The Influence of Fraud Diamond, Gender, Ethical

Ideology on Cheating Behavior of Accounting Student

Fauziah Aidafitri, Fathia Zahara, and Indayani

Accounting Department Faculty of Economics and Business,

Syiah Kuala University, Aceh, Indonesia

indayani@unsyiah.ac.id

Abstract. The purpose of this study is to examine the influence of fraud diamond,

gender and ethical ideology towards cheating behaviour among accounting

students in the Accounting department, Syiah Kuala University. The

questionnaire was selected as the data collection used in this study. By using

simple random sampling technique, there were 210 questionnaires from

accounting students have been analyzed by using multivariate technique analysis-

SEM. Through SEM, the results of this study showed that the dimension of fraud

diamond, which is called as pressure, opportunity, capability have positively

significant influence towards cheating behaviour, and dimension rationalization

have no influence on cheating behaviour. Gender was found to have a significant

influence on cheating behaviour and have different tendencies between the male

group and female group toward the specific category in fraud diamond and ethical

ideology. Then, ethical ideology, idealism and relativism were found to have a

significant influence on cheating behaviour..

Keywords: Cheating behavior · Fraud diamond · Gender and ethical ideology

1 Introduction

The last few decades, recent research conducted by Galil, Yarmolovsky, Gidron and

Geva (2019) suggests that cheating behavior is one of the very serious problems that

are very common in the academic world and in everyday life. Perpetrators who commit

fraud can come from various backgrounds and different backgrounds. In Indonesia, the

results of a survey conducted by the Association of Certified Fraud Examiners (ACFE),

the most widespread cases of fraud in the workplace are corruption, amounting to 67%,

followed by abuse of state’s assets and companies by 31%, and fraudulent of financial

statements of 2%. This makes corruption become the most detrimental act of fraud in

Indonesia with the most fraud perpetrators having an educational background at the

undergraduate and master level. A survey conducted by ACFE Indonesia (2016) shows

that a high educational background does not guarantee a person not to commit fraud in

the workplace.

Reiss and Mitra (1998) state that the potential for cheating in the world of work in

the future, is also assessed by the actions of students, by measuring how tolerant they

are to cheating. Fraud is a major problem facing the world of education (Young, 2013).

The phenomenon of academic cheating among students is a common thing. Fraud can

Aidafitri, F., Zahara, F. and Indayani, .

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student.

DOI: 10.5220/0010524200002900

In Proceedings of the 20th Malaysia Indonesia International Conference on Economics, Management and Accounting (MIICEMA 2019), pages 651-672

ISBN: 978-989-758-582-1; ISSN: 2655-9064

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

651

be interpreted as a fraudulent act that involves more than one form of fraud, by misusing

the work of others as one's own work (Davy et al., 2007). According to Webster's

dictionary, academic dishonesty or academic cheating is defined as participation that is

done intentionally to cheat on the work or work of others (Faucher and Caves, 2009).

There are various factors that influence students in their actions to commit fraud.

Accounting students who will later run the accounting profession are expected to

uphold moral and ethical values so as to create graduates who are professional and able

to work in a global environment and have high competitiveness. This can be realized

by accounting students by rejecting all forms of fraud that occur at the university level.

Fraud diamond theory is a fraud theory which was originally known as the fraud

triangle theory which was developed by one of the originators of research on fraud namely

Cressey in 1950 cited in (Wells, 2010: 13). Cressey (1950) in Wells (2010: 13) listed three

factors that cause fraud, including pressure, opportunity, and rationalization. This theory

was later developed and expanded by Wolfe and Hermanson (2004) by considering the

fourth element, capability. Fraud is able to occur if the people involved have the right

skills and abilities to cheat. People who have these abilities will then see opportunities

and take advantage that is not only done once (Wolfe and Hermanson, 2004).

Gender is another factor identified as influencing fraud (Januarti and Eriskawati,

2016). The results of research on the effect of gender variables on cheating behavior in

accounting students are still diverse. Ballantine et al., (2014) in their research stated

that gender positively affects the level of academic cheating of accounting students in

Ireland. Male students tend to be more intolerant of academic cheating while women

show more tolerant results of academic cheating. Other research conducted by Januarti

and Eriskawati (2016) regarding the effect of gender on cheating at Diponegoro

University shows that gender does not influence the academic cheating behavior of

accounting students.

Research by Forsyth (1980) developed an instrument called the Ethical Position

Questionnaire (EPQ) or an ethical ideology that is used as an approach to take ethical

decisions and be a determinant in ethical judgment. Ethical decisions can occur in

situations experienced by someone when facing cheating behavior. A person's ethical

ideology occurs because of two factors namely idealism and relativism (Forsyth, 1980).

Relativism refers to the extent to which a person will reject moral rules universally and

the actions that affect one's ethical judgment depend on the circumstances of each

individual involved (Ismail, 2014). The second factor, idealism, is described as the

concern of the individual for the welfare of others. Idealist individuals assume that the

consequences will be accepted according to the action taken. Thus, idealistic

individuals will not choose negative actions that will cause harm to others (Ismail,

2014). A high level of idealism shows a tendency to reject acts of fraud, while high

levels of relativism indicate a high level of fraud as well.

Research on academic cheating behavior especially in accounting students has also

been carried out by previous researchers. Ismail and Hana (2016) examined the trends

of cheating behavior between accounting students at universities in Malaysia with

gender and the rationalization of justification for cheating behavior as an independent

variable. The results showed that male students showed a greater tendency in

justification to cheat than female students. Students who cheat on their exams also have

a greater tendency to justify their cheating actions.

Research on the prevention of academic cheating behavior in the context of other

accounting students was conducted by Ballantine et al., (2014) by measuring gender

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

652

and ethical ideology on the level of intolerance of academic fraud at universities in

Ireland. The results of the study revealed that the variables that had a significant positive

effect on tolerance for cheating behavior were gender and idealism. The variable

relativism is known to be unrelated to the intolerance of fraudulent behavior, this proves

that accounting students in Ireland tend to be idealistic compared to relative (Ballantine

et al., 2014).

The accountant profession is one of the groups that has a high contribution to the

economic welfare of the community (Saat et al., 2012). Public accountants are

responsible for verifying a recorded transaction, validating it and reporting it according

to standards (Saat et al., 2012). Therefore, accountants have an obligation to protect the

public interest, and ensure that public and private finances are well managed. Public

expectations have increased for the accounting profession. The accounting profession

is expected to have high moral values and actions and integrity (Saat et al., 2012).

Accounting students who will later run the accounting profession are expected to

uphold moral and ethical values so as to create graduates who are professional and able

to work in a global environment and have high competitiveness. This can be realized

by accounting students by rejecting all forms of fraud that occur at the university level.

This study aims to see the consistency of study results regarding the influence of

fraud diamond and ethical ideology on cheating behavior. This study also examined

differences between male and female students with respect to their attitudes on each of

the dimensions of cheating behavior. The object of this research is the accounting study

program students at Syiah Kuala University. An academic dishonesty behavior should

not be tolerated because it will have negative consequences and will damage the image

of educational institutions, especially in universities. For this reason, a test is needed to

evaluate the possibility of actions to prevent fraudulent behavior from occurring.

2 Literature Review and Hypotheses

2.1 Cheating Behaviour

Cheating Behaviour is a behavior that uses illegal methods to achieve a profit. In the

world of education, cheating behavior that occurs is referred to as academic cheating

(Farnese, 2011). Fraud is defined as behavior that involves some form of deception,

whereby a person's work is misunderstood as his own work (Davy et al., 2007).

