Audit Quality Shows the Capability of Auditors in Detecting

Corruption: A Study of BPK Auditors of the Republic of Indonesia

Rahima Br. Purba

1

, Erlina

2

, Haryono Umar

3

, Iskandar Muda

4

1

Department of Accounting, University of North Sumatra, Jl. Prof. T.M Hanafiah, SH, USU Campus, Medan, Indonesia

2

Department of Accounting, University of North Sumatra, Jl. Prof. T.M Hanafiah, SH, USU Campus, Medan, Indonesia

3

Departement of Accounting, Perbanas Institute, Jl. Perbanas, Karet Kuningan Setiabudi, Jakarta, Indonesia

4

Department of Accounting, University of North Sumatra, Jl. Prof. T.M Hanafiah, SH, USU Campus, Medan, Indonesia

Keywords: Audit Quality, Corruption Detection, Audit

Abstract: Reflected in the Standar Pemeriksaan Keuangan Negara, auditors of the Badan Pemeriksa Keuangan have the

freedom and independence in planning, implementing, reporting, and monitoring the follow-up of audit

results. The ability to detect corruption is very necessary for each BPK RI auditor because if an auditor has

conducted an audit properly then they also cannot provide the right audit results. This study provides results

that the Auditor who conducts the audit in accordance with applicable regulations (audit quality) can

demonstrate the ability of auditors to detect corruption.

1 INTRODUCTION

1.1 Background

Audit has a very important position in believing that

the policy implementation has been as expected. In

this rapid development, the supervisory function

does not merely provide input on whether the

implementation is in accordance with the plan, but

also provides more useful inputs, among others,

monitoring activities are able to provide oversight

information, including in the field of planning,

whether the plans made are still relevant with the

existing environmental conditions, as well as other

information services needed for the implementation

of government management activities, as well as in

realizing good governance.

The Standar Pemeriksaan Keuangan Negara

(SPKN) state that the Republic of Indonesia Supreme

Audit Board (BPK) has the freedom and

independence in planning, implementing, reporting,

and monitoring the follow-up of the audit results

(Finance & Indonesia Audit Board, 2017). The role

of the audit is very important for the achievement of

the success and progress of the organization through

comparing the existing conditions with those that

should. If it turns out to be found irregularities

immediately taken corrective action. As part of the

management function, supervision is needed to help

management in three ways, namely: (1) improving

organizational performance, (2) giving opinions on

organizational performance and (3) directing

management to make corrections to the problems of

achieving existing performance (Herbert, 1977).

The condition of corruption in Indonesia can be

seen from a variety of sources, one of which is

Transparency International (TI), an international

Anti-Corruption community organization that issues

the country's Corruption Perception Index (CPI) or

Corruption Perception Index (CPI). CPI is a

composite index that measures the level of perception

of corruption in the public sector in countries in the

world. CPI is used by comparing the conditions of

corruption in one country against another country.

The development of the CPI in Indonesia in the last

five years shows that Indonesia is the 80 most corrupt

country in the world and for the ASEAN region,

Indonesia is still seen as a country that is prone to

corruption or the number 2 most corrupt compared to

neighboring countries (Indonesia International

Transparency, 2015).

466

Purba, R., Erlina, ., Umar, H. and Muda, I.

Audit Quality Shows the Capability of Auditors in Detecting Corruption: A Study of BPK Auditors of the Republic of Indonesia.

DOI: 10.5220/0009216304660472

In Proceedings of the 2nd Economics and Business International Conference (EBIC 2019) - Economics and Business in Industrial Revolution 4.0, pages 466-472

ISBN: 978-989-758-498-5

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Table 1.1. Corruption Crimes Based on Agencies

Agency

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Total

DPR and DPRD 0 0 0 0 7 10 7 2 6 2 2 3 15 9 4 67

Ministry /

Institution

1 5 10 12 13 13 16 23 18 46 26 21 39 31 47 321

BUMN/BUMD 0 4 0 0 2 5 7 3 1 0 0 5 11 13 5 56

Commission 0 9 4 2 2 0 2 1 0 0 0 0 0 0 0 20

Provincial

g

overnment

1 1 9 2 5 4 0 3 13 4 11 18 13 15 29 128

Regency / City

Government

0 0 4 8 18 5 8 7 10 18 19 10 21 53 114 295

Jumlah 2 19 27 24 47 37 40 39 48 70 58 57 99 121 199 887

Source: https://www.kpk.go.id/en/statistik/makakan/tpk-based-instantsi

Table 1.1. said that the highest number of

corruption cases in Indonesia from 2004 to 2018

occurred in the ministries and institutions (Corruption

Eradication Commission, 2010-2015). Many

government agencies in Indonesia get the best

opinion. However, throughout the 2000s they were

exposed to corruption cases.

