How the Role of Information Technology in the Quality

of Accounting Information Systems: Empirical Test on

Accredited Private Universities in Java

Ruhul Fitrios, and Nasrizal

Fakulty of Economic and Business, Universitas Riau, Pekanbaru, Indonesia

Abstract. Various government and private units have not yet implemented

quality accounting information system. Users need quality information generated

by accounting information systems to guide them in making quality decisions.

Information technology plays an important role in helping accounting

information systems to achieve this goal. This study is intended to examine the

role of information technology in producing the quality of accounting

information system. The research hypothesis was tested on 108 financial units of

A and B accredited Private Universities in Java selected using the stratified

random sampling method, and 71 sample units have returned the questionnaire.

The research methods used are descriptive and verification methods. The study

results show that information technology significantly influences the quality of

accounting information system. And it can be used to solve the problem on there

is no quality of accounting information system through the use of appropriate

information technology.

Keywords: Information technology · Accounting information system quality

1 Introduction

An organization is in an environment that generally changes faster than the changes in

the organization itself [1]. To continue to exist in their environment, the organization

must be able to adapt to changes in the environment. One such effort is seen in the

dependence of organizations with information technology and information systems,

both for operational needs and to maintain their strategic advantage [2]. Specifically

information technology plays a role in helping information systems produce

information for decision making and problem solving more thoroughly in organizations

[3][4].

An accounting information system produces useful accounting information, both

for internal and external party decision making [5]. Thus, quality information depends

on the quality of the information system that produces it [6]. Some of the characteristics,

such as: Integration, reliable, and flexible system describes the quality of the accounting

information system applied. The quality of system integration is reflected in the

integration of various components or sub-systems [7], data integration [3], and

integration between related systems [8]. The reliability of the system is seen in the

system's ability to minimize errors and produce true and consistent information [8].The

Fitrios, R. and Nasrizal, .

How the Role of Information Technology in the Quality of Accounting Information Systems: Empirical Test on Accredited Private Universities in Java.

DOI: 10.5220/0010520700002900

In Proceedings of the 20th Malaysia Indonesia International Conference on Economics, Management and Accounting (MIICEMA 2019), pages 563-571

ISBN: 978-989-758-582-1; ISSN: 2655-9064

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

563

use of quality accounting information systems helps improve the quality of decision

making by providing accurate and timely and relevant information [9][10].

But in reality the accounting information system applied in the units of government

and private not meet the quality characteristics such as: the system is not yet integrated

[11], the system is not reliable [12], and the system is not flexible [13]. Wahid [11] as

Head of the Information System Board (BSI) of the Islamic University of Indonesia

stated that the accounting information system at the Islamic University of Indonesia

was not yet integrated, because the system services available today were still

fragmented, so system users had to move platforms to access. In another part, Bisri [12]

as the Chancellor of Brawijaya University stated that there are some university revenues

that have not been included as university income, even though the internal campus

already has an Internal Control Unit (ICU). The statement shows the problem of the

reliability of the accounting information system to produce accurate information.

In addition, Niartiningsih [13], as the Kopertis Region IX Coordinator of Sulawesi,

described that the information systems at twelve private universities in South Sulawesi

are inflexible, because these private institutions have difficulty adjusting the reporting

system changes from the University Database System (UDS) to the Feeder System.

Based on some of the phenomena stated above, it can be concluded that there are

problems with integration, reliability and flexibility system in accounting information

systems in various universities in Indonesia.

Information technology used is one of the factors that influence the quality of

accounting information systems [10][14][15]. Information technology (IT) is a term

that refers to all technologies that collectively facilitate the development and

maintenance of information systems [4]. Information technology influences every

aspect of accounting which includes financial reporting, management accounting,

auditing and tax [10]. More specifically [14] states that information technology has a

major influence on accounting information systems because technology is the

foundation for accounting information systems. In addition, information technology has

significantly strengthened the role of accounting information systems to support the

decision making of every manager and knowledge worker in business [15].

Several previous studies have proven the importance of the role of information

technology for the quality of accounting information systems. Al Eqab & Ismail [16]

prove a positive and significant relationship between information technology and

accounting information systems. In line with the results of research Sacer & Oluic [17]

on small and medium-sized companies in Croatia that information technology

contributes significantly to the quality of accounting information systems. In addition,

Al-Zwyalif [18] also proved that the appropriate management of information

technology affects the usefulness of accounting information systems. Furthermore,

Susanto's research results [19] at universities in Bandung also concluded that

information technology influences the quality of accounting information systems.

