Antecedent and Consequence Total Quality Management

in Public Sector Performance

Sanusi Fauji, and Muchlish Munawar

Faculty of Economics and Business, Sultan Ageng Tirtayasa University, Indonesia

Abstract. The purpose of this study is to examine the Model of Organizational

Culture Application as an antecedent variabel of Total Quality Management and

the consequences variable on Public Organizational Performance. This study

uses population in the government in the City of Cilegon, Banten, with a sample

of echelon II, III and IV officials in the Regional Organization of the

Environment (OPD) Cilegon City, Banten. The sampling method in this study

used purposive sampling. This study uses a path analysis tool with the WarpPLS

version 5.0 program to test hypotheses. The results of this study found that there

is an influence between organizational culture and Total Quality Management,

so that it can improve the performance of public organizations in OPD in the

Government of the City of Cilegon.

Keywords: Antecedents Dan Consequences ꞏ Organizational Culture ꞏ Total

Quality Management ꞏ Public Organization Performance

1 Introduction

As part of public sector organizations, the performance of government agencies is now

becoming a concern. Communities began to question the quality they received from the

services carried out by government agencies. Even though the routine and development

budgets issued by the government are increasing, it seems that the community is not

satisfied with the quality of services provided (Putri, 2014). Whereas the government

apparatus is a person who is trusted and given the mandate by the state and citizens to

manage their government in order to improve the welfare of the people. Thus, its

effectiveness must be assessed based on the extent of the government's ability to

improve people's welfare

In a public organization environment, performance is a measure of achievement or

success in running an organization that is related to everything that the organization

does in a certain period of time. In fact, the problem that is often faced by many

organizations, namely employee performance which tends to decline over time which

affects the effectiveness of the organization (Tentama, 2015). Measurement of the

performance of public sector organizations needs to be done because it is useful as a

reference to improve organizational performance in order to be better in the future.

To increase competitive advantage, organizations must implement a quality culture

in every work activity and as an important and key factor in maintaining competitive

advantage. quality-oriented organization, the main focus is customer / community

942

Fauji, S. and Munawar, M.

Antecedent and Consequence Total Quality Management in Public Sector Performance.

DOI: 10.5220/0010609600002900

In Proceedings of the 20th Malaysia Indonesia International Conference on Economics, Management and Accounting (MIICEMA 2019), pages 942-951

ISBN: 978-989-758-582-1; ISSN: 2655-9064

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

satisfaction. To meet the quality of products or services that can satisfy the customer /

community, one appropriate way is to implement Total Quality Management (TQM)

practices that are considered to help organizations to meet the desires of customers /

communities (Malahayati, 2010). Many authors argue that the successful

implementation of TQM is dependent on the prevailing organizational culture, and the

need to change the organizational culture and workforce attitudes so that the

implementation of TQM is effective. Although the important role of organizational

culture has received wide recognition in ensuring the successful implementation of

TQM, there are differences in the empirical literature that examines the relationship

between organizational culture and the application of TQM practices. Although several

previous studies have examined the relationship between TQM practices and

organizational performance in developed countries in the west, including the Kaynak

study (2003) conducted in the United States and the Baird et al. (2011) in Australia.

However, because the cultural diversity in each country is different, this is one factor

that is believed to be able to inhibit the practice of TQM. Research and studies on the

application of TQM practices, especially when related to organizational culture factors

in Indonesia are still limited, given the cultural characteristics in Indonesia that are

different from the culture in which TQM was originally applied. Therefore, researchers

are interested in examining the relationship between organizational culture and the

application of TQM practices in improving the performance of public organizations in

the Regional Government Organization (OPD) of Cilegon City Government.

