An Empirical Study on Green Finance Promoting Industrial

Structure Upgrading Based on Econometric Model

Enlin Tang and Zebin Liu

*

School of Finance and Mathematics, Huainan Normal University, Huainan, Anhui, 232038, China

Keywords: Green Finance, Industrial Structure, VAR Mode.

Abstract: In recent years, with the rapid development of economy, global warming, ecological environment deteriora-

tion and other problems are becoming more and more serious. This paper uses the econometric model to

quantitatively analyze the green finance. Based on the analysis of the action mechanism of green finance on

the development of industrial structure and the development status of green finance and industrial structure,

this paper points out the problems existing in the development process of green finance, and uses Granger

causality test to make an empirical study on whether green finance has an impact on the development of

industrial structure.

1 INTRODUCTION

In recent years, with the increasingly serious environ-

mental problems such as global warming and air pol-

lution, most countries in the world pay more and more

attention to green finance.

Green finance refers to the

establishment of a green, low-carbon and circular

economic system through the scientific use of finan-

cial instruments such as green credit, funds and secu-

rities, combined with the development law of market

economy. Green finance is a financial activity that

supports environmental improvement and effective

utilization of resources, that is, it provides relevant fi-

nancial services such as project investment and fi-

nancing, project operation, risk management and so

on. Industrial structure is the focus of China's supply

side reform, and China's industrial structure adjust-

ment is inseparable from green finance. The govern-

ment continues to launch green finance policies to

guide funds from high energy consumption and high

pollution industries to green industries, encourage

and support enterprises to increase investment in

green industries, which can not only improve their

competitiveness in the industry from the perspective

of enterprise development, it can also promote the de-

velopment of green finance and the upgrading and op-

timization of industrial structure from a macro per-

spective (Ma, 2016). Therefore, based on the analysis

of the current development status of China's green fi-

nance and industrial system structure, this paper

points out the problems existing in the development

of China's green finance, further studies how green

finance affects the industrial structure, makes an em-

pirical analysis, and puts forward policy suggestions

to optimize the industrial structure through the devel-

opment of green finance.

2 AN EMPIRICAL ANALYSIS OF

THE IMPACT OF GREEN

FINANCE ON INDUSTRIAL

STRUCTURE

2.1 Selection of Empirical Methods

Vector Autoregressive Model is a model based on the

statistical nature of data. It is a model constructed by

the regression of current variables to lag variables. It

is used to explain the impact of various economic

shocks on economic variables. This paper studies the

impact of Green Finance on the development of in-

dustrial structure, so VAR is more appropriate here.

The mathematical expression of model VAR(p) is as

follows:

𝑦𝑡 = 𝜙𝑦𝑡 − 1+⋯ + 𝜙𝑝𝑦𝑡 − 𝑝 + 𝐻𝑥𝑡 + 𝜀𝑡, 𝑡 =

1,2, ⋯ , 𝑇 (1)

In Formula (1), Ky

t

represents the k-dimensional

endogenous variable column vector, Xt represents the

534

Tang, E. and Liu, Z.

An Empirical Study on Green Finance Promoting Industrial Structure Upgrading Based on Econometric Model.

DOI: 10.5220/0011751500003607

In Proceedings of the 1st International Conference on Public Management, Digital Economy and Internet Technology (ICPDI 2022), pages 534-537

ISBN: 978-989-758-620-0

Copyright

c

2023 by SCITEPRESS – Science and Technology Publications, Lda. Under CC license (CC BY-NC-ND 4.0)

column vector of d-dimensional exogenous variables,

p represents the lag order, T represents the number

of samples, and K∗k-dimensional matrix 𝜙1,…,𝜙𝑝

and k ∗ d dimensional matrices H refer to the coef-

ficient matrix to be estimated. 𝜀

represents the k-di-

mensional perturbation column vector, and the rela-

tionship between them can be correlated at the same

time. However, it is not related to their own lag value,

and it is not related to the variables on the right side

of the equation. Suppose Σ is the covariance matrix

of

t

ε

, which is a positive definite matrix of k∗k. The

expansion of equation 1 can be expressed as:

1

111 11

2

221 22

1

1

,1,2,,.

tp

tt tt

tp

tt tt

p

kt p

kt kt dt kt

y

yy x

y

yy x

H

TT

y

yy x

ε

ε

φφ

ε

−

−

−

−

−

−

=++ ++=

(2)

That is, the VAR(p) model with k time series

variables consist of k equations (Ma, Wang, Dong,

2007; Gao, Gan, 2012).

