The Interactive Effects of Superior Trust and Subordinate

Involvement in Decision Making on Budget Gaming and Budget Value

Rifal Hijira and SeTin SeTin

a

Faculty of Business, Maranatha Christian University, Jl. Surya Sumantri 65, Bandung, Indonesia

Keywords: Superior Trust, Subordinate Involvement in Decision Making, Budget Gaming, Budget Value.

Abstract: This study aims to investigate if the interaction between superior trust and subordinate involvement in

decision making has an impact on budget gaming and budget value. A survey questionnaire was conducted

and 145 Indonesian managers from manufacturing companies answered-questionnaire. Partial Least Square

was used to test the hypotheses. Results indicate that superior trust has a negative effect on budget gaming.

The finding suggests that superior trust is stronger in reducing the budget gaming when interacting with

subordinate involvement in decision making. In contrast, the relationship between superior trust that interacts

with subordinate involvement in decision making and budget value is insignificant. The results also indicate

that superior trust has a positive effect on budget value. We also find that the budget gaming significantly

mediates the relationship between superior trust and budget value. Specifically, the results find that budget

gaming significantly mediates the relationship between budget value and superior trust that interacts with

subordinate involvement in decision making. The study provides empirical evidence on how the interactive

between superior trust and subordinate involvement in decision making can be stronger in reducing budget

gaming behaviour and increasing budget value compared to if there is no involvement of subordinates in

decision making.

1 INTRODUCTION

Budget value is defined as the added value obtained

from the budgeting process after considering the time

spent by the management in the budgeting process

and the effectiveness of the budgeting system in

helping business units to achieve goals, including

reducing dysfunctional behavior (Libby and Lindsay,

2010). The budgeting process has the potential to add

value when the budgeting process focuses on

achieving company's goals (eg Neely et al., 2003;

Libby and Lindsay, 2010). Salterio, 2015 suggests to

focus on how, when, and where accounting and

management control practices can work well and be

beneficial to create value in the budgeting process.

Libby and Lindsay, 2019 state that superior trust

is beneficial in the budgeting process and makes an

important contribution to budget value. The trusting

relationship that is built early on between superiors

and subordinates could reduce dysfunctional

behavior and could contribute in creating budget

values. This is an important step for the development

a

https://orcid.org/0000-0001-7065-1093

of the budgeting literature (Libby and Lindsay, 2019).

Libby and Lindsay, 2019 support the perspective of

Jensen, 2001 who states that lack of trust is a problem

of traditional budgeting. This leads to the perspective,

that a control system is needed to create trust between

superiors and subordinates.

Previous studies have examined the relationship

between trust and budget gaming (budgetary slack).

For example, Gago-Rodríguez and Naranjo-Gil, 2016

found that superiors with high trust in subordinates

will produce low slack and vice versa, that distrust

tends to create slack. Gilabert-Carreras et al., 2012

and Maria and Nahartyo, 2012 also state that trust

reduces budgetary slack.

This study examines the relationship between

trust and dysfunctional budgetary behavior in a

broader framework, namely budget gaming. So far,

there are still a few studies that associate trust with

budget gaming. Libby and Lindsay, 2019 show that

trust has a negative effect on the budget gaming. This

means that the higher the trust, the lower the budget

gaming in the company. Superior trust is expected to

Hijira, R. and SeTin, S.

The Interactive Effects of Superior Trust and Subordinate Involvement in Decision Making on Budget Gaming and Budget Value.

DOI: 10.5220/0010749900003112

In Proceedings of the 1st International Conference on Emerging Issues in Humanity Studies and Social Sciences (ICE-HUMS 2021), pages 183-191

ISBN: 978-989-758-604-0

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

183

make superiors more open in welcoming

subordinates' participation in decision making

(Brower et al., 2009; Olson et al., 2007). The

existence of superior trust in subordinates leads to

higher quality interactions which make subordinates

more comfortable, confident, active in contributing

knowledge, dare to differ from others' views and

leading to higher quality decisions (Brower et al.,

2009; Olson et al., 2007).

Besides superior trust, the participation of

subordinates (managers) in making budget decisions

is also needed to produce better information related to

budgeting (Dunk, 1993). Hansen and Mowen, 2013

reveal that employees' participation in the budgeting

process will encourage creativity, increase

responsibility and provide challenges for lower and

middle level managers which lead to higher

performance achievement. The involvement of

middle and lower level managers in the budgeting

process will create decisions that are more realistic

and in line with company goals.

As the previous studies have confirmed the

relationship between trust and dysfunctional

behavior, namely that trust can reduce gaming, and

that the budgeting process also requires subordinate

involvement in decision making, this study suspects

that subordinate involvement in decision making

could strengthen (moderate) the effect of superior

trust on dysfunctional behavior (budget gaming). In

addition, to understand how superior trust benefits the

budgeting process and contributes to budget value

(Libby and Lindsay, 2019), this study also

investigates whether budget gaming mediates the

relationship between superior trust and budget value

and examines whether budget gaming mediates the

interaction between superior trust with subordinate

involvement in decision making with budget value.