The importance of the quality of accounting information systems to produce quality

information for decision makers, and the role of technology for information to improve

the quality of accounting information systems, this study aims

to examine how much

influence the information technology has on the quality of accounting information

systems.

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

564

2 Literature Review

2.1 Information Technology

Pearlson & Saunders [20] states that information technology is all forms of technology

used to create, store, exchange, and use information. Williams & Sawyer [21] reinforces

the above opinion that information technology describes every technology that has the

ability to help produce, manipulate, store, communicate, and or disseminate

information. In addition, Thomson & Baril [22] argues that information technology is

something that is used as a computing and communication tool that has the ability to

capture data (input), process and or convert, store and presents data (output). We define

that information technology is all forms of technology that have the ability to help

accounting information systems to process, store, transfer and transfer quality

information.

According to Innovation Diffusion Theory (IDT), there is a set of theoretical

constructs that represent information technology, including: image, visibility,

compatibility, result demonstrability, voluntariness of use, which is used for research

on acceptable technological innovation [23]. In another part according to Pearlson &

Saunders [20] information technology can be seen from the aspect of technical issues,

through the characteristics: adaptability, scalability, standardization, maintainability,

and security. Other experts, Turban, et al., [24] describe information technology

through 4 (four) characteristics, namely: dependable, manageable, adaptable, and

affordable. Likewise Thomson & Baril [22] suggested that there were 4 (four)

characteristics groups to measure the performance of information technology, namely

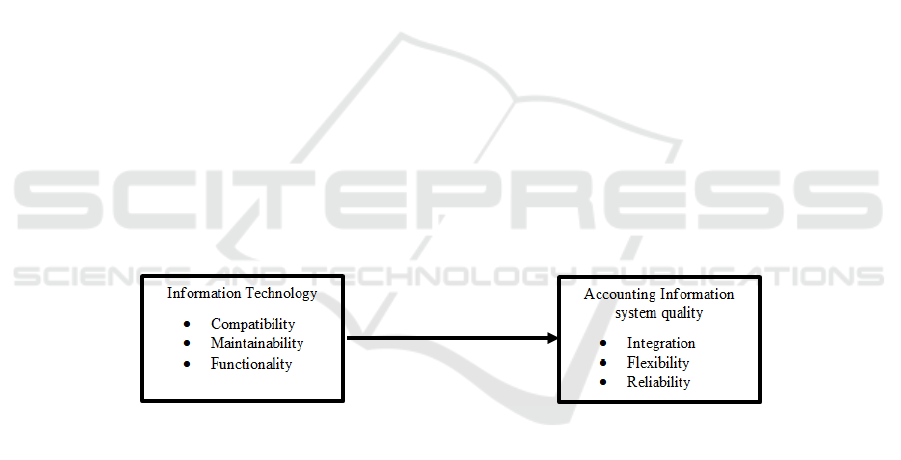

functionality, ease of use, compatibility, and maintainability. This study uses the

characteristics: compatibility, maintainability and functionality to measure the concept

of information technology.

2.1.1 Accounting Information System

Simkin, Roce, & Norman [10] state that an accounting information system is a

collection of data and processing procedures that produce financial information that is

needed by its users. Another opinion was expressed by Mancini, et al., [25] that the

accounting information system is a complex system consisting of a collection of

components that are closely interrelated (such as data, information, human resources,

information technology tools, models and procedures accounting). Furthermore

Susanto [26] defines accounting information systems more specifically, as a collection

(integration) of sub-systems / components both physical and non-physical that are

interconnected and work together in harmony to process financial transaction data into

financial information. We argue that an accounting information system is a collection

of components or subsystems that interact harmoniously to process financial data and

generate financial information for decision makers.

Petter, Delone & Mclean, [27] describe the quality of information systems through

characteristics-characteristics: ease of use, system flexibility, system reliability, and

ease of learning. The same thing was stated by Delone & McLean [28] that the quality

of information systems can be measured through the characteristics: ease-of-use,

functionality, reliability, flexibility, data quality, portability, integration, and

How the Role of Information Technology in the Quality of Accounting Information Systems: Empirical Test on Accredited Private

Universities in Java

565

importance. Fitrios [29] uses characteristics: flexibility, reliability, and integration to

determine the quality of accounting information systems. The quality of the accounting

information system in this study is measured by the characteristics: flexibility,

reliability and integration.

