The Implementation Corporate Social Responsibility Factors That

Affect the Corporate Political Activities in Riau Province

Made Devi Wedayanti

1

, Achmad Nurmandi

2

and Hasse J.

2

1

Universitas Islam Riau, Pekanbaru, Indonesia

2

Department of Political Science, Universitas Muhammadiyah Yogyakarta, Yogyakarta, Indonesia

Keywords:

Factors, Corporate Social Responsibility, Corporate Political Activity, Individual Factors, Institutional

Factors, Company Factors.

Abstract:

This study shows the implementation Corporate Social Responsibility factors that affect the Corporate Political

Activities in Riau Province. The research problem is still coming up from the companies side due to the

implementation of corporate social responsibility. The research problem is that there are still companies that

make the implementation of corporate social responsibility a form of company political activity. This research

is descriptive qualitative, the method of collecting data in the form of information interviews. Analysis of the

data obtained is done through data collection, verification, presentation, and conclusions. The results of the

study are three factors that influence CSR part of the CPA, namely individual factors, institutional factors and

company factors.

1 INTRODUCTION

The theory developed about CSR comes more from

economics (Scherer and Palazzo, 2011). The defini-

tion of CSR politics from political science or public

administration focuses more on corporate responsibil-

ity activities as political actors that focus on public

deliberation, collective decisions and public services

(Scherer and Palazzo, 2011), which not only provide

health facilities , education and environmental devel-

opment. The idea of a company as a political actor

in CSR is a challenge for future research (Frynas and

Stephens, 2015).

Literature review on political CSR literature has

two important aspects, namely legitimacy and insti-

tutions. Legitimacy is an important factor for com-

panies to always exist in certain countries, which is

a socially constructed reason or argument to provide

justification for company actions that are accepted

by the public (Scherer and Palazzo, 2011). Sec-

ond, CSR politics is related to institutional analysis

in social networks, national institutions and political

rules. The institutional review of CSR analyzes in-

stitutional mechanisms (El Ghoul et al., 2017), in-

volvement of civil society organizations, negotiating

CSR standards in various countries (Den Hond et al.,

2014) and issues such as the division of responsibil-

ities within multinational companies between local

roles and roles at the international level (Jamali and

Karam, 2018).

In the context of political institutions CSR has var-

ious types according to the political system of the

country concerned. CSR politics in the United States

and Europe is characterized by less regulation and

more incentives for the company’s social role (Matten

and Moon, 2008). Meanwhile in Japan, France and

South Korea, CSR politics gives a greater role to the

collaboration of workers, trade unions and civil soci-

ety organizations (Jamali and Karam, 2018). Philips,

a company in the Netherlands, has been developing

energy saving lamps for a long time, and is trying to

lobby the European Union to legalize their products.

Car companies in Germany reject filters that prevent

air pollution in diesel cars and encourage other types

that are more efficient. In developing countries, (Fry-

nas and Stephens, 2015) note that there are still re-

search gaps about complex formal and informal inter-

actions. The institutional context is not only related to

the state’s formal institutional mechanisms and poli-

cies but also the social values inherent in them. The

institutional and state values in question heterogeneity

and content versus homogeneity and consensus color

the implementation of CSR (Blindheim, 2015).

(Den Hond et al., 2014) introduced the concept

of CSR as a form of CPA (Corporate Political Activ-

ity) activity. CSR activities are always related to the

390

Wedayanti, M., Nurmandi, A. and J., H.

The Implementation Corporate Social Responsibility Factors That Affect the Corporate Political Activities in Riau Province.

DOI: 10.5220/0009162203900394

In Proceedings of the Second International Conference on Social, Economy, Education and Humanity (ICoSEEH 2019) - Sustainable Development in Developing Country for Facing Industrial

Revolution 4.0, pages 390-394

ISBN: 978-989-758-464-0

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

company’s political activity to increase its reputation.

