Using Population-based Metaheuristics and Trend Representative

Testing to Compose Strategies for Market Timing

Ismail Mohamed and Fernando E. B. Otero

University of Kent, Chatham Maritime, Kent, U.K.

Keywords:

Particle Swarm Optimization, Genetic Algorithms, Market Timing, Technical Analysis.

Abstract:

Market Timing is the capacity of deciding when to buy or sell a given asset on a financial market. Market Tim-

ing strategies are usually composed of components that process market context and return a recommendation

whether to buy or sell. The main issues with composing market timing strategies are twofold: (i) selecting the

signal generating components; and (ii) tuning their parameters. In previous work, researchers usually attempt

to either tune the parameters of a set of components or select amongst a number of components with prede-

termined parameter values. In this paper, we approach market timing as one integrated problem and propose

to solve it with two variants of Particle Swarm Optimization (PSO). We compare the performance of PSO

against a Genetic Algorithm (GA), the most widely used metaheuristic in the domain of market timing. We

also propose the use of trend representative testing to circumvent the issue of overfitting commonly associated

with step-forward testing. Results show PSO to be competitive with GA, and that trend representative testing

is an effective method of exposing strategies to various market conditions during training and testing.

1 INTRODUCTION

Trading in financial markets traces its history as far

back as the early 13

th

century. From humble begin-

nings where traders met to exchange basic commodi-

ties, financial markets have since evolved where se-

curities, stocks, bonds, commodities, currencies and

other financial instruments are traded electronically

within fractions of a second. A number of devel-

opments after the market crash of 1987 in the USA

heralded the birth of electronic exchanges, and usher-

ing with it a new form of trading: algorithmic trading

(Patterson, 2013). One of the issues faced by design-

ers of algorithmic trading systems is that of market

timing. Market timing is defined as the identification

of opportunities to buy or sell a given tradable item

in the market so as to best serve the financial goals of

the trader (Kaufman, 2013). A common approach de-

signers use to build strategies for market timing is to

use components that would take market data as input

and generate recommendations to buy, sell or do noth-

ing. A collection of these components would form the

core of the strategy, and it would be the job of the de-

signer to select which components to use and to tune

their parameters.

Since the introduction of electronic exchanges,

designers of algorithmic trading systems have in-

creasingly employed computational intelligence tech-

niques, one of which is Particle Swarm Optimiza-

tion (PSO). Despite its popularity in other domains,

PSO has seen limited use in the financial domain

and in particular within the market timing space.

This is compared with other metaheuristics such as

genetic algorithms (GA) and genetic programming

(GP). Within a few years of the introduction of elec-

tronic exchanges and trading in the mid 1990s, GA

and GP have been used to guide trading decisions and

form the core of market timing strategies. The ear-

liest PSO approach to market timing, on the other

hand, was introduced in 2011 (Briza and Naval Jr.,

2011). Compared to GA, PSO has seen relatively

limited adoption in the literature, despite PSO hav-

ing a performance advantage over GA according to

some studies (Hu et al., 2015; Soler-Dominguez et al.,

2017).

Recently, PSO was used to build market timing

strategies using six technical indicators and tested on

four stocks in a step-forward fashion (Mohamed and

Otero, 2018). In this paper, we conduct an extensive

study of the performance of PSO versus a standard

GA implementation. We selected a set of sixty three

signal generating components to evaluate how PSO

handles component selection and optimization com-

pared to a GA, the current incumbent in the domain.

Mohamed, I. and Otero, F.

Using Population-based Metaheuristics and Trend Representative Testing to Compose Strategies for Market Timing.

DOI: 10.5220/0008066100590069

In Proceedings of the 11th International Joint Conference on Computational Intelligence (IJCCI 2019), pages 59-69

ISBN: 978-989-758-384-1

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

59

We also introduce the concept of trend representative

testing and apply it to overcome limitations with step-

forward testing – the current standard testing method

when it comes to market timing.

The remainder of the paper is structured as fol-

lows. In Section 2 we review the approach to formal-

ize the problem of market timing in such a fashion

so as to consider both the selection of signal generat-

ing components and the tuning of their parameters. In

Section 3 we cover related work done in the applica-

tion of metaheuristics to the problem of market timing

and the associated limitations. In Section 4 we intro-

duce the concept of trend representative testing and

discuss how it can potentially overcome limitations

with current testing standards. In Section 5 we discuss

how PSO and GA were adapted to tackle market tim-

ing. We discuss our experimental setup, present the

results obtained and provide a critique of the perfor-

mance of the various metaheuristics involved in Sec-

tion 6. Finally, in Section 7 we present a conclusion

and suggestions for future research.

2 MARKET TIMING

As discussed previously, market timing is the capac-

ity of deciding when to buy or sell a given security.

Traders in financial markets have continuously looked

for ways to best decide when to take action with a

given stock, and here we discuss the various schools

of thought that have emerged over time. The schools

of thought can be roughly categorized into two major

styles: technical analysis and fundamental analysis.

Technical analysis can be defined as the analy-

sis of a security’s historical price and volume move-

ments, along with current buy and sell offers, for

the purposes of forecasting its future price (Kaufman,

2013). The philosophy behind technical analysis is

built upon three pillars: price discounts all the infor-

mation we need to know about the traded security,

prices move in trends and history has a likelihood

of repeating itself. The first pillar assumes that all

the forces that can affect the price of a security have

been accounted for and already exerted their influence

when the actual trade took place. This includes the

psychological state of the market participants, the ex-

pectations of the various entities trading in that partic-

ular security, the forces of supply and demand, and the

current state of the entity which the stock represents

amongst other factors. It is therefore sufficient to only

consider price movements and their history, as they

are a reflection of all these forces and their influence.

The second pillar assumes that prices move in trends

based on the actions of traders currently dealing in

that security and their expectations. The third pillar

assumes that markets, presented with an almost simi-

lar set of stimuli and circumstances, have a tendency

of reacting in the same fashion as it had in previous

exposures. This was proven empirically in the his-

tories of various securities across many markets over

time as traders react in the same consistent fashion to

shifts in price.

Techniques employing technical analysis will of-

ten take the form of functions known as indicators.

Indicators will take in price history, along with a set

of parameters that govern various aspects of an indi-

cators behavior, and return a signal: an indication of

whether it is favorable to buy or sell at the current

moment. As an exhaustive list of all indicators cur-

rently available to the modern trader would easily fill

multiple volumes, it is beyond the scope of this paper.

Instead, the reader is directed to the works of Pring

(Pring, 2002) and Kaufman (Kaufman, 2013) for a

more detailed look at the world of technical analysis.