A number of opinions obtained by a number of

ministries in Indonesia get the best audit results. But

not with the conditions occurring within the ministry

itself. Conditions of ongoing corruption. If viewed

from the perspective of audit quality, the ministry has

obtained the best results, but has not shown the

quality of the audit results themselves. This is in line

with research conducted by (Heriningsih & Marita,

2013) which states that BPK's audit opinion does not

affect the level of corruption. So it can be interpreted

that no matter how good the opinions obtained by the

auditee will not show a decreasing level of corruption.

The ability to detect corruption is one of the

factors that influence the quality of audit results

(Abdallah, Maarof, & Zainal, 2016). The auditor is

responsible for detecting corruption in the audited

financial statements and can communicate to

interested parties, if they find indications of fraud in

the financial statements. Detecting corruption is an

action to find out that corruption occurs, who is the

culprit, who is the victim, and what causes it.

Detecting corruption is not easy, because it requires

expertise in the process. Many cases occur due to the

fact that auditors of public accounting firms cannot

find misstatements or cannot detect corruption during

their auditing duties. This has a detrimental impact on

both the client and the auditor itself.

The cases that occurred above are evidence of the

auditor's failure to detect fraud. This failure has a

detrimental impact on business people. Detecting

corruption is very important, because if an auditor can

detect corruption, then the financial information

generated in the audited financial statements will be

relevant and reliable. Thus, decision making taken for

external and internal parties, will not be wrong and

the company can continue to grow in the future. If an

auditor cannot detect the fraud, then the decision

making will be wrong, which impacts on the

company's losses as well as the company's reputation

at stake. In addition, the public will also doubt the

level of ability and professionalism of the auditors in

detecting corruption in the financial statements. The

failure of auditors in detecting corruption is due to the

inability to collect relevant evidence (Purwanti &

Astika, 2017). The failure can be caused by several

factors that can influence the auditor in detecting

corruption, such as lack of auditor competence, low

auditor independence, high time pressure faced by the

auditor, lack of auditor skepticism when finding

indications of corruption, and low auditor

commitment to the place he works so the auditor is

difficult to detect corruption that occurs in the client

company.

The types of audits conducted by BPK-RI include

financial audits, performance audits, and audits with

specific objectives. With the implementation of the

audit, there have been many changes related to the

management of state and regional finances shown by

the increasing number of Ministries, Institutions,

Regional Governments, and even the Central

Government that obtained the Fair Without Exception

(WTP) opinion. However, audit findings in the form

of administration, ethics, and law have been

increasing in number over the years and cannot be

followed up on by auditees (Ministries, Institutions,

Regional Governments, Central Governments,

BUMN and BUMD).

This shows that the quality of audit results is still

inadequate, and one of the reasons is the inability of

Audit Quality Shows the Capability of Auditors in Detecting Corruption: A Study of BPK Auditors of the Republic of Indonesia

467

auditors to detect corruption as indicated by the

existence of several auditees who obtain WTP

opinion as corruptors by law enforcement officials.

1.2 Formulation of the Problem

The problem formulation of this research is whether

audit quality shows the auditor's ability to detect

corruption?

1.3 Research Purposes

The aim of this research is to analyze how audit

quality shows the auditor's ability to detect

corruption.

2 LITERATURE REVIEW

2.1 Theoretical Review

Attribution theory explains a process of how to

determine causes and motives about a person's

behavior (Gibson, 1994). This theory is increasingly

developed by explaining ways in assessing people

differently, depending on what meaning is attributed

(attributed) to a certain behavior (Kelly, 1972,

Robbins and Judge, 2008). The theory also refers to

how a person explains the causes of other people's

behavior or his own personality which will be

determined whether from internal or external and how

they affect individual behavior (Luthans, 1998). This

theory also explains the understanding of a person's

reaction to events around them, by knowing their

various reasons for the events experienced. In the

Correspondent Inference attribution theory (Edward

Jones and Keith Davis) explained that there are

behaviors related to the attitudes and characteristics

of individuals, it can be said that only seeing their

behavior will be known to brush and characteristics

of the person and can also predict someone's behavior

in dealing with certain situations . Steers (1977) and

Reed (1994) state that the existence of "attributes",

will naturally apply internally in an organization that

will affect employee attitudes especially those that

will be related to their work and organizational

commitment. This theory is closely related to the

ability of auditors to uncover corrupt acts. In exposing

corruption, the ability of auditors is influenced by

various factors. Attribution theory is also related to

how people judge the extent of the auditor's ability to

reveal corruption. Disclosure of these criminal acts of

corruption can be seen from whether the auditor is

able to provide evidence to encourage confidence

about the truth or error of each statement of an issue.

