Research on the Development of Data Application under the

Background of Financial Technology

Wenjing Hu

School of Economics, Sichuan University, Chengdu, China

Keywords: Digital Economy, Financial Technology, Production Factor.

Abstract: In the context of the rapid development of digital economy, how can the financial sector make effective use

of data as a production factor, solve the problem of information asymmetry between financial institutions and

"long tail customers", improve the efficiency of data application, strengthen the protection of the legitimate

rights and interests and privacy of information subjects, and give better play to the important value of data in

promoting economic and financial development, It is worthy of in-depth research.

1 INTRODUCTION

The Fourth Plenary Session of the 19th Central

Committee of the Chinese Party Central proposed to

improve the mechanism that labor, capital, land,

knowledge, technology, management, data and other

production factors contribute by market evaluation

and determine remuneration according to

contribution. This is the first time that Chinese Party

Central Committee proposed to take data as a

production factor to participate in income

distribution, which reflects the keeping pace with the

times of the basic socialist economic system under

the background of the rapid development of digital

economy. It is a major theoretical innovation. In the

financial field, the People's Bank of China has built

credit investigation system with financial data. On

this basis, using non-financial data other than

financial data to solve the problem of information

asymmetry between financial institutions and "long

tail customers" is of great significance for giving play

to the basic role of data in leveraging financial

resources and serving inclusive finance. Therefore, in

the current era of big data with the rapid development

of financial technology, based on the pilot

establishment of data exchanges in some regions, the

financial field tries to use cloud computing,

blockchain, internet of things and other technologies

to further break the non-financial data barriers, but it

also leads to a series of problems such as excessive

use of data and infringement of the legitimate rights

and interests of data subjects. How to effectively and

reasonably apply data as a production factor under the

background of financial technology is worthy of in-

depth research.

2 CURRENT SITUATION OF

DATA APPLICATION UNDER

THE BACKGROUND OF

FINANCIAL TECHNOLOGY

We strongly encourage authors to use this document

With the accelerated breakthrough and application of

new generation data technologies such as cloud

computing, big data, blockchain, internet of things,

industrial internet, 5G and artificial intelligence,

human society has ushered in the era of digital

economy after agricultural economy and industrial

economy. In 2020, the scale of Chinese digital

economy will reach 39.2 trillion yuan, ranking second

in the world, accounting for 38.6% of Chinese GDP.

It is expected that the proportion of digital economy

in Chinese GDP will exceed 50% by 2025. Making

good use of data resources, strengthening the mining

of data value and giving full play to the role of data

as a key production factor will effectively promote

the high-quality development of Chinese economy.

Hu, W.

Research on the Development of Data Application under the Background of Financial Technology.

DOI: 10.5220/0011156900003440

In Proceedings of the International Conference on Big Data Economy and Digital Management (BDEDM 2022), pages 55-60

ISBN: 978-989-758-593-7

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

55

Table 1: The scale of Chinese Internet development.

Year

Digital

Economy

Electronic

Commerce

Internet of

Things

Artificial

Intelligence

2020 39.2 trillion 37.2 trillion 1.7 trillion 303.1billion

2019 35.8 trillion 34.8 trillion —— ——

2018 —— 31.6 trillion 1.2 trillion 33.9 billion

Data sources: China Internet development report 2021, China Internet development report

2020, China Internet development report 2019.

Under the background of financial technology,

the financial field has become one of the earliest and

most widely used fields of data resources. After the

People's Bank of China built the credit investigation

system with financial data to help credit risk control,

the financial field began to further mine non-financial

data in order to improve the ability to prevent and

control credit risks. This trend is basically the same

as that of developed countries. The United States first

proposed and applied non-financial data in the

financial field. Especially after the rapid development

of financial technology, a large number of non-

traditional standard data outside the financial field are

cleaned, sorted and processed by technical means and

applied to prevent and control credit risk in the

financial field. This phenomenon is regarded as the

breakthrough application of "non-traditional data" in

the United States. Since then, non-traditional

standard data has been widely used in the

development of all walks of life. In China, the value

mining of data, especially non-traditional standard

data, is mainly concentrated in a number of service

industries such as finance, retail, clothing, food,

housing and transportation, and its application in

agriculture and industry is still in its infancy. In other

words, the data application in the financial field is

exploratory, which is mainly reflected in the

following aspects:

