Text Analysis in Finance: A Survey

Issam Aattouchi

1

, Mounir Ait Kerroum

1

and Saida Elmendili

2

1

Computer science research Laboratory, Faculty of Sciences, Ibn Tofail University, Kenitra, Morocco

2

Engineering Sciences Laboratory, National School of Applied Sciences, Ibn Tofail University, Kenitra, Morocco

Keywords: Finance analysis, NLP, DL, Financial Data Sources, Classification, Dictionaries, Word embeddings,

Word2vec, Bayesian Classifier.

Abstract: The new advancements in the domains of artificial intelligence and machine learning, have provided a vast

opportunity to provides a means to interpret external data correctly, learn from such data, and exhibit flexible

adaptation. The current combination of computing power and complex algorithms has made fields such as

Artificial Intelligence, and particularly its Deep Learning branch, very popular and influential. The financial

sector is undergoing a significant transformation in light of the new emerging artificial intelligence

technologies and the increasingly competitive markets. This article introduces a survey of research on the

analysis of the recent financial news, presenting and comparing different sources of information, methods and

models of content analysis in the financial markets (return on assets, volatility, interest rate, etc.). The purpose

of this surveys is providing a state-of-the-art, on the application of sentiment analysis methods, in the finance

domain, to provide systematic approach in decision making.

1 INTRODUCTION

The last breakthroughs in Artificial Intelligence and

Machine Learning have started getting a lot of

attention recently. Finance is one particular area

where sentiment analysis models started getting

traction, combining both computational power and

complex algorithms can now perform tasks that were

historically assigned to humans, such as object

recognition or speech. The inner force of these

techniques results in their astonishing capacities of

performing and dealing with unstructured data.

Natural Language Processing (NLP), as one of the

most promising fields in Machine Learning and

maybe its hottest area, has managed to resolve many

tasks that seemed extremely difficult in the past:

Information Retrieval, Information extraction,

Machine translation, Spam filter, Sentiment analysis,

etc. The main difficulty when applying NLP is the

high dimensionality of text data. Hence, many

methods are developed to quantify text into numerical

vectors.

In finance, the flows of news update the investor’s

understanding and influence their sentiment and

hence, shapes the financial markets (Asset returns,

Volatility, Interest rates, etc.). Thus, one of the most

critical challenges that an investor has to overcome is

to extract useful information from text data to use it

in decision making. More generally, obtaining an

accurate forecast of stock market movement is the

engine of financial prediction. Many algorithms are

used for this purpose. News Analytics in Finance is

the process of integrating quantified financial

information into the analysis procedure, in order to

improve the perception of the market by the investor.

2 DATA SOURCES

2.1 Data Sources Type

Investors receive data/news from different sources.

However, some sources are far more reliable than

others and cannot treated equally. In literature, we can

distinguish four classes of news sources:

Everyday news: This includes mainstream Media

which are broadcasted via newspapers, radio and

television.

Pre-news: This includes sources that reporters

process to give common news (e.g Securities and

Exchange Commission reports).

Social media: These sources are less reliable than

50

Aattouchi, I., Ait Kerroum, M. and Elmendili, S.

Text Analysis in Finance: A Survey.

DOI: 10.5220/0010728200003101

In Proceedings of the 2nd International Conference on Big Data, Modelling and Machine Learning (BML 2021), pages 50-59

ISBN: 978-989-758-559-3

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

the previous ones. They may contain dangerous

inaccurate information due to the simplicity of

spreading fake news. some financial statements are

divided into two main categories (Mitra & Mitra,

2011):

Regular announcements: These are all types of

news from reliable sources.

Event-driven announcements: News, social

media streams and rumours.

2.2 Financial Data Sources

In this survey, we present the data sources most

commonly used in Text Analysis in Finance:

Sedar - Public Company Documents Search

(SEDAR, 2015): The majority of relevant financial

information: quarterly earnings releases, financial

statements, and recent stock prices, are all published

in the “Investor Relations” section of company

websites.

Edgar - Company Name Search (SEC.Gov |

EDGAR - Search and Access, 2019): information

relating to the annual reports on the security of public

Customer companies is also available on the websites

of the security regulators.

Financial Statement Data Sets (SEC.Gov |

Financial Statement Data Sets, 2009): This data is

extracted from corporate financial reports using

eXtensible Business Reporting Language (XBRL).

Compared to the numeric and textual data sets of the

financial industry and their notes, the financial

statement data sets are the most reliable.

Financial Performance Data (Industry

Canada) (Financial Performance Data, 2015): This

benchmarking tool for SMEs is based on Canadian

tax return data. It includes industry averages (by

NAICS) for income statement and sheet objects,

profitability information and financial ratios.

It covers small and medium-sized businesses,

with incomes between $30,000 to $5,000,000.

World Bank Open Data (Data Catalog | Data

Catalog, 2015):On this site, you can find datasets

such as:

- Unit-level data sets and indicators are a series of

counts collected at regular periods over time.

- Unit-level data collected from many sources:

sample studies, population censuses, and

administrative systems.

- Data containing explicit geographic positioning

information, in raster format or vector.

IMF Data (IMF Data, 2015): The International

Monetary Fund publishes data in: the international

finances, debt rates, currency exchange reserves,

commodity payments and funds.To export some

datasets, you might be required to register, user is able

to export data as Excel, PDF, image, Powerpoint,

.html and .mht files without registering in some cases.

European Union Open Data Portal

(Data.Europa.Eu, 2015): The website funded by the

European Union- is a comprehensive portal, featuring

datasets from various sectors, which are free and easy

to access. User don’t need to register to download any

datasets either.

