The Role of Information Technology Capabilities in Improving

Cost-Effectivenesss and SME’s Performance

Bastian Elvin, Muchlish Munawar

Faculty of Economics and Business, Sultan Ageng Tirtaysasa University, Banten Province, Indonesia

Keywords: Information Capabilities Technology, Cost Effectiveness, SME's Performance, and Warp PLS.

Abstract: The purpose of this study is to empirically examine and analyze the role of information technology capabilities

in increasing the cost-effectiveness and business performance of SMEs. This study uses a sample of managers

or managers from Palm Sugar SMEs in Lebak Regency. The sampling method in the study used purposive

sampling. This study uses a path analysis tool with the WarpPLS version 5.0 program to test hypotheses. The

results showed that the role of information technology capabilities had a positive effect on increasing cost-

effectiveness and the ability of information technology could also improve SME's performance.

1 INTRODUCTION

Palm sugar has been an important source of

livelihood for farmers and is one of the core potentials

of the Lebak Regency. Palm Sugar Products are the

superior products of the Lebak District. Lebak

Regency is known as one of the biggest palm sugar-

producing regions in Indonesia. The palm sugar

industry in this district absorbs 5,406 workers through

2,982 micro and small business units, not counting

labor in its distribution channel. The annual

production capacity reaches 2,249.4 tons spread in 44

production centers. Problems that are often faced by

SMEs, in addition to marketing difficulties, are also

because the products they make are less competitive.

In addition, the competitiveness of their products is

indeed low, and the selling price is not competitive.

The presence of Information Technology (IT) is

changing the way in business by providing new

opportunities and challenges that are different from

conventional methods. IT is one of the main pillars of

the development of human civilization today that

must be able to provide added value to the wider

community (Saleh and Hadiyat, 2016). The issue that

then arises is the digital divide (IT) gap, especially in

remote areas, which are still very large. Therefore, it

becomes important and urgent to open isolation

access to information of people in remote areas;

provide a public information service center or

information access network to the countryside;

provide information needed by the community to

improve knowledge, economy, and standard of

living; facilitate community social groups so they can

develop creativity and showcase their products; as

well as providing a place for tenants to turn creative

ideas into innovative IT products in order to have

competitiveness, excellence, and value.

With information technology, a company's

activities can be carried out effectively and efficiently

in costs because with faster operational activities, and

greater profits will be obtained by the company.

Chriswan and Mahmudin (2008) stated that

information technology offers many opportunities to

reduce costs, increase efficiency, increase

effectiveness and revenues, and can improve cost

control. Sophisticated technology and information

can help companies to monitor the activities carried

out by their employees, so the company can obtain

information more quickly and accurately used in

decision making. If an error or deviation occurs, the

company can immediately take corrective actions so

that the effectiveness in the use of operational costs

can be identified quickly so that the company's goals

can be achieved (Salim Ridwan, 2014).

The relationship between information technology

and performance is of interest to academics and

practitioners. Several studies conducted by previous

researchers found a significant relationship between

information technology and performance. Kelley

(1994), Siegel and Griliches (1992) state that some of

the results of the study found a positive influence of

information technology on company performance at

the industry level

488

Elvin, B. and Munawar, M.

The Role of Information Technology Capabilities in Improving Cost-Effectivenesss and SME’s Performance.

DOI: 10.5220/0009966604880494

In Proceedings of the International Conference of Business, Economy, Entrepreneurship and Management (ICBEEM 2019), pages 488-494

ISBN: 978-989-758-471-8

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Implementation of Information Technology can

help reduce costs and can convey detailed

information about products and special prices

provided to consumers online and also facilitate the

transaction process without having to come to the

store directly and can get maximum results.

One function of the utilization of Information

Technology is material efficiency (cost) and non-

material (energy and time). In terms of costs,

companies can reduce costs by utilizing the telephone

and internet as a medium of offer because it is cheaper

than traditional. On the other hand, cost efficiency

can occur due to a reduction in manpower in certain

positions and primarily to improve performance.