First, help the financial institutions to achieve

precision marketing, by accurately classifying

customers through existing customer behavior data,

and predicting credit preferences of different types of

customers, so the financial institutions can conduct

more targeted marketing, recommend more suitable

financial products to customers, and improve

marketing efficiency. In addition, data application

also can help the financial institutions to reduce

ineffective costs in traditional marketing methods,

and improve customer satisfaction. Second, after

been provided data support for the development of

intelligent credit products, the financial institutions

can accurately match the customer credit amount and

interest rate for different types of customers,

implement low interest rate for low-risk customers

and high interest rate for high-risk customers, and

carry out automatic marketing and lending, so as to

effectively shorten the customer loan time and reduce

the manual input cost in the credit process. Third,

effectively prevent and control credit risk. For

example, in terms of anti fraud, compare existing

customer data to identify possible fraud by using the

advanced technology of big data, and mark more

suspicious fraud clues such as identity forgery by

applicating desensitization data shared among

financial institutions through blockchain and other

technologies.

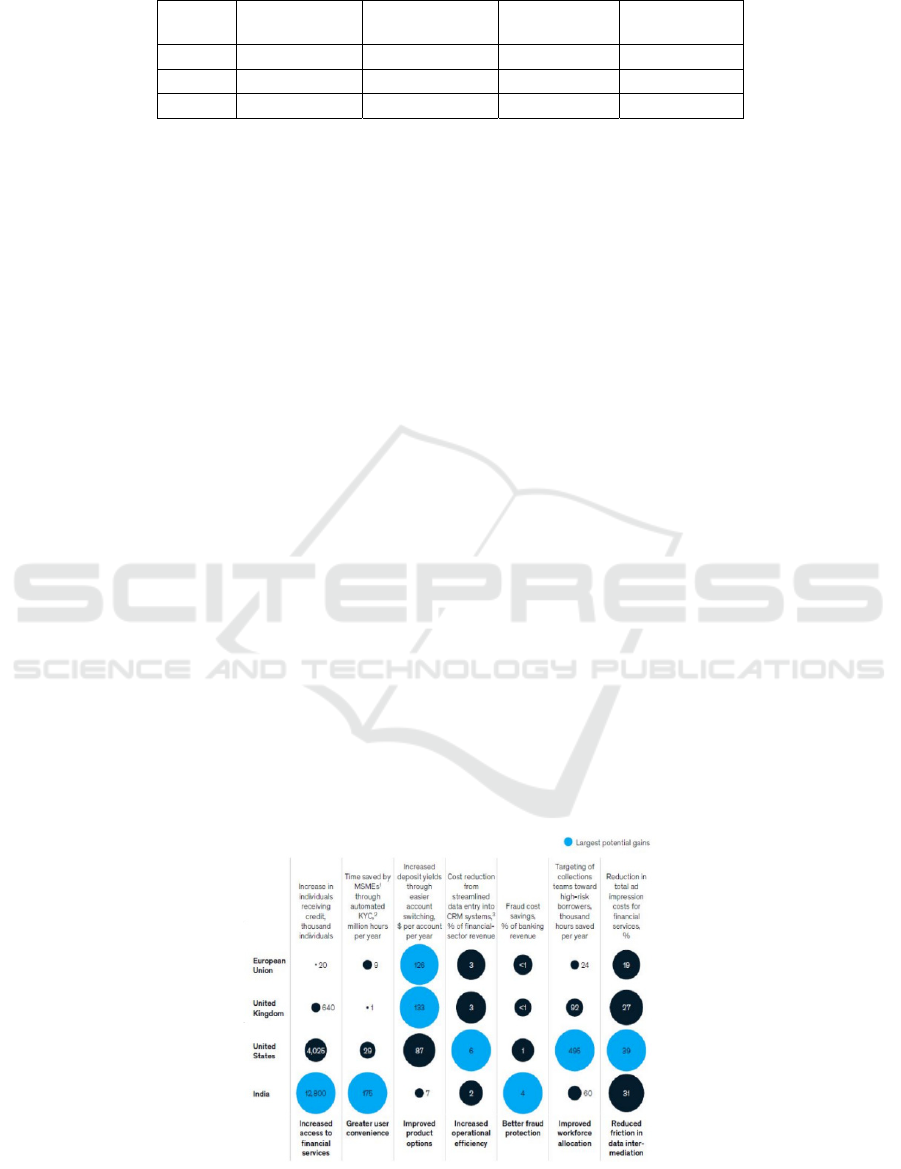

Sources: McKinsey, The value of open data for individuals and institutions.

