 4 Online News, and 12 research

articles. The coding process was carried out using

NVivo 12 Plus Software. There are seven codings that

are valid and confirmed at least three times in the data

sources studied. Below is a visualization image of the

resulting coding.

All coding in figure 1 is an answer to the research

question.Coding comes from content analysis of the

various data studied. The coding process uses the

facilities available in the NVivo 12 Plus software. The

following is a summary table and intensity of each

coding created.

Figure 1: Coding Visualization Image.

ISCP UTA ’45 JAKARTA 2023 - THE INTERNATIONAL SEMINAR AND CALL FOR PAPER (ISCP) UTA ’45 JAKARTA

306

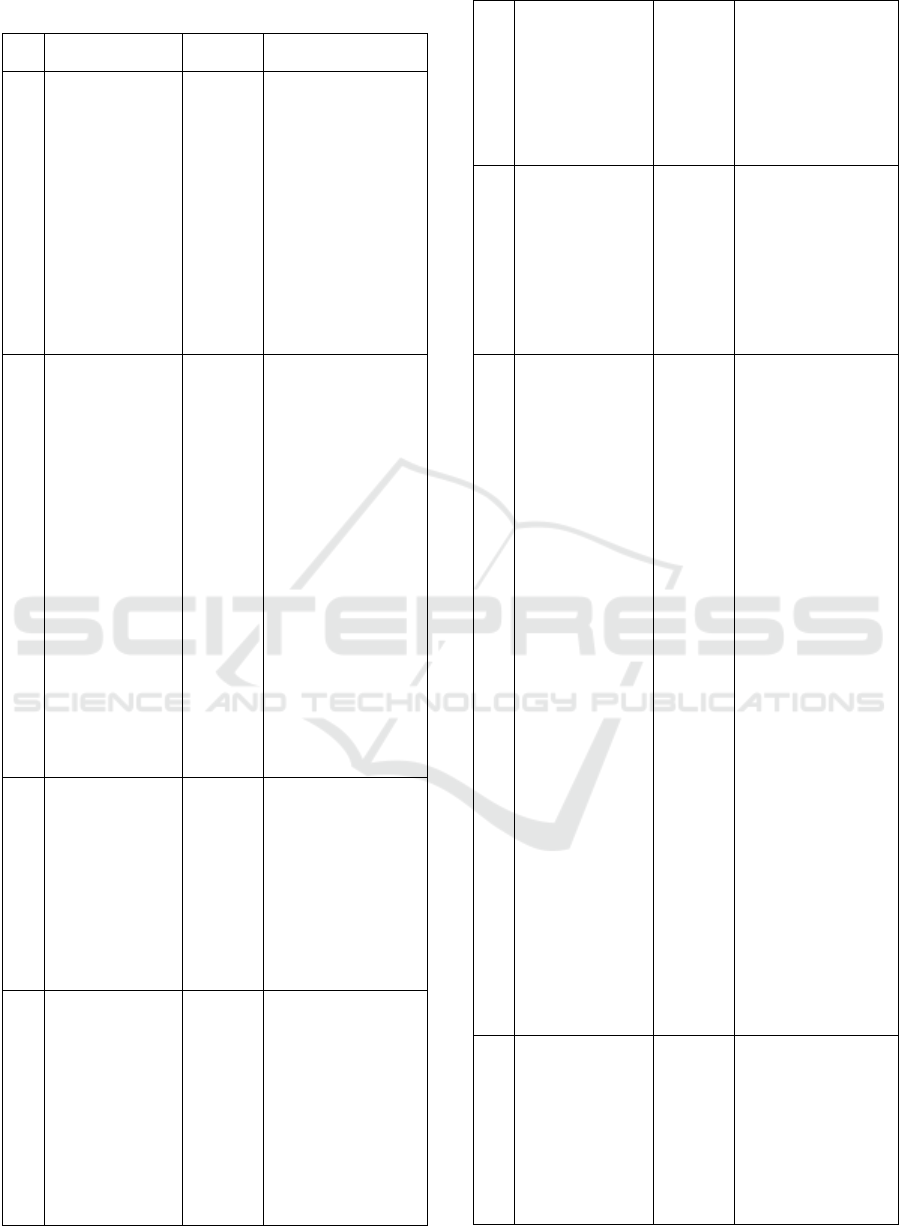

Table 1: Recapitulation of Coding.

