The Effect of Financial and Financial Technology Literation on

Financial Inclusion

Meiryani, Jessica Elizabeth, Andreas Chang and Yen Sun

Bina Nusantara University, Jakarta, Indonesia

Keywords: Financial Literacy, Financial Inclusion, Financial Technology, SME.

Abstract: The purpose of this study was to determine the effect of financial literacy and financial technology on financial

inclusion. This research method is carried out by distributing questionnaires to SME (Small Medium

Enterprises) respondents in West Jakarta area. The sample in this research used 130 respondents and statistical

testing was carried out using SPSS 25. The results showed that only financial literacy had a positive effect on

financial inclusion, while other independent variables had no effect on financial inclusion. It can be concluded

that financial literacy has an influence on financial inclusion because when someone has a high literacy level,

their ability to apply financial products and services is also wiser.

1 INTRODUCTION

The economic development of a country cannot be

separated from the financial sector and the role of the

government. In developing the financial sector, a

country is expected to increase access to financial

services. The mindset of the people in some areas of

the capital city of Jakarta is still modest in responding

to financial problems and the lack of socialization of

the importance of financial institutions and the

awareness of the people of Jakarta cannot be said to

have developed. So there is a need for changes that

bring people more inclusively in utilizing existing

financial access. Under these circumstances, people

need strong financial literacy to improve their welfare

and prevent being exposed to fraud in the financial

sector. Financial literacy is important because with

financial literacy, financial inclusion can be formed.

Thus, financial literacy is intended for anyone,

especially for middle and lower class people who

really need clearer knowledge of financial

instruments. MSMEs are micro, small and medium

enterprises. In growing the economic growth of the

UMKM community, it has a big contribution.

According to the Ministry of Education and Culture

(Culture, 2016), literacy is the ability to access,

understand, and use something intelligently through

various activities, including reading, viewing,

listening, writing and speaking.

According to the World Bank, financial inclusion

is a major supporting factor in reducing poverty and

increasing welfare. Financial inclusion itself is

defined as access to financial products and services

that are useful and affordable in meeting the needs of

the community and their businesses in terms of

transactions, payments, savings, credit and insurance

that are used responsibly and sustainably. The

elements that play a role in financial inclusion are

access, availability of financial products and services,

use and quality which are expected to reduce the

number of people who do not have bank accounts

because they do not have access to banking services.

There are many benefits that can be obtained when

financial inclusion has been achieved, such as

increasing economic efficiency and supporting

financial system stability. Before achieving financial

inclusion, several factors are needed to improve it, so

the public must understand financial inclusion. Along

with the development of information technology and

supported by a fast internet penetration rate, several

digital financial services have emerged that make it

easier for people to make transactions and to obtain

financing. The digital service in question is Financial

Technology, abbreviated as fintech. Based on

Pribadino (2016), Financial Technology (fintech) is a

combination of technology and financial features or it

can also be interpreted as innovation in the financial

sector with a touch of modern technology. Based on

the descriptions that have been previously described

74

Meiryani, ., Elizabeth, J., Chang, A. and Sun, Y.

The Effect of Financial and Financial Technology Literation on Financial Inclusion.

DOI: 10.5220/0011243200003376

In Proceedings of the 2nd International Conference on Recent Innovations (ICRI 2021), pages 74-79

ISBN: 978-989-758-602-6

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

in the above problem, the research problem can be

formulated as follows:

• Does financial literacy affect the financial

inclusion of the MSME community in West

Jakarta?

• Does financial technology affect the financial

inclusion of the MSME community in West

Jakarta? Based on the formulation of the

problem, the objectives of this study are to:

• To find out whether financial literacy affects

the financial inclusion of the people of West

Jakarta.

• To find out whether the effect of financial

technology on financial inclusion in West

Jakarta society.

