Status and Trends in Transboundary Carbon Management

Ruslan Batashev, Amir Bisultanov and Iman Pedayeva

Kadyrov Chechen State University, Grozny, Russia

Keywords: Transboundary carbon regulation, European Union, challenges, consequences, Russian Federation.

Abstract: Currently, the human environment associated with the consumption of energy, carbon-intensive products, is

one of the most pressing problems in the implementation of climate programs in various countries. The

introduction of a carbon pricing mechanism is the most fundamental tool for solving the problem of reducing

greenhouse gas emissions. The plan announced by the Union to introduce a mechanism to address the issue

of carbon pricing of an international nature, while avoiding additional risks and challenges for the cross-

border energy-intensive economy. The purpose of the article is to study trends in the field of cross-border

carbon regulation, to identify possible negative consequences for Russian producers of carbon-intensive

products.

1 INTRODUCTION

The main trend in the implementation of the program

aimed at reducing greenhouse gas emissions into the

atmosphere is set by the European Union. The data

published by some independent international research

companies show negative trends in the impact of

industrial production on the ecosystems of various

countries and regions. Thus, in mid-2021, the

contribution of the European Union economy to the

volume of carbon dioxide emissions into the

atmosphere amounted to 881 million tons. This is

slightly lower than the volumes recorded before the

start of the COVID-19 crisis. These data were

published by Eurostat at the beginning of 2022.

If we consider the structural composition of

greenhouse emissions by sectors of the economy in

the countries of the European Union, it can be seen

that the manufacturing industry accounts for up to

23% of emissions, electricity supply - 21%.

Households and agriculture in European countries

together account for up to 28%. The positive

dynamics observed in recent years in terms of

emissions in some European countries is associated

with recovery economic trends. At the same time, the

researchers agree that, despite the recovery effects of

the economies of individual countries, the trend of

greenhouse gas emissions in the European Union

shows a steady decline in the direction of the EU

targets.

Studies within the framework of international

projects conducted in 2021 indicate the continuing

negative trend in atmospheric pollution with

greenhouse gases. Thus, according to a research

project, the growth rate of greenhouse gas pollution

worldwide in 2021 was 4.9%.

2 MATERIALS AND METHODS

The methodological basis of the study is such

methods of general scientific knowledge as

classification, definition, axiomatic method,

graphical, statistical, comparative legal analysis,

synthesis and analogy, generalization and

justification, system method, extrapolation, methods

of induction and deduction. The information base was

the publications of domestic and foreign researchers

in the field of cross-border regulation. To substantiate

certain provisions of the study, data from the

statistical office of the European Union (Eurostat) and

the Russian Federal Statistics Service (Rosstat) were

used (Cross-border carbon tax in the EU: a challenge

to the Russian economy, https://econs.online/).

3 RESULTS

At the end of 2021, the countries of the European

Union proposed measures to reduce greenhouse gas

258

Batashev, R., Bisultanov, A. and Pedayeva, I.

Status and Trends in Transboundary Carbon Management.

DOI: 10.5220/0011569900003524

In Proceedings of the 1st International Conference on Methods, Models, Technologies for Sustainable Development (MMTGE 2022) - Agroclimatic Projects and Carbon Neutrality, pages

258-262

ISBN: 978-989-758-608-8

Copyright

c

2023 by SCITEPRESS – Science and Technology Publications, Lda. Under CC license (CC BY-NC-ND 4.0)

emissions with targets up to 2030. By 2050, according

to the developed package of proposals, the European

Union should become a carbon-free territory. To

achieve carbon neutrality in the EU by 2030, it is

necessary to reduce greenhouse gas emissions by 55%

compared to 1990 levels.

The implementation of grandiose plans to reduce

greenhouse gas emissions will definitely lead to

transformational changes in the economies of

countries based on carbon-intensive industries

(decrease in GDP, job cuts, etc.). For example,

energy-intensive products traditionally remain the

basis of Russian exports: fuel and energy products,

which accounted for 54.3% of total exports in 2021.

At the same time, machinery and equipment account

for the largest share of imports (49.2% in 2021).