According to Webster's dictionary academic cheating is defined as participation that

is done intentionally to cheat someone else's work (Faucher and Caves, 2009). The

definition of academic cheating according to Lewellyn and Rodriguez (2015) is

academic cheating covering all forms of cheating (for example plagiarism,

unauthorized assistance on assignments or examinations) and has increased a lot in

universities. Hendricks (2004) adds the definition of cheating behavior as actions such

as the use of copying notes during an exam, using unfair methods to study what is given

before the test, and copying from other students during the exam with or without the

owner's permission. Academic cheating becomes a more worrying problem when

students have entered the workforce (Davy et al., 2007; Aslam, 2011; Reiss and Mitra,

1998; Graves, 2008). This is a challenge both for educators and university institutions

to follow up the problem of fraud in the university environment. These challenges

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

653

become important especially for accounting students who are highly anticipated to

provide future professions with moral values and high integrity (Saat et al., 2012).

The act of cheating in a university environment can be in the form of activities such

as lectures in class, activities during exams, assignments given during lectures, the

relationship between lecturers and students, and the relationship between students and

academic activities (Hendricks, 2004). Cheating in the university environment in

general has been explicitly stated in the education law, so the problem of cheating has

legal force and is also contained in university academic regulations. The university has

in principle established that the academic environment is upheld on the basis of the

values of honesty, loyalty, responsibility, tolerance, etc. However, these values are not

always applied by students who study at the university.

2.2 Fraud Diamond

The development of fraud theory originally referred to a theory called fraud triangle

theory by Cressey (1950) cited in Wells (2010: 13). This theory explains fraud as a white-

collar crime which has three important conditions namely pressure, opportunity, and

rationalization. This theory shows that fraud is caused by one or more of these conditions.

However, the severity of fraud depends on the level of strength or weakness of the

condition (Thanasak, 2013). The fraud triangle theory was extended by Wolfe and

Hermanson (2004) who argued that the fraud triangle could be increased to be able to

prevent and detect fraud by considering the fourth element of fraud, namely capability.

Dorminey et al., (2012) stated that in addition to pressure, opportunity, and

rationalization, the theory of diamond fraud also saw the characteristics of each

individual who played a strong role in its influence on fraud. The fraud triangle theory

is expanded to become a fraud diamond with the aim that with the element of capability,

the occurrence of fraud can be controlled so that the fraud does not occur.

Wolfe and Hermanson (2004) add a capability factor by examining the evidence

which shows that fraud will not occur if the perpetrator does not have the capability.

Opportunities will open the initial door in committing fraud, while pressure and

rationalization will attract the perpetrators of fraud closer to the door, so that the

perpetrators of fraud must have the capability to recognize opportunities to be able to

walk through the door to commit fraud and then such acts of fraud it is hidden (Wolfe

and Hermanson, 2004).

2.3 Gender

Gender refers to differences in status, roles, functions and responsibilities between men

and women which are the result of social and cultural formation that is instilled through

the process of socialization from one generation to another (Puspitawati, 2013). Gender

is included in one of the demographic variables related to academic fraud (Donse and

Groep, 2013).

Dewi (2006) in her research stated that the concept of gender differs from gender.

Gender refers to biological differences between men and women. Concepts that explain

gender are caused by culturally determined views or social differences about the general

characteristics of men and women. The concept of gender originates from human

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

654

thought which is then formed in a dynamic community environment due to various

factors such as differences in religion, ethnicity, race, and certain customs.

There are two theories used to explain the effect of gender on cheating behavior,

namely the theory of differentiation socialization and structural theory (Ballantine et

al., 2014). Gender socialization theory holds that both men and women will carry

different values that originate from their environment. In this theory women will be

more likely to be socialized to follow the rules so that the possibility of women in

committing academic cheating is found to be less. But on the other hand, the structural

theory of the difference in values between men and women over time will be equal

because both of them undergo the same education, so that ethical behavior will be the

same between the two (Ballantine et al., 2014). Structural theory will build the same

attitudes and behaviors in terms of addressing matters relating to ethical and moral

values in the same environment.

2.4 Ethical Ideology

Ethical ideology is defined as a person's approach to ethical decision making and is

considered a determinant of ethical behavior in making decisions (Forsyth, 1980).

Forsyth (1980) states that a person's ethical judgment when making a decision consists

of two scales, namely idealism and relativism. Relativism measures the extent to which

a person will reject moral rules and they assume moral actions depend on the situation

and each individual involved when they will make ethical judgments (Ismail, 2014).

The attitude of relativism will reject ethical values in directing ethical behavior in which

people who have a relative nature will reject the principles of universal moral rules.

The second factor is idealism which illustrates the individual's concern for the welfare

of others, which assumes that there are consequences in every action taken so that they

will not choose to commit a crime that will cause bad consequences for others (Ismail,

2014). An idealistic behavior will make individuals continue to demand moral

principles that do not violate ethics, because an idealist will assume every action will

have its own impact which will have a good effect if what they do does not violate

moral rules. Forsyth (1980) states that the concepts of idealism and relativism have two

opposing concepts and the scale used is separate. The category of scale can be

categorized into four types of ethical ideology, namely situationism (where the level of

relativism and idealism is high), subjectivism (where the level of relativism is high,

whereas the idealism is low), absolutism (where the level of idealism is low and

relativism is low), and expressionism (where the level of relativism is high, while the

idealism is low), absolutism (where the level of idealism is low and relativism is low),

and expressionism (where the level of idealism and low relativism).

2.5 Hypotheses Development

Fraud Diamond variable contains four underlying elements, namely pressure,

opportunity, rationalization and capability, have shown different results and effects in

relation to fraud behavior based on the results of previous studies. Research according

to Mc Cabe (2004) shown that pressure is the greatest influence to be involved in

various forms of academic cheating. This is also in line with what was done by

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

655

Murdiansyah et al., (2017); Finn and Frone (2010); and Hendricks (2004) who proved

that pressure influences cheating behavior. Factors that make the most pressure to cause

academic cheating according to Hendricks (2004) are value competition (35%),

insufficient study time (33%) and heavy workload (26%). The opportunity variable

shows the same results as the research conducted by Murdiansyah et al., (2017) and

Deliana et al., (2017) where the results of the study prove that the opportunity has a

positive effect on student academic cheating behavior. The variable rationalization also

found the same results with research by Murdiansyah et al., (2017) and Ismail and Hana

(2016) which shown that rationalization affects the student behavior of academic

cheating. Then, for the last variable namely capability in the study Murdiansyah et al.,

(2017) proved that the capability has a negative effect on student academic cheating.

H1a. The higher a pressure, the higher the cheating behavior occurs to students.

H1b. The higher an opportunity, the higher the cheating behavior occurs to

students.

H1c. The higher a rationalization, the higher the cheating behavior occurs to

students.

H1d. The higher a capability, the higher the cheating behavior occurs to students.

Gender shows varied research results on its relationship with academic cheating

behavior (Kobayashi and Fukushima, 2012). Cheating behavior is more common in

male students than in women (Hendricks, 2004). This, according to Hendricks (2004),

is due to the theory of gender role socialization, which says women are socialized to

comply with regulations, while men tend to be less attached to socialization theory,

although it does not deny that women do not commit fraud if they have the opportunity.

According to Kidwell and Kent (2008) who examined cheating behavior among

Australian students studying on campus and through distance learning found that

gender significantly affected cheating behavior. It is the same as research by Ballantine

et al., (2014) which states that gender is significantly related to ethical decisions and

male students are known to be more involved in cheating than women. Different

research results were obtained in Januarti and Eriskawati (2016) who found that there

was no relationship between gender and academic cheating. The relationship between

gender variables and academic cheating was found not so strong, but most studies tend

to conclude that men will be more vulnerable to cheating (Donse and Groep, 2013).

H2. There is a difference between the influence of male and female students in

relation to cheating behavior.