2.2 Audit Quality

Audit quality is a concept that has many different

dimensions. Evidenced by the many studies that use

this variable with different dimensions. According to

DeAngelo (DeAngelo, 1981) audit quality is the

ability of auditors to detect errors in financial reports

and report them to users of financial statements.

According to (Lowensohn, Johnson, & Elder, 2005;

Setyaningrum, 2012) audit quality can be measured

by three approaches, namely (1) using audit quality

proxies, for example auditor size (Mansi, Maxwell, &

Miller, 2004), earnings quality (Kim , 2002), the

reputation of KAP (Beatty, 1989), the amount of audit

fees (Ward, Elder, & Kattelus, 1994), the existence of

lawsuits at the audlitor (Palmrose, 1988), and others;

(2) A direct approach, for example the audit process

carried out to what extent the KAP's adherence to

audit audit standards (O'Keefe, Simunic, & Stein,

1994); (3) Using perceptions from various parties

towards the audit process carried out by KAP

(Carcello, 1992). Deis and Giroux (1992), using the

Metric variable (QUALITY) which is measured

based on the results of Quality Control Review

(QCR) (Donald R. Deis & Giroux, 1992). In the

context of the Indonesian government sector, it uses

the first approach summarized by Lowensohn

(Lowensohn et al., 2005). According to (Jr. &

Walker, 1999) audit quality is related to the

professional behavior of an auditor. An auditor's

professionalism can be seen in terms of technical

abilities, knowledge, experience, and technological

expertise.

2.3 Corruption Detection

Auditing is directed to be able to detect fraud

(Singleton, Singleton, Bologna, & Lindquist, 2006).

In SAS 99 - Consideration of Fraud in a Financial

Statement Audit (AICPA, 2002b) stated that auditors

are required to submit fraud in the financial

statements. Documentation contains fraud risk, both

individually and in combination which has a

significant impact on the risk of financial statement

misstatement.

According to (CO Albrecht, 2008) there are 6

(six) signs of fraud, namely: (1) the peculiarities of

accounting, (2) weaknesses of internal control, (3)

irregularities / anomalies of analysis, (4) excessive

lifestyle, (5) unusual behavior, (6) complaints.

Deviations and corruption occur because there is

EBIC 2019 - Economics and Business International Conference 2019

468

power that is abused or the authority exercised is not

in accordance with the mandate that should be. Abuse

of power is carried out for personal or group gain and

will usually be followed by violation of the law.

Inappropriate practice by those who do not pay

attention to good and right measures and only

prioritize the interests of themselves or their own

groups.

In this condition it is stated that the perpetrators

of corruption and other violations have lost the values

of integrity that should be upheld as well as possible

in any condition, anytime, anywhere. Those who

commit acts of corruption are caused by open

opportunities, by pressure, accompanied by

rationalization, and by the power they have because

they have lost the main grip in thinking and acting,

that is integrity.

On the basis of this (Umar, 2016) adds one

element, namely Lack of Integrity (Lack of Integrity)

again the cause of corruption, it can be called the

Fraud Star. Umar said those who commit corruption

might be said to have experienced mental problems.

Since corruption is a crime, corruptors can be called

criminals.

2.4 Conceptual Framework and

Hypothesis

The following is the conceptual framework of this

research.

Figure 2.1. Research Conceptual Framework

The information system is a collection of

resources related to achieving certain goals. All

interrelated resources within an organization will

form a system in the organization (Bodnar &

Hopwood, 2013). Information quality is the quality of

output in the form of information produced by

information systems and used in decision making.

Information quality has several characteristics

namely relevant, timely, accurate, complete and

concise (Rai, Lang, & Welker, 2002).