Companies increase CSR activities to gain political

support, enlarge political coalitions, open access to

policy makers (Den Hond et al., 2014). This form of

CSR and CPA can be seen from the results of strate-

gies used by companies in actively influencing policy

makers (Den Hond et al., 2014). Thus it can be con-

cluded first, CSR and CPA independently influence

the reputation of the company. Second, the drive for

CSR as part of the CPA comes from the recognition

of problems generated through CSR and CPA efforts.

This research will be conducted in Riau Province.

Riau Province as the city which is the lyrics of the

oil city has many large and medium industrial com-

panies. Based on data from the Riau Province Central

Statistics Agency 2017, the total business sector of the

city is 526,966 companies with 14 types of compa-

nies. The author tries to answer what factors influence

CSR part of implementing the CPA. After conducting

research the Riau provincial government does not yet

have empirical data related to CSR of all provinces in

Riau only limited to making regional regulations Riau

province No. 6 of 2012 concerning corporate social

responsibility in Riau province, due to not running a

corporate social responsibility forum in each district

and for evaluation The implementation of corporate

social responsibility forums will be the next research

to be investigated. therefore this research is only lim-

ited to looking at CSR implementation factors which

are made into political activity of the company based

on the 2018 rehbein theory.

2 DISCUSSION

It is not always business in terms of CSR as a form of

political support that is said to be successful, there is

an implementation of CSR which makes companies

weak in getting political support. CSR sometimes has

contradictions with CPA policies. When a company

does not equate CSR and CPA, then shareholders can

be deliberately misled and provide references about

companies that cannot be trusted (Den Hond et al.,

2014).

Some researchers have also carried out studies on

supporting CSR not part of implementing the CPA.

An example of a company is a manufacturing com-

pany listed on the Indonesian stock exchange based

on this CSR which provides a misalignment of gov-

ernment tax management, this is related to increasing

the level of the company to implement CSR. A com-

pany in Slovenia develops a national corporate so-

cial responsibility (CSR) policy through multi-party

partnerships but because of the factors that support

the government, making it unable to obtain politi-

cal support, in this case the government becomes an

actor with executive power to support and support

CSR policies at the national (Golob and Hrast, 2018).

Multinational companies (MNCs) often carry out cor-

porate social responsibility (CSR) activities that sup-

port providing ’public goods’ and improving gover-

nance in policy making. This political CSR activity

(PCSR) will run well by increasing socio-political le-

gitimacy and is useful in building relations with the

state or other external stakeholders. Using theories

relying on resources, protection theory, and social

capital literature, finding MNC subsidiaries is highly

dependent on local resources, has a greater relation-

ship with related business managers and policy mak-

ers (Shirodkar et al., 2018). CSR taken is not part of

the CPA which is often caused because it is not related

to interests between the company and the government.

Other studies assess CSR and CPA strategies at the

macro level using safety factors and at the micro level

using company-level & individual factor factors (Re-

hbein et al., 2018) and In general institutional factors,

CSR and CPA related to macro planning are available

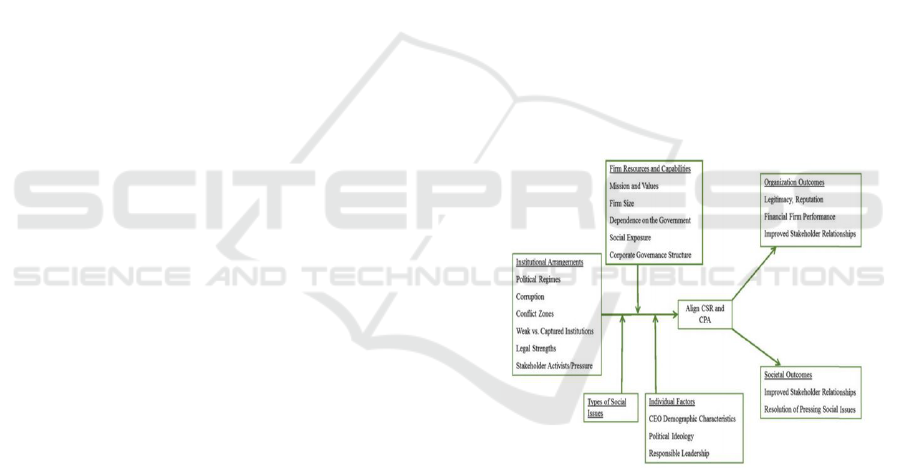

in the following figure:

Figure 1: CSR and CPA Related.

