Content Analysis of Corporate Social Responsibility (CSR) Activities

of Companies Listed in Indonesia Stock Exchange

Amlys Syahputra Silalahi

1

, Doli Muhammad Jafar Dalimunthe

1

and Aryanti Sariartha Sianipar

1

1

Department of Management, Universitas Sumatera Utara, Jl. Prof. T.M Hanafiah, SH, Kampus USU, Medan, Indonesia

Keywords: Corporate Social Responsibility, CSR Activities, Public Companies, Content Analysis.

Abstract: Corporate social responsibilities (CSR) gained intensive attention as indicated by massive appreciations given

to companies that have a high commitment to CSR activities. The Government also strived to arrange

regulation for corporates that operate in Indonesia, as stated in Corporate Laws No. 20 the year 2007. The

Government also regulated the allocation of 2%, 2,5% or 3% of companies' profit is compulsory to support

the CSR programs. This research strived to find the implementation of CSR activities among companies in

some industry classification listed in the Indonesia Stock Exchange in the year 2018. By observing 595 annual

reports of listed companies with content analysis, this study found that companies focused more on corporate

governance; employee growth; and scientific responsibility management system. The less attractive

dimension of CSR is tax contributions; energy saving and carbon reduction; and environmental management

and protection. Further examination within industry classifications revealed that companies that operate in

agriculture; mining; and consumer goods ranked the top on CSR. This implied that companies have a high

interest in charity and building a firm-employee relationship. This study also found that CSR activities of

state-owned enterprises were significantly outperformed the private-owned enterprises in major dimensions

of CSR.

1 INTRODUCTION

Corporate Social Responsibility Activities (CSR)

gain serious attention among practitioners. External

parties for instance business media appreciate

companies that conduct CSR. The Government

proposes a draft bill for Corporation that operates in

and/or related to natural resources are required to

conduct CSR programs (as stated in Corporate Law

No. 40 the Year 2007). Furthermore, the draft bill

enacted that companies are obligated to allocate 2%;

2.5%; or 3% of its net profit for CSR fund. This draft

bill later is modified to Draft Bill of Social Worker.

Nevertheless, a considerable amount of business

media release an award for firms that focus on CSR.

As a matter of fact, in 2018 an award was given to 61

CEOs who had priority on CSR activities. Later, the

existing draft bill turned into the draft bill of the social

worker. According to CSR disclosure of publicly held

firms in Indonesia, our observation on CSR score

among firms in 2018 describe that the focus lies in

corporate governance and employee growth. The data

is exhibited in table 1. This means that the orientation

of CSR is not consistent with the reason for firms’

operational in natural resources. Corporations should

focus on environmental and energy savings issues.

Later on, the name of the draft bill of social workers

tended to put on the responsibility of social works to

companies. Meanwhile, companies have

implemented an obligation in terms of income tax. If

the government enacted such regulation then what

was the purpose of paying taxes? The government

should also regulate the implementation mechanisms

of CSR, not only the profit allocation.

The implementation of CSR has been widely

conducted by all companies specifically public

companies. The trigger of this implementation is

government regulation. The government considered

that companies that explored and exploited natural

resources for obtaining profits to its institution must

conduct corporate social responsibilities. As

responsible corporates, they tend to give back the

money to society or the environment they involved in.

In China, the existence of industries brings impact to

pollution from energy consumption. The solution to

this issue is by reducing pollution, and this

achievement is possible if collaboration between

governments, corporations, scholars, and society are

184

Silalahi, A., Jafar Dalimunthe, D. and Sianipar, A.

Content Analysis of Corporate Social Responsibility (CSR) Activities of Companies Listed in Indonesia Stock Exchange.

DOI: 10.5220/0009201301840196

In Proceedings of the 2nd Economics and Business International Conference (EBIC 2019) - Economics and Business in Industrial Revolution 4.0, pages 184-196

ISBN: 978-989-758-498-5

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

strong (Wu and Hu, 2019). In Europe, CSR is

considered an integral part of a community or

environmental problem, and it also is a philanthropic

action in the USA. Meanwhile, in China companies

that have a plan to compete in the global market

should consider CSR activities. This was due to

investors' valuation reflected in stock price

movements (Kuo, Yeh and Yu, 2012).

Table 1: Average CSR Score of Publicly Held Companies

in Indonesia in 2018.

Subcate

g

ories of CSR CSR Score

Corporate Governance

(

CG

)

2.14

Em

p

lo

y

ee Growth

(

EG

)

2.13

Environmental

Management and

Protection

(

EMP

)

1.11

Energy Saving and

Reduction

(

ESR

)

0.87

Sustainable

Development (SD)

1.42

Product Quality Control

(PQC)

1.30

Protection of Consumer

E

q

uit

y

(

PCE

)

1.01

Supply Chain

Partnership (SCP)

0.90

Promotion of Indonesia's

technological

Develo

p

ment

(

PITD

)

0.93

Tax Contribution

(

TC

)

0.33

Scientific Responsibility

Management System

(

SRMS

)

1.46

Sound Corporate Image

(

SC

)

1.35

The studies of CSR in Indonesia focus on the

impact of CSR on corporate value and risk. Research

has focused on the debate between positive and

negative viewpoints of CSR. Some studies support

companies that practice CSR. Customers' trust toward

CSR programs is the main point of whether CSR

programs work or do not work. CSR activities work

when they obtain trust in the mind of customers. It

does not work when it can not obtain the trust of

customers. Trusting customers leads to a higher

relative attitude and intention toward the

brand/company with CSR programs than nontrusting

customers. The implication of this study is that

marketers should pay more attention to showing and

communicating to customers and the public about the

company’s concern over environment and safety.

Furthermore, companies also are encouraged to report

and evaluate CSR programs transparently and

periodically and maintaining a good reputation for

gaining customers' trust toward CSR activities

(Darsono, 2009).

