The Influence of Indonesian Legislative Assembly

Knowledge about Budget towards APBD Supervision

with Public Accountability and Organization

Commitment Moderating Variables: Empirical Study on

Legislative Assembly in Bengkulu Province

Nila Aprila, Fenny Marietza, Madani Hatta, and Ripi Martalia

Faculty of Economy and Business, University of Bengkulu, Bengkulu, Indonesia

Abstract. This research aims to examine the influence of legislative assembly

knowledge about budget towards APBD supervision with public accountability

and organization commitment moderating variables. The data collection uses

primary data obtained from questionnaire distribution to the respondents, who

are legislative assembly in Bengkulu Province. The totals of sample used in this

research are 45 respondents. The data collection technique is done by using

survey through questionnaire give to legislative assembly of Bengkulu Province

by cencus method. The analysis used is Statistical Package for the Social

Sciences (SPSS). The result of hyphotheses test showed that the legislative

assembly knowledge about budget has positive effect towards APBD

supervision, and legislative assembly knowledge about budget has positive effect

towards APBD supervision moderated by public accountability, while

organization commitment do not moderate relationship between legislative

assembly knowledge about budget and APBD supervision.

Keywords: Legislative assembly knowledge about budget · APBD supervision

Public accountability · Organization commitment

1 Introduction

In this era of reformation, it appears many complicated problems. These problems have

encompassed many aspects, from economics, social, cultures, politics, and security

defense. After the falling of new order in this reformation era, the agenda that becomes

government main highlight was the problem of eradicating the cases of corruption. This

problem was one of main causes of the falling of new order government. Even in

election, the agenda of eradicating corruption was an issue that becomes main topic and

becomes worth selling for candidates to attract the masses (Halim and Kusufi, 2012).

Law No. 17 of 2014 about People’s Consulative Assembly, House of

Representatives, Regional Representative Board, and Regional House of

Representatives mentioned that Regional House of Representatives have three

functions, they are legislation function, budget function and supervision function. This

is in line with Law article 96 paragraph 2 No. 23 of 2014 about local government that

is about budget and supervision function. Commonly, budget was a statement on the

Aprila, N., Marietza, F., Hatta, M. and Martalia, R.

The Influence of Indonesian Legislative Assembly Knowledge about Budget towards APBD Supervision with Public Accountability and Organization Commitment Moderating Variables:

Empirical Study on Legislative Assembly in Bengkulu Province.

DOI: 10.5220/0009870200002900

In Proceedings of the 20th Malaysia Indonesia International Conference on Economics, Management and Accounting (MIICEMA 2019), pages 339-352

ISBN: 978-989-758-582-1; ISSN: 2655-9064

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

339

estimation of performance that will be achieved during certain period of time which is

stated in financial measurement. While budget in the public sector was a document

which describes financial condition of an organization which covers information about

income, expenditure, and activity (Mardiasmo, 2009).

Supervision refers to an action done by the party outside of executive (society and

Legislative Assembly) to join in supervising government performance. The function of

Legislative Assembly related to supervision in Law No. 23 of 2014 was the board

authority to implement the supervision towards implementation of local and other

regulations, implementation of the State Budget Revenue, supervising local

government performance and policy in implementing local development, and

international cooperation in the region. According to Wasistiono and Wiyoso (2009)

supervision was an activity implemented to achieve vision, mission, and organization

goals smoothly without any deviation or every effort and activity to know and assess

the real facts regarding the implementation of tasks and activities whether it is as

appropriate or not. The members of Legislative Assembly actively involve in arranging

local regulation (not only approving the draft prepared by government) and play an

important role in the process of regional budgeting.

There are some phenomena in Bengkulu Province. First, regarding to budget abuse

about package arrears of construction of public works roads worth of Rp 5.64 billion,

when it is followed up is worth of Rp 5.01 billion, so there is still some that did not

followed up yet worth of Rp 629.27 billion. The result of checking over the capital

expenditure realization of irrigation road and network showed that from 29 road work

packages which are tested in quotes, there are 27 road work packages were not

appropriate to specification set in contract worth of Rp 5.64 billion. This has an impact

on the equity of capital expenditures presentation of irrigation road and network which

are presented in Budget Realization Report (MROL News Agency Bengkulu, June 10

th

,

2016). Second, Priority of the Provisional Budget Ceiling was stopped because of slow

RAPBD-P legalization. Third, the corruption allegation of road construction budget in

Enggano Island in 2016 done by PT. Gamely Alam Sari. Loss of state estimated up to

Rp 7.1 billion was mentioned when plenary in Legislative Assembly of Bengkulu

Province (Harian Rakyat Bengkulu, Tuesday, June 13

th

, 2017). Fourth, on August 25

th

,

2016 Regional Government Budget (APBD) of Bengkulu Province worth of Rp 1.9

trillion substracted by Rp 197 billion by the Ministry of Finance. This withdrawing

funds are caused by budget stacking in regional cash that has not been spent

(Liputan6.com August 25

th

, 2016). In August 2017, the budget absorption was still

29.76 percent until the end of December 2017 the budget absorption increases up to

72.33 percent (Ministry of Home Affairs December 28

th

, 2017).

The cases which were occured also caused because of less board knowledge about

budget in doing supervision towards Regional Government Budget. Boards were not

only having enough knowledge about budget in supervising Regional Government

Budget, but Purnomo (2016) & Ramdhani (2014) stated that board’s knowledge also

moderated by public accountability and organization commitment. By the boards are

having knowledge about budget moderated by public accountability and organization

commitment, it can influence board’s performance in detecting abuse and violation of

budget which is occured during the implementation of Regional Government Budget.

