Rolling Stock Leasing: Accounting and Economic Security Issues

Alexey Popov

1a

and Lidiia Chernishova

2b

1

Ural State University of Economics, Yekaterinburg, Russian Federation

2

Ural State University of Railway Transport, Yekaterinburg, Russian Federation

Keywords: Rolling stock, lease, right to use an asset, lease obligation, investment in lease, accounting, economic security.

Abstract: The article solves the problems of disclosing the methodology of accounting for rental of rolling stock by the

lessee and the lessor in accordance with the new federal accounting standard 25/2018 "Lease accounting",

and also highlights the peculiarities of the impact of rental accounting objects on the indicators of economic

security of enterprises. The issues of recognition of lease accounting items depend on the classification of

leases, which is given in this article with the allocation of key features of operational and non-operational

(financial) leases. The general principles of lease accounting have been adapted to the specifics of rolling

stock operations. The principles of formation of rolling stock rental accounting objects are highlighted: rights

to use wagons and containers, lease obligations, rental investments and interest income and expenses. For

each object, the rules of initial and subsequent evaluation, recognition and write-off are given. The subject of

accounting issues and further directions of scientific research is developed in terms of developing

methodological tools for the application of this FSB: making changes to the Chart of Accounts, updating

accounting forms. The ways of the influence of asset use rights, lease obligations, lease investments and

interest income and expenses generated in the reporting on financial indicators of economic security of

organizations: liquidity, profitability, financial stability with the formulation of proposals for leveling threats

of insolvency and deterioration of financial condition are formulated.

1 INTRODUCTION

Modern economic conditions dictate the

requirements for establishing stable supplies of goods

and restoring disrupted logistics chains during the

period of global economic sanctions. In the current

reality, the issues of renting rolling stock in order to

fulfill the conditions of supply and to meet the needs

of the production activities of economic entities and

the population with the necessary products are of

particular importance. As G.B. Titov notes, "the task

of managing the structure of the rolling stock fleet

(purchase, sale, rental and leasing of wagons) under

the influence of constantly changing demand for

transportation for a railway company is practically

impossible due to the technological

interconnectedness of autonomous participants in the

railway transportation market." (Titov, 2010)

However, in order to make sound economic

decisions, logistics business entities need accurate

a

https://orcid.org/0000-0002-2200-0568

b

https://orcid.org/0000-0003-0784-3046

and reliable information about the effectiveness of

their activities, including rolling stock rental

operations, which is formed in accounting and

financial statements. At the same time, in the

conditions of the program for the development of new

FSB and the adaptation of domestic accounting rules

to modern requirements, these issues become

particularly relevant. General economic and legal

issues of rolling stock rental are considered in their

works by A.A. Alferova (Alferova, 2020), A.I.

Timofeev (Timofeev, 2020), O.N. Glyadysheva

(Gladysheva, 2022) and others. The accounting

component of the rental of rolling stock is analyzed

by Tarasova T.M. (Tarasova, 2011), Gosteeva O.V.

(Gosteeva, 2013), Gorodilov M.A. (Gorodilov,

2020), Ivanenkova Ya.A. (Ivanenkova, 2020) and

others. At the same time, these works are mainly

based on the provisions of regulatory documents in

force before the entry into force of FSB 25/2018

"Lease Accounting" from 2022. The issues of the

application of the new "Lease" standard that has

Popov, A. and Chernishova, L.

Rolling Stock Leasing: Accounting and Economic Security Issues.

