Religiosity and Fraud Activity in Acehnese Millennials Worker

Mirza, Irin Riamanda

Lecturers of Psychology Departement at Syiah Kuala University

Keywords: Fraud, Religiosity, Millennial Workers, Islamic Sharia in Aceh.

Abstract: Aceh is a province that has the privilege of enforcing Islamic Sharia in Indonesia. This condition causes

Acehnese to be accustomed to implementing Islamic Sharia on each of their daily activities. Religiosity was

made as the variable to describe people’s habit in implementing Islamic sharia. The religiosity scale was

formulated based on the dimensions of Islamic Worldview and Religious Personality (Hamzah, et al., 2007).

Despite the familiarity of implementing Islamic sharia, various cases that violated sharia were still found,

such as corruption or fraud. This research was aimed to inspect the effect of religiosity toward the

occurrence of frauds in Aceh. The act of fraud can be seen from two things, namely fraud habits (pressure

and rationalization) and fraud opportunity (Tuanakotta, 2007). Albrecht (2012) was the one who explained

that the act of fraud mostly occurs because the perpetrator notice and gain the opportunity due to improper

control and supervision systems. Due to this condition, the hypothesis in this research was that religiosity

affects the occurrence of the act of fraud, when the opportunity to conduct fraud becomes the mediator. This

research was performed on Acehnese millennial workers, in which the data analysis performed through

Moderate Regression Analysis (MRA). The research result showed that the religiosity did not cause fraud

habits, but the effect will emerge if there is a moderation from fraud opportunity.

1 INTRODUCTION

Aceh is a province that has the autonomy in the

sectors of religion, custom, and education (Decree of

Prime Minister of RI No.1/Missi/1959). In addition,

Law No.44/1999 concerning the Administration of

the Autonomy of Aceh Special Region stipulates the

implementation of Islamic sharia thoroughly

(Kaffah) in Aceh. This matter which made Aceh

Province as the only province that implements

Islamic sharia in Indonesia. The governance of

Islamic sharia in Aceh did not just happen as it is

now, the civilization of Acehnese in culture and

custom are inseparable from the foundation of

Islamic law. Islamic teachings in the sectors of

worship, marriage, and inheritance have been

implemented since the past, even during the Aceh

sultanate era; therefore, they have permeated and

united with the daily life of Acehnese (Ibrahim,

2019).

In view of the above, it can be known that

Acehnese are accustomed to live religiously in

reference to Islamic sharia in their daily life.

According to Amawidyati and Utami (2007), the

religiosity of Islam is the degree of someone

religious internalization that is seen from the

appreciation of Aqidah/creed, sharia, and morals of

someone. According to Ismail and Desmukh (2012),

the religiosity in Islamic creed is the involvement in

religious practices (such as religious preaching

inside or outside the mosque), belief salience (the

internal belief towards Allah), and the frequency of

prayer. The implementation of Islamic law in the life

and customs of Acehnese elucidates a high

religiosity of Acehnese. Hazairin; the expert of

Islamic and customary laws in Indonesia described

that the presence of Islamic law in Indonesia is

because the law has taken place and elucidated the

nature of humans toward the truth of their God

(Wahidah, 2015).

The descriptions above explain that Acehnese are

accustomed to uphold Islamic sharia as the

foundation to act and behave. However, despite the

habits of Acehnese in implementing Islamic sharia,

some behaviors discrepant with sharia done by the

people were still found, such as corruption or fraud.

There were at least several studies that have

discussed the corruption cases in Aceh. Surya (2018)

discussed the corruption of village budget in Central

Aceh Regency, Maulana (2016) discussed the

198

Mirza, . and Riamanda, I.

Religiosity and Fraud Activity in Acehnese Millennials Worker.

DOI: 10.5220/0009440901980205

In Proceedings of the 1st International Conference on Psychology (ICPsy 2019), pages 198-205

ISBN: 978-989-758-448-0

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

corruption of regional budgeting in North Aceh,

Lubis and Marlina (2010) discussed the act of

corruption of good and service procurement in

District Court of Kuala Simpang. In addition, there

was a recent case occurred that caught the Aceh’s

governor within the brink of corruption case in that

very religious province. Another example of a fraud

case that has occurred in Aceh, as revealed by Bakri

(2017), there were 5 Bank’s employees in Aceh who

have been detained in a Civil Servant consumptive

credit fraud case which has cost the bank more than

2 billion rupiah. Moreover Nazar (2018) recorded

that in 2018 fraud cases were cases that ranked first

in Aceh Pidie.

