Identify Theft Detection on e-Banking Account Opening

Roxane Desrousseaux, Gilles Bernard and Jean-Jacques Mariage

LIASD Laboratory, Paris 8 University, France

Keywords:

Machine Learning, Fraud Detection, Behavior, Pattern, Banking, Identity Theft.

Abstract:

Banks are compelled by financial regulatory authorities to demonstrate whole-hearted commitment to finding

ways of preventing suspicious activities. Can AI help monitor user behavior in order to detect fraudulent activ-

ity such as identity theft? In this paper, we propose a Machine Learning (ML) based fraud detection framework

to capture fraudulent behavior patterns and we experiment on a real-world dataset of a major European bank.

We gathered recent state-of-the-art techniques for identifying banking fraud using ML algorithms and tested

them on an abnormal behavior detection use case.

1 INTRODUCTION:

BACKGROUND AND

MOTIVATIONS

Banking activity is changing. The customer relation-

ship, hitherto physical and face-to-face, is becoming

digitalized. Customers no longer need to go to agen-

cies and carry out by themselves more and more on-

line procedures. Even account opening is now of-

ten completely digital and banks need to insure that

the prospect (i.e person not yet customer) is the per-

son that he/she pretends to be and the reasons for its

account opening. Banks are particularly concerned

about detecting identity theft because this type fraud

can lead to huge losses of money, when an identity

theft has obtained a personal loan for example. This

type of fraud also generates a bad image of the bank

and is subject to international sanctions in the case of

an account used for financial trafficking.

Banks once had a close relationship with their

customers which is now often remote. The AI ap-

proach is based on Knowing Your Customer (KYC)

by knowing his behavior. For banking, the KYC

mainly refers to the requirement of checking a cus-

tomer’s ID when opening a new account. However,

faking an ID is so easy that identity theft is one of

the fastest-growing banking issues. There is no better

way to know your future client and identify risk than

by analyzing his/her behavior.

The main focus of this study is to help decide

whether a prospect opening a banking account on the

bank’s website is the person he/she claims to be.

Analysis of interaction between bank and cus-

tomer on a mass scale is new. The scientific com-

munity has put much effort to propose solutions that

could benefit to the banking industry. Non-linear

techniques as neural networks (NNs) seem doubtless

appropriate for detecting elaborate and heterogeneous

banking frauds. NNs offer means of dimensional re-

duction that maintain the characteristics and complex-

ity of the data structure. By preserving the relation-

ships, they make it possible to work on reduced for-

mats while also giving the ability to analyze more

complex problems (Zaslavsky and Strizhak, 2006).

2 RELATED WORK

The scientific literature signals as financial anomalies:

transactional fraud, money laundering, impersonation

or creation of false accounts, account theft, promo-

tional abuse, user behavior, cybersecurity.

The analysis of abnormal activity requires a large

amount of past data to learn what characterizes a be-

havior, based on time series, over several scales of

time. The main idea is to model a normal behavior

and find the deviant ones. Anomaly detection leads to

specific problems identified in the literature: 1) defin-

ing what a normal behavior is, because types of be-

haviors are numerous, 2) difficulty to adapt to a nor-

mal change of behavior without causing false alarms.

In order to model user’s behavior on a website or ap-

plication, many researches use variables such as the

number of visited pages, the keystroke or click speed,

the number of failed connections, the IP address and

device used, the number of specific events in a cer-

556

Desrousseaux, R., Bernard, G. and Mariage, J.

Identify Theft Detection on e-Banking Account Opening.

DOI: 10.5220/0008648605560563

In Proceedings of the 11th International Joint Conference on Computational Intelligence (IJCCI 2019), pages 556-563

ISBN: 978-989-758-384-1

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

tain time-lapse (Shanmugapriya and Ganapathi, 2017;

Mazzawi et al., 2017).

Detection of banking anomalies gathers informa-

tion on the customer, his accounts, his geographical

location, time, and information related to his sub-

scribed products. The space of banking transactions

is characterized by potentially large dimensions and

sparse vectors. The data brings together millions of

transactions per day, millions of individual account

activities, hundreds of product types. It is difficult to

effectively extract relevant attributes; money launder-

ing for example can range from a single transaction to

a series of complex transactional activities spanning

over several months. In terms of engineering, this

represents one of the worst forms of dimensionality

disorder with large scale differences and overloading

of variables.

Confidentiality restrictions of banking related data

have limited the progression of research. There is a

real lack of access to financial data for fraud detection

research. In order to deal with this problem, novel

approaches in fraud detection involve the use of sim-

ulators to produce enough financial data which con-

tains both the normal and fraudulent behavior. This

technique uses the advantages and benefits of simu-

lation, applied to financial domains to avoid the legal

and privacy concerns of real datasets. The main con-

cept behind the approach is to learn how the real cus-

tomers behave and interact as described by the real

data, and through simulation, recreate this behavior

by simulated fictitious customers in a way that does

not represent a leak of private financial records.