DOI: 10.5220/0011581200003527

In Proceedings of the 1st International Scientific and Practical Conference on Transport: Logistics, Construction, Maintenance, Management (TLC2M 2022), pages 175-180

ISBN: 978-989-758-606-4

Copyright

c

2023 by SCITEPRESS – Science and Technology Publications, Lda. Under CC license (CC BY-NC-ND 4.0)

175

entered into force and its introduction into accounting

practice have already been covered by a number of

researchers, in particular Plotnikov V.S. (Plotnikov,

2019), Lisovskaya I.A. (Lisovskaya, 2019),

Druzhilovskaya E.S. (Druzhilovskaya, 2019), and

others. However, these developments do not affect

the specifics of the transport industry. Of scientific

interest is also the foreign experience of economic

research in the field of vehicle rental, described in

particular by Miao R. (Miao, 2022), Long Yu. (Long,

2018), Roy D. (Roy, 2014) and others. In addition,

when carrying out rolling stock rental activities, close

attention should be paid to economic security issues

in order to reflect potential threats to the activities of

modern economic entities. These prerequisites

confirm the relevance of the chosen research topic

and determine its purpose – theoretical and

methodological substantiation of the methodology of

accounting for rental of rolling stock and assessment

of the impact of rental accounting objects on the

economic security of organizations acting as parties

to a rolling stock lease agreement. Achieving this goal

requires solving a number of tasks, including

identifying existing accounting problems and

assessing the economic security of rolling stock rental

operations, offering recommendations on improving

accounting methods and reporting on these

operations, as well as identifying measures aimed at

strengthening the economic security of economic

entities in the transport industry in order to ensure

sustainable development.

2 MATERIALS AND METHODS

In the course of scientific work, empirical methods of

scientific research were used, in particular, a review

of the legal and economic foundations of the rolling

stock lease agreement was conducted, which have a

significant impact on the methodology of accounting

for rental operations. When developing the

methodology, the classification method was used in

terms of the allocation of operating and financial

leases, the accounting procedure of which has

fundamental differences.

In addition, in order to achieve the goal of the

work, methods of theoretical research were used, in

particular, a detailed analysis of the provisions of FSB

25 was carried out with the identification of key

features of the formation of objects of accounting for

operating and financial leases: rights to use rolling

stock, lease obligations, lease investments, interest

income and expenses, the adaptation of the norms of

the standard to the principles of rolling stock lease

was carried out. Extrapolation and induction methods

were used to implement this adaptation. Analogies

were also made on a number of scientific issues, in

particular, proposals for calculating depreciation of

the rights to use an asset similarly to fixed assets, and

in addition, an abstraction method was used to justify

the impact of lease accounting objects on indicators

of economic security of enterprises and organizations.

This justification is built using deduction, which

allows you to decompose financial security indicators

into components and identify the nature of the impact

of rental operations on them.

3 RESULTS AND DISCUSSION

To substantiate the methodology of accounting for

rental operations, it is necessary to formulate the legal

and economic features of rolling stock rental

considered in the works of the above-mentioned

scientists (Titov, 2010; Alferova, 2020; Timofeev,

2020; Gladysheva, 2022), which, in particular, are

established in the letter of the Federal Tax Service of

the Russian Federation dated 04.06.2008 N SHS-6-

3/407@ "On the direction of the Letter of the Ministry

of Transport of the Russian Federation dated

20.05.2008 N CA-16/3729" together with the

specified letter. According to it, "the purpose of the

rolling stock lease agreement is to obtain temporary

possession and use of wagons and containers. The

lessee may use the wagons and containers transferred

to him at his discretion, both for transportation and

for other purposes (for example, temporary storage of

goods).

The subject of the rolling stock lease agreement

are individually defined wagons and containers (the

contracts specify the numbers of wagons and

containers to be leased).

The rental fee for rolling stock is not tied to a

specific transportation in any way and is calculated

based on the number of days the rental object is with

the lessee. The lease term is also not tied to a specific

transportation and is calculated by agreement of the

parties (usually months or years)".

With regard to the accounting of rental of rolling

stock, it is necessary to note the need to revise the

accounting policy of an economic entity in

connection with the entry into force of the Order of

the Ministry of Finance of the Russian Federation

dated 16.10.2018 N 208n "On approval of the Federal

Accounting Standard FSB 25/2018 "Lease

Accounting".