Abroad, studies on budget gaming are generally

conducted in western countries with a sample of

manufacturing companies. Specifically for the study

of budget value, only the study by Libby and Lindsay,

2019 was found,. There are also very few studies on

budget gaming in Asia in the private sector, for

example Huang and Chen, 2010 in Taiwan; SeTin et

al., 2019; Rachmat and SeTin, 2020. Budget studies

in Indonesia have so far been dominated in the realm

of the public sector and government agencies, for

example Komarawati, 2010, Herwiyanti, et al., 2016.

There are still limited studies on budget gaming and

budget value, both in Europe and in Asia. Therefore,

this study prefers managers of private companies in

Indonesia in order to increase the understanding of

behavior in budgeting and their contribution towards

budget value, particularly in relation to superior trust

and subordinate involvement in decision making.

This study also follows the direction of Daumoser et

al., 2018, namely that budget gaming requires further

research by examining various explanatory variables

as this topic is associated to the complex interaction

between individual and organizational interests.

This study contributes to the budgeting literature

because it extends the previous understanding of the

relationship between trust and budget dysfunctional

behavior. This study provides evidence that the trust

relationship that interacts with subordinate

involvement in decision making will be stronger in

reducing dysfunctional behavior in budget gaming.

This study is a recent study that systematically and

empirically examines the role of budget gaming

mediation in the relationship between superior trust

and budget value moderated by subordinate

involvement in decision making. Considering that

there are still very few studies on budget value and

budget gaming both abroad and domestically, the

results of this study enrich the literature on

management control systems, especially in the topic

of budgeting. This study also contributes practically

in providing understanding to managers about how

budget value is related to superior trust, subordinate

involvement in decision making, and budget gaming.

This study also provides an alternative practical

solution to the budgeting problem that has yet to be

resolved, namely the budget gaming problem.

2 LITERATURE REVIEW AND

HYPOTHESIS DEVELOPMENT

2.1 Literature Review

Superior trust is defined as the trust of senior

managers towards the capability of lower managers

(Libby and Lindsay, 2019). Superior trust generates

greater respect and trust towards the capability of

subordinates to perform well (Olson et al., 2007).

When the superior's trust is high, subordinates tend

not to take risks that would violate their superior's

trust by engaging in dysfunctional behavior (Lewis

and Weigert, 2012). Trust will increase the exchange

of information between superiors and subordinates,

thereby reducing information asymmetry. Higher

trust from superiors to subordinates would gain the

trust in subordinates which further negates the need

for gaming (Bart, 1988). Higher trust from superiors

also causes superiors to have high-quality interactions

ICE-HUMS 2021 - International Conference on Emerging Issues in Humanity Studies and Social Sciences

184

with subordinates, making subordinates more

comfortable and confident in actively contributing to

their local knowledge and even challenging the

perspective of others (Brower et al. 2009; Olson et al.,

2007), so this leads to the higher of quality decisions

from subordinates.

Budgeting involves complex decisions due to the

uncertainty of a changing competitive environment

(Libby and Lindsay, 2019). Subordinate involvement

in decision making means that subordinates are fully

involved in the budgeting process. Budget decisions

that involve subordinates in the budgeting process on

the one hand could improve manager performance,

and on the other hand can have negative

consequences on manager behavior, such as

manipulating information and manipulating budget

performance measures / doing budget gaming

(Lukka, 1988).

Budget gaming is a dysfunctional behavior in the

budget due to pressure to meet or make it easier to

achieve budget-related performance goals (Libby and

Lindsay, 2019). Budget gaming refers to the behavior

of reporting deviant information such as reporting

costs and income that are too low or too high,

delaying or accelerating expenses, making

investments that sacrifice profits (Libby and Lindsay,

2010). Simmons, 2012 states that budget gaming is a

behavior of developing budget information which is

not based on actual expectations of availability and

needs, but rather on the amount designed /

manipulated to achieve budget performance.

Budget value is defined as the value that could be

added to the business unit management of the

budgeting system / process that is conducted after

considering the time spent by management in the

budgeting process and the effectiveness of the budget

system in helping the business unit to achieve goals,

including reducing dysfunctional behavior (Libby

and Lindsay). , 2010). Budget value is defined as the

ability of a budget to help in achieving organizational

goals (Libby and Lindsay, 2019).