The results of ethical ideology research namely idealism conducted by Ballentine et

al., (2014) and Ismail (2014) stated that idealism is positively related and significantly

related to ethical judgment. This was also proved by Aziz and Cahyonowati (2015) who

stated that idealism positively influenced the ethical judgments of students. Another

idealism study was conducted by Januarti and Eriskawati (2016), who stated that

idealism, had a positive effect on student intolerance of cheating behavior. The research

has also shown that high levels of idealism in individuals will also make a person's

ability to conduct high ethical judgment. The attitude of idealism that exists in

accounting students can make a positive contribution to the improvement of ethics in

the classroom and continue in the workplace (Ballantine et al., 2014). The level of

idealism that is in a person will be clearer in recognizing if

there are moral issues related

to ethics (Januarti and Eriskawati, 2016).

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

656

Research related to ethical ideology that measured relativism conducted by Aziz

and Cahyonowati (2015) shown that relativism has a negative effect on student ethical

judgment, so that someone who has a low level of relativism will have a high ability to

conduct ethical judgments. There is also a research conducted by Januarti and

Eriskawati (2016) which stated that relativism influences student cheating behavior,

which contradicted with a research done by Ballantine et al., (2014) who found that

cheating behavior was not significantly influenced by relativism.

H3a. The higher the attitude of Idealism, the lower the tolerance level of student

cheating behavior.

H3b. The higher the attitude of relativism, the higher the tolerance level of

students cheating behavior.

3 Research Method

3.1 Research Design

The purpose of this study was to test the hypothesis or the hypothesis testing. A

hypothesis test is used to test the effect of fraud diamond, gender, and ethical ideology

as independent variables on cheating behavior as the dependent variable.

3.2 Research Population and Samples

Population used in this research is active students of accounting bachelor degree batch

2014, 2015, 2016, and 2017. The sampling technique used in this study was simple

random sampling, Sekaran and Bougie (2010:270) defined it as a sampling technique

that each element of the population has the same probability to be chosen as the

samples.

Table 1. Number of Population.

No Batch Male Female Total

1 2014 46 79 125

2 2015 35 65 100

3 2016 23 57 80

4 2017 39 53 92

Total 143 254 397

Source: Unsyiah Data Portal, 2018

According to Hair, et al. (2018), the general guidelines for minimum sample size in

SEM analysis is 10 times by the maximum number of arrows (paths) that affect a latent

variable (10 time rule of thumb) that is 6 lanes 10 times as many as 60 samples.

However, to provide statistical power, the sample size exceeds these conditions using

the Slovin formula. The total number of Accounting students used as a population is

397, and the error rate is 5%, the number of samples is calculated using the Slovin

formula.

𝒏=

𝑵

𝟏+𝑵𝒆

𝟐

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

657

Whereas:

n : Sample size

N : The number of populations

e : Rentang toleransi kekeliruan yang dapat diterima

𝒏=

𝟑𝟗𝟕

𝟏 + 𝟑𝟗𝟕. 𝟓%

𝟐

= 𝟏𝟗𝟗. 𝟐𝟒

Therefore, the minimum sample size used in this study is 200 students.

3.3 Data Sources and Collection Method

Sources of data in this study are primary data and secondary data. The primary data

used in this study was through a questionnaire. The questionnaire will be distributed

directly to respondents, which are undergraduate accounting students, from 2017, 2016,

2015 and 2014 classes. The questionnaire has been structured and containing closed

statements relating to the tested variables. Secondary data are descriptions made by

others and written by someone who is not involved in the research being carried out. A

dimension and indicator measurements in this study used is a Likert scale.

Questionnaires regarding cheating behaviour developed in according to the research

questionnaire of Hendricks (2004). The fraud diamond study of accounting student

cheating behaviour adapted a questionnaire developed by Noor et al., (2014), whereas

to assess ethical ideology, which is idealism and relativism, this study used the Ethics

Position Questionnaire developed by Forsyth (1980).

3.4 Variable and the Variable Operationalization Definition

3.4.1 Cheating Behaviour

Cheating behaviour is a dishonest act taken by someone in achieving a goal. Some

indicators used are copying other people's assignments, plagiarism of other people's

sources, doing assignments and tests according to ability, looking at notes/other sources

during the exam, working with friends, and refusing to give answers to others.

3.4.2 Fraud Diamond

Fraud diamond is a theory of fraud consisting of 4 dimensions, namely pressure,

opportunity, rationalization, and capability. Pressure variable indicators include

wanting high scores and ratings, avoiding failure, high competition, and dissatisfaction

with the results achieved. Indicators of opportunity using indicators include weak

supervision, inaccurate assessment, absence of strict penalties and rules, and

indifference of lecturer/supervisors. Variation of rationalization (rationalization) uses

indicators that are cheating is often done, the perpetrators commit fraud when in a state

of urgency, no party is harmed, and there is a difference between students. Capability

indicators use indicators that are the utilization of internal control weaknesses, high

self-confidence, and opportunities to influence others to cheat.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

658

3.4.3 Gender

Gender refers to the different statuses, roles, functions and responsibilities between men

and women which are the result of social and cultural formation that is embedded

through the process of socialization from one generation to another (Puspitawati, 2013).

3.4.4 Ethical Ideology

Idealism is the attitude that exists in individuals who will act according to what feels

right and the action is in accordance with the ethics that exist in society and will not

interfere with others. Idealism will address one's behaviour as an action that will not

violate ethical values. Indicator of idealism by using condition items developed by

Forsyth (1980). Relativism is a person's attitude in believing that ethical rules are

judged as not universal due to different cultures and have different rules. Therefore,

action is influenced by the point of view of a developing society and culture. A relative

individual will tend to reject moral principles and choose to follow what he considers

to be right. Indicators of relativism use condition items developed by Forsyth (1980).

3.5 Data Processing and Analysis Methods

The research data that has been obtained will then be tested and analyzed quantitatively

using a multivariate technique or called the Structural Equation Model (SEM). In SEM,

there are five stages in which each stage will be very influential with the next stage.

The stages in analyzing using SEM are:

1) Model Specification

In the process of modelling using SEM analysis techniques, the development of model

specifications is the first step to planning a design so that it can answer the research

objectives. The basis in building model specifications will become a framework for

thinking so that it will result in the development of an appropriate structural model

(Latan, 2013). In an analysis using SEM, the thing that concerns are the latent variable.

Latent variables are abstracts that cannot be directly measured (Unobserved variables),

making them require indicators or manifest variables to form latent constructs. These

visible indicators or variables are described as questions measured on a Likert scale.

The structural equation model (SEM) will also input the measurement error in

modelling (error term) associated with the factor in each measurement. The structural