The main research topic in the literature concern-

ing banking fraud is the detection of fraudulent credit

card transactions (Ngai et al., 2011; Krishnapriya,

2017; Anandakrishnan et al., 2018). A multitude of

techniques have been applied, ranging from simple

regression to sophisticated NNs. In a study (Sun-

darkumar and Ravi, 2015), Logistic Regression per-

formances on credit card churn prediction and insur-

ance fraud detection was compared to an undeter-

mined Decision Tree model, Support Vector Machine,

Probabilistic Neural Network, Group Method of Data

Handling and Multi-Layer Perceptron. More recently,

studies focus on using more elaborated NNs for de-

tecting transactional fraud, like Convolutional Neural

Networks (Fu et al., 2016), Autoencoder and Genera-

tive Adversarial Network (Chen et al., 2019).

In a study, (Wang et al., 2017) use Recurrent Neu-

ral Networks (RNNs) for detecting fraudulent trans-

actions on an E-commerce site which is similar to our

experiments because they also used browsing history

to characterize users behavior. They ignored all ses-

sions that did not lead to an order, labelled the fraudu-

lent orders using a business’s department sample and

modeled web sessions as sequences of clicks. They

also included information like dwell time (time spent

on a particular page), page loading time, browsing

time, geolocation, URL. . . Clicks of the same session

are fed into the model in the time order, and a risk

score is outputted for the last click (i.e. the check-

out action) for each session, indicating how suspi-

cious the session is. Performances of RNNs (vary-

ing number of layers and of neurons) are compared

to traditional methods including logistic regression,

Naive Bayes, SVM and Random Forest. Results are

validated using historical data and their research con-

cluded that their framework was able to support the

transaction volumes they had, while providing an ac-

curacy never achieved by traditional methods based

on aggregate features.

To our knowledge this is the first study on detect-

ing banking identity theft with ML algorithms on a

real-world dataset. The remainder of this paper is or-

ganized as follows: next section presents a description

of the real dataset used for our study. We will then in-

troduce the experimental setup with algorithms tested

and assessment metrics used. Finally we will provide

some results and analysis.

3 REAL DATA ANALYSIS

In this section we introduce the dataset used for de-

tecting identity theft, the preprocessing steps done

such as feature creation, and the preliminary statis-

tical analysis that allowed us to get more insights on

the fraudulent patterns.

3.1 Dataset Description

Data is provided by our industrial partner and due to

confidentiality policy it can not be provided in public

access. The dataset consists in navigational logs, con-

taining information about users activity on the bank’s

website. The browsing information captured in these

logs is spread among ≈ 50 tables (Page table, Click

table, Geolocation table, Device Table, etc. . . ). The

initial volume of logs available was enormous (Click

table for example represents between 50-90 millions

of lines per month). Approximatively 11 month of

browsing stored in a Hive database on a Hadoop clus-

ter, representing more than 2 million connexions per

month, 80 000 – 85 000 sessions for account opening.

The first preprocessing step was to gather, filter

and aggregate the navigational logs. Fraud team pro-

vided files containing samples of prospect numbers

Identify Theft Detection on e-Banking Account Opening

557

and their corresponding label (account opened or re-

fusal because of a manual identity theft detection by

the expert teams).

At some point of the online boarding process,

the prospect is assigned a prospect number and has

to login to his/her temporary account, to upload

his/her ID justification and other supporting docu-

ments. Prospects can take several web sessions to

complete their onboarding process, they can decide

to interrupt their inscription, come back later to ter-

minate and submit their form.

In our study, we filtered out navigational sessions

of interest by finding all sessions and activity related

to the prospects included in our sample. This was

done by finding trace in the navigational logs of a con-

nexion on the temporary account. The join queries

between all navigational tables are done on primary

database keys such as the web browsing session id,

session timestamps and other action/trigger event ids,

keys we can use to link information included in the

scattered data source. We created the explanatory

variables with Spark, we modeled the general behav-

ior of each prospect on the bank’s website and on-

boarding form: number of sessions, sessions dura-

tion, navigation speed (between pages, clicks), types

and average number of pages visited, device used,

screen resolution, geolocation, information provided

for account opening. The information given on the

online form can be numerical (savings amount, prop-

erty titles value) or categorical (income bracket, type

of working contract. . . ).

Finally we looked at the nature of the features cre-

ated, transformed and scaled them properly following

the general rules. Continuous values are scaled in the

range of 0 to 1, distributed normally with mean 0 and

standard deviation 1 (this is not fixed but ensuring a

correct range of input can help training). For cate-

gories without ordinal relationship, we used a One-

hot encoding, producing a binary vector with 0 in all

dimensions except 1 for the category the data belongs

to.

3.2 Preliminary Statistical Analysis

After gathering the data and constructing the features,

we did a preliminary analysis of the dataset. This step

is essential in every Data Science project and can pro-

vide interesting insights on the data. In our study,

we plotted variable distribution and correlation ma-

trix using Python visualization libraries and found the

following facts:

• Number of pages visited per session and click

speed don’t evolve over time and stay approxima-

tively the same for each user session (thus behav-

ior doesn’t change so much).

• A bigger number of pages visited does not always

mean longer sessions.

• Fraudsters tend to be faster in their navigation and

make shorter sessions.

• All fraudsters declare the same kind of profile rev-

enue.