2.2 Hypothesis Development

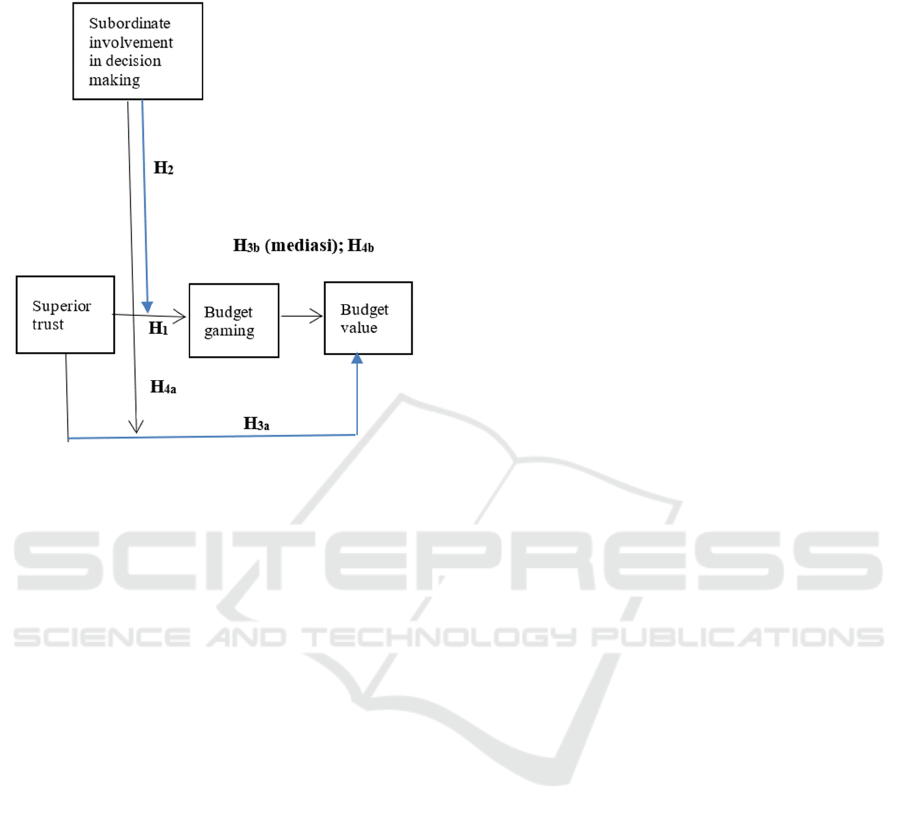

2.2.1 Superior Trust and Budget Gaming

Superior trust is the trust of the senior managers

towards the capability of lower managers (Libby and

Lindsay, 2019). High trust in the capability of

subordinate results in better respect and performance

of subordinates (Olson et al., 2007) so that it will

reduce information asymmetry and reduce the

tendency of subordinates to commit budget slack

(Gago-Rodríguez and Naranjo-Gil, 2016). This is

reinforced by Libby and Lindsay, 2019 which stated

that superior trust has a negative effect on the budget

gaming. The higher the trust of superiors in

subordinates, the less the budget gaming behavior

will be.

On the other hand, a lower level of superior trust

would cause a lack of open communication and

cooperation so that subordinates would embrace a

defensive behavior (Dirks and Ferrin, 2002).

Regarding the budget, Jensen, 2001 states that the

budgeting process could encourage managers to

behave dysfunctional against the long-term interests

of the company. Therefore, this study suspects that

the superior's trust in their subordinates can reduce

the budget gaming behavior. H1: Superior trust has

a negative effect on the budget gaming.

2.2.2 The Effect of Superior Trust on

Budget Gaming Moderated by

Subordinate Involvement in Decision

Making

Libby and Lindsay, 2019 state that trust has a

negative effect on the budget gaming. This means that

the higher the trust, the lower the budget gaming that

occurs in the company. Competent and capable

managers (subordinates) are less likely to rely on

fraud to achieve their budget targets if there is trust in

them. In addition, managers (subordinates) tend to

understand the negative impact of the budget gaming,

which is, it could negatively impact their future

rewards, causing them to act in a more collaborative

and honest way (Coletti et al., 2005). As the

budgeting process is an important and complex

activity because it has the possibility of functional

and dysfunctional impacts on the attitudes and

behavior of organizational members, to prevent

dysfunctional impacts of budgeting, all the upper,

middle and lower-level managers must be given the

opportunity to participate in the budgeting process

(Hansen and Mowen, 2013). Spreitzer and Mishra,

1999 found a positive relationship between superior

trust and managerial involvement in decision making.

This study suspects that the involvement of

subordinates in every decision making can strengthen

the relationship between superior trust and budget

gaming. H2: Superior trust will be stronger in

reducing the budget gaming when moderated by

subordinate involvement in decision making.

2.2.3 Superior Trust and Budget Value

In the budgeting process, budgeting involves slight

complex decisions, which often involve a level of

uncertainty due to the changing and more complex

The Interactive Effects of Superior Trust and Subordinate Involvement in Decision Making on Budget Gaming and Budget Value

185

competitive environment. This requires a higher

quality interaction between superiors and

subordinates and requires increased authority, shared

responsibility, and greater involvement in decision

making (Brower et al., 2009; Olson et al. 2007).

Therefore, value creation in the budgeting process is

highly dependent on the management of the

budgeting system. According to Libby and Lindsay,

2019, budget value is a perception of the added value

provided by a budgeting process. Budget value can

also be considered as the level of budget effectiveness

in helping business units to achieve their goals. Libby

and Lindsay, 2019 suggest that there is a significant

effect between superior trust and budget value. H

3a

:

Superior trust has a positive effect on budget

value.

2.2.4 Mediating Effects of Budget Gaming

on the Relationship between Superior

Trust and Budget Value

Libby and Lindsay, 2019 define superior trust as the

trust of senior managers in the capability of lower

managers. Superiors are more likely to receive

feedbacks from subordinates or there are

involvements of subordinates when the superior trusts

the subordinates' capability (Bol and Lill, 2015).