2 Theoritical Framework and Hypothesis Development

2.1 Influence between Organizational Culture and TQM

The first objective of this study is to examine the relationship between organizational

culture and TQM. Analysis of the relationship between organizational culture and TQM

is problematic with the debate over whether there is a difference between organizational

culture and TQM. Although the organizational culture and TQM are closely related, the

two things are actually different. Schein (1985) and Powell (1995) both support the

distinction between culture and TQM, which states that practices such as TQM may

reflect culture in an organization, but organizational culture itself is more embedded in

organizations that reflect stable patterns and beliefs and values - values developed in a

company (or business unit) over time. Given the inherent nature of culture, and the fact

that the culture of an organization reflects a combination of the characteristics of

various organizations and adopted practices, it is unlikely that the implementation of

one specific management practice such as TQM will have a large impact on the culture

of an organization (Hofstede et al., 1990). Instead, it is stated that the prevailing

organizational culture can support TQM by providing an environment conducive to the

successful implementation of TQM (Powell, 1995). The following hypothesis:

H1a. There is a significant positive influence between the dimensions of

organizational culture dengan

Antecedent and Consequence Total Quality Management in Public Sector Performance

943

TQM requires companies that are constantly looking for ways to improve work

processes so as to improve their ability to produce high-quality products / services.

Companies that have innovation will be more willing to experiment with new practices

such as TQM practices. They will continue to evaluate customer needs and market

expectations in order to develop new products and services and improve the current

production process (Juran, 1988; Baird et al. 2011). Therefore, companies that are more

innovating are more likely to adopt and make extensive use of TQM practices. The

research hypothesis is as follows:

H1b. There is a significant positive influence between the dimensions of

organizational culture with innovation instruments with a level of use of TQM

practices.

2.2 Effects between TQM and Performance

Several research results conclude that TQM as one of the best practice approaches to

improve company performance (Callystha and Devie, 2013; Munizu, 2013; Idris,

2011). In the opinion of Prayhoego and Devie (2013) that a good application of TQM

will be able to improve company performance, that the concept of TQM generally

describes a system that is collective (whole), where the system is related to the

implementation of quality management in order to achieve good organizational

performance. Furthermore according to Nasution (2004) states that TQM influences

organizational performance consisting of product design processes, process flow

management, statistical quality control, long-term relationships with customers,

employee attitudes and company performance on competitive advantage. The

implementation of TQM that can affect company performance is by applying the

elements of TQM as stated by Goetsch and Davis (Tjiptono and Diana, 2001), namely

customer focus, obsession with quality, scientific approach, long-term commitment,

teamwork, improvement system on an ongoing basis, improvement and training,

controlled freedom, unity of purpose, and the involvement in employee empowerment.

The research hypothesis is as follows:

H2. There is a significant positive effect between TQM and Organizational

Performance.

H2

Fig. 1. Theoretical Model.

Team Work

TQM

Innovation

H1a

H1b

Public Org

Performance

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

944

3 Methodology

This type of research is explanatory research. The quantitative method in this study was

used to empirically examine antecedent and consequence Total Quality Management

(TQM).

This study uses population in the government in the City of Cilegon, Banten, with a

sample of echelon II, III and IV officials in the Regional Organization of the Environment (OPD)

Cilegon City, Banten

. Criteria for selection of the sample in the study is aimed at the

sample (purposive sampling). To test the models and hypotheses used analysis of

Structural Equation Modeling (SEM).

This study uses a path analysis tool with the WarpPLS

version 5.0 program to test hypotheses..

In this study data analysis using the Partial Least Square (PLS) approach using

WarpPLS software. PLS is a structural equation model (SEM) based on components

or variances. According to Ghozali (2016) PLS is an alternative approach that shifts

from a covariance-based SEM approach to variant-based. Covariance-based SEM

generally tests causality / theory while PLS is more predictive model. PLS is a

powerful analysis method (Wold, 1985; Ghozali, 2016) because it is not based on

many assumptions. For example, the data must be normally distributed, the sample

does not have to be large. Besides being able to be used to confirm theories, PLS can

also be used to explain the presence or absence of relationships between latent

variables. PLS can simultaneously analyze constructs formed with reflexive and

formative indicators. This cannot be done by SEM which is based on covariance

because it will become an unidentified model.