4 EXPERIMENTS

This section is divided into three subsections. In the

first subsection we will describe the ML models used

for identity theft detection and preprocessing stage.

In the second, the assessment metrics used. The last

section presents our results.

The questions we wish to address are the follow-

ing:

• Which algorithms are going to work best; espe-

cially do multi-layer NNs have better results than

standard classifiers?

• Will oversampling lead to better performances?

• More generally how will preprocessing affect de-

tection results? Will the results be better with

multi-layer Autoencoder (AE) than with Principal

Component Analysis (PCA)?

4.1 Machine Learning Models

We present here the ML classifiers used in this study.

The low proportion of abnormal observations (out-

liers) is an issue in anomaly detection and unbalanced

learning. Anomalies are scarce and therefore little

present, and standard ML algorithms are not able to

learn classes of data that are not enough represented

in the learning dataset. Therefore, specific algorithms

have been devised for this task.

We studied three types of ML models: basic mod-

els, outlier dedicated algorithms, both from Scikit-

Learn library, and sophisticated NNs built with Keras

library. In the preprocessing stage, for dimension re-

duction, we compared PCA (from Scikit-Learn) with

Multi Layer AE (built with Keras) before applying

these models.

4.1.1 ML Classifiers

The following basic models were tested: k-Nearest

Neighbors (k-NN), linear SVM (SVM), CART De-

cision Tree (DT), Random Forest (RF), Multi Layer

Perceptron, in reality a Bilayer Perceptron with just

NCTA 2019 - 11th International Conference on Neural Computation Theory and Applications

558

one hidden layer (BLP), Adaboost, Naives Bayes

(NB) and Quadratic Discriminant Analysis (QDA).

As specific outlier detection models, we have cho-

sen three algorithms that are gaining popularity in

such tasks: Local Outlier Factor (LOF), Isolation For-

est (IForest), One-class SVM (OCSVM). A multitude

of variants of these algorithms have been proposed.

As a more sophisticated model, we built a Multi

Layer Perceptron (MLP) with three hidden layers

having rectified linear unit (ReLu) as activation func-

tion, a sigmoid function for the last layer, and a bi-

nary cross entropy loss function because we are in a

binary classification problem. The number of neurons

of each hidden layer is set to ≈ 80% of the number of

input features, as this was the value that gave the best

preprocessing performances.

We give below a brief description focusing on the

less well known algorithms.

IForest (Liu et al., 2008). This algorithm is based

on decision trees. The method takes advantage of two

quantitative properties of the outliers: (a) they have

fewest instances and (b) their attribute values greatly

differ from those of the more frequent classes. Thus,

outliers are more likely to be isolated early in the tree

and hence have shorter paths to the root.

LOF (Breunig et al., 2000). The LOF algorithm fo-

cuses on analyzing local densities of the data space.

It identifies regions of similar density and consider

as outliers data points from lower density regions. It

is based on k-NN; the density is estimated from the

distances between neighbours, computing the local

reachability of a point, given by the inverse average

reachability distance from its k neighbours (equation

1).

lrd(p) = 1/

∑

o∈KNN(p)

rdist

k

(p ← o)

|KNN(p)|

(1)

where KNN(p) is the set of p’s nearest neighbours.

The (asymmetric) reachability distance rdist from o

to p is defined by equation 2.

rdist

k

(p ← o) = max{k − dist(o), d(p,o)} (2)

The final LOF score then compares the locally rel-

evant lrd values:

LOF

k

(p) =

1

|KNN(p)|

∑

o∈KNN(p)

lrd

k

(o)

lrd

k

(p)

(3)

OCSVM (R

¨

atsch et al., 2000). In 2000, the popu-

lar Support Vector Machines algorithm was adapted

to focus on outliers in the following way. The idea is

to classify all non outlier data in one group, compute

the probability distribution of this group. A discrim-

inant function compares the probability of member-

ship of a given point, comparing it with a parame-

ter ρ ∈ [0,1]; this parameter is estimated by solving a

quadratic function. Let x

1

,x

2

,...,x

l

be training exam-

ples belonging to one class X, where X is a compact

subset of R

N

. Φ : X −→ H is a kernel map which

transforms the training examples to another space.

Then, to separate the data set from the origin, one

needs to solve the following quadratic programming

problem:

min

1

2

kwk

2

+

1

vl

l

∑

i=1

ξ

i

− ρ (4)

subject to

(w · Φ (x

i

)) ≥ ρ − ξ

i

i = 1, 2, . . ., l ξ

i

≥ 0 (5)

If w and ρ solve this problem, then the decision

function

f (x) = sign((w · Φ(x)) − ρ) (6)

will be positive for most examples contained in the

training set.

4.1.2 AE Dimensional Reduction

We provide below a description of the multi layer

sparse Autoencoder NN that we used for preprocess-

ing, against PCA.

AE. An AE is an autosupervised NN that applies

backpropagation and whose objective is to learn to re-

produce input vectors {x(1),x(2),...x(m)} as outputs

{ ˆx(1), ˆx(2),... ˆx(m)}.

In other words, it learns an approximation of the

identity function. By forcing constraints on the net-

work, such as limiting the number of hidden units,

interesting structure about the data can be discovered.