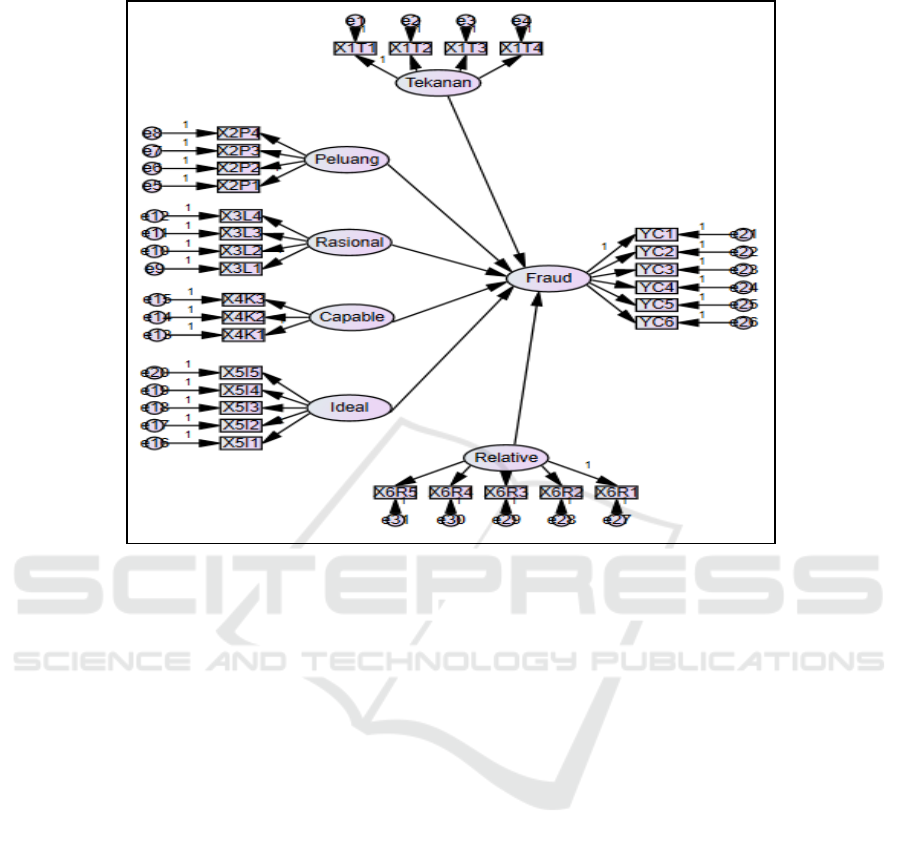

model contained in this study is as follows.

2) Model Identification

Identification of the model in the structural equation model (SEM) is a crucial thing to

do to see whether a model that has been built in accordance with the empirical data

obtained has good value so that later the model can be estimated. If a model contained

in SEM analysis has a wrong value, then the model cannot be estimated for the next

stage of Latan (2013: 43).

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

659

Fig. 1. Research Model.

3) Model Estimation

After the model specification and identification stages, the next stage is the model

estimation. In the estimation model, the estimation method must be determined first.

This study uses the Maximum Likelihod estimation method developed by Lawley in

1940. In the Maximum Likelihod method will produce the best parameter estimation

(unbiased) if the data used has met the Multivariate Normality assumption. Maximum

Likelihod also requires if a model specification is valid and the data used uses a

continuous-interval scale.

4) Model Evaluation

Model evaluation is used to evaluate a model using Confirmatory Factor Analysis. The

CFA is also tasked with testing the validity and reliability of latent constructs. Validity

test aims to see the validity of the statements contained in the research and see the level

of ability of an instrument to answer questions in latent constructs. In order to measure

the validity of a construct, it can be seen from the value of the loading factor where the

standardized loading estimate must exceed 0.50 or ideally 0.70. The reliability test aims

to determine the accuracy of the level of the measuring instrument used, and

measurement is said to be reliable if the measurement results have shown consistent

results even though it has been done for the same subject.

After testing has been carried out using CFA analysis, the next stage of the structural

model evaluation is knowing the significance of the P-Value, R-Square values and

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

660

evaluating the Overall Fit Model or Goodness of Fit Model bypassing the fit model

size:

a) Chi-Square

A model can be considered as a fit model if the Probability (P) > 0.05 or the Chi-

Square < Chi-Square table according to the degrees of freedom which has no

distinction between the previously observed covariance matrix input and the

predicted model (Latan 2013:50).

b) Goodness of Fit Indices (GFI)

GFI has a range of value 0-1. The higher the value, the better the specification

model. The suggested standards of GFI as the fit model is > 0.90 or > 0.95

(Latan,2013:53).

c) Root Mean Square Error of Approximation (RMSEA)

The value of RMSEA ≤ 0.05 shows an outstanding fit model. RMSEA of ≤ 0.06

– 0.08 shows an average well, and the RMSEA > 1.00 shows that the model

needed to be fixed (Latan,2013:54).

d) Expected Cross-Validation Index (ECVI)

A value of ECVI is used to evaluate the comparison between models. If the value

shown is smaller, then the model is better. In a single model, the ECVI value

which the model is close to the EVCI saturated value shows a good fit.

e) Normed Fix Index (NFI)

NFI range value is from 0-1; if the value gathered is higher, then the model is

better. NFI that shows > 0.90 is a very good fit, if between 0.80 < NFI< 0.90 is

a good fit.

f) Comparative Fit Index (CFI)

CFI range value is from 0-1, which if the value gathered is higher, then the result

is better. CFI value > 0.90 is a very good fit, while 0.80 < CFI < 0.90 is a good

fit.

g) Incremental Fit Index (IFI)

IFI range value is from 0-1, which if the value gathered is higher, then the result

is better. IFI value > 0.90 is a very good fit, while 0.80 < IFI < 0.90 is a good fit.

h) Relative Fit Index (RFI)

RFI range value is from 0-1, which if the value gathered is higher, then the result

is better. RFI value > 0.90 is a very good fit, while 0.80 < RFI < 0.90 is a good fit.

i) Adjust Goodness of Fit (AGFI)

Recommended value of AGFI is excellent if the result gathered is ≥ 0.90. If

AGFI shows 0.80 < AGFI < 0.90 is a good fit.

5) Model Modification

Model Modification conducted after model evaluation and tested the goodness of fit

estimation comprehensively, however in the process if the result shows that the model

is not a fit model, then modification or re-specification model is needed. A model that

is stated as a fit model recognized that it is accurate or correct.