Thus, some countries, including the Russian

Federation, will face the problem of the lack of

technologies and equipment to reduce the

concentration of greenhouse gases. The existing risks

and threats of the mechanisms proposed by the

European Union to combat greenhouse gas emissions

are the main argument, due to which individual

countries are in no hurry to assume obligations under

international climate agreements (Bazhan, 2020).

However, the economic rhetoric of the "green"

transition of the EU countries is not based on the

thesis of the possibility of sustainable development

against the backdrop of a decrease in the carbon

intensity of industries. Thus, since 1990, according to

Eurostat data, the GDP of the European Union has

grown by more than 50%, while the intensity of

greenhouse emissions (the ratio of emissions to GDP)

has halved, to 271 g of CO2-equivalent. According to

EU policymakers, these statistical observations show

that decarbonization and sustainable economic

growth are thus not mutually exclusive (CO2 braucht

einen Preis – mit einer wirtschaftspolitischen

Flankierung. Zukunft Soziale Marktwirtschaft Policy

Brief #2021/02).

The European Union is currently in the

implementation phase of the Transboundary Carbon

Management Mechanism (CBAM) (CBR). In

essence, CBAM regulation is a continuation and

extension of the European Emissions Trading System

(EU ETS). Its main idea is to prevent carbon leakage.

Carbon leakage refers to the movement of carbon-

intensive industries to countries or regions that do not

use tools to reduce greenhouse emissions. The carbon

tax on imports is one of the main tools of the EU

climate program "EU Green Deal" (Vaganov, 2021).

The initial stage of the introduction of carbon

regulation assumes an insignificant industry coverage

and includes the following products: ferrous

metallurgy, aluminum (including products from it),

cement, nitrogen fertilizers, and electricity (Makarov,

2017).

The key instruments of the transboundary carbon

correction mechanism have not been finally defined.

However, it is clear that the calculation of the cross-

border tax will be based on the volume of carbon

emissions attributable to products imported into the

EU. At present, the European Union has not decided

on the final configuration of the transboundary carbon

correction mechanism: 6 options for introducing

transboundary carbon regulation are being

considered.

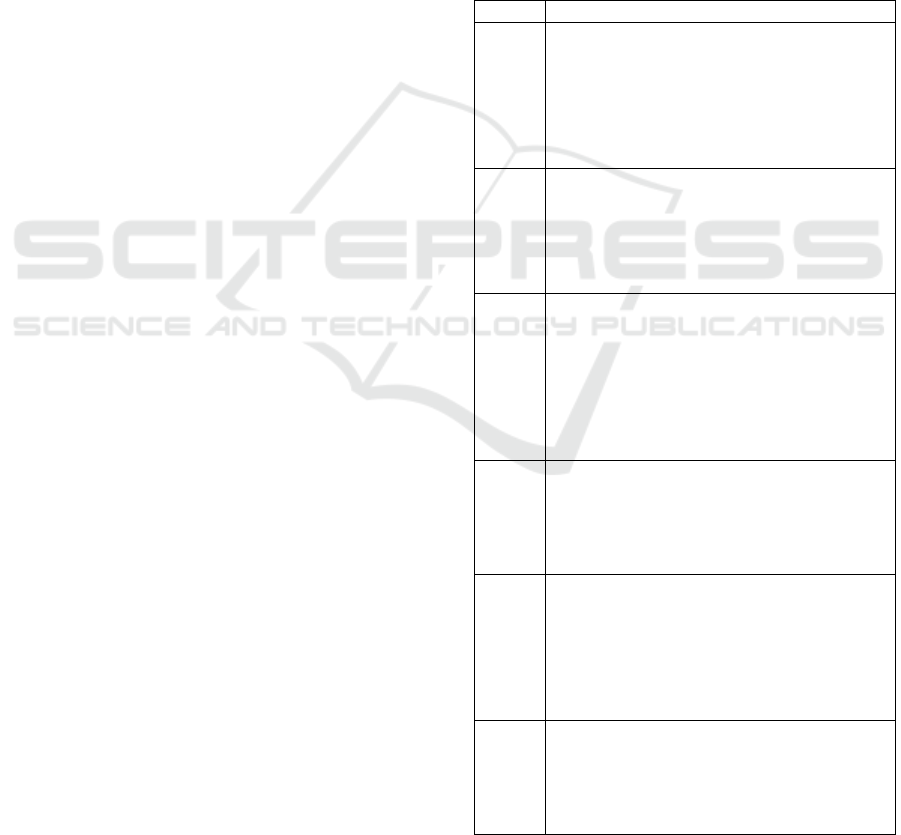

Table 1: Suggested options for introducing transboundary

carbon regulation.