When superiors trust is high, subordinates are less

likely to risk violating their superiors' trust by

engaging in gaming behavior (Lewis and Weigert,

2012). This context allows subordinates to debate in

a more realistic budget than when there is no trust

towards lower managers, and this could reduce the

motivation to behave in gaming and increase the

budget value (Libby and Lindsay, 2019). Libby and

Lindsay, 2019 suggest that superior trust has a

substantial effect, either directly or indirectly, on

managers' perceptions of budget value. This study

suspects that superior trust has an indirect effect on

budget value, namely through the budget gaming.

H

3b

: Budget gaming mediates the relationship

between superior trust and budget value.

2.2.5 The Effect of Superior Trust on Budget

Value if Moderated by Subordinate

Involvement in Decision Making

Libby and Lindsay, 2019 state that superior trust has

an effect on budget value through increased

involvement from lower levels of management in the

decision-making process in the field of budgeting.

Furthermore, lower-level managers often have more

complete knowledge and information about their area

of responsibility than higher-level management. This

enables them to contribute in planning, coordinating

with other units, identifying and resolving problems

(Shields and Shields, 1998; Spreitzer and Mishra,

1999).

Olson et al., 2007 states that higher trust

facilitates the active involvement of subordinates

because it could make them feel more comfortable

and confident, hence they openly and actively

provide their personal information and knowledge

and even without fear of consequences if they

disagree with their superiors and colleagues. On the

other hand, in the absence of superior trust,

subordinates are more likely to respond / refuse

politely rather than willing to actively provide and

directly challenge the views of others (Olson et al.,

2007). Hypothesis (H3a) suspects that superior trust

will increase budget value and if superior trust

interacts with subordinate involvement in decision

making, it will strengthen the relationship between

the two. Therefore, this study suspects that H

4a

:

Superior trust will be stronger in increasing the

budget value if it is moderated by subordinate

involvement in decision making.

2.2.6 The Mediating Effects of Budget

Gaming on the Interactive Relationship

between Superior Trust Moderated by

Subordinate Involvement in Decision

Making with Budget Value

Superior trust is expected to generate value for the

company and reduce the budget gaming. Libby and

Lindsay, 2019 explain that superior trust is negatively

related to budget gaming and positively related to

subordinate involvement in decision making.

According to Spreitzer and Mishra, 1999 and Olson

et al., 2007, high trust affects the budget value

through the involvement of lower-level management

in decision making in the field of budgeting. Libby

and Lindsay, 2019 state that in particular, higher trust

from superiors to subordinates would reduce the

vulnerability felt by senior managers due to the

participations of subordinates in the budgeting

process in a consequential way. This causes superiors

to welcome the active participation of subordinates,

and the involvement of subordinates is expected to

moderate the relationship between superior trust and

budget value when mediated by budget gaming. H

4b

:

Budget gaming mediates the effect between

superior trust and budget value which is

moderated by subordinate involvement in decision

making. The complete conceptual model and the

ICE-HUMS 2021 - International Conference on Emerging Issues in Humanity Studies and Social Sciences

186

relationships between the hypothesis can be seen in

Figure 1.

Figure 1: Conceptual Model.

3 METHODS

3.1 Sample Selection and Data

Collection

To test the hypothesis, this study uses data collected

through a questionnaire survey in Indonesia. The

sample of this study is operational level managers at

54 large manufacturing companies in Southeast

Sulawesi Province, Indonesia (https://sultra.bps.

go.id/, 2019). The size of the large companies refers

to data from the Central Bureau of Statistics in

Southeast Sulawesi Province, namely industries with

a workforce of> 100 people. The selected

manufacturing sector and sample based on the

number of employees are for industrial control

purposes and company size control (Lau and Scully,

2018). The manufacturing industry is also chosen

because it is a large industry that affects the economy

of a region/ country and large industries are also

chosen because accounting and control procedures

tend to be more sophisticated in larger companies (He

and Lau, 2012).

The sampling method is a non-probabilistic

random sampling method (snowballing technique),

by distributing questionnaires to managers known by

the researchers (9 managers from 8 companies) and

then distributing the questionnaires to other managers

at manufacturing companies. The reason for choosing

managers in Sulawesi province is because, so far,

studies on the budget in Indonesia have been largely

concentrated on Java island, while studies with

sample outside of Java are still rare. Studies on budget

gaming are still very rarely conducted in Asian

countries (Rachmat and SeTin, 2020), and studies on

budget values are still very rare, both in European and

Asian countries. There are 162 respondents of

managers of large manufacturing companies who

participated in this study. However, only 145

questionnaires were completed and could be

analyzed.

3.2 Measurement of Variables

Superior trust is measured using 5 (five) question

items adopted from Libby and Lindsay, 2019, namely

(1) Senior managers show high respect for lower level

managers; (2) Senior managers believe that lower

level managers want to do the job well; (3) Senior

managers believe that lower level managers are

capable of doing a good job; (4) Senior managers

assign responsibilities to lower level managers to

improve the performance of business units; (5) Senior

management believes that the performance of lower

level managers has a big impact on what could

happen in the business unit.

Subordinate involvement in decision making, is

measured using 4 (four) question items developed by

Libby and Lindsay, 2019, namely (1) I can

communicate vertically or horizontally depending on

where the manager needs information; (2) I reassess

tasks that are given continuously to deal with new

problems or new opportunities; (3) The business unit

where I work always takes advantage of teamwork to

achieve integration and adaptation in managing

functional dependencies. (4) The communication that

is often conducted in the business unit where I work

is often in the form of consulting, sharing

information, or giving advice.