The specified Standard is applied by the parties to

lease (sublease) agreements, as well as other

TLC2M 2022 - INTERNATIONAL SCIENTIFIC AND PRACTICAL CONFERENCE TLC2M TRANSPORT: LOGISTICS,

CONSTRUCTION, MAINTENANCE, MANAGEMENT

176

agreements, the provisions of which, individually or

in conjunction, provide for the provision of property

for temporary use by the lessor, leasing company,

rightholder, or other person for a fee to the lessee,

leaseholder, user, or other person.

For the application of the standard, the

identification of the rental object must be made, in

particular, as stated by FSB 25, the accounting object

is classified as rental accounting objects with the one-

time fulfillment of the conditions of paragraph five of

the said regulatory act, including:

− there is a fact that the lessor provides the rental

item to the lessee for a certain period of time;

− the rental item can be appropriately identified,

i.e. its characteristics are precisely indicated in

the contract, but neither the terms of the

contract nor the business practices provide for

the right of the lessor to change the rental item

to another or similar one by his decision at a

given moment throughout the term of the

contract;

− availability of the lessee's rights to receive

economic benefits from the use of the rental

item during the period of the lease agreement;

− the unconditional right of the lessee to

determine the purpose of using the rental item

at his discretion, if this purpose is not

determined by the technical characteristics of

the rental item. (Gorodilov, 2020)

In order to disclose the methodology of

accounting for the lease of rolling stock, it is

necessary to classify the lease in accordance with

FSB 25/2018, which is shown in Figure 1.

In addition, Paragraph 11 of FSB 25/2018 allows

the lessee to treat the lease as an operating one in any

of the following cases:

− the rental period does not exceed 12 months;

− the market value of the rental item does not

exceed 300,000 rubles, which can be typical

only for extremely worn-out rolling stock;

− the lessee refers to small business entities and

other economic entities that have the rights to

use simplified methods of accounting and

financial reporting. (Plotnikov, 2019)

With regard to the accounting of rolling stock

rental operations, if the lease is recognized as

operating, a comparison of the norms of the FSB

25/2018 put into effect with the accounting procedure

previously in force, in particular, provided for by the

Accounting Regulations, the Chart of Accounts, etc.

The basic accounting principles are presented in table

1.

With regard to finance leases, the new accounting

standard provides for a fundamentally new procedure

based on the provisions of IFRS 16 "Leases".

The lessee recognises the leased rolling stock as

the right to use the asset with simultaneous

recognition of the lease obligation. The assessment of

the right to use the asset (rolling stock) is made at the

actual cost, including the amount of the lease

obligation and the costs associated with the receipt of

the object.

The lease obligation is estimated as the sum of the

present value of lease payments payable for the entire

term of the contract based on the discount rate at

which the total amount of payments planned under

the contract corresponds to the fair value of the rolling

stock (Ivanenkova, 2020). At the same time, the

Lease: Operating Non-operating (financial)

Defi

nitio

a lease that provides for the retention of risks and

benefits for the lessor due to the lessor's

ownership of the rolling stock

a lease that provides for the transfer of economic benefits and risks

arising from the lessor's ownership of the rolling stock to the lessee

Classification features

- the lease term is significantly shorter and

incomparable with the period during which the

rental item will remain usable;

- the subject of lease are objects having an

unlimited period of use, the consumer properties

of which do not change over time;

- at the date of provision of the lease item, the

present value of future lease payments is

significantly less than the fair value of the lease

item;

- another circumstance indicating that the

economic benefits and risks arising from the

ownership of the rental item are borne by the

lessor.

- the terms of the lease agreement provide for the transfer of

ownership rights to the lessee;

- the lessee has the right to purchase the rental item at a price

significantly lower than its fair value at the date of realization of this

right;

- the lease term is comparable to the period during which the rental

item will remain usable;

- at the date of conclusion of the lease agreement, the present value of

future lease payments is comparable to the fair value of the leased

item;

- only the lessee has the opportunity to use the rental item without

significant changes;

- the lessee has the opportunity to extend the lease term established

by the lease agreement with a rent significantly lower than the market;

- another circumstance indicating the transfer of economic benefits

and risks to the lessee due to the lessor's ownership of the rental item.