Besides, it also helps a person in solving every problems occured as appropriate with

the position of the member of Legislative Assembly.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

340

This research refers to the research by Patiar et al (2014). The difference between

this research and the previous one is in the moderation variables, which are organization

commitment and public accountability, also, this research was done in Bengkulu

Province. The reasons of the researcher chooses those moderation variables were

because the interaction between board’s knowledge with organization commitment and

public accountability moderation variables are very important for the board to supervise

regional finance (APBD). Therefore, this research aimed to examine from those

moderation variables whether it has positive influence towards the interaction of

board’s knowledge in supervising regional finance (APBD). The reasons of this

research chooses the Secretariat Office of Legislative Assembly in Bengkulu Province

was because there are some phenomena and problems occured in Bengkulu Province

as have been stated.

The purpose of this research was to demonstrate empirically that Legislative

Assembly knowledge about budget has influence towards APBD supervision. To

demonstrate that Legislative Assembly knowledge about budget has influence towards

APBD supervision moderated by public accountability. And to demonstrate that

Legislative Assembly knowledge about budget has influence towards APBD

supervision moderated by organization commitment.

2 Literature Review

There are any agency relation when one of the parties (principal) hires other parties

(agent) to do a service and, in doing it, by delegating authority to make decision for the

agent (Anthony and Govindarajan, 2005). Ikhsan and Ishak (2005), stated that this

theory is based on economic theory. The agency problems at least involve two parties,

the principal who has authority to do an action, and the agent who receives principal

and authority delegation. In the context of making policy by the legislative, the

legislature is a principal who delegates authority to the agent such as government or

committee at legislative to make a new policy. This agency relation occurs after the

agent make a policy proposal and ends after the proposal is accepted or rejected (Halim

and Abdullah, 2006).

According to Assagaf (2015), the board’s knowledge about budget can be

interpreted as board’s knowledge on the mechanism of arranging the budget starting

from planning stage until accountability stage also board’s knowledge about regulations

that organize the regional financial management/APBD. One of knowledges which is

needed in supervising the regional financial supervision is the knowledge about budget.

If the board’s knowledge about budget is good, it is expected that the board’s member

can detect an abuse and a waste or a failure in implementing the budget. The high

board’s experience and knowledge will be helpful for a person in solving a problem

that he faced which is appropriate with the position of Legislative Assembly as people’s

representative.

Halim and Kusufi (2007) defined that the regional financial supervision is APBD

supervision, mainly if seen from the main component, so that APBD supervision can

be defined as all activities to ensure that in collecting the regional income, and

expendituring the regional outcome can run as accordance with the plans, rules and

purposes that have been set. Basically, the main purpose of supervision is to compare

The Influence of Indonesian Legislative Assembly Knowledge about Budget towards APBD Supervision with Public Accountability and

Organization Commitment Moderating Variables: Empirical Study on Legislative Assembly in Bengkulu Province

341

between what must be occured and what is occured in order to achieve a certain

purpose.

Public accountability is an obligation of trust holders party (agent) to give

responsibility, present, report, and express all activities that become their

responsibilities to the trust givers party (principal) that have right and authority to ask

for the responsibilities (Mardiasmo, 2009). According to Arianti (2017) public

accountabililty is defined as public responsibility principles which mean that the

process of budgeting from planning, arranging and implementing must be truly reported

and be accounted to Legislative Assembly and society. Accountability requires that the

decision maker behaves consistent with the received mandate.

According to Lubis (2010) organization commitment is a level of how far an

employee takes side on a particular organization and the purposes, and intended to keep

his membership in that organization. Organizational commitment is often defined

individually and related to the involvement of the person on the involved organization.

Employee’s commitment to the organization is one of attitudes that reflect feeling of

like or not of the employee towards the organization he works.

The agency relations between executive and legislative parties also occure in the

process of regional budgeting. The process of budgeting involves two parties, they are

executive and legislative. One of knowledges needed to do APBD supervision is the

knowledge about budget. By knowing about budget, the board’s member is expected to

be able to detect any abuse and waste or failure in implementing the budget. The high

board’s experience and knowledge will be very helpful for a person to solve problems

that he faced as appropriate with the position of Legislative Assembly as people’s

representative.

Widiyahningsih and Pujirahayu (2012), Utami and Syofyan (2013), Ramdhani

(2014), Rosita (2014), Zainal et al (2015), and Purnomo (2016) proved that board’s

knowledge about budget towards board’s supervision on regional finance (APBD)

indicated significant influence. From the above explanation, it can be formulated the

following hyphotheses:

H1: Legislative Assembly Knowledge about Budget has Positive Influence

towards APBD Supervision

2.1 Public Accountability and Legislative Assembly Supervision on

APBD

In the public sector organization, certainly the local government, the agency

relationship appears between the local government as agent and Legislative Assembly

as principal and public/citizen acts as principal who gives authority to the Legislative

Assembly (agent) to supervise the performance of local government. Ramdhani (2014)

stated that accountability becomes a logical consequence of the existing of relationship

between the agent and the principal. Board as a legislative member has to know and

understand the accountability guidance of government agencies in order to be able to

run the function in supervising the stages of arranging until APBD accountability

report. The failure in applying the operational standard of accountability procedures

causes time wasting, fund sources and other souces wasting, deviation of authority, and

decreased public trust towards government agencies.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