Financial market statistics (Bank of Canada,

2015): Various Bank of Canada and financial market

statistics such as bond yields, treasury bills, corporate

paper rate, publishes data, from 1991 to present.

Bank of Canada - Interest Rates (Interest

Rates, 2015): The Bank of Canada is a financial

institution in Canada. Valet Web Services provides

programmatic access to financial data from around

the world. User can get financial data and information

from the Bank of Canada using the Valet API, such

as daily exchange rates. Historical time series data are

available in Statistics Canada's CANSIM database.

FRED: Federal Reserve Economic Data

(Federal Reserve Economic Data | FRED | St.

Louis Fed, 2015): Federal Reserve Economic Data is

a database maintained by the Research Division of the

Federal Reserve Bank of St. Louis that contains over

765,000 economic time series from 96 sources. These

open Data include money, finance and banking,

national accounts, population, jobs and labour

markets, production and business operations, prices,

international data.

Quandl (Quandl, 2015): Analysts from the

world's biggest hedge funds, asset managers, and

investment banks use Nasdaq's Quandl platform.

Investment professionals will benefit from this

outstanding collection of financial, economic, and

alternative datasets.

Table I summarizes these Data Sources with their

own characteristics:

Table 1: Data Sources characteristics.

Data Sources T

yp

e of Data/Size

SEDAR Annual Information Form, Annual

Report, Annual Statement of

Payments, Financial Statements,

Fund Facts, Fund Summary,

Management’s Discussion &

Analysis (MD&A), Marketing

Material, Material Change Report,

Real Estate Offering Document,

Report of Exempt Distribution.

Text Analysis in Finance: A Survey

51

EDGAR The most common Documents

include: 10-K (Annual report), 10-Q

(Quarterly report), 8-K (Current

re

p

ort

)

..

Financial

Statement

Data Sets

Annual report, summary of the

company’s operations, events, an

acquisition, bankruptcy, disposal of

assets.

Financial

Performance

Data

(Industry

Canada)

Reports feature the number of

businesses in the selected industry,

detailed financial data on revenues

and expenses industry average's for

income statements and balance sheet

items ..

World Bank

Open Data

Time Series (14 681) Datasets and

Indicators level data, Microdata

(3 441) Unit-level data, Geospatial

(

777

)

Data.

IMF Data World Economic Outlook (WEO)

Databases, Statistical Data, Dataset

Portals, Financial Data/Rates,

Regional office document, financial

re

p

orts.

EU Open

Data Portal

open data sets across EU policy

domains, including the economy,

employment, science, environment

and education.

Financial

market

statistics

Report of monetary authorities,

Report of business performance and

ownership, financial statements and

p

erformance, financial markets.

Bank of

Canada

Measures the cost of overnight

general collateral funding in

Canadian dollars using Government

of Canada treasury bills and bonds as

collateral for repurchase transactions,

Money Market Yields, 10-Year

Lookup U.S. Prime Rate Charged by

Banks, Federal Funds Rate,

Commercial Pa

p

er.

Federal

Reserve

Economic

Data

Interest Rates (1,000+), Exchange

Rates (160+), Monetary Data (990+),

Financial Indicators (2,000+),

Banking (2,000+), Business Lending

(2,300+), Foreign Exchange

Intervention (3+), National Income

& Product Accounts (13,000+),

Federal Government Debt (3+), Flow

of Funds (38,000+), U.S. Trade &

International Transactions (410+),

Banking and Monetary Statistics,

1914-1941 (1,200+), Daily Federal

Funds Rate...

Quandl Equity Prices, Equity Fundamentals,

Equity Earnings, Estimates, Analyst

Ratings, Futures, Economics, FX and

Rates, Payment card transactions,

Satellite imagery / GPS

The data sources cited in this paper are open, so

you just need to choose the appropriate source to

answer a specific financial problem.

3 TEXT PRESENTATION

METHODS

The NLP faces a real challenge of the very high

dimensionality of textual data. Thus, transform

textual data into quantitative numerical data is a

challenging task. In fact, the text was examined on

three levels: text, content and the context.

Given that the leading role of the research is to

transform the text into useful information, the

complexity increases considerably with a considered

level. Therefore, the primary applications are those

that treat news simply as text.

Depending on the type of application used, textual

data is represented in very different ways (el

MENDILI, 2020). Note that for an investor, the

objective is to assign a relevant score to the news.

It could simply use the set of words that define the

sentences and take into account the context and the

second degree of these sentences. It looks pretty

natural that the complexity increases for the last

choice.

3.1 Dictionaries

The simplest way to represent a text is the dictionary.

It consists of taking the set of all possible words,

labelling them as positive/negative and using the

resulting group to assign a sentiment score to

sentences simply. Note that finance can define a

particular lexicon consisting only of financial words.

The General Inquirer (GI) integrated dictionary

(Gilman, 1968) and the DICTION text analysis

program (Wayback Machine, 2002) are the first two

popular lexicons used in financial news analysis.

Most researchers used the Harvard dictionary and The

General Inquirer word lists, because it was the first

lists readily available (LOUGHRAN &

MCDONALD, 2011) (Doran et al., 2010; Engelberg,

2008; Ferris et al., 2012; Henry & Leone, 2009; Ozik

& Sadka, 2012; TETLOCK, 2007; TETLOCK et al.,

2008).

Research has shown that more than 73.8% of the

number of words declared negative in the list

proposed in / Harvard are words that are not negative,

if used in the financial field (LOUGHRAN &

MCDONALD, 2011).

