Analysis of Restaurant Tax Revenue in Medan City During Covid-19

Pandemic

Faisal Eriza and Afri Rizki Lubis

Program Study of Development Study, Universitas Sumatera Utara, Jl. Dr. A. Sofiyan no 01, Padang Bulan, Medan,

Indonesia

Keywords: Tax, Reveue, Restaurant, Covid-19, Pandemic.

Abstract: The purpose of this research is to determine the effects of the covid pandemic on restaurant tax revenue in

Medan. The method used is qualitative descriptive research for this study sought to describe a social

phenomenon that is describing the fact. This study uses primary data and secondary data relating to restaurant

tax revenue in Medan before and after the covid pandemic. Data collection techniques used in this research

include observation, documentation, and interviews. The result of this study indicates that the covid pandemic

affects a decline in restaurant tax revenue caused by decreases in restaurants income, due to business operation

hour restrictions and time rules for dine-in visitor regulations. Owing to a decline in restaurant tax revenue

and people’s weak purchasing power causes numerous restaurants permanently closed. The realisation of

restaurant Tax Revenue of 2020-2021 targets set by Taxes & Levies Management Board of Urban Terrain

doesn’t reach their target. Whereas in 2015-2019 the realisation consistently exceeds the targets.

1 INTRODUCTION

Tax is an essential thing in the journey of a nation.

Almost all countries in this world apply the rules or

scheme about tax imposition directly or indirectly. No

exception in Indonesia itself. Tax is the one of the

biggest income sector for Indonesia. The tax revenue

fund is allocated by government to fulfill the country

needs in general and to reach the society’s welfare

and prosperity. The more people pay taxes, the more

facilities and infrastructure are built (Pandiangan,

2008: 5). One kind of tax is Local Tax. Therefore,

Local Tax is prioritized because able to become the

one of region financial source to improve the

distribution and development of society’s welfare in

that region. The local tax capability that owned by

each region is an indicator of the local government

readiness in regional autonomy. Hence, something

that obtained from local tax are directed to increase

Locally Generated Revenue (LGR) or also known as

Original Local Government Revenue, so that region

autonomy can be well-executed, therefore to increase

the LGR, it also needed the contribution from many

sectors, one of them is from food industrial sector.

Food industrial or also known as restaurant is the

incredible sector. Restaurant industry is fulfilled by

potential, prospect, and growing fast along with the

times. Restaurant tax that managed by Taxes &

Levies Management Board of Urban Terrain

(BPPRD) of Medan City is one of the Local Tax that

contribute towards good impact to increase LGR

because more restaurants in Medan City.

However, in the beginning of March 2020,

Indonesia was started the against the Covid-19 virus

that enter to Indonesia. Certainly, when the first time

Corona Virus in Indonesia, it gives the impact

indirectly for Indonesian state especially in economic

aspect. The implementation of Large- scale social

restrictions (PSBB) rule by government had give the

large impact especially on the decline for society’s

economic activity especially in food industries. And

for the tax income data in Medan city itself also

decreased and did not reach the target in pandemic

era, and here are some of data on Medan city at the

time before and while the pandemic occurred.

Eriza, F. and Lubis, A.

Analysis of Restaurant Tax Revenue in Medan City During Covid-19 Pandemic.

DOI: 10.5220/0011541100003460

In Proceedings of the 4th International Conference on Social and Political Development (ICOSOP 2022) - Human Security and Agile Government, pages 117-121

ISBN: 978-989-758-618-7; ISSN: 2975-8300

Copyright

c

2023 by SCITEPRESS – Science and Technology Publications, Lda. Under CC license (CC BY-NC-ND 4.0)

