Research on Management Accounting Framework based on Hall

Three-dimensional Structure and DSM

Yanyong Sun

1

, Guang Yu

1

and Ceng Zeng

2a

1

School of Management, Harbin Institute of Technology, Nangang Qu Xi Da Zhi Jie 92 th, Harbin, China

2

School of Accountancy, Shanghai University of Finance and Economics, Yang Puqu Guoding road 777th, China

Keywords: Hall 3D Structure Model, Management Accounting, Enterprise Operation, Design Structure Matrix (DSM).

Abstract: The management accounting framework aims to improve the operation control ability. In view of the lack of

internal relationship between management methods and operation control in the previous research on

management accounting framework systems, this paper puts forward the purpose of this research. We use

Hall's three-dimensional structure model for reference to construct the management accounting framework

based on operation control, and study the characteristics of operation control with the contingency elements

such as organizational structure, control methods, and ability improvement as the logical dimension; Taking

eight tools such as comprehensive budget, performance evaluation and responsibility body as the knowledge

dimension to promote the application of management accounting, the enterprise operation matrix is defined.

Design Structure Matrix (DSM) method is used to study the quantitative correlation between operation control

and management accounting tools, and reveal the quantitative relationship between management accounting

tools. Finally, the case of China Unicom verifies hierarchical characteristics between management accounting

tools.

1 INTRODUCTION

Enterprise operation is a complex system, which is

realized by the exchange of various information as

well as the cooperation of various management

methods. Aiming at improving the quality of

enterprise operational control, the management

accounting framework combines different

management accounting tools based on a certain

logic. Existing research puts forward management

accounting framework including value management,

balanced scorecard, comprehensive budget and

activity-based costing, and so on. However, these

management accounting frameworks lack analysis of

the internal relationship between management

accounting tools and operational control since they

are mainly revolved around a certain management

accounting tool. In the meanwhile, the existing

research ignores the defects of a single management

accounting tool and the correlation among different

management accounting tools since it mainly focuses

on the impact of a single management accounting tool

a

https://orcid.org/0000-0003-2387-4020

on specific operational control. It is necessary to

choose appropriate management accounting tools,

and deeply analyze the correlation between

operational controls and different management

accounting tools and the synergy among management

accounting tools according to organizational

characteristics, so as to ensure that the selected

management accounting toolset can effectively

connect with the enterprise operational control mode.

Therefore, it is of great theoretical and practical

significance to build a management accounting

framework based on operational control for the

application of management accounting tools and the

promotion of enterprise operational control ability.

Using Hall's three-dimensional structure model

for reference, this paper constructed a management

accounting framework based on operational control.

We investigated the characteristics of operational

control (logical dimension) such as organizational

structure, control method, and ability improvement,

management accounting tools (knowledge

dimension) including a comprehensive budget,

performance evaluation, and responsibility body.

Sun, Y., Yu, G. and Zeng, C.

Research on Management Accounting Framework based on Hall Three-dimensional Structure and DSM.

DOI: 10.5220/0011183000003440

In Proceedings of the International Conference on Big Data Economy and Digital Management (BDEDM 2022), pages 415-421

ISBN: 978-989-758-593-7

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

415

Based on the framework, we define the operation

matrix. Using the method of DSM matrix, the

quantitative correlation between operation control

and management accounting tools, the quantitative

correlation among management accounting tools

were determined. The case study of China Unicom

validates the central role of comprehensive budgeting

in enterprise operations management. The research

results reveal the significant correlation and

hierarchical features among management accounting

tools. Firstly, management accounting tools are

hierarchical in nature according to the relevance of

operational characteristics, and each hierarchical tool

cooperates with and complements each other and has

hierarchical characteristics. Secondly, the basic

functions of management accounting tools at

different levels are positioned variably with

quantitative intrinsic relationships with each other.

Thirdly, the management accounting practice based

on the operational dimension is the process of deeply

promoting the integration of business and finance.

2 LITERATURE REVIEW

Existing research puts forward management

accounting framework including value management,

balanced scorecard, comprehensive budget and

activity-based costing, and so on. With the

fundamental goal of continuously creating

shareholder value, Serebryakova put forward a value

management framework (VBM), which determines

specific internal goals, selecting strategy and

organizational design, identifying value drivers,

formulating action plans, and selecting performance

indicators and goals, performance evaluation, as well

as feedback improvement (Serebryakova 2021).

