The Role of Psychological Factors in the Intention to Use Mobile

Payment

Yuniarti and Hajan Hidayat

Managerial Accounting Study Program, Politeknik Negeri Batam, Indonesia

Keywords: Performance Expectancy, Facilitating Conditions, Hedonic Motivation, Perceived Security, Behavioral

Intention, Mobile Payment

Abstract: The rapid growth of mobile commerce businesses and the increasing number of transactions using mobile

devices are strengthening mobile payments as an instrument of payment. In addition, the Covid-19 pandemic

situation makes digital transactions also continue to increase. Regardless of the benefits provided by mobile

payments, the adoption of mobile payments is still considered in the early stages and quite new for consumers

in Indonesia. Telecommunication infrastructure facilities that are not evenly distributed and aspects of data

security that become obstacles in the development of mobile payment services. Departing from these

problems, the use of mobile payments still needs to be increased especially during this pandemic. The purpose

of this study is to find out the factors that influence the intention to use mobile payment from the psychological

side by using independent variables, namely performance expectancy, facilitating conditions, hedonic

motivation, and perceived security, and a dependent variable that is behavioral intention. The method of data

analysis is descriptive statistics and multiple regression. The results of this study are there is a positive

influence between performance expectancy variables and hedonic motivation variables towards behavioral

intention variables while facilitating conditions and perceived security variables do not affect behavioral

intention variables.

1 INTRODUCTION

The rapid growth of mobile commerce in Indonesia is

in line with the increasing number of internet users

who reached 185 million people in 2019 (Statista

Research Department, 2020). This situation is also

strongly supported by the development of smartphone

ownership that reaches 63 percent of the total

population of Indonesia in 2019 (Statista Research

Department, 2020). In addition, the rapid growth of

mobile commerce in Indonesia is also indicated to

increase due to the increasing need for digital

transactions amid the Covid-19 pandemic (Ronal,

2020). Bank Indonesia stated that digital transactions

have increased during the Covid-19 pandemic to

17.31 percent (tribunnews, 2020).

The increasing number of transactions using

mobile devices further strengthen the role of mobile

payment as one of the most important payment tools

in the mobile commerce business. The use of mobile

payment to make payments to mobile commerce-

based businesses can provide ease and speed in

transacting and is also able to be a secure payment

solution during physical distancing and self-

quarantine Jung, Kwon, & Kim (2020), Moorthy et

al. (2019) dan Sivathanu (2018). In addition, the

provision of cash-back, gifts, and cash discounts to

mobile payment users also further adds aspects of

benefits and advantages in using mobile payment

(Singh, Sinha, & Cabanillas, 2020).

However, aside from the benefits of using mobile

payment services. This service is considered still in

its early stages and still fairly new for consumers in

Indonesia (Agusta, 2018). This is when compared to

other countries such as China, Finland, and Sweden

(Robin, 2020). Moreover, the construction of

infrastructure facilities, especially

telecommunication infrastructure that has not been

evenly distributed, is an obstacle in utilizing this

digitalization potential (Hafid, 2020).

In addition, the use of mobile payments involving

highly sensitive personal and financial data results in

aspects of security risks such as theft, fraudulent

transactions, hacker attacks, privacy breaches, and

data breaches become the main considerations for a

person to conduct non-cash transactions Merhi, Hone,

264

Yuniarti, . and Hidayat, H.

The Role of Psychological Factors in the Intention to Use Mobile Payment.

DOI: 10.5220/0010862600003255

In Proceedings of the 3rd International Conference on Applied Economics and Social Science (ICAESS 2021), pages 264-273

ISBN: 978-989-758-605-7

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

& Tarhini (2019) dan Marria (2018). Departing from

the problem, the use of mobile payment still needs to

be improved. Moreover, during the Covid-19

pandemic, the use of mobile payments that facilitate

non-cash payments can support government policies

in the prevention of the Covid-19 pandemic during

the treatment of physical distancing and self-

quarantine (Hidayat, 2020). So the use of mobile

payment at this time becomes more important than

ever. This study will try to re-examine the factors that

influence the intention to use mobile payments during

the Covid-19 pandemic based on the psychological

factors felt by the users by using the identification of

the UTAUT2 model.

2 THEORITICIAL STUDY

2.1 Unified Theory of Acceptance and

Used of Technology 2 (UTAUT 2)

This theory was developed by Venkatesh, Morris,

Davis, & Davis (2003) this model then modified by

Venkatesh, Thong, & Xu (2012) by including three

additional elements, namely, price value, hedonic

motivation, and habits as well as three demographic

variables, namely age, gender, and experience which

were used as moderators of the effects of forming

UTAUT2. This study is an adaptation of the research

of Moorthy et al. (2019) where the study did not use

price value, habit variables, and three demographic

variables, namely age, gender, and experience. Two

other variables that are not included in this study are

the effort expectancy and social influence variables

because they do not affect behavioral intentions to use

mobile payment services.

2.2 Theory of Perceived Risk

The concept of perceived risk was first developed by

Bauer (1960) who defined perceived risk as the

uncertainty felt in a buying situation. This concept is

based on the idea that every buying activity involves

risk. The theory of perceived risk itself has been used

before to explain consumer behavior in decision-

making (Wu, Chiu, & Chen, 2020). Risk plays an

important role in consumer behavior and makes an

important contribution to behavioral intention and

decision making in purchasing, where the greater the

sense of uncertainty felt, the greater the barrier for

users to use a technology (Arora & Rahul, 2018).