2.2 Index Selection and Data Source

Here, we choose the green credit of financial institu-

tions to measure the scale of China's current green fi-

nancial development. Since the CBRC has only dis-

closed the green credit situation of 21 major financial

institutions since 2013, which is updated every half

year, the selected range of data here is from 2013 to

2020. We take the ratio of the green credit balance of

21 Financial Institutions disclosed by the CBRC to

the RMB loan balance as an indicator to measure the

scale of green financial development in China. The

symbols and specific meanings of green finance indi-

cators and industrial structure upgrading indicators

are shown in Table 1.

The industrial classification

methods mentioned in the above theory mainly in-

clude the intensive degree classification of production

factors and the traditional three industrial classifica-

tion. Because the data acquisition required by the in-

tensive degree classification of production factors is

difficult, and the traditional three industrial classifi-

cation can more intuitively and clearly reflect the evo-

lution of industrial structure, and

the data acquisition

is less difficult. Therefore, the traditional three indus-

try classification method is adopted here, and the pro-

portion of the added value of the secondary industry

and the tertiary industry in GDP is selected to meas-

ure the development of China's overall industrial

structure.

Table 1: Empirical indicators and their symbols and meanings.

Variable

type

Variable

name

Sym-

b

ol

Specific meaning

Green

financial

indicators

Green

credit ratio

GF

Green credit bal-

ance/ RMB loan

balance

Industrial

structure

upgrading

index

Industrial

structure

upgrading

TID

(Added value of

secondary industry

+ Added value of

tertiary industry)

/GDP

3 AN EMPIRICAL TEST OF

GREEN FINANCE

PROMOTING INDUSTRIAL

STRUCTURE UPGRADING

3.1 Unit Root Test

The stability test of variables GF and TID is the prem-

ise of empirical test, while ADF test is widely used in

China with high accuracy. Therefore, this paper uses

ADF test to test the stability of green financial indi-

cators and industrial structure indicators. The results

are shown in tables 2 and 3 below.

Table 2: Test results of GF stationarity of variables.

Method Statistic Prob**

ADF-Fisher Chi-square 10.4576 0.0054

ADF-Choi Z-stat -2.55170 0.0054

Intermediate ADF test results D(GF,2)

Series Prob Lag Max Lag Obs

D(SER01,2) 0.0054 0 0 6

Table 3: Test results of variable TID stationarity.

Method Statistic Prob**

ADF-Fisher Chi-square 19.37804 0.0001

ADF-Choi Z-stat -3.83853 0.0001

Intermediate ADF test results D(TID,2)

Series Prob Lag Max Lag Obs

D(SER02,2) 0.0001 0 0 6

The results of stationarity test show that the ADF

statistical value of the second-order difference of GF

vector and TID vector is lower than 1%, which indi-

cates that the second-order difference of GF vector

and TID vector is significant at the 1% level, and the

An Empirical Study on Green Finance Promoting Industrial Structure Upgrading Based on Econometric Model

535

negation of the original assumption at the 99% confi-

dence level indicates that it is a stable sequence.

3.2 Determining The Lag Order

After the stationarity test, the lag order of each varia-

ble needs to be determined. The operation results of

EViews are shown in Table 4. According to Akaike

information criterion (AIC) and Schwarz criterion

(SC), AIC, SC and HQ are the minimum when the lag

order is 2, so it can be determined that the optimal lag

order is 2.

Table 4: EViews operation results of variable lag order.