2.1.2 Framework and Hypothesis

Information technology affects the quality of accounting information systems. Valacich

& Schneider [3] suggested that information technology is used by accounting

information systems to collect, create and distribute useful data. Gelinas & Dull [14]

emphasize that the development of information technology has a major impact on

accounting information systems, because technology is the foundation on which

accounting information systems lean. More specifically other impacts of the use of

information technology are related to the time needed to carry out input-process-output,

to produce financial information [10]. With advances in technology, transaction-

financial transactions processed immediately, so that the accounting information

system can generate financial reports in real time [10].

The results of previous studies from Sacer & Oluic [17] concluded that information

technology contributes significantly to the quality of accounting information systems.

Furthermore Quintero, Mora, & Abrego [30] stated that information technology

supports the application of accounting information systems by increasing company

productivity, such as increasing administrative activities, and making decisions based

on information generated. Likewise, Susanto [19] conducted research at college

institution in Bandung to conclude that information technology has a significant effect

on the quality of accounting information systems.

Based on the description of the theories and the results of previous studies above, it

can be concluded that the research hypothesis that information technology affects the

quality of accounting information systems.

Fig. 1. Research Model.

3 Methodology

The research method used is descriptive research methods and causal research methods.

Descriptive method is intended to describe the characteristics of the data regarding the

event, person or situation under study [31]. While the causal research method is

intended to determine the cause and effect / effect of the relationship between two or

more variables [32].

This research was conducted at private universities accredited A and B in Java.

Unlike state universities as government tertiary education, private tertiary institutions

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

566

are owned and managed by certain individuals or groups / foundations. The funding for

the management and implementation of education is the full responsibility of the

tertiary institution. The population of accredited private universities A and B is 170.

The questionnaire was sent to 119 selected private universities that were selected

through the stratified random sampling method. A total of 71 universities returned

questionnaires with a total of 220 questionnaires fulfilling the criteria to be processed.

This study uses Structural Equation Modeling (SEM) based on Partial Least Square

(PLS) to test the validity and reliability and test the hypothesis. PLS-based SEM is used,

because latent variables are formed by dimensions and indicators.

4 Result and Discussion

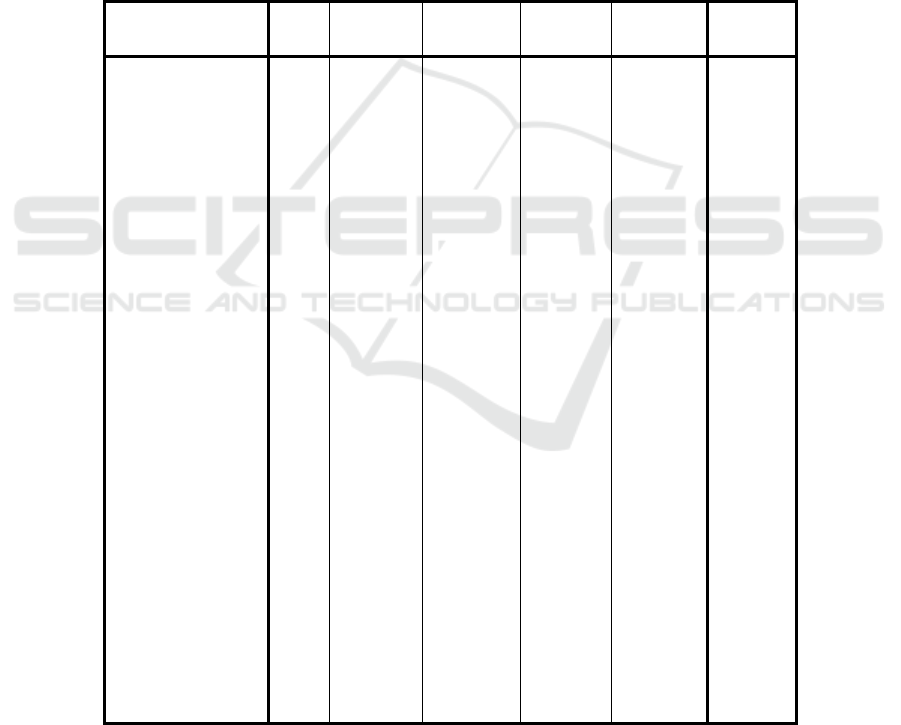

Table 1. Descriptive Statistics of Information Technology and Accounting Information System

Quality Variables.

N

Minimu

m

Maximum Mean

Std.