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

661

4 Results and Discussion

4.1 SEM Assumption Test

4.1.1 Confirmatory Factor Analysis Full Mode

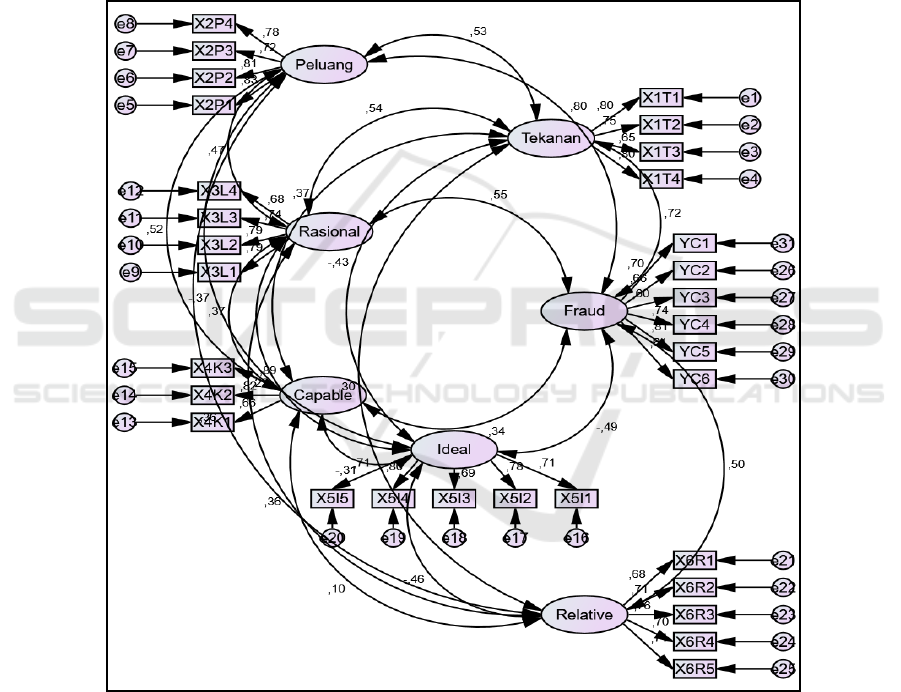

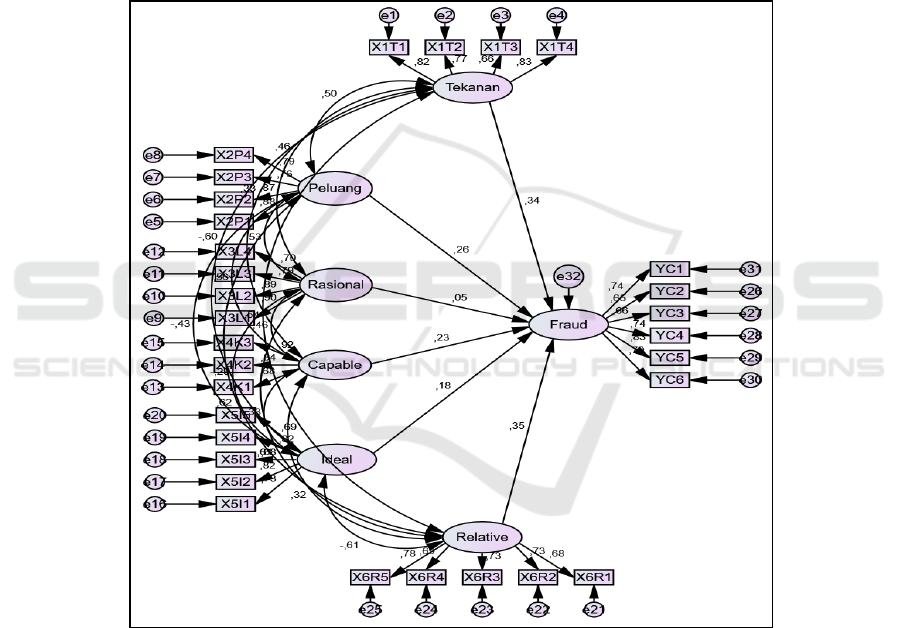

The CFA of all variable in the form of a full model can be seen in Figure 2. Based on

the research model, the gathered data then inputted and collected to be tested, in order

to see whether the assumption is fulfilled. The result of the data input process from each

tested variable is in Table 2.

Fig. 2. Result of CFA Test.

From the output of Table 2 know that the loading factor value for all indicators has

fulfilled the specified conditions, where the loading factor for each indicator is ≥ 0.50

so that the conclusion can be drawn that all constructing indicators tested are valid. This

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

662

is also the case with the construct reliability value of ≥ 0.70 which states that all

constructs meet the requirements and the instrument is declared reliable.

Table 2. Validity and Reliability Test Result.

Construct Dimension Indicator

Loading

Factor

Description

Construct

Reliability

Description

Fraud

Diamond

Pressure X1T1 0,804 Vali

d

0,842 Reliable

X1T2 0,753 Vali

d

X1T3 0,648 Vali

d

X1T4 0,802 Vali

d

Opportunity X2P1 0,826 Vali

d

0,840 Reliable

X2P2 0,812 Vali

d

X2P3 0,722 Vali

d

X2P4 0,781 Vali

d

Rationalistic X3L1 0,792 Vali

d

0,861 Reliable

X3L2 0,788 Vali

d

X3L3 0,738 Vali

d

X3L4 0,681 Vali

d

Capability

X4K1 0,661 Vali

d

0,834 Reliable

X4K2 0,821 Vali

d

X4K3 0,893 Vali

d

Ethical

Ideology

Idealism X5I1 0,714 Vali

d

0,823 Reliable

X5I2 0,782 Vali

d

X5I3 0,693 Vali

d

X5I4 0,799 Vali

d

X5I5 0,707 Vali

d

Relativism X6R1 0,683 Vali

d

0,856 Reliable

X6R2 0,707 Vali

d

X6R3 0,760 Vali

d

X6R4 0,703 Vali

d

X6R5 0,708 Vali

d

Cheating

Behaviour

Cheating in

Individual

Assignments

Y1C1 0,656 Vali

d

0,833 Reliable

Y1C2 0,596 Valid

Cheating in

Group

Assi

g

nments

Y1C3 0,740 Vali

d

Y1C4 0,808 Valid

Cheating in

Exa

m

Y1C5 0,607 Vali

d

Y1C6 0,698 Vali

d

Sumber: Data processed, 2019

4.1.2 Analysis of Structural Equation Model (SEM)

After analyzing the whole model with CFA analysis, which tests the dimensions of each

of the indicators as forming latent variables, the next step is to analyze data processing

at the full SEM model stage which is carried out by carrying out the suitability test and

statistical test. The results of data processing for the full SEM model analysis are shown

in Figure 3.

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

663

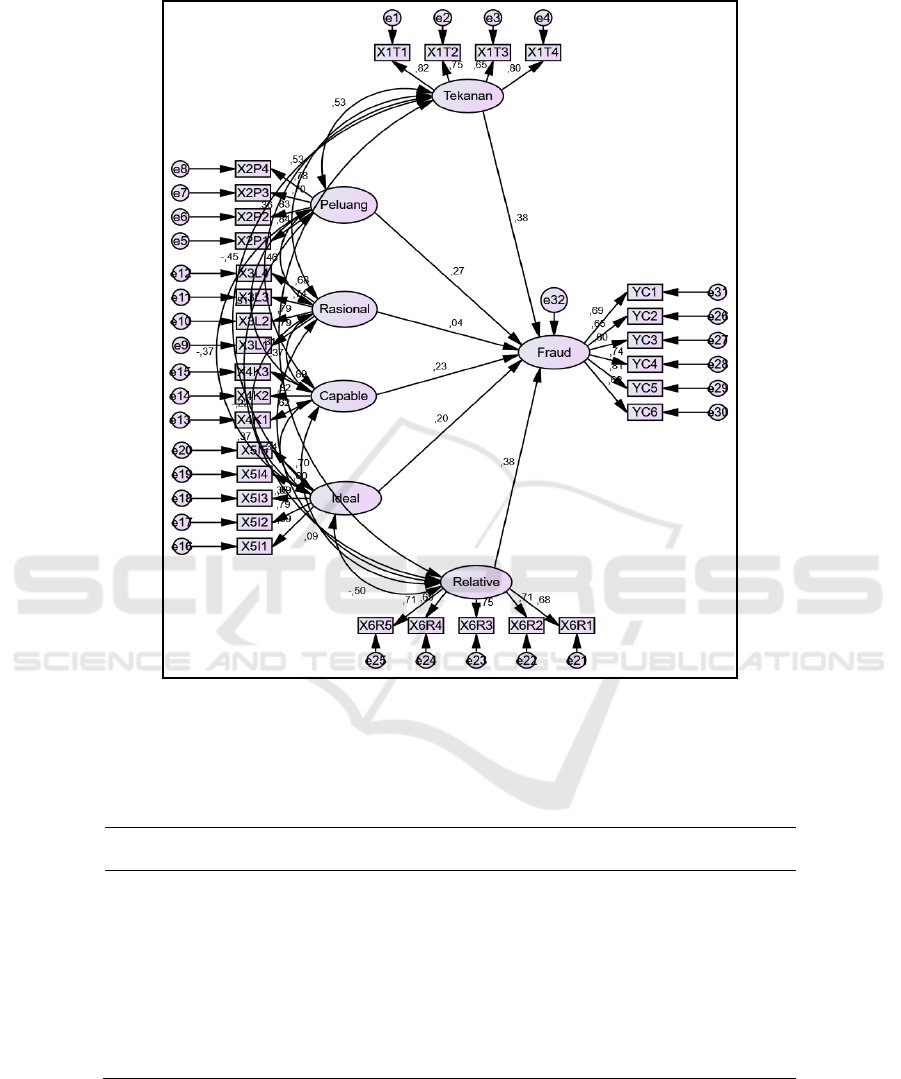

Fig. 3. SEM Full Model.

From the test results using SEM analysis, the model obtained an estimate of the

Goodness of Fit research model where the results can be summarized in the table below.

