The Effect of Profitability, Managerial Ownership and

Dividend Policy on Company Value on Property

Companies Listed on the Indonesia Stock Exchange

Chairil Akhyar, Marzuki, Ghazali Syamni

,

Nazir and Zahrina

Departement of Management, Faculty of Economic and Business,

Universitas Malikussaleh, Lhokseumawe, Indonesia

Chairil.akhyar@gmail.com,nazir_palohbatee@yahoo.com,

zahrina043@gmail.com

Abstract. The purpose of this study was to examine the effect of profitability,

managerial ownership and dividend policy on company value on property

companies listed on the Indonesia Stock Exchange. The data used in this research

were ROE, KM, DPR and PBV data on property companies in Indonesia Stock

Exchange during 2013-2016. The data of this study were accessed on

www.idx.co.id and www.bi.go.id. The method of data analysis in this study was

multiple linear regression analysis. The results of the study found that

Profitability (ROE) and Dividend Policy (DPR) had a positive and significant

effect on company value, while managerial ownership had a negative effect on

company value. The simultaneous test results found that profitability, managerial

ownership, and dividend policy had a significant effect on company value.

Keywords: Profitability ꞏ Managerial Ownership ꞏ Dividend Policy and

Company Value

1 Introduction

The development of the capital market in Indonesia is currently increasing; the capital

market is a market for a variety of long-term financial instruments that can be traded,

either in the form of debt or shares. The company will strive to achieve its goals, both

long-term goals and short-term goals in increasing the value of the company will be

seen from the stock market price. The Property Sector is one sector that has a high risk.

The Property Sector is strongly influenced by the economic conditions of a country. In

2016 is a year of business revival in the property sector. With the increase in property

sales in a number of regions in Indonesia, it is a resurgence point in the property sector.

However, in mid-2014 and throughout 2015 the property sector business in Indonesia

was considered weak due to economic growth which was under-estimated and the

movement of the rupiah and several currencies in other countries weakened against the

US dollar, (www.bisnis.com, 2016).

The value of the company is very important because the value of the company can

describe the company's performance which can affect the response of investors to the

company. According to Moniaga (2013) the value of a company can be said to be an

investor's perception of the company, which is often associated with stock prices.

Akhyar, C., Marzuki, ., Syamni, G., Nazir, . and Zahrina, .

The Effect of Profitability, Managerial Ownership and Dividend Policy on Company Value on Property Companies Listed on the Indonesia Stock Exchange.

DOI: 10.5220/0010598600002900

In Proceedings of the 20th Malaysia Indonesia International Conference on Economics, Management and Accounting (MIICEMA 2019), pages 809-816

ISBN: 978-989-758-582-1; ISSN: 2655-9064

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

809

Investors can use the value of the company as a basis for seeing the company's

performance in the coming period. Profitability is one of the factors that can affect a

company's value. Profitability can measure a company's ability to make a profit.

According to Husnan (2001) profitability is the ability of a company to generate profits

at certain levels of sales, assets and share capital. Managerial ownership, managers have

an important role in planning, organizing, directing, supervising, and making decisions.

Managerial share ownership can align between the interests of shareholders and

managers, because managerial ownership provides the opportunity for managers to be

involved in share ownership so that the position of the manager is equal to the

shareholders. Managerial is also a factor that determines the value of a company.

With increasing managerial ownership, managers will be motivated to improve their

performance so that they will have a good impact on the company.

Dividend policy is to determine how much profit the shareholders will get so that

the profits to be gained by these shareholders will determine the welfare of the

shareholders who are the main objectives of the company. If dividend distribution

decreases, the company's financial condition cannot be controlled. If the company

distributes dividends in a long period of time, the company's financial condition will be

controlled so that it can convince investors that the company has a good performance.

The problem formulation in this study is "Whether profitability, managerial ownership

and dividend policy have a partial effect on the value of the company in property

companies listed on the Indonesia Stock Exchange".

