Enterprise Resource Planning (ERP) User Acceptance Model with

Easy to Use as Intervening Variable

Arifin Lubis, Rustam, and Iskandar Muda

Accounting Departement, Economic & Bussiness Faculty, Universitas Sumatera Utara, Medan, Indonesia

Keywords: Easy to Use, Village Government, Enterprise Resource Planning

Abstract: The purpose of this research is to know the influence of technological resistance, understanding of task,

human resources, financial supporting and training to the successful implementation of the Village

Enterprise Resource Planning (ERP) Base Application with Easy to Use as intervening variable. The type of

this research is descriptive quantitative with the sample respondent of 84 Village Owned Enterprises in

Central Tapanuli Regency, North Sumatera, Indonesia. The statistical tool of this research is with Structural

Equation Modeling with of Smart-PLS software. The results show that financial supporting and training to

the successful implementation of the Village Enterprise Resource Planning (ERP) Base Application and

technological resistance, understanding of task and human resources are not influence. The Easy to Use as

intervening variable is not influence.

1 INTRODUCTION

Enterprise Resource Planning (ERP) is an integrated

system that supports the core business activities of

an organization which includes manufacturing,

logistics, finance, accounting, sales, marketing, and

humanresources (Nah et al., 2004, Pasaoglu, 2011,

Alsoub et al., 2018). An ERP system will help parts

of an organization to share data and information,

reduce costs, and improve management of business

processes. With the benefits offered by the system,

many companies are tempted to implement it. In

increasing the income of the community and

villages, the Village Government can establish a

Village Owned Enterprise in accordance with the

needs and potential of the village. The establishment

of Village-Owned Enterprises is stipulated by

Village Regulations based on the laws and

regulations. The form of Village-Owned Enterprises

as referred to in paragraph must be a legal entity. In

accordance with the mandate of the Village Law No

6/2014 every village needs to establish a BUMDES,

as one of the efforts to empower the community

while increasing Village Original Revenue (Suriadi

et al., 2015). Furthermore, the Ministry of Villages,

Transmigration and Disadvantaged Regions has

issued Ministerial Regulation No 4/2015 on

BUMDES. Welcoming this the Regional

Governments should also have issued a Regional

Regulation on Procedures for the Formation and

Management of Village-Owned Enterprises.

However, of the many villages that have formed

BUMDES, the level of management and knowledge

of HR capacity has not been maximized.

BUMDES Financial Management is sourced

from state finances (Village Funds), it is necessary

to pay attention to the rules in recording and

reporting accounting standards. If not careful, the

BUMDES manager can be dragged into legal

problems due to not paying attention to the

accounting problems of Bumdes. The main principle

that needs to be considered in the recording and

financial reporting of BUMDES is which accounting

standard will we use as a basis? This is important,

because in the future BUMDES Financial Report

will be audited. The audit process is the process of

comparing notes and reports that are made with

applicable standards. There are several financial

accounting standards (SAK) that can be referred to

for the compilation and recording of BUMDES

accounting, one of which is Entity Accounting

without Public Accountability (ETAP). This ETAP

Financial Accounting Standard is a fairly simple and

practical accounting standard used as a reference for

preparing BUMDES financial statements (Suriadi et

al., 2015).

Lubis, A., Rustam, . and Muda, I.

Enterprise Resource Planning (ERP) User Acceptance Model with Easy to Use as Intervening Variable.

DOI: 10.5220/0009197500090014

In Proceedings of the 2nd Economics and Business International Conference (EBIC 2019) - Economics and Business in Industrial Revolution 4.0, pages 9-14

ISBN: 978-989-758-498-5

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

9

The use of information technology based on

Computer Accounting Applications whose job is to

obtain financial reports automatically, quickly and

has a better level of accuracy than manually

(Amoako et al., 2004, Turetkenet al., 2019,

Youngberget al.,2019 and Zabukovšek et al., 2019).