Pareek put forward a management framework based

on the principle of the strategic management process,

which takes the Balanced Scorecard (BSC) as the

core and integrates tools such as budget, activity

management, and shareholder value index (Pareek

2021). Ploder focused on the combination of agile

project management and beyond budgeting (Ploder

2020). From the perspectives of economics,

psychology, and sociology, Choi found imply that the

patterns of budget ratcheting could be diverse based

on how local government officials strategically

respond to the dynamics between bargaining power

and the pressure of justifying budgets (Choi 2021).

The existing researches mainly discuss the influence

of specific management accounting tools such as

comprehensive budget, performance evaluation, and

balanced scorecard on specific operational control

when applying the management accounting

framework to operational control. For example,

Cools study the role of budgets in a creative context

(Cools 2017). They find expected creative firms use

their budgets in a more interactive way and

responsive creative firms use their budgets in a rather

diagnostic way. Artz study the effect of performance

measure used on the functional strategic decision.

Lima presents the results of the strategic planning

process and the use of the Balanced Scorecard as a

strategic management system for the Center for

Sustainable Development/Research Group on Energy

Efficiency and Sustainability (Greens), University of

Southern Santa Catarina (Unisul) (Lima 2021).

Malagueño investigate the effect of BSC in SMEs on

their financial performance and innovation outcomes

(Malagueno 2018).

An appropriate management accounting system

depends on the specific environment and

organizational structure design of the organization

itself. In the process of selecting management

accounting tools, enterprises should deeply analyze

the correlation between operational control and

different management accounting tools and the

synergy among management accounting tools

according to organizational characteristics, so as to

ensure that the selected management accounting

toolset can effectively connect with the operational

control mode of enterprises. As a result, it can give

full play to the efficacy of management accounting,

improve the level of enterprise operational control,

and then promote the high-quality development of

enterprises by building a management accounting

framework based on operational control.

3 MANAGEMENT ACCOUNTING

TOOLS

The application of management accounting tools in

enterprises is to solve the management problems that

restrict the ability of enterprise value creation.

Therefore, enterprises should not only consider the

internal relationship with enterprise operational

control but also consider the correlation between

management accounting tools when they implement

management accounting tools. For quite a long period

of time, the common topic concerned by both the

practical and academic circles engaged in the

research of management accounting is how to operate

management accounting to better support the

operational control of enterprises; what are the key

elements of an effective management accounting

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

416

framework; what is the relationship among these

factors and enterprise operational control activities;

what is the relationship between the internal elements

of the management accounting framework? Based on

operational control, this paper answers the above

questions in the way of constructing a management

accounting framework.

3.1 Management Accounting

Framework based on Hall's

Three-dimensional Structure

Hall's three-dimensional structure analysis method, a

system engineering methodology put forward by

American system engineering expert Hall in 1969,

can be used to solve the planning, organization, and

management problems of large and complex systems.

Hall's three-dimensional structure divides the whole

system engineering into different stages and steps

closely connected before and after and combines

various professional knowledge and skills needed to

complete these stages and steps. Hence, it formed a

three-dimensional structure composed of the time

dimension, logic dimension, and knowledge

dimension. This paper builds a management

accounting framework based on operational control

by drawing lessons from Hall's three-dimensional

structure analysis method.

Firstly, the time dimension of Hall's three-

dimensional structure represents the whole process of

system engineering activities arranged in time

sequence from beginning to end. The enterprise

operation process is divided into the planning stage,

scheme formulation stage, implementation stage, and

continuous improvement stage. Therefore, this paper

defines the above four stages as time dimensions.

Secondly, the thinking procedure that should be

followed in each stage of the time dimension is

represented by the logical dimension of Hall's three-

dimensional structure. The planning stage and the

programming stage need to be conducted under the

guidance of the organization's strategic objectives. In

this paper, the procedures to be followed in these two

stages are defined as organizational functions. In the

implementation stage, enterprises need to effectively

control the operation process to ensure the effective

implementation of the scheme. In this paper, the

procedures to be followed in the implementation

stage are defined as control activities.