Previous research provides different hypotheses

regarding this issue, for instance, the trade-off

hypothesis; managerial opportunism hypothesis;

good management hypothesis; and slack resource

hypothesis. A State-owned enterprise is prone to

encounter a trade-off hypothesis and managerial

opportunism hypothesis. Thus, the negative impact of

CSR practices experienced by government-owned

enterprises. Meanwhile, private owned companies

gained a positive impact from CSR activities

according to good management hypothesis.

Managerial opportunism hypothesis argued that

conflict between manager and principal occurs in

companies that practice CSR because managers

might excessively invest in slack resources (Tan and

Peng, 2010). There is limited research conducted in

emerging markets about CSR practices and disclosure

by using content analysis. The majority of studies

focused on marketing and legal perspective of CSR

practices and regulation.

This study strives to examine the practice of CSR

in public companies listed on the Indonesia stock

exchange. This research has two purposes: (1) to

observe the dimension of content analysis from CSR

practices published in CSR disclosure. (2) to examine

the difference between state-owned enterprises and

private-owned enterprises in each dimension of

content analysis. This study contributes to the

literature of CSR in terms of corporate focus in CSR

practices mainly in developing countries. According

to the impact of companies that explore and exploit

natural resources, the main activities of CSR should

be in environmental management and energy saving.

This study also will shed light on the implementation

of government regulation in state-owned and private-

owned enterprises. This research comprises of four

sections, section one provides an introduction.

Section two describes the literature review, and

section three explains the research method, and

section four concludes the study.

2 LITERATURE REVIEW

CSR is conducted to build trust and social capital.

(Starks, 2009) defines CSR as:

“Corporate social responsibility is the commitment

of businesses to contribute to sustainable economic

development by working with employees, their families,

the local community and society at large to improve their

Content Analysis of Corporate Social Responsibility (CSR) Activities of Companies Listed in Indonesia Stock Exchange

185

lives in ways that are good for business and for

development.”.

CSR has been known to give a positive impact on

company performance. In developing countries, CSR

is perceived as one important factor that attracts

international investors and believed to be one of the

important factors that provide access to the global

market (Kuo, Yeh and Yu, 2012). Another study

argued that CSR grows rapidly because it is used as

an effort to ensure the effectiveness of corporate

governance. Friedman (1970) in (Jo and Harjoto,

2011) initially explained the CSR concept. CSR is an

effort to build a business in line with the

shareholders'desire that generally strives to create as

much profit as possible that also conform with the

regulation in society embedded in constitution and

ethic.

2.1 CSR Implementation

There is a difference in CSR implementation in

developing countries and developed countries. The

implementation of CSR in the USA is considered a

part of philanthropy and in Europe is an integral part

of the community. Another driven factors of CSR

activities are internal and external factors. Internal

factors: economic reform; extensive development

method characterized by high input, energy

consumption, and pollution that harms the

environment (Kuo, Yeh and Yu, 2012).

In European Union countries there is an activation

of the European Modernization Directive that

obligates the member countries to create legislation

of employee and environmental activities. The

pressures also stem from investment rating systems,

and NGOs and environmental activists. Lately, the

implementation is conducted as a tool to improve

stakeholders' management or public relations and

good reputation of companies (Gao, 2011). CSR

reports of construction firms in European countries

ranked the top and the US ranked second, and Asia

was the following third rank (Liao et al., 2017). This

indicates that western countries have established the

best practice of CSR.

The implementation of CSR in Asia is followed

by globalization (Gao, 2011). The globalization is

measured by the level of foreign direct investment in

a country. At the firm level, there is a strong

relationship between international exposure such as

international sales or foreign ownership and CSR

activities. CSR in Asia is focused on community

involvement and followed by production processes

and employee relations.

CSR practices in emerging economies are still

debatable issues because the engagement in such an

issue was demanded a substantial amount of money

and resources that lead to a lower profit (Wan

Ahamed, Almsafir and Al-Smadi, 2014).

Furthermore being profitable is rather more important

than being socially responsible. Most firms in

developing countries practice CSR for legislation

requirements and reputation improvement. In

emerging economies, evidence was found that not all

emerging economy companies that facing uncertainty

are likely to imitate the CSR decisions of first-mover

firms or able to generate strategic advantages of CSR

practices.

2.2 CSR in Indonesia

The reason for CSR implementation in Indonesia is

because of the regulation. The pressures come from

the government that gave the obligation to companies

that operate in natural resources and environment to

conduct CSR that has stated in Government

Regulation (PP) No.47 Year 2012. Later, the

government plan to create a regulation that requires a

company to allocate 2%, 2,5% or 3% of its profit.

Prior to 2007, many social norms regulated work

safety, labor rights, limited welfare, environmental

protection, and consumer protection. But rather this

regulation was followed by weak law enforcement.

There was a conflict between economic interest and

stakeholder protection on issues such as labor

protection and environmental management. The

Government offered several benefits for companies

for instance lower tax rate and lower environmental

standards. This was for attracting foreign direct

investment. Not surprisingly, MNCs had the best

regulatory practices. Only multinational or large

corporations that conduct CSR (Rinwigati and

Waagstein, 2011). Local or small companies still

considered that CSR was a foreign concept. Wowoho

(2009) argued that CSR activities of companies in

Indonesia focused on issues for example charity,

education, research, health, and natural disaster

assistance. Very few cases put attention on the

environment, security, human rights, and other social

matters (Maemunah, 2007).

Later after the enactment of Corporate Law in

2007 that regulates CSR, questions arose. Whether

Indonesian companies held more burden on this

issue? There were two perspectives. First, if the CSR

practices are part of obeying government regulation

firms should be willing to accept decreasing profits.