2 Manuscript Preparation

The company will strive to achieve its objectives, both long-term goals such as being

able to increase the value of the company and the welfare of shareholders, as well as its

short-term goals for example maximizing the company's profits with the resources they

have. With the good value of the company, the company will be well looked at by

investors. Likewise the opposite if the value of the company is high, it can show good

company performance. Sartono (2001) states that the value of a company as a price that

is willing to be paid by investors if a company is to be sold. Company value can reflect

the value of assets owned by a company such as securities. In a company, managerial

ownership is often associated as an effort to increase the value of the company because

the manager other than as a management as well as the owner of the company.

According to Kasmir (2010) profitability ratio is the ratio used to assess the company's

profit in seeking an advantage. As for the notion of profitability according to Kasmir

(2014) is the ratio used to assess the company's profit in seeking an advantage.

According to Anita (2016) managerial ownership is a situation where the manager

has a company share or in other words the manager is also a shareholder of the

company. The managerial shareholding level of a company can be measured using the

proportion of shares in a company owned by management at the end of the year which

is expressed as a percentage, Haruman (2008). In the financial statements, notes to

financial statements are indicated by the percentage of company ownership by the

manager. Managerial ownership can be measured by the proportion of share ownership

held by managerial. According to Arifin (2014), formulated by the number of shares of

the management divided by the total shares outstanding. Managerial ownership is a

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

810

situation where the manager has a share of the company or in other words the manager

as a shareholder of the company and it can be concluded that managerial ownership is

the manager of the company concurrently as company management as well as active

shareholders in decision making.

Dividend policy determines how much profit shareholders will get. The profits that

these shareholders will get will determine the welfare of shareholders who are the main

objectives of the company. Dividend policy is an inseparable part of corporate funding

decisions. Dividend policy is a decision about how much current profits will be paid as

dividends instead of investments invested and how much is retained for reinvestment

in the company, Brigham and Houston (2010)

Dividend policy is an integral part of the company's funding decisions. Dividend

payout ratio determines the amount of profit that can be held as a source of funding.

The greater retained earnings the less the amount of profit allocated for dividend

payments. Definition of dividend payout ratio (dividend payout ratio) according to

Sartono (2009) states that "The ratio of dividend payments is the percentage of earnings

paid in the form of dividends, or the ratio between earnings paid in the form of

dividends and the total profit available to shareholders". Dividend policy in this

research is proxied in the form of Dividend Payout Ratio (DPR), where the DPR shows

the comparison between dividends paid by the company to shareholders in the form of

cash dividends with earnings per share (earning per share) formulated by calculating

dividends per share divided with earnings per share, Hanafi and Halim (2003).

2.1 The Conceptual Framework

The conceptual framework is a model that explains how the mindset is used to see the

direction of research and the relationship of a theory with important factors that have

been known in a particular problem.

From the conceptual framework it can be seen that the dependent variable in this study

is firm value (Y), while for the independent variables are profitability (X_1),

managerial ownership (X_2) and dividend policy (X_3). then to achieve partial

influence between the independent variables on the dependent variable used t test.

2.2 The Research Hypothesis

According to Sugiyono (2016) the hypothesis is a temporary answer to the research

problem formulation, in which the research problem formulation has been expressed in

the form of question sentences. As for the hypotheses that will be proposed in this study

are as follows:

H1: Profitability, Managerial Ownership and Dividend Policy have a positive effect on

Company Value on Property Companies listed on the Indonesia Stock Exchange.

The Effect of Profitability, Managerial Ownership and Dividend Policy on Company Value on Property Companies Listed on the Indonesia

Stock Exchange

811

3 Metode Penelitian

The object in this study is profitability, managerial ownership, dividend policy and

company value on property companies listed on the Indonesia Stock Exchange. The

location in this study is on the Indonesia Stock Exchange by accessing the official

website, www.idx.co.id.