4 Result and Discussion

4.1 Outer and Inner Model Testing

In testing the reliability value of a construct the value used for Cronbach's Alpha and

Composite Reliability is where both values are greater than 0.7 (> 0.7) for confirmatory

research and greater than 0.6 (> 0.6) for exploratory research is still acceptable. (Hair

et al., 2010, 2011; Pirouz 2006,; Ghozali 2016). Furthermore, the average variances

extracted (AVE) value of the construct must be above 0.5 (> 0.5). (Bagozzi and

Baumgartner, 1994; Ghozali, 2016).

Based on the approach in the reliability test above, the following are presented the

values of Cronbach's Alpha, Composite Reliability, Average variances extracted from

each construct of this study with confirmatory factor analysis with WarpPLS 5.0.

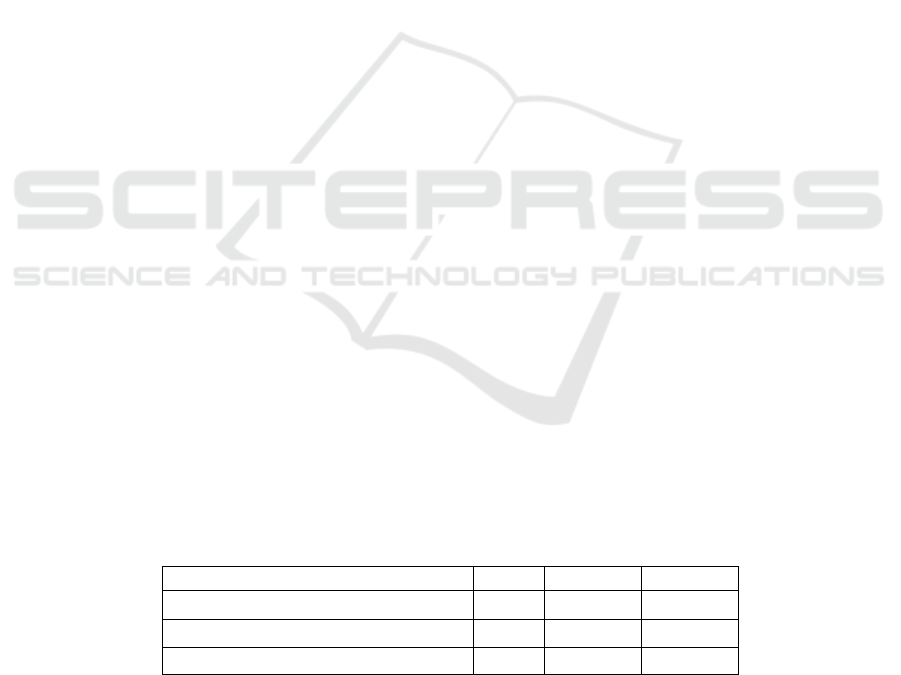

Table 1. Score of Composite reliabiLity Coeffecients, Cronbach Alpha Coefficients Dan

Average Variances Extracted.

ITC CE PERF

Composite reliability coefficients

0.905 0.921 0.880

Cronbach alpha Coefficients

0.873 0.905 0.834

Average Extracted

0.615 0.519 0.555

Antecedent and Consequence Total Quality Management in Public Sector Performance

945

Table 1 shows that the composite reliability value of the construct studied was above

the recommended threshold, where the composite reliability value was greater than 0.6

(> 0.6), namely: ITC of 0.905, CE of 0.921, and PERF of 0.880. Cronbach alpha

coefficients value of each construct is above the recommended threshold, where the

Cronbach alpha coefficients value is greater than 0.6 (> 0.6), namely: ITC of 0.873, CE

of 0.905, and PERF of 0.834.

Average variances extracted (AVE) value of each construct is above the

recommended threshold, where the AVE value is greater than 0.5 (> 0.5), namely: ITC

of 0.615, CE of 0.519, and PERF of 0.555. Based on the value of composite reliability,

cronbach alpha coefficient and Average variances extracted from the ITC, CE, and

PERF constructs that are above the recommended threshold, then all constructs have

met the composite reliability requirements

4.2 Full Model Testing

The results of testing the full research model with WarpPLS 5.0 are presented in Figure

2, table 2 and Table 3.