The gaming budget is measured by (five) question

items from Libby and Lindsay, 2019. Respondents

were asked to provide feedback regarding the

behavior of budget gaming in order to achieve budget

targets in their department. Among them are: (1)

Spending the unused budget at the end of the budget

period; (2) Delaying the necessary expenses; (3)

Accelerating sales at the end of the reporting period;

(4) Increase expenditure; (5) Negotiating budget

targets that are easier to achieve.

Budget value is measured by 3 (three) question

items developed by Libby and Lindsay, 2010.

Respondents are asked to give their opinion about the

The Interactive Effects of Superior Trust and Subordinate Involvement in Decision Making on Budget Gaming and Budget Value

187

value or benefits obtained from the budget system in

their department, which is related to (1) The time

spent in budgeting is equivalent with the benefits

received from the budget system; (2) The current

budget system helps companies to achieve goals,

including reducing dysfunctional behavior. (3) Even

though there is a possibility of deviant behavior in the

effort to reach the budget, the budget system that is

implemented still provides benefits for the company.

Every single question in all variables were

measured using a 7-point interval scale, namely a

scale of 1 (strongly disagree) to a scale of 7 (strongly

agree).

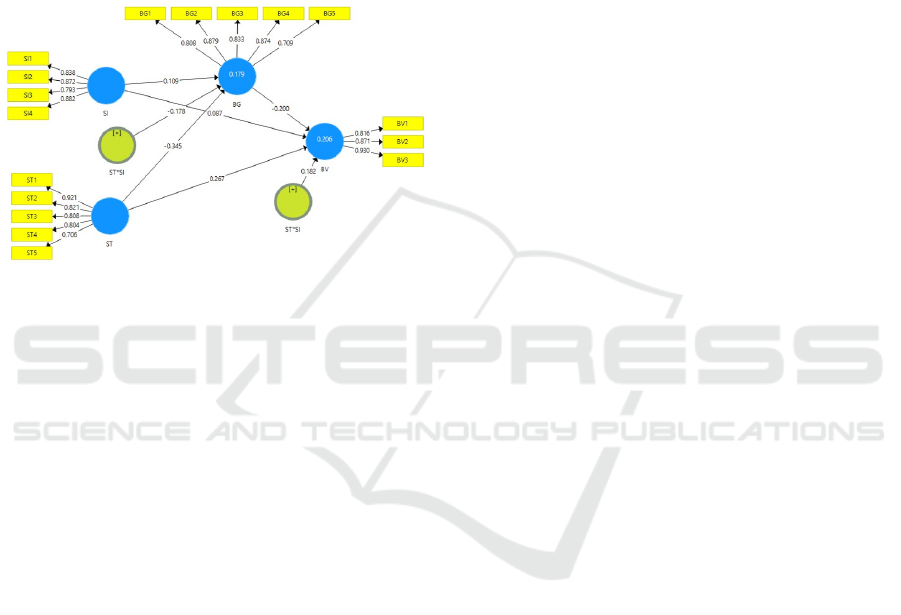

4 RESULTS AND DISCUSSION

Structural Equation Modelling (SEM) with a

component-based method (PLS-Partial Least Square)

is used for hypothesis testing. PLS produces a

measurement model, a model that connects latent

variables with manifest variables that can be used to

evaluate the validity and reliability of the instrument.

In addition, PLS also produces a structural model to

evaluate the goodness of fit of the model.

4.1 Measurement Model and

Structural Model

Validity is evaluated through convergent validity and

discriminant validity of each indicator, while

reliability is evaluated through Cronbach's Alpha

value and composite reliability. The validity test with

convergent validity uses the AVE (average variance

extracted) value. The AVE value that is accepted is a

value with a minimum threshold of 0.5 (Hair et al.,

2014). The average variance extracted (AVE) value

shows how much the variation is, in each indicator,

which could be explained by latent variables. Table 2

shows the AVE value for each construct ranging from

0.664 - 0.763. The results of the validity test show that

the convergent validity is acceptable. The results of

the validity test, which also uses discriminant

validity, which is based on the cross loading of the

indicator value, with the general rule that an

acceptable outer loading value is ≥ 0.7 (Hair et al.,

2014). Table 1 shows all items (17 items) of all

constructs (4 constructs) possess outer loading values

above 0.7. This means that there is no cross loading

and also shows an agreeable discriminant validity.

In order to find out whether the indicators used to

measure the three latent variables have a high degree

of conformity, composite reliability and average

variance extracted are calculated. According to Hair

et al., 2014 the composite reliability value between

0.70 to 0.9 is considered acceptable. Table 2 shows

that the Cronbach's alpha (CA) value for each

construct ranges from 0.843 - 0.880, and the

composite reliability (CR) value for each construct

ranges from 0.906 - 0.912. The results of this

reliability test show an acceptable internal

consistency reliability.

Table 1: Cross-Loading Between Construct.