Anomaly detection using dimensionality reduction is

based on the assumption that data has variables cor-

related with each other and can be embedded into a

lower dimensional subspace in which normal samples

and anomalous samples appear significantly different.

Consider an AE with several hidden layers; acti-

vation of unit i in layer l is given by equation 7.

a

(l)

i

= f

n

∑

j=1

W

(l−1)

i j

a

(l−1)

j

+ b

(l)

i

!

(7)

where W and b parameters are respectively weight

and bias.

Given a training set of m examples, the overall

cost function to minimize is shown in equation 8.

Identify Theft Detection on e-Banking Account Opening

559

J(W,b) =

"

1

m

m

∑

i=1

1

2

kx(i) − ˆx(i)k

2

#

+

λ

2

n

l

−1

∑

l=1

s

l

∑

i=1

s

l

+1

∑

j=1

W

(l)

ji

2

(8)

The first term in the definition of J(W,b) in equa-

tion 8 is an average sum-of-squares error term. The

second term is a regularization term, a weight decay

term aiming to prevent overfitting. The weight decay

parameter λ controls the relative importance of each

of those terms. Four main extensions of AEs have

been developed: Sparse (Deng et al., 2013), Denois-

ing (Vincent et al., 2008), Contractive (Rifai et al.,

2011) and Variational (Goodfellow et al., 2014).

The sparsity constraint we chose in our study

forces the neurons to be inactive most of the time, but

interesting structure in the data can still be discovered.

To enforce the constraint

ˆ

ρ

j

= ρ , where ρ is a spar-

sity parameter (usually close to zero), we add an extra

penalty term to our optimization objective that penal-

izes

ˆ

ρ

j

significantly deviating from ρ. Many choices

of the penalty term are possible but common choice is

based on the concept of Kullback–Leibler divergence

(see equation 9).

J

Sparse

(W,b) = J(W, b) + β

s

2

∑

j=1

KL(ρk

ˆ

ρ

j

) (9)

where J(W, b) is defined in equation 8, and β controls

the weight of the penalty term.

In Keras library, the Dense function constructs a

fully connected NN layer. If we enforce a representa-

tion constrained only by the size of the hidden layer,

the hidden layer is learning an approximation of PCA.

To add a sparsity constraint on the activity of the hid-

den representations, so fewer units fire at a given time,

we add in Keras an activity regularizer to our Dense

layer. When we add more than one hidden layer to

an AE, it helps to reduce a high dimensional data to

a smaller code representing important features. The

network used in our study is a 4-layered sparse AE

where each layer is a sparse encoding layer reducing

the number of features by 25% (we observed better

performances with a smooth decay of neuron number

in each layer). Each hidden layer becomes a more

compact representation than the last hidden layer.

4.2 Assessment Metrics

The most frequently used metrics are accuracy and

error rate. Considering a basic two-class classifica-

tion problem, then a representation of classification

performance can be formulated by a confusion ma-

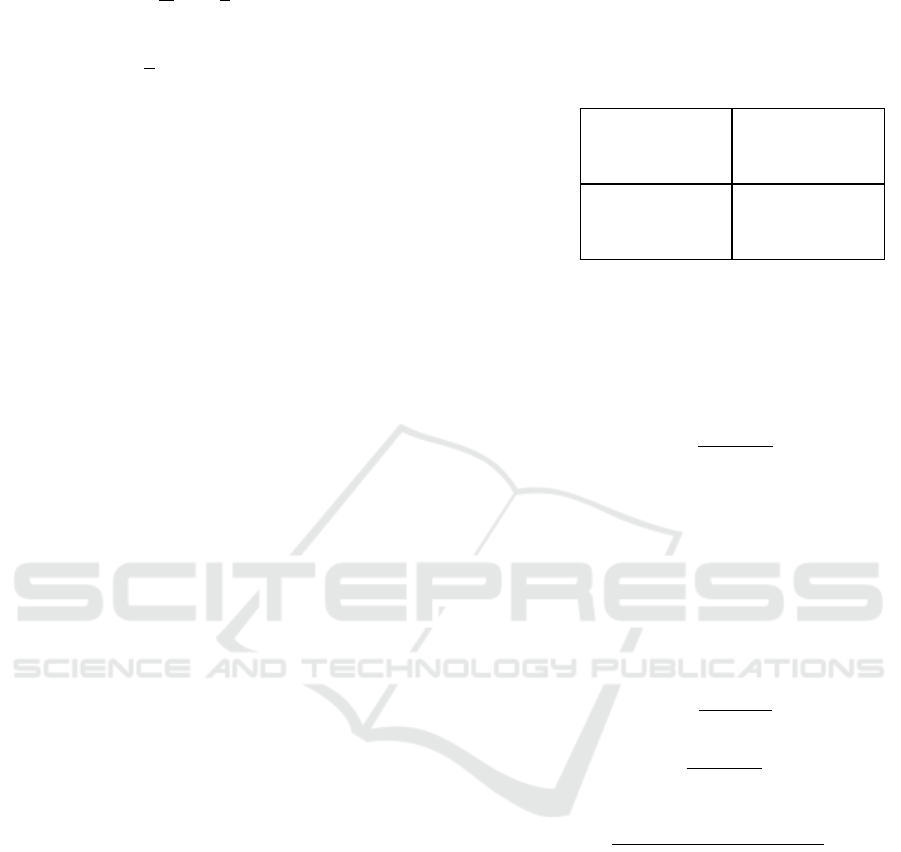

trix (contingency table), as illustrated in table 1. In

Table 1: Confusion matrix. P, N stand for predicted posi-

tive and negative classes, p, n for ground-truth positive and

negative label.