117

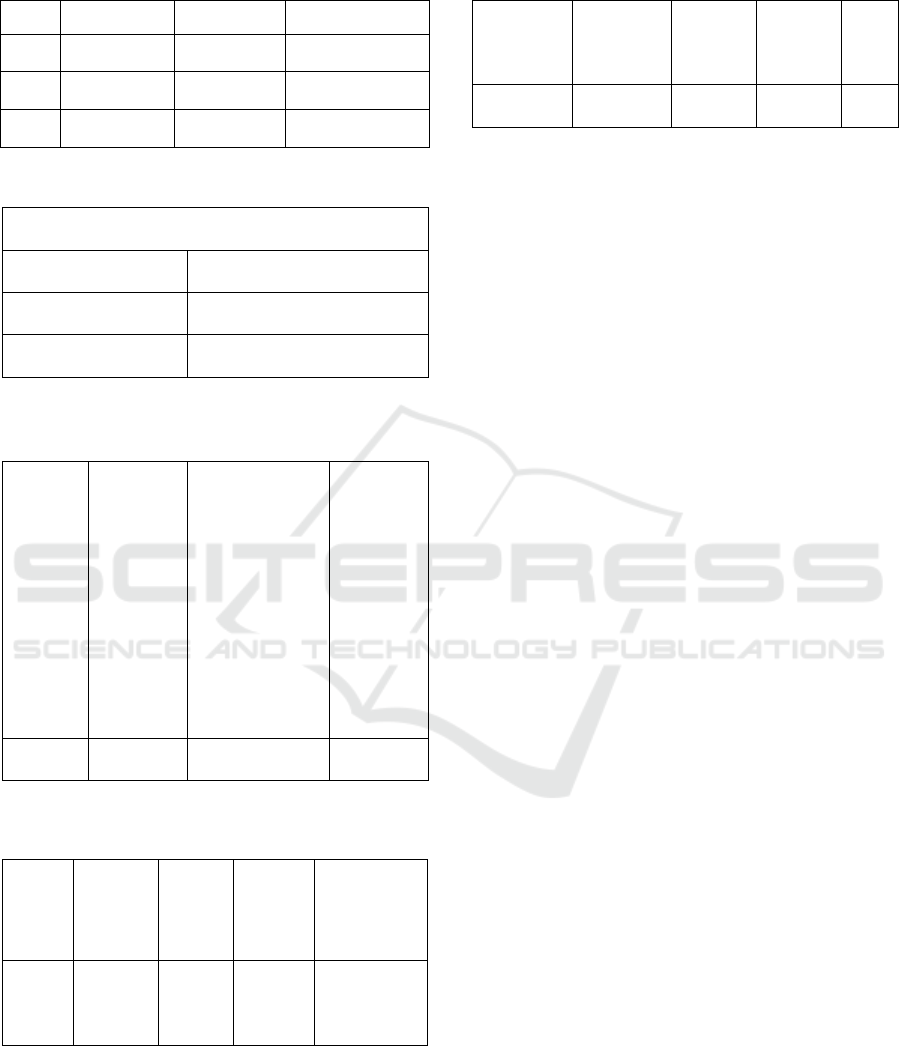

Table 1: Details of realization of medan city restaurant tax

in 2018-2020.

2018 2019 2020

Total 172.788.503.063

,71

209.883.937.063

,74

180.477.531.250,00

Target 170.000.000.000

,00

204.000.000.000

,00

180.000.000.000,00

Perce

ntage

101,64% 102,88% 76,93%

Table 2: Target and Realization of Tax.

Restaurant in 2021.

Table 3: Target Refocusing on Restaurant Tax.

Table 4: Reputation of Restaurant Taxpayer as of July 31,

2020.

Types

of

taxes

Active

taxpaye-r

Inactive

taxpayer

Incidental

taxpayer

Total

Restau

-rant

1629 697 557 2883

Table 5: Recapitulation of Restaurant Taxpayer as of July

31, 2020.

Types of

taxes

Active

taxpayer

Inactive

taxpayer

Incidental

taxpayer

Total

Restaurant 1894 697 559 3150

2 LITERATURE REVIEW

2.1 Tax

Tax is public's dues to the State treasury based on the

law (which can be enforced) by not receiving

reciprocal services (counter-achievements), which

can be shown directly and used to pay general

expenses (Djojohardikusuma, 2006:1).

2.1.1 Regional Tax

Regional Tax is a mandatory contribution to the

region owed by an individual or entity that is coercive

under the law without receiving direct compensation

and is used for regional purposes for the greatest

prosperity of the people. Examples: Vehicle Tax,

Vehicle Transfer Fee, Surface Water Tax, Cigarette

Tax, Hotel Tax, Restaurant Tax, Entertainment Tax,

Advertising Tax, Street Lighting Tax, etc.

2.1.2 Restaurant Tax

Restaurant Tax is a tax on services provided by

restaurants, while restaurant is a facility providing

food and beverages with a fee, which also includes

restaurants, cafeterias, canteens, stalls, bars, and the

like, including catering / catering services (Marihot

Pahala Siahaan, 2010:15).

2.1.3 Restaurant Tax Subject and Taxpayer

According to Marihot Pahala (2010: 330), those who

are subject to the restaurant tax are individuals or

entities who buy food and or drinks from restaurants.

In simple terms, the tax subjects are consumers who

buy food and drinks in restaurants. Meanwhile, the

taxpayer is an individual or entity operating a

restaurant, namely an individual or entity in any form

within the company or work environment conducting

business in restaurant or dining sector.