Deviation

Criteria

Compatibility

IT1 220 2.00 5.00 3.9364 .76184 enough

IT2 220 1.00 5.00 3.3045 1.03057 enough

Maintainability

IT3 220 1.00 5.00 3.4455 .93717 enough

IT4 220 2.00 5.00 3.6273 .82605 enough

IT5 220 1.00 5.00 3.5545 .88195 enough

Functionality

IT6 220 1.00 5.00 3.0182 1.43334 enough

IT7 220 1.00 5.00 3.7136 .81917 enough

Flexibility

AISQ1 220 1.00 5.00 3.4612 .88934 enough

AISQ 2 220 1.00 5.00 3.2146 1.0859 enough

Reliability

AISQ 3 220 1.00 5.00 3.5455 1.52318 enough

AISQ 4 220 1.00 5.00 3.9591 .85823 enough

AISQ 5 220 1.00 5.00 3.5864 .92555 enough

Integration

AISQ 6 220 1.00 5.00 3.7318 .87800 enough

AISQ 7 220 1.00 5.00 3.1364 1.28125 enough

AISQ 8 220 1.00 5.00 2.8000 1.23565 Not good

Valid N (listwise) 220

How the Role of Information Technology in the Quality of Accounting Information Systems: Empirical Test on Accredited Private

Universities in Java

567

Table 1 show that the average respondent's answers to questions related to indicators

of the information technology variable and the accounting information system quality

variable on the "sufficient" criteria, except AISQ 8 questions regarding integration

between systems showed the criteria of "not good". Each respondent's answer shows

that there is a gap between theory and reality in universities.

Evaluation of structural models is used to see the results of hypothesis testing. The

evaluation of the structural model evaluation results through path coefficient and R

Square will determine the ability of empirical data to support the theory [33].The ability

of information technology constructs to explain the constructs of the quality of

accounting information systems can be seen through the value of R Square. R Square

test results show a value of 0.6607 and can be said to be "moderate". This can be

interpreted that the information technology construct is able to explain the quality of

accounting information systems by 66.07%, while the remaining 33.93% is explained

by other variables.

The statistical hypothesis indicates whether or not there is an influence of

information technology on the quality of the accounting information system. The

structural model evaluation results provide a path coefficient with a positive sign of

0.813 and significant at alpha 5%, which is marked by a statistical t value of 19,217>

1.96 (see in table 2). The results of this study reject H

0

and accept H

1

. Thus it can be

concluded that information technology has a significant positive effect on the quality

of accounting information systems. That increasing the use of information technology

appropriately increases the quality of accounting information systems at private

accredited universities in Java.

This study empirically proved that information technology affects the quality of

accounting information systems. This result is shown by the statistical t value which is

greater than the critical value and is supported by a high path coefficient value. This

result is also strengthened by the R square value of 0.6607 which shows the ability or

role of information technology in explaining the quality of accounting information

systems.

Table 2. Path Coefficients (Mean, STDEV, T-Values).

Original

Sample

(O)

Sample

Mean

(M)

Standard

Deviation

(STDEV)

Standard

Error

(STERR)

T Statistics

(|O/STERR|)

AISQ -> AISQFLEX 0.812675 0.817258 0.027016 0.027016 30.081093

AISQ -> AISQINTERG 0.884474 0.883816 0.030005 0.030005 29.477473

AISQ -> AISQRELIAB 0.816081 0.819446 0.041333 0.041333 19.74381

IT -> AISQ 0.812834 0.809177 0.042298 0.042298 19.217018

IT -> ITCOMPAT 0.908885 0.907752 0.023265 0.023265 39.067152

IT -> ITFUNCT 0.857911 0.853234 0.031701 0.031701 27.062296

IT -> ITMAINT 0.963207 0.963631 0.008202 0.008202 117.44136

The significance of the influence and the magnitude of the role of information

technology on the quality of accounting information systems is supported by the strong

relationship of 3 (three) dimensions of information technology, namely: compatibility,

maintainability, and functionality of the construct (see in table 2). This result is shown

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

568

by the path coefficient value of the three dimensions is higher. Whereas in other parts

the quality of accounting information systems is also supported by the dimensions of

flexibility, reliability and integration which have a strong relationship with the construct

(see in table 2).

Furthermore, the results of empirical data collected in this study are able to describe

or explain the phenomenon of the lack of quality accounting information systems that

occur in the field. Empirical data shows that the average value per item question both

about information technology and accounting information systems that show a value of

"sufficient" and specifically for the question item "integration between systems" shows

the results of "not good" than the maximum value of 5. These results illustrate that

accounting information systems at private accredited universities are not yet of high

quality, and the information technology used has not been able to support the quality of

accounting information systems.