O

p

tion Descri

p

tion

Option 1

A tax imposed on high carbon-intensity

products imported into the EU. The basis for

calculating the amount of the tax is supposed

to use the average emissions of greenhouse

gases in the EU countries. At the same time,

importers are required to disclose the actual

carbon intensit

y

of im

p

orted

p

roducts.

Option 2

It involves the sale to importers of certificates,

the cost of which will be calculated based on

the average greenhouse gas emissions of the

ENC countries. At the same time, importers

are required to disclose the actual carbon

intensit

y

of im

p

orted

p

roducts.

Option 3

The cost of importing products into the

territory of the EU countries for producers of

carbon-intensive products will be determined

based on the actual volumes of greenhouse

gas emissions. It is assumed that CBAM

regulation sectors will not have access to free

allowances under the European Emissions

Trading Scheme (EU ETS)

Option 4

It is a variant of Option 3 and involves the

phased introduction of CBAM regulation with

a gradual phasing out of free quotas from

2025.

Option 5

The fundamental difference from other

options lies in the depth of impact of the

CBAM mechanism due to the expansion of

the volume of regulated products down the

value chain. This will cover the main

materials as part of the components and

finished products.

Option 6

It involves the establishment of an excise tax

on both carbon-intensive imported products

and products of European manufacturers. At

the same time, the mechanism for distributing

free emission allowances will be preserved.

Status and Trends in Transboundary Carbon Management

259

Option 4 is considered the most preferred.

According to the forecasts of the European

Commission, this scenario has clear advantages in

terms of reducing greenhouse gas emissions in the EU

and preventing carbon leakage in sectors that fall

within the CBAM zone. The phasing out of free

emissions allowances under the preferred scenario

would reduce greenhouse gas emissions by 1% in the

EU and 0.4% globally in CBAM-regulated industries

by 2030. leakage up to 29% (Motosova, 2014;

Troyanskaya, 2018).

4 DISCUSSION

The transitional option is more preferable for Russia,

given that the first stage includes only a limited

number of carbon-intensive products - the most

vulnerable to carbon leakage. The absence of the oil

and gas sector in the sectors subject to CBAM

regulation is explained by some experts by the fact

that accelerated measures for the transition to

environmentally friendly production, transport and

energy will lead to the fact that the need for products

of the fuel and energy complex in its traditional form

will objectively decrease.

An analysis of the proposed approaches to cross-

border carbon regulation in any of the proposed

options allows us to draw objective conclusions about

the presence of serious challenges and threats to

Russian exports, in the structure of which the main

share traditionally remains with the fuel and energy

complex (54% in 2021) (The structure of exports and

imports, http://government.ru/). The export of metals

and products from them also occupies significant

volumes in exports (10.4% in 2021). The chemical

industry accounts for 7.7% of exported products. The

total revenue of exporters in 2021 amounted to $492

billion (Estimation of the economic consequences of

the introduction of the EU cross-border carbon tax.,

https://ecfor.ru/en/: Russia's Climate Agenda:

Responding to International Challenges,

https://roscongress.org/en/).

Serious transformational consequences for the

Russian industry and exporters are predicted by

authoritative international independent research

groups. Thus, according to Boston Consulting Group

experts, the volume of carbon-intensive products that

fall into the CBAM-regulation zone will amount to

100-160 million tons. At the same time, experts

emphasize that at the first stage, CBAM regulation is

introduced only in relation to a limited range of

products. However, it is noted that this will lead to an

additional financial burden on Russian exporters in

the amount of $3-4.8 billion, provided that the entire

volume of greenhouse gas emissions is taxed.

