Social Activities Effect on Household Enterprise: A Descriptive

Analysis Form East Indonesia

Riswanti Budi Sekaringsih

Faculty of Islamic Economics and Business, State Islamic University (UIN), Sunan Kalijaga, Yogyakarta, Indonesia

Keywords: Informal Financial Market, Rotating Saving and Credit Association, Expenditure, Income, IFLS EAST.

Abstract: This research aims to explore empirically east Indonesian household entreprise on social activities and

financial wealth. We explore various indicators for example if individual have borrowed money from financial

institution, the number of community activites that they follow, joining rotating saving and credit association,

and their income from non-farm and farm business. This research uses IFLS (Indonesian Family Life Survey)

East that has wide range information on financial inclusion indicators and other socio-economics variables

that are not provided by other almost-similar-type database in East Indonesia. We use describtive statistic and

ordinary least square to estimate how social activites affected on household income and expenditure. The

findings that household who joining rotating saving and credit association will have higher expenditure and

lower income. Most of Indonesian people joining social activites that related on their expenditure and income.

More over this research leed people to know how to make informal financial market more efficient than

before.

1 INTRODUCTION

Economy crisis that hit Indonesia in the middle of

1997 and 2008 proved that micro and small

enterprises have proven as a self-sufficient business

who have a strong resistance. The data show that.

Data shows the number of micro and small

entrepreneurs 55,206,444 units that absorb

101,722,458 workers (Kementerian Koperasi dan

Usaha Kecil dan Menengah, 2015).

The definition of micro business is a business that

has assets or net assets of up to Rp. 50 million,

excluding land or buildings for business premises and

an annual sales turnover of up to Rp. 300 million

(Pemerintah Republik Indonesia, 2008). Usually

these micro-businesses are looking for a living and

are not export-oriented. Generally small and medium

micro business operators are households. This

business is carried out jointly by all household

members. The income earned will be used to finance

all household needs.

Household enterprise in this paper consists of two

types of households, the first is a household that

manages a business either independently or working.

The two agricultural households that process the land

then sell the produce. The household works

independently to fulfill their daily needs.

Unfortunately sometimes the household enterprise

has a low income so they have difficulty accessing

capital. This difficulty can be seen in their way to gain

financial access.

Financial acceas not only include primary savings

mobilization units with little or no lending; primary

lending units that are hardly involved in savings

mobilization. Further SOFIA (Survey on Financial

Inclusion and Access) found that limited access to

financial services has been identified as one of the key

constraints to people's participation in economic

activity in eastern Indonesia. Thats why in Indonesia

arises a lot of informal finance. This informal finance

is not related to banking.

The Eastern Indonesian Household Life Aspect

Survey (SAKERTI TIMUR or SAKERTIM) or also

known as the Indonesian Family Life Survey East

(IFLS East) conducted in 7 provinces in Eastern

Indonesia including: East Nusa Tenggara, East

Kalimantan, Southeast Sulawesi, Maluku, Maluku

North, West Papua and Papua. By using this

household data in East Indonesia. This study wants to

describe the effect of social activities undertaken by

households on income. This household income is

devoted to households that have businesses both

agricultural and non-agricultural. This research

consists of introduction, theoretical foundation,

methodology, discussion and closing.

52

Sekaringsih, R.

Social Activities Effect on Household Enterprise: A Descriptive Analysis Form East Indonesia.

DOI: 10.5220/0010114700002898

In Proceedings of the 7th ASEAN Universities International Conference on Islamic Finance (7th AICIF 2019) - Revival of Islamic Social Finance to Strengthen Economic Development Towards

a Global Industrial Revolution, pages 52-58

ISBN: 978-989-758-473-2

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

2 LITERATURE REVIEW

When associated with income, consumption is the

portion of income spent on consumption needs.

Whereas savings are the portion of income that is

saved or not spent. Therefore, income is equal to

consumption and savings. This concept does not only

apply to households but to households that have

businesses. To increase income, it is necessary to

increase capital and access to obtain better finance

than before.

Limited access to financial services has been

identified as one of the key constraints to people's

participation in economic activity for many living in

eastern Indonesia who are in rural areas, small

farmers, and micro to medium household enterprises

(SOFIA et al., 2017).