The above discussion illustrates that to improve the quality of accounting

information systems, it is necessary to increase the ability of the information technology

used. The ability of the information technology used can be seen through its

dimensions. The path coefficient value shows successive results from the dimensions

of "maintainability" followed by "compatibility" and "functionality". The information

technology used must have the ability to adapt to other information technologies

needed, have the ability to adapt to changes in the capacity of the accounting

information system. In addition, the information technology used must be supported by

the availability of parts and repair services.From the aspect of compatibility,

information technology is needed that is interoperable with other technologies, and they

have conformity to product standards. Then from the aspect of functionality, it takes

technology that has sufficient speed to send and receive data / information and has

sufficient connectivity capability to operate.

The results of this study are able to confirm the statement of Wilkinson, et al., [5]

where information technology is able to significantly improve the performance of a

company's accounting information system. The results of this study also reinforce the

statement put forward by Gelinas & Dull [14] that information technology has a major

impact on the quality of accounting information systems, and provides opportunities

for organizations to improve the efficiency and effectiveness of accounting information

systems [10].The results of this study further strengthen the results of previous studies:

Al-Eqab & Ismail [16], Al-Zwyalif [18], Sacer & Oluic [17], Quintero, Mora, &

Albegro [30], and Susanto [19] which concludes the importance of the role of

information technology on the quality of accounting information systems.

5 Conclusion

Based on the results of the research and discussion above it can be concluded that

information technology influences the quality of the accounting information system.

Not yet the quality of accounting information systems at accredited private universities

in Java which is characterized by accounting information systems that are not flexible,

not integrated and not reliable due to the inadequate use of the required information

technology.

How the Role of Information Technology in the Quality of Accounting Information Systems: Empirical Test on Accredited Private

Universities in Java

569

The results of this study are able to answer the research problem described through

phenomena. The use of information technology with the right characteristics can

minimize the problem of not yet quality accounting information systems.A limitation

of this study is the number of samples used and this study focuses on private

universities, not in combination with public universities. Information system quality

research can also be grouped by region and other status, owner groups, and others

References

1. Laudon, K.C., & Laudon, J.P.: Management Information Systems, Managing the Digital

Firm, Fourteenth Edition, Pearson Education Limited (2016)

2. Cupta, M., & Sharman, R.: Handbook of Research on Social and Organizational Liabilities

in Informations Security, Information Science Reference (IGI Global), Hershey, USA.

(2009)

3. Valacich, J.S., & Schneider, C.: Information Systems Today: Managing in the Digital

World, 7

th

Edition, Global Edition, Pearson Education Limited (2016)

4. Sousa, Kenneth J., & Oz., E.: Management Information Systems, Seventh Edition, Cengage

Learning, Stanford, USA (2015)

5. Wilkinson, J.W., Cerullo, M.J., Raval, V., & Wong on W.B.: Accounting Information

Systems Essential Concepts and Applications, Fourth Edition, John Wiley and Son, Inc.

(2000)

6. Stair, R., & Reynolds, G.: Fundamental of Information Systems, Sixth Edition, Course

Technology, Cengage Learning (2012)

7. Bentley, Jeffrey L. & Whitten D.: Systems Analysis and Design Methods, 7

th

Edition,

McGrawhill Irwin (2007)

8. Avison, D. & Fitzgerald, G.: Information Systems, Development Methodologies,

Techniques & Tools, 4

th

Edition International, McGraw-Hill UK (2006)

9. Romney, M.B., & Steinbart, P.J.: Accounting Information Systems, Thirteenth Edition,

Pearson Education Limited, Edinburgh Gate (2015)

10. Simkin, M.G., Roce, J.M., & Norman, C.S.: Core Concepts of Accounting Information

Systems, Twelfth Edition, John Wiley & Son, Inc. (2012)

11. Wahid, F.: UII-menyongsong-era-layanan-sistem-informasi-terintegrasi https:

//www.uii.ac. id/uii-menyongsong-era-layanan-sistem-informasi-terintegrasi/ (2018)

12. Bisri, M.: Rektor Akui Laporan Keuangan UB Masih Bermasalah, http://www.malang-

post.com/pendidikan/110505-rektor-akui-laporan-keuangan-ub-masih-bermasalah (2015)

13. Niartiningsih, A.: Dikti bekukan 12 perguruan tinggi di Sulsel. http://www. antaranews.

com/berita/519353/dikti-bekukan-12-perguruan-tinggi-di-sulsel (2015)

14.