Enterprises need to make the operation plan to

create value continuously in the stage of continuous

improvement. This paper defines the procedure to be

followed in this stage as capability improvement.

In the end, the knowledge dimension of Hall's

three-dimensional structure represents the

professional knowledge needed to complete these

stages and steps. Management accounting is carried

out around enterprise operational control, and it is a

control system that directly participates in enterprise

operation process management. Management

accounting tools are the concretization of

management accounting concepts and form important

support for the operational control of enterprises.

Therefore, this paper positions management

accounting tools as a knowledge dimension. As

shown in Fig. 1, this paper establishes a management

accounting framework based on operational control

by using Hall's three-dimensional structure model for

reference, and studies the internal relations and

quantitative methods among management accounting

tools based on enterprise operation characteristics.

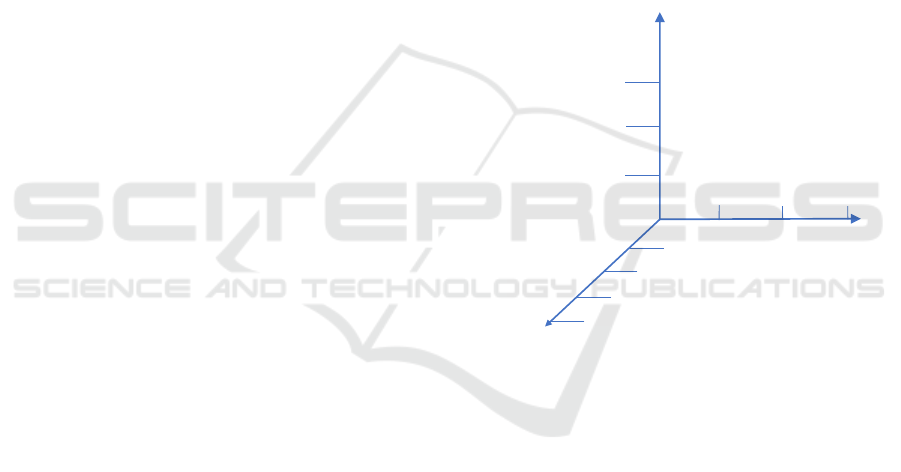

Figure 1: Management accounting framework model based

on operational control.

3.2 Enterprise Operation Matrix

Usually, based on the changes of the internal and

external environment, enterprises choose the

management accounting tools they need. In fully

competitive industries, enterprises are more willing to

apply management accounting tools to improve

operational efficiency and benefits when the internal

and external environment of enterprises tends to be

complex and changeable, to enhance their

competitiveness.

We construct the enterprise operation matrix

based on the above analysis. The logical dimension

refers to the collection of elements controlling

operation activities, which constitutes the ordinate of

enterprise operation matrix, and describes the static

planning and dynamic allocation of organizational

structure, control mode, ability improvement, and

Logical dimension

(Operational control)

Knowledge dimension

(Management

accounting tools)

Continuous improvement

Planning stage

Formulate a scheme

Im

p

lementation

p

hase

Comprehensive budget

Performance appraisal

Responsibility body

…

Organizational function

Control activities

Ability

improvement

function

Time dimension

(Implementation and

improvement)

Research on Management Accounting Framework based on Hall Three-dimensional Structure and DSM

