Financial Management Accountability of Sawang Lebar

Ilir Village North Bengkulu Regency

Abdulla, and Winda Nusa Winanda

Department of Accounting, Fakultas Ekonomi dan Bisnis, Universitas Bengkulu,

Bengkulu, Indonesia

Abstract. This article to explain the planning and budgeting process on

management of financial in Sawang Lebar Ilir Village, North Bengkulu Regency.

The informants of this study were the village head, village secretary, village

treasurer, government head, BPD chairman, BPD representative, BPD secretary,

and community representatives. Data was collected through an interview process

and documentation. The results of this study indicate that the planning and

budgeting process on management of financial has been carried out correctly in

accordance with applicable regulations and has been carried out in an accountable

and transparent manner. This article can provide additional knowledge for the

village government regarding the accountability of village fund management in

development planning and management.

Keywords: Accountability ꞏ Village fund management ꞏ Planning ꞏ Budgeting

1 Background

Nawacita is committed to develop Indonesia from the sidelines. As a form of this

commitment, the Jokowi-JK government has allocated village funds to all villages in

Indonesia. This village fund program is the first in Indonesia. The allocated village fund

aims at improving the welfare of the village community. The distribution of village

funds certainly requires moral and administrative responsibility from village officials

and the community to manage these funds well. To realize good governance in village

governance, especially village financial management requires the principles of

governance that are transparent, accountable and participatory which are carried out

with order and budget discipline (Permendagri No. 20 of 2018).

According to data obtained from a study conducted by the Corruption Eradication

Commission (KPK) since January 2015 on village financial management, both Village

Fund Allocation (ADD) and Village Funds, the KPK found 14 findings in four aspects,

namely regulatory and institutional aspects, administrative aspects, aspect of

supervision, and aspect of human resources (kompas.com). However, the phenomenon

of the findings by the KPK is contradicted to the findings of the management of village

funds in Sawang Lebar Ilir Village, Tanjung Agung Palik District, North Bengkulu

Regency. From the results of information obtained from the village head and village

apparatus, the management of village funds in the village is going well. This is

evidenced by the existence of transparency and accountability of village funds in this

village. The village apparatus always involves all components of the village, including

328

Abdulla, . and Winanda, W.

Financial Management Accountability of Sawang Lebar Ilir Village North Bengkulu Regency.

DOI: 10.5220/0009870100002900

In Proceedings of the 20th Malaysia Indonesia International Conference on Economics, Management and Accounting (MIICEMA 2019), pages 328-338

ISBN: 978-989-758-582-1; ISSN: 2655-9064

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

participation from the community, especially in the implementation of the Village

Development Plan (Musrenbang Desa) to prepare the APBDes.

The stages of village financial management that will be examined in this study only

focus on the accountability stages of planning and budgeting. That is because planning

is the first stage and the first step in village financial management. Through this

research, it is expected to obtain a description about the accountability of planning and

village financial management budgeting in Sawang Lebar Ilir Village.

2 Literature Review

2.1 Village Financial Management

In Permendagri No. 20 of 2018, it is explained that village finance is all rights and

obligations in the context of administering village governance that can be valued in

money including all forms of wealth related to the village's rights and obligations. These

rights and obligations can lead to income, expenditure, financing, and village financial

management. The process of village financial management (Village Fund Allocation

and Village Funds) is based on the Minister of Home Affairs Regulation No. 20 of 2018

concerning village financial management which includes planning and budgeting,

implementation and administration, as well as reporting and accountability.

2.2 Accountability

According to Government Regulation No. 24 of 2005 concerning public sector

accounting standards, accountability is responsible for managing resources and

implementing policies entrusted to reporting entities in achieving periodically

established goals. According to the Institute of State Administration (2003)

accountability is an obligation to provide accountability or answer and explain the

performance and actions of a person, legal entity or an organization to those who have

the right or authority to request information or accountability. Public accountability is

the obligation of the agent (agent) to provide responsibility, present, report, and disclose

all activities that are the responsibility of the trustee (principal) who has the right and

authority to request such accountability (Mardiasmo, 2002). Madiasmo divides public

accountability into 2 types, namely:

a. Vertical Accountability

Vertical accountability is the responsibility for managing funds to a higher

authority.

b. Horizontal Accountability (horizontal accountable)

Horizontal accountability is the responsibility for managing funds to public.