342

Sudiarta et al (2014), Purnomo (2016), and Arianti (2017) have proven that interaction

between board’s knowledge about budget has influence towards supervision over

APBD moderated by public accountability. The same thing also found in the research

by Ramdhani (2014), which stated that board’s knowledge about budget with public

accountability moderating variable has positive influence towards Legislative

Assembly supervision on APBD. Therefore, besides the knowledge about budget which

influences supervision done by the boards, the public accountability is expected to

increase the function of supervising. Then, it can be formulated the following

hyphotheses:

H2: Legislative Assembly Knowledge about Budget has Positive Influence

towards APBD Supervision Moderated by Public Accountability

2.2 Organization Commitment and Legislative Assembly Supervision

on APBD

Board’s psychology can be reflected from organization commitment that is really done

by the board as people’s representative. The board’s organization commitment is very

important remembering that the board’s member commonly came from politics (party).

It may strengthen or weaken the relation between board’s knowledge about budget and

APBD supervision. In the board’s performance context in Legislative Assembly,

organization commitment in the era of reformation and democration nowadays is

needed to be owned (Ramdhani, 2014).

Purnomo (2016) has proven that interaction between board’s knowledge about

budget has influence towards supervision over APBD moderated by organization

commitment. The same result also found in Ramdhani (2014), who stated that board’s

knowledge about budget moderated by organization commitment variable has positive

influence towards board’s supervision on APBD. From the above explanation, it can be

formulated the following hyphotheses:

H3: Legislative Assembly Knowledge about Budget has Positive Influence

towards APBD Supervision Moderated by Organization Commitment

3 Research Method

3.1 Data and Sample of the Research

This research was kind of research using quantitative approach that gives priority of

research towards data and empirical fact by using primary data sources (questionnaire).

The population in this research is Legislative Assembly of Bengkulu Province. The

sample in this research is all members of population. The method of taking this sample

is using cencus method. The reason of selecting the sample is by consideration that all

board’s members are joining in evaluating accountability report from local government

and approve the budget submitted by local government also supervise the

implementation of APBD. Besides, it is intended to obtain research findings which are

The Influence of Indonesian Legislative Assembly Knowledge about Budget towards APBD Supervision with Public Accountability and

Organization Commitment Moderating Variables: Empirical Study on Legislative Assembly in Bengkulu Province

343

more valid and unusual, so all members of Legislative Assembly became the

respondents.

3.2 Research Variables, Operational Definition and Variables

Measurement

1. Board’s Knowledge about Budget

According to Law No. 23 of 2014 about local government explained, Regional

Government Budget (APBD) is local annual financial planning assigned with local

regulation. According to Corynata (2007) the indicator used in measuring budget

knowledge variable is the perception of board’s member about budget

(RAPBD/APBD), procedures of implementing APBD, has understanding about

arranging the APBD based on related regulation, and detecting and identifying towards

wasting, failure or budget leak. This questionnaire referred to Corynata (2007) and

Robinson (2006). Variable measurement is using Likert-scale, with the scale from 1-5,

which means 1=Extremely Disagree, Disagree, Less Agree, Agree, and Extremely

Agree.

2. APBD Supervision

APBD supervision in this research is a supervision done by board’s member starting

from arranging the budget, legalizing the budget, implementing the budget and budget

accountability. According to Government Regulation No. 16 of 2010 about the Guide

of Arranging Legislative Assembly Regulation, the indicator of supervising local

financial is Legislative Assembly supervision which is done from arranging, legalizing,

implementing until reporting through assessment towards Report of Accountability

Description (LKPJ) of local head and follow up if there is any misappropriation in

accordance with the law regulation and Legislative Assembly order. This variable is

measured by using questionnaire referred to Corynata (2007) and Robinson (2006) then

developed and adapted according to researcher needs. Variable measurement is using

Likert-scale, with the scale from 1-5 which means 1=Extremely Disagree, Disagree,

Less Agree, Agree, and Extremely Agree.

3. Public Accountability

Public accountability is an obligation of trust holder party to provide accountability,

present, report, and express all activities that become his responsibility to the trust giver

party who has right and authority to ask for the accountability (Mardiasmo, 2009). This

questionnaire referred to Corynata (2007) and Widiyahningsih & Pujirahayu (2012).

Variable measurement is using Likert-scale, with the scale from 1-5 which means

1=Extremely Disagree, Disagree, Less Agree, Agree, and Extremely Agree.

4. Organization Commitment

Organization commitment is the nature of relationship between an individual with the

work organization, where the individual has self confidence towards the values of work

organization goals and there is a willingness to use his effort seriously for the sake of

work organization and has the strength desires to still become a part of that work

organization (Paramita and Andriyani, 2010). Organization commitment is measured

by using an indicator developed by Wirawan (2014) who explained three components

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

344

of organization commitment, they are Affective Commitment, Continuous

Commitment, and Normative Commitment. This questionnaire referred to the

questionnaire by Paramita and Andriyani (2010) and Wirawan (2014), then developed

and adapted according to researcher needs. Variable measurement is using Likert-scale,

with the scale from 1-5 which means 1=Extremely Disagree, Disagree, Less Agree,

Agree, and Extremely Agree.