Perceived risk has several components or types,

namely financial performance, social, physical, time-

loss, and security (Sanayei & Bahmani, 2012). This

study will focus on Perceived security which is

defined as a feeling of uncertainty or concern

regarding the security of personal and financial data

information when using a product or service.

Information security of personal and financial data is

a key element of the online purchasing process

(Justine, Hill, Gaines, & Wilson, 2009). In addition,

perceived security is also one of the main barriers to

adopting mobile payments (Chang, 2014).

2.3 Literature Review

Jung, Kwon, & Kim (2020) researched the

motivations and barriers in accepting mobile payment

services (MPSs) in America using the UTAUT

theory. This study results that the intention to use

MPSs is determined by social influence, knowledge,

trust, compatibility, and performance expectancy.

Another study by Singh, Sinha, & Cabanillas (2020)

proposed combining the UTAUT2 model with the

TAM (Technology Acceptance Model) model to

examine the factors that influence the intention to use

a mobile wallet and the intention to recommend a

mobile wallet in India. This study found that the

variables of usefulness, perceived risk, ease of use,

and attitude influenced the intention to use a mobile

wallet and the intention to recommend a mobile

wallet.

The research of Moorthy et al. (2019) which

examined 225 samples of workers in Malaysia using

the UTAUT2 variable stated that performance

expectancy, facilitating conditions, hedonic

motivation, and perceived security have a significant

influence on behavioral intention to use mobile

payments. The research of Merhi, Hone, & Tarhini

(2019) also uses UTAUT2 theory to examine the

factors that inhibit and can influence the adoption of

mobile banking services. This study states that

perceived security (PS), performance expectancy

(PE), Hedonic motivations (HM) have a significant

effect on behavioral intentions in the adoption of

mobile banking services. However, social influence

is not significant.

Another study by Nelloh, Santoso, & Slamet

(2019) developed a hypothesis related to continuance

intention or the intention of sustainability in the use

of mobile payment services that depend on the

perspective of trust and cognitive aspects. This study

results that cognitive aspects are not significant on

continuance intention or the intention of

sustainability in mobile payment services. On the

other hand, trust and security aspects show a positive

influence on continuance intention in mobile payment

services.

The Role of Psychological Factors in the Intention to Use Mobile Payment

265

2.4 Hypothesis Development

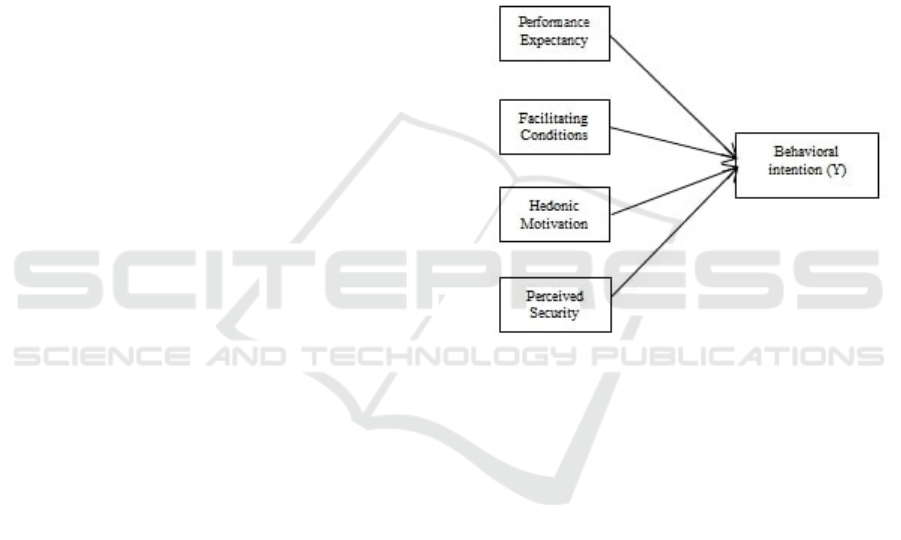

2.4.1 The Effect of Performance Expectancy

on Behavioral Intention

The perceived aspect of both the benefits and the

impact of use is expressed as an aspect of

performance expectancy. Every individual tends to

have the intention to use a technology if the benefits

and impacts of using it are by what is expected. Then

the researcher will test the following hypotheses:

H1: Performance expectancy has a positive effect

on behavioral intention to use mobile payment

2.4.2 The Effect of Facilitating Conditions

on Behavioral Intention

Technical and some operational infrastructures are

important in the development of mobile payment

services. In this case, it can be in the form of access

speed, availability of network infrastructure, and

security guarantees in digital transactions.

Facilitating conditions also have a positive

relationship to behavioral intention to use technology

according to Moorthy et al. (2019) and Shivathanu

(2018). Then the researcher will test the following

hypotheses:

H2: Facilitating conditions have a positive effect

on behavioral intention to use mobile payments

2.4.3 The Effect of Hedonic Motivation on

Behavioral Intention

Another important factor in researching consumer

behavior that has a significant and positive influence

on behavioral intention is Hedonic motivation

Moorthy et al. (2019), Merhi, Hone, & Tarhini

(2019), Sivathanu (2018). According to Moorthy et

al. (2019), if the use of technology can bring pleasure

and enjoyment to the user, the individual will tend to

accept the technology. Feelings of pleasure and

enjoyment expressed as aspects of hedonic

motivation can increase a person's interest in using a

particular service. Therefore, the researcher proposes

the following hypothesis:

H3: Hedonic motivation has a positive effect on

behavioral intention to use mobile payments

2.4.4 The Effect of Perceived Security on

Behavioral Intention

The situation where users feel safe in carrying out

transactions using mobile payments is very

important. The more stronger the security to protect

the financial and personal data the more willing

individual to adopt mobile payment. According to

some previous studies, there is a positive relationship

between perceived security and behavioral intention.