Figure 1: Classification of rental of rolling stock for the purposes of application of FSB 25/2018.

Rolling Stock Leasing: Accounting and Economic Security Issues

177

problems of fair value assessment are dealt with in

accordance with IFRS 13 and are beyond the scope of

this study.

The cost of the right to use the rolling stock is

repaid by depreciation. In order to calculate

depreciation, the useful life of the right of use, as a

rule, should not exceed the lease term, unless the

transfer of ownership of the rolling stock to the lessee

is assumed. The lessee chooses the depreciation

method by analogy with the depreciation of fixed

assets in accordance with FSB 6/2020, in particular,

the most common is the linear method and the method

proportional to the volume of transportation in kind.

The amount of the lease obligation after its

recognition increases by the amount of accrued

interest calculated using mathematical methods or

based on expert assessment discount rate and

decreases by the amount of actually paid lease

payments. Accrued interest according to the general

rules is included by the lessee in other (financial)

expenses in accordance with PBU 15/2008

(Accounting Standards), except in the case of using a

rolling stock to create another investment asset, i.e. an

object that requires a long time or significant costs for

its acquisition, construction or manufacture.

By the time the lease agreement is completed, the

cost of the right to use the rolling stock usually

corresponds to the liquidation value, and the

obligation must be fully repaid. Accordingly, the

specified liquidation value is written off at the

expense of the estimated liability formed upon

recognition of the right to use rolling stock, and in

case of its insufficiency - as part of other expenses. If

the ownership of the rolling stock passes to the lessee,

then he makes notes in the analytical accounting on

the accounts of fixed assets and depreciation, which

took into account the corresponding right to use the

rolling stock and its depreciation.

The lessor, upon the entry into force of the lease

agreement and the transfer of wagons to the lessor,

writes off the rolling stock from the balance sheet and

recognizes the investment in the lease as an asset.

An investment in a lease is estimated at its net

value, which is determined by discounting its gross

value at an interest rate at which the present gross

value is equal to the sum of the fair value of the rolling

stock and the costs incurred by the lessor in

connection with the lease agreement. (Popov, 2021)

The net value of the investment in the lease

increases by the amount of accrued interest and

decreases by the amount of actually received lease

payments. (Popov, 2021)

Interest accrued on investment in the lease is

recognized by the lessor as income, while also the

specified income should be classified either as

revenue or other income, depending on the subject of

activity.

In addition, Standard 25 provides for the lessor's

obligation to check the net value of the investment in

the lease for its impairment in accordance with IFRS

36 "Impairment of assets".

When the rolling stock is returned to the lessor,

wagons and containers are accepted for accounting as

fixed assets with simultaneous write-off of the

remaining net value of the investment in the lease,

and in the case of transfer of ownership to the lessee,

the investment in the lease is subject to write-off as

part of other expenses if it was not fully repaid.