From the De Hond & Rehbein (Den Hond et al.,

2014)(Rehbein et al., 2018) study above, it can be

seen that the factors that influence CSR as part of

the CPA in the company have 3 factors, First, individ-

ual factors which state that the character of the CEO

or leader influences CSR as part of the CPA . Fur-

thermore, the second factor, which is the source of

resources and capabilities of the company, Rehbein

(Rehbein et al., 2018) says that mission and value,

company size, corporate governance structure, and

corporate social exposure are influencing factors in

supporting CSR as part of the CPA. The third fac-

tor, namely institutional environmental factors such

as corruption, legal strength, pressure pressure, stake-

The Implementation Corporate Social Responsibility Factors That Affect the Corporate Political Activities in Riau Province

391

holders become a supporting factor for CSR to be part

of the CPA (Rehbein et al., 2018).

First, individual factors consist of top leadership

characteristics, corporate structural characteristics of

CSR and CPA departments, and interactions between

these departments, and the presence of agents of so-

cial change in the company (Wickert and De Bakker,

2018). In individual factors, there are many individ-

uals, from CEOs, CSR managers to outside affairs

managers or public affairs managers who might have

an impact on the formation of corporate social and

political responses. However, (Aguinis and Glavas,

2012) note that at the individual level there is a lack of

information about individuals doing CSR. Most of the

discussion of previous researchers emphasized how

attitudes to protect, moral development, and commit-

ment to social problems enhance corporate CSR. Sim-

ilar research (Wickert and De Bakker, 2018) focuses

on social issues and seeks to understand the obsta-

cles faced by CSR managers in implementing CSR.

However, most research focuses on the role the CEO

plays in determining trade-offs between sharehold-

ers and stakeholder priorities. Similar research (Mel-

lahi et al., 2016) argues that the focus on top man-

agement is very important to understand the types

of non-market strategies developed by the company.

Previous research suggests that the flow of research

that emerges in responsible leadership can be a pos-

sible source of understanding top management deci-

sions. (Doh and Quigley, 2014), for example, focus

on how top management can develop a more inclusive

approach with regard to various stakeholders, while

(Strand, 2014) explores why the company’s sustain-

ability position is placed on the top management team

and whether this affects the organization. This can

represent a CSR problem at the company’s leadership

level and can facilitate alignment with CPA activities

that are also strategic (Hadani and Schuler, 2013).

Second, company resources & capability factors

Enterprise level factors such as company mission,

company values, shareholder ownership, structure

and governance, concessions and financial visibility

(Aguinis and Glavas, 2012). Similar research deals

with additional empirical studies and a review of the

literature examining resources in CSR corporate gov-

ernance (De Villiers et al., 2011) (Jamali and Karam,

2018) also examined for a comprehensive review of

this literature (Walls et al., 2012). With respect to

CPA, (Lux et al. 2011) based on previous analysis

provides an overview of the specific factors of the

company that shape the company’s political invest-

ment, such as company size, company diversification,

and government sales. Based on previous CPA and

CSR research, it is possible that the company’s re-

sources and capabilities have a significant role in driv-

ing company decisions in implementing CPA. The au-

thor previously found that it is important to integrate

several drivers that CSR is part of implementing the

CPA. For example, including company mission and

values, corporate strategy, financial resources, visibil-

ity, and social and political exposure all seem to be

important in supporting motivation to support CSR as

part of CPA (Mellahi et al., 2016).

Third, institutional environmental factors, compa-

nies will be motivated to make CSR as part of the

CPA determined by the environmental characteristics

of the country of origin of the company. Institutional

factors are determined from the social interactions

of the company’s home country to create incentives

and barriers to the development of corporate social

or political policies (Dorobantu et al., 2017)(Mantere

et al., 2009)(Mellahi et al., 2016)(Windsor, 2007).