Lag LogL LR FPE AIC SC HQ

0 78.76521 NA*

1.03e-

12

-21.93292 -21.94837 -22.12393

1 86.39534 8.720150

4.08e-

13*

-22.97010 -23.01646 -23.54313

2 92.23880 3.339124

4.43e-

13

-

23.49680*

-

23.57407*

-

24.45186*

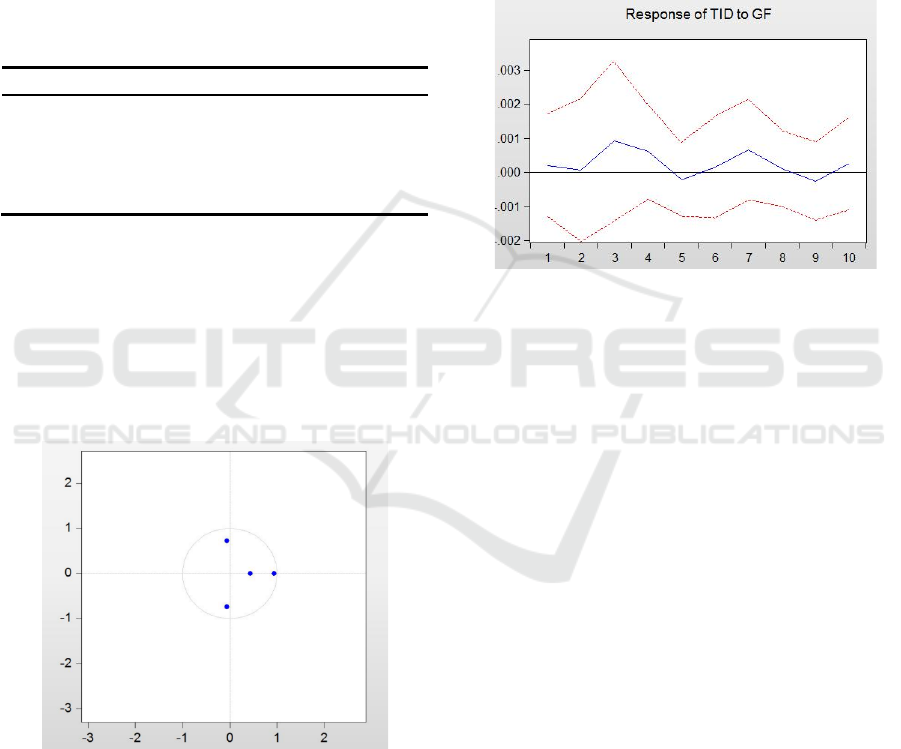

3.3 Stability Test

The stability test of VAR model is the premise of im-

pulse response function analysis. According to the

stability analysis of VAR model constructed by the

above variables, the results in Figure 1 show that the

reciprocal of unit eigenvalue of VAR model is in the

unit circle, indicating that the VAR model is stable.

Figure 1: Inspection diagram of AR root.