3.1 The Research Population

In a study there is a population called. According to Sugiyono (2016) the population is

an area of generalization consisting of objects or subjects that have the quality and

research of certain characteristics applied by researchers to be studied and then drawn

conclusions. The population used in this study is property companies that listed on the

Indonesia Stock Exchange, which are 49 companies.

3.2 The Research Sample

The part taken in the population is called the sample. According to Sugiyono (2016)

The sample is part of the number and characteristics possessed by the population.

Because researchers are not likely to learn everything in the population, for example

due to limited labor and time, researchers can use a sample taken from that population.

What is learned from the sample, the conclusion will be applicable to the population.

The samples were 31 property companies on the Indonesia Stock Exchange that have

complete data during the study period as purposive sampling method. While 18 more

companies did not meet the criteria.

3.3 The Types and Sources of Data

The type of data used in this study is secondary data. Sugiyono (2016) said that

secondary data is data obtained indirectly from books, records, existing evidence or

published and unpublished files which the quantitative data is measured in a numerical

scale (number). This quantitative data is in the form of time series data, that is data

arranged according to time on a particular variable.

In this study is used the quantitative data sources from www.idx.co.id and also the

internet, while qualitative data was collected through literature studies both books,

research journals and materials from the internet related to research.

3.4 Data Collection Technique

Data collection techniques used in this study are documentation study methods.

Documentation study method is collecting information from evidence and documents

relating to the object of research, in the form of financial statements consisting of

income statements, balance sheets carried out by the author to be used as material in

this study.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

812

Variable Operational Definition

The variables in this study consist of independent variables namely profitability,

managerial ownership and dividend policy, and the dependent variable is the value of

the company, so the following will be described by the operational definition of the

variable:

Profitability (ROE (X1)) is to illustrate the extent to which a company's ability to

generate profits will be obtained by shareholders.

Managerial ownership (X2) is a managerial condition of owning the company's

shares or in other words the manager as a shareholder of the company.

DPR (X3) is determining the amount of profit that can be held as a source of funding

and invested in the company

Company Value (Y) Comparison between stock prices and book value per share.

The value of the company is the price that is willing to be shared by the buyer if the

company is sold.

4 Results and Discussion

The Proprietary Company is one of the industrial sectors listed on the Indonesia Stock

Exchange (IDX). The development of the property industry is so fast now and will be

even greater in the future. This is due to the increasing population while the land supply

is fixed. At the beginning of 1968, the property industry began to emerge and starting

in the 80s, the property industry began to be listed on the IDX. As for the number of

property companies listed on the Stock Exchange in 2003 there were 30 companies.

Evidenced by the increasing number of property sectors that expand land banks

(assets in the form of land), do business expansion and up to 2016 the property sector

listed on the Stock Exchange increased to 49 companies.

Statistical Descriptive Analysis

Descriptive analysis was carried out to find out about the data perception used in the

study. In the descriptive analysis, we will see how the mean, median and maximum and

minimum values in the data used in this study

The results of the descriptive analysis in this study are as follows:

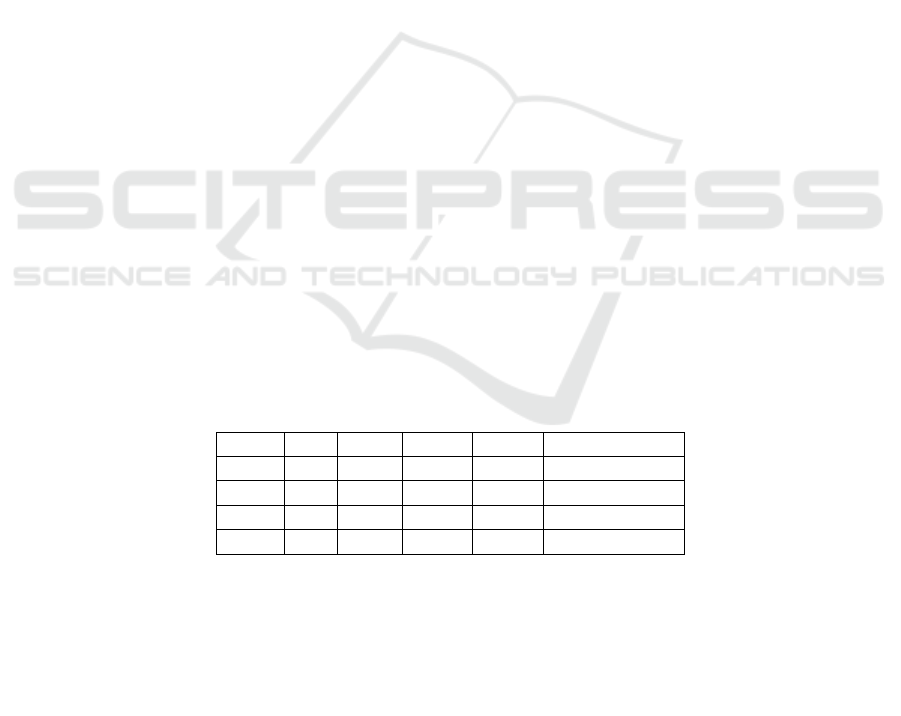

Table 1. Statistical Descriptive Analysis.

N

Min Max Mean Std. Deviation

ROE

124 0.14 52.43 10.55 9.40

KM

124 0.05 0.93 0.38 0.24

DPR

124 0.01 7.62 0.35 0.77

PBV

124 0.12 8.90 1.72 1.81

In Table 1 above, the number of observations made for this study was 124 observations.

The lowest value of ROE in this study is 0.14 while the highest value of ROE in this

study is 52.43. It is seen that the average value of ROE in this study is 10.55 with a

standard deviation value of 9.40. The average value of ROE is greater than the standard

deviation value. This shows that the ROE fluctuations in this study are fluctuations that

tend to be small.

The Effect of Profitability, Managerial Ownership and Dividend Policy on Company Value on Property Companies Listed on the Indonesia

Stock Exchange

813

In the table above, The lowest value of Management Ownership in this study is 0.05

while the highest value is 0.93. It can be seen that the average value is 0.38 with a

standard deviation value of 0.24. The average value is greater than the standard

deviation value. This shows that the fluctuations in KM in this study are fluctuations

that tend to be small. The lowest value of the DPR in this study is 0.01 while the highest

value is 7.62. that the average value of the DPR in this study is 0.35 with a standard

deviation value of 0.77. The average value of the DPR is smaller than the standard

deviation value. This shows that the fluctuations in the DPR in this study are

fluctuations that tend to be large. While the lowest value of PBV in this study is 0.12

while the highest value is 8.90. It can be seen that the average value of this study is 1.72

with a standard deviation value of 1.81. The average value is smaller than the standard

deviation value. This shows that PBV fluctuations in this study are fluctuations that

tend to be large.

The results of multiple linear regression in this study are as follows:

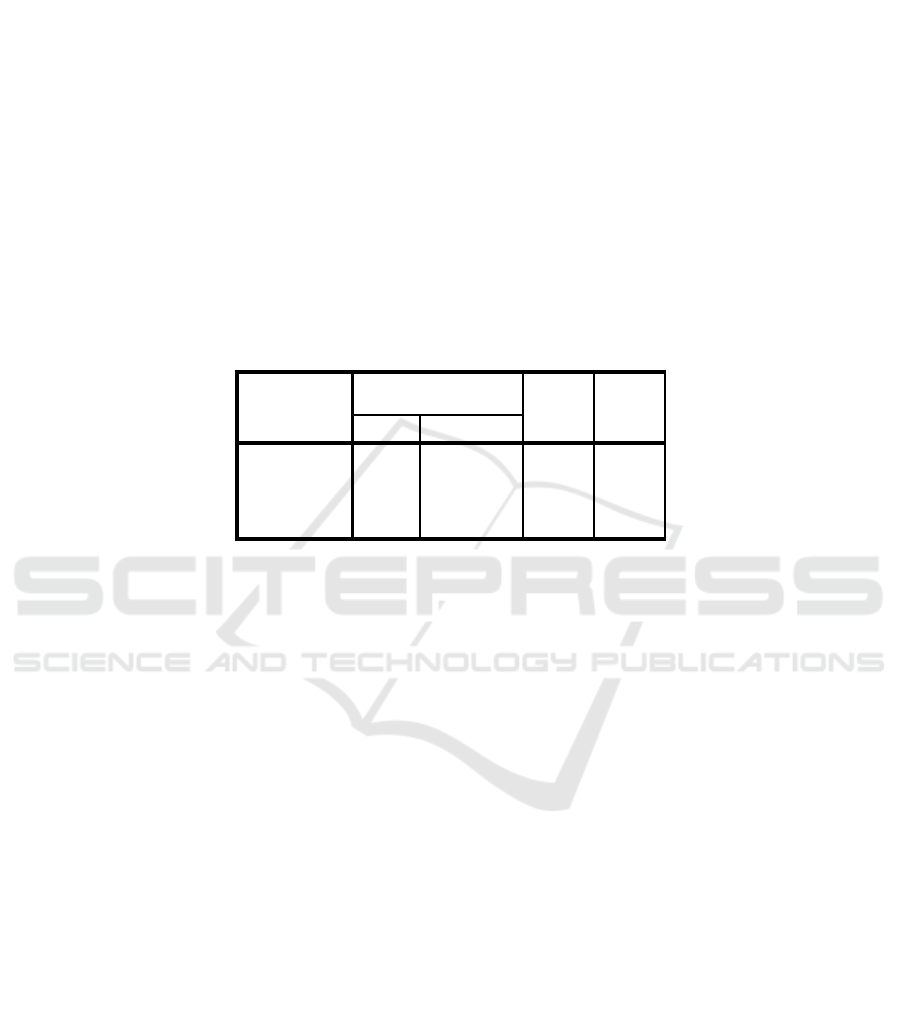

Table 2. Multiple Linear Regression Estimates.

Model

unbstandardized

Coefficients

t Sig.

B Std. Erro

r

(

Constant

)

-.089 .275 -.323 .748

ROE .261 .056 4.638 .000

KM -.461 .356 -1.294 .198

DPR .153 .071 2.135 .035

Based on Table 2 above, it can be arranged multiple linear regression equations in this

study as follows:

PBV = -0,089 + 0,261ROE - 0,461KM + 0,153DPR

The value of the constantan is -0.089 which indicates that if all the independent

variables in this study namely ROE, KM and DPR are 0 then PBV will remain constant

with a value of -0.089, ROE has a positive influence on PBV with a regression

coefficient of 0.216. This shows that if ROE is added by 1% it will increase the PBV

value by 0.216, KM has a negative influence on PBV with a regression coefficient of -

0.461. This shows that if KM is added by 1% it will decrease the PBV value by -0.461,

the DPR has a positive influence on PBV with a regression coefficient of 0.153. This

shows that if the DPR is increased by 1%, it will increase the PBV value by 0.153.