But some research on institutions on CSR and CPA

has developed separately. In relation to CSR, there

is a broad debate about institutional factors that dis-

cuss the types of social policies, practices and report-

ing that are applied by companies (Jackson and Apos-

tolakou, 2010) (Marano and Kostova, 2016)(Mat-

ten and Moon, 2008)(Rathert, 2016). Similar re-

search has been carried out to understand the rela-

tionship between institutional factors and the possi-

bility that companies will form political connections

(Dorobantu et al., 2017) find that companies are more

likely to form political ties when they do business in

countries where governance is more corrupt and prop-

erty rights protected the weak in the country. Given

that institutional factors influence corporate decisions

regarding CSR in CPAs, it is likely that the politi-

cal and social institutional arrangements of the home

countries will affect work and influence the imple-

mentation of CSR as part of the CPA (Dorobantu

et al., 2017).

Riau Province is a province that has been estab-

lished as a plantation company. And from 210 com-

panies in Riau province based on the results of the

study, it was found that there were three factors that

influence CSR as part of the CPA, first individual fac-

tors: this factor can support CPA activities determined

by the background of stockholders and company lead-

ership background, the greater the shareholder’s role

and company leaders in the government, the greater

the activity of company activities that can be done. for

example if the company has a leader or shareholder

who has a background that comes from a general or a

holder of power, the implementation of company ac-

tivities will run well, both for licensing and company

security. the second factor, is the company factor con-

sisting of company mission, company size and cor-

ICoSEEH 2019 - The Second International Conference on Social, Economy, Education, and Humanity

392

porate social pressure. the more influential the com-

pany’s mission towards the government mission, the

greater the company’s political activity. the larger the

size of the company, the greater the movement of the

company’s political activity and the greater the com-

pany’s social pressure, the greater the company’s po-

litical activity. The third factor is institutional factors,

this factor contains the power of law, zone of con-

flict and corruption. the greater the company’s politi-

cal activity, the greater the legal strength held by the

company, the greater the company’s political activity,

the smaller the zone of conflict the company has. Fur-

thermore, the greater the company’s political activity,

the greater the likelihood of corporate corruption.

3 CONCLUSIONS

The implementation of corporate social responsibil-

ity is one form of corporate political activity and to

carry out corporate political activities, supporting fac-

tors are needed. The conclusion of this study is that

there are three supporting factors, first individual fac-

tors, second, company factors, third, institutional fac-

tors.

First individual factors: this factor can support

CPA activities determined by the background of

shareholders and company leadership background,

the greater the role of shareholders and company lead-

ers in the government, the greater the activities of

company activities that can be done. for example if

the company has a leader or shareholder who has a

background that comes from a general or a holder of

power, the implementation of company activities will

run well, both for licensing and company security.

the second factor, is the company factor consisting

of company mission, company size and corporate so-

cial pressure. the more influential the company’s mis-

sion towards the government mission, the greater the

company’s political activity. the larger the size of the

company, the greater the movement of the company’s

political activity and the greater the company’s social

pressure, the greater the company’s political activity.

The third factor is institutional factors, this factor con-

tains the power of law, zone of conflict and corruption.

the greater the company’s political activity, the greater

the legal strength held by the company, the greater the

company’s political activity, the smaller the zone of

conflict the company has. Furthermore, the greater

the company’s political activity, the greater the likeli-

hood of corporate corruption.

REFERENCES

Aguinis, H. and Glavas, A. (2012). What we know and

don’t know about corporate social responsibility: A

review and research agenda. Journal of management,

38(4):932–968.

Blindheim, B.-T. (2015). Institutional models of corpo-

rate social responsibility: A proposed refinement of

the explicit-implicit framework. Business & society,

54(1):52–88.

De Villiers, C., Naiker, V., and Van Staden, C. J. (2011).

The effect of board characteristics on firm envi-

ronmental performance. Journal of Management,

37(6):1636–1663.

Den Hond, F., Rehbein, K. A., de Bakker, F. G., and

Lankveld, H. K.-v. (2014). Playing on two chess-

boards: Reputation effects between corporate social

responsibility (csr) and corporate political activity

(cpa). Journal of Management Studies, 51(5):790–

813.