2 THEORITICAL FRAMEWORK

AND HYPOTHESIS

DEVELOPMENT

2.1 Information Technology Capability

and Cost Effectiveness

Chriswan and Mahmudin (2008) stated that

information technology offers many opportunities to

reduce costs, increase efficiency, increase

effectiveness and revenues, and can improve cost

control. Sophisticated technology and information

can help companies to monitor the activities carried

out by their employees, so the company can obtain

information more quickly and accurately used in

decision making. If a mistake or deviation occurs, the

company can immediately take corrective actions so

that the effectiveness in the use of operational costs

can be identified quickly so that the company's goals

can be achieved. Previous research that supports this

research is a study conducted by Salim Ridwan

(2014) and Ilker Calayoglu & Murat Azaltun (2013),

which suggests that information technology has a

significant effect on the cost-effectiveness of an

organization. Therefore, the following hypotheses are

proposed:

Hypothesis 1: There is a positive relationship

between Information Technology Capabilities and

cost-effectiveness.

2.2 Information Technology Capability

and SME’s Performance

Diewert and Smith (1994), Hitt and Brynjoltsson

(1995), Dewan and Min (1997), Devaraj and Kohli

(2003) indicate that there is a positive relationship

between technology and company performance.

Devaraj and Kohli (2003) state that there are some

studies that do not find a significant relationship

between information technology and performance.

Baily (1986), Roach (1987), Morrison and Berndt

(1991), Devaraj and Kohli (2003) found a negative

relationship between information technology

relatedness variables that are associated with

company performance. In addition, Berndt and

Morrison (1995) and Kohli (1999) find that there is

no significant relationship between investing in

information technology and performance. The above

findings are not consistent with previous studies

conducted by Kelley (1994), Siegel and Griliches

(1992), Diewert and Smith (1994), Hitt and

Brynjoltsson (1995), Dewan and Min (1997); Devaraj

and Kohli (2003). Research conducted by Nengah,

(2005) also found that information technology

contributes a positive and insignificant value to

business process performance and competitive

dynamics. The regulation and management of

information technology in companies with integrated

business units have important implications for the

company's ability to utilize cross-unit synergies

(Brown and Magill 1994, 1998; Sambamurthy and

Zmud 1999; Weil and Broadbent 1998; Weill and

Ross 2004). The concept of cross-business synergy is

central to the performance of companies integrated

business units with a diverse business portfolio

(Goold and Luchs, 1993; Tanriverdi and

Venkatraman, 2004).