When analyzing the implications of a cross-border

tax, different research groups approach the issue from

different methodological platforms. Thus, the KPMG

research group analyzes three scenarios for the

introduction of cross-border carbon regulation, each

of which has its own specific impact on Russian

producers: optimistic (the tax will be introduced only

in 2028); basic (CAR will be introduced in 2025);

negative (CAR will be introduced in 2022). An

optimistic approach to forecasting the introduction of

CAR is based on the notion that it will be charged as

the difference between the actual greenhouse gas

emissions of domestic producers and the benchmark

in the EU sectors of the economy. In this case, the

exporters of natural gas, nickel, copper will become

the most vulnerable, since the energy intensity of

these products is much higher than European

indicators. The fiscal burden is expected by experts in

the amount of 6 billion euros for the period 2028-

2030). The baseline scenario for the introduction of

CAR assumes that this will happen in 2025. Only

direct greenhouse gas emissions will fall within the

CBAM regulation zone. The fiscal burden is expected

in the period 2025-2030. in the amount of 33.3 billion

euros. The introduction of a cross-border tax this year

characterizes the most negative scenario for Russia

and will provide for CBAM regulation not only of

direct emissions, but also of indirect ones. By indirect

means emissions of greenhouse gases in the sectors of

production that are directly related to exporters. The

fiscal burden under this scenario is expected in the

period 2022-2030. in the amount of 50.6 billion euros,

which is approximately 10% of the revenue of

Russian exporters in 2021.

Representatives of the Institute for Economic

Forecasting of the Russian Academy of Sciences,

assessing the economic consequences of the

introduction of the EU cross-border carbon tax,

identify the following key goals for the introduction

of CBAM regulation: structural changes to stimulate

the intensification of economic growth; increasing the

competitiveness of European manufacturers;

reducing the negative impact on the environment. The

following threats to Russia stand out. First, the

introduction of cross-border carbon regulation will

lead to a reduction in demand for traditional Russian

exports (carbon-intensive). Secondly, the growth of

export costs and the cost of using borrowed capital.

Thirdly, the ratification of commitments to reduce

greenhouse gas emissions that are incommensurable

with the economic damage.

MMTGE 2022 - I International Conference "Methods, models, technologies for sustainable development: agroclimatic projects and carbon

neutrality", Kadyrov Chechen State University Chechen Republic, Grozny, st. Sher

260

Considering that the mechanism of the cross-

border carbon tax has not been fully developed, it is

very difficult to make forecasts regarding the

formation of the fiscal burden on domestic producers.

The contours of future prices for greenhouse gas

emissions are not yet clear. Currently, the cost of

buying emissions allowances on the European trading

floor varies from 45 to 100 euros per tonne of CO2

equivalent.

In our opinion, when integrating the Russian

Federation into international mechanisms for carbon

regulation, it is necessary to proceed from the fact that

the TUR and the prospect of a phased increase in

prices for greenhouse gas emissions have a number of

negative institutional consequences for Russia:

− increased social tension. The economic

condition of the Russian population is currently

characterized by a decline in real disposable

income over the past years. Socially

disadvantaged groups of the population and

low-income households will lose purchasing

power as a result of a sharp increase in the prices

of energy and carbon-intensive consumer

goods. If the negative scenario (accounting for

indirect CO2 emissions) of the introduction of

CAR is implemented, the decline in the

consumer ability of the population will deepen

further down the value added chain;

− for the corporate sector, the introduction of

CAR sectoral difficulties are associated with a

decrease in profitability and job cuts. First of all,

we are talking about the capital-intensive

sectors of the Russian economy, since high

capital costs are also characterized by large

volumes of energy consumption, which results

in an increase in greenhouse emissions;

− the introduction by the European Union of a

unilateral transboundary carbon regulation with

the prospect of higher prices for emissions will

lead to a decrease in the international

competitiveness of Russian producers.

Countries that already have national

mechanisms for carbon regulation (for example,

China) can become more competitive and force

Russian suppliers out of international markets;

− the absence of a national system of carbon

regulation in the Russian Federation may in the

future lead to a “carbon leak” from countries

falling under the CBAM regulation and having

or starting to implement carbon regulation

mechanisms, which will lead to a further

increase in the carbon intensity of the sectors of

the Russian economy and increase the intensity

of greenhouse gas emissions;

− lack or limited access to technologies that allow

reducing, capturing and using carbon emissions.