Merhi, Hone, & Tarhini (2019), Moorthy et al.

(2019), Nelloh, Santoso, & Slamet (2019) Oliveira,

Thomas, Baptista, & Campos (2016). To confirm the

impact of perceived security, the researcher

formulated the following hypothesis:

H4: Perceived security has a positive effect on

behavioral intention to use mobile payment

The research model can be seen in Figure 1:

Figure 1: Research Model

3 RESEARCH METHOD

3.1 Population and Sample

Quantitative approach method was used by this study.

The population studied were students from two major

universities in the city of Batam (Batam Polytechnic

and Riau Islands University) among the age group

(17-25 years). Purposive sampling method was used

with a technique of non-probability sampling.

3.2 Variable Operations and

Measurement

3.2.1 Performance Expectancy

The level of trust or confidence of an individual in the

use of a technology that will help him achieve an

increase in work quality (Venkatesh, Thong, & Xu,

2012) this define as performance expectancy. There

are four indicators of measuring the perception of

ICAESS 2021 - The International Conference on Applied Economics and Social Science

266

performance expectancy including the level of

perceived benefits in completing the payment

process, the ability to complete the payment process

more quickly, the ability to facilitate, assist, and

support work and increase productivity.

3.2.2 Facilitating Conditions

Consumers' perceptions of the support and

infrastructure and technical resources available to

facilitate the use of a system is refer to the definition

of facilitating conditions (Venkatesh, Morris, Davis,

& Davis, 2003). There are four indicators of

measuring the perception of facilitating conditions in

this study including resources, the knowledge

required, compatibility with other technologies used,

and assistance from others when experiencing

difficulties (assistance).

3.2.3 Hedonic Motivation

According to Venkatesh, Thong, & Xu (2012), a

feeling of pleasure or joy that is felt when using

technology is defined as hedonic motivation. There

are three indicators of hedonic motivation

measurement, namely using mobile payment, namely

mobile payment is very fun, mobile payment is very

convenient, and mobile payment is very entertaining.

3.2.4 Perceived Security

According to Arpaci, Cetin, & Turetken (2015)

perceived security is an individual's belief that the

technology used ensures the security of sensitive

information used such as personal data and financial

transactions. In this case, when using mobile

payment, consumers will be asked to fill in their

phone number, pin code, location of consumption,

etc. Therefore, the financial data must be kept

confidential, not stored or used by other unauthorized

individuals or unauthorized users. The measurement

indicators of perceived security in this study include

guarantees of data security and confidentiality.

3.2.5 Behavioral Intention

The level of user intention to use new products or

services (in this case mobile payment services) in the

future is explain as behavioral intention (Venkatesh,

Morris, Davis, & Davis, 2003). There are three

indicators of measuring behavioral intention

perceptions, namely by assessing the consumer's

desire to keep utilize mobile payment henceforward,

the desire to utilize mobile payment in everyday life,

and consumer planning to use mobile payment

sustainably.

3.3 Data Processing and Analysis

Techniques

Multiple linear regression with SPPS was used in this

study with equation as follows :

BI = α +β1PE +β2FC+β3HM +β4PS+e

Formula information:

BI: Behavioral intention

PE: Performance expectancy

FC: Facilitating conditions

HM: Hedonic motivation

PS: Perceived security

e: Error tolerance

4 RESULT

After collecting data using a questionnaire that was

distributed using a google form, a total of 102

samples students from Batam State Polytechnic and

Riau Islands University were collected through the

purposive sampling method.

4.1 Descriptive Statistical Analysis

The data of 102 respondents will be analyzed based

on the average, median, and mode of data. The results

of the descriptive statistical analysis are described in

table below.

Description:

SS: Strongly Agree

S: Agree

N: Neutral

TS: Disagree

STS: Strongly Disagree

The Role of Psychological Factors in the Intention to Use Mobile Payment

267

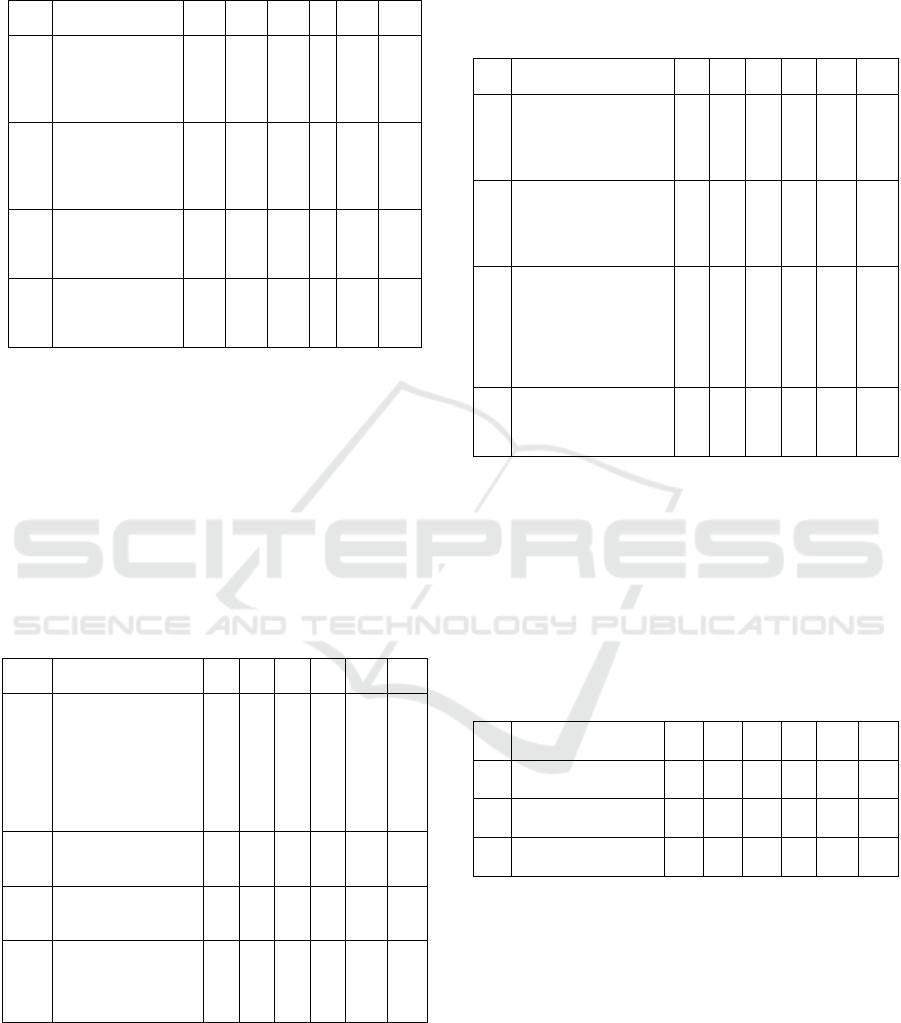

Table 1: Descriptive statistical table

Performance expectancy

No Questions SS S N

T

S

STS

Tot

al

1

Mobile payment

does not provide

benefits in

completing my

payment process

34 51 10 5 2

10

2

2

Using mobile

payment will make

my payment

process faster

47 46 8 0 1

10

2

3

Using mobile

payment makes it

easier, helps and

supports my work

28 48 22 3 1

10

2

4

Using mobile

payment will

increase my

productivity

19 43 39 1 0

10

2

Source: Primary data processed by the author

In this performance expectancy variable, there are 4

question components. Where the majority of

respondents answered agree on the four questions

posed on the first variable. So it can be concluded that

respondents generally have a level of trust or

confidence in the use of a technology that will help

them achieve a fairly good increase in the quality of

their work.

Facilitating Conditions

No Questions SS S N TS STS

Tot

al

1

I don't have the

resources or facilities

(such as smartphone,

internet connection,

merchant with mobile

payment option)

needed to use mobile

payment

35 51 11 5 0 102

2

I have the necessary

knowledge to use

mobile payments

21 61 18 2 0 102

3

Mobile payment is

compatible with other

systems that I use

15 54 31 2 0 102

4

I can get help from

other people when I

have trouble using

mobile payment

18 57 25 1 1 102

Source: Primary data processed by the author

In the second variable, namely Facilitating

Conditions, there are 4 question components. In

general, respondents chose the answer to agree on the

four questions asked. So in general, respondents have

a fairly high perception of the support and

infrastructure, and technical resources available to

facilitate the use of a system (in this case mobile payment).

Perceived security

No Questions SS S N TS STS

Tot

al

1

I feel unsafe sending

sensitive information

when making

transactions with mobile

payments

4 30 37 28 3 102

2

I feel that mobile

payment is safe to send

my personal and financial

information

7 38 46 10 1 102

3

I feel that the sensitive

information that I

provide when using

mobile payment is

protected and its

confidentiality

guaranteed

7 33 45 13 4 102

4

Overall mobile payment

is a safe place to send

sensitive information and

make transactions

5 39 49 9 0 102

Source: Primary data processed by the author

The third variable is perceived security which has 4

question components. The majority of respondents

chose a neutral answer so that in general respondents

felt neutral regarding the security of sensitive

information used such as personal data and financial

transactions during the use of mobile payments.

Hedonic motivation

No Questions SS S N TS STS

Tot

al

1

Using mobile payment

is very boring

16 69 14 3 0 102

2

Using mobile payment

is very convenient

30 49 21 2 0 102

3

Using mobile payment

is very entertaining

10 31 57 3 1 102

Source: Primary data processed by the author

In the fourth variable, namely hedonic motivation,

there are 3 question components. Where in the first

and second questions the majority of respondents

chose the answer to agree, while in the third question

the majority answered is neutral. In general,

respondents agree that they feel happy or happy while

using mobile payments.

ICAESS 2021 - The International Conference on Applied Economics and Social Science

268

Behavioral intention

No Questions SS S N TS STS

Tot

al

1

I don't intend to use

mobile payment in the

future

27 61 13 1 0 102

2

I will try to use mobile

payment in my daily life

18 52 29 2 1 102

3

I plan to continue using

mobile payment as much

as possible

12 37 45 7 1 102

Source: Primary data processed by the author

The dependent variable is the behavioral intention

which has 3 question components. Where in the first

and second questions the majority of respondents

chose the answer to agree, while in the third question

the majority answered are neutral. So in general,

respondents have a fairly good level of intention to

use mobile payments again in the future.