Hypothesis 2: There is a positive relationship

between Information Technology Capabilities and

SME’s performance

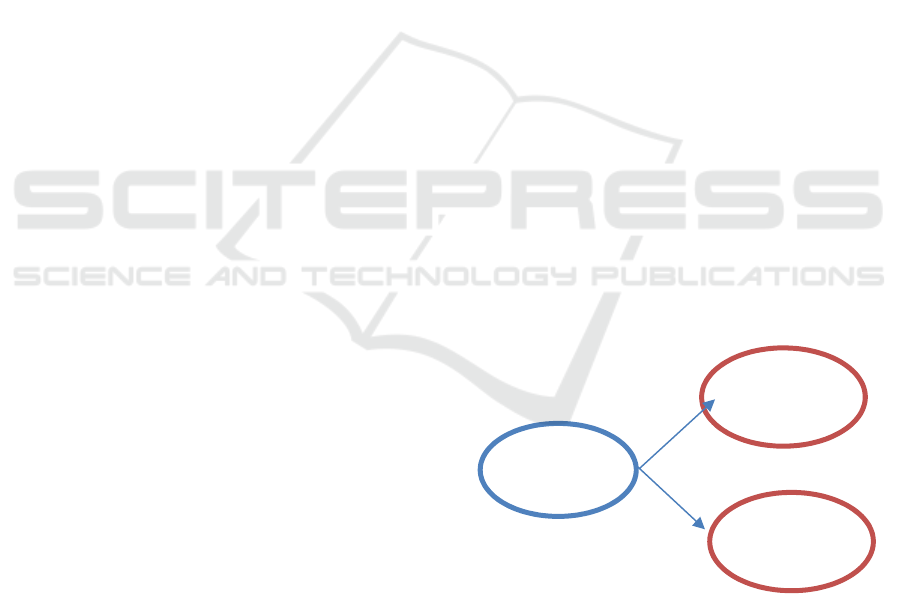

Figure 1. Theoretical Model

3 METHODOLOGY

This type of research is explanatory research. The

quantitative method in this study was used to

empirically examine the role of technology

Capability Inf

Technology

Cost-

Effectivenes

SME’s

Performance

H1

H2

The Role of Information Technology Capabilities in Improving Cost-Effectivenesss and SME’s Performance

489

capabilities on SME's cost efficiency and

performance. The sample in this study is a manager

of SME’s at the Palm Sugar SME’s in Lebak

Regency, Banten province. Criteria for selection of

the sample in the study is aimed at the sample

(purposive sampling). To test the models and

hypotheses used analysis of Structural Equation

Modeling (SEM). In testing the model using SEM

PLS (Partial Least Square).

In this study, data analysis using the Partial Least

Square (PLS) approach using WarpPLS software.

PLS is a structural equation model (SEM) based on

components or variances. According to Ghozali

(2016), PLS is an alternative approach that shifts from

a covariance-based SEM approach to variant-based.

Covariance-based SEM generally tests

causality/theory, while PLS is a more predictive

model. PLS is a powerful analysis method (Wold,

1985; Ghozali, 2016) because it is not based on many

assumptions. For example, the data must be normally

distributed; the sample does not have to be large.

Besides being able to be used to confirm theories,

PLS can also be used to explain the presence or

absence of relationships between latent variables.

PLS can simultaneously analyze constructs formed

with reflexive and formative indicators. This cannot

be done by SEM, which is based on covariance

because it will become an unidentified model.

4 RESULT AND DISCUSSION

4.1 Outer and Inner Model Testing

In testing the reliability value of a construct, the value

used for Cronbach's Alpha and Composite Reliability

is where both values are greater than 0.7 (> 0.7) for

confirmatory research and greater than 0.6 (> 0.6) for

exploratory research is still acceptable. (Hair et al.,

2010, 2011; Pirouz 2006; Ghozali 2016).

Furthermore, the average variances extracted (AVE)

value of the construct must be above 0.5 (> 0.5).

(Bagozzi and Baumgartner, 1994; Ghozali, 2016).

Based on the approach in the reliability test above,

the following are presented the values of Cronbach's

Alpha, Composite Reliability, Average variances

extracted from each construct of this study with

confirmatory factor analysis with WarpPLS 5.0.

Table 1: Score of Composite reliability coeffecients,

Cronbach alpha coefficients and Average variances

extracted

ITC CE PERF

Composite

reliability

coefficients

0.905 0.921 0.880

Cronbach

alpha

Coefficients

0.873 0.905 0.834

Average

Extracted

0.615 0.519 0.555

Table 1 shows that the composite reliability value

of the construct studied was above the recommended

threshold, where the composite reliability value was

greater than 0.6 (> 0.6), namely: ITC of 0.905, CE of

0.921, and PERF of 0.880.

Cronbach alpha coefficient value of each

construct is above the recommended threshold, where

the Cronbach alpha coefficient value is greater than

0.6 (> 0.6), namely: ITC of 0.873, CE of 0.905, and

PERF of 0.834.

Average variances extracted (AVE) value of each

construct is above the recommended threshold, where

the AVE value is greater than 0.5 (> 0.5), namely:

ITC of 0.615, CE of 0.519, and PERF of 0.555.