417

other elements realizing business objectives under the

condition of functional division. Knowledge

dimension means the collection of management

accounting tools. The abscissa of enterprise operation

matrix proposed in this paper consists of

comprehensive budget, performance evaluation,

responsibility body, lean cost, supply chain, sales

support, integration of industry and finance, decision

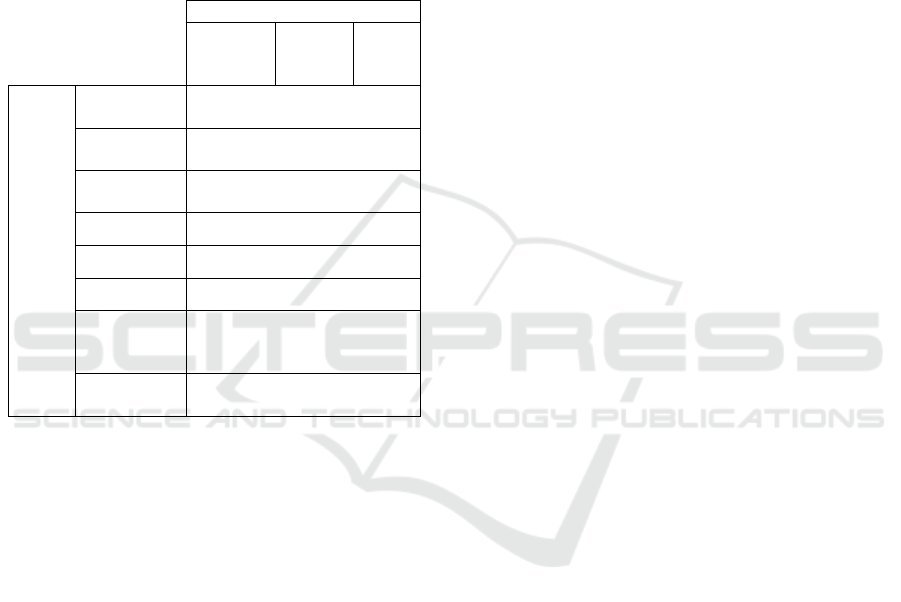

support, and other methods. See Table 1.

Table 1: Operation control dimension and management

accounting tool dimension of enterprise operation matrix.

Operation control

Organizati

onal

function

Control

activities

Ability

improv

ement

Manag

ement

accoun

ting

tools

Comprehensi

ve budget

Performance

a

pp

raisal

Responsibility

b

ody

Lean cost

Supply chain

Sales support

Integration of

industry and

finance

Decision

su

pp

ort

Enterprise operation matrix reflects the internal

logical relationship between operation control

dimension and management accounting tools. The

correlation between the elements of the enterprise

operation matrix is different due to the influence of

the enterprise operating environment. From the

perspective of system engineering, the correlation

and impact of operation matrix elements can be

scientifically quantified and evaluated. Therefore, we

further select the verification method for the

quantitative correlation of enterprise operation matrix

elements. If we can prove that there is an internal

correlation between the constituent elements of the

operation control dimension and management

accounting tools, the internal correlation between

management accounting tools can also be indirectly

proved.

4 CASE ANALYSIS

The correlation and influence of operational matrix

elements can be scientifically quantified and

evaluated from the perspective of system

engineering. Therefore, the Design Structure Matrix

(DSM) method was selected as the verification

method of quantitative correlation, which is used to

describe the interdependence between different

elements in complex systems (Loureiro 2020). The

enterprise operation matrix composed of operation

control and management accounting tools is a

complex of the correlation of factors such as

products, processes, organizations, and activities.

Therefore, the quantitative research using the DSM

model is suitable for the enterprise operation matrix

model proposed in this paper.

In order to analyze the characteristics of operation

control and management accounting tools, we

introduce the Delphi evaluation method to evaluate

the score of the correlation of the constituent

elements of China Unicom's enterprise operation

matrix quantitatively. Using a valuation scale ranging

from 0 to 5 (0=Unconsidered; 1=Worth a little

consideration; 2=Worth considering; 3=Partly true;

4=Meaningful; 5=Makes sense).

4.1 Quantifying the Impact of

Operational Control on

Management Accounting Tools

The quantitative correlation of the operational control

matrix evaluation is shown in Table 2. The

quantitative correlation between organizational

function α and control activity β is 5, while the

quantitative correlation between control activity β

and organizational function α is 4, indicating that

organizational function α has a greater influence on

control activity β than control activity β has on

organizational function α. Meanwhile, there is another

typical correlation relationship between capability

enhancement ϒ and control activity β. The

quantitative correlation effect of capability

enhancement ϒ on the correlation with control

activity β is 3, while the quantitative correlation effect

of control activity β on capability enhancement ϒ is 1.

It shows that the influence of ability improvement on

control activity β is greater than that of control activity

β on ability improvement. Similarly, the quantitative

correlation effect of organizational function α on

capability enhancement ϒ is 1, while the quantitative

correlation effect of capability enhancement ϒ on

organizational function α is 2. It shows that the

influence of capability enhancement on organizational

function α is greater than that of organizational

function α on capability enhancement.