Fundamental analysis is the process of deriving

the value of a security’s value by analysis of the fi-

nancial state of the company it represents (Penman,

2013). This will include analyzing current and previ-

ous financial documents and accounting records for

the company, considering current management per-

sonnel and their performance in the past, sales perfor-

mance history, earning history, current market senti-

ment towards the company and macroeconomic con-

ditions, amongst many other factors. After consider-

ing these factors, analysis can arrive at a fair value

for the security and a projection for it moving for-

ward. Fundamental analysis is built on the core as-

sumption that a discrepancy occurs between a secu-

rity’s fair price and market price as the market moves

to close that gap. Recommendations for buying or

selling the security are therefore based on identifying

this discrepancy and how best to utilize it to achieve

returns. As the rate of release of information could

become an issue with some of the traditional infor-

mation sources, fundamental analysis has grown to

include techniques such as sentiment analysis over so-

cial media streams.

Instead of following a purest approach, a large

number of traders would base their strategies on tech-

niques from both schools. It is quite common for

traders to use fundamental analysis for portfolio com-

position, then use technical analysis for market tim-

ing. It would actually be prudent to use methods from

both schools to hedge the trader’s risk in one or more

of the components being mistaken or fed false data

1

,

and thus produce signals that might result in losses. In

this paper, we have chosen to focus on using technical

analysis indicators for the purposes of market timing.

ECTA 2019 - 11th International Conference on Evolutionary Computation Theory and Applications

60

As alluded to earlier, a market strategy could be

built using a collection of components, where every

component t consumes information regarding a secu-

rity and returns a signal indicating whether to buy or

sell. A component’s signal is limited to three values:

1 for a buy recommendation, −1 for a sell recommen-

dation and 0 for a hold recommendation. Every com-

ponent will also have a weight and a set of parameters.

The parameters will control the behavior of that com-

ponent and are unique to every component type. The

weight controls how much influence the component

has on the overall signal produced by the candidate

solution. The overall signal of the candidate solution

is taken as the aggregation of weighted components,

and interpreted as follows: buy when positive, sell

when negative or hold otherwise. Formally, we can

present this formulation as follows:

solution = {w

1

t

1

, ..., w

n

t

n

}, ∀t

i

: {t

1

i

, ...,t

x

i

} (1)

signal =

n

∑

i=1

w

i

t

i

(2)

where x denotes the number of parameters for the

component at hand, w represents the weight assigned

to the component at hand, t represents a single com-

ponent and n is total number of components within the

solution. The weights for the components are all nor-

malized to be between 0 and 1, and have a total sum

of 1. As we are seeking to select the least possible

subset that achieves our set objectives, varying com-

binations of components, along with varying values

for component weights and parameters, will produce

a rich landscape of candidates that return different sig-

nal values for the same market conditions.

3 RELATED WORK

In two recent and comprehensive studies, Hu et al.

(Hu et al., 2015) and Soler-Dominguez et al. (Soler-

Dominguez et al., 2017) investigate the use of compu-

tational intelligence techniques in finance. While the

study by Soler-Dominguez et al. was more holistic

in its coverage, the study done by Hu et al. was fo-

cused on the use of computational intelligence in the

discovery of trading strategies. Both studies consid-

ered a large number of metaheuristics that belong un-

1

An example of this would be using a purely funda-

mental approach while trading Enron before its crash and

bankruptcy in late 2001. A post-mortem investigation

by the U.S. Securities and Exchange Commision (SEC)

showed that the information published in the firm’s finan-

cial documentation were false, leading to investments by

market participants that were built on mislead assumptions.

der the computational intelligence umbrella, and that

included evolutionary algorithms (GA, GP, differen-

tial evolution), swarm intelligence (PSO, ACO, artifi-

cial bee colony optimization), stochastic local search

(simulated annealing, ILS, tabu search, GRASP),

fuzzy systems and neural networks amongst others.

Both studies cover a combined time span starting with

the early 1990’s and ending with recent times.

By surveying the techniques covered in both stud-

ies, we can see that genetic algorithms (GA), and to a

slightly lesser extent genetic programming (GP), are

the most applied metaheuristics when it comes to the

issue of market timing. One of the earliest works us-

ing GA was by Allen and Karjalanien (Allen and Kar-

jalainen, 1999). In it, Allen and Karjalanien use a

GA to develop trading rules based on technical anal-

ysis indicators, and benchmarked their results against

a buy-and-hold strategy and out of sample data. An-

other approach is to use GA to directly optimize the

parameters of one or more financial analysis indica-

tors, be they fundamental or technical in nature. Ex-

amples of such an approach can be seen in the work

of de la Fuente et al. (de la Fuente et al., 2006) and

Subramanian et al. (Subramanian et al., 2006) – the

latter tackling market timing as a multi-objective opti-

mization problem. Both of these approaches directly

encode the indicator parameters into the GA chromo-

some, and use the metaheuristic to arrive at the val-

ues for these parameters that produce the best results.

Other approaches since then use GA to improve the

fitness of another primary metaheuristic in charge of

producing the trading signals by optimizing its param-

eters. These primary, signal-producing metaheuris-

tics included fuzzy systems, neural networks, self-

organizing maps (SOM) and a variety of classification

algorithms. A thorough breakdown of such synergis-

tic approaches can be seen in (Hu et al., 2015). More

recent approaches using GA to tackle market timing

can be seen in the work of Kampouridis and Otero

(Kampouridis and Otero, 2017) and Kim et al. (Kim

et al., 2017).

Particle swarm optimization (PSO) has not seen

the popularity of GA and GP in the space of market

timing. Though introduced much later than GA, PSO

has started seeing some adoption in the area. The

earliest PSO approach to tackle market timing was

proposed by Briza and Naval, Jr. (Briza and Naval

Jr., 2011). Inspired by Subramanian and colleagues

(Subramanian et al., 2006), the authors optimized

the weights of instances of five technical indicators

who had preset parameter values according to indus-

try wide standards. All the weighed instances of the

technical indicators would then produce a cumulative

signal whether to buy or sell. The authors approached

Using Population-based Metaheuristics and Trend Representative Testing to Compose Strategies for Market Timing

61

the issue of market timing as a multi-objective opti-

mization problem, and optimized for percentage of

return and the Sharpe ratio. Chakravarty and Dash

(Chakravarty and Dash, 2012) also used PSO for mar-

ket timing by utilizing it to optimize a neural network

capable of predicting movements in an index price.

Similarly Liu et al. (Liu et al., 2012) used PSO to op-

timize a neural network that generated fuzzy rules for

market timing and reported positive results.