Second, if companies concentrated on costly and

destructive actions to achieve profits (for instance

EBIC 2019 - Economics and Business International Conference 2019

186

competition; product quality; employee safety; and

environment) then by being socially responsible

would be considered by managers and directors as an

investment (Rinwigati and Waagstein, 2011).

In Indonesia, CSR practices will contribute to

companies' good reputation if the customer had trust

in CSR programs. Several issues on CSR programs

are most important to gain trust from customers, for

instance, concern on products and services safety, the

efforts to reduce environmental hazards, and the

company reputation as a "good" company (Darsono,

2009). According to an observation of companies'

websites in seven countries, the researcher found that

Indonesia's CSR companies reached 24% among the

top 50 companies (Chapple and Moon, 2005). The

research also found in 24% of those CSR companies,

72.7% had minimal; 9.1% medium; and 18.2%

extensive CSR reportings. Minimal means the report

consists of only one to two pages, meanwhile medium

comprised of three to ten pages. Extensive category

contained more than ten pages of CSR reports. They

also found that each 27.3% of the surveyed

companies focused on community involvement,

production process, and employee relations.

The CSR practices should be followed by trust

toward CSR programs in Indonesia (Darsono, 2009).

Marketers must pay more attention to:

Showing and communicating to the customers

and public about the company concern over

environment and safety;

Reporting and evaluating CSR programs

transparently and periodically;

Maintain and develop the company's good

reputation.

2.3 Private and State-Owned

Enterprise CSR Implementation

In countries where the government requires

corporations to contribute to a better society,

companies gained the reward from investors when

they commit to CSR and comply with new CSR

standards (Arya and Zhang, 2009).

2.3.1 CSR Implementation of Private

Owned Enterprises (POE)

Private owned enterprise has specific objectives set

by shareholders. Managers serve the interest of

shareholders in terms of profit. Profit maximization is

still important, meanwhile, a good reputation should

not be ignored. Private owned enterprises face more

competition and financial distress than State-owned

enterprises. Therefore they had to maintain a close

relationship with supply chain partners to gain high-

quality material and lower prices of raw material, thus

improve competitiveness. CSR disclosure of private-

owned enterprises better in supply chain partnership

(Kao et al., 2018).

Private owned enterprises specifically with

foreign ownership or multinational corporations were

the first to engage and acknowledge the

implementation of CSR prior to the enactment of

CSR regulation in 2007. This policy was driven by its

headquarters and pressures from society. Companies

that bring CSR into practice are the ones operating in

a more highly developed sector, for instance, natural

resources exploitation or exploration and

manufacturing industry. These sectors are exposed to

higher-profile lawsuits and cases (Rinwigati and

Waagstein, 2011).

2.3.2 CSR Implementation of State-Owned

Enterprises (SOE)

State-owned enterprise (SOE) was designed to have a

purpose in line with government goals. In SOEs, the

board of directors was selected by a political decision

from the Ministry of SOEs and other political powers.

In China, self-interested politicians tend to obtained

benefits of political control over SOEs. The

Government encountered dual roles of the

administrator of social affairs and the owner of SOEs.

As controlling shareholders government supposed to

benefit from value maximization. In another case, the

authoritative government might enhance political

capital and promotion by promoting activities in

regional development, fiscal health, social stability,

through their involvement in SOEs. Thus, the

government played a role in political and social

objectives. Government connections in corporations

lead to extracting resources for both social and

political interests (Chen et al., 2011).

A study in China that strived to find the role of

SOEs in CSR engagement. There was evidence that

State-owned enterprise (SOE) has significantly

superior performance in environmental management,

promotion of China’s technological development,

and tax contribution (Kuo, Yeh and Yu, 2012). The

Government appointed managers at the SOEs in

China to comply with political power and survival

(Kao et al., 2018). In Indonesia, the government still

intervenes corporate policies. Thus, this study

hypothesized that there is a signficant difference

between SOEs and POEs CSR practices.

Content Analysis of Corporate Social Responsibility (CSR) Activities of Companies Listed in Indonesia Stock Exchange

187

3 RESEARCH METHODS

3.1 Sample

The selected sample of this study comprised of 595

publicly held companies listed in Indonesia Stock

Exchange. The CSR disclosures originated from

annual reports published in Indonesia Stock

Exchange during the year 2018. Actually, this study

employed a cross-sectional data to capture the

behavior of corporations that engaged in CSR

programs. Then this research split the sample into two

categories, state-owned enterprise, and private-

owned enterprise. That process resulted in 14 or

2,35% state-owned enterprises (SOEs) and or 581 or

97,65% private-owned enterprise (POEs).

3.2 Content Analysis

Content analysis is considered as a systematic and

objective technique that enables a researcher to

transform qualitative and text reports into the

quantitative analysis (Kao et al., 2018). Initially,

variables observed in the content analysis consists of

two quantitative and qualitative items. Quantitative

items are the data measured in quantity units,

meanwhile, qualitative items refer to text narratives.

We modified the dimensions into 12 categories that

comprise of each item. Generally, the dimensions

consist of:

Corporate Governance and ethical value (CG);

Employee Growth (EG);

Environmental Management and Protection

(EMP);

Energy Saving and Reduction (ESR);

Sustainable Development (SD);

Product Quality Control (PQC);

Protection of Consumer Equity (PCE);

Supply Chain Partnership (SCP);

Promotion of Indonesia's technological

Development (PITD);

Tax Contribution (TC);

Scientific Responsibility Management System

(SRMS);

Sound Corporate Image (SC).

Details of the dimensions and items are

described in Appendix 1. Every dimension was

comprised of several items. We checked each item

contained in the firms' annual reports and gave

scores proportionally according to the items written

in annual reports. The score ranging from 0 to 3,

with 0 is the lowest score and 3 is the highest score.

For example, Corporate governance consisted of 5

items, the scoring for firm A after the annual report

was checked only contained 3 items. Then, the CSR

score was proportionally 1.2 which was (2/5x3).