The quantitative relevance of operational control

activities to the assessment of management

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

418

accounting tools is represented in a domain mapping

matrix, as detailed in Table 3. Among them,

comprehensive budget A, as a tool of strategy

implementation, is affected by the quantitative

correlation of organizational function α, control

activity β, and ability improvement, all of which are

5. Organizational function α is to define the mission

and rules of the organization, control activity β

advances the implementation goals, and capability

enhancement ϒ is to match and invest resources,

indicating that the operational control elements are all

important in influencing the quantitative relevance of

the comprehensive budget, and advancing the

comprehensive budget A is influenced by the

combination of organizational function α, control

activity β, and capability enhancement ϒ. At the same

time, another typical correlation is that the

quantitative correlation of organizational function α,

control activity β, and ability promotion affects

decision support G by 3, 2, and 1 respectively. It

shows that decision support G has a great correlation

with organizational process α, but ϒ is less affected

by ability improvement, and the influence of control

activity β on decision support G is between them.

Other management accounting tools are influenced

by the quantitative relevance of operational control

elements as detailed in Table 3.

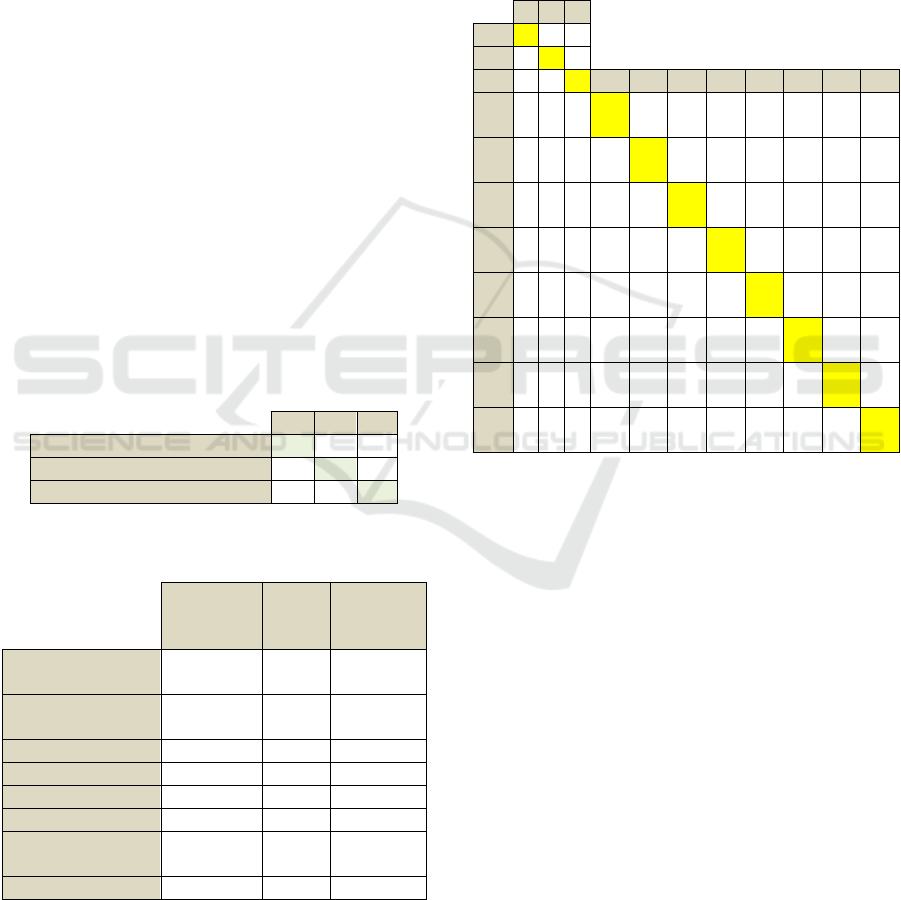

Table 2: Operational control dimension matrix DSM.

α β ϒ

Organizational function α α 4 2

Control activity β 5 Β 3

Ability improvement ϒ 1 1 ϒ

Table 3: Management accounting tools and operations

control matrix DMM.