2.3 The Accountability Dimension

The accountability dimension that must be fulfilled by public sector organizations as

described by Ellwood 1993 in (Mahmudi, 201) includes: 1) Accountability for probity

Financial Management Accountability of Sawang Lebar Ilir Village North Bengkulu Regency

329

and legality is the accountability of public institutions to behave honestly and to obey

the applicable legal provisions in working or in running an organization that is related

to avoiding misuse of office, kolusi, and corruption. 2) Managerial accountability is the

responsibility of public institutions to manage the organization efficiently and

effectively. 3) Program accountability is related to the consideration of whether or not

a goal has been set, and whether it has considered an alternative program that can

provide optimal results with minimal costs. 4) Policy accountability is the

accountability of public institutions for the policies taken. 5) Financial accountability

is the responsibility of public institutions to use public money economically, efficiently

and effectively.

3 Research Methods

3.1 Types of Research

The type of research used in this research is descriptive research with a qualitative case

study approach. Qualitative research is a research that explains the facts, conditions,

situations, and events that occur in the field naturally by conducting in-depth analysis

(Sugiyono, 2016). Descriptive research is a type of research that aims at explaining

something through a study. This study only aims at describing explaining phenomena

naturally without looking at relationships or comparing a variable (Ulum and Juanda,

2016). Qualitative research with a type of case study is a type of qualitative research

that focuses on the specification of cases in an event that includes individuals, cultural

groups, or a portrait of life (Sugiyono, 2016).

3.2 Research Instruments

The main instrument of qualitative research is the researcher himself. To be an

instrument, researchers are required to have the provision of theory and broad insights

to be able to ask questions, analyze, and construct the social situations that are being

studied to be more extensive and meaningful (Sugiyono, 2016). In this study, the main

research instrument is the researcher himself, who is assisted by a recorder, camera,

and question and answer transcript.

3.3 Research Location

The research location in this study is Sawang Lebar Ilir Village, Tanjung Agung Palik

District, North Bengkulu Regency. Researchers chose this place to become a place of

research to find out and analyze to what extent the village financial management,

especially planning and budgeting in the village, has been going well and correctly

according to the accountability principles and to what extent the village financial

management in Sawang Lebar Village has followed the applicable regulations.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

330

3.3.1 Research Informant

The main data source of this research is the informant. Informants are people who

provide information about the situation and conditions of the research background

(Sugiyono, 2016). The informant is the main data source to answer the research

problem. The informants in this study consist of village head who has served and

worked for 2.5 years with the last education degree of senior high school, village

secretary who has served and worked for 2.5 years and the last education of

undergraduate degree in Biology, village treasurer who has served and worked for 2.5

years with the last education degree of senior high school, the section head of

government who has served and worked for 2.5 years with the last education degree of

undergraduate degree, the Village Consultative Body (BPD) consisting of the chairman,

deputy and secretary of the BPD who have served and worked for 3 years with the last

education of senior high school, and three (3) villagers residing in Sawang Lebar Ilir

Village, Tanjung Agung Palik District, North Bengkulu Regency with the last

education degrees of one senior high school and two elementary schools.

3.4 Data Type

The type of data used in this study are primary data and secondary data. Primary data

are data collected by researchers directly from the first source (Ulun and Juanda, 2016).

In this study primary data were obtained through direct interviews with informants.

While secondary data are data obtained not from the first party (Sugiyono, 2016). In

this study secondary data are obtained from activity documents, APBDes report

documents, and other documents in the village which are obtained from the village

apparatus and BPD of Sawang Lebar Ilir Village, Tanjung Agung Palik District, North

Bengkulu Regency.

3.5 Method of Collecting Data

Data collection method is a process that emphasizes on the way researchers reveal the

process of getting data from various techniques, sources, and research actions. In this

research the data collection technique used is triangulation/combination. Triangulation

method is defined as a data collection technique that is a combination of various data

collection methods and from existing data sources. The triangulation data collection

method used in this study is interviews and documentation.