More recently, Chen and Kao (Chen and Kao,

2013), used PSO to optimize a system that relied on

fuzzy time series and support vector machines (SVM)

to forecast the prices of an index for the purposes of

market timing. Ladyzynski and Grzegorzewski (La-

dyzynski and Grzegorzewski, 2013) used a combina-

tion of fuzzy logic and classification trees to identify

price chart patterns, while PSO is used to optimize the

parameters of the aforementioned hybrid approach. In

their results, the authors have noted that use of PSO

vastly improved the predictive capacity of the fuzzy

logic and classification tree hybrid, and that the over-

all system proved to be promising. In the work by

Wang et al. (Wang et al., 2014), a combination of

a reward scheme and PSO was used to optimize the

weights of two technical indicators. The Sharpe ratio

was used to measure the performance of the hybrid,

and in their results, the authors note that their system

outperformed other methods such as GARCH. Bera

et al (Bera et al., 2014) used PSO to only optimize

the parameters of a single technical indicator. Al-

though trading on the foreign exchange instead of the

stock exchange, the authors note that their system has

shown to be profitable in testing. Sun and Gao (Sun

and Gao, 2015) used PSO to optimize the weights on

a neural network that predicted the prices of securi-

ties on an exchange. The authors note that their sys-

tem was able to predict the price with an error rate

of around 30% when compared to the actual prices.

Karathanasopoulos and colleagues (Karathanasopou-

los et al., 2016) used PSO to optimize the weights

on a radial basis function neural network (RBF-NN)

that is capable of predicting the price of the crude oil

commodity. Though not on the stock exchange, the

trading of commodities occurs on similar exchanges

and uses many of the same market timing techniques.

Compared to two classical neural network models, the

authors note that their PSO-augmented approach sig-

nificantly outperformed them in predictive capacity.

In the nine discussed publications on the use of

PSO in market timing, we can see a salient trend:

PSO is used in a secondary role to optimize a primary

metaheuristic or computational intelligence technique

that is responsible for signal generation. There are

only three exemptions: (Briza and Naval Jr., 2011),

(Wang et al., 2014) and (Bera et al., 2014). In these

three publications, the authors used PSO as the only

metaheuristic, and within them PSO was either used

to optimize the weights of a set of technical indicators

or their parameters, but not both in unison. The only

attempt we are aware of that considers both the se-

lection of technical indicators and optimize their pa-

rameters was by Mohamed and Otero in (Mohamed

and Otero, 2018). In it, the authors used PSO to both

optimize the parameters of six technical indicators, as

well as tune the weights of the generated signals and

prune ineffective ones. They tested their work against

four stocks and show that using PSO was a viable ap-

proach albeit with some caveats: only a limited num-

ber of indicators was used (6 in total); a small number

of datasets (4 in total); and no baseline algorithm is

used to assess the performance of PSO.

The work proposed in this paper addresses limita-

tions identified in the literature so far: (1) it considers

the optimization of both selection of technical indica-

tors and their parameter values; and (2) avoid the ten-

dency of strategies to overfit when using step-forward

testing by proposing the use of trend representative

testing.

4 TREND REPRESENTATIVE

TESTING

The prominent method of testing a market timing

strategy in the literature surveyed is a procedure

known as step-forward testing (Kaufman, 2013; Hu

et al., 2015; Soler-Dominguez et al., 2017). In step-

forward testing, a stream of security data is divided

chronologically into two sections: the earlier section

for training and the later for testing. Although rela-

tively easy to implement, this approach has a number

of shortcomings. During training with this method,

the training mechanism might only be exposed to the

upwards, downwards or sideways trends available in

the data. This raises the likelihood of the strategy pro-

duced to be overfit to one of those trends only and the

chances of the strategy performing poorly in opposite

trends. For example, if during training, all the data

available represented uptrends, then a strategy trained

with such data would produce poor results in a down-

trend, and vice versa. Standard strategies taken during

training, such as k-fold cross validation, are not easily

applicable due to the structure of the data.

In order to overcome the limitations associated

with step-forward testing, we propose the use of trend

representative testing, as suggested by domain experts

(Kaufman, 2013). The idea behind trend representa-

tive testing is to have a library of security data that

ECTA 2019 - 11th International Conference on Evolutionary Computation Theory and Applications

62

represents all three trends at various intensities and

time lengths. Exposing strategies to these various

trends during training improve their chances of per-

forming better under numerous market conditions.

The process of building the trend representative

dataset is as follows. First, raw security data is down-

loaded from a publicly available data provider. Sec-

ond, this data is scanned for price shocks, and when

one is detected, the raw data is divided into two cords

– one before and one after the price shock respec-

tively. The reason we remove price shocks is that

they are outlier events, and including them in training

data would imply that these highly irregular and very

disruptive events can be readily predicted, which is

not the case. Besides being catastrophic events, price

shocks are rare and training a strategy to use them

would be highly impractical. Price shocks are defined

as price actions that are five times the Average True

Range (ATR) within a short period of time (Kaufman,

2013). The cords are then subsampled with moving

sliding windows of various sizes to produce strands

that can be used for training and testing. The final

step is to categorize these strands into upwards, down-

wards and sideways trends based on the Directional

Index technical indicator (Pring, 2002) to ascertain in-

tensity and direction.

In order to use this new dataset, we propose ran-

domly picking a representative upwards, downwards

and sideways strand from the pool of strands desig-

nated for testing. This triplet is then used by the al-

gorithm within an iteration to measure the fitness of

its candidate solutions. First a candidate solution is

tested against each individual strand, and the results

averaged to arrive at the final fitness for that candi-

date within that particular iteration. After all the can-

didates for the iteration have been assessed, a new

triplet is selected for the next iteration and the pro-

cess is repeated until the algorithm has completed its

run. The idea behind trend representative testing is

that we want discourage niching or specializing in one

particular trend type and instead promote discovering

market timing strategies that fair well against various

market conditions.

5 METAHEURISTICS AND

MARKET TIMING

In this section we will explore how to encode our mar-

ket timing formalization, explaining how the meta-

heuristics were adapted to use this encoding and

tackle the problem of market timing.

Figure 1: An example of an encoded candidate solution

with three components.