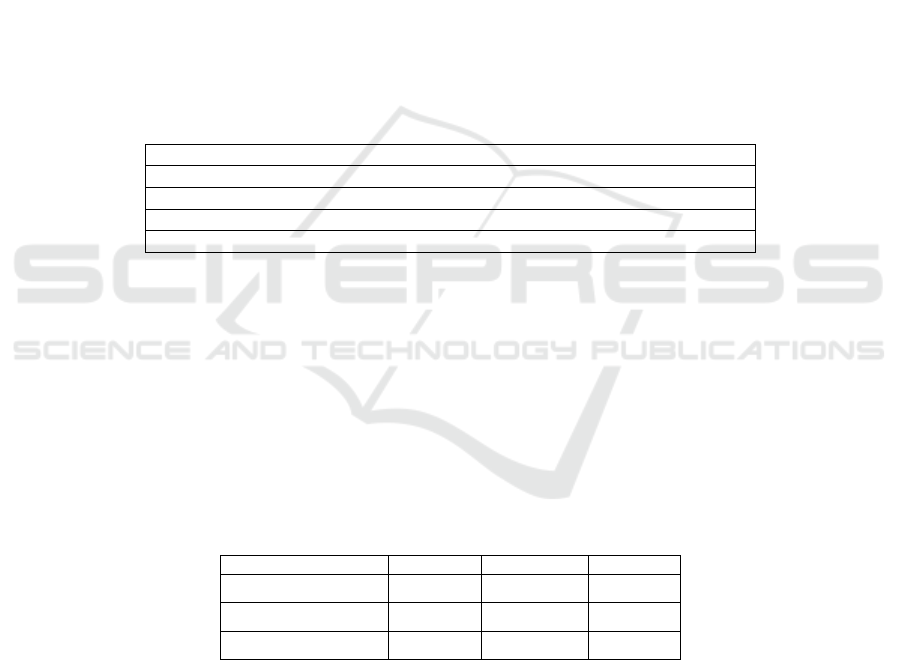

Table 2. Model Fit dan Quality Indice Full Model.

A

verage Path Coefficient (APC)= 0.833, P<0.001

A

vera

g

e R-S

q

uared

(

ARS

)

= 0.698, P<0.001

A

vera

g

e ad

j

usted

R

-S

q

uared

(

AARS

)

= 0.696, P<0.001

A

vera

g

e

f

ull collineartit

y

VIF

(

AAVIF

)

= 4.895, acce

p

table if <= 5, ideall

y

<= 3.3

Tenenhaus GoF (GoF) = 0.623, small >= 0.1, medium >= 0.25, large >= 0.3

6

Based on the Model Fit and Quality Indice Full Model output presented in Table 2, it

is known that the Average path coefficient (APC) has an index of 0.833 with a p-value

<0.001, Average R-squared (ARS) has an index of 0.698 with a p-value < 0.001 and

Average adjusted R-squared (AARS) have an index of 0.696. The p-value for APC,

ARS and AARS that is recommended as a fit model is 5 0.05 (Ghozali and Latan, 2017;

Kock, 2012). Thus it can be concluded that this study is fit. This is also supported by

the value of Average full collinearity VIF (AAVIF) = 4,895, less than the value of 5

(acceptable). Thus indicating that there is no multicollinearity problem between

indicators and between exogenous variables. The predictive power of the model

described by GoF is 0.713, including the large category because it is greater than 0.36.

Table 3. R-Squared, Adj R-Square dan Full Collin VIF.