3.6 Data Analysis Method

Qualitative data analysis is mostly done together with data collection. It is inductive

which means the analysis based on data obtained in the field (Sugiyono, 2016). Data

analysis method used in this research is qualitative data analysis that follows the

concept of Miles and Huberman. Activities in the data analysis consist of data

reduction, data display, and conclusion drawing.

Financial Management Accountability of Sawang Lebar Ilir Village North Bengkulu Regency

331

3.7 Data Credibility Testing Techniques

After the researchers analyze the data, the next step conducted is to test the credibility

or validity of the data. The validity of the data is carried out with the aim of testing the

confidence of the data obtained from a study. In this study the validity of the data used

is the credibility test. According to Sugiyono (2016), data credibility test is a trust to

the data of research result.

4 Research Results Aand Discussion

4.1 Description of Research Area

Sawang Lebar Ilir Village is included in Tanjung Agung District, North Bengkulu

Regency, Bengkulu Province which has an area of 1,805 ha. Sawang Lebar Ilir Village

consists of three villages, each is led by village head. Sawang Lebar Ilir Village area is

a crossing area to the center of North Bengkulu Regency, namely Arga Makmur. The

condition of the community is quite diverse with quite dense population, quite complex

social condition, various professions, and very fast development.

The geographical boundaries of the village of Sawang Lebar Ilir are as follows:

Northern border : Sawang Lebar Village

Southern border : Pasar Kerkap Village and Air Napal Village

Western border : Desa Talang Kering and Desa Talang Jarang

Eastern border : Senabah Village

4.2 Vision and Mission of Sawang Lebar Ilir Village

In carrying out village development, Sawang Lebar Ilir Village compiles the village's

vision and mission as a reference and objective of the village's development. Village

development and welfare are built according to the contents of the vision and mission

that has been established.

“ Meningkatkan kemandirian untuk mewujudkan masyarakat yang berdaya guna dan

sejahtera

4.3 Misi Desa

1. Menumbuhkan kembangkan kegiatan keagamaan dalam masyarakat

2. Mengembangkan sarana dan prasarana kebutuhan desa sesuai dengan tujuan guna

terwujudnya pembangunan desa yang optimal

3. Berperan aktif dalam menjaga keamanan dan ketertiban desa

4. Meningkatkan mutu/kualitas aparat desa selaku abdi di desa dalam pelayanan

terhadap masyarakat

5. Cepat dan tepat dalam melaksanakan tugas dan tanggungjawab

6. Membangun kemandirian seluruh stakeholder

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

332

4.4 Village Vision

"Increasing independence to realize an efficient and prosperous society”

4.5 Village Mission

1. Developing religious activities in the community.

2. Developing facilities and infrastructure for village needs in accordance with the

objectives for the realization of optimal village development.

3. Playing an active role in maintaining security and order in the village.

4. Improving the quality of village apparatus in serving the community.

5. Fast and precise in carrying out the duties and responsibilities

6. Building independence of all stakeholders.

4.6 Description of the Informant

The informants in this study are divided into two groups, namely village apparatus and

community parties represented by the People's Consultative Body (BPD) and direct

community representatives. The village apparatus plays the role of village financial

manager, especially in the village financial planning and budgeting stages. Village

apparatus, BPD, and the community who are informants in this study can be seen in the

following table 1:

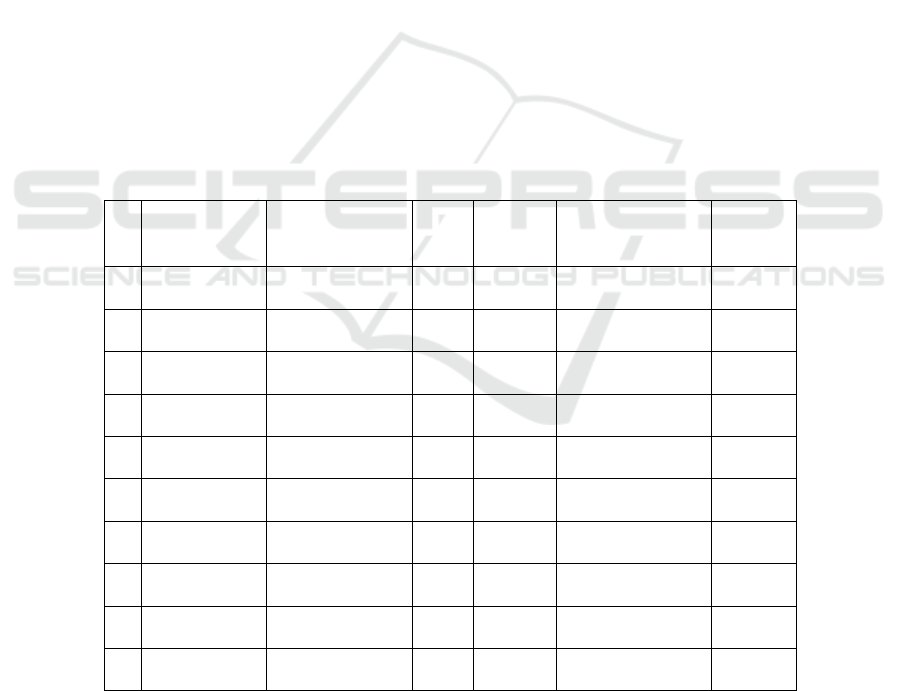

Table 1. Data of Informants.

No Name Position Age Gender

Last Education

Degree

Length

of Work

1 Zurbaini Village Head 35 yr Male Senior high school 2.5 years

2 Eka Septiani Village Secretary 29 yr Female

Undergradute in

Biolog

y

2.5 years

3 Nirwana Village Treasurer 36 yr Female Senior high school 2.5 years

4 Rahmat Sukur BPD Chairman 36 yr Male Senior high school 3 years

5 Ely Herweni BPD Deputy 32 yr Female Senior high school 3 years

6 Neti Nopita BPD Secretary 39 yr Female Senior high school 3 years

7 Yogi Pratama

Section Head of

Government

31 yr Male Undergraduate 2.5 years

8 Ronsoni Villager 44 yr Male Senior high school -

9 Ajum Villager 57 yr Male Elementary -

10 Mardani Villager 57 yr Male Elementary -

Source : Research Result, 2019

Financial Management Accountability of Sawang Lebar Ilir Village North Bengkulu Regency

333

The informants of this study can be seen in table 4.1. There are 10 informants in

this study. From all the informants, it is known that on average, the highest level of

education of village apparatus senior high school, and there are villagers who are only

graduated from elementary school.

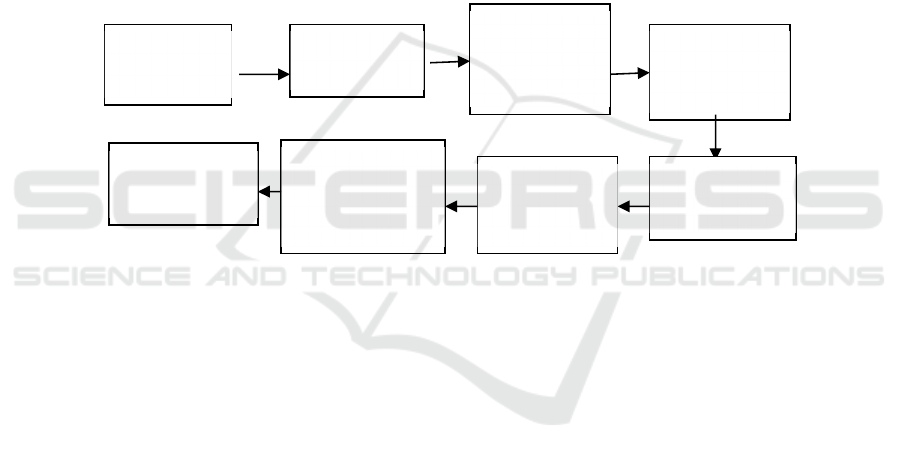

4.7 Village Financial Planning

According to North Bengkulu Regent Regulation No. 6 of 2019 concerning Village

Financial Management in North Bengkulu Regency, the village government arranged

a village development plan according to its authority with reference to the North

Bengkulu Regency government development plan. Village development planning

includes RPJMDesa and RKPDesa, which is arranged in a time frame and stipulated by

village regulations. RKPDesa becomes the basis for the preparation of APBDesa

documents. Broadly speaking, village financial planning and budgeting in the village

of Sawang Lebar Ilir starting from RPJMDesa to the establishment ofAPBDesa can be

described as follows:

In this study it can be seen that the planning and budgeting of financial management

in Sawang Lebar Ilir Village starts from the preparation of the Village Medium Term

Development Plan (RPJMDesa) that is from the beginning of the preparation, the origin

of the preparation, the preparation process, the deliberation process, people who

attended the deliberations, as well as the guidance preparation of each stage of village

financial planning and budgeting.