5.1 Individual Representation and

Fitness

Before discussing how the metaheuristics were

adapted to tackle market timing with the aforemen-

tioned formalization, let us first consider how we can

encode a candidate solution and assess the fitness of

these individuals. The first step to work with the pro-

posed formalization of market timing is to find an ap-

propriate encoding for candidate solutions. A candi-

date solution would be a collection of signal gener-

ating components, each with a weight and set of pa-

rameters. For example, if we had three signal generat-

ing components such as the technical indicators Mov-

ing Average Converge Diverge (MACD), the Relative

Strength Indicator (RSI) and the Chaikin Oscillator

(Chaikin), we could possibly have a candidate solu-

tion of:

0.3×MACD(Fast Period = 12, Slow Period = 27,

Smooth Period = 9)

+0.2×RSI(Overbought = 70, Oversold = 30,

Period = 14)

+0.5×Chaikin(Fast Period = 3, Slow Period = 10)

where the number preceding the indicator represents

its weight and the values in the brackets represent the

values of parameters per indicator. A visual example

can be seen in Figure 1.

As the metaheuristics used are all based on a pop-

ulation of individuals, where each individual repre-

sents a candidate solution, we choose to encode a

candidate solution as a multi-tier associative array.

The top level binding associates an indicator identifier

with a set of of its parameters. The bottom level bind-

ing associates a parameter identifier with its value.

These parameters are dependent on indicator type, but

all indicators have an instance of a weight parameter.

We choose to encode individuals in this manner

as this allows us the flexibility of using as many com-

ponents as we would like, without having to worry

about the type and amount of parameters per com-

ponent used or memorize a mapping of positions as

would have been the case of using an array. The se-

mantics of how to handle the components and tune the

weights and parameters is then left to be implemented

Using Population-based Metaheuristics and Trend Representative Testing to Compose Strategies for Market Timing

63

in the metaheuristics, as will be discussed shortly. A

new candidate solution is generated by instantiating

components from the available catalog with random

values for the parameters and adding it to the dictio-

nary representing the individual.

As for assessing the fitness of an individual, we

chose to maximize the Annualized Rate of Return

(AROR) generated by backtesting the individual at

hand. Backtesting would simulate trading based on

the aggregate signal produced by a solution over a

preset time period for a given asset. As for AROR,

this can be defined as:

AROR

simple

=

E

n

E

0

×

252

n

(3)

where E

n

is final equity or capital, E

0

is initial equity

or capital, 252 represents the number of trading days

in a typical American calendar and n is the number of

days in the testing period.

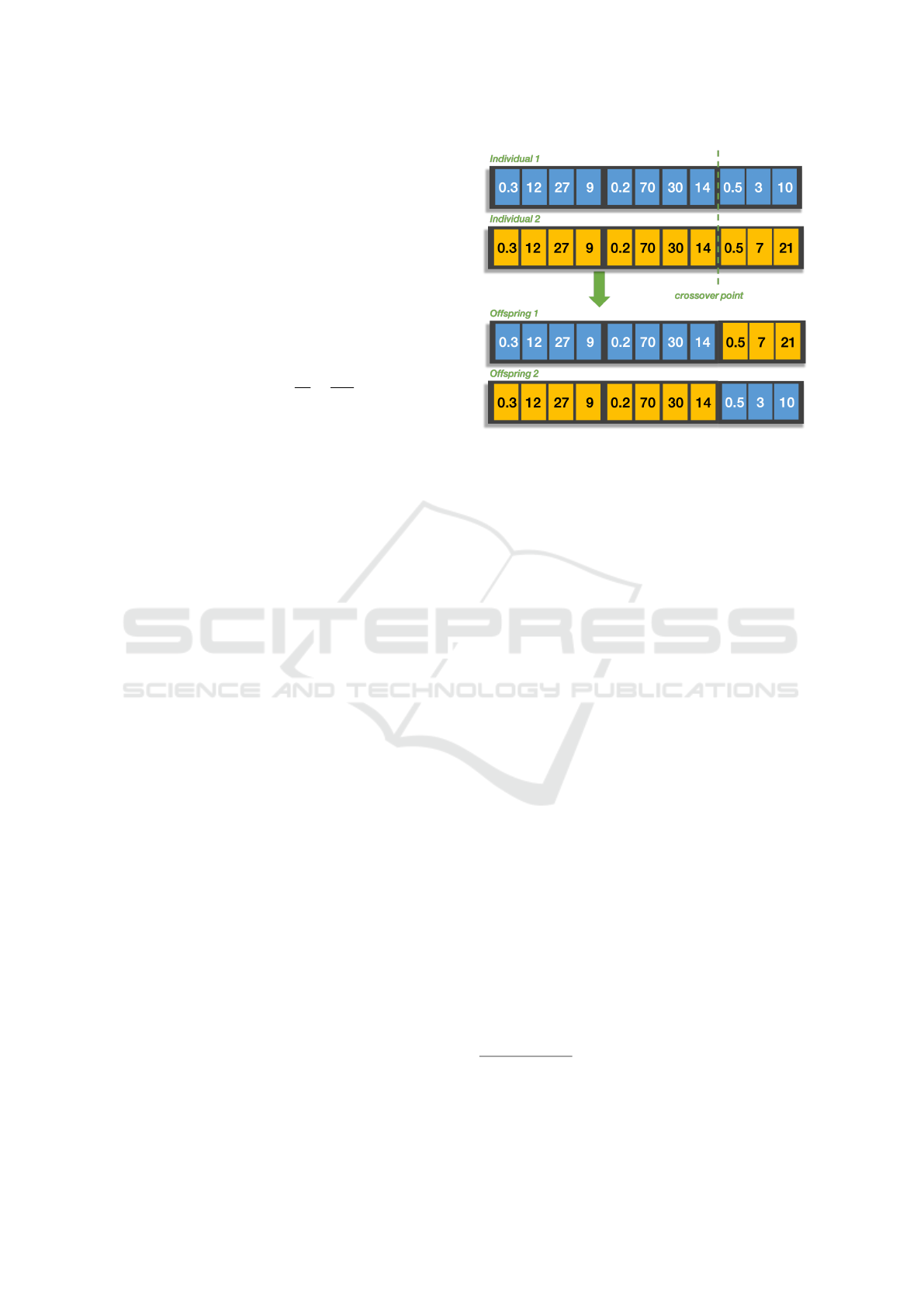

5.2 Genetic Algorithms

In order to apply genetic algorithms (GA) to tackle

market timing using our proposed formalization, we

started with a typical implementation of GA and mod-

ified its operators in order to accommodate how we

encode candidate solutions. First, individuals selected

for crossover are chosen using a typical tournament

procedure, with the tournament size being a user-

defined parameter. In preparation for crossover, the

components in the genotype of individuals selected

are ordered by key. A crossover point is then se-

lected at random such that it lands between the def-

inition of two components but not within them. Us-

ing the example mentioned earlier, we can gener-

ate a crossover point either between the definition of

MACD and RSI, or between RSI and Chaikin. An

example of a crossover operation can be seen in Fig-

ure 2. When a mutation event is triggered, a random

component in an individual’s genotype is replaced

by a newly instantiated copy of the same component

type. This newly instantiated copy would use random

values for the constituent parameters, but still within

valid range.