Program prediction

Ground truth

p n

P

TP

(True Positive)

FP

(False Positive)

N

FN

(False Negative)

TN

(True Negative)

Count: P

C

N

C

this paper, the minority (fraudulent) class is used as

the positive class and the majority (non fraud) class

as the negative class. With this convention, accuracy

and error rate are respectively defined as in 10 and 11.

Accuracy =

T P + T N

P

c

+ N

c

(10)

ErrorRate = 1 − Accuracy (11)

It can be difficult to mesure performances of a

classifier on unbalanced data. In the case of highly

skewed datasets, ROC curve may provide an overly

optimistic view of an algorithm’s performance. Un-

der such situations there are three standard assessment

metrics which are useful to unbalanced learning, de-

fined as follows:

Precision =

T P

T P + FP

(12)

Recall =

T P

T P + FN

(13)

F1-Score =

(1 + β)

2

· precision · recall

β

2

· precision + recall

(14)

where β is the relative importance of precision and

recall, usually β = 1.

For our study, we focused on precision, recall

(sensitivity), F1-score and specificity (false alarm

rate).

4.3 Evaluation Results

All the hyper-parameters of the models mentioned

above have been tuned using GridSearch() class. Per-

formances described in this subsection are calcu-

lated on a k-stratified cross validation (Mosteller and

Tukey, 1968).

In the preprocessing stage, we tested dimension

reduction using PCA or Multi Layer AE, removal

NCTA 2019 - 11th International Conference on Neural Computation Theory and Applications

560

of categorical features, removal of features with low

variance, and oversampling.

To compute confusion matrices and evaluate per-

formance metrics of the classifiers, we divided our

dataset (2200 non fraud / 396 frauds) into a learning

dataset (70%) and a testing dataset (30%). Test set

consists of 660 observations of class 0 (non fraud) et

119 observations of class 1 (fraud). Anomalies are

equally distributed in both learning and test datasets.

Each observation is described by more than 250 fea-

tures (including categorical features with One-hot

representation). Tables 2 to 5 show performances ob-

tained by the candidate models on different prepro-

cessings of the dataset.

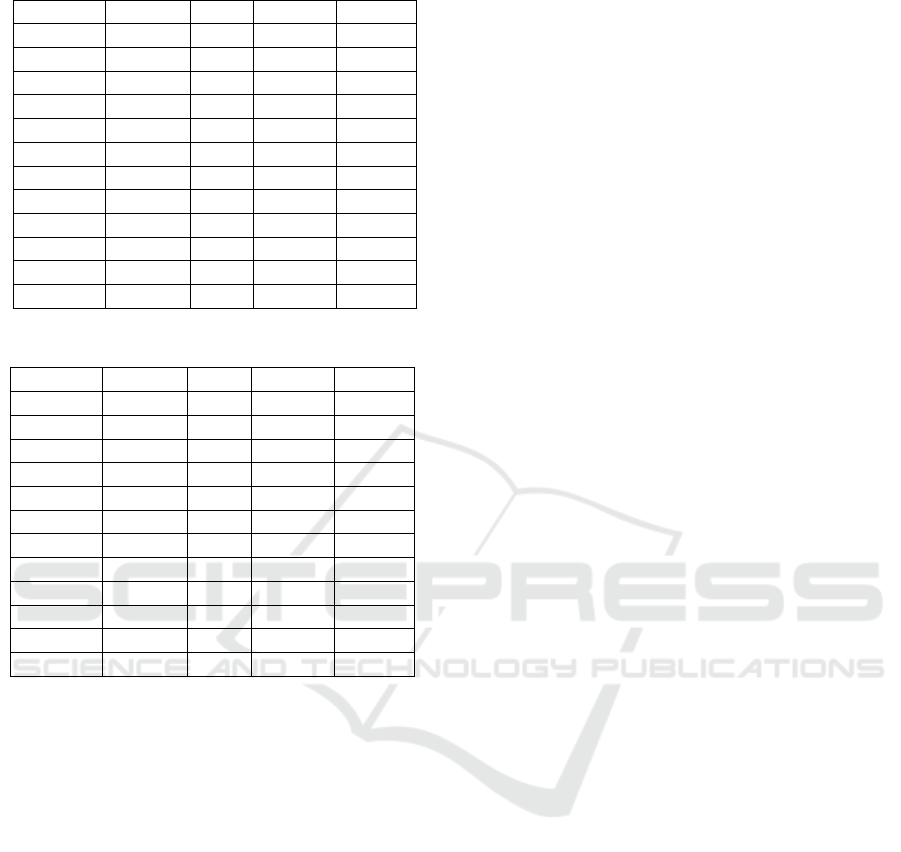

Performances are worse on the PCA reduced data

for every classifier and thus demonstrate it is unsuit-

able to our problem. MLP achieved best F1-score

(0.83) on the PCA preprocessing (where the simpler

BLP only performed 0.67). Table 3 shows classi-

fier performances after having applied dimensional

reduction using Multi Layer sparse AE. Performances

are improved for all classifiers. Best performance

was achieved by OCSVM with a F1-score of 0.90.