Based on the case data above, it is known that

fraud behavior is common in Aceh. According to

Albrecht et al. (2012), fraud is any diversity of

activities designed through individual tactics to gain

benefit by falsifying document representations, and

surprising, cunning, and unfair tricks; causing others

to be deceived. Association Certified Fraud

Examiners (ACFE) describes fraud as all crimes that

produce benefit from others with deception as the

main modus operandi by presenting false data or

hiding the truth. Based on this definition, it can be

classified that corruption is one of the types of fraud.

High number of corruptions occurred in Aceh

amidst the implementation of Islamic sharia and the

high religiosity of its people is a contradictive

illustration. This condition made the researcher to

conduct in-depth study about the relationship

between both variables. This research focused on

Aceh’s millennial workers. This focus was

determined to test if the millennial workers of Aceh

conceive high religiosity value, and have the

indication of conducting fraud. The selection of

millennial workers as the target of research sample

was due to their familiarity with the sophisticated

technology of industry 4.0 revolution. Shamim,

Cang, Yu, Li (2017) produced a research in which

due the sophisticated technology of industry 4.0

revolution, subordinates did not trust their supervisor

because they rarely or never give complete

information or because some things have been

covered up from them.

The argument mentioned above describes that

the millennial generation who accustomed to

technologies often trigger the emergence of Fraud,

such as data falsification. Considering that Aceh’s

millennial workers are customarily very discipline in

implementing Islamic sharia and familiar with the

sophistication of technology, thus, this sample target

are very suitable with the research purpose. This

condition made the researcher to become interested

in inspecting the relationship between religiosity and

fraud activities on millennial workers in Aceh.

2 LITERATURE REVIEW

2.1 Fraud

Tuanakotta (2007) explained about the fraud

triangle, which illustrates the reason why people

conduct fraud. According to his research, this Fraud

Triangle consists of opportunity, pressure, and

rationalization. Opportunity is the condition that

facilitates the managerial and workers to manifest

the chances of fraud due to the undetectable

activities as a result of poor managerial supervision

(Tuanakotta, 2007; Tunggal, 2011). Pressure is a

motivation to conduct fraud in which the social

status becomes a burden for someone in doing fraud

(Tuanakotta, 2007; Tunggal, 2011). In addition, the

rationalization is an important element in the

occurrence of fraud because the perpetrators seek for

the justification over their actions. Tunggal (2011)

described rationalization as the characters or ethics

that allow the management or workers to conduct

dishonest acts, living within a quite pressuring

environment, which made them to rationalize

dishonest actions.

2.2 Religiosity

Religiosity variable in this research used the grand

theory of Hamzah et al (2007). The reason of the

application of this grand theory was because the

religiosity concept in this theory is based on the

Islamic creed which its development was started

with grounded research on Muslim samples through

the comparison of religiosity theories exist before in

non-Muslim population. Added with the

development of religiosity dimensions in the theory

which started from qualitative studies toward

Islamic scholars which based on the concept that

religiosity of someone can be embodied through

three concepts, namely Islam (faith), Iman

(acceptance and belief) and Ihsan (the final goal of

the implementation of Islam and iman).

Hamzah et al. (2007) defined religiosity as the

level of religiousness of someone that is based on

the concept of Tawhid (Islamic monotheism). The

concept of Tawhid in Islam according to Hamzah et

al is aqidah (creed) and akhlak (morals). According

to Hamzah et al, aqidah illustrates how far

individuals have faith and comprehension on rukun

iman (the pillars of faith). In addition, akhlak

Religiosity and Fraud Activity in Acehnese Millennials Worker

199

describes how far individuals can act by reflecting

their obedience to Allah which associated with the

implementation of rukun islam (the pillars of Islam).

According to Hamzah et al (2007), religiosity

dimension consists of two aspect, namely Islamic

worldview, and religious personality (Muslim

personality). Islamic worldview is the knowledge

and perception regarding the pillars of faith (arkan

al-iman). The sub-dimensions of Islamic worldview

include 1) Creator-Creation, the awareness of

individuals regarding the presence of God and how

individuals are considered as close and connected to

the Creator; 2) Existence-Transcendence, spiritual

knowledge and comprehension of someone in

understanding every thing that happens as well as

the awareness of individuals on the reality of life,

both physical and spiritual according to the

perspective of Islam; 3) All-Encompassing Religion,

how someone implements Islamic teachings in their

daily lives (Hamzah et al, 2007).