Figure 1: Potential Gains from Open Data for Finance by 2030.

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

56

However, the support level of data application in

the financial field in different countries is different,

and the data application modes are also different

among countries. In addition, there are great

differences in the value generated by data application

due to the differences in market conditions, the

robustness of digital financial infrastructure and

regulations.

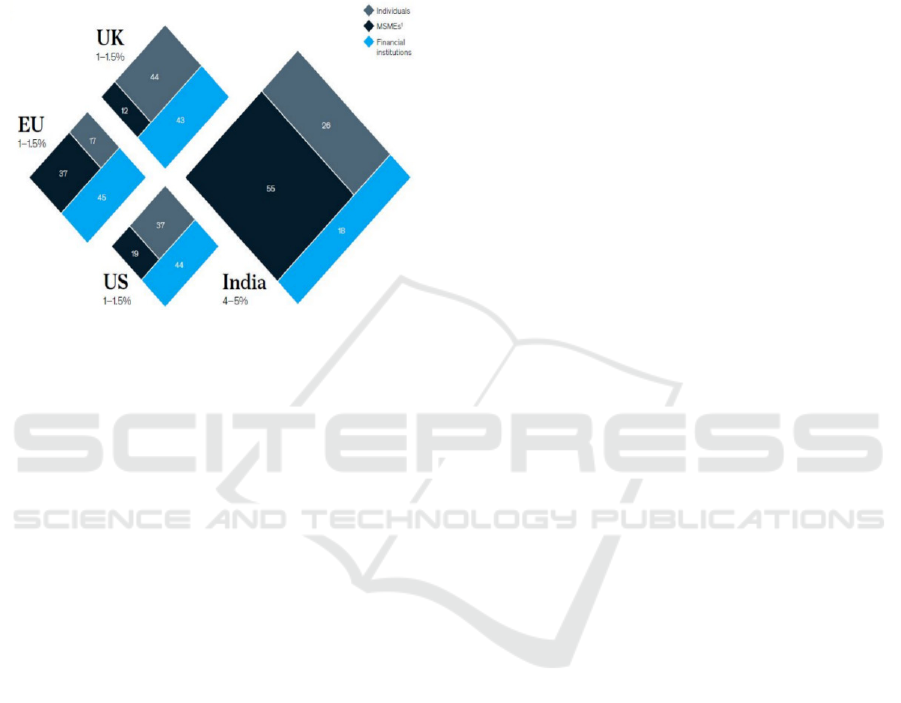

Sources: McKinsey, The value of open data for individuals and

institutions.

Figure 2: Potential GDP Impact by 2030 by Broad

Attribution to Market Participants, % of GDP.