Setyaningrum states in his research, an indicator

of audit quality is the value of audit findings

(Setyaningrum, 2012) based on research (DeAngelo,

1981) which states that the value of audit findings

shows the ability of BPK auditors in detecting errors

in local government financial statements.

Although the auditor has received education, has

competence, and has experience coupled with being

required by various regulations including SAS 99

(AICPA, 2002a) which states that auditors and

auditees must brainstorm to discuss any possible

frauds in the auditee's financial statements. The goal

is first so that the auditor can share experience with

the auditee about how fraud can be done and hidden.

The second is to convey tone at the top or a general

description of the audit conducted. The auditor must

also collect information related to fraud risk in the

financial statements. More precisely SAS 99 provides

guidance for auditors on how to identify / evaluate

fraud risk in financial statements. The auditor must

also pay attention to areas that are at risk of fraud.

H1: Audit quality shows the ability of auditors to

detect corruption

3 METHOD

This type of research is a causal design with a bergina

design to analyze the relationships between one

variable with another variable, or how a variable

affects other variables (Sugiyono, 2016).

The operational definition of variables is

intended to clarify the variables that will be examined

where the main problems of this study are:

1. Audit Quality (X) is an audit process that starts

from planning, implementation, up to reporting

can be ensured to really focus according to the

rules and ensure that there is control or

supervision in the process (Ball, Tyler, & Wells,

2015; Dickins , Johnson-Snyder, & Reisch, 2018;

Futri & Juliarsa, 2014; Pitanen, 2016; Sulaiman,

2011; The Institute of Chartered Accountants in

England & Wales, 2002; Zahmatkesh &

Rezazadeh, 2017). This variable uses the interval

scale.

2. Corruption Detection (Y) is the auditor must be

able to assess that there are errors and

irregularities that may cause financial reports to

contain material misstatements (AICPA, 2002a;

WS Albrecht, Albrecht, Albrecht, & Zimbelman,

2012; Hillison, Pacini, & Sinason, 1999; Koroy,

2008; Umar, 2012, 2016; Wilks & Zimbelman,

2004; Zimbelman, 1997).

Audit Quality Shows the Capability of Auditors in Detecting Corruption: A Study of BPK Auditors of the Republic of Indonesia

469

This variable uses the interval scale.

The population of this research is all auditors in

the Republic of Indonesia Supreme Audit Board. The

sampling technique used is convenience sampling

where the minimum sampling is 50 questionnaires.

The distribution of questionnaires was carried out by

1242 people (to BPK auditors who were spread across

all representatives). However, the returned

questionnaire was 99 respondents. The data collection

technique is a survey that is through a media

questionnaire that is made online through the Google

form site that is spread via office email and also

through social media applications namely Whatsapp.

Data analysis techniques used are using Structural

Equation Model (SEM) analysis using statistical tools

SmartPLS (Latan & Ghazali, 2017).

4 RESULT AND DISCUSSION

4.1 Research Result

4.1.1 Outer Model Evaluation

(Measurement Model)

Validity Test based on Outer Loading Value and

Average Variance Extract (AVE). The following are

the results of the vaccination and reliability test based

on outer Loading, Average Variance Extracted (AVE)

and Cronbach’s Alpha (CA) and Composite

Reliability (CR)

Table. 4.1. the results of vaccination and reliability test

based on outer Loading, Average Variance Extracted

(AVE) and Cronbach’s Alpha (CA) and Composite

Reliability (CR).