3.3 Analysis Method

Data analysis in this research was done using the assist of SPSS (Statistical Package for

Social Sciences) program version 16.0 for Windows. The analysis method done in this

research was statistical descriptive test, data qualidity test, and classical assumption

test.

3.4 Hyphotheses Test

The research hyphotheses is examined by using simple linear regression (single

regression) and interaction test or MRA (Moderated Regression Analysis). The test

towards hyphotheses 1 uses simple linear regression model that is examined on the

equation 1, hyphotheses 2 and 3 use MRA (Moderated Regression Analysis), with the

following equation models:

Y= α + β

1

x

1

+e........ (H1)

Y= α + β

1

x

1

+ β

2

x

2

+ β

3

x

1

x

2

+e....(H2)

Y= α + β

1

x

1

+ β

4

x

3

+ β

5

x

1

x

3

+ e....(H3)

Information:

Y = Regional Financial (APBD) Supervision

α = Constants

β1- β5 = Regression Coeffisient

X

1

= Board’s Knowledge about Budget

X

2

= Accountability

X

3

= Organization Commitment

X

1

X

2

= Interaction between the board’s knowledge about budget and public

accountability

X

1

X

3

= Interaction between the board’s knowledge about budget and organization

commitment

E = Error

The Influence of Indonesian Legislative Assembly Knowledge about Budget towards APBD Supervision with Public Accountability and

Organization Commitment Moderating Variables: Empirical Study on Legislative Assembly in Bengkulu Province

345

4 Research Finding and Discussion

4.1 Descriptive Statistics

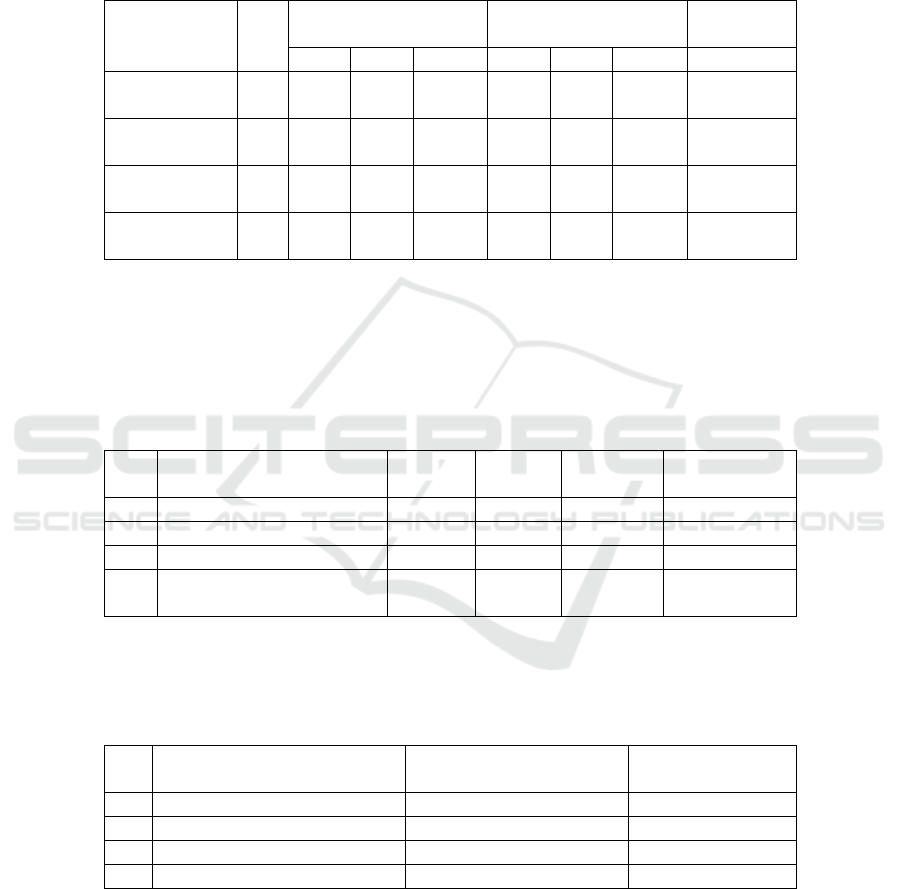

Table 1. Descriptive Statistics.

Variables n Theoretical Range Actual Range Std.