On June 24, 2021, McKinsey released the

research report Financial data unbound: The value of

open data for individuals and institutions. Combined

with the actual situation of different economies such

as the European Union, India, the United States and

the United Kingdom, the report analyzes the main

mechanisms and values of openning and sharing

financial data. According to the report, by 2030, the

wide use of openning data ecosystem in the EU, the

UK and the United States, may promote the economy

as high as 1.5% of GDP, and India may be as high as

4% to 5%. However, due to the lack of breadth of data

sharing in the European Union and the lack of

standardization of financial data in the United States,

the potential value that the United States and the

European Union can obtain from financial data is

expected to less than 10%; The UK's data ecosystem

is more perfect, but the breadth of data sharing is still

not enough. The potential value that can be obtained

is expected to account for 30-40%; India's data

aggregator provides a high level of standardization

and wide sharing for sharing data, enabling India to

obtain 60% - 70% of the potential value from

financial data. In other words, for emerging

economies, due to the current low level of financial

access and financial depth, the credit needs of

individual business and enterprises have not been

met. With the more data application in the financial

field, the possibility of obtaining loans has been

improved. Once these economies obtain loans and put

them into production and operation, every unit of real

capital will be increased, it will bring greater

economic growth potential, and create great value. As

a developing country, China has huge data that can be

used as a production factor and applied in the

financial field. At present, on the premise of the

legitimate rights and interests protection of data

subjects, we need to seize the opportunity of the rapid

development of financial science and technology,

make more data resources and create more economic

value in the financial field, and make finance truly

serve economic development.

3 PROBLEMS EXISTING IN THE

DATA APPLICATION IN THE

FINANCIAL FIELD

3.1 After Data Became a Production

Factor, the Constraint of Data

Application Has Increased

The application of massive data has subverted the

traditional credit risk control mode and efficiency in

the financial field. Financial institutions obtain

customer data authorization by signing agreements

for credit risk control, and use the data to post loan

management and other links of credit activities. More

and more non-traditional standard data has been

applied in inclusive finance. It enterprise financing

and the internet finance have gradually expanding the

scope of financial services to "long tail customers"

without credit data, increasing the loan availability of

them, and effectively promote the in-depth

development of the financial market. However, after

data becomes a production factor, customers also put

forward more demands on the ownership and even

derivative value of their own data, by requiring

stricter standardization and management of data. If

the data is applied arbitrarily in the financial field

without restriction and its economic value is obtained

by the financial institutions, the legitimate interests of

the data subject will be damaged, especially when the

data is applied without authorization and consent,

which will affect the feasibility of data application.

Therefore, the data application in distribution as a

new production factor also puts forward higher

compliance and value-added requirements for data

flowing, sharing, trading and other behaviors in the

financial field (Chang 2018).

Research on the Development of Data Application under the Background of Financial Technology

57

3.2 The Data Standard Has Not Been

Established, Which Reduces the

Efficiency of Data Application

At present, the data application in finance field is

carried out by financial institutions relying on their

own credit system, and the credit system among

different financial institutions have different

structures, that will result in some differences in the

application processes such as data acquisition and

cleaning. In particular, the data acquisition boundary

has not been unified, and some small financial

institutions with weak risk control capabilities are at

the stage of blind obedience in data application, and

a large number of useless data are added to the scope

of application. On the one hand, the accuracy and

efficiency of data application may be reduced,

resulting in rights protection events. On the other

hand, the structure and continuity of data is very

important for the efficient and beneficial of data

analysis, if a large number of fragmented and

unstructured data is incorporated into the application

scope, the corresponding work links such as

collection, calculation and cleaning will lead to a

significant increase in the cost of data application.

The fragmented and unstructured of data may also

lead to the change or disappearance of many signals

hidden in the data over time, and that will change the

accuracy of the model.

3.3 The Algorithm Opacity Brought by

Technology will Affect the Data

Application

The most distinctive feature of digital economy is

taking data as the key production factor, participating

in wealth creation, adopting the operation mode of

"data + algorithm + product", and finally tending to

be "intelligent" form. The data application in

financial field, such as credit scoring, often based on

the data model of complex calculus, that will lead to

the lack of explicability of the application methods,

and unequal treatment or discrimination in financial

services (Ba, Hou, Tang, 2016). In addition,

fragmented data often lacks historical records, and

can not be accessed publicly, so it is difficult to carry

out backtracking test, which also challenges the

accuracy of data application. And due to the different

data application methods among different financial

institutions, some data are collected and accessed in

real time, some data are stored regularly by technical

means, that will result in uncertainty and low

economic efficiency of data application.