The calculation was mathematically expressed as

follows:

CSR score=

IR

ID

×3

(1)

IR was the number of items reported in the annual

report, and ID was the items contained in dimension.

Thus, a firm's CSR score when the items were

completely reported in every dimension had the

highest score of 3. Meanwhile, when all of the items

reported in the annual report were unavailable, the

score would be zero.

3.3 Data Analysis

The first objective of this study was to find the pattern

of CSR activities reported by public companies listed

in Indonesia Stock Exchange by observing the

dimensions and items available in the annual reports.

Second, to examine the differences of each CSR

dimension in content analysis between state-owned

and private-owned enterprises. The Analysis of the t-

test was employed to examine the differences. The t-

test hypothesis was stated as follows:

H0: μ

1

= μ

2:

there is no significant difference between

the means of CSR score of SOEs and POEs

H1: μ

1

≠ μ

2

: there is a significant difference between

the means of CSR score of SOEs and POEs

If the t-statistic is smaller than t-table (t-stat < t-table),

then we can not reject the null hypothesis.

Conversely, if the t-stat is larger than t-table (t-stat >

t-table), then we reject the null hypothesis.

4 EMPIRICAL FINDINGS

The empirical findings of the study are reported in

three sections. The first section presents descriptive

statistics of the CSR score among the corporations.

Second, we provide information about the content

analysis which contains the pattern of CSR score for

each dimension of CSR. The last section presents the

findings on t-test between two samples, state-owned

enterprise (SOE) and private-owned enterprise

(POE).

4.1 Descriptive Statistics

Basic information regarding the sample is presented

in Table 2. As presented in the table, there were 12

dimensions in CSR Scoring.

EBIC 2019 - Economics and Business International Conference 2019

188

Table 2: Descriptive statistics of CSR scores within the

overall sample.

CSR

Dimensions

Mean Standard

Deviation

Min Max

Corporate

Governance

and ethical

value (CG)

2.14

0.66

0 3

Employee

Growth

(

EG

)

2.12

0.84

0 3

Environmental

Management

and Protection

(

EMP

)

1.11

0.84

0 3

Energy Saving

and Reduction

(

ESR

)

0.87

0.93

0 3

Sustainable

Development

(SD)

1.42 1.12 0 3

Product

Quality

Control (PQC)

1.30

1.12

0 3

Protection of

Consumer

E

q

uit

y

(

PCE

)

1.01

0.79

0 3

Supply Chain

Partnership

(

SCP

)

0.89

0.85

0 3

Promotion of

Indonesia’s

technological

Development

(

PITD

)

0.93

0.91

0 3

Tax

Contribution

(TC)

0.33

0.69

0 3

Scientific

Responsibility

Management

System

(SRMS)

1.47

0.96

0 3

Sound

Corporate

Ima

g

e

(

SC

)

1.38

0.83

0 3

Total 14.95

7.36

1.20

31.40

When we broke down the observation into each item,

the three highest average scores were in issues such

as corporate governance and ethical value; employee

growth; and The Scientific Responsibility

Management System. The Number of observations

was 595 publicly listed companies. The top three

highest scores regarding the CSR activities were in

corporate governance and ethical value; employee

growth; and the scientific responsibility management

system. According to this result, the majority of

companies' CSR practices were related to social

works, but not related to environmental or energy-

saving activities.

4.2 Content Analysis of CSR among

Industries

Our sample comprised of companies operated in

several industries. We followed the Indonesia Stock

Exchange (IDX) classification of industries, such as

agriculture (AGR); basic industry and chemicals

(BIC); consumer goods (COG); financial (FIN);

infrastructure (INF); mining (MIN); miscellaneous

industries (MSC); property, real estate and building

(PRB); trade service and investment (TSI).

Figure 1: Total CSR Scores among industries.

The CSR scores for each industry classification

are shown in figure 1. According to figure 1, trade

service and investment had the lowest total score of

CSR (12.07). Meanwhile, the highest score was

possessed by agriculture (17.98). Contrary to the

regulation, industry such as mining; basic industry

and chemicals; and infrastructure which were

considered operationally dependent on environment

17,98

16,13

16,39

16,10

14,85

16,44

14,46

15,08

12,07

TOTAL

CSR

SCORE

Trade,service,andinvestment

Propertyrealestateandbuilding

Miscellaneous

Mining

Infrastructure

Financials

ConsumerGoods

BasicIndustryandChemicals

Agriculture

Content Analysis of Corporate Social Responsibility (CSR) Activities of Companies Listed in Indonesia Stock Exchange

189

and energy precisely found to be less socially

responsible.

According to the average score of total CSR score

(14.95), there were three industries that scored below

the average, namely infrastructure (14.85);

miscellaneous industries (14.46); trade service and

investment (12.07). On the other side, industries like

agriculture (17.98); mining (16.44); consumer goods

(16.39); basic industry and chemicals (16.13);

financials (16.10); property real estate and building

(15.08) obtained above-average scores. The most

socially responsible industries were agriculture;

mining and consumer goods.

We further examine the top three dimensions that

corporations focused on, namely corporate

governance, employee growth

, and scientific

responsibility management system. The details can be

seen in figure 2. The CSR score was calculated

according to the average of the industry.

We further examine the highest scores mentioned

prior to this paragraph. The Corporate governance

score of each industry was depicted in figure 3.

0.0

0.4

0.8

1.2

1.6

2.0

2.4

CG

E

G

EMP

ESR

SD

PQC

P

CE

S

CP

P

IT

D

T

C

SRMS

SC

Means

Figure 2: Average score of CSR dimension.

Figure 3: Score of corporate governance dimension of CSR

among industries.