Deviation

Min Max Mean Min Max Mean

APBD

Supervision

36 12 60 36 44 60 52.11 3.875

Budget

Knowled

g

e

36 6 30 18 22 30 25.89 2.227

Public

Accountabilit

y

36 6 30 18 20 30 26.14 2.295

Organization

Commitmen

t

36 9 45 27 27 40 33.19 3.454

Source: Processed Primary Data, 2018

4.2 Result of Data Quality

4.2.1 Result of Validity Test

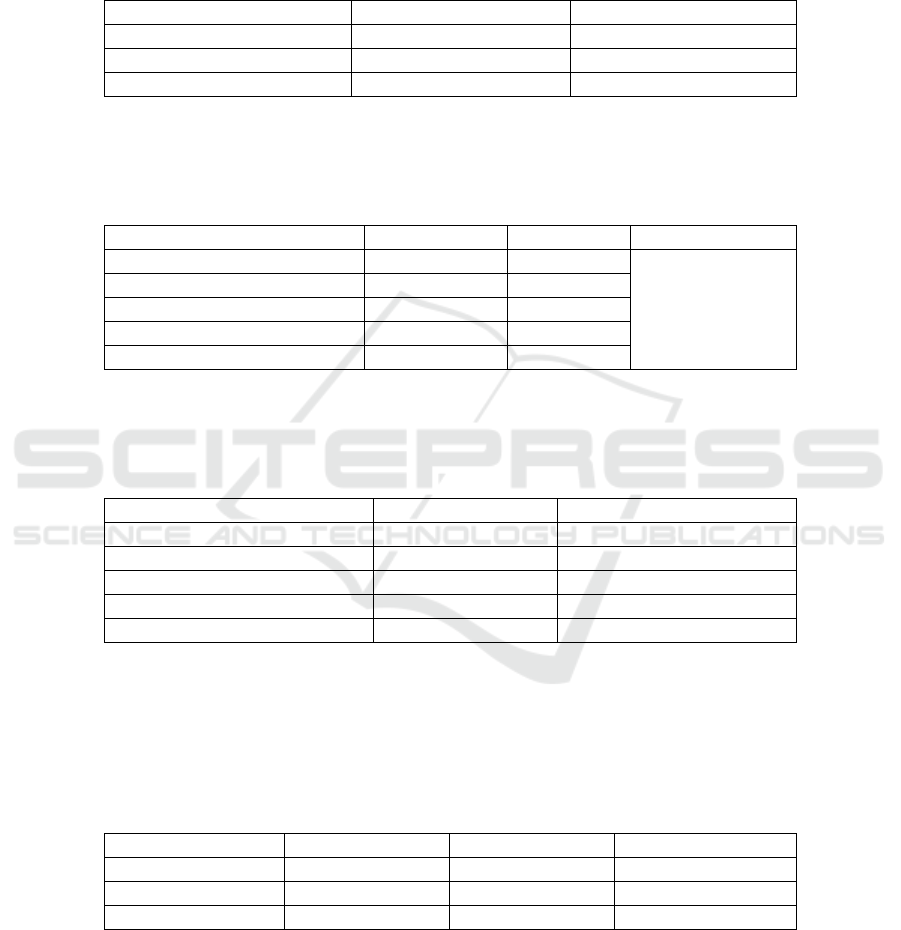

Table 2. The Result of Data Validity Test.

No. Variables KMO Sig MSA

Values

Information

1 APBD Supervision 0.999 0.000 0.754 Vali

d

2 Bud

g

et Knowled

g

e 0.999 0.000 0.795 Vali

d

3 Public Accountabilit

y

0.999 0.001 0.649 Vali

d

4 Organization

Commitmen

t

0.998 0.004 0.642 Valid

Source: Processed Primary Data, 2018

4.2.2 Result of Reliability Test

Table 3. The Result of Data Reliability Test.

No Variables Cronbach Alpha

Values

Information

1 APBD Supervision 0.794 Reliable

2 Bud

g

et Knowled

g

e 0.824 Reliable

3 Public Accountabilit

y

0.761 Reliable

4 Or

g

anization Commitmen

t

0.756 Reliable

Source: Processed Primary Data, 2018

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

346

4.3 Result of Classical Assumption Test

4.3.1 Result of Normality Test

Table 4. The Result of Data Normality Test.

Variables Asymp Sig. (2-tailed) Information

Bud

g

et Knowled

g

e 0.400

N

ormal

Public Accountabilit

y

0.200

N

ormal

Or

g

anization Commitmen

t

0.588

N

ormal

Source: Processed Primary Data, 2018

4.3.2 Result of Multicolonierity Test

Table 5. The Result of Multicolonierity Test.

Variables Tolerance VIF Information

Budget Knowledge 1.000 1.000

Free

Multicolonierity

Public Accountability 0.738 1.250

PAAP Moderation 0.845 1.184

Organization Commitment 0.874 1.144

PAKO Moderation 0.874 1.145

Source: Processed Primary Data, 2018

4.3.3 Result of Heteroscedasticity Test

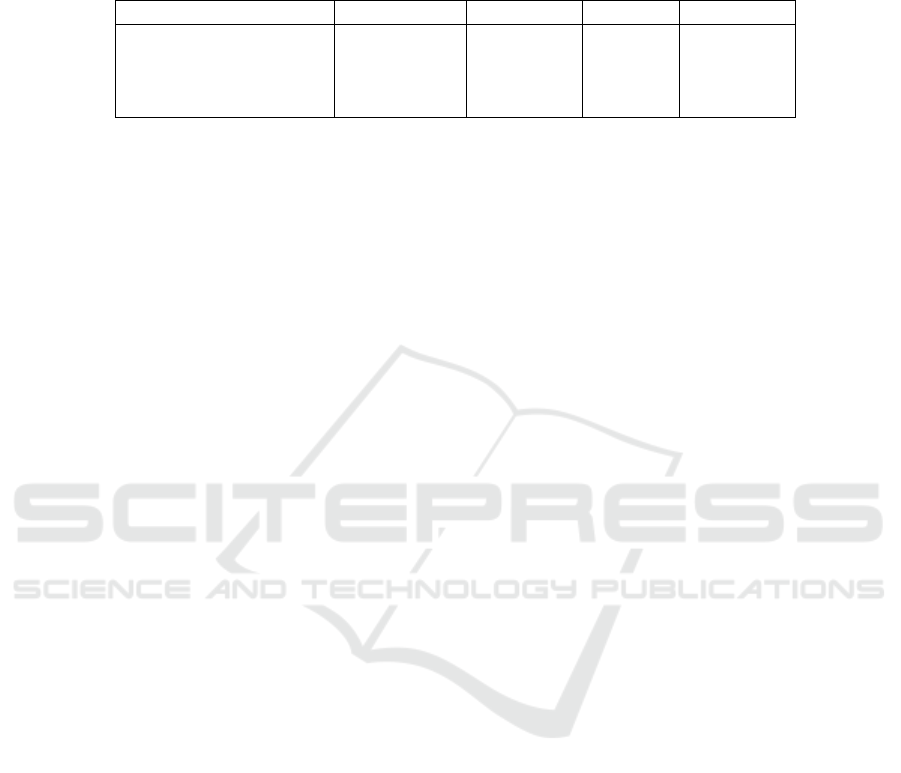

Table 6. The Result of Heteroscedasticity Test.