Tree based models like AdaBoost, DT and RF per-

formed well too. On the 119 fraudulent cases in test

dataset, RF correctly classified 93 of them (with 2

false alarms) and DT detected 101 of them (with 8

false alarms). The MLP also achieved a good F1-

score of 0.84 but with very little improvement com-

pared to performances on PCA preprocessing.

We had more than 20 categorical features in our

initial dataset. When embedded using the One-hot

representation, this created a sparse data matrix with a

lot of low variance features. We decided to test candi-

date models with removal of these attributes and per-

formances picked up as shown in Table 4. OCSVM

with F1-score of 0.93 performed best, followed by

SVM with a F1-score of 0.91. Both of the SVM-

based models were able to detect all fraudulent cases.

We also observed that Naive Bayes made its best per-

formances with this preprocessing with a F1-score of

0.88.

Table 5 shows performances after oversampling.

In our case, we created synthetical copies of the

fraudulent cases until we reach a balanced distribu-

tion (same number of fraud/non fraud observations).

Test dataset consists of 660 non fraud cases and 660

fraud cases. As expected, classification performances

picked up and all models achieved their best scores

(with a minimum F1-score of 0.68). Random For-

est got the best F1-score of 0.99 (7 false alerts and 5

frauds missed). SVM and OCSVM were able to de-

tect all fraudulent cases and raised less than 30 false

alarms.

Overall, IForest and LOF did not perform well, as

they mislabeled the fraudulent cases as normal and

caused too many false alarms. They were capable of

detecting at least 75% of the frauds on the oversam-

pled dataset but they were far from meeting Random

Forest or SVM based models performances.

Table 2: Performances with PCA dimensional reduction.

Algorithm Accuracy Recall Precision F1 Score

k-NN 0.8929 0.4797 0.7252 0.5775

SVM 0.9402 0.6085 1.0000 0.7566

DT 0.6737 0.7190 0.8735 0.7888

RF 0.9479 0.6994 0.9453 0.8040

BLP 0.9183 0.5656 0.8484 0.6787

AdaBoost 0.9437 0.7525 0.8612 0.8032

NB 0.2858 0.9570 0.1710 0.2901

QDA 0.8536 0.0404 1.0000 0.0776

IForest 0.4568 0.4604 0.8195 0.5896

OCSVM 0.8447 0.8908 0.4953 0.6366

LOF 0.3880 0.3250 0.8730 0.4736

MLP 0.9538 0.7601 0.9233 0.8338

Table 3: Performances with AE dimensional reduction.

Algorithm Accuracy Recall Precision F1 Score

k-NN 0.9318 0.6464 0.8737 0.7431

SVM 0.9564 1.0000 0.7778 0.8750

DT 0.9666 0.8487 0.9266 0.8860

RF 0.9641 0.7815 0.9789 0.8692

BLP 0.9332 0.7143 0.8252 0.7297

AdaBoost 0.9537 0.7676 0.9156 0.8351

NB 0.6470 0.6723 0.2532 0.3678

QDA 0.3979 0.9412 0.1951 0.3232

IForest 0.9148 0.5378 0.8486 0.6584

OCSVM 0.9730 0.8232 1.0000 0.9030

LOF 0.9248 0.5909 0.87640 0.7058

MLP 0.7330 0.8359 0.8470 0.8414

The amount of time needed for learning and the

time needed for labeling a new observation are two

important criteria that we have not yet taken into ac-

count in this study. Our raw logs needed a heavy ini-

tial cleaning step, and feature creation was the most

CPU consuming. Once the final dataset prepared and

the large learning data matrix created we focused on

reducing the dimensionality disorder by selecting the

best features and by applying different reduction tech-

niques. The preliminary analysis mentioned (sub-

section 3.2) revealed that several categorical features

were useless. With feature selection and application

of dimensional reduction we were able to train all

models in acceptable time although BLP/MLP were

very long to train as their number of hidden neurons

was quite large.

Identify Theft Detection on e-Banking Account Opening

561

Table 4: With low variance and category features removal.

Algorithm Accuracy Recall Precision F1 Score

k-NN 0.7253 0.8159 0.8535 0.8343

SVM 0.8509 1.0000 0.8504 0.9191

DT 0.9476 0.7601 0.8801 0.8157

RF 0.7723 0.8563 0.8726 0.8644

BLP 0.7369 0.7977 0.8805 0.8371

AdaBoost 0.7272 0.7850 0.8022 0.8298

NB 0.8027 0.9163 0.8600 0.8873

QDA 0.2114 0.0781 0.9005 0.1438

IForest 0.6675 0.7668 0.8281 0.7963

OCSVM 0.9451 1.0000 0.8722 0.9318

LOF 0.9537 0.7601 0.9233 0.8337

MLP 0.8124 0.9527 0.8455 0.8959

Table 5: Performances with oversampling.