Crossover and mutation are used to generate a new

population for the next generation, and this procedure

continues until the allocated budget of generations are

exhausted. An archive is used to keep track of the elite

individuals per generation, with the most fit individual

in the archive reported at the end of the GA run as the

proposed solution.

Figure 2: An example of a crossover operation.

5.3 Particle Swarm Optimization

We now turn our attention to adapting Particle Swarm

Optimization (PSO) to tackle market timing. PSO

will use the same encoding of the solution to represent

a particle within its swarm, but the standard dynamics

of PSO operators will have to be changed in order to

adapt it to the problem at hand and use the solution

encoding proposed.

The basic PSO model can be seen in Algorithm

1. This model supports both l-best and g-best neigh-

borhood structures, based on the neighborhood size.

When the neighborhood size is less than the total size

of the population, we have an l-best neighborhood

structure, otherwise we have a g-best neighborhood

structure. A number of modifications are introduced

in order to adapt PSO to tackle market timing. The

first modification was that we pushed down the imple-

mentation of the addition, subtraction and multiplica-

tion operators required by the velocity update mech-

anism (lines 8–15) to be at the component level and

not the metaheuristic level, in order to be agnostic to

the types of signal generating components and their

parameters. This would no longer limit the parameter

types to either be in the binary or real-valued domains.

A designer is now free to include a signal generat-

ing component of an arbitrary number of parameters

and parameter types as long as the implementation of

that component provides overrides to the necessary

operators. Secondly, we also adopted a number of

measures to promote convergence within the swarm

and prevent velocity explosion (Clerc, 2002).

2

The

2

Early experiments indicated the tendency of particles to

adopt ever increasing values for velocity if left unchecked,

leading to the particles quickly seeking the edges of the

search space and moving beyond it.

ECTA 2019 - 11th International Conference on Evolutionary Computation Theory and Applications

64

Algorithm 1: Basic PSO high-level pseudocode.

1: initialize swarm S

2: repeat

3: for every particle x

i

in S do

4: if f (x

i

) > personal best(x

i

) then

5: personal best(x

i

) ← f (x

i

)

6: end if

7: for every component j in particle i do

8: bias ← αv

i j

(t)

9: cognitive ← c

1

r

1

(y

i j

(t)− x

i j

(t))

10: social ← c

2

r

2

( ˆy

i j

(t)− x

i j

(t))

11: v

i j

(t + 1) ← bias + cognitive + social

12: if j ∈R then

13: x

i j

(t + 1) ← x

i j

+ v

i j

(t + 1)

14: else if j ∈ [0, 1] then

15: Pr(x

i j

(t + 1) → 1) : sigmoid(v

i j

(t + 1))

16: end if

17: end for

18: end for

19: until stopping criteria met

20: return fittest particle

first of the measures is that we used a decreasing in-

ertia schedule. This means that for every step of the

algorithm, inertia for every particle decreases by an

amount defined by a function based on the number

of iterations left. The second measure we adopted

was that we scaled down v

i j

(t + 1) before updating

a particle’s state by a user-defined factor. As an alter-

native to velocity scaling, we also considered Clerc’s

Constriction as defined in (Clerc, 1999). The PSO

would now be able to optimize both the parameters

and weights of these components in relation to a fi-

nancial fitness metric.

A common problem faced by search metaheuris-

tics, PSO included, is getting stuck in local optima.

Multiple measures have been devised since the intro-

duction of the basic model to remedy that problem

with varying degrees of success (Engelbrecht, 2005).

Inspired by the work done by Abdelbar with Ant

Colony Optimization (ACO) in (Abdelbar, 2008), we

introduced a variation of PSO that stochastically up-

dates the velocity of its particles only when it is favor-

able in terms of fitness. We will refer to this variation

of PSO in the remainder of this paper as PSO

S

. The

modifications required for PSO

S

are reviewed next.

Every particle x in the swarm S represents a candi-

date solution. From our earlier discussion, this means

that a particle’s state is a collection of weighted com-

ponents, where each component has its own set of pa-

rameters. A particle starts out with an instance of all

the available signal generating components, each in-

stantiated with random weights and parameter values.

In contrast with the basic PSO model, the cognitive

and social components of the velocity update equa-

tion are modified to be calculated as:

cognitive =

(

y

i

(t)− x

i

(t) if rand() < |

f (y

i

(t))

f (x

i

(t))+f (y

i

(t))

|

0 otherwise

(4)

social =

(

ˆy

i

(t)− x

i

(t) if rand() < |

f ( ˆy

i

(t))

f (x

i

(t))+f ( ˆy

i

(t))

|

0 otherwise

(5)

• x: particle

• i: current particle index

• y: personal best

• ˆy: neighborhood best

• f (x): the fitness of x

• r and(): random number between 0 and 1

According to equations 4 and 5, the cognitive and so-

cial components will only stochastically influence ve-

locity update if there is an improvement in fitness, fol-

lowing a hill climbing fashion.

6 EXPERIMENTAL SETUP AND

RESULTS

In order to evaluate the effectiveness of the pro-

posed formulation in composing effective market tim-

ing strategies, we tested our PSO, PSO

S

and GA. As

all three algorithms have parameters, testing was pre-

ceded with hyper-parameter optimization performed

using the iterated racing procedure (IRace) (L

´

opez-

Ib

´

a

˜

nez et al., 2016). The IRace procedure was run

with a budget of 300 iterations and a survivor limit

of one, in order to arrive at a single configuration for

each metaheuristic. The results of the IRace proce-

dure can be seen in Table 1. In regards to PSO, IRace

arrived at swarm sizes that are similar for both vari-

ants. The configuration discovered for PSO uses a

much lower number of iterations when compared with

the configuration for PSO

S

. We can also see that the

PSO configuration is slightly more reliant on the cog-

nitive component with an l-best neighborhood span-

ning half the swarm, while the PSO

S

configuration

is slightly more reliant on the cognitive component

with a g-best neighborhood structure. Both PSO con-

figurations favored velocity scaling over Clerc’s con-

striction, with PSO using relatively larger steps while

PSO

S

uses relatively smaller steps based on the scal-

ing factors. After hyper-parameter optimization, we

ended up with two PSO configurations: a fast acting

l-best PSO and a slower g-best PSO with stochas-

tic state update. As for GA, the findings of IRace

show that the configuration had a relatively high mu-

tation rate and a relatively low crossover rate when

Using Population-based Metaheuristics and Trend Representative Testing to Compose Strategies for Market Timing

65

Table 1: IRace discovered configurations for each of the

algorithms tested.