According to Abebe, et.al. (Abebe, Tekle, &

Mano, 2018), promoting savings is important to

enterprise development because one way of building

adequate capital to overcome credit constraints and

withstand transitory business shocks, a safer option

for storing wealth than keeping money at home,

creating a relationship with formal financial

institutions, the cost of internal financing of

investment through savings is often much lower than

the cost of accessing credit and help in cases of

emergencies.

In Ethiopia (Abebe et al., 2018) , we found that

entrepreneurs who received only the financial literacy

training did not significantly increase saving. They

conducted a randomized controlled trial with 426

samples of operating micro-entrepreneurs in Addis

Ababa. Microentrepreneurs do not know the

importance of internally accumulating financial

resources and they also lack the necessary financial

or it is difficult to keep it up over the course of their

business operations. Because many household

enterprises have difficulty accessing formal finance,

they make certain associations. These include

savings, lending to members of associations or groups

such as: savings collectors and money keepers,

commercial lenders (money lenders), friends, family

and non-commercial lenders, self-help financial

groups that include different levels of savings and

credit rotating ones and licensed cooperative societies

or unions (State, 2013).

These are the group of informal finance as the

Rotating Savings and Credit Association (ROSCAS,

Arisan in Bahasa). They are the most basic forms of

savings and credit arrangements including regular

fixed amounts of contributions to a common pool of

funds by members in turn. Orders of receiving the

amounts are decided by negotiation, lottery or any

other agrements. Sometimes this method can be

called a lottery saving.

State, et.al (2013) Found that the informal finance

sector has considerable experience and knowledge

about dealing with small business borrowers and that

their performance in relation to financing small

business has been positive especially in Asia and

Latin America. Using A multi-stage sampling

technique to obtain information from 240

respondents. Then the data is analyzed using

descriptive and inferential statistics. Informal sources

of credit have been known to gain preferences from

micro and small-scale entrepreneurs. Informal

financial markets have been recognized as an engine

of rural and urban development.

3 ANALYSIS MODEL

3.1 Data and Method

3.1.1 Data

This paper uses IFLS East. IFLS East is a survey that

has been conducted in 2012. This survey cover in 7

provinces in Eastern Indonesia including: East Nusa

Tenggara, East Kalimantan, Southeast Sulawesi,

Maluku, Maluku North, West Papua and Papua.

Information in individual and household data levels

cover all socio-economic information, such as

education, occupation, religion, health, marriage,

active in the community and so forth. Furthermore, at

the community level we can obtain information about

the condition of infrastructure, socio-economic

conditions, and various social programs in the

community including the existence of financial

facilities that exist in every village.

In this study, we combine information of

individual, household, and community levels. The

purpose is to obtain a comprehensive picture of

household who being enterprise both in farm and non-

farm business and their demographic, socio-

economic and community characteristics. According

to that, we have 2310 households. More detail

explanation about our sample can be found in

Appendix.

3.1.2 Method

Descriptive statistics is used to get first description

and to compare average of each variable. For

instance, we compare the percentage of household

who have join community activities, rotating saving

and credit association and their income or

Social Activities Effect on Household Enterprise: A Descriptive Analysis Form East Indonesia

53

expenditure. The results are tabulated by using

STATA 14 and then transferred to the Microsoft

Excel 2016.

For control variables, we combine some variables

from individual and household levels. For individual

characteristics, we consider age, gender, education

level, and marital status as control variables. While

for household characteristics, we consider household

members, and household’s location. Lastly,

community characteristic will be represented by the

number of community activities and urban or rural

area. Then the formulate econometric specifications

as follows:

Financial Enterprise

)1(εββXcβXhβXdββY

i54i3i2i10i

XaXk

(1)

Where Y in the first model are the nominal amount of

income or expenditure in household. Then Xd

i

are

demographic characteristics (education, age, gender,

and marital status), Xh

i

is household characteristics

(education level of head household and the number of

household’s member), Xc

i

is community

characteristics (urban/rural), Xc

i

is number of

community activities that household join, and Xa

is

household join in rotating saving and credit

association. This research applies crossection data

analysis.