The methodology for assessing the economic

security of enterprises engaged in rental operations

with rolling stock is based on the general principles

formulated by Podmolodina I.M. (Podmolodina,

2012), Esembekova A.Yu. (Esembekova, 2016),

Mironova O.A. (Mironova, 2015) and others. As

noted by S.E. Metelev, "the most important tasks of

railway transport are to ensure the stable operation of

railways, accessibility, high quality of services

provided, reduction of total economic costs for the

transportation of passengers and cargo, satisfaction of

growing solvent demand. The solution of these tasks,

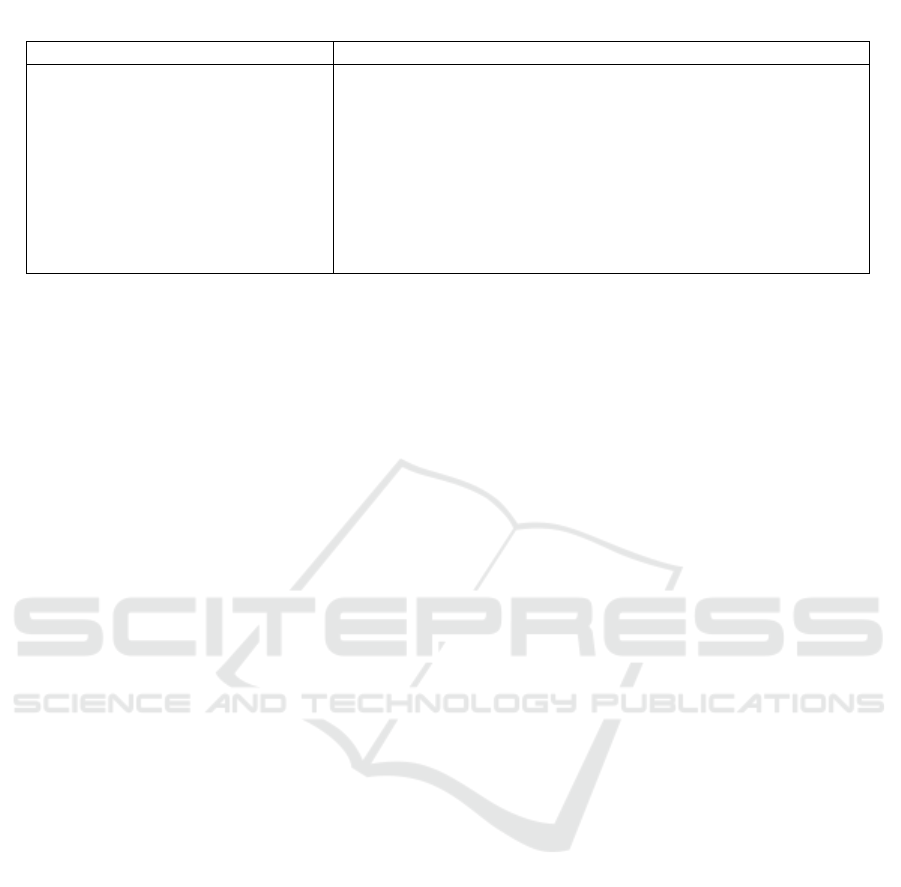

Table 1: Methodology of accounting for operations on operating lease of rolling stock

Lessee Lessor

The rental item is accepted by the lessee

to the off-balance sheet account 001 in

the assessment provided for by the

contract.

The lessee of rolling stock recognizes

lease payments as an expense on a

straight-line basis over the lease term or

on the basis of another systematic

approach reflecting the nature of the

lessee's use of economic benefits.

The lessor of the rolling stock does not change the previous accepted

accounting procedure for the asset in connection with its lease, except

for changes in estimated values, i.e. continues to take into account

wagons and containers as part of fixed assets, only a revision of the

period of use, depreciation method and other parameters is possible.

Operating lease income is recognized on a straight-line basis or on the

basis of another systematic approach reflecting the nature of the lessee's

use of the economic benefits of the leased item. Depending on the

subject matter of the owner of the wagons, these revenues are recognized

as either revenue or other income.

TLC2M 2022 - INTERNATIONAL SCIENTIFIC AND PRACTICAL CONFERENCE TLC2M TRANSPORT: LOGISTICS,

CONSTRUCTION, MAINTENANCE, MANAGEMENT

178

ultimately, provides the transport component of

national economic security". (Metelev, 2006)

The most important group in the structure of

indicators of economic security of enterprises are

financial indicators, which are emphasized in this

paper.

The first indicator is the absolute liquidity ratio,

defined as the ratio of cash and cash equivalents to the

amount of short-term liabilities. According to the

FSB 25 methodology, the current part of the lease

obligation, including accrued interest, is included in

the short-term obligations of the lessee of the rolling

stock, respectively, the presence of this obligation

reduces liquidity.

The next indicator is the current liquidity ratio

(coverage ratio), determined by the ratio of current

assets to the value of short-term liabilities. In this

case, the specified indicator of the lessee, in addition

to the lease obligation, is influenced by the amount of

accrued depreciation of the right to use rolling stock

and accrued interest on the lease obligation, since in

the case of using rolling stock for the purpose of

creating investment assets, which include, in

particular, work-in-progress, the specified

depreciation and interest are included in the cost of

inventories, accordingly, the current liquidity ratio

due to these interest rates can be increased in a certain

way.