PSO PSO

S

GA

Population 45 Population 59 Population 53

Iterations 28 Iterations 261 Generations 266

Neighbors 26 Neighbors 59 Mutation Probability 0.6306

c1 2.4291 c1 3.2761 Crossover Probability 0.455

c2 3.4185 c2 2.363 Tournament Size 22

Clamp Scaling Clamp Scaling

Scaling Factor 0.8974 Scaling Factor 0.551

compared to typical values used for those parame-

ters. This suggests that the solution landscape is on

the rugged side, with sharp peaks and deep valleys

that require radical moves to traverse. The discov-

ered population size and the number of generations

are similar in size to those of PSO

S

.

All algorithms are trained and tested using trend

representative testing. The data used contains 30

strands, representing 10 upwards, 10 downwards and

10 sideways trends at various intensities. The de-

tails of the trend dataset can be seen in Table 2. The

columns in Table 2 describe the symbol of the source

stock data, the beginning date, the ending date and the

trend of every strand in the dataset. The data has then

been split into 10 datasets, where each dataset would

contain one of each trend for testing and the remain-

ing 27 are then used for training. Each step in the

training and testing procedure is repeated 10 times to

cater for the effects of stochasticity.

In total, 63 signal generating components were

used in both training and testing. These 63 compo-

nents are of the technical variety, and contain a selec-

tion of momentum indicators, oscillators, accumula-

tion/distribution indicators, candlestick continuation

pattern detectors and candlestick reversal pattern in-

dicators. Where the components took parameters that

affected periods of data to look at, an upper limit of

45 days was set, so that we could get at least 5 trad-

ing signals within a single trading year (which is on

average compromised of 252 days in the US market).

Any other parameter was initialized to random values

and the best performing setting discovered by the al-

gorithms as they traverse the solution landscape.

Table 3 shows the minimum, median, mean

and maximum fitnesses achieved by each algorithm,

dataset and trend. GA showed a slight edge over

the PSO variants with all three trends in dataset 1,

while PSO

S

showed a clear advantage with the down-

trend in dataset 7. The basic PSO variant takes most

of the wins based on means, when compared to GA

and PSO

S

. By looking at overall averages in Table 4,

we can see that all three algorithms showed a higher

overall fitness during a downtrend when compared

with the other two trends, leaving us with an unbal-

Table 2: Data strands used for training and testing.

Id Symbol Begin Date End Date Length Trend

BSX1 BSX 2012-10-10 2013-07-09 185 ↑

LUV1 LUV 2008-08-22 2010-05-07 430 ↔

KFY1 KFY 2007-05-16 2007-10-12 105 ↓

EXC1 EXC 2003-04-14 2003-08-20 90 ↑

LUV2 LUV 2004-12-03 2005-05-04 105 ↔

KFY2 KFY 2007-03-20 2007-09-21 130 ↓

AVNW1 AVNW 2005-07-18 2006-01-12 125 ↑

PUK1 PUK 2010-08-12 2012-04-03 415 ↔

LUV3 LUV 2008-09-02 2009-01-30 105 ↓

KFY3 KFY 2003-03-13 2003-08-04 100 ↑

EXC2 EXC 2002-10-03 2003-08-04 210 ↔

LUV4 LUV 2003-11-21 2004-04-01 90 ↓

EXC3 EXC 2003-05-12 2003-10-15 110 ↑

PUK2 PUK 2005-05-12 2006-03-13 210 ↔

MGA1 MGA 1996-02-29 1996-07-08 90 ↓

ED1 ED 1997-07-02 1997-11-20 100 ↑

EXC4 EXC 1999-08-20 2000-03-30 155 ↔

PUK3 PUK 2002-03-19 2002-07-25 90 ↓

BSX2 BSX 2009-04-22 2009-09-18 105 ↑

ED2 ED 2011-12-15 2012-05-16 105 ↔

JBLU1 JBLU 2003-05-15 2003-11-10 125 ↓

MGA2 MGA 2012-12-28 2013-10-14 200 ↑

MGA3 MGA 1995-09-19 1996-12-13 315 ↑

ATRO1 ATRO 1997-06-04 1997-11-28 125 ↓

AVNW2 AVNW 2003-03-07 2003-08-05 105 ↑

EXC5 EXC 2015-03-12 2016-09-02 375 ↔

AVNW3 AVNW 2013-06-11 2013-11-20 115 ↓

IAG1 IAG 2015-11-09 2016-08-24 200 ↑

MGA4 MGA 1995-10-17 1996-04-22 130 ↔

IAG2 IAG 2012-01-19 2012-06-04 95 ↓

anced performance. Nevertheless, performing better

in downtrends is positive when compared with buy-

and-hold strategies which would fail under such con-

ditions. This issue of unbalanced performance with

various trend types can perhaps be overcome if the

problem of market timing is approached as a multi-

objective one, where we try to discover a Pareto front

with solutions that maximize fitness across all three

trends. By having the performance of the three algo-

rithms explicitly compared across a variety of trends,

we have a better approximation of the performance of

the strategies produced by these algorithms under live

market conditions, and therein lies the advantage of

using trend representative testing. With step-forward

testing, we are limited to the price movements in the

training section of the data. This can easily lead to

strategies that are overfit to one particular type of

trend, because that was all they were exposed to dur-

ing training. With trend representative testing, we ex-

plicitly avoid this issue by exposing our algorithms to

a variety of trends during both training and testing.

Table 5 shows the rankings of the algorithms af-

ter performing the non-parametric Friedman test with

the Holm’s post-hoc test by trend type on the mean

results (Garc

´

ıa et al., 2010). The first column shows

the trend type; the second column shows the algo-

rithm name; the third column shows the average rank,

ECTA 2019 - 11th International Conference on Evolutionary Computation Theory and Applications

66

Table 3: Computational results for each algorithm over the 10 datasets. The min, median, mean and max values are determined

by running each algorithm 10 times on each dataset. The best result for each dataset and trend combination is shown in bold.