4.8 Village Medium Term Development Plan (RPJMDesa)

Village planning is divided into medium term planning and short term planning.

Medium-term planning is called the village medium term development plan

(RPJMDesa) while the short-term planning is called the village RKP (Village

Government Work Plan). The planning stages of village financial management in

Sawang Lebar Ilir Village started with the village medium-term development plan

(RPJMDesa). The village medium term development plan was made at the beginning

of the village administration period or after the election of the village head. The

preparation of RPJMDesa in the village of Sawang Lebar Ilir was also formulated after

Village

Regulation

about

Design of RKP

Desa

RKP Desa (List

of Village

Priority 2019)

Village Regulation

about RKP Desa

2019

Raperdes about

APBDesa 2019

Consultation among

Village Head, BPD

and the involved

components

Village Regulation

about APBDesa

2019

Consultation

about Village

Planning and

Bud

g

etin

g

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

334

the inauguration of the elected village head, based on a statement from the chairman of

BPD, Bapak Rahmat Sukur:

"... In the drafting of the village regulation on APBDesa, I did not do it myself

... I was also assisted by another drafting team from the village apparatus, after

that we convey it to the village head when it was finished compiling. Then the

village head discussed the draft with the BPD for agreement. "

This is in line with what was said by Mr. Zurbaini as the Village Head, he stated

that:

"... There is a planning team of its own. The team has a chairman, secretary and

treasurer. So it is very necessary for the team to compile a Raperdes about the

APBDesa, then afterwards it is discussed and agreed with the BPD. "

The Government of Sawang Lebar Ilir Village has prepared a planning and budget

document in the form of the Village Budget and Expenditure (APBDesa) as explained

earlier which includes:

a) The village head forms the APBDesa compilation team consisting of the

village head, village secretary, institutions, and village community leaders.

b) *The APBDesa draft preparation team examines the proposal of village

development activity plan in the RKPDesa which covers a variety of things.

c) The drafting team carries out a draft APBDesa based on the RKPDesa, and

legislation.

d) The draft APBDesa that has been prepared, is then submitted to the village

head for a village discussion which is followed by the village government,

BPD, community representatives, sub-district authorities, and the police

station.

e) APBDesa results from village discussion are being improved, then the village

secretary will prepare a Perdes draft on APBDesa and village heads bring the

APBDesa Raperdes to BPD for joint discussion and approval.

f) After the APBDesa draft is approved by the BPD, the village head then adopts

the APBDesa Raperda as a Perdes on the APBDesa along with the stipulation

of the APBDesa implementation policy. The policy is the management of

village goods, putting in order the decisions of the Village Financial

Management Technical Implementation (PTPKD), setting village treasurers,

collecting village revenue, managing village assets.

g) The agreed APBDesa will then be submitted by the village head to the Regent

through the Camat for evaluation

Based on the sequence of the APBDesa document preparation process, it can be

seen that the government of Sawang Lebar Ilir Village has applied the principle of

accountability well in the process. The process of drafting APBDesa in Sawang Lebar

Ilir Village is in accordance with the regulation of Permendagri No. 20 of 2018 by

following the flow contained in the regulation. The process involves various existing

components including the community in village discussion, and being opened in the

formulation process. The drafting team carries out the administration well by

documenting all stages of the process in the formulation of the APBDesa document.

The APBDesa document has been discussed and approved by the BPD which is then

established by Perdes and can be accessed by the village community and related parties

Financial Management Accountability of Sawang Lebar Ilir Village North Bengkulu Regency

335

in the management of the village government. This proves that the village government

has implemented accountability in the management of the Sawang Lebar Ilir village

government.