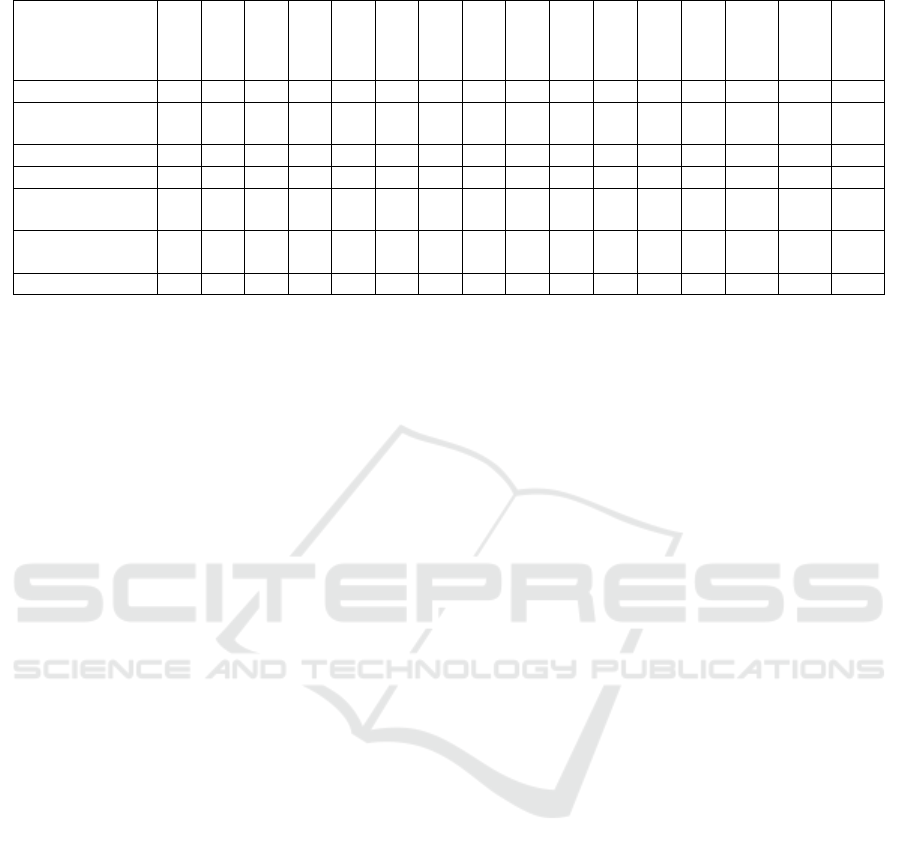

Indikator Outer Loading AVE CA CR

KA1 0.891

0.774 0.982 0.983

KA2 0.899

KA3 0.89

KA4 0.889

KA5 0.912

KA6 0.926

KA7 0.894

KA8 0.927

KA9 0.892

KA10 0.798

KA11 0.922

KA12 0.869

KA13 0.888

KA14 0.878

KA15 0.856

KA16 0.779

KA17 0.828

DK1

0.855

0.806 0.984 0.985

DK2

0.823

DK3

0.863

DK4

0.732

DK5

0.893

DK6

0.905

DK7

0.922

DK8

0.933

DK9

0.916

DK10

0.945

DK11

0.918

DK12

0.945

DK13

0.892

DK14

0.925

DK15

0.93

DK16

0.944

Based on the results of testing the validity of using

the outer loading value in table 4.1. the results

obtained are all loading values> 0.4, which means

they have met the validity requirements based on the

loading value.

4.1.2 Hypothesis Testing Direct Effect (Inner

Model)

The following is the path coefficient value and the P-

Values value for testing the significance of direct

effects.

Table 4.2. Testing the Significance of Direct Effects

Relationshi

p

Path

Coefficient

T-

Statistics

P-

Values

KA -> DK 0.337 2.497 0.013

Figure 4.1 Testing the Significance of Direct Effects

(Dirrect Effect)

Based on Table 4.2 and Figure 4.1, the path

coefficient value from DK to DK is positive, which is

0.337. Because the value of the path coefficient is

positive, it means that the train has a positive effect

on DK. known value of P-Values KA to DK 0.013

EBIC 2019 - Economics and Business International Conference 2019

470

<0.05, then KA has a positive and significant effect

on DK.

Thus it can be concluded that the hypothesis is

accepted, namely audit quality shows the auditor's

ability to detect corruption.

4.2 Discussion

The results of the study stated that audit quality shows

the ability of auditors to detect corruption. In line with

what setyaningrum stated that the audit quality

indicator is the value of audit findings (Setyaningrum,

2012), which is based on research (DeAngelo, 1981)

which states the value of audit findings shows the

ability of BPK auditors to detect corruption. Although

the auditor has received education, has competence,

and has experience coupled with being required by

various regulations including SAS 99 (AICPA,

2002a) which states that auditors and auditees must

brainstorm to discuss any possible frauds in the

auditee's financial statements. The goal is first so that

the auditor can share experience with the auditee

about how fraud can be done and hidden. The second

is to convey tone at the top or a general description of

the audit conducted. The auditor must also collect

information related to fraud risk in the financial

statements. More precisely SAS 99 provides guidance

for auditors on how to identify / evaluate fraud risk in

financial statements. The auditor must also pay

attention to areas that are at risk of fraud.