Have the ability to display data quickly, easily and

efficiently. Having a security system in the form of a

password, can present comparative financial

statements in accordance with the data in the desired

period. Benefits of Computerized Accounting is to

use information technology based on Computer

Accounting Applications whose job is to obtain

financial reports automatically, quickly and have a

better level of accuracy than manually (Widjaja et

al., 2018 and Sternad et al., 2019). Have the ability

to display data quickly, easily and efficiently. Has a

security system in the form of a password, can

present comparative financial reports in accordance

with the data in the desired period. BUMDES

Financial Application, is an application developed to

help the financial management and administrative

management of BUMDES, BUMDES Financial

Applications are developed based on daily

operational needs that will be met when running

BUMDES, by adopting other financial business

entities. So that the flow and reporting meet

financial reporting standards. Althunibat et al (2019)

states that if you want to implement an ERP system,

the infrastructure includes production, payroll, sales,

purchasing and financial reporting. All activities are

integrated as a whole and carried out simultaneously

through one window.

Bhattacharya et al (2019) discusses The

Effectiveness of the Accounting Information System

Under the Enterprise Resources Planning (ERP)

states that the ERP system will support and create an

effective running of the organization. The research

needs to be followed up on the scale of government

organizations so that it can be seen how effective the

system is capable of creating effectiveness in local

government. Based on the results of research by

Beselga and Alturas (2019) that the success of ERP

implementation is measured by the resulting

financial statements. The success of the system is in

harmony with the perception of its users (users) and

has an impact on service. The conclusion of his

research states that the implementation of ERP

systems can improve the timeliness in publishing

financial reports. These results indicate that the ERP

system is able to shorten the flow of the process of

making financial statements because of its ability to

coordinate and integrate information data across

business processes. A fundamental question is

whether non-profit organizations such as local

governments are ready to run ERP where the local

government is currently implementing Regional

Management Information System where the

component is one of the ERP infrastructure applied.

2 METHOD

This study uses primary data.The hypothesis was

tested by using Structural Equation Modeling with

SMART PLS software 3.0. The data analysis

technique in this research employed Structural

Equation Modeling (SEM). The equationisformed as

follows:

Y = α + b1X1 + b2X2 + b3X3+ b4X4 +

b5X5+b6Z+e

X1 = Technological Resistance

X2 = Understanding

X3 = Human Resources

X4 = Financial Supporting

X5 = Training

Z = Easy to Use

Y = Successful implementation of the

Village Enterprise Enterprise Resource Planning

(ERP) Base Application

b1,….b5 = Coefficient

α = Constant

e = Error

Analysis using SEM requires some suitability

index to measure the correctness of data and models.

3 RESULT

3.1 Result

3.1.1 Evaluation of Structural Model (Inner

Model)

The evaluation of inner model through the

bootstrapping menu also generates t-statistics values.

The criteria are t-statistic> 1.66 (value α = 5%, one

tail). The result of t-statistics value in the table path

coefficients is presented in the following Figure 1 as

a follows :