2 THEORETICAL FRAMEWORK

2.1 The Effect of Financial Literacy on

Financial Inclusion

There are several supporting components to get the

welfare of the people in Indonesia. The components

in question are in the form of economic growth,

poverty reduction, income distribution and financial

system stability. By using instruments for policy in

the form of financial literacy and financial inclusion

seen from various aspects such as economic

conditions, demographic conditions, and

geographical conditions and cultural conditions in

Indonesia (Sari and Dwilita, 2018). The decision of

business actors to access capital from financial

institutions and manage their finances with various

related parties certainly illustrates how the level of

financial inclusion is defined as a situation in which

all adults of working age have effective access to

credit, savings, payments, and insurance from formal

service providers. Financial inclusion data in

Indonesia shows the level of financial inclusion at

67.8% in 2016, which increased by 8.1% from the last

survey in 2013, which was 59.7%. This means that

the Indonesian people have access to formal financial

service institutions. To achieve a good level of

financial inclusion, an individual or a business actor

must go through a decision-making process to use the

resources they have. With the era of globalization, the

influence of modernization has brought socio-cultural

changes in Indonesian society from a traditionalist to

a more modern one and is reflected through

increasingly advanced public financial management

patterns and utilizing financial products and services

from formal financial institutions (Sari and Dwilita,

2018). However, not all Indonesian people have

accepted this modernization.

Some regions in Indonesia still use traditional

(non-formal) institutions to facilitate the financial

needs of these communities because they are based

on the principles of trust and respect for customs

which are quite strong and make Indonesians more

comfortable to carry out financial activities through

traditional institutions compared to formal financial

institutions (Sari and Dwilita, 2018). One of the target

groups of SNLKI (National Strategy for Indonesian

Financial Literacy) in 2017 is MSMEs (Micro, Small

and Medium Enterprises). MSMEs have an important

and strategic role in denominational development in

Indonesia and play a role in absorbing workers in

Indonesia and distributing development products. In

the process of developing MSMEs can be facilitated

by the financial market, and can lead to substantial

poverty reduction which will affect national

economic growth (Fauzan and Ahmad, 2019).

Sanistasya et al. (2019), suggested that financial

institutions be more active in providing education for

the products and services offered and adjusting the

needs of MSMEs from time to time so as to encourage

them to develop more. So, the writer formulates the

fifth hypothesis which is in the form:

H5: Financial literacy has an influence on the

financial inclusion of the MSME community in the

West Jakarta area.

2.2 The Influence of Financial

Technology on Financial Inclusion

In the current era of globalization, technological

progress is a new driver of economic growth.

Especially when it is related to the financial sector,

fintech has been able to become a new instrument

with the hope of increasing financial growth and

financial inclusion. fintech itself has become popular

in recent years. In essence, fintech is a financial

service based on innovative technology that is

integrated online to facilitate various transactions

such as installment payments, insurance premiums,

household bills, money transfers, balance checks,

funding, investments and others (Alimirruchi, 2017).

The basic forms of Fintech include payments (Digital

Wallets, P2P Payments), investment (Equity

Crowdfunding, Peer to Peer Lending), financing

(Crowdfunding, Microloans, Credit Facilities),

insurance (Risk Management) and crossprocess (Big

Data Analysis, Predictive Modeling) ), as well as the

security infrastructure of Fauzan Ahmad (Fauzan and

Ahmad, 2019).

The Effect of Financial and Financial Technology Literation on Financial Inclusion

75

From the diversity of forms of fintech, it has

become the main support in facilitating various

community activities in Indonesia. The recent strong

role of fintech in achieving public access to easy

access to finance is likely to have an impact that will

be able to increase financial inclusion in Indonesia.

Previous research stated that fintech was able to

increase financial inclusion and financial literacy

quite well, (Sari and Kautsar, 2020). In addition,

increasing financial inclusion through digitalization

of banks that are integrated with fintech has a positive

effect in increasing financial inclusion (Yoshino and

Morgan, 2017). Research by Annisa et al (2019). with

the title ”DETERMINING FACTORS OF

FINANCIAL INCLUSION IN INDONESIA” said

that financial technology has a significant

contribution in increasing financial inclusion. With

the existence of financial technology, people who

previously did not have formal banking accounts now

have accounts in various technologybased financial

services. Thus, the authors formulate the sixth

hypothesis, namely in the form of :

H6: Financial Technology has an influence on the

financial inclusion of the MSME community in the

West Jakarta area.