Variables Sig Information

Budget Knowledge 0.293 Free Heteroscedasticit

y

Public Accountability 0.808 Free Heteroscedasticit

y

PAAP Moderation 0.485 Free Heteroscedasticit

y

Organization Commitment 0.686 Free Heteroscedasticit

y

PAKO Moderation 0.131 Free Heteroscedasticit

y

Source: Processed Primary Data, 2018

4.4 Regression Test

4.4.1 F Significant Test

Table 7. The Result of F Test.

Model F Sig. Information

Equation 1 16.247 0.000 Si

g

nifican

t

Equation 2 6.867 0.001 Si

g

nifican

t

Equation 3 5.528 0.004 Si

g

nifican

t

Source: Processed Primary Data, 2018

The Influence of Indonesian Legislative Assembly Knowledge about Budget towards APBD Supervision with Public Accountability and

Organization Commitment Moderating Variables: Empirical Study on Legislative Assembly in Bengkulu Province

347

4.4.2 Determination Coefficient Test (R2)

Table 8. The Result of Determination Coefficient Test.

Regression of Equation 1

R Square 0.323

Adjusted R

2

0.303

Regression of Equation 2

R Square 0.433

Adjusted R

2

0.370

Regression of Equation 3

R Square 0.381

Adjusted R

2

0.312

Source: Processed Primary Data, 2018

4.4.3 Test of Hyphotheses 1

Table 9. The Result of Hyphotheses 1 Test.

Variable Coefficient t-count Sig. Result

Budget Knowledge 0.569 4.031 0.000 Accepted

Source: Processed Primary Data, 2018

The significant value was 0.000 < 0.05, so the first hyphotheses is accepted. It

means that the better Legislative Assembly knowledge about budget which is owned,

it will increase the role of Legislative Assembly in APBD supervision, or the higher

knowledge about budget owned by Legislative Assembly members, so the better the

role of Legislative Assembly in APBD supervision.

4.4.4 Test of Hyphotheses 2

Table 10. The Result of Hyphotheses 2 Test.

Variables Coefficient t-count Sig. Result

Budget Knowledge

Public Accountability

Moderation

0.206

0.538

0.329

1.273

3.188

2.087

0.214

0.004

0.046

Accepted

Source: Processed Primary Data, 2018

The result of regression from this second hyphotheses states that Legislative

Assembly knowledge about budget has positive influence towards APBD supervision

moderated by public accountability is accepted. The higher interaction of Legislative

Assembly knowledge about budget with the public accountability, so the local finance

supervision done by the board will be more increased.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

348

4.4.5 Test of Hyphotheses 3

Table 11. The Result of Hyphotheses 3 Test.

Variables Coefficient t-count Sig. Result

Budget Knowledge

Organization

Commitment

Moderation

0.414

0.360

-0.166

2.399

2.222

-0.717

0.024

0.035

0.480

Rejected

Source: Processed Primary Data, 2018

The result of regression from the third hyphotheses for organization commitment

stated that Legislative Assembly knowledge about budget has positive influence

towards APBD supervision moderated by organization commitment can not be

accepted (rejected) because organization commitment moderating variable that

influence interaction between budget knowledge with APBD supervision is not

significant, so it can be concluded that organization commitment variable is not a

moderating variable, which indicated that the third hyphotheses is rejected.

5 Conclusion

Based on the result of this research, it can be concluded that:

1. Legislative Assembly knowledge about budget has positive influence towards

APBD supervision. It indicates that the higher level of budget knowledge, so the

better APBD supervision done by Legislative Assembly.

2. Legislative Assembly knowledge about budget is proven that it has positive

influence towards APBD supervision moderated by public accountability. The

higher interaction between Legislative Assembly knowledge and public

accountability, so APBD supervision done by Legislative Assembly will be better

and increase.

3. Legislative Assembly knowledge about budget is not proven that it has positive

influence towards APBD supervision moderated by organization commitment. It

indicates that organization commitment variable is not a moderating variable

because it is not strengthen or weaken the relations between Legislative Assembly

knowledge about budget towards APBD supervision, because from the result of

absolute difference value test is not proven as moderating.

5.1 Suggestion

Based on the research finding, discussion and conclusion above, also consideration of

any limitation in this research, so it suggested for the further researcher to consider the

following things:

1. For the further research, it is expected to add independent variable or moderating

variable to know other variables which can influence and strengthen/weaken the

dependent variable, such as leadership style and political background.

The Influence of Indonesian Legislative Assembly Knowledge about Budget towards APBD Supervision with Public Accountability and

Organization Commitment Moderating Variables: Empirical Study on Legislative Assembly in Bengkulu Province

349

2. For the further research, it is expected to add or change questionnaire instrument

which is easier to be understood by respondents so that the variable can be measured

perfectly.