Indicator ST SI BG BV

ST1 0.921 0.037 -0.336 0.331

ST2 0.821 0.066 -0.306 0.274

ST3 0.808 0.016 -0.343 0.304

ST4 0.804 0.101 -0.282 0.309

ST5 0.706 0.026 -0.259 0.203

SI1 0.114 0.838 0.045 0.113

SI2 -0.027 0.872 0.079 0.075

SI3 0.063 0.793 0.086 0.062

SI4 0.049 0.882 0.068 0.103

BG1 -0.240 0.034 0.808 -0.252

BG2 -0.345 0.086 0.879 -0.294

BG3 -0.354 0.064 0.833 -0.256

BG4 -0.354 0.094 0.874 -0.286

BG5 -0.233 0.045 0.709 -0.217

BV1 0.376 0.084 -0.178 0.816

BV2 0.263 0.048 -0.330 0.871

BV3 0.292 0.144 -0.321 0.930

Note: ST (Superior Trust); SI (Subordinate Involvement); BG

(Budget Gaming); BV (Budget Value)

Table 2: Construct Reliability (CR) and Average Variance

Extracted (AVE).

Latent Variable CR CA AVE

Superior trust (ST) 0.908 0.872 0.664

Subordinate

involvement (SI)

0.910 0.868 0.717

Budget gaming (BG) 0.912 0.880 0.677

Budget value (BV) 0.906 0.843 0.763

Structural model is a model that connects

exogenous latent variables with endogenous latent

variables or the relationship between endogenous

variables and other endogenous variables. R Square

value is used to test the structural model. The value of

R square shows the magnitude of the effect of certain

independent latent variables on the dependent latent

variables based on the research model. In general, the

R square value is 0.75; 0.50; and 0.25 is interpreted

as substantial, moderate, and weak (Hair et al. 2014).

The results show that the prediction oriented measure

ICE-HUMS 2021 - International Conference on Emerging Issues in Humanity Studies and Social Sciences

188

(R

2

= 0.52%) for budget gaming, which is described

by superior trust and the interaction of superior trust

with subordinate involvement in decision making.

The results also show the value of (R

2

= 0.26%) for

the budget value, which is described by superior trust,

the interaction of superior trust with subordinate

involvement in decision making, and budget gaming.

These results indicate that the superior trust variable

and the interaction of superior trust with subordinate

involvement in decision making have more predictive

power for budget gaming than budget value.

Figure 2: Path Diagram Model.

4.2 Hypothesis Testing Results &

Discussion

4.2.1 The Effect of Superior Trust on

Budget Gaming

The results of the path analysis between superior trust

and budget gaming show negative and significant

results, namely the value of path coefficient is -0.345;

p-value 0.020. These results indicate that both the

direction and the strength of the path coefficients for

the effect of superior trust and budget gaming support

Hypothesis 1. These results are in accordance with

Libby and Lindsay, 2019 which state that superior

trust has a negative effect on budget gaming. This

means that the higher the trust of superiors in

subordinates, the less the budget gaming behavior

will be. The results also support the view of Olson et

al., 2007, namely that high superior trust in the

capability of subordinates will result in better respect

and performance of subordinates.

4.2.2 The Effect of Superior Trust Moderated

by Subordinate Involvement in Decision

Making on Budget Gaming

The second tested hypothesis is that superior trust will

be stronger in reducing budget gaming when being

moderated by subordinate involvement in decision

making. Figure 2 shows that the path coefficient of

superior trust moderated by subordinate involvement

in decision making on budget gaming is negative with

a probability value (0.000) smaller than 0.01. Thus, it

can be concluded that superior trust moderated by

subordinate involvement in decision making has a

negative and significant effect on the budget gaming.

Since the p-value of 0.000 (hypothesis 2) is smaller

than the p-value of 0.020 (hypothesis 1), it can be

concluded that superior trust will be stronger in

reducing budget gaming when being moderated by

subordinate involvement in decision making (H2 is

supported). These results support Libby and Lindsay,

2019 which state that trust has a negative effect on

budget gaming. This means that the higher the trust,

the lower the budget gaming that occurs in the

company. The results also support Coletti et al., 2005,

namely that competent and capable managers

(subordinates) tend not to rely on fraud to achieve

budget targets if there is trust in them. In addition,

managers (subordinates) tend to understand the

negative effect of the budget gaming, which is, to

negatively effect their future rewards, causing them

to act in a more collaborative and honest way.

4.2.3 The

Effect of Superior Trust on Budget

Value

Figure 2 also shows that superior trust positively and

significantly affects the budget value, namely the path

coefficient of 0.267; p-value of 0.010. These results

support hypothesis 3a. In the budgeting process,

budgeting involves complex decisions due to the ever

changing competitive environment. This leads to the

need for higher quality interactions between superiors

and subordinates and demands increment in authority,

shared responsibility, and greater involvement in

decision making (Brower et al., 2009; Olson et al.,

2007). The results are also in accordance with Libby

and Lindsay, 2019 which show that superior trust has

a significant effect on budget value.

4.2.4 The Effect of Superior Trust on Budget

Value

mediated by Budget Gaming

Hypothesis 3b which is being tested, is the effect of

superior trust on budget value mediated by budget

gaming. Figure 2 shows that the path coefficient of

superior trust to budget value mediated by budget

gaming is positive (path coefficient 0.069; p-value

0.028). Thus it can be concluded that the budget

gaming mediates the effect between superior trust and

budget value. (Hypothesis 3b is supported).