4.2 Validity Test

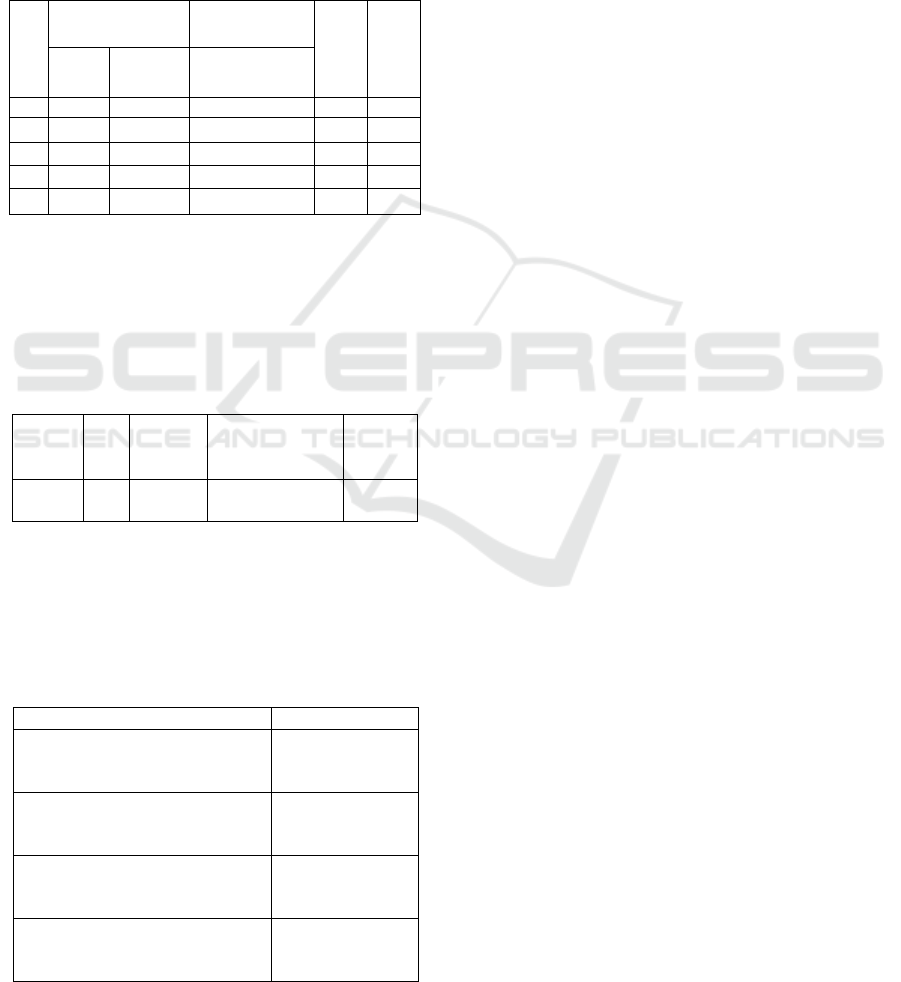

Table 2: Validity test

Variabel Item r

hitun

g

r

tabel

Conclusion

Performance

Expectancy

(X1)

item 1 .724 .306 Valid

item 2 .821 Valid

item 3 .758 Valid

item 4 .827 Valid

Facilitating

Conditions

(X2)

item 1 .766 .306 Valid

item 2 .820 Valid

item 3 .666 Valid

item 4 .542 Valid

Hedonic

Motivation

(X3)

item 1 .823 .306 Valid

item 2 .907 Valid

item 3 .813 Valid

Perceived

Security (X4)

item 1 .756 .306 Valid

item 2 .595 Valid

item 3 .770 Valid

item 4 .697 Valid

Behavioaral

Intention (Y)

item 1 .686 .306 Valid

item 2 .915 Valid

item 3 .899 Valid

Based on table 2 above, it is found that each question

on the questionnaire is declared valid.

4.3 Realibility Test

Table 3: Realibility Test

Variabel Realibility

Cronbach

Alpha

Cutt of

Cronbach

Al

p

ha

Conclusion

Performance

Ex

p

ectanc

y

0,782 0,60 Reliable

Facilitating

Conditions

0,657 0,60 Reliable

Hedonic

Motivations

0,804 0,60 Reliable

Perceived

Securit

y

0,658 0,60 Reliable

Behavioral

Intention

0,784 0,60 Reliable

From these results, it can be concluded that all instruments

are reliable whose meaning is reliable and can be used to

measure the same object at different times.

4.4 Classic Assumtion Test

4.4.1 Normality Test

Table 4: Normality Test Result

Information Significance Conclusion

Asymp.sig 0.788 Normal

Distribution

Significance value is 0.788 so it is greater than 0.05, so it

can be judge that the data is normally distributed.

4.4.2 Multicollinearity Test

Table 5: Multicollinearity Test Result

Tolerance VIF

Performance Expectancy 0,531 1,884

Facilitating Conditions 0,66 1,515

Hedonic Motivation 0,57 1,753

Perceived Security 0,863 1,159

For each independent variable is at tolerance value > 0.10

and vif < 10, therefore it can be judge that all independent

variables in this study are free from multicollinearity.

4.4.3 Heteroscedasticity Test

Table 6: Heteroscedasticity Test Result

T Sig

Performance Expectancy 1,312 0,193

Facilitating Conditions -0,708 0,48

Hedonic Motivation -1,536 0,128

Perceived Security -1,388 0,168

The Role of Psychological Factors in the Intention to Use Mobile Payment

269

In this test, the significance value is above the limit

value of 0.05, therefore it is judge that the regression

model in this study is feasible to use and is free from

heteroscedasticity.