References

A.A, Zainal, Ahmad Sayudi., dan Sarwani. 2015. Pengaruh Pengetahuan Dewan Tentang

Anggaran dan Partisipasi Masyarakat Terhadap Penyusunan APBD. JSAI: Vol.2, No.1,Hal

37-49.

Anthony, Robert N. dan Govindarajan Vijay. 2005. Management Control System. Buku 2.

Jakarta: Salemba Empat.

Ariati, Elsi. 2017. Pengaruh Pengetahuan Dewan Tentang Anggaran Terhadap pengawasan

Keuangan Daerah (APBD) dengan Political Backround, Akuntabilitas Publik dan

Transparansi Kebijakan Publik Sebagai Variabel Pemoderasi. JOM Fekon. Vol.4 No 1,

Februari.

Assagaf, Abubakar. 2015. Pengaruh Pengetahuan Anggota DPRD Terhadap Pengawasan APBD

Dengan Partisipasi Masyarakat, dan Transparansi Kebijakan Publik Sebagai Variabel

Moderasi (Studi pada DPRD Kota Ternate dan DPRD Kota Tidore Kepulauan). Tesis

Program Pasca Sarjana Universitas Khairun Ternate. Dipublikasikan

Bastian, Indra. 2010. Akuntansi Sektor Publik-Suatu Pengantar. Edisi 3. Jakarta: Erlangga.

Coryanata, Isma. 2007. Akuntabilitas, Partisipasi Masyarakat, dan Transparansi Kebijakan

Publik sebagai pemoderating Hubungan pengetahuan Dewan tentang Anggaran dan

Pengawasan keuangan daerah (APBD). Simpsium Nasinal Akuntansi X. Makassar.

Ghozali, Imam. 2013. Aplikasi Analisis Multivariate Dengan Program SPSS, Edisi Keenam.

Jakarta: Universitas Diponegoro.

Halim, Abdul. 2007. Akuntansi Keuangan Daerah. Jakarta: Penerbit Salemba Empat.

Halim, Abdul & Muhammad Syam Kusufi. 2012. Akuntansi Sektor Publik. Jakarta: Penerbit

Salemba Empat.

Halim, Abdul & Muhammad Syam Kusufi. 2007. Seri Bunga Rampai Manajemen Keuangan

Daerah: Akuntansi dan Pengendalian Pengelolaan keuangan Daerah. Edisi Revisi

Yogyakarta:UPP STIM YKPN.

Halim, Abdul & syukriy Abdullah. 2006. Hubungan dan Masalah Keagenan di Pemerintahan

Daerah: Sebuah Peluang Penelitian Anggaran dan akuntansi. Jurnal Akuntansi Pemerintahan.

Vol 2, No 1, Hal: 53-64.

Harian Rakyat Bengkulu. 2016, 24 Oktober. Deal-Deal Ketok Palu APBD-P. Tersedia di

http://harianrakyatbengkulu.com/ver3/2016/10/24/deal-deal-ketok-palu-apbd-p/ (diakses

pada 24 Oktober 2016).

Harian Rakyat Bengkulu. 2016. Kejati Periksa Dua Pejabat Pemerintah Provinsi Sebagai Saksi

korupsi Jalan Pulau Enggano. Tersedia di http://harianrakyatbengkulu.com/ver3/2017/06/

13/kejati-periksa-dua-pejabat-pemprov-sebagai-saksi-korupsi-jalan-pulau-enggano/(diakses

pada 13 juni 2017).

Ikhsan, Arfan dan Ishak Muhammad. 2005. Akuntansi Keprilakuan. Jakarta: Salemba Empat.

Jensen, M.C, and Meckling W. 1976. Theory of the Firm : Manajerial Behavior, Agency Cost

and Ownership Structure. Journal of Financial Economics 3. Pp : 305-360.

Kementerian Dalam Negeri. 2017, 28 Desember. Jelang Akhir 2017, Serapan Anggaran Pemprov

Bengkulu 72,33 Persen. Tersedia di http://www.kemendagri.go.id/news/2017/12/28/jelang-

akhir-2017serapann anggaran-pemprov-bengkulu-7233-persen (Diakses pada 28 Desember

2017).

Kusumawati, Eny. 2014, Pengaruh Pengetahuan Dewan Tentang Anggaran Terhadap

Pengawasan Keuangan Daerah (Studi Empiris Pada DPRD Provinsi Jawa Tengah Dan DPRD

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

350

Kabupaten Karanganyar).Seminar Nasional dan Call Of Paper, ISBN 978-602-70429-2-6

Juni.FEB UMS.

Liputan6.Com. 2016, 25 Agustus. Anggaran Bengkulu Dipotong Rp 197 Miliar. Tersedia di

http://regional.liputan6.com/read/2585820/anggaran-bengkulu-dipotong-rp-197-miliar

(diakses pada 25 Agustus 2016).

Lubis, Arfan Ikhsan. 2010. Akuntansi Keperilakuan. Jakarta: Penerbit Salemba Empat.

Mardiasmo. 2009. Akuntansi Sektor publik. Yogyakarta: Penerbit Andi.

Nordiawan, Deddy. 2009.Akuntansi Sektor Publik. Jakarta: Salemba empat.