In the process of formulating and compiling these APBDes documents, it can be

seen that several accountability dimensions have been applied, namely:

a) Management accountability, in which in the management of the preparation of

APBDesa documents, the village government has formulated and arranged

regularly according to their authority. The team and the village government

have carried out an orderly administration written with good documentation in

the process of formulating the APBDesa document.

b) Legal accountability and honesty, all the stages of the preparation of the

APBDesa have followed and in accordance with the rules contained in

Permendagri No 20 of 2018 regarding guidelines for village financial

management.

c) Accountability policy, each process of formulating the APBDesa has involved

the community from the beginning of the preparation of the APBDesa so that

the policy has been in linewith the proposals from the community.

5 Closing

The village government in the village of Sawang Lebar Ilir has prepared a planning and

budget document in the form of RPJMDesa with the stages as stated in the Minister of

Home Affairs Regulation No. 20 of 2018 regarding guidelines for village financial

management. At the stage of drafting RPJMDesa, Sawang Lebar Ilir village has applied

the principle of accountability. The process is in accordance with existing regulations,

RPJMDesa is stipulated by Perdes and can be accessed by the community and related

parties in village government management. Accountability in the compilation of

RKPDesa also has several dimensions of accountability, namely management

accountability, legal accountability and honesty, and policy accountability.

The Government of Sawang Lebar Ilir Village has prepared a planning and budget

document in the form of a Village RKP at a stage such as that contained in Permendagri

No. 20 of 2018 concerning guidelines for village financial management. the

government of Sawang Lebar Ilir Village has applied the principle of accountability

well. The village government has implemented accountability in the management of

the village government in Sawang Lebar Ilir Village and can be identified 3 dimensions

of accountability from the preparation of the RKPDesa namely management

accountability, legal accountability and honesty, and policy accountability.

The process of drafting APBDesa in Sawang Lebar Ilir Village is in accordance

with the regulation of Permendagri No. 20 of 2018 by following the flow contained in

the regulation. It involves various existing components including the community in

village discussions, and being opened in the formulation process. The village

government has implemented accountability in the management of of Sawang Lebar

Ilir village, which has 3 dimensions of accountability, namely management

accountability, legal accountability and honesty and policy accountability. This

research can provide information and contribute to the development of knowledge

about village financial management, especially at the stage of village financial planning

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

336

and budgeting as an evaluation material for the Government of Sawang Lebar Ilir

Village in carrying out its responsibilities towards the management of village financial

Planning and Budgeting in order to avoid future obstacles. This research can provide

additional understanding and knowledge for village apparatus and the community about

village financial management accountability, especially in the planning and budgeting

stages. This research is expected to provide scientific information and can be a

reference for further research.

This study lacked maximum data results from several informants, due to the lack of

understanding of the informants in answering and explaining the questions given by

researchers. This caused the difficulty in conducting interviews and communicating in

depth to the informants. This study was unable to collect overall data from the village

secretary and did not get all the supporting documents because the village secretary

refused to be interviewed in detail and also could not get information on the interview

of the village head because one of the village head refused to be interviewed because

he was busy and other village head could not be met.This study did not get explanatory

data from village facilitators because there were no interviews with village facilitators

because village facilitators did not live in the village. Based on the limitations in this

study, then further research is recommended to get maximum data results by directing

informants to better understand the research theme. Future researchers is expected to

study and understand the characteristics of the research object to be studied. Further

researchers are advised to increase the number of research objects so that they can add

more informants to get the maximum data. The next research is expected to be able to

add interview information to village facilitators to clarify the data obtained.

References

Andini, Hanni. 2018. Penerapan Prinsip Akuntabilitas dan Prinsip Transparansi dalam

Pengelolaan Keuangan Desa. Skripsi Fakultas Ekonomi Universitas Sanata Dharma

Yogyakarta

Apriliana, Riska. 2017. Pengelolaan Alokasi Dana Desa Dalam Mewujudkan Good Governance.