4.5 Hypothesis Test

4.5.1 Multiple Linear Regression

Table 7: Multiple Linear Regression Test Result

Based on the table above, the regression equation for this

study is:

BI = 0,511 + 0,359PE +0,036FC + 0,336HM + 0,054PS + e

4.5.2 Coefficient of Determination (R2)

Table 8: Coefficient of Determination Test Result

Model R Square Adjusted R Square Std.

Error of

the

Estimate

1 .756 .571 .553 1.222

4.6 Data Analysis

The following is a summary table of test results from

this study:

Table 9: Summary of test result

Hypothesis Conclusion

H1: Performance expectancy has

a positive effect on behavioral

intention to use mobile payment

Supported

H2: Facilitating conditions have

a positive effect on behavioral

intention to use mobile payment

Not Supported

H3: Hedonic motivation has a

positive effect on behavioral

intention to use mobile

p

a

y

ment

Supported

H4: Perceived security has a

positive effect on behavioral

intention to use mobile

p

a

y

ment

Not Supported

4.6.1 The Effect of Performance Expectancy

on Behavioral Intention

The results of the analysis based on table 9 show that

H1 is supported. This designate that the greater the

performance expectancy or benefits obtained by

mobile payment users, the greater the behavioral

intention or desire of users to use mobile payments.

In this case, students of Batam State Polytechnic and

Riau Islands University are in the age range (17-25

years). In addition, during the Covid-19 pandemic

where there are concerns about the spread of the

Covid-19 virus through physical money, the mobile

payment system is an option in offering convenience

and secure solutions for payments during physical

distancing and self-quarantine.

In compliance with earlier research, namely

Sivathanu (2018) and Oliveira, Thomas, Baptista, &

Campos (2016) that have the same result, as another

research by Sivathanu (2018) states that consumers

use mobile payment services because these services

can provide benefits to simplify and improve the

quality of their daily transactions.

4.6.2 The Effect of Facilitating Conditions

on Behavioral Intention

The outcome of the analysis based on table 9 show

that hypothesis H2 is not supported, namely

facilitating conditions do not affect behavioral

intention. This finding is in compliance with previous

research, namely Mahendra, Winarno, & Santosa

(2017). This research respondents were aged 17-25

years. Where mobile payment consumers at this age

believe that they already have sufficient resources and

knowledge to use mobile payment services. This is

because the younger population has more knowledge

to use a technology which in this case is a mobile

payment service. In addition, now supporting

facilities (facilitating conditions) for mobile

payments are easy to find and obtain by many people,

such as smartphones and internet networks.

4.6.3 The Effect of Hedonic motivation on

Behavioral intention

The outcomes of the analysis in table 4.12 show that

the H3 hypothesis is supported. In this study, mobile

payment is a new way of conducting financial

payment transactions where this service is considered

to be still in its early stages and is still quite new for

consumers in Indonesia. This is what causes the use

of mobile payments to be able to provide a sense of

pleasure, enjoyment, and comfort when using mobile

payments. In addition, mobile payment has many

Unstandardized

Coefficients

Standardized

Coefficients

T Sig.

B Std. Error Beta

0,511 1,129 0,452 0,652

X1 0,359 0,071 0,463 5,055 0,000

X2 0,036 0,078 0,038 0,459 0,647

X3 0,336 0,093 0,317 3,596 0,001

X4 0,054 0,053 1,033 1,033 0,304

ICAESS 2021 - The International Conference on Applied Economics and Social Science

270

diverse features, making it fun when used. Therefore,

users will tend to accept and continue to use mobile

payments.

Study by Morosan & Defranco (2016) stated that

in practice the use of mobile payments is not only

because of the usability aspect but also entertaining to

use. For example, by providing cash-back prizes, as

well as cash discounts to mobile payment users as

loyalty points to users.

4.6.4 The Effect of Perceived Security on

Behavioral Intention

The test outcomes that have been summarized in table

4.12 show that the H4 hypothesis is not supported,

namely perceived security does not affect behavioral

intention. This shows that the Batam State

Polytechnic students and the Riau Islands University

who were respondents in this study did not think too

much about security in using mobile payments.

The students as consumers are not afraid and do

not feel worried about the risks that exist when using

mobile payments. Risks can be in the form of theft,

fraudulent transactions, hacker attacks, privacy

violations, and data breaches. When using mobile

payment itself, users will be asked to provide their

phone number, pin code, location of consumption,

etc. which most students do not object to.

Respondents in this study did not feel worried if their

account could be used by other people, because the

password was only owned by the user. However, the

results of this study could be different if the research

respondents were extended to workers who have an

older age or business people. Where the greater the

possibility of the nominal payment transactions made

when using mobile payments, the higher the worry

about security and abuse.

4.7 Conclusion, Limitations,

Implications, and Sugesstions

4.7.1 Conclusion

Performance expectancy variable and the hedonic

motivation variable have positive influence on the

behavioral intention variable, while the facilitating

conditions variable and the perceived security

variable unaffected to the behavioral intention

variable.

4.7.2

Limitations

In conducting this research, the writer has several

limitations, namely as follows: (1) The data processed

by the research is obtained from a questionnaire

instrument which is purely derived from the

perception of respondents' answers, so that the results

of this study are subjective; (2) There are limited

locations and research subjects which are only

students of Batam State Polytechnic and Riau Islands

University, this will give different results if the

research subjects are carried out with a wider scope;

(3) This study only considers the context of

consumers, where the level of intention to use mobile

payments can also be influenced by the availability of

payment method options provided by merchants,

therefore further research can also look at it from the

merchant's point of view; (4) Only explains the

factors that influence the intention to use mobile

payments of 0.571 or 57.1%, so it is necessary to add

other factors beyond what this research proposes.