Based on the value of composite reliability,

Cronbach alpha coefficient and Average variances

extracted from the ITC, CE, and PERF constructs that

are above the recommended threshold, then all

constructs have met the composite reliability

requirements

4.2 Full Model Testing

The results of testing the full research model with

WarpPLS 5.0 are presented in Figure 2, Table 2 and

Table 3

Table 2: Model Fit dan Quality Indice Full Model

Average Path Coefficient (APC)= 0.833, P<0.001

Average R-Squared (ARS) = 0.698, P<0.001

Average adjusted R-Squared (AARS) = 0.696, P<0.001

Average full collinearity VIF (AAVIF)= 4.895,

acceptable if <= 5, ideally <= 3.3

Tenenhaus GoF (GoF) = 0.623, small >= 0.1, medium

>= 0.25, large >= 0.36

Based on the Model Fit and Quality Indice Full

Model output presented in Table 2, it is known that

the Average path coefficient (APC) has an index of

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

490

0.833 with a p-value <0.001, Average R-squared

(ARS) has an index of 0.698 with a p-value < 0.001

and Average adjusted R-squared (AARS) have an

index of 0.696. The p-value for APC, ARS, and

AARS that is recommended as a fit model is 5 0.05

(Ghozali and Latan, 2017; Kock, 2012). Thus it can

be concluded that this study is fit. This is also

supported by the value of Average full collinearity

VIF (AAVIF) = 4,895, less than the value of 5

(acceptable). Thus indicating that there is no

multicollinearity problem between indicators and

between exogenous variables. The predictive power

of the model described by GoF is 0.713, including the

large category because it is greater than 0.36.

Table 3 presents the structural model analysis

outputs about R-squared (R2), Adjusted R-squared

(Adj. R2), Full Collinearity VIF and Q-Squared (Q2).

R2 shows the percentage of endogenous construct

variance/criterion can be explained by the construct

hypothesized to influence it (exogenous / predictor)

(Sholihin and Ratmono, 2014). Adj. R2 is similar to

R2 but is used to avoid estimation bias in R2, because

the more predictor variables in the model, R2 will be

greater and continue to increase (Ghozali and Latan,

2016). Criteria for R2 and Adj. R2 ≤0.70, ≤0.45, and

≤0.25 show strong, moderate, and weak models.

Table 3 R-Squared, Adj R-Square and Full Collin VIF

ITC CE PERF

R-squared

0.562

Adjusted R-

squared

0.802

0.559

Full Collin VIF 4.973 4.962 3.360

Based on table 3, it can be seen that R-squared

(R2) and Adjusted R-squared (Adj. R2) of this

research model tend to be moderate because the

Barada is above 0.25%. Full Collinearity VIF is used

to check whether collinearity problems occur

vertically or laterally (Ghozali and Latan, 2017). The

criterion for a model that is free from vertical and

lateral multicollinearity problems is that the Full

Collinearity VIF value must be lower than 3.3.

However, values ≤5 are still acceptable (Ghozali and

Latan, 2017; Sholihin and Ratmono, 2014; Kock,

2012). Based on table 3, it can be seen that the model

used in this study is free from the problem of vertical

or lateral collinearity. Because all VIF Full

Collinearity values are less than 5.

After the structural model has been declared fit

and can be accepted by data quality testing, then

analysis and interpretation of the structural model will

be used to test the research hypothesis. Bootstrapping

method for research models with SEM Analysis with

WarpPLS 5.0 of each construct with the following

results: R-squared (R2), Adjusted R-squared (Adj.

R2), and Full Collinearity VIF.

Table 4 Path Coefficient, P-value and Effect Size Full

Model

Relationship

Estimate Effect

Size

P-Value Decision

ITC CE

0.897 0.804 (<0.001)*

H1 :

Accepted

ITCPERF

0.750 0.562 (<0.001)*

H2:

Accepted

The variation of certain exogenous variables to

endogenous variables is called effect size. Effect size

measures the contribution of variants from each

predictor in the R-Square coefficient model of a

particular endogenous variable. Effect sizes can be

grouped into three categories, namely weak (0.02),

medium (0.15), and large (0.35) (Sholihin and

Ratmono, 2014).