BML 2021 - INTERNATIONAL CONFERENCE ON BIG DATA, MODELLING AND MACHINE LEARNING (BML’21)

52

To remedy this problem, Loughran and

McDonald's developed a new dictionary of 3,532

unique lists of financially binding Words (Ding et al.,

2017), using the US Security and Exchange

Commission portal, from 1994 to 2008. The

Loughran-McDonald Financial Sentiment Dictionary

(LMFSD) is used by several subsequent research

(Azmi Shabestari et al., 2019; Jangid et al., 2018;

Kearney & Liu, 2013).

3.2 One-hot Encoding of Words and

Characters

Text is the most common form of sequence data. It can

be whether as a sequence of words or characters. The

most common (and essential) numerical

representation of text is the one-hot encoding.

The idea is elementary. We consider a space of

dimension N =Number of words in a dictionary, and

we represent each word as a binary vector of size N

(The vector is all zeros except one index, which

determines the order of the word in the dictionary).

A sentence is then naturally represented after

tokenization (split words in a sentence by blank or

punctuation) by a vector of size N. Each entry

represents the number of occurrences of i-word of the

dictionary in the sentence.

We can assign a weight to each word describing its

polarity (This leads to a new vector with the same non-

zeros elements but with a weighted value representing

the cumulative effect) (Vargas et al., 2017).

3.3 Word Embeddings

The vectors obtained by one-hot encoding are sparse,

binary and ultra-high dimensional. One can imagine

representing text data with dense vector to gain both

complexity and effectiveness.

The simplest way to associate a dense vector to a

word is to choose the vector at random. However, the

resulting space is also random and do not represent

the text’s inherent structure. To gain incoherence, one

can say that the geometric distance between two

vectors must reflect the semantic (or contextual)

relationship between words.

For example, we may want to have similar

distances between synonyms (or antonyms, actually)

or a vector which enables us to pass from single to

plural words. Precisely, the resulted space should

somehow map reasonably the human language with

numerical vectors. Similarly, the literature called

semantic space models of meaning or vector space

(Akbik et al., 2018; Harris, 1954; Landauer &

Dumais, 1997; Peters et al., 2018;

Sahlgren, M, 2006;

Turney & Pantel, 2010

).

3.4 Word2Vec (Skip-gram model)

Google released Word2Vec in 2013 as a useful tool.

It includes two (nearly identical) models: Skip-gram

and Continuous Bag of Words (Mikolov et al., 2013;

Mikolov, Sutskever, et al., 2013).

Its goal is to convert each pair of words into a

calculable numeric vector while maintaining the

degree of resemblance and analogy between them.

Word2vec has been the main spark of NLP since its

publication, and it is now widely employed in the

discipline.

We will introduce the Skip-gram model to

understand its functioning. In the skip-gram, our

primary focus is on one word (called Centre), and we

try to predict words that will appear around it (called

backgrounds). More precisely, we are mainly

interested in the conditional probabilities of each set

under the given centre word.

4 SENTIMENT CLASSIFICATION

We investigate below Das and Chen algorithm (Das

& Chen, 2007) to classify news into positive/negative

and scoring them. The goal is to detect the investor’s

sentiment from stock message boards.

To implement their algorithm, they needed to use

specific databases (Mitra & Mitra, 2011):

Dictionary: Used to determine the nature of

words (Adjective, adverb, etc.).

Lexicon: A collection of finance words.

Grammar: The training corpus of base messages

used. Note that the lexicon and grammar define here

the context of statements. We cite information about

five classifiers:

4.1 Naive Classifier (NC)

Naïve Classifier is the primary language-dependent

classifier. Given a sentence/news item, we can assign

a simple sentiment score created on the lexical word

count. Say, for instance, that if the number of

positive/optimistic words exceeds the number, of

negative/pessimistic words, the message is labelled

positive and vice versa.

We can also naively assign a sentiment score

(difference between the number, of positive and

Text Analysis in Finance: A Survey

53

negative words) (Shihavuddin et al., 2010).

4.2 Vector Distance Classifier

Using our dictionary of words D, we consider here a

one-hot encoding representation of words. With a D-

dimensional space.

Thus, we can represent each sentence by a vector

(each entry represents simply the number of

occurrences of the corresponding word in D).

Das and Chen (2007), has used this algorithm

which is built on the same principle used by search

engines.

4.3 Discriminant-based Classification

The previous classifiers did not distinguish between

words. However, some words, are far more potent

than others. As seen in (Natural Language Processing

Tested in the Investment Process through New

Partnership | J.P. Morgan, 2018), sentimental words

that are frequently repeated/used (We do not consider

linkage words) must be treated differently by the

classifier.

Hence, this leads us to redefine the counting-

based method by weighting words, the commonly

used tool is Fisher’s Discriminant.

4.4 Adjective-adverb Classifier

Another approach for Classification is to consider

filter words, so that we take a subset of sentences that

includes only segments with high emphasis (i.e.,

adverbs and adjectives).

Using dictionaries like CUVOALD (Computer

Usable Version of the Oxford Advanced Learner’s

Dictionary), one can quickly build programs

performing sentimental counting across these specific

lexicons.

4.5 Bayesian Classifier

Bayesian Classification is the most famous technique

used in practice. We can find its applications in

almost all AI-powered fields as (Mbadi, S, 2018).

The main idea is to compute prior probabilities

using Datasets and then calculate posteriors ones by

the Bayes formula. The universality and the

simplicity of this approach are maybe the reasons

behind its success.

In the context of text classification, the classifier

is trained on pre-trained corpus and try to learn some

statistical features of this text. It uses word-based

probabilities, and thus Bayesian classifier is an

independent language, since he sees sentence as a

simple bag of words.