Correlation Analysis and Determination Coefficients

Correlation coefficient is a value that shows how much the independent variables

relationship to the dependent variable. Meanwhile, the coefficient of determination is a

value that shows how much the independent variable is able to explain the dependent

variable. The results of the correlation and determination analysis in this study are as

follows:

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

814

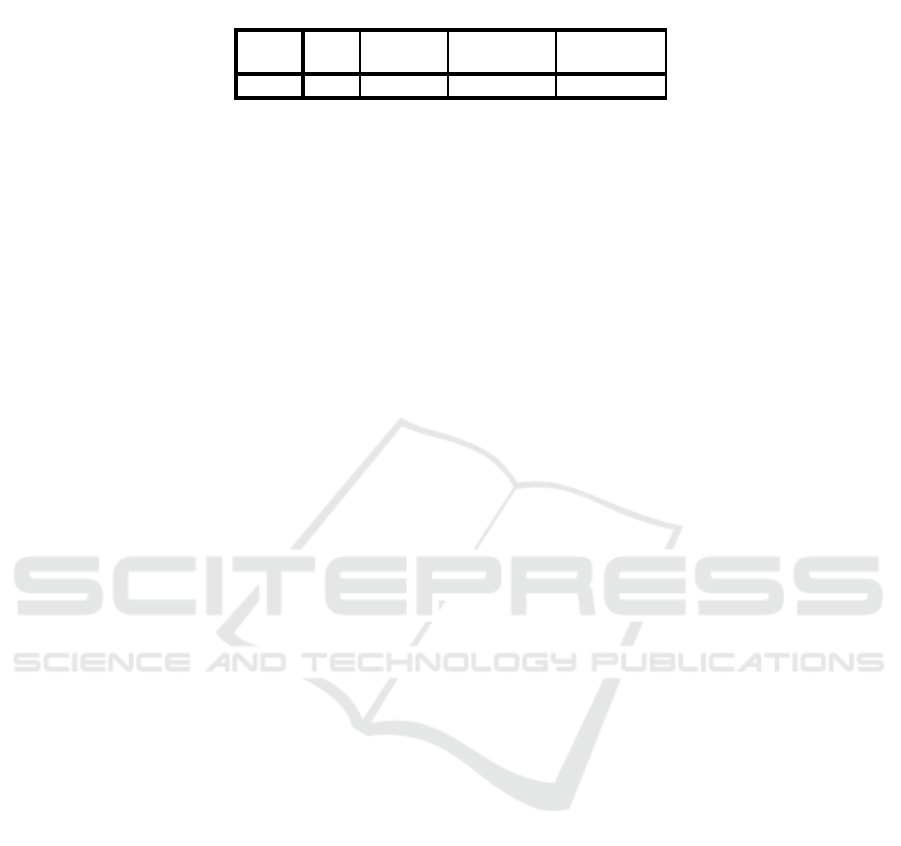

Table 3. Correlation and Determination Coefficients.

Model R R Square

Adjusted R

Square

Std. Error of

the Estimate

1 .397

a

.157 .136 .84754

Based on Table 3 above, it can be seen that the correlation coefficient is R of 0.379 or

39.7%. This finding shows that ROE, Managerial Ownership and DPR have a

relationship of 39.7% to PBV. Meanwhile, the correlation coefficient value, namely

Adjusted R Square in this study amounted to 0.136 or 13.6%. This finding shows that

ROE, Managerial Ownership and DPR are able to explain PBV by 13.6% while the

remaining 86.4% is explained by other factors not analyzed in this study.

Hypothesis Testing

Based on Table 3 Multiple Linear Regression Estimates, it can be seen that the ROE

count is 4.638 and the significance value is 0.000. The ttable value in this study which

is calculated with df = 124-4 at a significance level of 5% produces a number of

1.65765. Therefore, it can be concluded that t count (4.638)> t table (1.65765) and

significance value (0.000) <0.05, so H1 is accepted which means that profitability has

a positive and significant impact on the value of the Property Company on the BEI.

Multiple Linear Regression, It can be seen that the calculation of Management

Ownership is 1,294 and the significance value is 0,198. The t table value in this study

which is calculated with df = 124-4 at a significance level of 5% produces a number of

1.65765. Therefore, it can be concluded that tcount (1,294) <ttable (1,65765) and

significance value (0,198)> 0,05 then H2 is rejected which means managerial

ownership does not have a significant effect on the value of Property Companies on the

IDX. Whereas Multiple Linear Regression Estimates, it can be seen that the DPR count

is 2.135 and the significance value is 0.035. The ttable value in this study which is

calculated with df = 124-4 at a significance level of 5% produces a number of 1.65765.