No. Coding Intensity Reference

1 Two-way

communication

during the audit

process

4

• Agha (2022) –

Article

• Azizah &

Wahyuni

(2022) –

Article

• Mulyandini &

Natita (2021) –

Article

• Pejuang RSP

(2023) –

You Tube

2 Mastering

general audit

procedures

6

• Agha (2021) –

Article

• Ariyanto

(2022) –

Article

• Awaliah &

Setiawan

(2023) –

Article

• Bella et al

(2020) –

Article

• Emkamalopek

(2021) –

You Tube

• Pejuang RSP

(2023) –

You Tube

3 Have an

attitude of

professionalism

3

• Hermina

(2022) –

Article

• Tedjasuksmana

(2021) –

Article

• Zhafirah et al

(2022) –

Article

4 Able to extract

audit evidence

from

information

and

communication

5

• Azizah &

Wahyuni

(2022) –

Article

• Bella et al

(2022) –

Article

• Tedjasuksmana

(2021) –

Article

• NQA

Certification

(2020) –

You Tube

• Pejuang RSP

(2023) –

You Tube

5 Have IT-based

audit

certification

3

• DQS (2022) –

Online News

• Journal of

Accountancy

(2022) –

Online News

• SWA (2020) –

Online News

6 Mastering

digital

technology

9

• Agha (2021) –

Article

• Ariyanto

(2022) –

Article

• Febriyana et al

(2023) –

Article

• Minarhadi &

Trianingsih

(2022) –

Article

• Mulyandini &

Natita (2021) –

Article

• Sari & Novita

(2021) –

Article

• You r s ay.id

(2021) –

Online News

• NQA

Certification

(2021) –

You Tube

• NQA

Certification

(2020) –

You Tube

7 Understand

management

information

systems

3

• Mulyandini &

Natita (2021) –

Article

• Zhafirah et al

(2022) –

Article

• DQS (2022) –

Online News

Auditor Competency to Conduct Remote Audits

307

4.1 Two-Way Communication during

the Audit Process

Auditors now have the possibility to carry out audits

remotely thanks to the emergence of real-time two-

way online communication technology (Azizah &

Wahyuni, 2022). By utilizing technology and

communication, several stages can be carried out

remotely using information systems and technology,

such as drones, Google Meet, Zoom, and others

(Mulyandini & Natita, 2021). This remote audit

process requires examining documents uploaded and

stored on platforms such as Google Drive. These

documents are very important to assess/recheck

thoroughly because they play an important role in the

remote audit process later (RSP, 2020).

4.2 Mastering General Audit

Procedures

Remote audit procedures are generally the same as

audit procedures in general, the only difference being

that they understand technology which can help

auditors learn about the information systems that will

be used later to help make it easier to check audited

financial reports (Emkamalopek, 2021). Audits using

digital technology also support assessors if on-site

visits are not possible. Later the Auditee will

communicate with the auditor via conference services

such as Zoom or Live Streaming (Agha, 2022). It is

important for auditors to allocate sufficient time to

explain the remote audit process approach to

stakeholders. This will help anticipate gaps in

understanding, especially regarding the use of

technological tools during the audit process. These

tools may include drone cameras, remote attendance

at conferences, and obtaining necessary

authorizations for video and photography capture.