Organization

al function α

Control

activity

β

Ability

improvemen

t ϒ

Comprehensive

budget A

5 5 5

Performance

evaluation B

5 4 3

Responsible body C 5 5 4

Lean cost D 3 4 5

Supply chain E 3 4 3

Sales support F 2 4 3

Integration of industry

and finance G

4 5 2

Decision support H 3 2 1

The multi-domain matrix is an analysis of the

characteristics of the application of management

accounting tools in a business and is reflected as an

intrinsic link between management accounting tools

in a business operations control environment. The

multi-domain matrix constructed by using

operational control dimension DSM (Table 2) and

domain mapping matrix (Table 3) is shown in Table

4, and the quantitative correlation between

management accounting tools is calculated according

to DSM method.

Table 4: Operational control and management accounting

tool MDM.

α β ϒ

α α 4 2

β 5 β 3

ϒ 1 1 ϒ A B C D E F G H

A 5 5 5 A

32

5

37

5

31

5

26

5

23

5

29

5

16

5

B 5 4 3

34

0

B

31

8

27

1

22

7

20

4

25

1

13

7

C 5 5 4

39

0

31

6

C

30

8

25

8

22

9

28

6

16

0

D 3 4 5

30

0

24

7

28

2

D

19

7

17

2

22

1

12

7

E 3 4 3

28

0

22

9

26

2

21

9

E

16

0

20

3

11

7

F 2 4 3

25

0

20

7

23

4

19

3

16

1

F

17

9

10

7

G 4 5 2

34

0

27

6

31

7

26

8

22

2

19

5

G

14

0

H 3 2 1

18

0

14

3

16

8

14

5

12

1

11

0

13

3

H

4.2 Quantifying the Correlation

between Management Accounting

Tools

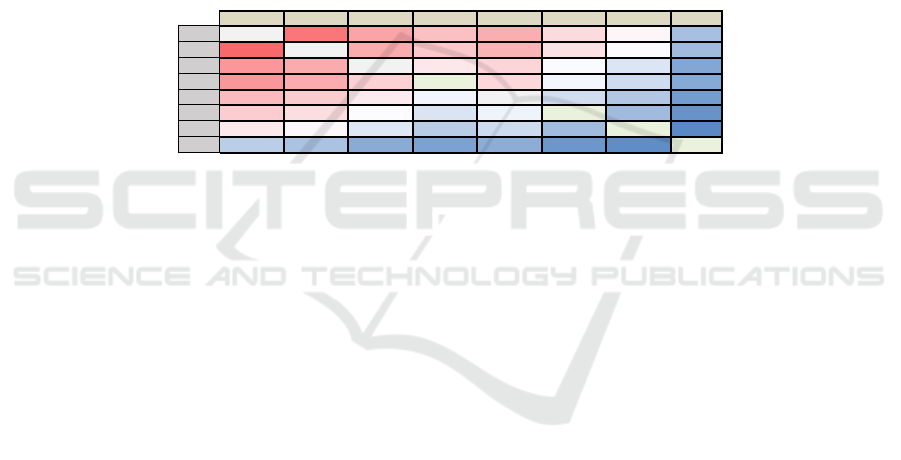

The management accounting tool DSM is derived

from the multi-domain matrix MDM (Table 4) by

optimizing the ranking according to the correlation

value and increasing the color scale, as shown in

Table 5. Firstly, the quantitative relevance of

comprehensive budgets to other management

accounting tools is at the top of the list. It can be seen

that the strategic position and function of

comprehensive budget have quantitatively verified

the position of the comprehensive budget as the core

tool of enterprise management and control. Secondly,

the quantitative correlation among comprehensive

budget, responsibility body, and performance

evaluation is above 316, which also shows that these

three management accounting tools together

constitute the key elements to enhance the operational

capability of enterprises. Thirdly, among the impacts

on the comprehensive budget, the quantitative

Research on Management Accounting Framework based on Hall Three-dimensional Structure and DSM

419

relevance of the responsibility body 390 ranks first,

the quantitative relevance of the performance

evaluation system 340, while the quantitative

relevance of the business-financial integration 340,

the quantitative relevance of the lean cost 300, the

quantitative relevance of the supply chain 280, the

quantitative relevance of the sales support 250, and

the quantitative relevance of the decision support

180, indicating that the responsible body is the core

element to achieve the budget decomposition.