Based on table 4, it can be seen that the variable

Information Technology Capability (ITC) has the

biggest effect size on the Cost-Effectiveness (CE)

variable, which is 0.804. The effect size of the effect

of ITC on the PERF variable of 0.562 is also quite

large. Thus it can be concluded that Information

Technology Capability (ITC) has a greater role from

the perspective of Cost-effectiveness (EC) compared

to PERF.

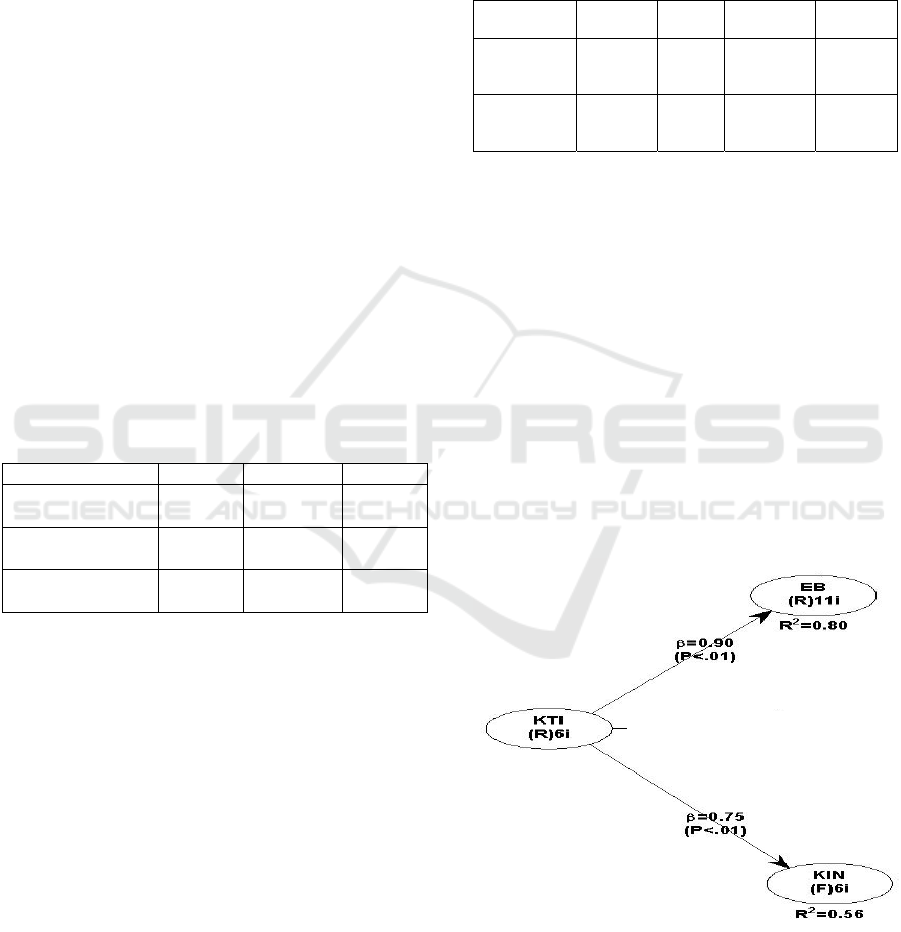

Figure 2 Output WarpPLS 5.0 Full Model

The Role of Information Technology Capabilities in Improving Cost-Effectivenesss and SME’s Performance

491

4.3 Hypothesis Testing

Hypothesis 1 states that Information Technology

Capability (ITC) has a significant positive effect on

Cost-effectiveness (CE). To prove this hypothesis, a

direct effect test was conducted with WarpPLS

version 5.0. Tests performed are model fit testing,

path coefficient analysis, and p-value. The test results

are presented in Figure 2; Table 2; Table 3 and Table

4. Based on table 2, it is known that the model fit

criteria have been met, where the APC, ARS, AARS

values are below 0.05, the AFVIF value <5, and the

GoF value are included in the large category that is

above 0.36. Table 4 presents the path coefficients

produced are 0.897 and significant with p values

<0.001 (α1%). Thus it can be concluded that

hypothesis 1 is accepted. This means that Information

Technology Capability (ITC) has a significant

positive effect on Cost-Effectiveness (CE) with a

coefficient of determination of 0.804 shown in table

3.