EBIC 2019 - Economics and Business International Conference 2019

10

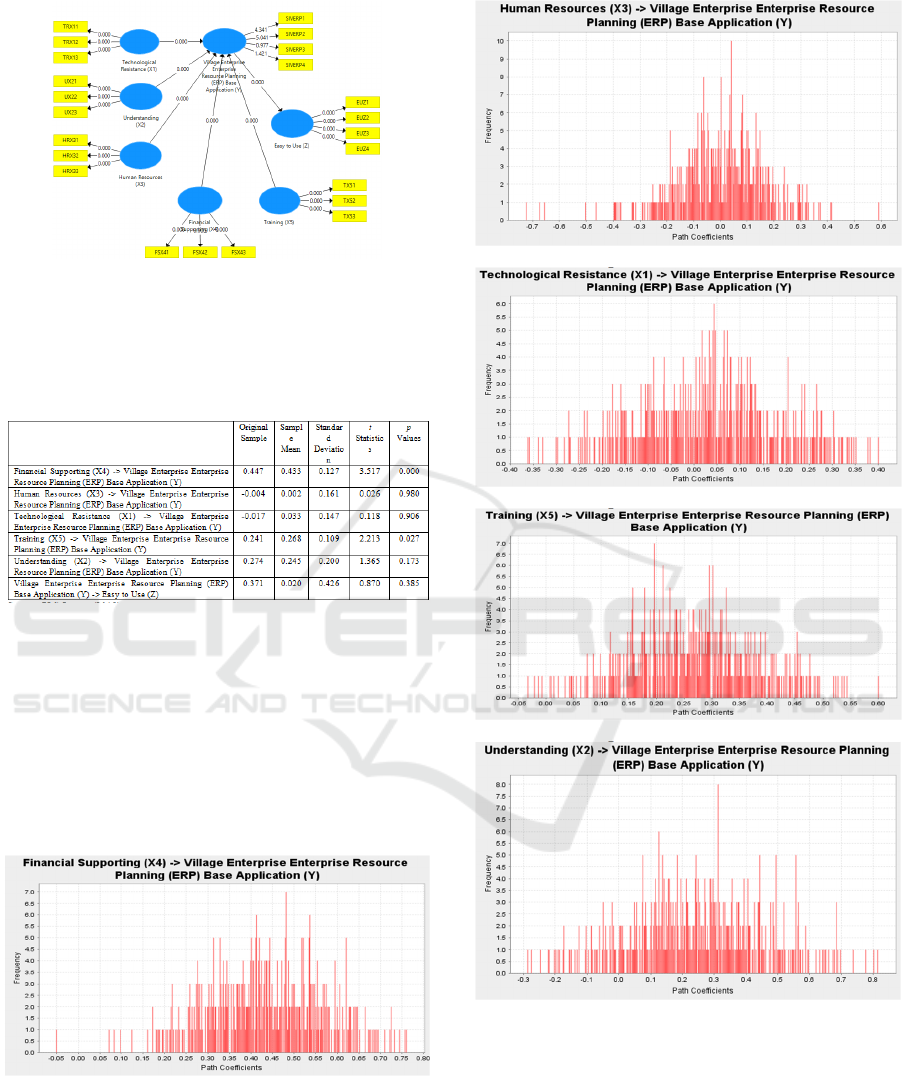

Figure 1. Overall Model with Coefficient

The statistic result of this research in the following

Table1 :

Table 1. Path Coefficients

Source: PLS Output (2019).

These results show that the financial supporting

and training to the successful implementation of the

Village Enterprise Resource Planning (ERP) Base

Application andtechnological resistance,

understanding of task and human resources are not

influence. The Easy to Use as intervening variable is

not influence.The path coefficient generated is in the

following Figure as a follow :

Source: PLS Output (2019).

Source: PLS Output (2019).

Source: PLS Output (2019).

Source: PLS Output (2019).

Source: PLS Output (2019).

Enterprise Resource Planning (ERP) User Acceptance Model with Easy to Use as Intervening Variable

11

Source: PLS Output (2019).

Source: PLS Output (2019).

Figure 2. Path Coefficient Figure

The statistic result in the following Table2 :

Table 2. Indirect Effects Total

Easy to

Use (Z)

Easy to Use (Z)

Financial Su

pp

ortin

g

(

X4

)

0.166

Human Resources

(

X3

)

-0.002

Technolo

g

ical Resistance

(

X1

)

-0.006

Training (X5) 0.089

Understanding (X2) 0.101

Village Enterprise Enterprise Resource

Planning (ERP) Base Application (Y)

Source: PLS Output (2019).

The Total Effect show inTable 3 as a follows :

Table 3. Total Effects

Village Enterprise Enterprise

Resource Planning (ERP)

Base Application (Y)

Easy to Use (Z)

Financial Supporting (X4) 0.447

Human Resources (X3) -0.004

Technological Resistance

(X1)

-0.017

Training (X5) 0.241

Understanding (X2) 0.274

Village Enterprise

Enterprise Resource

Planning (ERP) Base

Application (Y)

Source: PLS Output (2019).