3 RESEARCH METHODOLOGY

This research uses quantitative methods. The

variables in this study use a Likert scale, where the

distribution of questionnaires focuses on people who

have their own businesses or MSMEs (Micro, Small

and Medium Enterprises). The determination of the

number of samples in this study used the Hair

formula, so that there were 130 respondents who had

to fill out a questionnaire. The test which is done is

validity and reliability test. This research was

conducted from September 2020 to February 2021.

The method of presenting data used in this study is a

method of documentation, the data obtained is

documented in tabular form, after which it is

processed using predetermined methods. Researchers

use multiple linear regression as a data processing

tool to determine the effect of independent variables

on the dependent variable.

Researchers used SPSS 25 as a tool or application

in this study. The determination of the number of

samples used in this study is based on the Hair

formula. According to Hair et al. (2019), determining

the number of representative samples depends on the

number of indicators used multiplied by five to ten

observations. According to Hair et al. (2019), the

sample size should be 100 or larger. As a general rule,

the minimum sample size is at least five times as

many as the number of question items to be analyzed,

and the sample size. Therefore, in this study, the

number of samples used is multiplied by 5, so that the

minimum sample used is 130 MSMEs. Hair formula

is as follows:

• Number of Samples = Total Indicators × 5 =

26 × 5 = 130 Thus, the number of samples to

be used in this study is 130 samples.

• Sampling Unit While the sample is part of the

number and characteristics of the population

(Sugiyono, 2010) Therefore, the samples of

this study are: MSMEs domiciled in West

Jakarta.

• Method of collecting data In this study,

researchers obtained data using primary data

collection methods, namely by using a

questionnaire or questionnaire. The

questionnaire is a data collection technique

that is carried out by giving a set of questions

or written statements to the respondent to

answer (Sugiyono, 2010). The questionnaire is

an efficient data collection technique if the

researcher knows exactly what variables to

measure and what can be expected from the

respondent. In addition, a questionnaire is also

suitable if the number of respondents is large

enough and spread over a large area.

Questionnaires can be in the form of closed or

open questions / statements, can be given to

respondents in person or sent by post, or the

internet.

4 RESULT AND DISCUSSION

This study uses primary data obtained from

distributing questionnaires using google form.

Respondents in this study focused only on people

who have businesses or UMKM (Micro, Small and

Medium Enterprises). Researchers used the Hair

formula with a sample of 130 SMEs and the number

of questionnaires distributed was 171 pieces. The

number of respondents obtained was 130 respondents

who filled in the data completely without a single

unanswered question.

4.1 Description of Research Objects

The object of research in this study is financial

literacy and financial technology on financial

inclusion. The statements in the questionnaire are

ICRI 2021 - International Conference on Recent Innovations

76

answered using a Likert scale with the following

ratings.

4.2 Descriptive Statistical Analysis

Results

Descriptive statistics serve to describe or provide an

overview of the object under study through sample or

population data (Sugiyono, 2010). Data presentation

in the form of tables, graphs, diagrams, and quantities

such as minimum, maximum, sum, mean, and

standard deviation.

4.3 Validity Test Results

It can be seen that the validity measurement for

financial literacy variables using Pearson Correlation

shows that the R value obtained from the results of

running SPSS 25 is greater than the R-Table (R-Table

= 0.1723). It can be concluded that all questions made

by researchers based on reference journals can be

declared valid, so that 10 questions representing

financial literacy variables can be used for the

questionnaire. Then the measurement of the validity

for the financial technology variables which consists

of 6 questions describes each valid question to

represent the financial technology variables. The R

value from running SPSS 25 using Pearson

Correlation has a value above the R-Table (R-Table

= 0.1723) so it can be said that all of them are valid

and can be used for distributing questionnaires. The

last 10 questions that represent financial inclusion

variables can be declared valid because the R value

from running SPSS 25 is above the R-Table value (R-

Table = 0.1723) so that these questions can be used in

distributing questionnaires.