4.6 Support Vector Machines

Support Vector Machine or simply SVMs are widely

used classifiers similar to cluster analysis. However,

they are mainly used to very-high-dimensional

spaces, which makes sense in the context of a text

represented by ultra-high dimensional spaces via one-

hot encoding.

The main idea of SVMs is to find, given a training

corpus, that best separate classes. Classification

methods for sentiment extraction are applied to news

or tweets datasets (Ghiassi et al., 2013; Li et al.,

2009). Li et al. (2009) use several machine learning

methods classifiers to obtain the sentiments from

Tweets. Its implementation shows that the Support

Vector Machine classifier is more efficient than the

naive Bayes classifier and decision trees.

5 UNSUPERVISED FINANCIAL

NETWORKS ANALYTICS

Rather than basing our analysis on text messages and

attempting to give emotion scores or forecast market

movements, we might consider the market as a vast

network. That is, modelling interconnected stocks

using flows of information.

It appears that strongly connected stocks reactions

are highly correlated. Thus, this graph modelling will

allow us to extract patterns/features that is used

inferentially. However, how should we define our

network? What do we mean by correlated stocks?

There are many possible implementations. For

example, Das and Sisk (2005), built a network based on

the number of standard handles forwarded to pairs of

stock.

5.1 Centrality

After modelling the problem with networks, the field

of graph theory lends itself naturally. Centrality

measures are among the most widely used indices

based on network data. A node is called central, if it

has strong connections (directly or indirectly), to

other nodes.

Ambrus et al. (2018), Ambrus and Elliott (2020),

lighten how this measure, can be computed, they

explain that risk-sharing in shape studies where

transfers between pairs of agents can only depend on

BML 2021 - INTERNATIONAL CONFERENCE ON BIG DATA, MODELLING AND MACHINE LEARNING (BML’21)

54

the income generated by the agents to which they are

both linked in a pre-existing network.

5.2 Communities

Another essential feature of graphs is communities.

More precisely, a community is a cluster of nodes,

which can be detected using classical algorithms:

Lloyd’s heuristic or the walk trap algorithm (Note that

the problem of clustering is NP-hard, these algorithms

do not always give the optimal solutions but are very

practical).

Finally, communities tend to react uniformly due

to the strong presence of contagion phenomena inside

them. As proposed by (Schweitzer et al., 2009),

currently, the risk system literature has started to use

the topology of financial networks to measure

systemic risk. The complexity of the economic

system is perhaps extended with new paradigms using

the different economic networks (Billio et al., 2012;

Creel et al., 2015; Diebold & Yilmaz, 2015; Hautsch

et al., 2014).

5.3 Latent Dirichlet Allocation (LDA)

Latent Dirichlet allocation (David M Blei et al.,

2003), describe the Topics in a word space and

describe the documents in a Topics space, based on

calculating the DIRICHLET distribution of words for

each Topic and the calculating of the DIRICHLET

distribution of Topic for each document. The space of

the projection of a document is a latent space of low

dimension.

More specifically, LDA is a three-level

hierarchical Bayesian model, in which each item is

considered a finite mixture of latent topics. This

algorithm is used for different purposes as: Topics

extraction, Reduction of dimension, novelty

detection, summarization, similarity and relevance

judgments, etc.

The algorithm's goal is to depict short descriptions

of texts (or any other collection of data) that enable

processing of the text corpora while preserving the

essential statistical relationships that are useful for

basic tasks. LDA generally works best due to its

generative nature. LDA is different in how it

considers documents as a mixture of topics and topics

as a distribution over words as shown in (Asadi

Kakhki et al., 2018; Feuerriegel et al., 2016).

6 DEEP LEARNING IN FINANCE

Deep learning is a subfield of machine learning,

which involves computers processing large amounts

of data using artificial neural networks that mimic the

structure of the human brain.

Whenever new information is incorporated, the

existing connections between neurons are subject to

change and expand, this operation allows the system

to learn things without human intervention,

autonomously, while improving the quality of its

decision-making and forecasts. Among the different

techniques, Deep Multilayer Perceptron (DMLP),

CNN, RNN, LSTM, Restricted Boltzmann Machines

(RBMs), Deep Belief Networks (DBNs), and

Autoencoders (AEs).

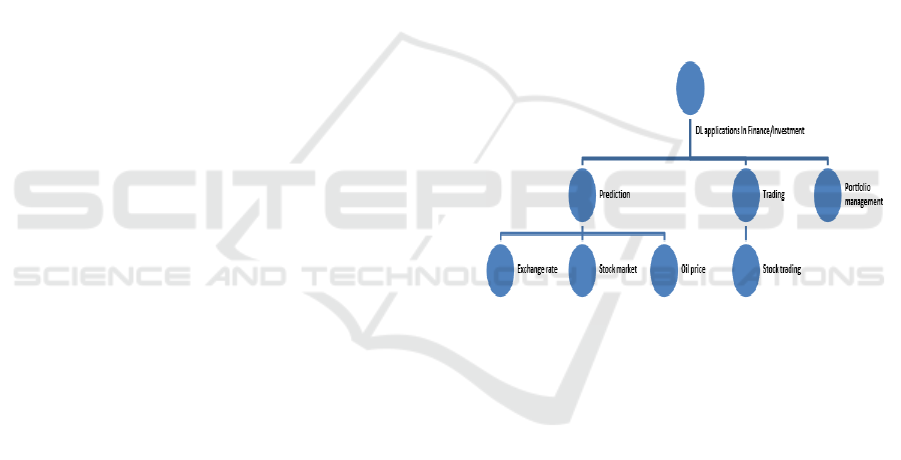

About 15 studies on the application of deep

learning to a specific finance domain are examined in

this part. Figure 1 depicts the link between commonly

used DL models:

Figure 1: link between commonly used DL models

We give a review of some DL model's

applicability in two financial fields: Prediction and

trading.