ITC CE PERF

R-squared

0.562

Adjusted R-squared

0.802

0.559

Full Collin VIF 4.973 4.962 3.360

Table 3 presents the structural model analysis outputs about R-squared (R2),

Adjusted R-squared (Adj. R2), Full Collinearity VIF and Q-Squared (Q2). R2 shows

the percentage of endogenous construct variance / criterion can be explained by the

construct hypothesized to influence it (exogenous / predictor) (Sholihin and Ratmono,

2014). Adj. R2 is similar to R2 but is used to avoid estimation bias in R2, because the

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

946

more predictor variables in the model, R2 will be greater and continue to increase

(Ghozali and Latan, 2016). Criteria for R2 and Adj. R2 ≤0.70, ≤0.45 and ≤0.25 show

strong, moderate and weak models.

Based on table 3 it can be seen that R-squared (R2) and Adjusted R-squared (Adj.

R2) of this research model tend to be moderate because the barada is above 0.25%. Full

ollinearity VIF is used to check whether collinearity problems occur vertically or

laterally (Ghozali and Latan, 2017). The criterion for a model that is free from vertical

and lateral multicollinearity problems is that the Full Collinearity VIF value must be

lower than 3.3. However, values ≤5 are still acceptable (Ghozali and Latan, 2017;

Sholihin and Ratmono, 2014; Kock, 2012). ased on table 3 it can be seen that the model

used in this study is free from the problem of vertical or lateral colonierity. Because all

VIF Full Collinearity values are less than 5. After the tructural model has been declared

fit and can be accepted by data quality testing, then an analysis and interpretation of the

structural model will be used to test the research hypothesis. Bootstrapping method for

research models with SEM Analysis with WarpPLS 5.0 of each construct with the

following results: R-squared (R2), Adjusted R-squared (Adj. R2), and Full Collinearity

VIF.

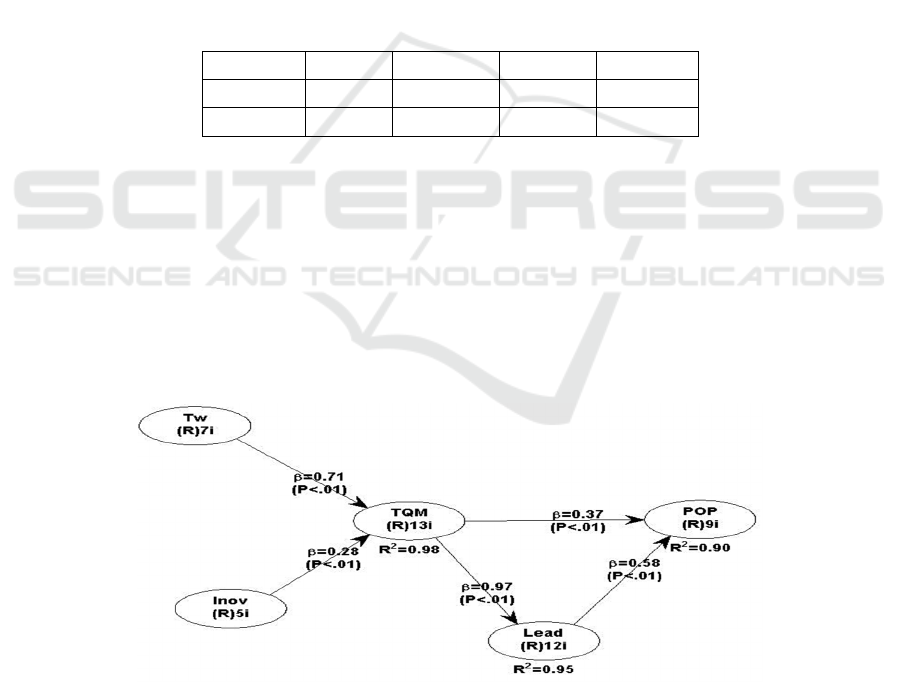

Table 4. Path Coefficient, P-value dan Effect Size Full Model.

Relationship Estimate Effect Size P-Value Decision

ITC CE 0.897 0.804 (<0.001)* H1: Accepted

ITCPERF 0.750 0.562 (<0.001)* H2: Accepted

Variation of certain exogenous variables to endogenous variables is called effect

size. Effect size measures the contribution of variants from each predictor in the R-

Square coefficient model of a particular endogenous variable. Effect sizes can be

grouped into three categories, namely weak (0.02), medium (0.15) and large (0.35)

(Sholihin and Ratmono, 2014).