4.4 T-test Results

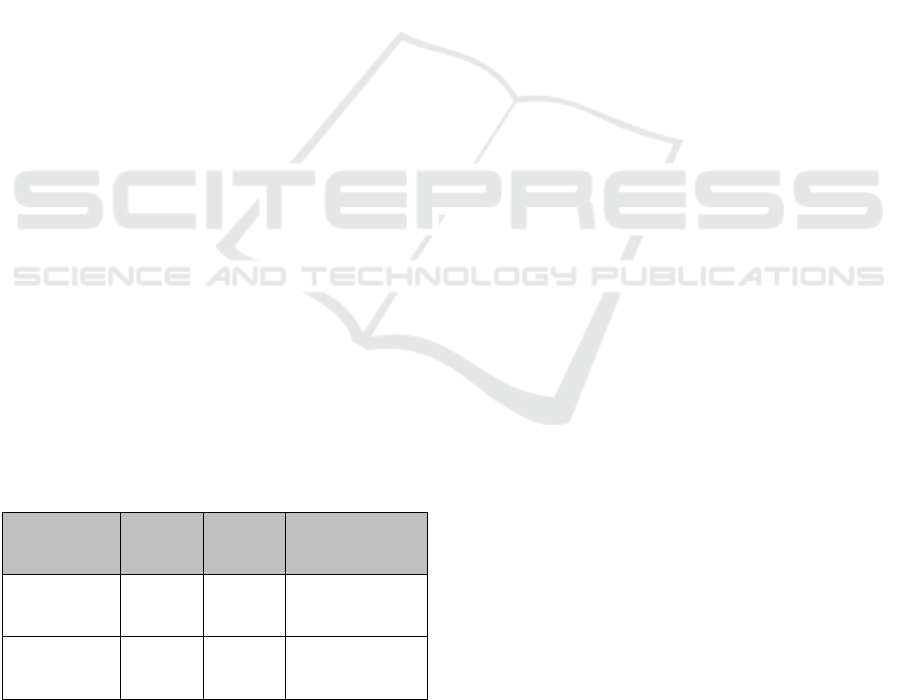

Table 1: T Test Results.

Independent

Variable

Beta Sig. Conclusion

Financial

Literac

y

0,585 0,000 Has influence

Financial

Technolo

gy

0,027 0,763 Has no influence

T test was conducted to determine the effect of

each independent variable partially on the dependent

variable. If the significance value is below 0.05, it can

be said that the independent variable has an influence

on the dependent variable. Meanwhile, if the

significance value is above 0.05, it can be said that the

independent variable has no influence on the

dependent variable. There is 1 independent variable

that has an influence on financial inclusion. The

independent variable that affects the dependent

variable is financial literacy. Meanwhile, the financial

technology variable has no influence on financial

inclusion because it has a significance value above

0.05. Financial literacy variables have an influence on

financial inclusion.

4.5 T Test Results

The F test is carried out to see whether the

independent variables together have an influence on

the dependent variable. If the significance value is

below 0.05, it can be said that the independent

variables jointly have an influence on the dependent

variable. Meanwhile, if the significance value is

above 0.05, it means that the independent variable has

no effect on the dependent variable. It can be

concluded that the significance value of the F test is

0.000, so it can be said that the variables of financial

literacy and financial technology together have an

influence on the financial inclusion variable

4.6 R-Square Test Results

The R-Square test is used to predict and see how

much influence the variable x contributes to the

variable y together. The R-Square value obtained

from SPSS 25 processing is 0.362, which means that

the independent variable describes 36.2% of having

contributed to the financial inclusion variable.