Target for

restaurant

tax before

the end of

2020

Initial target of

restaurant tax at

the beginning of

p

andemic

(secondquarter of

2020)

Intial target

of

restaurant

tax at the

beginning

of

p

andemic

(secondqua

rter 0f

2020)

Restaurant 245.000.000.0

00,00

171.500.000.000,00 180.000.000.0

00,00

In 2021, as of May 31, 2021

Target 250.859.144.759,00

Realization 65.559.352.384,00

Percentage 26,13%

ICOSOP 2022 - International Conference on Social and Political Development 4

118

2.1.4 Restaurant Tax Collection Method

According to Tax Law article 8 (1) of the restaurant

tax imposition base is the amount of received

payment or properly received for restaurant. The

collection of restaurant tax can not be bought by the

entire stock that means the entire process of restaurant

tax collection activity are can not be handed over to

third parties. However, there is the probability of

cooperation with third parties in tax collection

process, such as the tax form printing, the delivery of

letters to taxpayer, or the collecting data of tax object

and tax subject. Some activities that can not be

collaborated with third parties are the activity of the

calculation of amount owed tax, the control of tax

deposition, and collecting taxes.

3 METHODS

This type of research used in this study is qualitative

by conducting data studies in descriptive or

descriptive form. This method of research attempts to

describe and interpret the objects in accordance with

reality. The descriptive method is implemented

because the data analysis is presented descriptively.

The study was conducted in Taxes & Levies

Management Board of Urban Terrain Medan. Medan

City Taxes & Levies Management Board of Urban

Terrain was selected as the research setting by

considering their tasked, collecting regional taxes on

provincial taxes, which include restaurant taxes.

To obtain the representative data, the key

informant and the main informant are necessarily

needed who comprehend and related to the problem

being studied as well as the additional informant who

can provide the information even though not directly

involved in studied social interactions.

4 RESULT AND DISCUSSION

4.1 Taxes & Levies Management Board

of Urban Terrain’s Profile

(BPPRD)

Before regarded as the Taxes & Levies Management

Board of Urban Terrain (BPPRD), it was known as

the Regional Revenue Service (DISPENDA). In the

beginning, DISPENDA of Medan City was the sub-

section of finance division that managed the revenue

and regional income. In this subsection, there are no

more sub-sections, because at this time, there were no

many taxpayers or levies that domiciled in Medan

City. With consideration of development and the rate

of population growth in Medan city, towards the

Regional Regulation, the financial sub-section was

changed into the revenue section. In the income

section, several sub-sections manage the tax revenue

and regional levies that are the obligations for

taxpayers or levies in Medan city area, which involve

21 sub-districts such as Medan city, Medan Area,

Medan Maimun, Medan Polonia, Medan Denai,

Medan Baru, Medan Amplas, Medan Barat, Medan

Johor, Medan Selayang, Medan Sunggal, etc.

4.2 Description of Main Duties and

Functions of Taxes & Levies

Management Board of Urban

Terrain (BPPRD)

The following are the forms of strategies or efforts

carried out by the One-Stop Integrated Investment

and Licensing Service Office Province North

Sumatra to increase investment in North Sumatra

Province based on the indicators:

According to the decision of the Mayor Medan

city, Number 27 Year 2017 about Main Duties and

Functions of Taxes & Levies Management Board of

Urban Terrain (BPPRD) of Medan city, towards this

decision what is meant by

1. The region is Medan city.

2. Regional Government is the administration of

government affairs by regional government and

Regional Houses of Representatives according

to the principle of autonomy and assistance

tasks with the principle of autonomy as wide as

possible in the system and principle of Unitary

State of the Republic of Indonesia (NKRI) as

referred to the 1945 Constitution of the Republic

of Indonesia.

3. Regional Government is the Mayoralty as the

administration element of Regional

Government that lead the implementation of the

Government affairs also the authority of

autonomous region.

4. The mayor is Mayor of Medan city.

5. Regional Secretary is the Regional Secretary of

Medan city.

6. Agency is the Taxes & Levies Management

Board of Urban Terrain (BPPRD) of Medan

city.

7. The Head of the Agency is the Head of the

Taxes & Levies Management Board of Urban

Terrain (BPPRD) of Medan city.

Analysis of Restaurant Tax Revenue in Medan City During Covid-19 Pandemic

119

8. Secretary is the Secretary of the Taxes & Levies

Management Board of Urban Terrain (BPPRD)

of Medan city.

9. State Civil Apparatus, herein after abbreviated

as ASN employees is the profession for the Civil

Servant and the government staff with work

agreements working for government agencies.

10. State Civil Apparatus Employees, herein after

abbreviated as ASN is the profession for the

Civil Servant and the government staff with

work agreements by the service supervisor and

assigned tasks in government position or

entrusted with other state duties and paid

according to the laws and regulations.