These results have the correlation with the

previous findings, which show superior trust has a

The Interactive Effects of Superior Trust and Subordinate Involvement in Decision Making on Budget Gaming and Budget Value

189

negative effect on budget gaming (significant, H1 is

supported) and the budget gaming has a negative

effect on the budget value (path coefficient -0.200; p-

value 0.017 is smaller than 0.05). This finding also

supports Hair et al., 2014 that mediation is considered

significant if all path coefficients are also significant.

This result is also in accordance with Lewis and

Weigert, 2012, that when the superiors' trust is high,

subordinates tend not to take the risk of violating their

superiors' trust by engaging in dysfunctional

behavior. In addition, Libby and Lindsay, 2019 state

that superior trust has a substantial impact, either

directly or indirectly on budget value.

4.2.5 The Effect of Superior Trust

Moderated Subordinate Involvement

in Decision Making on Budget Value

Figure 2 shows that the path coefficient of superior

trust moderated by subordinate involvement in

decision making (ST*SI) on budget value is positive

with a p-value of 0.239. These results conclude that

superior trust moderated by subordinate involvement

in decision making has no effect on budget value

(Hypothesis 4a is not supported). Although

Hypothesis 3a is supported, namely that superior trust

increases budget value, this relationship cannot be

strengthened by subordinate involvement in decision

making. This indicates that the possibility of the

management's perception of the value / benefits of the

budget is not related to whether or not subordinates

are involved in the decision-making process.

4.2.6 The Effect of Superior Trust Interaction

with Subordinate Involvement in

Decision Making on Budget Value

Mediated by Budget Gaming

Hypothesis 4b which is being tested is the effect of

the interaction between superior trust with

subordinate involvement in decision making (ST*SI)

on budget value (BV) mediated by budget gaming

(BG). Figure 2 shows that the path coefficient of

interaction between superior trust and subordinate

involvement in decision making on budget value

mediated by budget gaming is 0.035; p-value 0.084.

Thus it can be concluded that the interaction of

superior trust with subordinate involvement in

decision making mediated by budget gaming is a

significant effect on budget value (Hypothesis 4b is

supported). These results have the correlation with

the previous findings which support that the

relationship between superior trust and subordinate

involvement in decision making (ST*SI) on budget

gaming (significant, H2 is supported) and the

relationship between budget gaming and budget value

is significant (path coefficient -0.200; p. -value

0.017). These results are in accordance with Spreitzer

and Mishra, 1999; Olson et al., 2007, namely that

high trust affects budget value by increasing the

involvement / participation of managers in the

budgeting decision-making process.

5 CONCLUSIONS

The results of this study concluded that first, superior

trust has a negative effect on budget gaming; second,

superior trust is stronger in reducing the budget

gaming when moderated by subordinate involvement

in decision making; third, Superior trust has a positive

effect on budget value; fourth, the budget gaming

mediates the relationship between superior trust and

budget gaming; Fifth, budget gaming mediates the

effect of the interaction between superior trust and

subordinate involvement in decision making on

budget value. The study results also concluded that

although superior trust increases the budget value, if

superior trust is moderated by subordinate

involvement in decision making, it is not adequate in

increasing the budget value.

The results of this study have significant

implications for both theory and practice. First,

subordinate involvement in decision making and

superior trust are important components in budgeting

and this study also provides an important

understanding of how the two interact with

dysfunctional behavior in budgeting. In particular,

this study shows that superior trust is more effective

at reducing budget gaming when moderated by

subordinate involvement in decision making. Second,

this study also enriches the budgeting literature,

especially on budget value. The finding about budget

gaming can mediate the relationship between superior

trust and budget value provides an understanding of

the importance of superior trust in increasing budget

value because of its role in reducing the budget

gaming. This study also provides an understanding

that it is very important to involve subordinates and

superior trust in designing a budget system which

could overcome gaming behavior.

Third, these findings recommend that superior

trust is very important, therefore, finding ways to

increase superior's trust should always be an

important agenda of a company, for example, through

good recruitment and promotion practices,

constructive and non-threatening feedback, training

and mentoring programs, and others.

ICE-HUMS 2021 - International Conference on Emerging Issues in Humanity Studies and Social Sciences

190

The study's plan also provides some future

research opportunities. First, this study is limited to

only a few variables, such as superior trust,

subordinate involvement in decision making, budget

gaming, and budget value. Further research can

explore other variables that may affect budget value,

such as budget based bonuses and budget emphasis;

Second, this research uses a survey method, therefore

the limitations of this method are most likely inherent

in this study, for example the limitations in obtaining

a representative sample and an unbiased sample.

Future studies can use experimental methods to

ensure the causal relationship between superior trust

and subordinate involvement in decision making on

budget gaming and budget value; Third, this study is

supported by a relatively small sample of data, and

this is likely to reduce the power of statistical tests.

Therefore, future studies are suggested to expand the

sample data.

REFERENCES

Bart, C. (1988). Budgeting gamesmanship. Acad. Manag.

Exec. 2(4), 285–294.