The results of the Table show that through the

Financial Supporting variable is the strongest

traversed by the Easy to Use variable. In addition to

hypothesis testing through the bootstrapping menu

that produces t-statistics, inner model evaluation is

also done by reviewing the R-Square value. The R-

square value generated from the inner model

evaluation is presented in the following Figure 3 :

Source: PLS Output, (2019)

Figure 3. F Square

The results show from the Figure 3 show that

financial supporting and training are significant. The

R Square show in Table 3 as a follows :

Table 3. R-Square Value

R

Square

R

Square

Adjusted

Eas

y

to Use

(

Z

)

0.138 0.127

Village Enterprise Enterprise

Resource Planning (ERP)

Base A

pp

lication

(

Y

)

0.452 0.415

Source: PLS Output. (2019).

The results showed a coefficient of determination

equal to 41.5 %.

3.2 Discussion

ERP is part of the entity's infrastructure and is very

important for the survival of the company. Everyone

and the part that will be affected by the ERP must be

involved and provide support. ERP exists to support

business functions and increase productivity, not

vice versa (Calisir et al., 2009, Lim et al., 2005,

Seymour et al., 2007 and Regmi et al., 2019). The

purpose of ERP implementation is to improve the

competitiveness of rural business entities. There are

certain methodologies for ERP implementation that

are more guaranteed success. What needs to be done

is to identify the risks involved in ERP

implementation and then how to manage them. The

EBIC 2019 - Economics and Business International Conference 2019

12

potential for successful implementation will be even

greater if these risks can be minimized.

Strengthen the ability of implementation to

estimate the resources and time needed to carry out

functions in ERP implementation projects. This

inability is generally caused by less detailed

planning, which is usually due to a lack of

experience and knowledge of the project

management team regarding similar work. It could

also be due to the misperception of the implementers

of the scope of work as outlined in the standard for

various reasons (Fiaz et al., 2018, Hasan, 2018, Ding

et al., 2019 and Okcu et al., 2019). Or because the

initial planning was made only for the needs of

fulfilling administrative compliance, for example for

the needs of auction selection, project charter,

billing, and the like

ERP systems tend to replace the old system at

both the tactical and management levels. Everything

must be run consistently which means the way that

is applied in running something must be the same for

all areas. Besides that special treatment will be

carried out in one area will not be realized without

changing the system configuration. Some of the

causes of ERP implementation failures are training.

The biggest difficulty lies in changing the practice of

work that must be done. Besides that training that

involves many modules should be carried out.

Companies must choose between changing business

processes to adjust the system or vice versa, with

implications in terms of cost and time to change the

system. Only a few organizations implement ERP

without consulting a consultant. However,

consultants often do acts that harm their clients by

not sharing responsibility.

4 CONCLUSIONS

The results show that financial supporting and

training to the successful implementation of the

Village Enterprise Resource Planning (ERP) Base

Application and technological resistance,

understanding of task and human resources are not

influence and Easy to Use as intervening variable is

not influence.

REFERENCES

Alsoub, R. K., Alrawashdeh, T. A., &Althunibat, A. 2018.

User Acceptance Criteria For Enterprise Resource

Planning Software Systems. International Journal Of

Innovative Computing Information And Control,

14(1), 297-307.

Althunibat, A., Zahrawi, A. A., Tamimi, A. A.,

&Altarawneh, F. H. 2019. Measuring the Acceptance

of Using Enterprise Resource Planning (ERP) System

in Private Jordanian Universities Using TAM Model.

International Journal of Information and Education

Technology, 9(7).

Amoako, G.K., & Salam, A. F. 2004. An extension of the

technology acceptance model in an ERP

implementation environment. Information &

management, 41(6), 731-745.

Beselga, D., & Alturas, B. 2019. Using the Technology

Acceptance Model (TAM) in SAP Fiori. In World

Conference on Information Systems and Technologies

(pp. 575-584). Springer, Cham.

Bhattacharya, M., Wamba, S. F., &Kamdjoug, J. R. K.

2019. Exploring the Determinants of ERP Adoption

Intention: The Case of ERP-Enabled Emergency

Service. International Journal of Technology Diffusion

(IJTD), 10(4), 58-76.