Profitability indicators determine the efficiency of

companies and their economic security, which,

depending on the type of profitability, are calculated

by the ratio of profit to revenue, cost, balance sheet

currency and other indicators. In this case, the impact

of lease accounting objects on the economic security

of the lessee of the rolling stock can be disclosed

using factor analysis, since, as indicated above,

depreciation of the right to use the asset and interest

on the lease obligation are included in the cost and

expenses, which reduces the company's profit

(negative impact), also in the case of calculating the

return on assets, if by increasing the amount of the

right to use the asset, profitability decreases. The

nature of the influence of interest on the lease

obligation on the coefficient of security of interest

payable is similar.

An important group of indicators are indicators of

financial stability, in particular the financial

independence coefficient, determined by the ratio of

equity to the balance sheet currency and the level of

financial leverage calculated by the ratio of long-term

liabilities to equity. According to these groups of

factors, the presence of lease accounting objects in the

form of lease obligations also has a negative impact,

since these lease obligations are included in long-term

liabilities, increasing the share of borrowed capital

and increasing the balance sheet currency without

creating corresponding assets and leading to an

increase in expenses.

Thus, taking into account the predominantly

negative nature of the impact of rental accounting

objects on the indicators of economic security of the

lessee of rolling stock, it is necessary to consider

options for assessing the effectiveness of the

acquisition of rolling stock from appropriate sources

in order to reflect the threats of insolvency. To make

a decision on the acquisition or lease of rolling stock,

a recommendation may be proposed for calculating a

financial cash flow model based on discounted value

and calculating the NPV (net present value) indicator.

For the lessor of rolling stock, the presence of an

asset in the balance sheet - an investment in lease does

not have a fundamental impact on economic security

indicators, since this investment is formed by

retraining other types of non-current assets. The

recommendation for strengthening economic security

in this case is the calculation and comparison of the

efficiency of using rolling stock in its own transport

and logistics activities and use by leasing also based

on the analysis of the cash flows generated by the

specified rolling stock.

4 CONCLUSION

Thus, the results of the study made it possible to

formulate a number of conclusions and proposals in

accordance with the designated goal. At the moment,

there is a need to develop methodological tools for

assessing rental accounting objects in accordance

with FSB 25/2018, as well as for applying the

discount rate, since the provisions of the standard

disclose general approaches, but do not contain the

necessary tools for correctly reflecting rolling stock

rental operations. The chart of accounts should be

adapted to the application of FSB 25/2018, in

particular, accounts should be entered into it to

account for the rights to use the asset, lease

obligations and lease investments. Changes should

also be made to the financial reporting forms, in

particular, the articles Right to use the Asset,

Investments and Leases should be included in the

composition of non-current assets, and the article

Lease obligations should be included in the

composition of long-term liabilities. These

developments should be attributed to further areas of

scientific research that allow us to form better and

more analytical financial information for making

investment and financial decisions.

Rolling Stock Leasing: Accounting and Economic Security Issues

179

The indicator approach to assessing the level of

financial security of the enterprise and the analysis of

the financial condition is also subject to clarification,

since the financial coefficients provided for by

generally accepted methods do not take into account

the specifics of the new objects introduced into

accounting practice. One of the directions of further

scientific research in the field of strengthening the

economic security of subjects of the transport

industry is risk hedging, analyzed in particular by

M.V. Leshchev (Leshchev, 2015) The development

of these areas will allow the appropriate interpretation

of financial information regarding logistics and

manufacturing companies participating in the rolling

stock lease agreement, which will allow them to

reflect threats to economic security and comply with

the vector of sustainable development.

REFERENCES

Titov, G. B., 2010. Economic methods of managing the

process of modification of universal rolling stock.