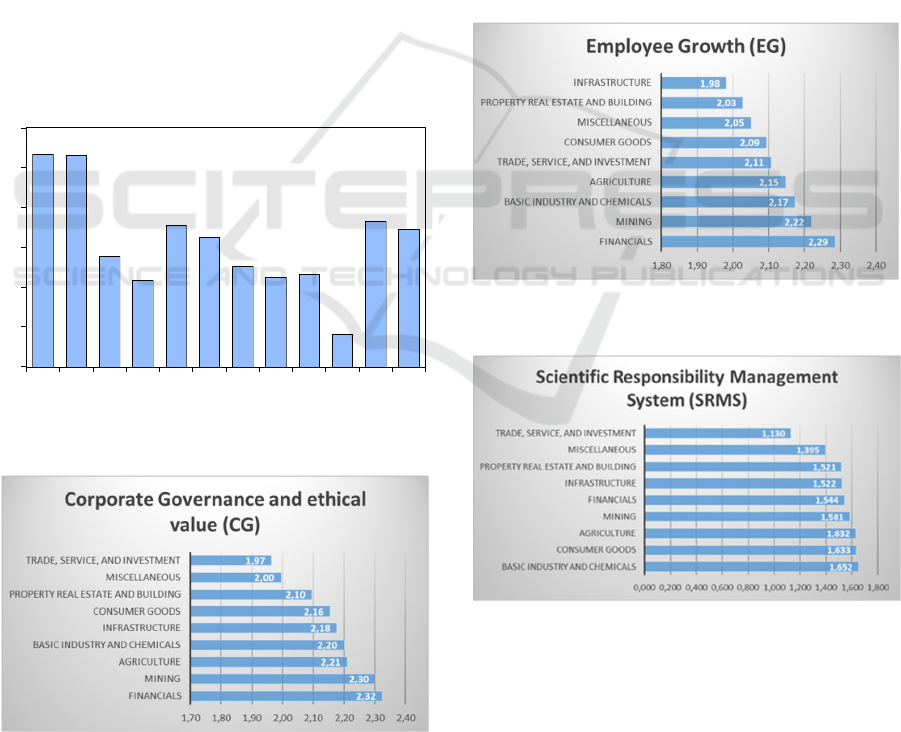

According to the figure industry that scored the

highest performance were financials, mining, and

agriculture. Meanwhile, the second dimension of

CSR that most companies practiced was employee

growth. This dimension consisted of issues such as

employee protection, benefits, non-discrimination,

and the labor union. According to figure 4, the

industry that focused on this issue were financials,

mining, and basic industry and chemicals. The third

highest score was the scientific responsibility

management system. Further description can be seen

in figure 5. As exhibited in figure 5, industry such as

basic industry and chemicals, consumer goods, and

agriculture were top three companies that paid most

attention to issues, for instance, the availability of

independent CSR management institution, linearity

between ethical conducts and management system,

and the introduction of stakeholder communication

and performance improvement mechanisms.

Figure 4: Score of employee growth dimension of CSR

among industries.

Figure 5: Score of scientific responsibility management

system dimension of CSR among industries.

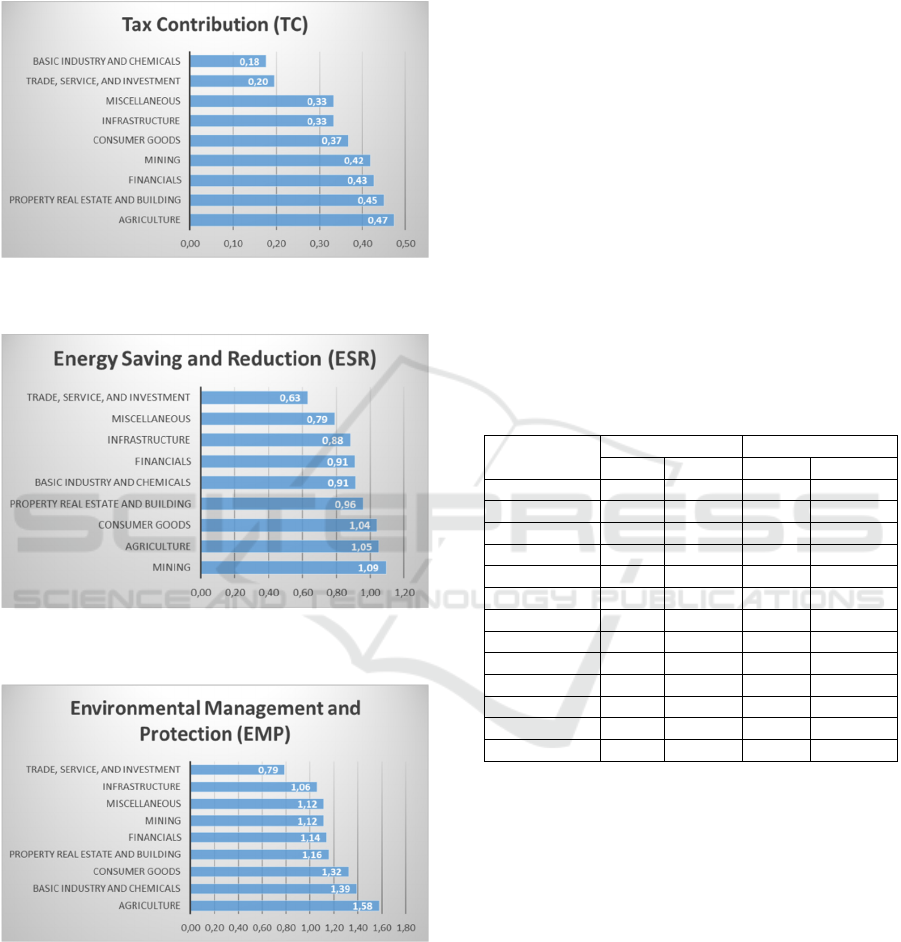

The least score in each dimension was tax

contribution; energy saving and reduction; and

environmental management and protection. The

Industry that focused on this issue was agriculture.