Calisir, F., AltinGumussoy, C., & Bayram, A. 2009.

Predicting the behavioral intention to use enterprise

resource planning systems: An exploratory extension

of the technology acceptance model. Management

research news, 32(7), 597-613.

Ding, Q., Wang, X., Tian, J., & Wang, J. 2019.

Understanding the Acceptance of Teaching Method

Supported by Enterprise WeChat in Blended Learning

Environment. In 2019 International Symposium on

Educational Technology (ISET) (pp. 211-214). IEEE.

Fiaz, M., Ikram, A., & Ilyas, A. 2018. Enterprise Resource

Planning Systems: Digitization of Healthcare Service

Quality. Administrative Sciences, 8(3), 38.

Hasan, B. 2018. Effects of General and ERP Self-Efficacy

Beliefs on the Acceptance of ERP Systems. Journal of

Information & Knowledge Management, 17(03),

1850031.

Lim, E. T., Pan, S. L., & Tan, C. W. 2005. Managing user

acceptance towards enterprise resource planning

(ERP) systems–understanding the dissonance between

user expectations and managerial policies. European

Journal of Information Systems, 14(2), 135-149.

Nah, F. F. H., Tan, X., &Teh, S. H. 2004. An empirical

investigation on end-users' acceptance of enterprise

systems. Information Resources Management Journal

(IRMJ), 17(3), 32-53.

Okcu, S., Koksalmis, G. H., Basak, E., &Calisir, F. 2019.

Factors Affecting Intention to Use Big Data Tools: An

Extended Technology Acceptance Model. In Industrial

Engineering in the Big Data Era (pp. 401-416).

Springer, Cham.

Pasaoglu, D. 2011. Analysis of ERP usage with

technology acceptance model. Global Business and

Management Research, 3(2), 157-165.

Regmi, R., Zhang, Z., Khanal, S., Zhang, H., & Kim, J.

2019. An empirical study on user acceptance of ERP

system by international students in Chinese HEIs: A

TAM approach. International Journal of Higher

Education, 6(1).

Enterprise Resource Planning (ERP) User Acceptance Model with Easy to Use as Intervening Variable

13

Seymour, L., Makanya, W., &Berrangé, S. 2007. End-

users’ acceptance of enterprise resource planning

systems: An investigation of antecedents. In

Proceedings of the 6th annual ISOnEworld conference

(pp. 1-22).

Suriadi, A, Rudjiman, Mahalli, K,,Achmad, N (2015). The

Applicative Model of The Village_Owned Enterprises

(BUMDES) Development In North Sumatera. Global

Journal of Arts, Humanities and Social Sciences 3(12),

48-62.

Sternad,Zabukovšek, S., Picek, R., Bobek, S.,

ŠišovskaKlančnik, I., &Tominc, P. 2019. Technology

Acceptance Model Based Study of Students’ Attitudes

Toward Use of Enterprise Resource Planning

Solutions. Journal of Information and Organizational

Sciences, 43(1), 49-71.

Turetken, O., Ondracek, J., &IJsselsteijn, W. 2019.

Influential characteristics of enterprise information

system user interfaces. Journal of Computer

Information Systems, 59(3), 243-255.

Widjaja, H. A. E., Larasati, A. P., Respati, R., &Ranaputri,

V. 2018. The Evaluation of Enterprise Resource

Planning (ERP) Financial Accounting and Control

Using Technology Acceptance Model. In 2018

International Conference on Computing, Engineering,

and Design (ICCED) (pp. 69-74). IEEE.

Youngberg, E., Olsen, D., & Hauser, K. 2009.

Determinants of professionally autonomous end user

acceptance in an enterprise resource planning system

environment. International journal of information

management, 29(2), 138-144..

Zabukovšek, S. S., Bharadwaj, S. S., Bobek, S., &Štrukelj,

T. 2019. Technology acceptance model-based research

on differences of enterprise resources planning

systems use in India and the European Union.

Engineering Economics, 30(3), 326-338.

EBIC 2019 - Economics and Business International Conference 2019

14