Table 3. The Goodnes of Fit (GOF) Test.

GOF Cut-Off Absolute Fit

M

easures

Estimation

Result

Description

Chi-S

q

uare < X

2

825,247 Less Goo

d

RMSEA ≤0,08 <0,05 0,069 Good Fit

PNFI ≥0,90 0,60-0,90 0,695 Good Fit

NFI ≥0,90 0,80<NFI<0,90 0,783 Less Goo

d

CFI ≥0,90 0,80<CFI<0,90 0,877 Less Goo

d

IFI ≥0,90 0,80<IFI<0,90 0,878 Good Fit

RFI ≥0,90 0,80<RFI<0,90 0,756 Less Goo

d

GFI ≥0,90 0,80<GFI<0,90 0,806 Good Fit

TLI ≥0,90 0,80<TLI<0,90 0,861 Good fit

AGFI ≥0,90 0,80<AGFI<0,90 0,768 Less Goo

d

Sumber: Data processed, 2019

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

664

Chi-square is very sensitive to sample size, therefore, to get a fit model, an analysis

can be seen from other goodness of fit measures. The value gathered from the analysis

shows that the chi-square value of 825,247 with an opportunity of 0,000 shows that the

model is less fit, but from the other goodness of fit measures, it shows that some get

good fit values, which are RMSEA, PNFI, IFI, TLI and GFI then from that, it can be

said that the model proposed in this study is acceptable.

4.2 Hypothesis Testing

After all the assumptions are met, then the hypothesis that has been prepared previously

is tested. Hypothesis testing is done based on the value of the critical ratio (CR) of the

relationship of a causality test results conducted by SEM.

Table 4. Hypothesis Test Result.

Estimate

Standard

Erro

r

Critical

Ratio

Probability

Erro

r

Standardize

Esimate

Description

Frau

d

Opportunit

y

0,170 0,42 4,056 0,000 0,269 Significant

Frau

d

Pressure 0,233 0,41 5,921 0,000 0,379 Si

g

nificant

Fraud

Rationality 0,026 0,046 0,556 0,578 0,043

Not

Significant

Significant

Frau

d

Ca

p

abilit

y

0,231 0,039 5,919 0,000 0,226 Si

g

nificant

Frau

d

Idealis

m

0,171 0,043 4,057 0,000 0,198 Significant

Frau

d

Relativis

m

0,275 0,054 5,047 0,000 0,384 Si

g

nificant

Sumber: Data processed, 2019

Table 4 shows that all CR values obtained are above 1.96 and a probability of 0,000,

except for the rationalization dimension. Therefore, from the estimation results of the

structural model, it is stated that all hypotheses can be accepted, except for the

dimensions of rationality in the diamond fraud construct, which hypotheses are rejected

because the probability error value is > 0.05. The results of testing the hypothesis test

also found that in the diamond fraud construct which is the dimensions, pressure,

opportunities, and capabilities significantly influence cheating in a positive direction,

which increases the pressure, opportunity and capability in a person will also increase

the level of fraud in its environment. In the construct of ethical ideology, it is known

that the dimensions of idealism and relativism are equally influential on student

cheating behaviour in a positive direction, which if high levels of idealism and

relativism will also increase cheating behaviour. In contrast to the dimensions of

rationality, found that there is no significant effect between the level of rationalization

with the behaviour of fraud that occurs.

4.2.1 The Effect of Fraud Diamond on the Cheating Behaviour of Accounting

Students

The result of SEM analysis illustrated that the dimension of pressure significantly

influences to the student’s cheating behaviour which is 37.9% with positive direction,

which means that the higher pressure of the students will make the cheating behaviour

more likely to have by them. This result is in line with the research by Murdiansyah et

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

665

al., (2017), Finn and Frone (2010), and Hendricks (2004) that prove that pressure

influence cheating behaviour.

On the dimension of opportunity, the estimation result shows the value of 26.9%

which means that the opportunity influences the cheating behaviour on students as

26.9% with positive direction. It illustrates that the greater opportunity that the students

have, the greater opportunity of cheating activity will be conducted by students. This

result also proved by the research conducted by Murdiansyah et al., (2017) and Deliana

et al., (2017).

The result also shows that there is no significant influence of rationality dimension

on the cheating behaviour, which means that the hypothesis is rejected. The collected

data could not prove the level of rationality has a relationship with the cheating

behaviour of students.

In addition, the result of the capability dimension shows that the capability level of

a person influences the cheating behaviour on students as 22.6%, with a positive

direction. It shows that the higher capability tends to lead the cheating behaviour a

person has. This result is contrary to the research of Murdiansyah et al. (2017) which

resulted that a capability will negatively influence cheating behaviour.

4.2.2 The Effect of Ethical Ideology on Cheating Behaviour of Accounting

Students

The output of estimation value by using SEM analysis shows that ethical ideology

construct which consists of idealism and relativism influence cheating behaviour of

accounting students. The dimension of idealism affects 19.8% of the cheating

behaviour in a positive direction. Research on the dimension of idealism also conducted

by Ballentine et al., (2014) and Ismail and Hana (2014) which resulted that idealism

positively affects students’ behaviour. For the result of the dimension of relativism

shows that it influences cheating behaviour as 38.4%, which means that the higher

relativism level will lead to more cheating behaviour is done. This is in line with the

research of Aziz and Cahyonowati (2015) and Januarti and Eriskawati (2016) who

stated that relativism influences cheating behaviour.

4.3 SEM Analysis in Gender

The hypothesis testing of the relationship of gender on student cheating behaviour, a

test was conducted to be able to see how the tendencies of each gender group with the

help of SEM analysis method to see the differences between male and female groups

in relation to student cheating behaviour.

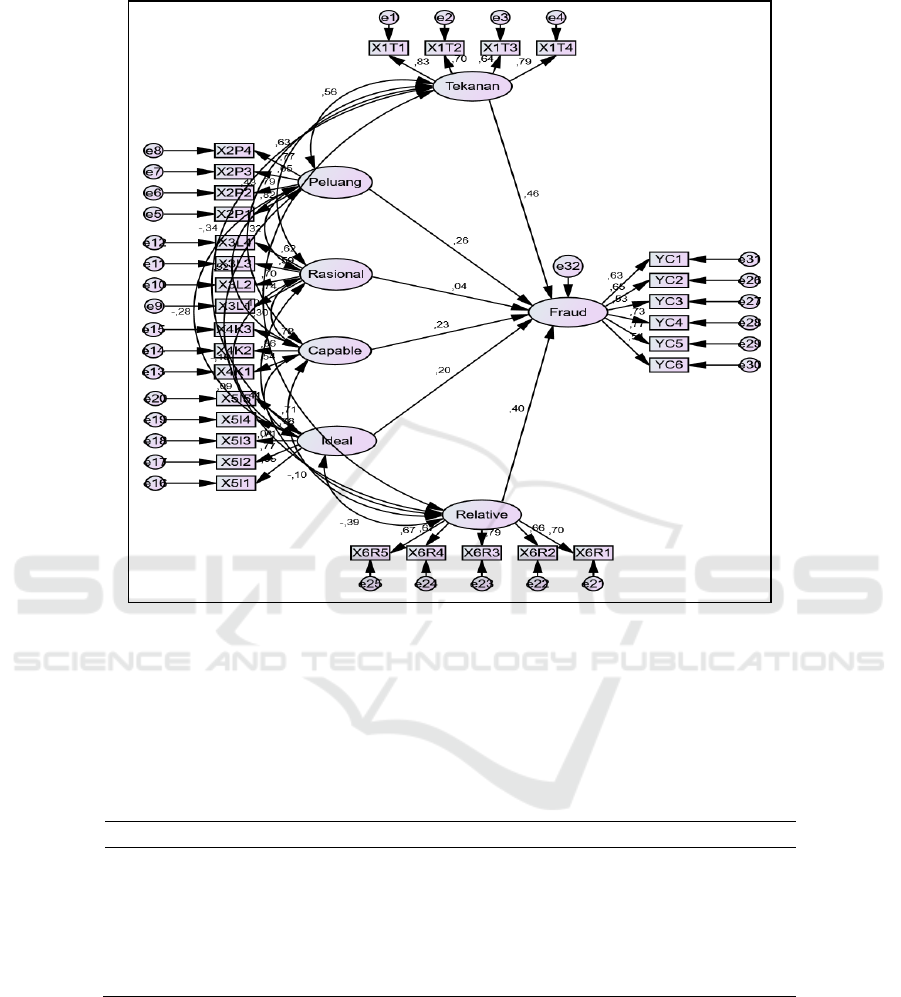

4.3.1 Relationship of Male Group to Cheating Behaviour

SEM analysis is used to help see how the group responds to statement indicators about