The dimension of religious personality (Muslim

personality) is the trait and behavior showed by

someone, then, be evaluated by referring to Islamic

teachings and the obligation of humans in Islam (the

pillars of Islam) which are based on the direct

relationship of someone with Allah (worship). This

dimension is the elucidation of the pillars of Islam.

The sub-dimensions of religious personality

(Muslim personality) include 1) Self, the assessment

of internal condition (nafs) and external condition

(physical) of humans; 2) Social, the assessment

regarding the relationship of someone with Allah

which measured from the capability in

understanding and connecting with the social

environment; 3) Ritual, illustrating the direct

relationship of humans with Allah through worship

rituals according to the Islamic teachings (Hamzah

et al, 2007).

2.3 The Relationship Between

Religiosity and Fraud

Islamic sharia implemented in Aceh is the

implementation of customs that are upheld highly by

Acehnese which based on Islamic law. The Aceh’s

proverb (hadis maja) reads “adat ngon hukom

(agama) lage zat ngon sifeut” (customs and laws of

religion such as matters and natures) describes that

customs and religious laws in Aceh are inseparable

just like matters and natures. Every customary law

applies in Aceh comes from the law of Islam.

Acehnese has been internalized with Islamic culture,

therefore, they have high strength of religiosity

(Hartini, 2011). This matter is consistent with the

argument of Abubakar and Anwar (2011) which

explained that the implementation of Islamic sharia

in Aceh since the pace has developed the value of

religiosity within the people and be made as a norm

that regulates every individual act.

The habit of implementing Islamic sharia in the

daily life emerges high religiosity on Acehnese.

Jalaluddin (2002) elucidated religiosity as the

religious norm which generally used by people that

functions as social control in the process of

interaction. The argument above explained that

when a community has a high level of religiosity,

individuals will have a means of control over what is

allowed or prohibited socially. This condition

illustrates that religious individuals must know the

good things to do and the activities that must be left

behind because they are inappropriate according to

Islamic sharia.

Fraud is one of the crimes that harms a group of

individual, let alone the organization that employs

them. When an individual has a high level of

religiosity, he/she will avoid such behavior because

that individual knows that the action is prohibited by

God. This is because the individual has a control

system to restrain evil deeds. However, in reality,

Fraud cases were still found in Aceh. This

phenomenon is contradictory to the status of Islamic

sharia of the province in which the community has a

high level of religiosity.

Fraud itself according to Tuanakotta (2007)

might occur when there is an opportunity. In line

with this argument, Albrecht (2012) argued that the

main cause of fraud is because the perpetrator

notices a gap and gain an opportunity due to poor

control and monitoring systems. This opportunity

factor which makes individuals to have a desire to

conduct fraud and truly realize it. This occurrence of

the phenomenon high corruption rate among the

religious society in Aceh can be discussed through

the theory mentioned above. Therefore, the

hypothesis of this research was:

H1 : Religiosity affects the emergence of fraud

activities if it’s moderated by the opportunity to

conduct fraud.

3 RESEARCH METHOD

The sample collecting technique in this research was

a purposive sampling while the characteristics of the

subject in this research were (1) junior employees

who have been working for at least six months. The

limitation of the minimum period of service was

with an assumption that the employees have been

ICPsy 2019 - International Conference on Psychology

200

capable to adapt and assess their company

environment. (2) junior employees aged between 18-

36 years old who identical to generation Y. This

condition is consistent with the characteristics of

generation Y (millennial) which according to Howe

& Strauss (2000) is individuals born in 1982 to

2000. (3) having at least diploma degree, which

indicates that the subject can understand the scale

given by the researcher and the sophistication of

technology because they are educated. There were

138 research samples which later be analyzed

through a linear regression data analysis.

4 RESULT

4.1 Hypothesis Test

According to Table 1 below, it can be known that

the significance value of religiosity amounts to

0.522 (p>0.05). This result explains that if the

moderation variable is unavailable, thus, religiosity

wont affect the variable of fraud habit.

Table 1: Parameter Significance Test (Dependent

Variabel: Fraud Habit).

Model

Unstandardi

zed

Coefficients

Standardize

d

Coefficients

T

Sig.

B

Std.