Meanwhile, the industry that practiced energy-saving

and reduction was mining. Finally, the agriculture

EBIC 2019 - Economics and Business International Conference 2019

190

industry best practiced was regarding environmental

management and protection compared to other

industries. The details were depicted in figure 6

through 8.

Figure 6: Score of tax contribution dimension of CSR

among industries.

Figure 7: Score of energy-saving and reduction dimension

of CSR among industries.

Figure 8: Score of environmental management and

protection dimension of CSR among industries.

The results of content analysis in this research

revealed that the majority of companies performed

corporate governance, employee growth, and

scientific responsibility management system. These

issues were contradictive to findings in China where

companies focused on energy-saving and carbon

reduction, development of circular economy, and

promotion of research, new techniques and methods

of energy saving/carbon reduction (Kuo, Yeh and Yu,

2012). Chinese companies conducted CSR since the

issues of global warming and the environment had

seriously been an important issue. On the other hand,

the government of Indonesia, that released regulation

in the same issues never created an implementation

practice to the regulation. As a result, most companies

practices of CSR irrelevant with the main cause of

CSR, which is to be environmentally responsible.

4.3 CSR Practices of SOEs and POEs

The overall sample then split into two categories

according to ownership type namely state-owned

enterprises (SOEs) and private-owned enterprises

(POEs). The descriptive statistics of the two

classifications are presented in Table 3.

Table 3: Descriptive statistics of CSR scores within the

state-owned and private-owned enterprise.

CSR

Dimensions

SOEs POEs

Mean Stdev Mean Stdev

CG 2.53 0.42 2.13 0.66

EG 2.61 0.56 2.11 0.84

EMP 2.19 0.73 1.08 0.83

ESR 1.71 1.07 0.85 0.92

SD 2.43 0.64 1.39 1.12

PQC 1.89 1.09 1.29 1.12

PCE 1.64 0.63 0.99 0.79

SCP 1.43 0.85 0.89 0.85

PITD 1.43 0.76 0.92 0.91

TC 0.85 0.98 0.32 0.68

SRMS 1.85 0.86 1.45 0.96

SC 2.04 0.69 1.34 0.83

Total 22.54 4.38 14.75 7.32

As presented in table 3, there was a significant

difference in total CSR scores between state-owned

enterprises (22.54) and privately-owned enterprises

(14.75). Meanwhile, a further examination of each

dimension resulted in a significantly different CSR

score between SOEs and POEs in the majority of

issues. To examine the significance, further analysis

was conducted using the t-test. The details were

shown in table 4. As indicated in table 4 the quality

of total CSR scores of state-owned enterprises was

significantly better than private-owned enterprises.

According to table 4, it can be inferred that CSR

disclosure of private-owned enterprise and state-

owned enterprises were statistically different in

overall dimensions except for tax contributions and

scientific responsibility management system. This

Content Analysis of Corporate Social Responsibility (CSR) Activities of Companies Listed in Indonesia Stock Exchange

191

indicates that overall CSR practices between state and

private-owned enterprises were significantly

different, mainly private-owned enterprises practiced

CSR worse than state-owned enterprises. The results

support the findings found in China that state-owned

enterprises focus more on the issues of CSR

specifically energy saving and reduction; and

promotion of research, techniques, and methods of

energy saving/reduction (Kuo, Yeh and Yu, 2012).

Private owned companies encountered an agency

problem regarding CSR practices. State-owned

companies had greater incentives to involve in CSR

as this activity helped the government to reduce

community and social burdens. This also helped the

government to improve its political reputation and

decrease financial encumbrance (Qian, Gao and

Tsang, 2015).

Table 4: Results of t-test CSR scores and CSR score

dimensions between POEs and SOEs.

CSR Dimensions Mean

(

t-stat

)

CG -0.3351**

(-2.47)

EG -0.4559**

(

-2.57

)

EMP -0.9983***

(

-4.79

)

ESR -0.8640***

(-3.00)

SD -1.0344***

(

-5.78

)

PQC -0.6368**

(

-2.47

)

PCE -0.6498***

(-3.77)

SCP -0.5422**

(-2.35)

PITD -0.5129**

(

-2.50

)

TC -0.5266

(-1.91)

SRMS -0.4045

(-1.73)

SC -0.5181***

(

-3.42

)

Total -7.7117***

(

-6.17

)

*** p-values < 1%

** p-values < 5%

Indonesia is one of many countries in Asia that

regulated CSR practices. The government regulated

that enterprises should be responsible for societies

specifically because their operational activities are

associated with the environment and should also

perform corporate social responsibility. For private-

owned companies, this mandate has both positive and

negative impacts. Positive impact because private-

owned companies were valued by investors, later if

they are a highly responsible firm they tend to have a

positive reputation among stakeholders such as

government, employees, customers, communities,

and investors (Qian, Gao and Tsang, 2015). On the

other hand, a negative impact might happen as CEOs

decided to excessively involved in CSR. Excessive

investment in CSR was considered a slack

investment, brought less return on investment. This

would destroy the financial performance. In this case,

CEOs only took action based on self-interest as their

reputation might be better in the perspective of

employees, communities and the environment

(Barnea and Rubin, 2010). Findings in China,

private-owned enterprise gained positive impact on

CSR engagement, supporting the good management

hypothesis (Kao et al., 2018). Good management

hypothesis implies that firms that engaged in CSR

would obtain a higher reputation to resolve conflicts

between managers and non-investing stakeholders

(consumers and employees).

The implementation of such regulation seemed to

be applied better by state-owned enterprises.