PSO

S

GA PSO

Dataset Trend Test Strand Min Median Mean Max Min Median Mean Max Min Median Mean Max

0 ↑ IAG1 -9.71 -5.79 -6.19 -3.42 -10.35 -5.99 -6.25 -1.39 -4.41 -4.26 -4.01 -3.04

↔ MGA4 0.93 1.19 1.25 1.70 0.39 0.88 0.91 1.60 0.66 1.78 1.60 2.09

↓ IAG2 0.69 0.93 1.22 2.17 0.80 1.95 1.71 2.16 2.17 2.17 2.17 2.17

1 ↑ BSX1 -0.85 -0.34 -0.39 -0.11 -0.67 -0.35 -0.36 -0.13 -5.91 -0.31 -0.85 -0.02

↔ LUV1 -1.10 -0.34 -0.42 -0.08 -1.33 -0.10 -0.28 -0.01 -1.71 -0.11 -0.45 -0.04

↓ KFY1 2.00 2.07 2.07 2.17 2.01 2.08 2.22 2.67 1.86 2.09 2.14 2.66

2 ↑ EXC1 2.80 2.83 2.85 2.92 2.80 2.82 2.83 2.90 2.80 2.80 2.80 2.80

↔ LUV2 2.17 2.31 2.30 2.46 2.09 2.27 2.31 2.64 2.21 2.43 2.44 2.62

↓ KFY2 1.65 2.00 2.04 2.85 1.61 1.75 1.77 2.05 1.56 1.98 2.15 3.61

3 ↑ AVNW1 -3.58 -1.84 -1.21 1.22 -3.83 -2.01 -1.59 1.29 -1.97 0.70 0.10 1.26

↔ PUK1 -2.45 -1.25 -1.00 0.38 -2.84 -1.44 -1.32 0.00 -2.37 -0.05 -0.39 0.00

↓ LUV3 1.58 2.67 3.02 6.12 -0.85 2.91 2.03 4.63 1.08 3.06 3.17 4.70

4 ↑ KFY3 1.39 2.42 2.40 2.94 2.08 2.49 2.45 2.67 2.67 2.72 2.74 2.80

↔ EXC2 0.08 1.13 0.99 1.62 0.16 0.91 0.84 1.55 -0.53 1.31 1.03 1.60

↓ LUV4 2.77 2.85 2.85 2.95 2.80 2.83 2.84 2.96 2.80 2.80 2.80 2.80

5 ↑ EXC3 1.52 2.02 2.00 2.39 1.39 1.64 1.71 2.14 1.96 2.03 2.12 2.38

↔ PUK2 -1.51 -0.23 -0.28 0.76 -4.10 -0.10 -0.88 0.51 0.06 0.59 0.58 1.07

↓ MGA1 2.80 3.14 3.15 3.80 2.80 2.99 2.98 3.15 2.80 2.80 2.80 2.80

6 ↑ ED1 -0.03 1.26 1.21 2.32 0.38 1.14 1.10 1.98 1.75 1.75 1.88 2.44

↔ EXC4 1.20 1.97 2.35 3.96 1.53 2.27 2.33 3.72 0.95 2.07 2.33 3.47

↓ PUK3 2.25 2.43 2.60 3.66 2.38 2.45 2.57 3.66 2.80 2.80 2.80 2.80

7 ↑ BSX2 3.25 3.42 3.48 3.76 3.13 3.42 3.51 4.03 2.28 3.22 3.13 3.32

↔ ED2 2.35 2.52 2.51 2.67 2.46 2.57 2.58 2.70 2.36 2.44 2.45 2.63

↓ JBLU1 6.59 10.68 10.28 13.09 -0.07 9.41 7.99 12.06 0.62 8.08 7.56 11.95

8 ↑ MGA2 -4.87 -4.63 -3.29 0.00 -6.38 -4.34 -4.50 -3.39 -4.69 -4.33 -3.28 -0.04

↔ MGA3 -1.96 -0.10 -0.08 1.34 -1.09 -0.08 -0.13 0.51 -0.17 0.27 0.23 0.48

↓ ATRO1 4.76 9.51 9.17 11.51 -8.86 9.75 8.49 16.08 5.29 9.10 8.68 11.31

9 ↑ AVNW2 3.94 4.77 4.63 5.67 2.09 4.14 4.20 5.65 2.68 3.67 3.48 3.99

↔ EXC5 -0.59 -0.35 -0.19 0.56 -1.18 -0.40 -0.27 0.96 -0.61 0.44 0.27 0.87

↓ AVNW3 1.86 2.01 2.02 2.20 1.75 1.96 1.97 2.14 1.75 1.92 1.94 2.10

Table 4: Overall average fitness by trend for each algorithm.

Algorithm

Trend PSO

S

GA PSO

Downtrend 3.84 3.46 3.62

Sideways 0.74 0.61 1.01

Uptrend 0.55 0.31 0.81

Table 5: Average rankings of each algorithm according to

the Friedman non-parametric test with the Holm post-hoc

test over the mean performance. No statistical differences

at the significance level 5% were observed.

Trend Algorithm Ranking p-value Holm

Downtrend PSO

S

(control) 1.7 – –

PSO 2.0 0.6708 0.05

GA 2.3 0.1797 0.025

Sideways PSO (control) 1.7 – –

GA 2.0 0.5023 0.05

PSO

S

2.3 0.1797 0.025

Uptrend PSO

S

(control) 1.9 – –

GA 1.9 0.9999 0.05

PSO 2.2 0.5023 0.025

where the lower the rank the better the algorithm’s

performance; the fourth column shows the p-value of

the statistical test when the average rank is compared

to the average rank of the algorithm with the best rank

(control algorithm); the fifth shows the Holm’s criti-

cal value. Statistically significant differences at the

5% level between the average ranks of an algorithm

and the control algorithm are determined by the fact

that the p-value is lower than the critical value, indi-

cating that the control algorithm is significantly better

than the algorithm in that row. The non-parametric

Friedman test was chosen as it does not make assump-

tions that the data is normally distributed, a require-

ment for equivalent parametric tests. We can see from

this table that PSO and PSO

S

were ranked higher than

GA in both downtrends and sideways, with a close

tie for uptrends, although not at a statistically signif-

icant level. This suggests that PSO, both in its basic

and modified flavors, is competitive with GA when it

comes to the domain of market timing. PSO, in par-

ticular, has an advantage over GA in that it achieves

these highly competitive results with an order of mag-

nitude fewer number of iterations using a similar pop-

ulation size. The stochastic state update modification

has given PSO

S

a small improvement in ranking when

tested in downtrends and uptrends over the PSO, al-

though this is achieved with a greater number of iter-

ations.

Using Population-based Metaheuristics and Trend Representative Testing to Compose Strategies for Market Timing

67

7 CONCLUSION

In this paper, we reviewed a formulation for the mar-

ket timing problem and introduced three new contri-

butions: (i) using trend representative testing to ex-

pose potential solutions to various market conditions

while training and testing; (ii) designed GA and PSO

algorithms to tackle market timing and finally (iii)

compared our proposed GA and PSO algorithms us-

ing 30 strands (stocks undergoing a particular trend)

and 63 signal generating components. Our results

showed that the PSO variants are competitive to GA –

which is the most widely used metaheuristic in mar-

ket timing – and ranked better when it came to perfor-

mance, with one variant doing so at a fraction of the

number of iterations used by GA.