Moscow State University of Railway Engineering

(MIIT) Ministry of Railways of the Russian Federation.

Alferova, A. A., 2020. Freight car rental and its impact on

the competitiveness of railway transport. Topical issues

of the economy of high-speed transport. pp. 8-11.

Timofeev, A. I., Gulenko, P. I., 2020. The economic aspect

of the decision to replace rolling stock in suburban

traffic. Actual problems of development of industry

markets: national and regional level. pp. 100-102.

Gladysheva, O. F., Severova, M. O., 2022. Analysis of the

effectiveness of locomotive rental services on non-

public tracks. Biological sciences, p. 89.

Tarasova, T. M., 2011. Management accounting and

internal control of the activities of rolling stock

operators.

Gosteeva, O. V., 2013. Reflection of the accounting of the

rolling stock of a transport company in different

conditions of commercial use when applying IFRS.

Bulletin of the University. 4. pp. 99-102.

Gorodilov, M. A., Kadochnikova, A. V., 2020.

Development of the theory and methodology of lease

accounting in accordance with International Financial

Reporting Standards.

Ivanenkova, A. Ya., Buintseva, Yu. M., 2020. Analysis of

the company's income from the rental of rolling stock

in the context of changes in the methodology of their

formation. European Journal of Natural History. 4. pp.

68-72.

Plotnikov, V. S., Plotnikova, O. V., 2019. FSB 25/2018

"Lease Accounting" and IFRS 16 "Lease": comparative

analysis of the main provisions. Account. Analysis.

Audit. 6 (6). pp. 42-51.

Lisovskaya, I. A., Trapeznikova, N. G., 2019. Complex

issues of application of FSB 25/2018 "Lease

accounting". International Accounting. 22 (11). pp.

1208-1222.

Druzhilovskaya, E. S., 2019. Examples of lease accounting

according to FSB 25/2018. Accounting. 6. pp. 18-26.

Miao, R., Guo, P., Huang, W., Li, Q., Zhang, B., 2022.

Profit model for electric vehicle rental service:

Sensitive analysis and differential pricing strategy.

Energy. 249. 123736.

Long, Y., Sun, H., Zhu, B., Wang, H., Xu, T., Wang, J.,

2018. Design and Implementation of Virtual Service

System of Electric Vehicle Time-Sharing Rental Based

on Multi-Agent Technology. 5th International

Conference on Information Science and Control

Engineering (ICISCE). pp. 1104-1107.

Roy, D., Pazour, J. A., De Koster, R., 2014. A novel

approach for designing rental vehicle repositioning

strategies. IIE Transactions. 46 (9). pp. 948-967.

Popov, A. Yu., 2021. Rental investments in the conditions

of new industrialization: issues of identification,

assessment and economic security. The new

industrialization of Russia: economics-science-man. p.

176.

Podmolodina, I. M., Voronin, V. P., Konovalova, E. M.,

2012. Approaches to assessing the economic security of

enterprises. Bulletin of the Voronezh State University of

Engineering Technologies. 4. pp. 156-161.

Esembekova, A. U., Borovinsky, V. A., Pavlutskikh, M. V.,

2016. Methodology for assessing the level of economic

security of organizations. Finance and Management. 2.

pp. 62-70.

Mironova, O. A., 2015. Economic security: problems and

ways to ensure it. Economy. Taxes. Law. 1. pp. 79-83.

Metelev, S. E., 2006. National security and development

priorities of Russia: socio-economic and legal aspects.

Omsk Institute (branch) of State Educational Institution

of Higher Professional Education "Russian State

University of Commerce and Economics". p. 224.

Leshchev, M. V., 2015. Methods of hedging risks when

operating a rolling stock fleet on railway transport and

ensuring the sustainable development of business

structures. Transport business of Russia. 2. pp. 121-

125.

TLC2M 2022 - INTERNATIONAL SCIENTIFIC AND PRACTICAL CONFERENCE TLC2M TRANSPORT: LOGISTICS,

CONSTRUCTION, MAINTENANCE, MANAGEMENT

180