fraud and see how the estimated value of the results obtained and the effect of each

variable to be tested. The structural model of the SEM analysis of the gender group of

male students can be seen in Figure 4.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

666

Fig. 4. Structural Model Test of Male Group.

The output results from the data that have been inputted in the Amos program; it

was found that the loading factor of each indicator ≥0.50 indicates that the indicator is

valid. Then the results of the output are then analyzed by looking at the relationship of

male gender groups with the construct being tested. Table 5 shows the relationship of

male gender groups to the constructs contained in the study.

Table 5. Analysis Result of Male Group Structural Equation.

Estimate S.E. C.R. P Standardized Estimate

Fraud <--- Opportunity ,266 ,063 4,242 *** 0,496

Fraud <--- Pressure ,262 ,069 3,811 *** 0,530

Fraud <--- Rationality ,016 ,062 ,256 ,798 0,025

Fraud <--- Capability -,195 ,083 -2,356 ,018 -0,250

Fraud <--- Idealism -,111 ,061 -1,834 ,067 -0,168

Fraud <--- Relativism ,097 ,053 1,842 ,066 0,156

Sumber: Data processed, 2019

Table 5 shows that for the male group, fraud diamond construct that is the pressure

dimension has an effect of 49.6% in relation to fraud behaviour, the opportunity

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

667

dimension has an effect of 53% with cheating behaviour, the rationality dimension has

no effect, and the capability dimension negative effect on cheating behaviour by 25%.

In the construct of ethical ideology, idealism has a negative effect of 16.8% in relation

to cheating behaviour, and the dimension of relativism affects cheating behaviour by

15.6% in a positive direction.

4.3.2 Relationship of Female Groups to Cheating Behaviour

SEM analysis is performed to see how the response of the female group to the indicators

of the construct being tested, and to get how the estimated value of the effect of each

variable to be tested. The structural model of the SEM analysis of the gender group of

the female can be seen in Figure 5.

Fig. 5. Struktural Model Test of Female Group.

The output of the female group for each question indicator was found that the

loading factor of each indicator was 50.50, so it showed that the indicator was valid.

Then next, the results are analyzed by looking at the level of influence of each construct

being tested. Table 6 shows the relationship of female groups to the construct contained

in the study.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

668

Table 6. Analysis Result of Female Structural Equation.

Estimate S.E. C.R. P Standardized Estimate

Frau

d

<--- O

pp

ortunit

y

,208 ,066 3,151 ,002 0,293

Frau

d

<--- Pressure ,249 ,062 3,988 *** 0,327

Frau

d

<--- Rationalit

y

,018 ,060 ,299 ,765 0,032

Frau

d

<--- Capabilit

y

,249 ,062 3,988 *** 0,223

Frau

d

<--- Idealis

m

,208 ,066 3,151 ,002 0,210

Frau

d

<--- Relativis

m

,288 ,091 3,172 ,002 0,384

Sumber: Data processed, 2019

The results obtained from the testing of the female group from the diamond fraud

construct are the opportunity dimension influences on cheating behaviour by 32.7%,

the pressure dimension influences the cheating behaviour with a percentage of 32.7%,

the rationality dimension is found to have no effect on the cheating behaviour from the

results estimate that has a value <0.05, the capability dimension is known to have an

effect of 22.3%. For the construct of ethical ideology, the idealism dimension is known

to have a 21% effect on cheating behaviour, while the relativism dimension has a 38.4%

effect on student cheating behaviour.

4.4 Independent Sample T-Test Group Gender Male and Female

After each gender group has been analyzed, to see whether there are differences

between male and female gender groups in relation to cheating behaviour can be seen

in table 7.

Table 7. Structural Weight Group Independent Sample T-Test.

Model DF CMIN P NFI

Delta-1

IFI

Delta-2

RFI

rho-1

TLI

rho2

Structural covariances 21 50,376 ,000 ,011 ,013 ,002 ,003

Structural residuals 22 51,027 ,000 ,011 ,013 ,002 ,002

Measurement residuals 53 118,986 ,000 ,025 ,031 ,003 ,004

Sumber: Data processed, 2019

Table 7 shows that the P-value on structural covariances <0.05 shows that there are

significant differences between groups of men and women in this full model. The

difference in gender sensitivity to each construct is shown in table 8.

Table 8. Construct Sensitivity According to Gender.

DV

IV Male Female Plus-Male Plus-Female

Fraud <---

Opportunit

y

0.496 0.293 0.203 -

Frau

d

<--- Pressure 0.53 0.327 0.203 -

Frau

d

<--- Rationalit

y

0.025 0.032 - 0.007

Frau

d

<--- Capabilit

y

-0.25 0.223 - 0.473

Frau

d

<--- Idealis

m

0.168 0.21 - 0.042

Frau

d

<--- Relativis

m

0.156 0.384 - 0.228

Sumber: Data processed, 2019

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

669

The result obtained from Table 8 explains that the influence of opportunity and

pressure on cheating behaviour, the male gender group is known to have greater

responsiveness than female because it has a greater Beta value than female. However,

for the variable rationalization, capability, idealism and relativism of the female group

were more responsive than the male group.

5 Conclusions, Implications, and Limitations of Research

5.1 Conclusions

The results showed that the variables that significantly influenced accounting student

cheating behaviour were pressure, opportunity, capability, idealism and relativism,

while the rationality variable was known not to have a significant effect on student

cheating behaviour.

When reviewed the relationship to the influence of each dimension, the dimension

of pressure has a significant effect on student cheating behaviour, where the influence

of pressure on cheating is 37.9% in a positive direction which when high pressure in

students will increase cheating behaviour. In the Opportunity dimension, the estimation

results show a value of 26.9%, where it states that the opportunities that influence

student cheating behaviour are 26.9% in a positive direction. This shows that the greater

the opportunities, the greater the fraudulent activity. The dimension of rationalization

has no influence and is not significant on cheating behaviour. The capability dimension

shows that the level of ability possessed by someone will influence the cheating

behaviour of students by 22.6% in a positive direction. This shows that the higher one's

ability will increase the tendency to cheat. The idealism dimension influences 19.8%

of cheating behaviour in a positive direction. In the dimension of relativism, the value

that affects a person's relative level of cheating behaviour is 38.4%, where the higher

the level of relativism in one's eating will further increase the cheating behaviour that

occurs.

In terms of the different gender groups, there are differences in the influence

between men and women on their actions of cheating. On the dimensions of opportunity

and pressure, the influence of cheating behaviour on male gender groups was found to

be more responsive than women, but for the variables of rationalization, capability,

idealism and relativism, the female group turned out to be more responsive than the

male group.