Indonesia's state-owned enterprise CEOs were

appointed by the government. This implies that the

mandate would be greater for state-owned

enterprises. These findings were significant in energy

saving and carbon reduction, environmental

management and protection supporting the studies

conducted in the emerging country (Gao, 2011).

SOEs were utilized by political power to improve

government reputation and reduce financial burdens.

5 CONCLUSIONS

This research is conducted to provide evidence about

CSR practices reported in annual reports published by

publicly listed companies. CSR research within the

emerging countries is very limited. In this research,

we aim to find evidence of CSR practices by using

content analysis in publicly held companies listed in

Indonesia Stock Exchange (IDX) in 2018. First

purpose of this study is to find the quality of CSR

disclosure of public companies in several industry

classifications and the dimensions they focus on.

Second, we examine whether the quality of CSR

practices of state-owned enterprises (SOEs)

outperform the private-owned enterprise (POEs).

This study finds evidence that Indonesia's public

companies have conducted CSR according to the

EBIC 2019 - Economics and Business International Conference 2019

192

regulation. The quality of each dimension of CSR that

practiced by several industries varies. According to

the total score of CSR, the industry that performed

highest in CSR disclosure is agriculture. Meanwhile

mining that perceived as highly associated with

environmental exploration and exploitation industry

scored the third-highest among industries. Further,

the examination of each CSR dimension implies that

the focus of companies involved in CSR is on

"corporate governance, employee growth, and

scientific responsibility management system. The

implementation of CSR from major companies is

associated with charity and building a firm-employee

relationship. Issues regarding environmental are less

attractive to public companies. In terms of corporate

governance and employee growth, the best performer

was the financial industry. Meanwhile, the scientific

responsibility management system was practiced best

by basic industry and chemicals.

Further examination was conducted to obtain

evidence of the difference between SOEs and POEs

CSR practices. Overall, CSR practices of private-

owned enterprises are underperformed by the CSR

practices of state-owned enterprises. The differences

are significant in each dimension of CSR except tax

contributions and scientific responsibility

management system. This result implies that state-

owned companies have already satisfied the mandates

regulated by the government. This also indicates that

the government utilized state-owned enterprises to

improve political reputation and reduce financial

burdens. SOEs served as institutions that endure

greater social purpose than private-owned

enterprises.

This research contributes to the literature in

emerging countries considering the limited number of

studies available associated with emerging markets.

Indonesia as one of the countries which regulated the

CSR practices should clearly state the mechanisms of

CSR implementation. Companies that explore and

exploit natural resources should focus more on

environmental issues rather than social, charity, or

firm-employee relationship. The government as a

policymaker should revisit the draft bill and regulate

the mechanisms of CSR implementation. If CSR

implementation focuses more on social activities,

then what will be the benefits of companies paying

taxes? The social purpose that perceived as state-

owned enterprise obligation has been widely

practiced by private-owned enterprises.

ACKNOWLEDGEMENTS

This research is funded by USU according to A

Contract of Conducting Research Talenta USU Fiscal

Year 2019 number 4167/UN5.1.R/PPM/2019 1 April

2019. We also would like to be thankful for the

research assistance of Afriani Sarah and Marti

Latifolia.

REFERENCES

Arya, B. and Zhang, G. (2009) ‘Institutional reforms and

investor reactions to CSR announcements: Evidence

from an emerging economy’, Journal of Management

Studies, 46(7), pp. 1089–1112. doi: 10.1111/j.1467-

6486.2009.00836.x.

Barnea, A. and Rubin, A. (2010) ‘Corporate Social

Responsibility as a Conflict Between Shareholders’,

Journal of Business Ethics, 97(1), pp. 71–86. doi:

10.1007/s10551-010-0496-z.

Chapple, W. and Moon, J. (2005) ‘Business & Society’.

doi: 10.1177/0007650305281658.

Chen, S. et al. (2011) ‘Government intervention and

investment efficiency: Evidence from China’, Journal

of Corporate Finance. Elsevier B.V., 17(2), pp. 259–

271. doi: 10.1016/j.jcorpfin.2010.08.004.

Darsono, L. I. (2009) ‘Corporate Social Responsibility and

Marketing: What Works and What Doesn’t’, Gadjah

Mada International Journal of Business, 11(2), p. 275.

doi: 10.22146/gamaijb.5524.

Gao, Y. (2011) ‘CSR in an emerging country : a content

analysis of CSR reports of listed companies’, Baltic

Journal of Management, 6, pp. 263–291. doi:

10.1108/17465261111131848.

Jo, H. and Harjoto, M. A. (2011) ‘Corporate Governance

and Firm Value: The Impact of Corporate Social

Responsibility’, Journal of Business Ethics, 103(3), pp.

351–383. doi: 10.1007/s10551-011-0869-y.

Kao, E. H. et al. (2018) ‘The relationship between CSR and

performance: Evidence in China’, Pacific Basin

Finance Journal, 51(June 2016), pp. 155–170. doi:

10.1016/j.pacfin.2018.04.006.

Kuo, L., Yeh, C. C. and Yu, H. C. (2012) ‘Disclosure of

Corporate Social Responsibility and Environmental

Management: Evidence from China’, Corporate Social

Responsibility and Environmental Management, 19(5),

pp. 273–287. doi: 10.1002/csr.274.

Liao, P. et al. (2017) ‘Communicating the Corporate Social

Responsibility ( CSR ) of international contractors :

Content analysis of CSR reporting Communicating the

corporate social responsibility ( CSR ) of international

contractors : Content analysis of CSR reporting’,

Journal of Cleaner Production. Elsevier Ltd,

156(April), pp. 327–336. doi:

10.1016/j.jclepro.2017.04.027.

Qian, C., Gao, X. and Tsang, A. (2015) ‘Corporate

Philanthropy, Ownership Type, and Financial

Content Analysis of Corporate Social Responsibility (CSR) Activities of Companies Listed in Indonesia Stock Exchange

193

Transparency’, Journal of Business Ethics, 130(4), pp.