Hypothesis 2 states that Information Technology

Capability (ITC) has a significant positive effect on

Business Performance (PERF). To prove this

hypothesis, a direct effect test was conducted with

WarpPLS version 5.0. Tests performed are model fit

testing, path coefficient analysis, and p-value. The

test results are presented in Figure 2; Table 2; Table

3 and Table 4.

Based on table 2, it is known that the criteria for

model fit have been fulfilled, where the APC, ARS,

AARS values are below 0.05, AFVIF values <5, and

GoF values are included in the large category above

0.36. Table 4 presents the path coefficients produced

are 0.750 and significant with p values <0.001 (α1%).

Thus it can be concluded that hypothesis 2 is

accepted. This means that Information Technology

Capability (ITC) has a significant positive effect on

SME’s Performance (PERF) with a coefficient of

determination of 0.562 shown in table 3.

4.4 Summary of Hypothesis Testing

General conclusions in testing hypotheses to answer

research questions can be seen in table 5.

Table 5 Summary of Hypothesis Testing Results

Hypothesis

Hasil

Pengujian

Decision

Hypothesis 1 :

There is a positive

relationship between

Information

Technology

Significant

(+)

coefficient

0,804

score p<0,001

Accepted

Capabilities and cost-

effectiveness.

Hypothesis 2 :

There is a positive

relationship between

Information

Technology

Capabilities and

SME’s performance

Significant

(+)

coefficient

0,562

score p<0,001

Accepted

4.5 Discussion

This section will discuss research findings that have

been analyzed and tested in the previous section. The

discussion is based on the value of the results of

statistical testing with WarpPLS 5.0 software, which

is based on the building of theory and empirical

research referred to and developed in this study. The

discussion will be conducted based on the results of

data analysis and hypothesis testing proposed in this

study and the relationship with the findings from

previous studies

4.5.1 Information Technology Capability

(ITC) Has a Significant Positive Effect

on Cost-Effectiveness (CE)

Hypothesis 1 of this study states that Information

Technology Capability (ITC) has a positive effect on

Cost-Effectiveness (CE). The test results using

WarpPLS 5.0 show a path coefficient of 0.897 and a

p-value <0.01. Based on these figures, it is concluded

that hypothesis 1 can be accepted, meaning that

Information Technology Capability (ITC) has a

positive effect on Cost-Effectiveness (CE).

Chriswan and Mahmudin (2008) stated that

information technology offers many opportunities to

reduce costs, increase efficiency, increase

effectiveness and revenues, and can improve cost

control. Sophisticated technology and information

can help companies to monitor the activities carried

out by their employees, so the company can obtain

information more quickly and accurately used in

decision making. If a mistake or deviation occurs, the

company can immediately take corrective actions so

that the effectiveness in the use of operational costs

can be identified quickly so that the company's goals

can be achieved. Previous research supporting this

research was a study conducted by Salim Ridwan

(2014) and Ilker Calayoglu & Murat Azaltun (2013),

which suggested that information technology

significantly influences the effectiveness of cost

control in an organization.

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

492

Cost control must primarily be aligned with the

goals to be achieved by the company, one of the goals

to be achieved by the company is to obtain maximum

profit by issuing the lowest costs, therefore by

controlling the production costs, the company hopes

to get a large profit. A company in order to compete

in a market environment, the company is also

required to be able to create a good product

innovation, and the price is lower or at least the same

as the price offered by its competitors.