3.4 Impulse Response Function

Analysis

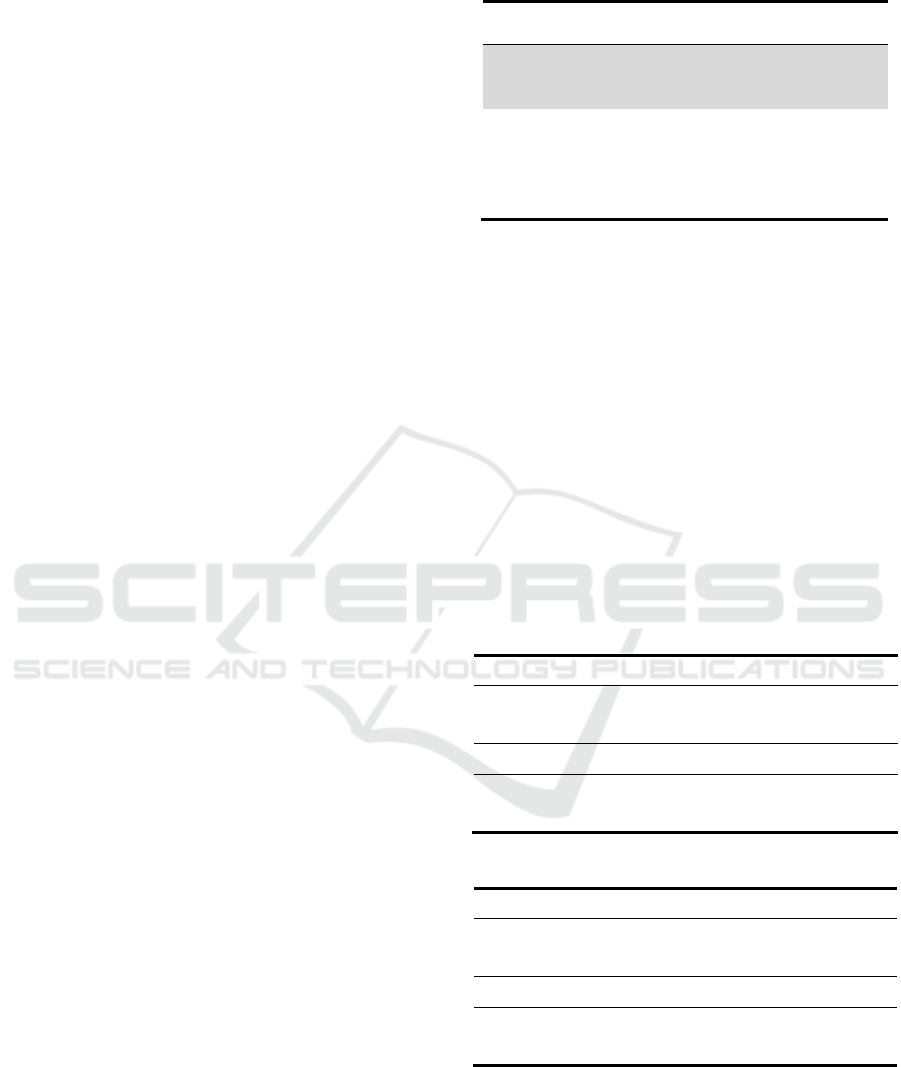

Figure 2 shows the impulse response function of in-

dustrial structure upgrading to green finance.

Through the observation of the function diagram, it

can be found that after the external impact of a stand-

ard deviation is applied, the pulse response character-

istics of industrial structure upgrading to green fi-

nance are as follows:

From the beginning to the third period, the impact

of industrial structure upgrading on green finance

gradually increased and reached the peak in the third

period. From the third period to the fifth period, it

showed a downward trend, and from the fifth period,

it showed a first upward and then downward trend

again.

Figure 2: Impulse response function of TID to GF.

4 CONCLUSION

Through theoretical analysis, it is concluded that

green finance mainly affects industrial institutions

through capital formation mechanism, capital-ori-

ented mechanism and information disclosure mecha-

nism. Through data collection and analysis, the cur-

rent situation of China's green finance development

and industrial structure development is revealed, and

on this basis, the problems faced by green finance to

promote the development of industrial structure are

obtained. The empirical research shows that there is a

significant causal relationship between the develop-

ment of green finance and the upgrading and optimi-

zation of industrial structure. That is to say, China can

promote the optimization of industrial structure

through the implementation of green finance policies,

thus making the economic development model

change from the traditional extensive model to the en-

ergy saving and environmental protection model. On

this basis, the specific policies and opinions on the

development of green finance to promote the upgrad-

ing of industrial structure are given from 4 aspects,

including the understanding of green finance at a

higher level, the improvement of green financial sys-

tem, the establishment of incentive and restraint

ICPDI 2022 - International Conference on Public Management, Digital Economy and Internet Technology

536

mechanism, and the increase in the training of green

financial professionals.

ACKNOWLEDGEMENT

This work is supported by Key Project of Humanities

and Social Sciences of Anhui Provincial Department

of Education (SK2020A0405), Support Project for

Outstanding Young Talents in Colleges and Univer-

sities of Anhui Province in 2022 (gxyq2022065),

Huainan Normal University Research Projects

(2021XJYB005), Huainan Guiding Projects of Sci-

ence and Technology (2021062).

REFERENCES

Gao Kuo,Gan You-qing. Dynamic analysis on the fluctua-

tion of pig price and production factor price in China

[J]. Statistics and Decision,2012, (5): 132-134.

Li Zhong. Research on green financial innovation and Chi-

na's industrial transformation [J]. Contemporary Eco-

nomics,2011(24):98-100.

Ma Jun. The Evolution of and Prospect for Green Finance

in China [J]. Comparative Economic and Social Sys-

tems,2016, (06):25-32.

Ma Xiao-bin, Wang Ting, Dong Xia. Application of vector

autoregressive method in pig price prediction [J]. Chi-

nese Journal of Animal Science,2007, (23):4-6.

Rao Shu-ling, Chen Yin, Ma Jun. Develop green finance in

depth [J]. Chinese Finance,2018, (18):55-56.

An Empirical Study on Green Finance Promoting Industrial Structure Upgrading Based on Econometric Model

537