We suggest the following avenues of future re-

search. First, use a more sophisticated measure of

financial fitness. This would allow us to simulate

hidden costs of trading such as slippage. Second,

approach the problem of market timing as a multi-

objective one by trying to maximize performance

across the three types of trends and against multiple fi-

nancial objectives. Finally, adapt more metaheuristics

to tackle market timing and compare its performance

against the currently proposed ones in significantly

larger datasets. We could then use meta-learning to

understand if and when metaheuristics perform sig-

nificantly better than others under particular condi-

tions and use that information to build hybrid ap-

proaches that use more than one metaheuristic to build

strategies for market timing.

REFERENCES

Abdelbar, A. (2008). Stubborn ants. In IEEE Swarm Intel-

ligence Symposium, SIS 2008, pages 1 – 5.

Allen, F. and Karjalainen, R. (1999). Using genetic algo-

rithms to find technical trading rules. Journal of Fi-

nancial Economics, 51(2):245–271.

Bera, A., Sychel, D., and Sacharski, B. (2014). Improved

Particle Swarm Optimization method for investment

strategies parameters computing. Journal of Theoret-

ical and Applied Computer Science, 8(4):45–55.

Briza, A. C. and Naval Jr., P. C. (2011). Stock trading sys-

tem based on the multi-objective particle swarm opti-

mization of technical indicators on end-of-day market

data. Applied Soft Computing, 11(1):1191–1201.

Chakravarty, S. and Dash, P. K. (2012). A PSO based in-

tegrated functional link net and interval type-2 fuzzy

logic system for predicting stock market indices. Ap-

plied Soft Computing, 12(2):931–941.

Chen, S.-M. and Kao, P.-Y. (2013). TAIEX forecasting

based on fuzzy time series, particle swarm optimiza-

tion techniques and support vector machines. Infor-

mation Sciences, 247:62–71.

Clerc, M. (1999). The swarm and the queen: towards a de-

terministic and adaptive particle swarm optimization.

In Proceedings of the 1999 Congress on Evolution-

ary Computation-CEC99 (Cat. No. 99TH8406), vol-

ume 3, pages 1951–1957.

Clerc, M. (2002). Think locally act locally-a framework for

adaptive particle swarm optimizers. IEEE Journal of

Evolutionary Computation, 29:1951–1957.

de la Fuente, D., Garrido, A., Laviada, J., and G

´

omez, A.

(2006). Genetic algorithms to optimise the time to

make stock market investment. In Genetic and Evolu-

tionary Computation Conference, pages 1857–1858.

Engelbrecht, A. P. (2005). Fundamentals of Computational

Swarm Intelligence. John Wiley & Sons Ltd.

Garc

´

ıa, S., Fern

´

andez, A., Luengo, J., and Herrera, F.

(2010). Advanced nonparametric tests for multiple

comparisons in the design of experiments in compu-

tational intelligence and data mining: Experimental

analysis of power. Inf. Sci., 180(10):2044–2064.

Hu, Y., Liu, K., Zhang, X., Su, L., Ngai, E. W. T., and Liu,

M. (2015). Application of evolutionary computation

for rule discovery in stock algorithmic trading: A lit-

erature review. Applied Soft Computing, 36:534–551.

Kampouridis, M. and Otero, F. E. (2017). Evolving trading

strategies using directional changes. Expert Systems

with Applications, 73:145–160.

Karathanasopoulos, A., Dunis, C., and Khalil, S. (2016).

Modelling, forecasting and trading with a new sliding

window approach: the crack spread example. Quanti-

tative Finance, 7688(September):1–12.

Kaufman, P. J. (2013). Trading Systems and Methods. John

Wiley & Sons, Inc, 5th edition.

Kim, Y., Ahn, W., Oh, K. J., and Enke, D. (2017). An

intelligent hybrid trading system for discovering trad-

ing rules for the futures market using rough sets and

genetic algorithms. Applied Soft Computing, 55:127–

140.

Ladyzynski, P. and Grzegorzewski, P. (2013). Particle

swarm intelligence tunning of fuzzy geometric proto-

forms for price patterns recognition and stock trading.

Expert Systems with Applications, 40(7):2391–2397.

Liu, C. F., Yeh, C. Y., and Lee, S. J. (2012). Application

of type-2 neuro-fuzzy modeling in stock price predic-

tion. Applied Soft Computing, 12(4):1348–1358.

L

´

opez-Ib

´

a

˜

nez, M., Dubois-Lacoste, J., P

´

erez C

´

aceres, L.,

St

¨

utzle, T., and Birattari, M. (2016). The irace pack-

age: Iterated racing for automatic algorithm configu-

ration. Operations Research Perspectives, 3:43–58.

Mohamed, I. and Otero, F. E. (2018). Using Particle

Swarms to Build Strategies for Market Timing: A

Comparative Study. In Swarm Intelligence: 11th

International Conference, ANTS 2018, Rome, Italy,

October 29–31, 2018, Proceedings, pages 435–436.

Springer International Publishing.

Patterson, S. (2013). Dark Pools: The Rise of A.I. Trad-

ing Machines and the Looming Threat to Wall Street.

Random House Business Books.

ECTA 2019 - 11th International Conference on Evolutionary Computation Theory and Applications

68

Penman, S. H. (2013). Financial Statement Analysis and

Security Valuation. McGraw-Hill.

Pring, M. (2002). Technical Analysis Explained. McGraw-

Hill.

Soler-Dominguez, A., Juan, A. A., and Kizys, R. (2017). A

Survey on Financial Applications of Metaheuristics.

ACM Computing Surveys, 50(1):1–23.

Subramanian, H., Ramamoorthy, S., Stone, P., and Kuipers,

B. (2006). Designing Safe, Profitable Automated

Stock Trading Agents Using Evolutionary Algo-

rithms. In Genetic and Evolutionary Computation

Conference, volume 2, page 1777.

Sun, Y. and Gao, Y. (2015). An Improved Hybrid Algorithm

Based on PSO and BP for Stock Price Forecasting.

The Open Cybernetics & Systemics Journal.

Wang, F., Yu, P. L., and Cheung, D. W. (2014). Combining

technical trading rules using particle swarm optimiza-

tion. Expert Systems with Applications, 41(6):3016–

3026.

Using Population-based Metaheuristics and Trend Representative Testing to Compose Strategies for Market Timing

69