Error

Beta

(Const

ant)

46

.2

60

9.953

4.648

.000

Religi

osity

-

0.

04

0

0.062

-0.055

-0.641

.522

4.1 The Test of Moderated Regression

Analysis

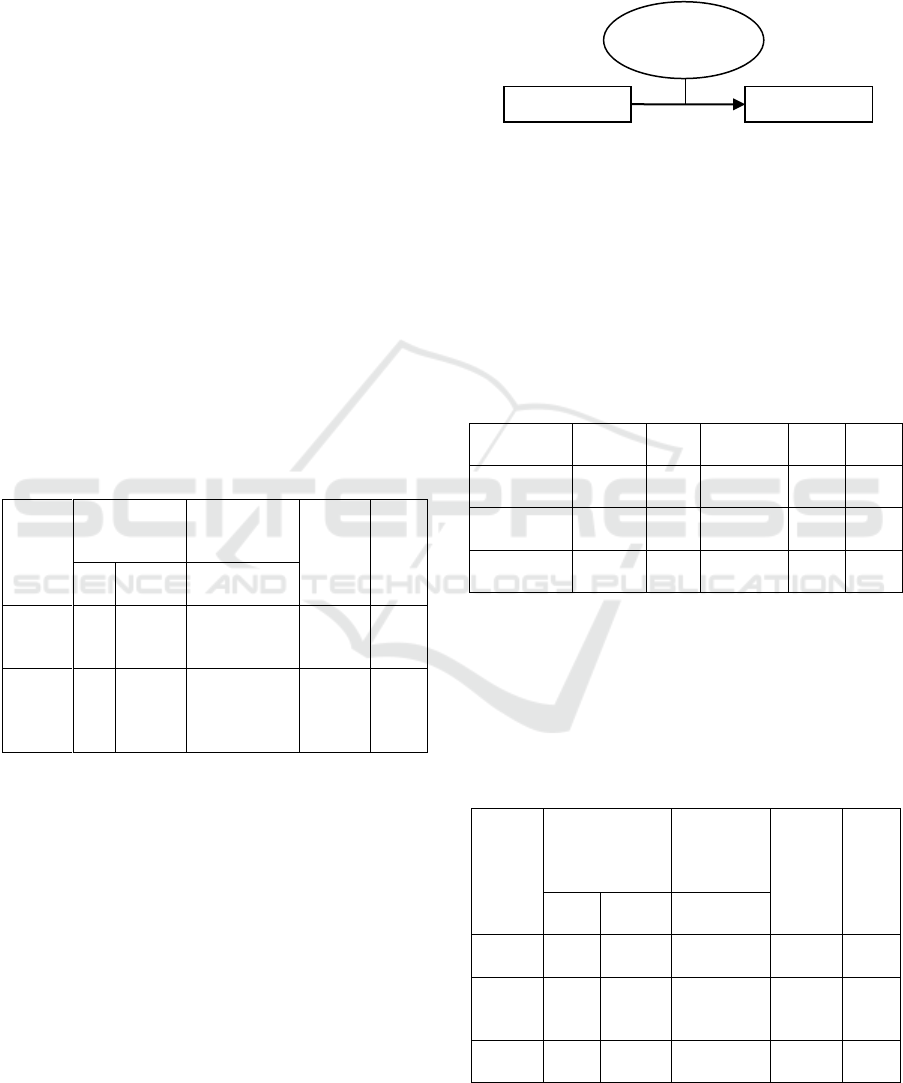

The test of moderated regression analysis is the

linear regression analysis in which the element of

interaction (the multiplication of two ore more

dependent variables) exists within the regression

formula named the product variable. The way to see

the moderation effect within the MRA formulation

statistically is through the significant role of the

product variable toward the dependent variable. The

variable tested through MRA in this research was

fraud opportunity. The variable of fraud opportunity

will be inspected if it can affect the relationship

between independent variable (religiosity) and

dependent variable (fraud habit). A variable will be

determined as moderating if the presence of such

variable will strengthen or weaken the relationship

between independent and dependent variables.

Figure 1: The Relationship of Religiosity toward Fraud

Habit with Fraud Opportunity as the Moderator.

According to Table 1, it can be known that the

value of F = 129.376, with 0.000 (p<0.05)

significance value, thus, it can be concluded that

they hypothesis is accepted. It means that the

variables of religiosity and fraud opportunity

generated simultaneous significant effect on fraud

habit variable.