Based on table 4 it can be seen that the variable Information Technology Capability

(ITC) has the biggest effect size on the Cost Effectiveness (CE) variable, which is

0.804. The effect size of the effect of ITC on the PERF variable of 0.562 is also quite

large. Thus it can be concluded that Information Technology Capability (ITC) has a

greater role from the perspective of Cost effectiveness (EC) compared to PERF.

Fig. 2. Output WarpPLS 5.0 Full Model.

Antecedent and Consequence Total Quality Management in Public Sector Performance

947

4.3 Hypothesis Testing

Hypothesis 1 states that Information Technology Capability (ITC) has a significant

positive effect on Cost effectiveness (CE). To prove this hypothesis, a direct effect test

was conducted with WarpPLS version 5.0. Tests performed are model fit testing, path

coefficient analysis and p-value. The test results are presented in Figure 2; Table 2;

Table 3 and Table 4. Based on table 2 it is known that the model fit criteria have been

met, where the APC, ARS, AARS values are below 0.05, the AFVIF value <5 and the

GoF value are included in the large category that is above 0.36. Table 4 presents the

path coefficients produced are 0.897 and significant with p values <0.001 (α1%). Thus

it can be concluded that hypothesis 1 is accepted. This means that Information

Technology Capability (ITC) has a significant positive effect on Cost Effectiveness

(CE) with a coefficient of determination of 0.804 shown in table 3.

Hypothesis 2 states that Information Technology Capability (ITC) has a significant

positive effect on Business Performance (PERF). To prove this hypothesis, a direct

effect test was conducted with WarpPLS version 5.0. Tests performed are model fit

testing, path coefficient analysis and p-value. The test results are presented in Figure 2;

Table 2; Table 3 and Table 4.

Based on table 2, it is known that the criteria for model fit have been fulfilled, where

the APC, ARS, AARS values are below 0.05, AFVIF values <5 and GoF values are

included in the large category above 0.36. Table 4 presents the path coefficients

produced are 0.750 and significant with p values <0.001 (α1%). Thus it can be

concluded that hypothesis 2 is accepted. This means that Information Technology

Capability (ITC) has a significant positive effect on SME’s Performance (PERF) with

a coefficient of determination of 0.562 shown in table 3.

4.4 Discussion

This section will discuss research findings that have been analyzed and tested in the

previous section. The discussion is based on the value of the results of statistical testing

with WarpPLS 5.0 software which is based on the building of theory and empirical

research referred to and developed in this study. The discussion will be conducted based

on the results of data analysis and hypothesis testing proposed in this study and the

relationship with the findings from previous studies

4.4.1 Information Technology Capability (ITC) Has a Significant Positive Effect

on Cost Effectiveness (CE)

Hypothesis 1 of this study states that Information Technology Capability (ITC) has a

positive effect on Cost Effectiveness (CE). The test results using WarpPLS 5.0 show a

path coefficient of 0.897 and p-value <0.01. Based on these figures it is concluded that

hypothesis 1 can be accepted, meaning that Information Technology Capability (ITC)

has a positive effect on Cost Effectiveness (CE).

Chriswan and Mahmudin (2008) stated that information technology offers many

opportunities to reduce costs, increase efficiency, increase effectiveness and revenues

and can improve cost control. Sophisticated technology and information can help

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

948

companies to monitor the activities carried out by their employees, so the company can

obtain information more quickly and accurately used in decision making. If a mistake

or deviation occurs, the company can immediately take corrective actions so that the

effectiveness in the use of operational costs can be identified quickly so that the

company's goals can be achieved. Previous research supporting this research was a

study conducted by Salim Ridwan (2014) and Ilker Calayoglu & Murat Azaltun (2013)

which suggested that information technology significantly influences the effectiveness

of cost control in an organization.