The ability to detect corruption is one of the

factors that influence the quality of audit results

(Abdallah et al., 2016). The auditor is responsible for

detecting corruption in the audited financial

statements and can communicate to interested parties,

if they find indications of fraud in the financial

statements. Detecting corruption is an action to find

out that corruption occurs, who is the culprit, who is

the victim, and what causes it. Detecting corruption is

not easy, because it requires expertise in the process.

Many cases occur due to the fact that auditors of

public accounting firms cannot find misstatements or

cannot detect corruption during their auditing duties.

This has a detrimental impact on both the client and

the auditor itself.

By using the Fraud Star Model (Pressure,

Opportunity, Justification, Ability, and Loss of

Integrity), auditors can understand how to detect

corruption.

5 CONCLUSIONS

Based on the analysis and discussion as well as the

test results in this study, it can be concluded that the

quality of the audit shows the ability of BPK auditors

of the Republic of Indonesia in detecting corruption.

This gives meaning that if the audit that we do is in

accordance with the guidelines starting from the pre-

planning, planning, implementation, and reporting

stages with discipline, the auditor is able to detect

corruption. In addition, with the ability of auditors to

detect corruption, the possibility of creating quality

audit results will increase.

REFERENCES

Abdallah, A., Maarof, M. A., & Zainal, A. (2016). Fraud

detection system: A survey. Journal of Network and

Computer Applications.

https://doi.org/10.1016/j.jnca.2016.04.007

AICPA. (2002a). AU Section 316 Consideration of Fraud

in a Financial. In October (pp. 167–218).

AICPA. (2002b). Statement on Auditing Standards: SAS

No. 99. AU Section 316, Consideration of Fraud in a

Financial Statement Audit. Retrieved from

http://www.aicpa.org/Research/Standards/AuditAttest/

DownloadableDocuments/AU-00316.pdf

Albrecht, C. O. (2008). International Fraud : A

Management Perspective.

Albrecht, W. S., Albrecht, C. O., Albrecht, C. C., &

Zimbelman, M. F. (2012). Fraud Examination. South-

Western Cengage Learning.

https://doi.org/10.1017/CBO9781107415324.004

Badan Pemeriksa Keuangan, & Indonesia, R. (2017).

Standar Pemeriksaan Keuangan Negara.

Ball, F., Tyler, J., & Wells, P. (2015). Is audit quality

impacted by auditor relationships? Journal of

Contemporary Accounting & Economics.

https://doi.org/10.1016/j.jcae.2015.05.002

Beatty, R. P. (1989). Auditor Reputation and the Pricing of

Public Offerings. The Accounting Review, 64(4), 693–

709.

Bodnar, G. H., & Hopwood, W. S. (2013). Accounting

Information Systems.

DeAngelo, L. E. (1981). Auditor Size And Audit Quality.

Journal of Accounting and Economics, 3(3), 183–199.

https://doi.org/10.1016/0165-4101(81)90002-1

Dickins, D., Johnson-Snyder, A. J., & Reisch, J. T. (2018).

Selecting an auditor for Bradco using indicators of audit

quality. Journal of Accounting Education, (July), 0–1.

https://doi.org/10.1016/j.jaccedu.2018.07.001

Donald R. Deis, J., & Giroux, G. A. (1992). Determinants

of Audit Quality in the Public Sector. The Accounting

Review, 67(3), 462–479. Retrieved from

http://www.jstor.org/stable/247972%5Cnhttp://www.js

tor.org/page/info/about/policies/terms.jsp

Audit Quality Shows the Capability of Auditors in Detecting Corruption: A Study of BPK Auditors of the Republic of Indonesia

471

Futri, P. S., & Juliarsa, G. (2014). Pengaruh Independensi,

Profesionalisme, Tingkat Pendidikan, Etika Profesi,

Pengalaman, dan Kepuasan Kerja Auditor Pada

Kualitas Audit Kantor Akuntan Publik di Bali. E-Jurnal

Akuntansi Universitas Udayana, 7, 444–461.

Herbert, L. (1977). Performance Auditing. Performance

Auditing.

Heriningsih, S., & Marita. (2013). Pengaruh Opini Audit

dan Kinerja Keuangan Pemerintah Daerah terhadap

Tingkat Korupsi Pemerintah Daerah (Studi Empiris

pada Pemerintah Kabupaten dan Kota di Pulau Jawa).