4.5.2 Information Technology Capability

(ITC) Has a Significant Positive Effect

on SME’s Performance (PERF)

Hypothesis 2 of this study states that Information

Technology Capability (KTI) has a positive effect on

Business Performance (KIN). The test results using

WarpPLS 5.0 show the path coefficient of 0.750 and

p-value <0.01. Based on these figures, it is concluded

that hypothesis 3 can be accepted, meaning that

Information Technology Capability (KTI) has a

positive effect on Business Performance (KIN).

This hypothesis is supported by previous

researchers finding a significant relationship between

information technology and performance. Kelley

(1994), Siegel, and Griliches (1992) state that some

of the results of the study found a positive effect of

information technology on company performance at

the industry level. Diewert and Smith (1994), Hitt and

Brynjoltsson (1995), Board and Min (1997), Devaraj

and Kohli (2003) indicate that there is a positive

relationship between technology and company

performance.

However, this research is not supported by

Devaraj and Kohli (2003), stating that there are some

studies that do not find a significant relationship

between information technology and performance.

Baily (1986), Roach (1987), Morrison and Berndt

(1991), Devaraj and Kohli (2003) find a negative

relationship between information technology

relatedness variables that are associated with firm

performance. In addition, Berndt and Morrison

(1995) and Kohli (1999) find that there is no

significant relationship between investing in

information technology and performance.

The above findings are not consistent with

previous studies conducted by Kelley (1994), Siegel

and Griliches (1992), Diewert and Smith (1994), Hitt

and Brynjoltsson (1995), Council and Min (1997);

Devaraj and Kohli (2003). Research conducted by

Nengah (2005) also found that information

technology contributes a positive and insignificant

value to business process performance and

competitive dynamics.

5 CONCLUSION

With information technology, a company's activities

can be carried out effectively and efficiently in costs

because with faster operational activities, and greater

profits will be obtained by the company. Chriswan

and Mahmudin (2008) stated that information

technology offers many opportunities to reduce costs,

increase efficiency, increase effectiveness and

revenues, and can improve cost control.

This study found a relationship between

Information Technology Capability and SME's

Performance. This hypothesis was supported by

previous researchers finding a significant relationship

between information technology and performance.

Kelley (1994), Siegel, and Griliches (1992) state that

some of the results of the study found a positive effect

of information technology on company performance

at the industry level.

REFERENCES

Arifin, Ikhsan Nurul. 2016. Analisis Target Costing Dalam

Upaya Pengurangan

Biaya Produksi Untuk Peningkatan Laba Kotor Pada

Mandala Bakery. Jurnal Berkala Ilmiah Efisiensi. Vol

6. No.3.

AD Ramdansyah dan HER Taufik, 2017. Adoption Model

of E-Commerce from SMEs Perspective in

Developing Country Evidence – Case Study for

Indonesia, European Research Studies Journal Volume

XX, Issue 4Β, 2017.

Alexandru-Emil Popa, 2014. The Financial Factors that

Influence the Profitability of SMEs, International

Journal of Academic Research in Economics and

Management Sciences., Vol. 3, No. 4.

BC Shia, AD Ramdansyah, S Wang, 2014. Forecasting E-

Commerce Trend in Indonesia, Proceedings of the 19

th

International Conference on Information Quality

(ICIQ).

BC Shia, M Chen, AD Ramdansyah, S Wang, 2015.

Comparison of Decision Making in Adopting E-

Commerce between Indonesia and Chinese Taipei

(Case Study in Jakarta and Taipei City), American

Journal of Industrial and Business Management, 2015,

5, 748-768.

BC Shia, M Chen, AD Ramdansyah, S Wang, 2016.

Measuring Customer Satisfaction toward

Localization Website by WebQual and Importance

Performance Analysis (Case Study on AliexPress Site

The Role of Information Technology Capabilities in Improving Cost-Effectivenesss and SME’s Performance

493

in Indonesia), American Journal of Industrial and

Business Management, 2016, 6, 117-128.