3.1.3 Result and Analysis

Before performing regression analysis, it is important

to look at descriptive statistics that enables us to see

common features. For this research we found 2,310

households who lives in the sample province. In our

study we tried to combine households that have

farming businesses and households that have non-

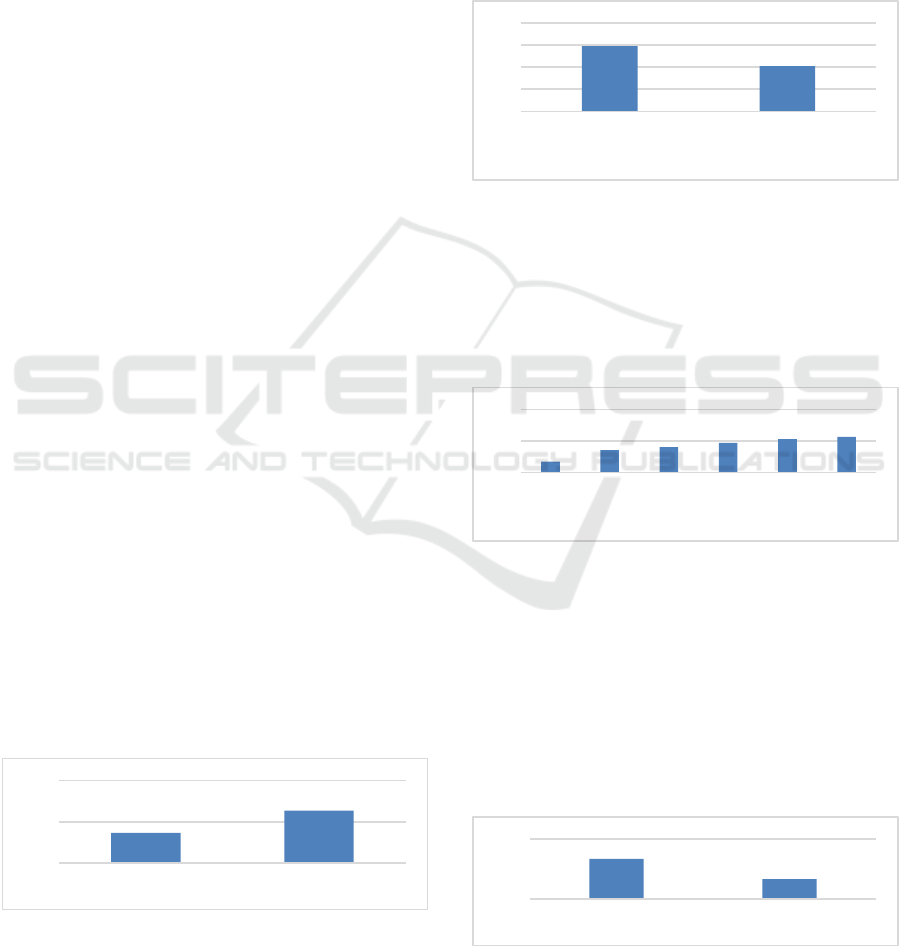

farm businesses. Further on figure 1. is 63.4% of the

respondents are farmers who have cultivated land.

This means that more than half of farmers in

Indonesia have land to be cultivated either by planting

rice or other food crops.

Figure 1: Percentace Of Responden Who Are Being Farmer

and Having Land.

Besides farmers we also observe households that

have a businesses or we called them household

enterprises. Small businesses run are generally small

business and intended to make a living. This

household business is usually carried out by

household members or all family members or helping

other families with kinship. In Figure 2, 40.83% of

households have a business. Coverage of household

enteprise that are run generally are micro-small and

medium businesses.

Figure 2: Percentace Of Who Being Household Enterprise.

Then about their social activities. Most of East

Indonesian people love to join social activities. This

fact can be proved on figure3, there are only 6.97%

who aren’t join any social activities. This ini meant

more than 93% respondent joint minimal one social

activities.

Figure 3: Percentace Of Number Social Activities That

Followed By Household.

Further if we see figure 4, its only 32.94% of

household in East Indonesia who are joining rotating

saving and credit association or arisan. Social

activities that most they are joining can be community

meeting, cooperatives, village saving and loans,

PNPM Madani, and women activities (PKK). the

more social activities will have an impact on the

reduced time to work.

Figure 4: Percentace of Household who Joining Arisan.

0

50

100

No Land Farmer Own Land Farmer

0

20

40

60

80

No Household

Enterprise

Own Household

Enterprise

6,97

14,24

16,15

18,83

21,17

22,65

0

20

40

0 1 2 3 4 5 and

more

67,06

32,94

0

100

not participate participate arisan

7th AICIF 2019 - ASEAN Universities Conference on Islamic Finance

54

As shown in appendix, we know that 45% of

responden were living in urban area. Further if we see

in figure 5, we can find out that the respondent was

on the seven province of east Indonesia. And the

biggest respondent are comming from West Nusa

Tenggara and South East Sulawesi, 16% of total

respondent. More over 42% of the sample are joining

community activites that related to finance. 47% said

that they join arisan or rotating saving and credit

association. And the average money that they

contribute about 343.190.9 rupiah in month.