6.1 Prediction

We look at this subject from three aspects of

prediction: exchange rates, stock markets, and oil

prices:

Galeshchuk and Mukherjee (2017), assert that a

single hidden layer NN or SVM performs worse than

a basic model such as moving average (MA).

However, they discovered that due of the consecutive

layers of DNN, CNN could obtain higher

classification accuracy in predicting the direction of

the change in exchange rate.

Ravi et al. (2017), use MLP (FNN), chaos theory,

and multiobjective evolutionary algorithms to create

Text Analysis in Finance: A Survey

55

a hybrid model. Their Chaos+MLP + NSGA-II model

has a remarkably low mean squared error (MSE) of

2.16E-08.

Kim et al. (2015), suggest a deep convolutional

neural network architecture for predicting whether or

not a customer is suitable for bank telemarketing. The

number of layers, learning rate, initial value of nodes,

and other factors that should be established when

building a deep convolutional neural network are

discussed and presented.

Lee et al. (2017), employed FFNN, Support

Vector Regressor (SVR), and RBM-based DBN to

analyze the revenues and profitability of

organizations. They present a corporate performance

prediction model based on deep neural networks that

employs financial and patent metrics as predictors.

An unsupervised learning phase and a fine-tuning

phase are included in the proposed paradigm.

A constrained Boltzmann machine is used in the

learning phase. The fine-tuning step employs a

backpropagation algorithm and a recent training data

set that reflects the most recent trends in the

association between predictors and business

performance. When compared to the SVR-based

model, the suggested approach has a prediction error

reduction of 1.3–1.5 times. The suggested model, in

particular, outperforms SVR-based models in

predicting the performance of companies that

experience earnings surprises or shocks. This

demonstrates that the proposed model has long-term

predictability, whereas general prediction models

exhibit a decline in prediction accuracy over time.

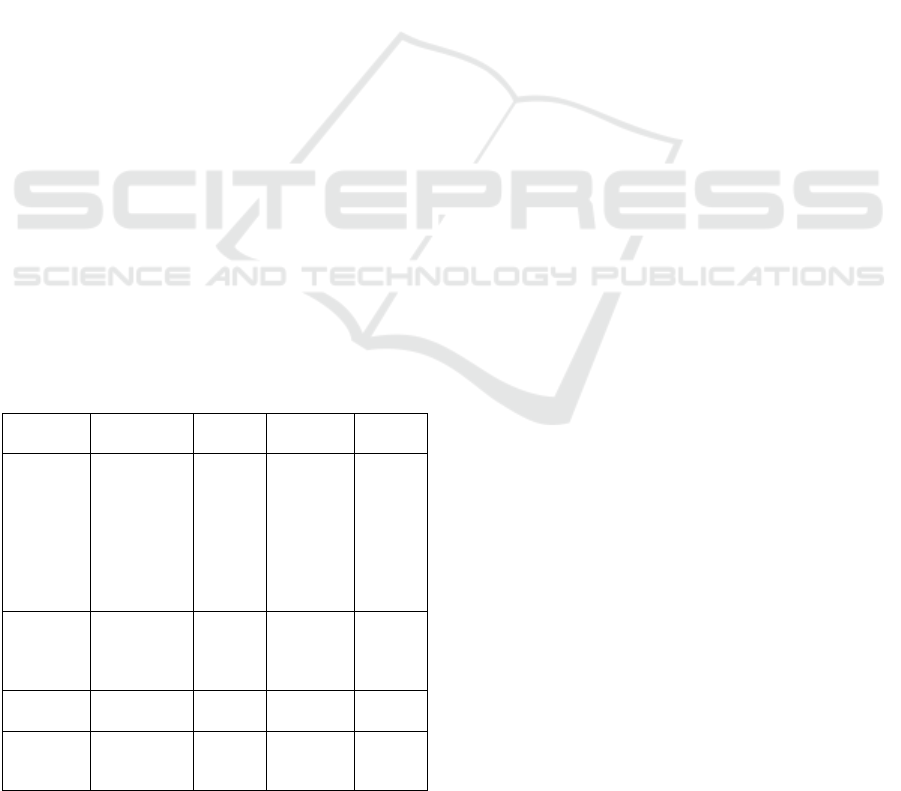

Table II summarizes these models with their own

characteristics:

Table 2: Prediction model’s characteristics.

Source Method

Performance

Environ

ment

Feature Set accuracy

Galeshchu

k and

Mukherjee

(2017)

CNN - Exchange

rate

92.62%

(for

USD/JP

Y

83.72%

for

GBP/US

D)

Ravi et al.

(2017)

Hybrid

(Chaos,

MLP,

MOPSO)

MATLA

B/Gretl

Exchange

rates

99.91%

Kim et al.

(2015)

DCNN - Bank

marketing

76.70%

Lee et al.

(2017)

FFNN+SVR

+RBM

Boltzma

nn

machine

Revenues

organizatio

ns

90%

According to several papers, only a hybrid paradigm

might perform better. These approaches bring

together effectiveness and performance, to get

promising results.

6.2 Trading

Algorithmic trading (or Algo-trading) is defined as

the use of algorithmic models to make buy-sell

decisions. These decisions might be based on simple

rules, efficient processes, mathematical models or

complicated techniques, as in machine/deep learning.