4.7.3

Implications

The implications of this study are aimed at knowing

the main factors that influence consumer intentions to

use mobile payment services, especially during the

Covid-19 pandemic. This study proposes four

hypotheses based on the results of the analysis, two

hypotheses are proven to affect the intention to use

mobile payments, and the other two hypotheses are

rejected. It was found that performance expectancy

and hedonic motivation affect the intention to use

mobile payments and facilitating conditions and

perceived security has no effect. This study shows

that the research model can explain the intention to

use mobile payment by 57.1% and the remaining

42.9% is influenced by other factors beyond what this

research proposes.

The results of this study indicate that performance

expectancy has the strongest influence on the

intention to use mobile payment based on its level of

significance. This is by previous studies, namely

Jung, Kwon, & Kim (2020), Moorthy et al. (2019),

Merhi, Hone, & Tarhini (2019), Sivathanu (2018),

Oliveira, Thomas, Baptista, & Campos (2016),

Morosan & Defranco (2016). Performance

expectancy has a strong influence on mobile payment

because each individual tends to have the intention to

use mobile payment services if the benefits and

impacts of the use obtained are by what is expected.

So that mobile payments must be designed according

to consumer needs, mobile payment service providers

in this case can further improve service performance,

so that they can further increase the usefulness of

transactions.

Likewise with hedonic motivation which has an

effect after performance expectancy. This is in line

with previous research by Moorthy et al. (2019),

The Role of Psychological Factors in the Intention to Use Mobile Payment

271

Merhi, Hone, & Tarhini (2019) and Sivathanu (2018).

When users feel happy and comfortable when using

mobile payment services, the intention to continue

using mobile payments will increase. Therefore,

hedonic motivation is an important factor in the use

of mobile payments. Thus, mobile payment service

providers can improve features and services on

mobile payment applications to provide an

entertaining and enjoyable transaction experience.

4.7.4 Sugesstions

Based on the limitations that have been described, the

suggestions for further research are: (1) Adding the

more to the quota of samples and expanding the

research place so that the research results can be more

accurate; (2) Adding other predictor factors that were

not previously present in this study, but still have a

relationship with the variables studied.

REFERENCES

Chang, T.-K. (2014). A Secure Operational Model for

Mobile payments. The Scientific World Journal.

Hidayat, K. (2020, April 30). Ini sederet kebijakan BI

mendorong transaksi digital di tengah pandemi corona.

Dipetik December 29, 2020, dari

keuangan.kontan.co.id:

https://keuangan.kontan.co.id/news/ini-sederet-

kebijakan-bi-mendorong-transaksi-digital-di-tengah-

pandemi-corona

Hoffman, D. L., Novak , T. P., & Peralta, M. (1999).

Building Consumer Trust in Online Environments:The

Case for Information Privacy. Communications of the

ACM, Volume 42, Number 4, 80-85.

Jung, J.-H. (2020). Mobile payment service usage: U.S.

consumers’ motivations and intentions. Computers in

Human Behavior Reports, 1-7.

Lu, Y., Yang, S., & Chau, P. Y. (2011). Dynamics between

the Trust Transfer Process and Intention to Use Mobile

payment Services: A Cross-Environment Perspective.

Information & Management 48(8), 393-403.

Luvita, D. (2019, Februari 25). Fintech berkembang pesat

di kota Batam ? Dipetik Maret 2020, dari

www.duniafintech.com:

https://www.duniafintech.com/fintech-berkembang-

pesat-di-batam/

Mahendra, Y. A., Winarno, W. W., & Santosa, P. I. (2017).

Pengaruh Perceived security terhadap Pengadopsian In-

App Purchase pada Aplikasi Mobile. JNTETI, Vol. 6,

No. 2, 184-193.

Marria, V. (2018, December 21). What A Cashless Society

Could Mean For The Future. Dipetik October 5, 2020,

dari

https://www.forbes.com/sites/vishalmarria/2018/12/21

/what-a-cashless-society-could-mean-for-the-

future/#62ab57493263

Sivathanu, B. (2018). Adoption of digital payment systems

in the era of demonetization in India. Journal of Science

and Technology Policy Management.

Statista Research Department. (2020, August 13).

Indonesia: number of internet users 2015-2025. Dipetik

October 20, 2020, dari www.statista.com:

https://www.statista.com/statistics/254456/number-of-

internet-users-in-indonesia/

Agusta, J. (2018, March 5). Mobile payments In Indonesia:

Race to Big Data Domination. Diambil kembali dari

MDI Ventures : White Paper: https://bit.ly/2QS5AWF

Arora, N., & Rahul, M. (2018). The Role of Perceived risk

in Influencing Online Shopping Attitude Among

Women in India. Int. J. Public Sector Performance

Management, Vol. 4, No. 1, 98-113.

Bauer, R. (1960). Consumer behavior as risk taking. Dalam

R. Hancock, Dynamic marketing for a changing world

(hal. 389-398). Chicago: American Marketing

Association.

Budiaji, W. (2013). Skala Pengukuran dan Jumlah Respon

Skala Likert. Jurnal Ilmu Pertanian dan Perikanan, 127-

133.

Ghozali, I. (2013). Aplikasi Analisis Multivariate dengan

Program SPSS (Edisi Ketujuh ed.). Semarang: Badan

Penerbit Universitas Diponegoro.