Bol, J.C., Lill, J.B (2015). Performance target revisions in

incentive contracts: Do information and trust reduce

ratcheting and the ratchet affect? Account. Rev. 90(5),

1755–1778.

Brower, H. H., Dineen, B.R., Lester, S.W., Korsgaard. M.A

(2009). A closer look at trust between managers and

subordinates: Understanding the effects of both trusting

and being trusted on subordinate outcomes. J. Manag.

35(2), 327–347.

Coletti, A.L., Sedatole, K.L., Towry, K.L. (2005). The

effect of control systems on trust and cooperation in co-

llaborative environments. Account. Rev. 80(2), 477–500.

Daumoser, C., Hirsch, B., Sohn, M. (2018). Honesty in

budgeting: A review of morality and control aspects in

the budgetary slack literature. J. Manag. Control. 29(2),

115–159.

Dirks, K.T., Ferrin, D.L (2002). Trust in leadership: Meta-

analytic findings and implications for research and

practice. J. Appl Psychol. 87(4), 611–628.

Dunk, A.S. (1993). The effect of budget emphasis and

information asymmetry on the relation between

budgetary participation and slack. Account. Rev. 68(2),

400–410.

Gago-Rodríguez, S., Naranjo-Gil, D. (2016). Effects of

trust and distrust on effort and budgetary slack: An

experiment. Manag. Decis. 54(8), 1908–1928.

Gilabert-Carreras, M., Gago, S., Naranjo-Gil, D. (2012).

The relationship between trust and budgetary slack: An

empirical study. In EEML 2012–Experimental

Economics in Machine Learning. 49–60.

Hair, J. F., Ringle, C.M., Sarstedt, M. (2014). A Primer on

partial least squares structural equation modelling

(PLS-SEM). Thousand Oaks, CA: Sage.

Hansen, D.R., Mowen, M. (2013). Managerial Accounting,

Salemba Empat. 8

th

edition.

He, J., Lau, C. (2012). Does the reliance on nonfinancial

measures for performance evaluation enhance

managers’ perceptions of procedural fairness. Stud.

Manag. Financial Account. 25, 363-388.

Huang, C.L., Chen, M.L. (2010). Playing devious games,

budget emphasis in performance evaluation, and

attitudes towards the budgetary process. Manage.

Decis. 48(6), 940-951.

Jensen, M.C. (2001). Corporate budgeting is broken—let’s

fix it. In: Harv. Bus. Rev. 79(10), 94–101.

Lau, C.M., Scully, G., Lee, A. (2018). The effects of

organizational politics on employee motivations to

participate in target setting and employee budgetary

participation. J Bus Res. 90, 247-259.

Lewis, J.D., Weigert, A.J. (2012). The social dynamics of

trust: Theoretical and empirical research, 1985–2012.

Social Forces. 91(1), 25–31.

Libby, T., Lindsay, R.M. (2010). Beyond budgeting or

budgeting reconsidered? A survey of North-American

budgeting practice. Manag. Account. Res. 21, 56-75.

Libby, T., Lindsay, R.M. (2019). The effects of superior

trust and budget-based controls on budgetary gaming and

budget value. J. Manag. Account. Res. 31(3), 153–184.

Lukka, K. (1988). Budgetary biasing in organizations:

Theoretical framework and emperical evidence.

Account Organ Soc. 13(5), 281-301.

Maria, D., Nahartyo, E. (2012). Budgetary slack,

participatory budgeting, distributive and procedural

justice, subordinate’s trust in supervisor. Jurnal dan

Prosiding SNA - Simposium Nasional Akuntansi.

Neely, A., Bourne, M., Adams, C. (2003). Better budgeting

or beyond budgeting? Measuring Business Excellence

7(3), 22-28.

Olson, B., Parayitam, S., Bao, Y. (2007). Strategic decision

making: The effects of cognitive diversity, conflict, and

trust on decision outcomes. J. Manag. 33(2): 196–222.

Salterio, S.E. (2015). Barriers to knowledge creation in

management accounting research. J. Manag. Account

Res. 27(1): 151–170.

Rachmat, R.S., SeTin, S.T (2020). Budget based bonus,

budget emphasis, budget gaming, and the impact on

budget value. Jurnal Keuangan dan Perbankan. 4(3),

363-374.

SeTin, S. T, Sembel, R., Agustine, Y. (2019). Budget

gaming behavior: Evidence in Indonesia manufacturing

companies. Jurnal Keuangan dan Perbankan. 23(2),

258-269.

Shields, J.F., Shields, M.D (1998). Antecedents of parti-

cipative budgeting. Account Organ Soc. 23(1), 49–76.

Simmons., Cynthia V. (2012). Participative budgeting,

budget evaluation, and organizational trust in post-

secondary educational institutions in Canada. J. Acad

Admin Higher Educ. 8(2), 41-53.

Spreitzer, G.M., Mishra, A.K. (1999). Giving up control

without losing control: Trust and its substitutes’ effects

on managers’ involving employees in decision making.

Group & Organization Management. 24(2), 155–187.

https://sultra.bps.go.id/2019.

The Interactive Effects of Superior Trust and Subordinate Involvement in Decision Making on Budget Gaming and Budget Value

191