Karaoglu and Arpaci (2017) present a technique

for detecting trading signals based on a dynamic

threshold selection, by combining many different

rules-based systems and augmenting them using the

Recurrent Neural Network algorithm.

Recurrent Neural Networks (RNNs) learn the

connection weights of subsystems with arbitrary

input sequences, making them ideal for time series

data. With the purpose of detecting probable

excessive movements in a noisy stream of time series

data, the suggested model is based on Piecewise

Linear Representation and Recurrent Neural

Network. To discover irregularities, they employ an

exponential smoothing approach. The tests revealed

that this model delivers successful trading data

results, but its scalability needs to be improved.

S. Wang et al. (2017), present a unique State

Frequency Memory (SFM) recurrent network, to

record multi-frequency trading patterns from

historical market data and create long and short-term

predictions over time. Stock prices are determined by,

short and/or long-term commercial and trading

activity that represent various trading patterns and

frequency. These patterns, are frequently elusive,

because they are influenced by a variety of uncertain

political economic elements in the real world, such as

corporate performance, government regulations, and

even breaking news that spreads across markets.

Deng et al. (2017), employed Fuzzy Deep Direct

Reinforcement Learning (FDDR) to predict stock

prices and provide trading signals. They present a

recurrent deep neural network (NN) for the modeling

and trading of real-time financial signals. The

proposed model, interacts with deep representations

and makes trading decisions in an unknown

environment to acquire the ultimate rewards.

Table III summarizes these models with their own

characteristics:

BML 2021 - INTERNATIONAL CONFERENCE ON BIG DATA, MODELLING AND MACHINE LEARNING (BML’21)

56

Table 3: Algo-trading model’s characteristics.

Source Method

Performance

Environme

n

t

Feature

Se

t

accurac

y

Karaoglu

and

Arpaci

(2017)

LSTM, PLR,

RNN

Big

Data/SPA

RK

Stock

Exchange

98.4%

Zhang et

al.

(2017)

SFM recurrent

network

- Stock

Price

88.9%

Deng et

al.

(2017)

RL + Fuzzy

Deep Direct

Reinforcemen

t Learning

(FDDR),DML

P

Keras Price

Data

97%

The majority of Algo-trading research focused on

predicting stock or index prices. Meanwhile, LSTM

was the most used DL model.

7 CONCLUSION

Finance has long been one of the most researched

domains for deep learning.

Algorithmic trading, Stock market forecasting,

portfolio allocation, credit risk assessment, asset

pricing, and the derivatives market are among the

areas where deep learning researchers have been

working on developing models, that can provide real-

time working solutions for the financial industry.

Indeed, unsupervised methods and in-depth

learning are essential tools for analyzing financial

news. In our study, we described different techniques

for extracting useful information. We have presented

tools that perform feature extraction from a corpus.

And as a synthesis of this study, we found that using

a hybrid approach that brings together the

effectiveness of several methods will get promising

results. In our future paper, it is relevant to propose a

new framework applied to real problems in text

analysis in finance.

This approach will therefore be implemented and

tested in practice on a case study, to present the

experimental strengths.

REFERENCES

Akbik, A., Blythe, D., & Vollgraf, R. (2018). Contextual

string embeddings for sequence labeling. 1638‑1649.

https://aclanthology.org/C18-1139

Ambrus, A., & Elliott, M. (2020). Investments in social ties,

risk sharing, and inequality. The Review of Economic

Studies, 88(4), 1624–1664.

https://doi.org/10.1093/restud/rdaa073

Ambrus, A., Gao, W., & Milan, P. (2018). Informal Risk

Sharing with Local Information. SSRN Electronic

Journal. Published.

https://doi.org/10.2139/ssrn.3220524

Asadi Kakhki, S. S., Kavaklioglu, C., & Bener, A. (2018).

Topic Detection and Document Similarity on Financial

News. Advances in Artificial Intelligence, 322–328.

https://doi.org/10.1007/978-3-319-89656-4_34

Azmi Shabestari, M., Moffitt, K., & Sarath, B. (2019). Did

the banking sector foresee the financial crisis? Evidence

from risk factor disclosures. Review of Quantitative

Finance and Accounting, 55(2), 647–669.

https://doi.org/10.1007/s11156-019-00855-y

Bank of Canada,. (2015). Bank of Canada,.

https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=

1010013901

Billio, M., Getmansky, M., Lo, A. W., & Pelizzon, L.

(2012). Econometric measures of connectedness and

systemic risk in the finance and insurance sectors.

Journal of Financial Economics, 104(3), 535–559.

https://doi.org/10.1016/j.jfineco.2011.12.010

Creel, J., Hubert, P., & Labondance, F. (2015). Financial

stability and economic performance. Economic

Modelling, 48, 25–40.

https://doi.org/10.1016/j.econmod.2014.10.025

Das, S. R., & Chen, M. Y. (2007). Yahoo! for Amazon:

Sentiment Extraction from Small Talk on the Web.

Management Science, 53(9), 1375–1388.

https://doi.org/10.1287/mnsc.1070.0704

Das, S. R., & Sisk, J. (2005). Financial Communities. The

Journal of Portfolio Management, 31(4), 112–123.

https://doi.org/10.3905/jpm.2005.592103

Data Catalog | Data Catalog. (2015). World Bank.

https://datacatalog.worldbank.org

data.europa.eu. (2015). Europa Data.

https://data.europa.eu/data/datasets?locale=en

David M Blei, Andrew Y Ng, & Michael I Jordan. (2003).

Latent dirichlet allocation. the Journal of machine

Learning research, 3, 993‑1022.