4.3 Have an Attitude of

Professionalism

When conducting remote audits, an auditor must

remain aware of his professional responsibilities,

maintain a skeptical mindset, and be careful when

carrying out tasks such as evaluating the quality of

documents or making observations in the field

(Tedjasuksmana, 2021). Based on SKPN Number 1

of 2017, the crucial aspect of being a good auditor lies

in the ability to think critically. This requires an

auditor's ability to consistently research and verify the

evidence collected during the audit (Hermina, 2022).

By checking the quality of audit results related to the

examination, an auditor still considers

professionalism as a relevant factor. Auditors can also

minimize risks that arise in the future (Zhafirah et al.,

2022)

4.4 Able to Extract Audit Evidence

from Information and

Communication

By applying information and communication

technology, auditors can conduct remote audits to

collect reliable data and assess existing internal

controls. This process involves analytical procedures

and interaction with the auditee (Tedjasuksmana,

2021). Auditors can also utilize remote audit

techniques through information and communications

technology to collect critical audit evidence and

assess compliance with audit standards without

having to be physically present at the client's location

(Azizah & Wahyuni, 2022). Drone cameras, and

other technologies involved in the audit process,

illustrate the limitations when implementing remote

audits. Anticipating differences in understanding of

these limitations is critical, therefore it is important

for the auditor to dedicate sufficient time to explain

the planned remote audit approach to stakeholders

(RSP, 2020).

4.5 Have IT based Audit Certification

Zakir explained that this remote audit is a long-

distance audit without visiting the location, either in

whole or in part by using technology (Rahayu, 2020).

Therefore, auditors are required to have certification,

even though it is the same as auditing in general,

auditors must have high performance abilities, skills

and additional levels of excellence compared to other

auditors (Konig, 2022). By using policy standards or

having certification, auditors are expected to be able

to carry out remote audits with the help of information

and communication technology and be able to carry

out two-way communication such as when holding

meetings via Zoom with auditees. Having

certification means that an auditor is able to carry out

audits from any location, but does not rule out the

possibility of still going to the location (Certification,

2021).

4.6 Mastering Digital Technology

When using digital technology, the audit will still

cover every area even if an on-site visit is not

possible. The duration of a remote audit is equivalent

to an on-site customer audit. During most audits,

auditees will be contacted via conference services

ISCP UTA ’45 JAKARTA 2023 - THE INTERNATIONAL SEMINAR AND CALL FOR PAPER (ISCP) UTA ’45 JAKARTA

308

(Febriyana et al., 2023). The use of digital technology

covers all areas that will later be inspected by

auditors, this can be done if a site visit is not possible

(Agha, 2022). The use of digital technology-based

audits aims to support assessors where site visits are

not possible (on-site). Several technologies that can

be used to carry out remote audits include an online

conference system (Skype, Google Meet, WA video

call, Webex, Zoom). Apart from that, auditors can

also use email and telephone calls (Salbiyatul, 2021)

4.7 Understand Management

Information Systems

The auditor's understanding of information

technology and the related controls that use it helps

the auditor learn more about information systems

related to financial reporting. Inspection procedures

are carried out using computers, especially in

processing relevant data using an inspection

information system (Zhafirah et al., 2022)With

remote, procedures or even entire audits are carried

out using information systems and ICT in electronic

companies, giving the effect that collecting evidence

using remote audits can improve the quality of audit

results (Mulyandini & Natita, 2021).

5

CONCLUSIONS

The results of this research have obtained answers to

the research questions posed at the beginning. There

are seven points of competency required by auditors

to be fit or competent to carry out remote audits or

remote audits. The seven competencies are: Two-way

communication during the audit process, Master

general audit procedures, Have a professional

attitude, Able to extract audit evidence from

information and communication, Have IT-based audit

certification, Master digital technology, and

Understand management information systems. The

results of this research can be implemented by

auditors so that they have adequate competence to

carry out remote audits. Research recommends seven

competencies to become a reliable auditor in the high-

tech era, where the majority of audit processes will be

carried out remotely. The implication of this research

is that auditors who conduct remote audits need to

learn seven competencies provided by the result of

this research. Apart from that, seven competencies

need to be tested quantitavely to determine what

competencies really influence the performance of

auditors conducting remote audits.