11. Civil Servant, herein after abbreviated as PNS

are Indonesian citizens who fulfill certain

requirements, are appointed as the ASN

employees on a permanent basis by staffing

officials to occupy government positions.

12. Government Affairs is the power of government

as the President obligation which its

implementation managed by the state ministry

and Regional Government administrators to

protect, serve, empower, and prosper the

community.

13. Regional Apparatus Work Unit, herein

abbreviated as SKPD is the regional apparatus

in the regional government as the budget or

goods user.

14. Regional Apparatus is the supporting element of

Mayor and DPRD in the administration of

government affairs as the region authority.

4.3 Data Presentation

In obtaining the necessary data to answer the research

problem, there are some steps that carried out by the

author, involve: First, the research begins with the

collection of various written documents. Second, the

author conducts the interview with some selected

informants to obtain the information with

comprehensive facts regarding to the problem

research. Informants in this research were four

peoples as the employees or staff in the Taxes &

Levies Management Board of Urban Terrain

(BPPRD) of Medan city.

The type of interview that chosen by the author is

systematic interview type, where before the interview

is starting, the first step is the author compiles the

asked questions list. The compiled questions clearly

related with the Effect of Pandemic Covid-19 Virus

on Restaurant Tax revenues in Medan city. However,

within the process itself, the author does not rule out

the emergence of new questions that can learn in-

depth the information from the informant.

In this interview, there are some question which

asked to the informants about the problem of

Pandemic Impact of Covid-19 towards Restaurant

Tax revenues in Medan city. The author only sorts

some informant as the main informants according to

their relevant field and position with the result that the

entire raised problems in this research could be

answered.

According to the research and observation results

that was conducted by the author, can be concluded

that: The impacts that occur because of pandemic

virus towards Restaurant Tax revenues in Medan city

is decrease because decreased restaurant’s income

and the restriction of visitors amount that cause the

absence of consumers at certain hours and the

decrease of consumers amount. Taxes & Levies

Management Board of Urban Terrain (BPPRD) of

Medan city has the annual tax target with different

nominal in every year. However, during the pandemic

Covid-19 era, Taxes & Levies Management Board of

Urban Terrain (BPPRD) of Medan city provide the

dispensation for restaurant because the decline of

public consumption so that causes many restaurants

are permanently close. Taxes & Levies Management

Board of Urban Terrain (BPPRD) of Medan city

provide the dispensation for many restaurants that

affected by pandemic era such as the tax delays for

several months.

From 2015-2019, the number of realizations

always exceeds the biggest target, especially in 2019.

From the year before pandemic era, taxpayers always

increase and during the pandemic era in 2021,

taxpayers continued to increase than 2020. There is

no difference in calculation of tax payment in

restaurant and Micro, Small, and Medium Enterprises

(UMKM). The criteria of restaurant and UMKM that

must be taxed are if that restaurant has gross income

of IDR 9,000,000 each month. However, there is no

specific policy for UMKM to pay the tax before

pandemic era.

REFERENCES

Adityo Susilo, C. d. Maret 2020. Coronavirus Disease

2019: Tinjauan Literatur Terkini. Jurnal Penyakit

Dalam Indonesia Vol. 7 No. 1.

Edward, W. M. 2013. Efektivitas dan Kontribusi

Penerimaan Pajak Hotel dan Pajak Restoran Terhadap

Pendapatan Asli Daerah Kota Manado. E-Journal Vol.

1 No. 3: 871-881.

Handayani, R. T. 2020. Jurnal Ilmiah Permas: Jurnal

Ilmiah STIKES Kendal Vol. 10 No. 3, hal 373 - 380.

ICOSOP 2022 - International Conference on Social and Political Development 4

120

Ilyas, W. B. 2013. Hukum Pajak. Jakarta: Salemba Empat.

Nugraha, L. d. 2004. Analisis Efektivitas Pajak Hotel dan

Pajak Restoran dan Kontribusinya Terhadap

Pendapatan Asli Daerah diKota Bandung. Jurnal

Umum Administrasi Vol. 4: 1-10.

Salamah, B. &. 2020. Pengaruh Pandemi Covid Terhadap

Penerimaan Pajak di Negara Indonesia Pada Tahun

2020. Vol. 1, No. 2, hal 277-289.

Siregar, N. Y. 2021. Dampak Covid-19 Terhadap

Penerimaan Pajak Negara Pada Sektor UMKM di

Indonesia. Jurnal STIE IBMI Medan Vol. 3 No. 1.

Yusriani, d. 2020. Masa-Masa Covid 19 Mengenal dan

Penanganan dari Bebagai Perspektif Kesehatan.

Analysis of Restaurant Tax Revenue in Medan City During Covid-19 Pandemic

121