Davis, F.D, 1989. Perceived Usefulness, Perceived Ease

of Use, and User Acceptance of Information

Technology. MIS Quarterly,13, 319-340.

Fabrizio Gilardi, 2010. Who Learns from What in Policy

Diffusion Processes.American Journal of Political

Science 54(3):650– 666.

Hendrickson, A. R.; Massey, P. D.; Cronan, T. P. 1993.

On the test-retest reliability of perceived usefulness

and perceived ease of use scales. MIS Quarterly 17:

227-230

James N. K. Kinuthia and David M. Akinnusi, 2014.

The magnitude of barriers facing e-commerce

businesses in Kenya, Journal of Internet and

Information system, Vol. 4(1), pp.12-27.

Jordana, J. 2011. The Global Diffusion of Regulatory

Agencies: Channels of Transfer andStages of

Diffusion. Comparative Political Studies 44 (10):

1343–1369.

Jumayah Abdulaziz Mohammed, Mahmoud Khalid

Almsafir and Ahmad Salih Mheidi Alnaser, 2013.

The Factors That Affects E-Commerce Adoption in

Small and Medium Enterprise: A Review, Australian

Journal of Basic and Applied Sciences, 7(10): 406-

412 ISSN 1991-8178.

Maryama,Siti. 2016. Peneraparan E-Commerce Dalam

Peningkatan Daya Saing. Jurnal Liquidity. Vol.2 No.1.

Muhammed Kursad Ozlen, Ensar Mekic and Ena

Kumbara, 2014. Perceived Benefits of E- Commerce

among Manufacturing and Merchandising Companies,

International Journal of Academic Research in

Economics and Management Sciences, Vol. 3, No. 2,

ISSN: 2226-3624

N Ummi, I Dwisvimiar, PF Ferdinant, AI Saeful, MM

Utami; 2016. Pengembangan Proses Produksi Gula

aren Semut di Kabupaten Lebak Melalui Modernisasi

dan Implementasi Teknologi Spray Drier menuju

GMP dan SII 2043-87, Publikasi Kegiatan Hi-Link

dalam Seminar Internasinal ICBM.

Ondrej Zizlavsky, 2014. The Balanced Scorecard:

Innovative Performance Measurement and

Management Control System, Journal of Technology

Management & Innovation, Volume 9, Issue 3.

Palupi, Ayu Tiara. 2016. Analisi Biaya Standar Untuk

Mendukung Efisiensi Biaya Prodsuksi Perusahaan.

Jurnal Administrasi Bisnis (JAB)|Vol. 36 No. 1.

Puryati, Dwi. 2017. Biaya Produksi, E-Commerce dan

Penjualan Produk Pada Sentra Kaos Bandung. Jurnal

Online Insan Akuntan, Vol.2, No.2 Desember 2017,

217 - 228

Rogers, Everett M. 1983. Diffusion of innovations (3rd

ed.). New York: Free Press of Glencoe. ISBN

9780029266502.

Saleh dan Hadiyat (2016). Penggunaan Teknologi

Informasi di Kalangan Pelaku Usaha Mikro Kecil

Menengah di Daerah Perbatasan (Studi di Kabupaten

Belu Provinsi Nusa Tenggara Timur). Jurnal

Pekommas, Vol. 1 No. 2, Oktober 2016: 141 - 152

Segars, A. H.; Grover, V., 1993. Re-examining

perceived ease of use and usefulness: A confirmatory

factor analysis. MIS Quarterly 17: 517–525.

Venkatesh, V.; Morris, M. G.; Davis, G. B.; Davis, F. D.,

2003. User acceptance of information technology:

Toward a unified view. MIS Quarterly 27 (3):

425–478.

Wasfi Alrawabdeh, 2014. Environmental Factors

Affecting Mobile Commerce Adoption - An

Exploratory Study on the Telecommunication

Firms in Jordan, International Journal of Business

and Social Science, Vol. 5, No. 8

ICBEEM 2019 - International Conference on Business, Economy, Entrepreneurship and Management

494