Table 2: The Result of F-Test.

Model

Sum of

Square

Df

Mean

Square

F

Sig

Regression

15715.

296

3

5238.43

2

129.

376

.000

Residual

5425.6

61

134

40.490

Total

21140.

957

137

According to Table 3, it can be known that the

significance of fraud opportunity variable amounts

to 0.000 (p<0.05). This result elucidates that the

variable of fraud opportunity has a very significant

effect toward fraud habit.

Table 3: The Significance Test Result of Individual

Parameters (Dependent Variable: Fraud Habit).

Model

Unstandardiz-

ed

Coefficients

Standardiz

-ed

Coefficien

ts

T

Sig.

B

Std.

Error

Beta

(Const

ant)

44.8

51

5.212

8.605

.000

Religi

osity

-

0.04

3

0.032

-0.060

-1.355

.001

Opport

unity

0.26

0

0.014

1.814

18.72

7

.000

Fraud

Opportunity

Religiosity

Fraud Habit

Religiosity and Fraud Activity in Acehnese Millennials Worker

201

Table 4: The Correlation Result of Independent Variables

toward Dependent Variable.

Model

R

R

Adjusted

R Square

Std. Error of

the Estimate

1

0.862

0.743

0.738

6.363

Table 4 explains the effective contribution given

by religiosity and fraud opportunity variables toward

fraud habit. Based on 0.743 of R Square score, it can

be known that the contribution of religiosity variable

toward fraud habit which moderated by fraud

opportunity variable amounts to 74.3%.

Table 5: The Analysis of Variable Indicator.

Aspect/Indicator

Mean

High

Moderate

Low

Fraud

Opportunity

2

(mode

rate)

27

56

55

General

Information

52

62

57

37

Fraud Habit

Pressures

36.4

8

29

101

1. Keeping

Dignity

5.8

1

38

99

2. Self-Failure

8.15

3

56

79

3. External

Business

Factor

8.96

7

69

62

4. Adversity

7.26

3

37

98

5. Improving

status

4.59

3

14

121

6. Bad

Relationship

with

Supervisor

1.63

3

55

80

Rationalization

3.4

1

38

99

Religiosity

158.3

6

102

36

-

Islamic

Worldview

42.5

124

14

-

1. Creator –

Creation

17.28

112

26

-

2. Existence –

Transcendenc

e

13.34

121

17

3. All-

Encompassin

g Religion

11.95

80

58

-

Muslim

Personality

115.7

8

92

46

-

1. Self

38.81

62

76

-

2. Social

39.42

88

50

-

3. Ritual

42.58

85

53

-

According to Table 5, it can be seen that the

religiosity values of respondents are on a high

category (102 samples of 138 = 74%). This

condition illustrates the majority of the respondent

who are very religious. Respondents also have high

values for both religiosity variables, either Islamic

Worldview or Muslim Personality. However, the

smallest values on both sub-dimensions of

religiosity are the sub-dimension of all

encompassing religion (high = 80) in the dimensions

of Islamic worldview and the sub-dimension of self

(high = 62) in the dimension of Muslim personality.

The table above also explains that most of the

respondents experience the opportunity to conduct

fraud in moderate category (value = 2). This results

indicates that most of the respondents experience the

opportunity to conduct the act within their

organization despite the low category in conducting

fraud habit earned by the majority of the respondents

(seen from the majority of indicators on fraud habit

variable which are in the low category). This result

indicates the need of control system to inhibit the

growth of fraud within the organization by

considering the characteristic of respondents in this

research as junior employees who barely start

working but already have the opportunity in

conducting fraud. If respondents are getting used to

take the opportunity, it might be possible that they

will be more cunning in taking the chance once they

become the leader of the organization.

5 DISCUSSION

According to the results above, it is known that

religiosity did not moderate by the opportunity in

conducting fraud, did not associate with fraud

behavior. These findings are consistent with the

survey result of Lingkar Survey Indonesia (LSI) that

studied the relationship between the religiosity and

the act of corruption which produced a result that the

majority of respondents were quite religious and

mostly consider their religion when making a

decision (Putri, 2017). Based on this finding, LSI

mentioned that the meaning of religion and

ritualistic habit underwent by individuals only have

a significant relationship with the attitude of

respondents toward corruption, however, they were

not correlating with the act of corruption, more

religious only means more anti-corruption, the act of

corruption still continues and it has no relationship

with the matter of religion (Putri, 2017).