Algorithm Accuracy Recall Precision F1 Score

k-NN 0.8097 0.9009 0.8777 0.8891

SVM 0.9713 1.0000 0.9442 0.9713

DT 0.9689 0.9682 0.9697 0.9689

RF 0.9909 0.9924 0.9894 0.9909

BLP 0.9523 0.9621 0.9435 0.9527

AdaBoost 0.9826 0.9712 0.9938 0.9824

NB 0.6750 0.7076 0.6643 0.6853

QDA 0.5477 0.9758 0.5477 0.6833

IForest 0.7222 0.8209 0.8466 0.8336

OCSVM 0.9886 1.0000 0.9778 0.9888

LOF 0.9333 0.6590 0.8729 0.7510

MLP 0.9667 0.9803 0.9543 0.9671

From a business validation point of view, we se-

lected the best models (oversampled Random Forest

and OCSVM) and tested classification to all historical

onboarding accounts (only non fraud). We observed

that our framework labeled some of them as fraud-

ulent and reported them to the dedicated team. On

these alerts, 25% were totally false alerts. In the re-

maining 75%, approximatively half of them were ac-

tually fraud cases mislabeled (often discovered later

and not updated in the tracking file). The other half

were accounts actually under observation because of

fraud suspicion.

5 CONCLUSION

In this paper we proposed a ML-based framework for

detecting identity theft on e-banking account open-

ing. We aggregated massive amounts of data, com-

bined several types of features, including behavioral

browsing characteristics. We applied different pop-

ular preprocessing techniques such as oversampling

and dimensional reduction with PCA. Most recent

scientific work now supports the use of auto- or un-

supervised NNs to detect anomalies and reduce di-

mensions while preserving information. In particu-

lar, studies have shown that AEs are able to detect

much more subtle anomalies than conventional linear

techniques such as PCA (Sakurada and Yairi, 2015).

We benchmarked 12 classifiers with different prepro-

cessings and concluded that using multi layer sparse

AE did improve our classification performances com-

pared to PCA. We also observed a clear improvement

of performances just by removing the embedded cat-

egorical features, outperforming scores on PCA and

AE preprocessing. This clearly demonstrates the im-

portance of the training dataset used and the feature

engineering process. However, applying a dimen-

sional reduction was imperative in our case as each

observation was described by a large number of fea-

tures and without dimensional reduction step, classi-

fiers did require a lot more training time. Like other

related banking fraud research (Quah and Sriganesh,

2008; Ahmad et al., 2017; Ryman-Tubb and D’Avila

Garcez, 2010; Kamesh et al., 2019) our work will

now focus on adapting our framework for real-time

streaming data and on the extraction of comprehensi-

ble rules for the business team.

Integrating data-level solutions with classifiers,

resulting in robust and efficient learners, is very pop-

ular in recent years for unbalanced problems (Abdi

and Hashemi, 2016). Some works propose the hy-

bridization of sampling techniques and the use of a

cost-sensitive learning or of kernel-based methods.

We applied the same techniques in our study and

performed expected results: tree-based models (DT,

RF, Adaboost) and SVM based models achieved best

scores, especially with oversampling.

In such cases where the unbalance ratio in the

data is so important, the anomaly is poorly repre-

sented, lacks a clear structure and potentially strong

variance is induced. Direct application of relation-

ship based preprocessing methods such as oversam-

pling can actually damage the classification perfor-

mance and lead to over-fitting. In our case, business

validation on historical data indicates that the selected

RF and OCSVM models are able to fit on new obser-

vations.

Our proposed framework is an interesting decision

making tool for detecting identity theft on the digi-

tal account opening. We discovered interesting fraud

patterns and overall, we observed the same results as

other related works: behavior of the fraudsters is sta-

tistically different from legitimate users and real users

browse following a certain pattern. In contrast, fraud-

sters behave more uniformly, generally going directly

to the purpose of their theft, browsing quickly. Un-

NCTA 2019 - 11th International Conference on Neural Computation Theory and Applications

562

fortunately these types of deeper analysis are often

restrained from publication and research studies like

ours can rarely provide detailed experimental setup or

disclose chosen solution.

REFERENCES

Abdi, L. and Hashemi, S. (2016). To combat multi-class im-

balanced problems by means of over-sampling tech-

niques. IEEE Transactions on Knowledge & Data En-

gineering.

Ahmad, S., Lavin, A., Purdy, S., and Agha, Z. (2017). Un-

supervised real-time anomaly detection for streaming

data. Neurocomputing, 262:134–147.

Anandakrishnan, A., Kumar, S., Statnikov, A., Faruquie, T.,

and Xu, D. (2018). Anomaly Detection in Finance:

Editors’ Introduction. In KDD 2017 Workshop on

Anomaly Detection in Finance, pages 1–7.

Breunig, M. M., Kriegel, H.-P., Ng, R. T., and Sander, J.

(2000). LOF: identifying density-based local outliers.

In ACM sigmod record, volume 29, pages 93–104.