3.4 Credit Agencies May Bring New

Independent Credit Risks

With the rapid development of financial technology,

credit agencies, relying on their technical advantages

such as data mining, begin to collect and process

various behavior data in a comprehensive, multi

angle and multi-level manner, and as the risk control

party, to attract customers and provide credit services

for financial institutions, such as providing

suggestions of credit decision, sharing a part of credit

profits and bearing a part of credit risks. With the

gradual refinement of social division of labor, the

technical advantages of credit agencies become more

prominent. However, with the deeper and deeper

involvement of credit agencies in credit business,

especially when their role changes from the provider

of data to the processor of data products for financial

institutions, and even replaces the credit risk control

role of financial institutions, a series of independence

risks will be caused by interest conflicts. Especially if

the financial institutions only bear a small part of the

credit business risk, and most of the risk is borne by

government departments or guarantee companies, the

financial institutions will reduce their input costs in

data collection, processing and other links as far as

possible from the perspective of driving profit, and

rely on credit agencies to make credit decisions (Ye

2015).

4 POLICY SUGGESTIONS ON

DATA APPLICATION IN THE

FINANCIAL FIELD

Financial technology is a double-edged sword for

data application, which needs to be treated

dialectically. We should not only recognize its

advantages in expanding traditional data sources, but

also recognize its disadvantages in personal privacy

and data security, so as to give better play to the value

of data as a production factor in promoting economic

and financial development.

4.1 Strengthen the Protection of the

Legitimate Rights of Data Subjects

First, improve legislation. Personal Information

Protection Act, Data Security Act, Data Transaction

Rule and other laws, clarify the rights and obligations

of data, infringement form and compensation system

of data, and realize the legal using of data and the

rights protection of the data subjects. Especially in the

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

58

context of trade internationalization, we should pay

attention to the data application of the process of

cross-border data flow. For example, increase the

research on data opening and sharing, actively

participate in the research and formulation of

international rules, promote the legislation of cross-

border data flow, and strengthen the classified

management and risk assessment of cross-

border data.

Second, make full use of financial technology to

protect the business secrets and privacy of data

subjects. Build a complete and effective data security

guarantee system and data management system to

ensure the security of the whole life cycle of data,

such as data collection, processing, using and sharing.

For example, use the blockchain technology to make

the data exchange between nodes follow a fixed

algorithm, ensure data security and the privacy of

data subjects from the underlying technical

architecture, and solve the problem of trust between

nodes. At the same time, improve the data

authorization and objection handling mechanism, and

strictly protect the credit rights and interests of data

subjects, such as the right to know, the right to

objection, the right to correction and the right to

repair.

4.2 Promote the Establishment of the

Right Confirmation and Pricing

Mechanism of Data as a Production

Factor

First, clarify the data property rights. Explore and

improve the data property rights identification rules

according to the characteristics of data generation

conditions and processing methods, establish a

perfect data transaction mechanism on the basis of

clear property rights, and build reasonable transaction

rules and equity distribution model, establish a

trading market of all kinds of data, promote the

smooth flow and efficient application of data in the

financial field, and give play to the important role of

data in improving productivity and promoting

economic development. Second, improve intellectual

property protection. Effectively ensure the innovative

development of data mining, analysis, modeling and

other technologies, and promote the effective

transformation of data resources into data products,

which support the development of information

economy. Promote professional data application

institutions such as credit agencies to play a more

important role in collecting market transactions and

other economic activity data, encourage them to

participate in the collection, transaction and

application of data, provide better credit investigation

products for enterprises and farmers, and promote the

healthy and vigorous development of digital

economy (Pian, Xie, 2020).

4.3 Clarify the Data Collection and

Application Standards

First, promote the standardization of data collection.

In view of the different of formats and quality of

unstructured data, establish a unified data collection

and processing mode, strengthen the anonymization

and de identification of data, ensure the scientificity

and unity of data collection, and prevent differential

discrimination caused by data processing or

infringement of the rights and interests of data

subjects (Yang, Tian, Liu, 2021). Second, establish a

unified data application specification according to the

risk characteristics presented by the type and

application of data. Establish a new application mode

composed of computer related technologies such as

point-to-point transmission, distributed storage,

consensus mechanism and encryption algorithm. In

this mode, distributed data storage generates

interconnected data blocks and stamped with time

stamps to form an open and transparent time series

chain and improve the efficiency of data application

(Talin, Li, 2018). Third, strengthen the construction

of financial infrastructure. Promote the

interconnection of various infrastructures, give play

to the advantages of financial infrastructure in data

circulation and security protection. And on this basis,

research and demonstrate the establishment of a data

sharing center or the pilot of financial data sharing

relying on the existing system to promote the security

protection and open utilization of financial data (Ju,

Zou, Fu, 2018).