Fourthly, the financial integration to comprehensive

budgeting is relatively large and must be considered

in the process of implementing the management

accounting framework. Fifthly, the quantitative

relevance of lean cost, supply chain, and sales support

to other management accounting tools is at the

medium level, which is related to the fact that they

are operation-oriented management accounting tools

and the management attributes supporting the

operation level. Sixthly, the quantitative correlations

among lean cost, supply chain, and sales support are

less than their quantitative correlations among

comprehensive budget, performance evaluation, and

accountability body, indicating significant

hierarchical nature of quantitative correlations among

management accounting tools. Seventhly, the

quantitative relevance of decision support to various

management accounting tools is weak, which is

related to the fact that decision support is based on the

information integration attribute of various

management accounting tools, and also related to the

fact that decision support is the management attribute

supporting the management of enterprises.

Table 5: Management accounting tool DSM.

A C B G D E F H

A A 375 325 295 315 265 235 165

C 390 C 316 286 308 258 229 160

B 340 318 B 251 271 227 204 137

G 340 317 276 H 268 222 195 140

D 300 282 247 221 D 197 172 127

E 280 262 229 203 219 E 160 117

F 250 234 207 179 193 161 F 107

H 180 168 143 133 145 121 110 G

To sum up, DSM is used to prove that there is a

quantitative correlation between the operation control

elements of the case enterprise and the management

accounting tools, as well as in the management

accounting tools, so as to demonstrate the

effectiveness of the enterprise operation matrix.

5 CONCLUSIONS

In order to overcome the defects of the former

management framework system lacking quantitative

research on the internal relationship between

management methods and operation control. Firstly,

this paper uses Hall's three-dimensional structure

model to construct a management accounting

framework based on operational control. Secondly,

taking the contingency elements such as

organizational structure, control methods, and ability

improvement as the logical dimension, this paper

studies the characteristics of enterprise operation

control, takes eight tools such as comprehensive

budget, performance evaluation, and responsibility

body as the knowledge dimension to promote the

application of management accounting and defines

the enterprise operation matrix accordingly. Finally,

a case study is conducted to verify the core role of

comprehensive budget in enterprise operation

management, and it constitutes the key method

affecting enterprise operation ability together with

responsibility body and performance evaluation. The

results reveal that there are significant correlations

and hierarchical characteristics among management

accounting tools.

REFERENCES

C. Ploder, T. Dilger, P. Schttle. (2020). Agile Project

Budgeting-Teaching the Combination of Agile Project

Management and Beyond Budgeting Basics. J.

Edulearn. 7,1145.

G. B. Loureiro, J. Ferreira, P. Messerschmidt. (2020).

Design structure network (DSN): a method to make

explicit the product design specification process for

mass customization. J. Research in Engineering

Design. 31(2), 197-220.

M. Cools, K. Stouthuysen, A. Van den Abbeele. (2017).

Management Control for Stimulating Different Types

of Creativity: The Role of Budgets. J. Journal of

Management Accounting Research. 29(3): 1-21.

M. Lima, G. Mazon, B. Castro, S. L. Bocasanta, José

Baltazar Salgueirinho Osório de Andrade Guerra.

(2021). The book, Strategic Planning for a Sustainable

Development Centre Using the Balanced Scorecard.

Cham: Springer International Publishing.

R. Malagueno, E. Lopez-Valeiras, J. Gomez-Conde.

(2018). Balanced Scorecard in SMEs: Effects on

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

420

Innovation and Financial Performance. J. Small

Business Economics. 51(1), 221-244.

S. K. Pareek, S. Mukherjee. (2021). Balanced Scorecard

and Its Application Through Strategic Management

Perspective in Real Estate Industry. J. Advances in

Smart Grid and Renewable Energy. 1,69-77.

T. Serebryakova, O. Gordeeva, O. Kurtaeva, A. Anisimov.

(2021). Theoretical framework of accounting and

analysis for value-based management. J. SHS Web of

Conferences. 94(5):01034.

Y. S. Choi, M. O. Kim, H. R. Jung, H. Cho. (2021).

Bargaining power and budget ratcheting: Evidence

from South Korean local governments. J. Management

Accounting Research. 53(3/4), 100767.

Research on Management Accounting Framework based on Hall Three-dimensional Structure and DSM

421