851–867. doi: 10.1007/s10551-014-2109-8.

Rinwigati, P. and Waagstein, P. R. (2011) ‘The Mandatory

Corporate Social Responsibility in Indonesia :

Problems and Implications’, 98(3), pp. 455–466.

Available at: https://www.jstor.org/stable/41476143.

Starks, L. T. (2009) ‘EFA keynote speech: “corporate

governance and corporate social responsibility: What

do investors care about? What should investors care

about?"’, Financial Review, 44(4), pp. 461–468. doi:

10.1111/j.1540-6288.2009.00225.x.

Tan, J. and Peng, M. W. (2010) ‘Organizational Slack and

Firm Performance During Economic Transitions: Two

Studies from an Emerging Economy’, Ssrn,

1263(March 1998), pp. 1249–1263. doi:

10.2139/ssrn.1552171.

Wan Ahamed, W. S., Almsafir, M. K. and Al-Smadi, A. W.

(2014) ‘Does Corporate Social Responsibility Lead to

Improve in Firm Financial Performance? Evidence

from Malaysia’, International Journal of Economics

and Finance, 6(3), pp. 126–138. doi:

10.5539/ijef.v6n3p126.

Wu, C. M. and Hu, J. L. (2019) ‘Can CSR reduce stock

price crash risk? Evidence from China’s energy

industry’, Energy Policy. Elsevier Ltd, 128(January),

pp. 505–518. doi: 10.1016/j.enpol.2019.01.026.

APPENDIX

Dimensions Items

Corporate Governance

and ethical value (CG)

1-1 Specification of

corporate governance

structure

1-2 Compliance with

laws and regulations

1-3 Conformance of the

company’s core

management strategies

with CSR principles,

promised framework

agreement, and

standards

1-4 Availability of

consistent social

responsibility policies

1-5 Engagement in

active responding to

reasonable expectations

and demands of

stakeholders to create

harmony.

Employee Growth

(EG)

2-1 Growth of job

opportunities and

emplo

y

ees

Dimensions Items

2-2 Sufficient social

security and insurance

for employees

2-3 Efforts on ensuring

non‐discrimination,

maternity benefits,

salary equity, and

adequacy of holidays

2-4 Active engagement

in employee training

and cultivation of local

technical and

managerial human

resources

2-5 Paying attention to

the maintenance of

harmonious labor

relations, development,

and operation of a labor

union.

Environmental

Management and

Protection (EMP)

3-1 Paying attention to

environmental

protection and use of

consistent standards

around the globe

3-2 Active engagement

in promoting

environmental

awareness

3-3 Availability of

tangible measures of

environmental

protection and effective

fulfillment of the

responsibility for

environmental

protection

3-4 Dedication to the

production of

environmentally

friendly products or

services

3-5 Active launch or

participation in

extensive

environmental

protection projects.

Energy Saving and

Reduction (ESR)

3-6 Paying attention to

energy saving/carbon

reduction and

EBIC 2019 - Economics and Business International Conference 2019

194

Dimensions Items

development of the

circular economy

3-7 Using clean

energies and diffusing

this idea to other people

in the community

3-8 Promotion of

research, new

techniques, and

methods of energy

saving/carbon

reduction.

Sustainable

Development (SD)

3-9 Availability of the

awareness of and

strategies for

sustainable

development

3-10 Performance in

the sustainability of

strategies, production,

profitability, research,

and environmental

protection

3-11 Paying attention to

the sustainable use of

the environment and

resources.

Product Quality

Control (PQC)

4-1 Strengthening

product quality control

at all times to provide

qualified products to

consumers

4-2 Using quality

control methods that

are stricter than

external standards.

Protection of

Consumer Equity

(PCE)

5-1 Availability of a

sound after‐sales

service system and

active engagement in

collecting and reacting

to consumer feedbacks

5-2 Evaluation of

customer satisfaction

and active handling of

customer complaints

5-3 Voluntary recall of

defective products and

provision of

compensation

Dimensions Items

5-4 Voluntary recall of

defective products and

provision of

compensation.

Supply Chain

Partnership (SCP)

6-1 Providing fair

opportunities of the

transaction to upstream

and downstream firms

in the supply chain

6-2 Promoting healthy

business ethics in the

supply chain

6-3 Leading more

enterprises to become

outstanding corporate

citizens

Promotion of

Indonesia's

technological

Development (PITD)

7-1 Degree of research,

investment, and

openness of core

technologies

7-2 Engagement in the

active transformation

of advanced

development results

into productivity and

inducing enhancement

of development quality

of other enterprises

7-3 Contribution of

new technologies and

products to national and

social development as

well as changes in

social production and

lifestyles.

Tax Contribution (TC) 8-1 Longitudinal and

cross‐sectional

comparison of tax

revenue and its growth

8-2 The effects of tax

contribution on

regional economic

development

8-3 The effects of

paying tax actively on

the development of the

entire industry.

Scientific

Responsibilit

y

9-1 Availability of an

independent CSR

Content Analysis of Corporate Social Responsibility (CSR) Activities of Companies Listed in Indonesia Stock Exchange

195

Dimensions Items

Management System

(SRMS)

management institution

and incorporation of

CSR performance into

core management

strategies

9-2 Availability of a

management system

that supports business

principles or ethical

norms

9-3 Introduction of

stakeholder

communication and

performance

improvement

mechanisms.

Sound Corporate

Image (SC)

10-1 Availability of

corporate culture that

highly emphasizes

social responsibility

10-2 Adequacy of

information

communication and

disclosure mechanisms

10-3 Availability of

active and effective

improvement

mechanisms

10-4 Experience of

being awarded or

honored for leading

other competitors in

CSR performance.

EBIC 2019 - Economics and Business International Conference 2019

196