5.2 Implications

This research is expected to be beneficial for educational institutions or institutions,

especially universities, to pay more attention to the issue of fraud in the university

environment, so that prevention is obtained and reduce the problem of fraud in the

university environment, especially in accounting study programs so that it will create

quality graduates and respect moral values.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

670

5.3 Limitations

The limitations of this study are that the sample is limited to accounting students who

study at Syiah Kuala University only and in gathering research conclusions based only

on primary data collected through questionnaires, so that it can cause misperceptions

of respondents in answering questionnaire statements that may differ from actual

conditions which are a condition which cannot be controlled because it is beyond the

ability of the researcher.

References

ACFE Indonesia. (2016). Suvey Fraud Indonesia.

Aslam, M. S. (2011). The Impact Of Personality Traits On Academic Dishonesty Among

Pakistan Students. The Journal Of Commerce, 3(2), 50–61. Retrieved From

http://www.ciitlahore.edu.pk/papers/abstracts/146-8588087886673289558.pdf

Aziz, A., & Cahyonowati, N. (2015). Pengaruh Ethical Ideology Terhadap Ethical Judgements

Pada Mahasiswa Akuntansi, 4, 1–8.

Ballantine, J. A., Mccourt Larres, P., & Mulgrew, M. (2014). Determinants Of Academic

Cheating Behavior: The Future For Accountancy In Ireland. Accounting Forum, 38(1), 55–

66. https://doi.org/10.1016/j.accfor.2013.08.002

Cressey, D. R. (1950). The Criminal Violation Of Financial Trust. American Sociological

Review, 15(6), 738–743.

Davy, J.A., Kincaid, J.F., Smith K.J., & Trawick, M. (2007). An Examination Of The Role Of

Attitudinal Characteristics And Motivation On The Cheating Behavior Of Business Students.

Ethics And Behaviour, 17(3), 281–302.

Deliana, Abdulrshmsn, N. (2017). Perilaku Kecurangan Akademik (Academic Fraud)

Mahasiswa Akuntansi Pada Perguruan Tinggi Negeri.

Dewi, S. R. (2006). Gender Mainstreaming : Feminisme, Gender Dan Transformasi Institusi.

Jurnal Perempuan, No 50.

Donse, L., & Groep, I. H. Van De. (2013). Academic Dishonesty Among College Students :

Predictors And Interventions. Social Cosmos, 10(1), 40–50.

Faucher, D., & Caves, S. (2009). Academic Dishonesty: Innovative Cheating Techniques And

The Detection And Prevention Of Them. Teaching And Learning In Nursing, 4, 37–41.

Farnese, M. L., Tramontano, C., Fida, R., & Paciello, M. (2011). Cheating Behaviors In

Academic Context: Does Academic Moral Disengagement Matter? Procedia - Social And

Behavioral Sciences, 29(2010), 356–365. https://doi.org/10.1016/j.sbspro.2011.11.250

Finn, K. V., & Frone, M. R. (2010). Academic Performance And Cheating : Moderating Role Of

School Identification And Self-Efficacy, (January 2015), 37–41.

https://doi.org/10.3200/joer.97.3.115-121

Forsyth, D. (1980). A Taxonomy Of Ethical Ideologies. Journal Of Personality And Social

Psychology, Vol. 39 No, 175–184.

Galil, A., Yarmolovsky, J., Gidron, M., & Geva, R. (2019). Cheating behavior in children:

Integrating gaze allocation and social awareness. Journal of experimental child

psychology,178, 405-416.

Graves, M. S. (2008). Student Cheating Habits: A Predictor Of Workplace Deviance. Journal Of

Diversity Management, 3(1), 15–22.

Hendricks, B. (2004). Academic Dishonesty : A Study In The Magnitude Of And Justifications

For Academic Dishonesty Among College Undergraduate And Graduate Students. Jurnal Of

College Student Development, Thesis, 212–260.

The Influence of Fraud Diamond, Gender, Ethical Ideology on Cheating Behavior of Accounting Student

671

Ismail, S. (2014). Effect Of Ethical Ideologies On Ethical Judgment Of Future Accountants:

Malaysian Evidence. Asian Review Of Accounting, 22(2), 145–158. https://doi.org/10.1108/

ara-08-2013-0052

Ismail, S & Hana ,Salwa. (2016). Cheating Behaviour Among Accounting Students: Some

Malaysian Evidence. Accounting Research Journal, Vol. 29. https://doi.org/10.1108/arj-02-

2016-0015

Januarti, Indira & Eriskawati, E. (2016). The Influence Of Relativism, Idealism, And Gender On

The Students’s Academic Cheating Behaviour. Jurnal Dinamika Akuntansi, 8, 73–83.

Kidwell, L. A., & Kent, J. (2008). Integrity At A Distance: A Study Of Academic Misconduct

Among University Students On And Off Campus. Accounting Education, 17(SUPPL.1).

https://doi.org/10.1080/09639280802044568

Kobayashi, E., & Fukushima, M. (2012). Gender, Social Bond, And Academic Cheating In

Japan. Sociological Inquiry, 82(2), 282–304. https://doi.org/10.1111/j.1475-682x.2011.0

0402.x

Latan, H. 2013. Structural Equation Modelling: Konsep dan Aplikasi Menggunakan Program

Lisrel8.80. Bandung: Penerbit Alfabeta

Lewellyn, P. G., & Rodriguez, L. C. (2015). Does Academic Dishonesty Relate To Fraud

Theory ? A Comparative Analysis. American International Journal Of Contemporary

Research, 5(3), 1–6.

Mc Cabe, Donald (2004). Academic Dishonesty At The Graduate Level. Ethics & Behavior,

11(3), 287–305. https://doi.org/10.1207/s15327019eb1103

Murdiansyah, I., Sudarma, M., & Nurkholis. (2017). Pengaruh Dimensi Fraud Diamond

Terhadap Perilaku Kecurangan Akademik ( Studi Empiris Pada Mahasiswa Magister

Akuntansi Universitas Brawijaya ). Jurnal Akuntansi Aktual, 4(2), 121–133.

Noor, R. M., Ridhuan, M., & Dangi, M. (2014). Empirical Study On Student ’ S Higher

Education Institution System Using Fraud Diamond Theory. Gading Business And

Management, 18(2), 31–50.

Puspitawati, H. (2013). Konsep , Teori Dan Analisis Gender. Institut Pertanian Bogor.

Reiss, M. C., & Mitra, K. (1998). The Effects Of Individual Difference Factors On The

Acceptability Of Ethical And Unethical Workplace Behaviors. Journal Of Business Ethics,

17, 1581–1593. https://doi.org/10.1023/a:1005742408725

Saat, M. M., Porter, S., & Woodbine, G. (2012). A Longitudinal Study Of Accounting Students

’ Ethical Judgement Making Ability. Accounting Education: An International Journal, 21:3,

215-229. https://doi.org/10.1080/09639284.2011.562012

Sekaran & Bougie. (2010). Research Methods For Business: A Skill Building Approach 5th

Edition. (J. Wiley, Ed.) (7th Ed.). New York.

Sugiyono. (2007). Metode Penelitian Pendidikan (Pendekatan Kuantitatif, Kualitatif, dan R &

D). Bandung: Alfabeta.

Thanasak, R. (2013). Beyond The Fraud Diamond. International Journal Of Management And

Administrative Sciences, 2, Pp.01-05.

Webster. (2000). Webster Dictionary.

Wells, T Joseph. 2010. Principle of Fraud Examination. Fourth Edition. Wiley : USA

Wolfe, B. D. T., & Hermanson, D. R. (2004). The Fraud Diamond : Considering The Four

Elements Of Fraud, 2.

Young, D. (2013). Perspectives On Cheating At A Thai University. Language Testing In Asia,

3(1), 6. https://doi.org/10.1186/2229-0443-3-6

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

672