Patiar., Sri Rustiyaningsih., dan Dwi Handayani. 2014. Pengaruh Pengetahuan Dewan tentang

Anggaran terhadap pengawasan Keuangan Daerah (APBD) dengan Variabel Moderating

Partisipasi Masyarakat dan Transparansi Kebijakan Publik. Jurnal Riset Manajemen dan

Akuntansi: Vol.02, No.01, Hal:14-24.

Pramita Devi Yulindan dan Lilik Andriyani. 2010. Determinasi Hubungan Pengetahuan Dewan

Tentang Anggaran dengan Pengawasan Dewan Pada Keuangan Daerah (APBD). SNA 13.

Purwokerto.

Purnomo, Debby. 2016. Determinasi Hubungan pengetahuan Dewan Tentang Anggaran dengan

Pengawasan Dewan Pada Keuangan daerah (APBD). JOM FEKON: Vol. 3. No. 1

Ramdhani, Dadan. 2014. Determinasi Hubungan pengetahuan Dewan Tentang Anggaran dengan

Pengawasan Dewan Pada Keuangan daerah. Jurnal Akuntansi.

Republik Indonesia. Undang-Undang Nomor 17 Tahun 2014 tentang Majelis Permusyawaratan

Rakyat, Dewan perwakilan Rakyat, Dewan Perwakilan Daerah, dan Dewan Perwakilan

Rakyat Daerah.

_______________. Undang-Undang Republik Indonesia Nomor 23 tahun 2014 tentang

Pemerintah Daerah.

_______________. Peraturan Pemerintah Nomor 58 Tahun 2005 tentang Pengelolaan keuangan

Daerah.

_______________. Peraturan Pemerintah Nomor 16 Tahun 2010 tentang Pedoman Penyusunan

Peraturan dewan perwakilan Rakyat Daerah tentang Tata Tertib Dewan Perwakilan Rakyat

Daerah.

Robins, Stephen P dan Jugde Timothy A. 2008. Prilaku Organisasi, Jilid 1, Edisi 12. Jakarta:

Salemba Empat.

Robinson. 2006. Pengaruh Kualitas Anggaran Terhadap Efektifitas pengawasan Anggaran

:Pengetahuan Tentang Anggaran Sebagai Variabel Moderating (Studi Empiris Pada DPRD

Kabupaten Kota se-Provinsi Bengkulu). Tesis Program Pasca Sarjana Magister Sains

Akuntansi Universitas Diponegoro Semarang.

Rosita, Ni Made Ana., Nyoman Trisna H dan Ni Kadek Sinarwati. 2014. Pengaruh Latar

Belakang Anggota Dewan dan Pengetahuan Dewan Tentang Anggaran Terhadap

Pengawasan Keuangan Daerah (APBD) Dengan Variabel Moderating Transparansi

Kebijakan Publik. E-Journal S1 Akuntansi Universitas Pendidikan Ganesha.

Sekaran, Uma. 2011. Metodologi Penelitian untuk bisnis, Edisi 4, Buku 1. Jakarta: Salemba

Empat.

Sugiyono. 2011. Metode Penelitian Pendidikan (Pendekatan Kuantitatif, Kualitatif, dan R & D).

Bandung: Alfabeta.

Sudiarta, Gede Dewa.,Ni Luh Gede Erni S, dan Edy Sujana. 2014. Analisis Pengaruh

Pengetahuan Dewan Tentang Anggaran Terhadap Pengawasan Keuangan Daerah dengan

Akuntabilitas Publik, Partisipasi Masyarakat dan Transparansi Kebijakan Publik Sebagai

Variabel Moderating. e-journal S1 Akuntansi Universitas Pendidikan ganesha: Vol.2. No.1

Ulum, Ihyaul dan Ahmad Juanda. 2016. Metodologi Penelitian Akuntansi. Malang : Penerbit

Aditya Media Publishing.

Utami, Kurnia dan Efrizal Syofyan. 2013. Pengaruh Pengetahuan Dewan Tentang Anggaran

Terhadap Pengawasan Keuangan Daerah Dengan variabel Pemoderasi Partisipasi

Masyarakat dan Transparansi Kebijakan Publik. Jurnal WRA : Vol.1. No. 1

The Influence of Indonesian Legislative Assembly Knowledge about Budget towards APBD Supervision with Public Accountability and

Organization Commitment Moderating Variables: Empirical Study on Legislative Assembly in Bengkulu Province

351

Wasistiono, Sadu dan Yonatan Wiyoso. 2009. Meningkatkan Kinerja Dewan Perwakilan Rakyat

Daerah (DPRD). Bandung: Fokus Media

Widiyahningsih dan Pujirahayu. 2012. Pengaruh Pengetahuan Anggota Legislatif Daerah

Tentang Anggaran Terhadap Pengawasan Anggaran Pendapatan dan Belanja Daerah Dengan

Akuntabilitas Sebagai Variabel Moderating. Jurnal Akuntansi UPI. ISSN 2088-2106.

Wirawan. 2014. Kepemimpinan: Teori, Psikologi, Prilaku Organisasi, Aplikasi dan Penelitian.

Jakarta : Raja Grafindo Persada.

Wulandari, Trini dan Deviani. 2013. Pengaruh Pengetahuan Dewan Tentang Anggaran Terhadap

Pengawasan Keuangan Daerah Dengan variabel Pemoderasi Akuntabilitas Publik. Jurnal

WRA : Vol.1. No. 2.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

352