Deng, Y., Bao, F., Kong, Y., Ren, Z., & Dai, Q. (2017).

Deep Direct Reinforcement Learning for Financial

Signal Representation and Trading. IEEE Transactions

on Neural Networks and Learning Systems, 28(3), 653–

664. https://doi.org/10.1109/tnnls.2016.2522401

Diebold, F. X., & Yilmaz, K. (2015). Financial and

Macroeconomic Connectedness: A Network Approach

to Measurement and Monitoring (Illustrated ed.).

Oxford University Press.

Ding, Y., Yu, C., & Jiang, J. (2017). A Neural Network

Model for Semi-supervised Review Aspect

Identification. Advances in Knowledge Discovery and

Data Mining, 668–680. https://doi.org/10.1007/978-3-

319-57529-2_52

Doran, J. S., Peterson, D. R., & Price, S. M. (2010).

Earnings Conference Call Content and Stock Price: The

Case of REITs. The Journal of Real Estate Finance and

Economics, 45(2), 402–434.

https://doi.org/10.1007/s11146-010-9266-z

Text Analysis in Finance: A Survey

57

el MENDILI, S. (2020). Towards a Reference Big Data

architecture for sustainable smart cities. International

Journal of Advanced Trends in Computer Science and

Engineering, 9(1), 820–827.

https://doi.org/10.30534/ijatcse/2020/118912020

Engelberg, J. (2008). Costly Information Processing:

Evidence from Earnings Announcements. SSRN

Electronic Journal. Published.

https://doi.org/10.2139/ssrn.1107998

Federal Reserve Economic Data | FRED | St. Louis Fed.

(2015). Federal Reserve. https://fred.stlouisfed.org

Ferris, S. P., Hao, G. Q., & Liao, S. M. Y. (2012). The

Effect of Issuer Conservatism on IPO Pricing and

Performance*. Review of Finance, 17(3), 993–1027.

https://doi.org/10.1093/rof/rfs018

Feuerriegel, S., Ratku, A., & Neumann, D. (2016). Analysis

of How Underlying Topics in Financial News Affect

Stock Prices Using Latent Dirichlet Allocation. 2016

49th Hawaii International Conference on System

Sciences (HICSS). Published.

https://doi.org/10.1109/hicss.2016.137

Financial performance data. (2015). FP DATA.

http://www.ic.gc.ca/eic/site/pp-pp.nsf/eng/home

Galeshchuk, S., & Mukherjee, S. (2017). Deep networks for

predicting direction of change in foreign exchange

rates. Intelligent Systems in Accounting, Finance and

Management, 24(4), 100–110.

https://doi.org/10.1002/isaf.1404

Ghiassi, M., Skinner, J., & Zimbra, D. (2013). Twitter

brand sentiment analysis: A hybrid system using n-

gram analysis and dynamic artificial neural network.

Expert Systems with Applications, 40(16), 6266–6282.

https://doi.org/10.1016/j.eswa.2013.05.057

Gilman, R. C. (1968). The General Inquirer: A Computer

Approach to Content Analysis.Philip J. Stone , Dexter

C. Dunphy , Marshall S. Smith , Daniel M. Ogilvie.

American Journal of Sociology, 73(5), 634–635.

https://doi.org/10.1086/224539

Harris, Z. S. (1954). Distributional Structure. WORD,

10(2–3), 146–162.

https://doi.org/10.1080/00437956.1954.11659520

Hautsch, N., Schaumburg, J., & Schienle, M. (2014).

Financial Network Systemic Risk Contributions.

Review of Finance, 19(2), 685–738.

https://doi.org/10.1093/rof/rfu010

Henry, E., & Leone, A. J. (2009). Measuring Qualitative

Information in Capital Markets Research. SSRN

Electronic Journal. Published.

https://doi.org/10.2139/ssrn.1470807

IMF Data. (2015). IMF. https://www.imf.org/en/Data

Interest Rates. (2015). Bank of Canada.

https://www.bankofcanada.ca/rates/interest-rates/

Jangid, H., Singhal, S., Shah, R. R., & Zimmermann, R.

(2018). Aspect-Based Financial Sentiment Analysis

using Deep Learning. Companion of the The Web

Conference 2018 on The Web Conference 2018 -

WWW ’18. Published.

https://doi.org/10.1145/3184558.3191827

Karaoglu, S., & Arpaci, U. (2017). A Deep Learning

Approach for Optimization of Systematic Signal

Detection in Financial Trading Systems with Big Data.

International Journal of Intelligent Systems and

Applications in Engineering, Special Issue(Special

Issue), 31–36.

https://doi.org/10.18201/ijisae.2017specialissue31421

Kearney, C., & Liu, S. (2013). Textual Sentiment Analysis

in Finance: A Survey of Methods and Models. SSRN

Electronic Journal. Published.

https://doi.org/10.2139/ssrn.2213801

Kim, K. H., Lee, C. S., Jo, S. M., & Cho, S. B. (2015).

Predicting the success of bank telemarketing using deep

convolutional neural network. 2015 7th International

Conference of Soft Computing and Pattern Recognition

(SoCPaR). Published.

https://doi.org/10.1109/socpar.2015.7492828

Landauer, T. K., & Dumais, S. T. (1997). A solution to

Plato’s problem: The latent semantic analysis theory of

acquisition, induction, and representation of

knowledge. Psychological Review, 104(2), 211–240.

https://doi.org/10.1037/0033-295x.104.2.211

Lee, J., Jang, D., & Park, S. (2017). Deep Learning-Based

Corporate Performance Prediction Model Considering

Technical Capability. Sustainability, 9(6), 899.

https://doi.org/10.3390/su9060899

Li, N., Liang, X., Li, X., Wang, C., & Wu, D. D. (2009).