Cost control must primarily be aligned with the goals to be achieved by the

company, one of the goals to be achieved by the company is to obtain maximum profit

by issuing the lowest costs, therefore by controlling the production costs the company

hopes to get a large profit. A company in order to compete in a market environment,

the company is also required to be able to create a good product innovation, and the

price is lower or at least the same as the price offered by its competitors.

4.5.2 Information Technology Capability (ITC) has a significant positive effect on

SME’s Performance (PERF)

Hypothesis 2 of this study states that Information Technology Capability (KTI) has

a positive effect on Business Performance (KIN). The test results using WarpPLS 5.0

show the path coefficient of 0.750 and p-value <0.01. Based on these figures it is

concluded that hypothesis 3 can be accepted, meaning that Information Technology

Capability (KTI) has a positive effect on Business Performance (KIN).

This hypothesis is supported by previous researchers finding a significant

relationship between information technology and performance. Kelley (1994), Siegel

and Griliches (1992) state that some of the results of the study found a positive effect

of information technology on company performance at the industry level. Diewert and

Smith (1994), Hitt and Brynjoltsson (1995), Board and Min (1997), Devaraj and Kohli

(2003) indicate that there is a positive relationship between technology and company

performance.

However, this research is not supported by Devaraj and Kohli (2003) stating that

there are some studies that do not find a significant relationship between information

technology and performance. Baily (1986), Roach (1987), Morrison and Berndt (1991),

Devaraj and Kohli (2003) find a negative relationship between information technology

relatedness variables that are associated with firm performance. In addition, Berndt and

Morrison (1995) and Kohli (1999) find that there is no significant relationship between

investing in information technology and performance.

The above findings are not consistent with previous studies conducted by Kelley

(1994), Siegel and Griliches (1992), Diewert and Smith (1994), Hitt and Brynjoltsson

(1995), Council and Min (1997); Devaraj and Kohli (2003). Research conducted by

Nengah, (2005) also found that information technology contributes a positive and

insignificant value to business process performance and competitive dynamics.

References

Ahire, S.L. and Dreyfus, P. (2000). “The impact of design management and process management

on quality: an empirical investigation”. Journal of Operations Management, Vol.18, pp. 549-

75.

Antecedent and Consequence Total Quality Management in Public Sector Performance

949

Baird, K.M., Harrison, G.J. and Reeve, R.C. (2007). “The culture of Australian organizations and

its relation with strategy”. International Journal of Business Studies, Vol. 15 No. 1, pp. 15-41.

Baird, K.M., Jia Hu, K. and Reeve, R.C. (2011). “The relationships between organizational

culture, total quality management practices and operational performance”. International

Journal of Operations & Production Management, Vol. 31 No. 7, pp. 789-814.

Balakrishnan, R., Linsmeier, T.J. and Venkatachalam, M. (1996). “Financial benefits from JIT

adoption: effects of customer concentration and cost structure”. The Accounting Review,

Vol. 71 No. 2, pp. 183-205.

Ciptani, Monika Kussetya. (1999). Pengukuran Biaya Kualitas : Suatu Paradigma Alternatif.

Jurnal Akuntansi dan Keuangan Vol. 1, No. 1: 68 -83.

Forza, C. and Filippini, R. (1998). “TQM impact on quality conformance and customer satisfaction:

a causal model”. International Journal of Production Economics, Vol. 55 No. 1, pp. 1-20.

Gotzamani, K.D. and Tsiotras, G.D. (2001). “An empirical study of the ISO9000 standards’

contribution towards total quality management”. International Journal of Operations &

Production Management, Vol. 21 No. 10, pp. 1326-42.

Gozhali, I. (2008). Model Persamaan Struktural Konsep dan Aplikasi Dengan Program AMOS

16.0. Semarang. Badan Penerbit Universitas Diponegoro.

Hofstede, G., Neuijen, B., Ohayv, D.D. and Sanders, G. (1990). “Measuring organizational

cultures: a qualitative and quantitative study across twenty cases”. Administrative Science

Quarterly, June, pp. 286-316.