4.4 Strengthen the Supervision of Data

Application in the Financial Field

First, credit agencies establishe independent system

of department, personnel and salary. Credit agencies

should establish a clear internal organizational

structure and a responsible firewall system, ensure

the collection of customer information, the design of

risk model and other credit departments are

independent of other departments such as business

marketing, and ensure that the compensation of credit

department personnel is not related to the scale of

financial institution credit business. At the same time,

credit agencies shall establish an independent

compliance department to supervise the compliance

status of credit reporting department and personnel.

Second, financial institution should deeply

Research on the Development of Data Application under the Background of Financial Technology

59

participate in the whole process of designning the risk

control mode, and negotiate with credit agenies on

key elements such as specific data items and model

weighting coefficient of risk control model.

Especially when the defect rate of credit business

exceeds a certain value, both parties should find out

the cause in time and adjust the model parameters.

Third, financial institution should independently

carry out secondary risk control. The risk control

function of credit agenies can not completely replace

the offline investigation and secondary risk control of

financial institution. Financial institution should

make independent credit decisions on the basis of

comprehensive analysis of the credit reports provided

by credit agenies and Credit Reference Center of The

People's Bank of China, and comprehensive

understanding of the actual business situation of

customers, so as to reduce the dependence on the

credit agenies.

5 CONCLUSIONS

At present, the data application in Chinese financial

field is still in its infancy, but with the rapid

development of financial technology, data

application will usher in explosive development. The

improvement of data subjects' awareness of their own

rights and interests protection, the lack of data

application standards, the opacity of application

algorithms, and the independence of professional data

application institutions such as credit agenies will

become obstacles to the development of data

application. Therefore, we proposes to strengthen the

protection of the legitimate rights and privacy of

data subjects by improving legislation and scientific

and technological support, protect data property

rights by establishing the right confirmation and

pricing mechanism of data, promote the security

protection and open utilization of financial data by

clarifying the data collection and application

standards, and ensure the independence and

effectiveness of data application in the financial field

by increasing supervision.

REFERENCES

Ba Shusong, Hou Chang, Tang Shida (2016), current

situation, problems and optimization path of big data

risk control [J], financial theory and practice, issue 2

(439 in total), 23-26.

Chang Zhenfang(2018), research on the construction of

Internet financial credit system and risk management

[D], Doctoral Dissertation of Nanjing University.

China Internet association (2020), China Internet

development report 2019 [R]

https://www.isc.org.cn/article/37331.html.

China Internet association (2020), China Internet

development report 2020 [R],

https://www.isc.org.cn/article/37989.html.

China Internet association (2021), China Internet

development report 2021 [R],

https://www.isc.org.cn/zxzx/xhdt/listinfo-40203.html.

Ju Chunhua, Zou Jiangbo, Fu Xiaokang(2018). Design and

Application Research of big data credit investigation

platform integrated with blockchain technology [J].

Computer science, 11: 522-526,552.

McKinsey (2021), Financial data unbound: The value of

open data for individuals and institutions[R],

https://www.mckinsey.com/industries/financial-

services/our-insights/financial-data-unbound-the-

value-of-open-data-for-individuals-and-institution.

Pian Yuanyuan, Xie Yu (2020). Construction of multi

platform Internet credit investigation system based on

blockchain technology [J]. Credit investigation,4: 22-

26.

Talin, Li menggang(2018). Analysis on the application

prospect of blockchain in the field of Internet financial

credit investigation [J]. Journal of Northeast University

(SOCIAL SCIENCE EDITION),9: 466-474.

Yang Yuyan, Tian Kun, Liu Yuanzhao (2021), Theoretical

and practical exploration of financial technology

sharing platform based on alliance chain [J]. Credit

investigation, 6: 64-68.

Ye Wenhui (2015), Operation mode and regulatory

Countermeasures of big data credit agencies -- Taking

Alibaba sesame credit as an example [J]. International

finance,8: 18-22.

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

60