It should be noted that the promotion of non-

energy exports in Russia is included in the

roadmap of national priorities. The

development and implementation of high-tech

and low-carbon technologies for the supply of

products to international markets and the

domestic market, according to experts, should

become one of the significant growth points for

the domestic economy. Companies should

become the driver of technological progress, as

the increase in carbon prices creates objective

prerequisites for taking measures to reduce

carbon emissions technologically. Companies'

technology incentives are fueled by the desire of

consumers to use products with a lower carbon

footprint, as this reduces their consumer costs.

Thus, market competition allows significant

technological advances to be made to reduce the

carbon intensity of products. However, it is

obvious that the development of basic

technological innovations in the field of carbon

regulation is impossible without state

participation. Many sectors of the economy

cannot be imagined without basic technologies.

For example, these are aviation, Internet

technologies, nuclear energy, etc. Due to the

great economic uncertainty and limited

financial resources, private enterprises are not

interested in investing in such sectors of the

economy. Market maturity and the required

level of profit when investing in basic

technologies is achieved over an extended

period of time. Government support for

investments in basic technologies to reduce the

carbon intensity of products has a high

multiplier potential, as they extend to other

sectors of the economy or longer along the value

chain (Dorsey-Palmateer, 2020).

5 CONCLUSIONS

Conclusion and conclusions. Given the negative

expectations, in our opinion, the Russian Federation

needs to provide response measures in the following

areas:

− development and implementation of a domestic

system for reporting and monitoring of

emissions and removals of greenhouse gases. It

is believed that the current accounting

mechanism for carbon emissions and removals

does not fully reflect the actual picture. This

Status and Trends in Transboundary Carbon Management

261

problem is especially relevant for developing

countries. The development of a national

emission accounting system for the Russian

Federation is necessary in order to ensure the

comparability of international data;

− creation and development of domestic carbon

markets in order to ensure the receipt of carbon

fees in the country's budget system, which will

make it possible to subsequently compensate

domestic producers for payments made through

various government programs (subsidizing the

industry, concessional lending, tax preferences

(the most preferable, in our opinion, option

etc.).

REFERENCES

Cross-border carbon tax in the EU: a challenge to the

Russian economy. https://econs.online/.

Russia's Climate Agenda: Responding to International

Challenges. The report was prepared by the CSR

Foundation together with the Analytical Center for the

Fuel and Energy Complex of the REA of the Ministry

of Energy of Russia and Situation Center LLC,

https://roscongress.org/en/.

Estimation of the economic consequences of the

introduction of the EU cross-border carbon tax. Institute

of Economic Forecasting of the Russian Academy of

Sciences, https://ecfor.ru/en/

The structure of exports and imports. Collection of the

Federal Customs Service, (http://government.ru/).

CO2 braucht einen Preis – mit einer wirtschaftspolitischen

Flankierung. Zukunft Soziale Marktwirtschaft Policy

Brief #2021/02.

Bazhan, A. I., Roginko, S. A., 2020. EU Border Adjustment

Carbon Mechanism: Status, Risks and Possible

Response. Series “Analytical Notes of the Institute of

Europe of the Russian Academy of Sciences”. 4.

Vaganov, E. A., Porfirev, B. N., Shirov, A. A., Kolpakov,

A. Yu., Pyzhev, A. I., 2021. Assessment of the

contribution of Russian forests to reducing the risks of

climate change. 17(4). pp. 1096-1109.

Dorsey-Palmateer, R., Niu, B., 2020. The effect of carbon

taxation on cross-border competition and energy

efficiency investments - Energy Economics. Elsevier.

Motosova, E. A., Potravny, I. M., 2014. Pros and cons of

introducing a carbon tax: foreign experience and

Russia's position on the Kyoto Protocol. All-Russian

economic journal ECO. 7.

Troyanskaya, M. A., Tyurina, Yu. G., 2018. Taxes on air

emissions: foreign experience. International

Accounting.

Makarov, I. A., Stepanov, I. A., 2017. Carbon regulation:

options and challenges for Russia. Bulletin of Moscow

University. 6.

MMTGE 2022 - I International Conference "Methods, models, technologies for sustainable development: agroclimatic projects and carbon

neutrality", Kadyrov Chechen State University Chechen Republic, Grozny, st. Sher

262