Meanwhile, 43.9% is described by other variables

which are not used in this study.

5 CONCLUSION AND

SUGGESTION

5.1 Conclusion

After the researcher processes and tests the data,

conclusions can be drawn from the results of the

hypothesis as follows:

• Testing the first hypothesis in the form of the

effect of financial literacy on financial

inclusion. Based on the results of the research

that has been done, it can be seen that the

significance value of the financial literacy

variable <0.05 is 0.000. According to Chen

The Effect of Financial and Financial Technology Literation on Financial Inclusion

77

and Volpe (1998), someone who has high

financial literacy will have higher success.

• The second hypothesis testing is the effect of

financial technology on financial inclusion.

Based on the results of the research that has been

done, it can be seen that the significance value of the

variable financial technology

> 0.05 is 0.303.

According to Aribawa (2016), it is stated that

financial technology is used by companies and banks

to enter into new market sectors, so it can be said that

financial technology is not a major factor because its

main purpose is to penetrate new markets.

5.2 Suggestion

Based on the research that has been done, there are

several suggestions that can be used as material for

consideration for further researchers, the government

and the banking sector.

• The next researcher, Further researchers are

expected to conduct research in more detail

and be able to describe what factors most

influence financial inclusion, so as to assist the

government in evaluating programs related to

financial inclusion. In further research, it is

hoped that researchers can reveal financial

technology products in more detail, so that the

research is more specific.

• Government, This research is expected to

serve as an illustration for the government to

evaluate activities related to financial

inclusion, whether they are effective or require

improvement. So that the even distribution of

financial inclusion can be evenly distributed

from Sabang to Merauke.

• Banking, This research is expected to assist

banks in formulating programs that will

support government financial inclusion

programs so that assistance from banks can

make it easier for the government to

implement activities that support equitable

distribution of financial services.

REFERENCES

Ali, N., Fatim, K., & Ahmed, J. (2019). Impact Of Financial

Inclusion On Economic Growth In Pakistan. Pakistan:

Pakistan Economic and Social Review.

Alimirruchi, W. (2017). Analyzing Operational and

Financial Performance on the Financial Technology

(Fintech) Firm. Semarang: Diponegoro University

Amaliyah, R., & Wistiatuti, R. S. (2015). Analysis Of

Factors Affecting The Level Of Financial Literation In

Tegal City MSMEs. Semarang: Department of

Management, Faculty of Economics, Semarang State

University, Indonesia.

Annisa, Y. N., Setyadi, S., & Arifin, S. (2019). Determining

Factors Of Financial Inclusion In Indonesia. Indonesia:

Sultan Ageng Tirtayasa University.

Aribawa, D. (2016). The Effect Of Financial Literation On

The Performance And Sustainability Of MSMEs In

Central Java. Yogyakarta: Atma Jaya Yogyakarta

University.

Atkinson, A., & Messy, F.-A. (2015). Measuring Financial

Literacy: Results of the OECD / International Network

on Financial Education (INFE) Pilot Study. OECD

Publishing.

Bank Indonesia. (2014, January 27). Inclusive Finance

Booklet. Retrieved from www.bi.go.id: www.bi.go.id

Chen, H., & Volpe, R. P. (1998). An analysis of personal

financial literacy among college students. Financial

Services Review, 7 (1), 107–128.

Demirguc-Kunt, A., Beck, T., & Honohan, P. (2015).

Finance for All Policies and Pitfalls in Expanding

Access. Washington: World Bank.

Dorftleitner, Hornuf, Schmitt, & Weber. (2017, Sunday

March). Coursehero.com. Retrieved from Coursehero:

http://www.coursehero.com

Evans, O., & Adeoye, B. (2016). Determinants of Financial

Inclusion in Africa: A Dynamic Panel Data Approach.

Africa: University of Mauritius Research Journal.