Skripsi Institut Agama Islam Negeri Surakarta

BPK . 2017. Kejelasan Dana Desa Dalam Anggaran Pendapatan dan Belanja Negara

Kementerian Desa, Pembangunan Daerah Tertinggal, dan Transmigrasi Indeks Desa

Membangun Tahun 2015

Kamus Besar Bahasa Indonesia. 2014. Edisi 4

Keputusan Menteri Pendayagunaan Aparat Negara RI No 25/KEP/M.PAN 2002

Lembaga Administrasi Negara (LAN) No 589/X/6/Y/199 dalam Pedoman Penyusunan

Pelaporan Akuntabilitas Kinerja Instansi Pemerintah Tahun 2003

Mahmudi. 2013. Manajemen Kinerja Sektor Publik. Yogyakarta. UPP STIM YKPN

Mardiasmo. 2002. Akuntansi Sektor Publik. Yogyakarta. C.V. Andi Offset

Nafidah, Lina Nasehatun. 2017. Akuntabilitas Pengelolaan Keuangan Desa di Kabupaten

Jombang. Jurnal Ilmu Akuntansi Volume 10

Peraturan Menteri dalam Negeri No 20 Tahun 2018 Tentang Pedoman Pengelolaan Keuangan

Desa

Peraturan Menteri dalam Negri No 81 Tahun 2015 Tentang Evaluasi Desa dan Kelurahan serta

Perlombaan desa dan kelurahan

Peraturan Menteri Desa, Pembangunan Daerah Tertinggal, dan Transmigrasi Republik Indonesia

Nomor 22 Tahun 2016

Financial Management Accountability of Sawang Lebar Ilir Village North Bengkulu Regency

337

Peraturan Bupati Bengkulu Utara No 6 tahun 2019 tentang pedoman pengelolaan keuangan desa

dalam Kabupaten Bengkulu Utara

Peraturan Pemerintah Nomor 8 Tahun 2016 Tentang Perubahan Kedua Atas Peraturan

Pemerintah Nomor 60 Tahun 2014 Tentang Dana Desa yang Bersumber dari Anggaran

Pendapatan dan Belanja Negara

Peraturan Pemerintah Republik Indonesia Nomor 24 tahun 2005 Tentang Standar Akuntasi

Sektor Publik

Peraturan Pemrintah Nomor 47 Tahun 2015 Tentang Perubahan Atas Peraturan Pemerintah

Nomor 43 Tahun 2014 Tentang Peraturan Pelaksanaan Undang-Undang No. 6 Tahun 2014

tentang Desa

Peraturan Pemerintah Republik Indonesia Nomor 71 tahun 2010 Tentang Standar Akuntansi

Pemerintahan

Peraturan Pemerintah No 72 Tahun 2005 Tentang Desa

Ramli, Mustazir. 2017. Akuntabilitas Pengelolaan Keuangan Desa. Jurnal Ilmu Akuntansi

Volume 10

Sugiyono. 2016. Memahami Penelitian Kualitatif. Bandung. alfabeta

Undang-Undang Republik Indonesia Nomor 6 Tahun 2014 Tentang Desa

Undang-Undang Republik Indonesia Nomor 15 Tahun 2004 Tentang Pemeriksaan Pengelolaan

dan Tanggungjawab Keuangan Negara

Undang-Undang Republik Indonesia Nomor 22 Tahun 1999 Tentang Pemerintah Desa

Undang-Undang Republik Indonesia Nomor 23Tahun 2014 Tentang Pemerintah Daerah

Undang-Undang Republik Indonesia Nomor 32 Tahun 2004 Tentang Pemerintah Desa

Ulum, Ihyaul dan Ahmad Juanda. 2016. Metedologi Penelitian Akuntansi. Malang. Penerbit

Aditya Media Publishing

Nadia, Ambaranie. 2015.KPK Temukan Potensi Masalah dalam Pengelolaan Dana

Desa.Beritaonline(https://nasional.kompas.com/read/2015/06/12/20021111/KPK.Temukan.

Potensi.Masalah.dalam.Pengelolaan.Dana.Desa,diakses15Februari 2019)

Zainuddin, 2018. Akuntabilitas Praktik Pengelolaan Keuangan Desa Gamtala Halmahera Barat

Privinssi Maluku Utara. Jurnal Soedirman Accounting Review Volume 03 Nomor 01

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

338