Doh, J. P. and Quigley, N. R. (2014). Responsible lead-

ership and stakeholder management: Influence path-

ways and organizational outcomes. Academy of Man-

agement Perspectives, 28(3):255–274.

Dorobantu, S., Kaul, A., and Zelner, B. (2017). Nonmarket

strategy research through the lens of new institutional

economics: An integrative review and future direc-

tions. Strategic Management Journal, 38(1):114–140.

El Ghoul, S., Guedhami, O., and Kim, Y. (2017). Country-

level institutions, firm value, and the role of corporate

social responsibility initiatives. Journal of Interna-

tional Business Studies, 48(3):360–385.

Frynas, J. G. and Stephens, S. (2015). Political corporate

social responsibility: Reviewing theories and setting

new agendas. International Journal of Management

Reviews, 17(4):483–509.

Golob, U. and Hrast, A. (2018). The reluctant state: A failed

attempt to develop a national csr policy. In The Crit-

ical State of Corporate Social Responsibility in Eu-

rope, pages 121–136. Emerald Publishing Limited.

Hadani, M. and Schuler, D. A. (2013). In search of el do-

rado: The elusive financial returns on corporate po-

litical investments. Strategic Management Journal,

34(2):165–181.

Jackson, G. and Apostolakou, A. (2010). Corporate so-

cial responsibility in western europe: an institutional

mirror or substitute? Journal of business ethics,

94(3):371–394.

Jamali, D. and Karam, C. (2018). Corporate social respon-

sibility in developing countries as an emerging field of

study. International Journal of Management Reviews,

20(1):32–61.

Mantere, S., Pajunen, K., and Lamberg, J.-A. (2009). Vices

and virtues of corporate political activity: The chal-

lenge of international business. Business & Society,

48(1):105–132.

Marano, V. and Kostova, T. (2016). Unpacking the institu-

tional complexity in adoption of csr practices in multi-

national enterprises. Journal of Management Studies,

53(1):28–54.

The Implementation Corporate Social Responsibility Factors That Affect the Corporate Political Activities in Riau Province

393

Matten, D. and Moon, J. (2008). “implicit” and “explicit”

csr: A conceptual framework for a comparative under-

standing of corporate social responsibility. Academy

of management Review, 33(2):404–424.

Mellahi, K., Frynas, J. G., Sun, P., and Siegel, D. (2016). A

review of the nonmarket strategy literature: Toward a

multi-theoretical integration. Journal of Management,

42(1):143–173.

Rathert, N. (2016). Strategies of legitimation: Mnes and

the adoption of csr in response to host-country insti-

tutions. Journal of International Business Studies,

47(7):858–879.

Rehbein, K., den Hond, F., and Bakker, F. G. (2018). Align-

ing adverse activities? corporate social responsibility

and political activity. In Corporate Social Responsi-

bility, pages 295–324. Emerald Publishing Limited.

Scherer, A. G. and Palazzo, G. (2011). The new political

role of business in a globalized world: A review of

a new perspective on csr and its implications for the

firm, governance, and democracy. Journal of man-

agement studies, 48(4):899–931.

Shirodkar, V., Beddewela, E., and Richter, U. H. (2018).

Firm-level determinants of political csr in emerging

economies: evidence from india. Journal of business

ethics, 148(3):673–688.

Strand, R. (2014). Strategic leadership of corporate sustain-

ability. Journal of Business Ethics, 123(4):687–706.

Walls, J. L., Berrone, P., and Phan, P. H. (2012). Corpo-

rate governance and environmental performance: Is

there really a link? Strategic Management Journal,

33(8):885–913.

Wickert, C. and De Bakker, F. G. (2018). Pitching for so-

cial change: Toward a relational approach to selling

and buying social issues. Academy of Management

Discoveries, 4(1):50–73.

Windsor, D. (2007). Toward a global theory of cross-border

and multilevel corporate political activity. Business &

Society, 46(2):253–278.

ICoSEEH 2019 - The Second International Conference on Social, Economy, Education, and Humanity

394