Kaluarachchi, K.A.S.P. (2010). “Organizational culture and total quality management practices:

a Sri Lankan case”. The TQM Journal, Vol. 22 No. 1, pp. 41-55.

Kaynak, H. (2003). “The relationship between total quality management practices and their

effects on firm performance”. Journal of Operations Management, Vol. 21, pp. 405-35.

Kiella, M.L. and Golhar, D.Y. (1997). “Total quality management in an R&D environment”.

International Journal of Operations & Production Management, Vol. 17 No. 2, pp. 184-98.

Kuo, Tsuang and Gwo Yang Tsai (2017). “The effects of employee perceived organisational

culture on performance: the moderating effects of management maturity”. Department of

Business Management, National Sun Yat-sen University, Kaohsiung City, Taiwan. Volume

30, 2019 - Issue 3-4

Malahayati, Anastasia. (2010). “Implementasi Adopsi Total Quality Management (TQM)

Terhadap Budaya Kualitas (Studi pada PT. Aryan Indonesia/Kidzania Jakarta)”. Tesis S2

Universitas Pembangunan Nasional “Veteran”. Jakarta.

Mahfouz, S.S.A. (2019). “TQM practices and organizational performance in the manufacturing

sector in Jordan: The mediating role of HRM practices and innovation”. Journal of

Management and Operational Research, 1(22).

Mardiyah, Aida Ainul dan Listianingsih. (2005). “Pengaruh Sistem Pengukuran Kinerja, Sistem

Reward, dan Profit Center Terhadap Hubungan Antara Total Quality Management dengan

Kinerja Manajerial”. Makalah disampaikan pada SNA VIII Solo, 15 – 16 September 2005.

Mohamud, G. Y., Muhamud, A. S., & Mohamed, B. H. (2015). “The relationship between

strategic management and organizational performance in Mogadishu-Somalia”. European

Journal of Research and Reflection in Management Sciences, 3(2), 42-51.

O’Reilly, C.A., Chatman, J. and Caldwell, D.F. (1991). “People and organizational culture: a

profile comparison approach to assessing person-organizational fit”. Academy of

Management Journal, Vol. 34 No. 3, pp. 487-516.

Oruma, B. W., Mironga, J. M., & Muma, B. O. (2014).”Top management commitment towards

implementation of Total Quality Management (TQM) in construction companies in Nakuru

county Kenya”. International Journal of Economics, Finance and Management Sciences,

2(6), 332-338.

Powell, T.C. (1995). “Total quality management as competitive advantage: a review and

empirical study”. Strategic Management Journal, Vol. 16, pp. 15-37.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

950

Prajogo, D.I. and McDermott, C.M. (2005). “The relationship between total quality management

practices and organizational culture”. International Journal of Operations & Production

Management, Vol. 25 No. 11, pp. 1101-22.

Rad, M.M.A. (2006). “The impact of organizational culture on the successful implementation of

total quality management”. The TQM Magazine, Vol. 18 No. 6, pp. 606-625.

Rahman, N., Othman, M., Yajid, M., Rahman, S., Yaakob, A., Masri, R., Ramli, S & Ibrahim, Z.

(2018). “Impact of strategic leadership on organizational performance, strategic orientation

and operational strategy”. Management Science Letters, 8(12), 1387-1398.

Samson, D. and Terziovski, M. (1999). “The relationship between total quality management

practices and operational performance”. Journal of Operations Management, Vol. 17 No. 4,

pp. 393-409.

Santoso, Singgih. (2011). Structural Equation Modeling (Konsep dan Aplikasi dengan AMOS

18). Jakarta. Penerbit PT Elex Media Komputindo.

Wicaksono, Setiawan. (2006). “Pengaruh Implementasi Total Quality Management (TQM)

Terhadap Budaya Kualitas (Studi pada PT. Hari Terang Industry – Surabaya)”. Tesis S2

Universitas Brawijaya. Malang.

Antecedent and Consequence Total Quality Management in Public Sector Performance

951