Gelinas, U.J., & Dull, R.B.:

Accounting Information Systems, Seventh Edition, Thomson

South Western

(2008)

15. Marakas, G.M., & O’Brien, J.A.: Introduction to Information Systems, Sixteenth Edition,

International Edition, McGraw-Hill Education (2013)

16. Al-Eqab, M., & Ismail, N.A.: Contingency Factors and Accounting Information System

Design in Jordanian Companies, IBIMA Business Review,

http://www.ibimapublishing.com/journals/IBIMABR/ ibimabr.html Vol. 2011, pp. 1-13

(2011)

17. Sacer, I.M., & Oluic, A.: Information Technology and Accounting Information Systems

Quality in Croation Middle and Large Companies, Journal of Information and

Organizational Sciences (JIOS), Vol. 37, pp. 117-126 (2013)

MIICEMA 2019 - Malaysia Indonesia International Conference on Economics Management and Accounting

570

18. Al-Zwyalif, I.M.: IT Governance and its Impact on the Usefulness of Accounting

Information Reported in Financial Statements, International Journal of Business and Social

Science, Vol. 4, pp. 83-94 (2013)

19. Susanto, A.: Second Order Model for Measuring the Impact of Information Technology on

The Quality of Accounting Information Systems Research at Higher Education in Bandung,

Journal of Engineering and Applied Sciences, 12(4) 1018-1027 (2017)

20. Pearlson, K.E., & Saunders, C.S.: Managing and Using Information Systems A Strategic

Approach, 5

th

edition, John Wiley & Son, Inc. (2013)

21. Williams, B.K., & Sawyer, S.C.: Using Information Technology, A Practical lntroduction

to Computer & Communications, Ninth Edition, Complete Version, McGraw-Hill/Irwin,

NY (2011)

22. Thomson, R., & Baril, W.C.: Information Technology and Management, 2

nd

Edition,

Mc.Graw-Hill, USA (2003)

23. Venkatesh, V., Morris, M.G., Davis, G.B., & Davis, F.D.: User Acceptance of Information

Technology, MIS Quarterly, Vol. 27, No. 3, pp. 425-478 (2003)

24. Turban, E., Volonino, L., & Wood, G.R.: Information Technology for Management

Advancing Sustainable, Profitable Business Growth, 9

th

Edition, John Wiley & Sons, Inc.

(2013)

25. Mancini, D., Vaassen, E.H.J., & Dameri, R. P.: Accounting Information Systems for

Decision Making, Springer-Verlag Berlin Heidelberg (2013)

26. Susanto, A.: Sistem Informasi Akuntansi: Struktur-Pengendalian- Resiko-Pengembangan,

Edisi Perdana, Lingga Jaya, Bandung (2013)

27. Petter, S., DeLone, W., & McLean, E.: Measuring Information Systems Success: models,

dimensions, measures, and interrelationships, European Journal of Information Systems,

Vol. 17, 236-263 (2008)

28. Delone, W.H, .& McLean, E.R.: The DeLone and McLean Model of Information Systems

Success: A Ten-Year Update, Journal of Management Information Systems, Spring, Vol.

19. No. 4 (2003)

29. Fitrios, R.: The Influence of Environmental Uncertainty on The Accounting Information

Systems Quality and its Impact on The Accounting Information Quality, Journal of

Theoretical and Applied Information Technology, Vol. 96, No. 21 (2018)

30. Quintero, M., Mora, A., & Abrego, A.: Enterprise Technology in Support for Accounting

Systems, an Innovation and Productivity Approach, JISTEM - Journal of Information

Systems and Technology Management, Revista de Gestão da Tecnologia e Sistemas de

Informação. Vol. 12, No. 1, pp. 29-44 (2015)

31. Sekaran. U & Bougie, R.: Research Methods for Business, A Skill Building Approach, Sixth

Edition. John Wiley & Sons, Inc. (2013)

32. Hair, Jr. JF., Wolfinbarger, M.F., Ortinau, D.J. & Bush R.P.: Essentials of Marketing

Research, 2nd edition, McGraw-Hill/Irwin, NY (2010)

33. Hair, Jr, JF., Hult, GTM., Ringle., CM. & Sarstedt M.: A Primer on Partial Least Squares

Structural Equation Modeling (PLS-SEM), Sage Publications, Inc. LA (2014)

How the Role of Information Technology in the Quality of Accounting Information Systems: Empirical Test on Accredited Private

Universities in Java

571