The findings above are consistent with the results

of this research if seen from the categorization of

ICPsy 2019 - International Conference on Psychology

202

religiosity variable of the respondents, no

respondents conceive low religiosity, all respondents

were in high and moderate levels. This condition

indicates that the level of religiosity of respondents

in running their routines according to the order of

religion is high. However, if seen from the

opportunity to conduct fraud, respondents were in

moderate category despite the fact that they are

junior employees who barely start their career within

the organization. It means that at the beginning of

their career, the opportunity to conduct fraud can be

felt already, let alone if they have the power within

the organization.

Akhrani (2019) explained that the personality of

corruptor experienced a split personality, therefore,

they behave in the opposite way from Tawhid which

made the word and action of the corruptor to be

inconsistent. According to the argument mentioned

above, it can be known that a thing that makes

individuals to conduct fraud is because they do not

act according to what they know because there is a

split of personality within themselves. On the other

side, Ismail (2012) described that there are two

theoretical studies of psychology of religion which

can discuss the act of corruption, namely the

religious orientation and psychographic. According

to Ismail (2012), the religious orientation of

corruptor is an extrinsic religiosity, namely people

who live or use the religion they embraced, thus,

they tend to use religion for their self-interest. Ismail

in this research affirmed that this extrinsic

orientation is religious due to the presence of a

reinforcement that attracts the participation in the

religion in which if this reinforcement is cease to

exist, they will leave religion for the sake of

themselves.

If examined through psychographic theory of

Ismail (2012), there are five dimensions of

religiosity exist in psychographic theory, namely

dimension of ideology, dimension of ritualistic,

dimension of intellectual, dimension of experiential,

and dimension of consequential. Ideological,

ritualistic, and intellectual dimensions are owned by

every religious person because they related to the

doctrine of religion which differs the embraced

religion with others, what should be done and what

to avoid as well as the ritual that should be

performed (Ismail 2012). However, according to

Ismail (2012), experiential dimension and

consequential dimension are the deeper dimensions

of the three dimensions mentioned above that

differentiate between becoming religious and

devout. The experiential dimension is associated

with the religious experience of someone in the daily

life, if someone has been strong with the three

dimensions above but has the opportunity to conduct

a corruption, he/she will ignore the opportunity, it

means that religiosity has become the part of his/her

life experience and he/she has done good deeds

toward anyone at anytime (Ismail, 2012). In

addition, the consequential dimension is associated

with the effect of someone in becoming religious

within their daily life, and is the highest dimension

in embracing a religion (Ismail, 2012). According to

Ismail, when individuals aware that caring toward

poor people is the mission of the teaching of

religion, thus, they will avoid conducting corruption

no matter how small it is.

According to the explanation of two researchers

above, it can be known that individuals conduct

fraud amidst themselves who conceive religious

values because the religiosity dimension is yet to be

high. Those individuals are still on the phases of

knowing and comprehending religious teachings, but

yet to achieve the phase of implementing experience

and understanding the consequences of becoming a

religious person. Another word to describe the

religiosity value of Acehnese millennial workers is

that they still have an extrinsic religiosity

orientation. The characteristic of extrinsic religiosity

value is having a religious reason due to the

strengthening factor outside themselves in which

when the factor is vanished, thus, they will remove

the religiosity itself.

By considering that the religiosity of Acehnese

has been present since a long time ago, growth and

developed into the custom believed by Acehnese.

This condition can describe that the religiosity value

of Acehnese is extrinsic-oriented. Islamic teachings

are passed down when individuals are still children

through Quran recitals which eventually informing

the community to know what is allowed and what is

prohibited based on the teaching of Islam. This

condition which provide the information from the

data of research results that the respondents own

very high values for social and ritual on the sub-

dimension of Muslim personality within the

religiosity dimension. On the other side, this

research resulted in self dimension as the dimension

with the smallest value between the those three. This

result also consistent with the arguments of the

researchers mentioned above who related the

absence of intrinsic orientation or experiential and

consequential dimensions on the religiosity level of

corruptors. This result which made LSI to conclude

that the religiosity of someone in conducting

religious orders only toward the state of

Religiosity and Fraud Activity in Acehnese Millennials Worker

203

respondents’ behavior to be anti-corruption but not

correlated to the corruption habit.