REFERENCES

Agha, R. Z. (2022). Teknik Remote Audit di Masa Pandemi

COVID-19. Ekonomi & Bisnis, 21(2), 205–214.

https://doi.org/10.32722/eb.v21i2.5632

Ariyanto, S. (2022). Pengaruh Pelaksanaan Remote Audit

Terhadap Kinerja Pemeriksa BPK Perwakilan Provinsi

Riau Selama Masa Pandemi. Journal of Islamic and

Accounting Research, 1.

https://journal.uir.ac.id/index.php/jafar

Azizah, F., & Wahyuni, N. (2022). Kemampuan Remote

Auditing dalam Meningkatkan Asersi Manajemen di

Masa Pandemi. Jurnal Riset Dan Aplikasi: Akuntansi

Dan Manajemen, 6(1), 1–16.

https://doi.org/10.33795/jraam.v6i1.001

Baatwah, S. R., & Al-Ansi, A. A. (2022). Dataset for

understanding the effort and performance of external

auditors during the COVID-19 crisis: A remote audit

analysis. Data in Brief, 42, 108119.

https://doi.org/https://doi.org/10.1016/j.dib.2022.1081

19

Basilotta, V. G. P., Matarranz, M., Casado, L.-A. A., &

Otto, A. (2022). Teachers’ digital competencies in

higher education: a systematic literature review.

International Journal of Educational Technology in

Higher Education, 19(1), 1–16.

Bhattacharjee, S., Hillison, S. M., & Malone, C. L. (2020).

Auditing from a distance: The impact of remote

auditing and supervisor monitoring on analytical

procedures judgments. Available at SSRN 3613440.

Castka, P., & Searcy, C. (2023). Audits and COVID-19: A

paradigm shift in the making. Business Horizons, 66(1),

5–11.

https://doi.org/https://doi.org/10.1016/j.bushor.2021.1

1.003

Certification, N. (2021). NQA Webinar: Preparing for your

Remote Audit (8th January 2021).

https://www.youtube.com/watch?v=PeDwgrLKusw

Crucean, A. C., & Hategan, C.-D. (2023). Impact of

Information Technology on Audit Quality: European

Listed Companies’ Evidence. In Contemporary Studies

of Risks in Emerging Technology, Part B (pp. 327–

339). Emerald Publishing Limited.

https://doi.org/10.1108/978-1-80455-566-820231018

Emkamalopek. (2021). Apa arti remote audit?

https://www.youtube.com/watch?v=0MAiTIYNdK4

Fan, K., Bao, Z., Liu, M., Vasilakos, A. V, & Shi, W.

(2020). Dredas: Decentralized, reliable and efficient

remote outsourced data auditing scheme with

blockchain smart contract for industrial IoT. Future

Generation Computer Systems, 110, 665–674.

https://doi.org/https://doi.org/10.1016/j.future.2019.10.

014

Febriyana, N., Utami, S., Armadhani, V., Nur, M., Putri, A.,

Christian, J., & Ratnawati, T. (2023). Studi Literatur:

Remote Audit. Jurnal Ilmiah Ilmu Kesehatan Dan

Kedokteran, 1(3), 108–120.

https://doi.org/10.55606/termometer.v1i3.1960

Auditor Competency to Conduct Remote Audits

309

Hafidhah, H., & Yandari, A. D. (2021). Training Penulisan

Systematic Literature Review dengan Nvivo 12 Plus.

Madaniya, 2(1), 60–69.

Hermina, A. (2022). Pengaruh Remote Auditing, Computer

Assisted Audit Techniques, dan Skeptisme Profesional

terhadap kualitas audit (Studi Empiris pada Kantor

Akuntan Publik di Wilayah Jakarta Utara). 8.5.2017,

2003–2005.