Network Environment and Financial Risk Using

Machine Learning and Sentiment Analysis. Human and

Ecological Risk Assessment: An International Journal,

15(2), 227–252.

https://doi.org/10.1080/10807030902761056

LOUGHRAN, T., & MCDONALD, B. (2011). When Is a

Liability Not a Liability? Textual Analysis,

Dictionaries, and 10-Ks. The Journal of Finance, 66(1),

35–65. https://doi.org/10.1111/j.1540-

6261.2010.01625.x

Mbadi, S. (2018). Predicting Stock Market Movement

Using an Enhanced Naïve Bayes Model for Sentiment

Analysis Classification

Mikolov, T., Chen, K., Corrado, G., & Dean, J. (2013).

Efficient estimation of word representations in vector

space. arXiv:1301.3781 [cs].

http://arxiv.org/abs/1301.3781

Mikolov, T., Sutskever, I., Chen, K., Corrado, G., & Dean,

J. (2013). Distributed representations of words and

phrases and their compositionality. arXiv:1310.4546

[cs, stat]. http://arxiv.org/abs/1310.4546

Mitra, G., & Mitra, L. (2011). The Handbook of News

Analytics in Finance (1st ed.). Wiley.

Natural language processing tested in the investment

process through new partnership | J.P. Morgan. (2018).

J.P. Morgan. https://www.jpmorgan.com/news/natural-

language-processing-tested-in-the-investment-process-

through-new-partnership?source=cib_di_jp_mal0418

Ozik, G., & Sadka, R. (2012). Media and Investment

Management. SSRN Electronic Journal. Published.

https://doi.org/10.2139/ssrn.1633705

Peters, M., Neumann, M., Iyyer, M., Gardner, M., Clark,

C., Lee, K., & Zettlemoyer, L. (2018). Deep

Contextualized Word Representations. Proceedings of

the 2018 Conference of the North American Chapter of

BML 2021 - INTERNATIONAL CONFERENCE ON BIG DATA, MODELLING AND MACHINE LEARNING (BML’21)

58

the Association for Computational Linguistics: Human

Language Technologies, Volume 1 (Long Papers).

Published. https://doi.org/10.18653/v1/n18-1202

Quandl. (2015). Quandl. https://www.quandl.com/

Ravi, V., Pradeepkumar, D., & Deb, K. (2017). Financial

time series prediction using hybrids of chaos theory,

multi-layer perceptron and multi-objective

evolutionary algorithms. Swarm and Evolutionary

Computation, 36, 136–149.

https://doi.org/10.1016/j.swevo.2017.05.003

Sahlgren, M. (2006). The Word-Space Model : Using

distributional analysis to represent syntagmatic and

paradigmatic relations between words in high-

dimensional vector spaces.

Schweitzer, F., Fagiolo, G., Sornette, D., Vega-Redondo,

F., Vespignani, A., & White, D. R. (2009). Economic

Networks: The New Challenges. Science, 325(5939),

422–425. https://doi.org/10.1126/science.1173644

SEC.gov | EDGAR - Search and Access. (2019, December

16). EDGAR. https://www.sec.gov/edgar/search-and-

access

SEC.gov | Financial Statement Data Sets. (2009, January 1).

FS Data Set. https://www.sec.gov/dera/data/financial-

statement-data-sets.html

SEDAR. (2015). SEDAR.

https://www.sedar.com/search/search_form_pc_en.ht

m

Shihavuddin, A., Mir Nahidul Ambia, Mir Mohammad

Nazmul Arefin, Mokarrom Hossain, & Adnan Anwar.

(2010). Prediction of stock price analyzing the online

financial news using Naive Bayes classifier and local

economic trends. 2010 3rd International Conference on

Advanced Computer Theory and

Engineering(ICACTE). Published.

https://doi.org/10.1109/icacte.2010.5579624

TETLOCK, P. C. (2007). Giving Content to Investor

Sentiment: The Role of Media in the Stock Market. The

Journal of Finance, 62(3), 1139–1168.

https://doi.org/10.1111/j.1540-6261.2007.01232.x

TETLOCK, P. C., SAAR-TSECHANSKY, M., &

MACSKASSY, S. (2008). More Than Words:

Quantifying Language to Measure Firms’

Fundamentals. The Journal of Finance, 63(3), 1437–

1467. https://doi.org/10.1111/j.1540-

6261.2008.01362.x

Turney, P. D., & Pantel, P. (2010). From Frequency to

Meaning: Vector Space Models of Semantics. Journal

of Artificial Intelligence Research, 37, 141–188.

https://doi.org/10.1613/jair.2934

Vargas, M. R., de Lima, B. S. L. P., & Evsukoff, A. G.

(2017). Deep learning for stock market prediction from

financial news articles. 2017 IEEE International

Conference on Computational Intelligence and Virtual

Environments for Measurement Systems and

Applications (CIVEMSA). Published.

https://doi.org/10.1109/civemsa.2017.7995302

Wayback Machine. (2002). Rhetorica.Net.

https://web.archive.org/web/*/rhetorica.net

Zhang, L., Aggarwal, C., & Qi, G. J. (2017). Stock Price

Prediction via Discovering Multi-Frequency Trading

Patterns. Proceedings of the 23rd ACM SIGKDD

International Conference on Knowledge Discovery and

Data Mining. Published.

https://doi.org/10.1145/3097983.3098117

Text Analysis in Finance: A Survey

59