When the level of individual religiosity is yet to

achieve the experiential and consequential phases

(or external-oriented religiosity), thus, when the

opportunity to conduct fraud occurs, the religious

values (ideological, ritualistic, intellectual

dimensions) are seemed to disappeared. It is known

that fraud mostly occurs because the perpetrator

notices the gap and gains the opportunity due to poor

control and supervision systems. The opportunity

factor makes individuals to have a desire in

conducting fraud and truly realize it (Albrecht,

2012). Considering that the most contributing thing

in causing someone to conduct fraud is the

opportunity, when the religiosity value of

individuals only reaches the phase of knowing what

good and bad, and conducting prayers, the

individuals will still be tempted to take the

opportunity. They apparently forget the

consequences that have to be taken by individuals

with a high religiosity level, or the grace of religious

experience that will be acquired when doing the

deeds ordered by God.

Eventually, this condition will emerge a

rationalization as if what they do wouldn’t be

categorized as wrong. Rationalization is one of the

dimensions of fraud habit as the most important

element in the occurrence of fraud, which assessed

from the characters or ethics that allow the

managements or workers to conduct dishonest acts,

living in a quite pressuring environment, and

causing them to rationalize dishonest actions

(Tunggal 2011). A control system that is referring to

the intrinsic value of individuals in protecting

themselves from the emergence of fraud opportunity

is required. The most proper way is through the

improvement of religious value of experiential and

consequential religiosity of someone.

Ruankaew (2016) examined the dimensions of

the fraud triangle, and added another dimension to

the fraud triangle which according to him was the

cause of fraud, namely capacity. Ruankaew defines

capacity as the position or function a person has in a

company that can give him the ability to create or

exploit fraud opportunities that no one else has.

Based on this definition it is known that just having

an opportunity alone cannot strengthen the presence

of fraud, but when someone has the capacity such as

the authority and responsibility for a position that

has an opportunity to commit fraud, it will lead to

fraud behavior on the individual.

Internal control can stem this dimension of

capacity or position. Suryandari, Yuesti, and

Suryawan (2019) explained that the opportunity

would lead to fraud due to weak internal control and

poor supervision management. When the

management of supervision is good, even though the

position and capacity are as good as any with great

authority, the individual will be responsible for that

authority, because the individual is aware that he is

always under internal supervision and will not

commit fraud. This is in accordance with the opinion

of Skousen et al (2009) which explains the

opportunity factors can be filtered through effective

monitoring in every organizational structure in the

organization.

6 CONCLUSION

According to the research results, it can be known

that the religiosity value of Acehnese millennial

workers is only limited to knowing and

understanding their religion, aware of allowed and

prohibited things taught by their religion, and doing

the ritual ordered by their religion. However, it is yet

to reach the phase of implementing the experiential

religiosity to the consequences owned by a religious

person. This condition that cause them to still take

the opportunity of conducting fraud despite the high

religiosity value. This result indicates that religiosity

is not associated with fraud habit, however, if

opportunity exists as the moderating variable, thus,

the two variables are not correlated. This research

suggest the importance of establishing an intrinsic

self control system with the enforcement of

religiosity experiential and consequential values.

This effort is aimed for the individuals to be able of

resisting the temptation despite the existing

opportunity in conducting fraud.

This research has some limitations. The variables

used in this research have low objectiveness level

when they are performed through a quantification

method. This condition might occur because the

subjects can hide the actual information related to

themselves due to the sensitive variables used in this

research. A qualitative method such as in-depth

interview combined with intense observations will

acquire the actual habit regarding fraud and the

religiosity.

REFERENCES

Abubakar, & Anwar. (2011). Strategi dan hambatan

penerapan Qanun Khalwat dalam pencegahan perilaku

ICPsy 2019 - International Conference on Psychology

204

Khalwat remaja kota Banda Aceh. Jurnal Pendidikan

Serambi Ilmu, 9(2), 1-75.

Akhrani, L. A. (2019). Dapatkah Religiusitas

Menyelamatkan Anggota Partai Politik dari Jeratan

Korupsi? Kajian Religiusitas terhadap Sikap Korupsi

Anggota Partai Politik. Interaktif: Jurnal Ilmu-Ilmu

Sosial, 11(1), 69-92.

Albrecht, W., et.al. 2012. Fraud Examination.

Connecticut: Cengage Learning.

Amawidyati, S. A. G., & Utami, M. S. (2007). Religiusitas

dan psychological well

‐

being pada korban gempa.