Konig, J. (2022). Remote Audit - Prasyarat, peluang, dan

batasan. https://www.dqsglobal.com/id-

id/informasi/blog/remote-audit-prasyarat,-peluang,-

dan-batasan

Li, C., Khan, A., Ahmad, H., & Shahzad, M. (2022).

Business analytics competencies in stabilizing firms’

agility and digital innovation amid COVID-19. Journal

of Innovation & Knowledge, 7(4), 100246.

https://doi.org/https://doi.org/10.1016/j.jik.2022.10024

6

Mulyandini, V. C. &, & Natita, R. K. (2021). Pendekatan

Remote Audit dan Agility Dalam Meningkatkan

Kualitas Audit Di Masa Pandemi Covid-19.

Accounthink : Journal of Accounting and Finance,

6(02), 145–157.

https://doi.org/10.35706/acc.v6i02.5400

Natow, R. S. (2020). The use of triangulation in qualitative

studies employing elite interviews. Qualitative

Research, 20(2), 160–173.

Rahayu, E. M. (2020). Sucofindo Terapkan Remote Audit

Sertifikasi.

https://swa.co.id/swa/trends/management/sucofindo-

terapkan-remote-audit-sertifikasi

RSP, P. (2020). Pelaksanaan Proses Audit Jarak Jauh

(Remote Audit).

https://www.youtube.com/watch?v=RjBoWjLkGbo

Salahudin, S., Nurmandi, A., & Loilatu, M. J. (2020). How

to Design Qualitative Research with NVivo 12 Plus for

Local Government Corruption Issue in Indonesia?

Jurnal Studi Pemerintahan, 369–398.

Salbiyatul, F. (2021). Remote Audit Pemerintahan Apakah

Efektif?

https://yoursay.suara.com/kolom/2021/07/03/150959/r

emote-audit-pemerintahan-apakah-efektif

Sitorus, R. R., & Tambun, S. (2023). Pelatihan riset

kualitatif bidang akuntansi dengan perangkat lunak

NVivo pada prodi magister akuntansi Universitas

Pendidikan Ganesha. Ruang Cendekia: Jurnal

Pengabdian Kepada Masyarakat, 2(1), 13–21.

Spencer, L. M., & Spencer, P. S. M. (2008). Competence at

Work models for superior performance. John Wiley &

Sons.

Tambun, S. (2021). Peningkatan Kemampuan Melakukan

Riset Kualitatif dengan Menggunakan Software NVivo

12 PLus di LAN Pusat Pelatihan dan Pengembangan

dan Kajian Desentralisasi dan Otonomi Daerah di

Samarinda. Jurnal Pemberdayaan Nusantara,

1(2).

Tambun, S., & Sitorus, R. R. (2023). Pelatihan Aplikasi

NVivo untuk Riset Kualitatif Bidang Akuntansi kepada

Para Peneliti di Universitas Dhyana Pura. Joong-Ki:

Jurnal Pengabdian Masyarakat, 2(1), 129–138.

Tedjasuksmana, B. (2021). Optimalisasi Teknologi Dimasa

Pandemi Melalui Audit Jarak Jauh Dalam Profesi Audit

Internal. Prosiding Senapan, 1(1), 313–323.

Zhafirah, Almira Rahma & Sukarmanto, Edi & Maemunah,

M. (2022). Pengaruh Remote Auditing terhadap

Kualitas Audit yang Dimoderasi oleh Teknologi

Informasi Audit. 2, 406–413.

https://doi.org/10.29313/bcsa.v2i1.1710

Ziprecruiter. (2023). How Much Do Remote Auditor Jobs

Pay per Hour ?

ISCP UTA ’45 JAKARTA 2023 - THE INTERNATIONAL SEMINAR AND CALL FOR PAPER (ISCP) UTA ’45 JAKARTA

310