Buletin Ekonomi, 11(1), 1–86.

https://doi.org/10.1017/CBO9781107415324.004

Hillison, W., Pacini, C., & Sinason, D. (1999). The internal

auditor as fraud‐buster. Managerial Auditing Journal,

14(7), 351–363.

https://doi.org/10.1108/02686909910289849

Jr., A. H. C., & Walker, P. L. (1999). Catanach, Walker -

The international debate over mandatory auditor

rotation a conceptual research framework. Journal of

International Accounting, Auditing and Taxation, 8(1),

43–66.

Koroy, T. R. (2008). Pendeteksian Kecurangan (Fraud)

Laporan Keuangan oleh Auditor Eksternal. Jurnal

Akuntansi Dan Keuangan, 10(1), 22.

Latan, H., & Ghazali, I. (2017). Partial Least Squares,

Konsep, Metode dan Aplikasi Menggunakan WarPLS

5.0, Third Edition. Badan Penerbit Universitas

Diponegoro.

Lowensohn, S., Johnson, L. E., & Elder, R. J. (2005).

Auditor Specialization and Perceived Audit Quality,

Auditee Satisfaction adn Audit Fees in the Local

Goverment Audit Market. Journal of Accounting and

Public Policy, 1271(970), 1–38.

Mansi, S. A., Maxwell, W. F., & Miller, D. P. (2004). Does

Auditor Quality and Tenure Matter to Investors ?

Evidence from the Bond Market. Journal of Accounting

Research, 42(4), 755–793.

O’Keefe, T. B., Simunic, D. a, & Stein, M. T. (1994). The

Production of Audit Services: Evidence from a Major

Public Accounting Firm. Journal of Accounting

Research, 32(2), 241–261.

https://doi.org/10.2307/2491284

Palmrose, Z.-V. (1988). An Analysis of Auditor Litigation

and Audit Service Quality. The Accounting Revies,

63(1), 55–73.

Pitkanen, J. (2016). Audit Quality; The Effect of Prior

Experience.

Purwanti, I. G. A. D. S., & Astika, I. bagus P. (2017).

Pengaruh Auditor’s Professional Skepticism, Red

Flags, Beban Kerja Pada Kemampuan Auditor Dalam

Mendeteksi Fraud. E-Jurnal Akuntansi Universitas

Udayana, 21

(2), 1160–1185.

Rai, A., Lang, S. S., & Welker, R. B. (2002). Assessing the

validity of IS success models: An empirical test and

theoretical analysis. Information Systems Research,

13(1), 50–69. https://doi.org/10.1287/isre.13.1.50.96

Setyaningrum, D. (2012). Analisis Faktor-Faktor Yang

Mempengaruhi Kualitas Audit BPK-RI, 1–28.

Singleton, T., Singleton, A., Bologna, J., & Lindquist, R.

(2006). Fraud Auditing and Forensic Accounting.

Sugiyono. (2016). Metode Penelitian Kuantitatif,

Kualitatif, dan R&D. Bandung: Penerbit Alfabeta.

Sulaiman, N. A. (2011). Audit Quality in Practice : A Study

of Perceptions of Auditors , Audit Committee Members

and Quality Inspectors A thesis submitted to the

University of Manchester for the degree of Doctor of

Philosophy in the Faculty of Humanities Noor Adwa

Sulaiman.

The Institute of Chartered Accountants in England &

Wales. Audit Quality (2002).

Umar, H. (2012). Pengawasan Untuk Pemberantasan

Korupsi. Jurnal Akuntansi & Auditing, 8(2), 95–189.

Umar, H. (2016). Corruption The Devil. Jakarta: Penerbit

Universitas Trisakti.

Ward, D. D., Elder, R. J., & Kattelus, S. C. (1994). Further

Evidence on the Determinants of Municipal Audit Fees.

The Accounting Review, 69(2), 399–411.

https://doi.org/10.2307/248594

Wilks, T. J., & Zimbelman, M. F. (2004). Concepts to

Prevent and Detect Fraud, 18(3), 173–184.

Zahmatkesh, S., & Rezazadeh, J. (2017). The effect of

auditor features on audit quality. TÉKHNE - Review of

Applied Management Studies.

https://doi.org/10.1016/j.tekhne.2017.09.003

Zimbelman, M. F. (1997). The Effects of SAS No. 82 on

Auditors’ Attention to Fraud Risk Factors and Audit

Planning Decisions. Journal of Accounting Research,

35(82), 75. https://doi.org/10.2307/2491454

EBIC 2019 - Economics and Business International Conference 2019

472