Jurnal Psikologi, 34(2), 164 – 176.

Bakri (2017, April 27). Lima Karyawan Bank Aceh

Ditahan [Halaman web] diakses dari

https://aceh.tribunnews.com/2017/04/27/lima-

karyawan-bank-aceh-ditahan.

Hamzah, A., Krauss, S.E., Noh, S.M., Suandi, T., Juhari,

R., Manap, J., Mastor, K.A., dkk. (2007). Muslim

religiosity & personality assessment: Prototype for

nation building. Malaysia: Institut Pengajian Sains

Sosial.

Hartini, N. (2011). Remaja Nanggroe Aceh Darussalam

pasca Tsunami. Jurnal Psikologi, 24(1), 45-51.

Howe, N., & Strauss, W. (2000). Millennials rising: The

next great generation. Vintage.

Ibrahim, A. (2019, Desember 22). Peraturan Perundang-

undangan tentang Pelaksanaan Syariat Islam di Aceh

[Halaman web] diakses dari https://ms-

aceh.go.id/berita1/artikel/183-peraturan-perundang-

undangan-tentang-pelaksanaan-syariat-islam-di-

aceh.html

Ismail, R. (2012). Keberagamaan Koruptor Menurut

Psikologi (Tinjauan Orientasi Keagamaan dan

Psikografi Agama). ESENSIA: Jurnal Ilmu-Ilmu

Ushuluddin, 13(2), 289-304.

Ismail, Z., & Desmukh, S. (2012). Religiosity and

psychological well-being. Journal of Business and

Social Science, 11(3), 20-28.

Jalaluddin. (2002). Psikologi agama. Jakarta: Raja

Grafindo Persada.

Lubis, F. H., & Marlina, M. (2010). Penegakan Hukum

dalam Tindak Pidana Korupsi Pengadaan Barang dan

Jasa (Studi pada Pengadilan Negeri Kuala

Simpang). JURNAL MERCATORIA, 3(2), 88-101.

Maulana, Z. (2016). Persepsi Masyarakat terhadap Faktor-

faktor yang Mempengaruhi Korupsi Anggaran

Pendapatan Belanja Daerah (APBD) di Aceh

Utara. Jurnal Manajemen dan Keuangan, 5(2), 573-

581.

Nazar, M. (2018, Agustus 1). Polisi Ungkap 422 Kasus

Kejahatan di Pidie, Kasus Penipuan Ranking Pertama

[Halaman Web] diakses dari

https://aceh.tribunnews.com/2018/08/01/polisi-

ungkap-422-kasus-kejahatan-di-pidie-kasus-penipuan-

rangking-pertama.

Putri, B. U. (2019, Desember 26). Survei : Tidak Ada

Hubungan Tingkat Kesalehan dan Perilaku Korupsi

[Halaman Web] diakses dari

https://nasional.tempo.co/read/1034127/survei-tak-

ada-hubungan-tingkat-kesalehan-dan-perilaku-korupsi

Ruankaew, T. (2016). Beyond the fraud

diamond. International Journal of Business

Management and Economic Research (IJBMER), 7(1),

474-476.

Shamim, S., Cang, S., Yu, H., & Li, Y. (2017). Examining

the feasibilities of Industry 4.0 for the hospitality

sector with the lens of management

practice. Energies, 10(4), 499.

Skousen, Christopher J., Kevin R. Smith, and Charlotte J.

Wright. 2009. “Detecting and Predicting Financial

Statement Fraud: The Effectiveness of The Fraud

Triangle and SAS No.99”. Journal of Advances in

Financial Economics, Vol. 13, pp. 53-81.

Surya, A. (2018). Problematika Penyidik Dalam

Penetapan Tersangka Tindak Pidana Korupsi Dana

Desa Di Kabupaten Aceh Tengah. RESAM Jurnal

Hukum, 4(1), 1-16.

Tuanakotta, T.M. (2007). Akuntansi Forensik dan Audit

Investigasi. Jakarta : Salemba Empat.

Tunggal, Amin Widjaja. (2011). Financial Fraud : Teori

dan Kasus. Jakarta : Harvarindo.

Wahidah (2015). Pemikiran Hukum Hazairin. Syariah

Jurnal Ilmu Hukum, 15(1), 37-50.

Religiosity and Fraud Activity in Acehnese Millennials Worker

205