Chen, J., Shen, Y., and Ali, R. (2019). Credit Card Fraud

Detection Using Sparse Autoencoder and Generative

Adversarial Network. In 2018 IEEE 9th Annual In-

formation Technology, Electronics and Mobile Com-

munication Conference, IEMCON 2018, pages 1054–

1059. IEEE.

Deng, J., Zhang, Z., Marchi, E., and Schuller, B. (2013).

Sparse autoencoder-based feature transfer learning for

speech emotion recognition. In 2013 Humaine Asso-

ciation Conference on Affective Computing and Intel-

ligent Interaction, pages 511–516. IEEE.

Fu, K., Cheng, D., Tu, Y., and Zhang, L. (2016). Credit

card fraud detection using convolutional neural net-

works. In Lecture Notes in Computer Science (includ-

ing subseries Lecture Notes in Artificial Intelligence

and Lecture Notes in Bioinformatics), volume 9949

LNCS, pages 483–490. Springer, Cham.

Goodfellow, I., Pouget-Abadie, J., Mirza, M., Xu, B.,

Warde-Farley, D., Ozair, S., Courville, A., and Ben-

gio, Y. (2014). Generative adversarial nets. In

Advances in neural information processing systems,

pages 2672–2680.

Kamesh, V., Karthick, M., Kavin, K., Velusamy, M., and

Vidhya, R. (2019). Real-time fraud anomaly detec-

tion in e-banking using data mining algorithm. South

Asian Journal of Engineering and Technology, 8(S

1):144–148.

Krishnapriya, D. (2017). Identification of Money Laun-

dering based on Financial Action Task Force Using

Transaction Flow Analysis System. Bonfring Interna-

tional Journal of Industrial Engineering and Manage-

ment Science, 7(1):01–04.

Liu, F. T., Ting, K. M., and Zhou, Z.-H. (2008). Isolation

forest. In 2008 Eighth IEEE International Conference

on Data Mining, pages 413–422.

Mazzawi, H., Dalal, G., Rozenblatz, D., Ein-Dorx, L., Nin-

iox, M., and Lavi, O. (2017). Anomaly detection in

large databases using behavioral patterning. In Data

Engineering (ICDE), 2017 IEEE 33rd International

Conference on, pages 1140–1149.

Mosteller, F. and Tukey, J. W. (1968). Data analysis, in-

cluding statistics. In Lindzey, G. and Aronson, E., edi-

tors, Handbook of Social Psychology, Vol. 2. Addison-

Wesley.

Ngai, E. W. T., Hu, Y., Wong, Y. H., Chen, Y., and Sun, X.

(2011). The application of data mining techniques in

financial fraud detection: A classification framework

and an academic review of literature. Decision sup-

port systems, 50(3):559–569.

Quah, J. T. S. and Sriganesh, M. (2008). Real-time credit

card fraud detection using computational intelligence.

Expert systems with applications, 35(4):1721–1732.

R

¨

atsch, G., Sch

¨

olkopf, B., Mika, S., and M

¨

uller, K.-R.

(2000). SVM and boosting: One class. GMD-

Forschungszentrum Informationstechnik.

Rifai, S., Vincent, P., Muller, X., Glorot, X., and Bengio,

Y. (2011). Contractive auto-encoders: Explicit invari-

ance during feature extraction. In Proceedings of the

28th International Conference on International Con-

ference on Machine Learning, pages 833–840. Omni-

press.

Ryman-Tubb, N. F. and D’Avila Garcez, A. (2010).

SOAR - Sparse Oracle-based Adaptive Rule extrac-

tion: Knowledge extraction from large-scale datasets

to detect credit card fraud. In Proceedings of the Inter-

national Joint Conference on Neural Networks, pages

1–9. IEEE.

Sakurada, M. and Yairi, T. (2015). Anomaly Detection

Using Autoencoders with Nonlinear Dimensionality

Reduction. In Proceedings of the MLSDA 2014 2nd

Workshop on Machine Learning for Sensory Data

Analysis - MLSDA’14, pages 4–11, New York, New

York, USA. ACM Press.

Shanmugapriya, D. and Ganapathi, P. (2017). A Wrapper-

Based Classification Approach for Personal Identifi-

cation through Keystroke Dynamics Using Soft Com-

puting Techniques. In Identity Theft: Breakthroughs

in Research and Practice, pages 267–290. IGI Global.

Sundarkumar, G. G. and Ravi, V. (2015). A novel hybrid un-

dersampling method for mining unbalanced datasets

in banking and insurance. Engineering Applications

of Artificial Intelligence, 37:368–377.

Vincent, P., Larochelle, H., Bengio, Y., and Manzagol, P.-

A. (2008). Extracting and composing robust features

with denoising autoencoders. In Proceedings of the

25th international conference on Machine learning,

pages 1096–1103. ACM.

Wang, S., Liu, C., Gao, X., Qu, H., and Xu, W.

(2017). Session-Based Fraud Detection in Online E-

Commerce Transactions Using Recurrent Neural Net-

works. In Joint European Conference on Machine

Learning and Knowledge Discovery in Databases,

pages 241–252.

Zaslavsky, V. and Strizhak, A. (2006). Credit card fraud de-

tection using self-organizing maps. Information and

Security, 18:48.

Identify Theft Detection on e-Banking Account Opening

563