Therefore, it can be concluded that tcount (2.135)> t table (1.65765) and significance

value (0.035) <0.05 then H3 is accepted which means that the dividend policy has a

positive and significant effect on the value of the Property Company on the IDX.

5 Conclusion

Based on testing the hypothesis that has been done in analyzing the effect of

profitability, managerial ownership and dividend policy on company value, it can be

concluded that ROE profitability proxies and dividend DPR policy proxies have a

positive and significant influence on the value of the company in the property

companies listed on the Exchange Indonesian securities. While managerial ownership

has a negative effect on the value of the company in property companies listed on the

Indonesia Stock Exchange. Profitability, managerial ownership and dividend policy

simultaneously have a significant effect on company value.

The Effect of Profitability, Managerial Ownership and Dividend Policy on Company Value on Property Companies Listed on the Indonesia

Stock Exchange

815

References

Arifin, S. 2014. Pengaruh Profitabilitas, Likuiditas, Growth Potential, dan Kepemilikan

Manajerial terhadap Kebijakan Dividen. Skripsi. Sekolah Tinggi Ilmu Ekonomi Indonesia

(STIESIA). Surabaya.

Anita dan Arief .(2016). Pengaruh kepemilikan manajemen dan kebijakan dividen terhadap nilai

perusahaan. Jurnal Manajemen.

Brigham dan Houston . (2010). Dasar-dasar manajemen keuangan, Buku satu. Edisi Kesepuluh,

Ahli Bahasa Ali Akbar Yuliyanto. Salemba Empat, Jakarta.

Brigham dan Houston. (2008). Manajemen keuangan. Edisi kedelapan. Penerbit Erlangga.

Jakarta.

Ghozali, Imam. (2011). Aplikasi Analisis Multivariate dengan program IBM SPSS 23.

Universitas Diponegoro, Semarang.

Halim, Abdul. (2015). Manajemen Keuangan Bisnis Konsep dan Aplikasinya Edisi 1. Mitra

Wacana Media, Jakarta.

Hanafi, A. Halim. (2008). Analisis Laporan Keuangan Edisi 1, Cetakan 3. UPPAMP-YKPN,

Yogyakarta.

Haruman, T. (2008). Pengaruh Struktur Kepemilikan Terhadap Keputusan Keuangan dan Nilai

Perusahaan (Survey pada Perusahaan Manufaktur PT. Bursa Efek Indonesia). Prosiding

Simposium Nasional Akuntansi XI. Pontianak.

Husnan, Suad.(2001). Dasar - Dasar Teori Portofolio dan Analisis Sekuritas. Unit Penerbit dan

Percetakan AMP YKPN, Yogyakarta.

Kasmir,2010, Pengantar manajemen keuangan,penerbit Kencana, Jakarta.

——(2014). Bank dan Lembaga Keuangan lainnya. PT Raja Grafindo Persada, Jakarta.

Moniaga, Fernandes. (2013). Struktur Modal, Profitabilitas dan Struktur Biaya Terhadap Nilai

Perusahaan Industri Keramik, Porcelen dan Kaca Periode 2007-2011. Jurnal EMBA. Vol 1.

No 4. Hal 433-442.

Sartono,A.2001. Manajemen keuangan teori dan aplikasi.Edisi Keempat.BPFE Yogyakarta.

Sugiyono. (2016). Metode Penelitian Bisnis. Cetakan 12. Alfabeta, Bandung.

www.bisnis.com. Diakses: 9 Agustus 2017

www.idx.co.id. Diakses: 6 Januari 2018.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

816