Hafid, M. (2020, June 19). Pandemi dan Pemerataan

Infrastruktur Telekomunikasi. Dipetik October 20,

2020, dari detikNews: https://news.detik.com/kolom/d-

5059820/pandemi-dan-pemerataan-infrastruktur-

telekomunikasi

Jung, J.-H., Kwon, E., & Kim, D. H. (2020). Mobile

payment service usage: U.S. consumers’ motivations

and intentions. Computers in Human Behavior Reports,

1-16.

Justine, R., Hill, R. P., Gaines, J., & Wilson, M. R. (2009).

Advertising and Consumer Privacy. Journal of

Advertising, 51-61.

Kementerian Riset, Teknologi Dan Pendidikan Tinggi.

(2020). PANGKALAN DATA PENDIDIKAN

TINGGI KEMENTERIAN RISET, TEKNOLOGI

DAN PENDIDIKAN TINGGI. Dipetik December 30,

2020, dari forlap.kemdikbud.go.id:

https://forlap.kemdikbud.go.id/

Merhi, M., Hone, K., & Tarhini, A. (2019). A cross-cultural

study of the intention to use mobile banking between

Lebanese and British consumers: Extending UTAUT2

with security, privacy Lebanese and British consumers:

Extending UTAUT2 with security, privacy and trust.

Technology in Society.

Moorthy, K., T'ing, L. C., Yee, K. C., Huey, A. W., In, L.

J., Feng, P. C., et al. (2019). What drives the adoption

of mobile payment? A Malaysian perspective. Int J Fin

Econ, 1–16.

Morosan, C., & Defranco, A. L. (2016). It's about time:

Revisiting UTAUT2 to examine consumers’ intentions

to use NFC mobile payments in hotels. International

Journal of Hospitality Management, 17-29.

Nelloh, L. A., Santoso, A. S., & Slamet, M. W. (2019). Will

Users Keep Using Mobile payment? It Depends on

ICAESS 2021 - The International Conference on Applied Economics and Social Science

272

Trust and Cognitive Perspectives. Procedia Computer

Science 161, 1156–1164.

Oliveira, T., Thomas, M., Baptista, G., & Campos, F.

(2016). Mobile payment: Understanding the

determinants of customer adoption and intention to

recommend the technology. Computers in Human

Behavior, 404-414.

Robin. (2020, January 16). Top 6 cashless society

countries: Finland, Sweden and China lead way.

Dipetik August 19, 2020, dari netimperative:

http://www.netimperative.com/2020/01/16/top-6-

cashless-society-countries-finland-sweden-and-china-

lead-way/

Ronal. (2020, June 19). Bank Indonesia Sebut Layanan

Digital Meningkat Drastis di Tengah Pandemi. Dipetik

October 5, 2020, dari

https://pasardana.id/news/2020/6/19/bank-indonesia-

sebut-layanan-digital-meningkat-drastis-di-tengah-

pandemi/

Sanayei, A., & Bahmani , E. (2012). Integrating TAM and

TPB with Perceived risk to Measure Customers’

Acceptance of Internet Banking. International Journal

of Information Science and Management, 25-37.

Santoso, S. (2018). Mahir Statistik Parametrik. Dalam S.

Santoso, Mahir Statistik Parametrik (hal. 38). Jakarta:

PT Elex Media Komputindo.

Sekaran, U. (2009). Research methods for business =

metodologi penelitian untuk bisnis . Jakarta: Salemba

Empat.

Singh, N., Sinha, N., & Cabanillas, F. J. (2020).

Determining factors in the adoption and

recommendation of mobile wallet services in India:

Analysis of the effect of innovativeness, stress to use

and social influence. International Journal of

Information Management, 191-205.

Statista. (2019, September 5). Share of internet users

Indonesia 2019 by age group. Dipetik Desember 2020,

dari www.statista.com:

https://www.statista.com/statistics/997264/share-of-

internet-users-by-age-group-indonesia/

Statista Research Department. (2019, September 5). Share

of internet users in Indonesia in 2019, by age group.

Dipetik October 22, 2020, dari www.statista.com:

https://www.statista.com/statistics/997264/share-of-

internet-users-by-age-group-indonesia/

Statista Research Department. (2020, July 30). Smartphone

penetration as share of population in Indonesia 2015-

2025. Dipetik October 20, 2020, dari

www.statista.com:

https://www.statista.com/statistics/321485/smartphone

-user-penetration-in-indonesia/

tribunnews. (2020, July 16). BI: Transaksi Uang Elektronik

Melambung 17,31 Persen di Tengah Pandemi. Dipetik

December 29, 2020, dari www.tribunnews.com:

https://www.tribunnews.com/bisnis/2020/07/16/bi-

transaksi-uang-elektronik-melambung-1731-persen-di-

tengah-pandemi

Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D.

(2003). User acceptance of information technology:

Toward a unified view. MIS Quarterly, Vol. 27, No. 3,

425-478.

Venkatesh, V., Thong, J. Y., & Xu, X. (2012). Consumer

Acceptance and Use of Information Technology:

Extending the Unified Theoryof Acceptance and Use of

Technology. MIS Quarterly, Vol. 36, No. 1, 157-178.

Wu, I.-L., Chiu, M.-L., & Chen, K.-W. (2020). Defining the

determinants of online impulse buying through a

shopping process of integrating perceived risk,

expectation-confirmation model, and flow theory

issues. International Journal of Information

Management.

Yeh, M. L., & Tsen, Y. L. (2017). The College Students'

Behavior Intention Of Using Mobile payments In

Taiwan: An Explanatory Research. International

Journal of Management and Applied Science, 89-93.

The Role of Psychological Factors in the Intention to Use Mobile Payment

273