Fanta, A. B., & Mutsonziwa, K. (2016). Gender and

Financial Inclusion: Analysis of financial inclusion of

women in the SADC region. SADC: FinMark Trust.

Fauzan, & Ahmad. (2019). The Role of Financial

Technology in Improving Inclusive Finance in

MSMEs. . BJB University Journal, 5 (5), 1–14.

Hair, J., Black, W., Babin, B., & Anderson, R. (2019).

Multivariate Data Analysis: A Global Perspective.

Louisiana: Pearson.

Hsueh. (2017, March 10). Coursehero.com. Retrieved from

course hero: http://www.coursehero.com.

Culture, K. P. (2016). School Literacy Movement Pocket

Book. Jakarta: Ministry of Education and Culture.

Mwathi, A. W., Kubasu, A., & Akuno, N. R. (2019). Effects

of Financial Literacy on Personal Financial Decisions

among Egerton University Employees, Nakuru County,

Kenya. Kenya: International Journal of Economics,

Finance and Management Sciences.

Financial Services Authority. (2015, February 2018). OJK

creates financial habitats for students to become

financially literate. Retrieved from Consumer

Education: http://sikapiuangmu.ojk.go.id/

Financial Services Authority. (2016). Presidential

Regulation of the Republic of Indonesia Number 82 of

2016 concerning the National Strategy for Financial

Inclusion (SNKI). Jakarta: Financial Services

Authority.

Financial Services Authority. (2016). National Survey of

Financial Literacy and Inclusion. Jakarta: Financial

Services Authority.

ICRI 2021 - International Conference on Recent Innovations

78

Pribadino, Law, One, & the West. (2016, Sunday March).

Coursehero.com. Retrieved from Coursehero:

http://www.coursehero.com

Richard M, K., Stephen I, N., Josphat K, K., & David N, K.

(2016). The Influence of Demographic Characteristics

on Investment on Financially Included Youth in Nyeri

and Kirinyaga Counties. International Journal of

Academic Research in Accounting, Finance and

Management Sciences ,, Human Resource Management

Academic Research Society, International Journal of

Academic Research in Accounting, Finance and

Management Sciences, vol. 6 (4), pages 196-204.

Sanistasya, P. A., Raharjo, K., & Iqbal, M. (2019). The

Effect of Financial Literacy and Financial Inclusion on

Small Enterprises Performance in East Kalimantan.

Indonesia: Faculty of Administrative Sciences,

Brawijaya University.

Sari, A. N., & Kautsar, A. (2020). Analysis of the Influence

of Financial Literacy, Financial Technology, and

Demography on Financial Inclusion in Communities in

the City of Surabaya. Surabaya: State University of

Surabaya.

Sari, P. B., & Dwilita, H. (2018). Financial Technology

(Fintech) Prospects In North Sumatera Viewing From

The Side Of Financial Literation, Financial Inclusion

And Poverty. Medan: Accounting, Faculty of

Economics & Business, Pancabudi Development

University.

Spielhofer, T., Benton, T., Evans, K., Featherstone, G.,

Golden, S., Nelson, J., & Smith, P. (2009). Increasing

Participation: Understanding Young People who do not

Participate in Education or Training at 16 and 17.

United State of America: National Foundation for

Educational Research.

Steelyana, E. (2013). Women and Banking: An overview of

the Role of Financial Inclusion in Women MSME

entrepreneurs in Indonesia. Journal of The Winners

Vol. 14 No.2., 95-103.

Sugiyono. (2010). Research and Development Methods.

Research and Development. Bandung: Alfabeta

Publisher.

Yoshino, N., & Morgan, P. (2017). Financial Inclusion,

Regulation, and Education. China: Asian Development

Bank Institute.

Zia, I. Z., & Prasetyo, P. (2018). Analysis of Financial

Inclusion Toward Poverty and Income Inequality.

Semarang: Development Economics Department,

Faculty of Economics, Semarang State University.

The Effect of Financial and Financial Technology Literation on Financial Inclusion

79