Figure 5: Percentace Of Household Location Distribution.

For financial numbers, we found that the average

total income is 24.300.000 rupiah in year. Meanwhile

for non farm business enterprise 8.623.800 rupiah in

month and 5.836.482 rupiah for farm business

enterprise.

As explained before, we have two variables. Each

interest variable will have three difference types of

regression and each type will be distinguished by the

type of enterprise, which is farm or non- farm. To test

those regression we use Ftest for overall variables and

T-test for every variables.

For income variable we found that age has

negative impact on farm income. This is mean that if

the farmer geting older they got lower income as the

decrease of their power. Join arisan or rotating saving

and credit association has negatif impact specialy on

farming. Its the same case for household who has loan

that has negative impact on income.

The otherwise for expenditure, age, education,

and join arisan or rotating saving and credit

association has positive impact on expenditure. Its

mean they get older their spending is getting bigger.

Household who has higher education mean spend

more money than other. And who join rotating saving

and credit association its mean more money to spend.

But household size has negative impact in

expenditure.

4 CONCLUSIONS

This research attempts to explain how social activities

determinant East Indonesia income and expenditure.

Together with all the variable gender, age, eduvation,

marital status, household size, house location, join

arisan, ever having loan and being farm or

enterpreneur are affect on household income or

expenditure. We found that social activities has

negative impact specially in income. Its show that

social activities not a good way to collect capital for

household enterprise.

Because of the inaccessibility of formal

institutions, household entreprise arrange themselves

to start business with resources from their self. Other

possible mechanisms, maybe we need to put some

social cultural factor that could explain East

Indonesian Income and Expenditure, require further

research

REFERENCES

Abebe, G., Tekle, B., & Mano, Y. (2018). Changing Saving

and Investment Behaviour: The Impact of Financial

Literacy Training and Reminders on Micro-businesses.

Journal of African Economies, 27(5), 587–611.

https://doi.org/10.1093/jae/ejy007

Kementerian Koperasi dan Usaha Kecil dan Menengah.

(2015). No Title Perkembangan Data Usaha

Mikro, Kecil, Menengah (UMKM) Dan Usaha Besar

(UB) Tahun 2010 - 2015. Retrieved from

http://www.depkop.go.id/uploads/laporan/1562040307

_SANDINGAN_DATA_UMKM_2010-2015_.pdf

Pemerintah Republik Indonesia. (2008). Undang-Undang

Republik Indonesia Nomor 20 Tahun 2008. Retrieved

from https://jdih.kemenkeu.go.id/fulltext/2008/20TAH

UN2008UU.htm

SOFIA, (BPS), K. K. dan U. K. dan M. B. P. S., Ibrahim,

N., Verliyantina, Anantadjaya, S. P., Finardi, B. A., …

Intan K. P., E. (2017). The Model of Crowdfunding to

Support Small and Micro Businesses in Indonesia

Through a Web-based Platform. International Journal

of Entrepreneurship and Small Business, 4(1), 51–62.

https://doi.org/10.13189/ujaf.2017.050101

State, O. (2013). Estimating Growth In Investment Of

Micro And Small Scale Enterprises In Nigeria Ojenike

Joseph Olusola Olowoniyi Adeyemi Olusola. 3(1), 111–

123.

Wooldridge, J. M. (2002). Econometrics Analysis Of Cross

Section And Panel Data. Cambridge: MIT Press.

Wooldridge, J. M. (2003). Introductory Econometrics: A

Modern Approach 2E. Ohio: Thomson South-Western.

West Nusa Tenggara

16%

East

Kalima

ntan

11%

South

East

Sulawesi

16%

Maluku

15%

North

Maluku

13%

West

Papua

14%

Papua

15%

Social Activities Effect on Household Enterprise: A Descriptive Analysis Form East Indonesia

55

APPENDIX

Descriptive Statistic

Variable

Description

Obs

Mean

Std. Dev.

Min

Max

hhid12

0

pid12

2,310

1

0

1

1

pidlink

0

age

age

2,310

44.18095

13.09813

17

105

sex

gender 1=male

2,310

0.831602

0.374301

0

1

marstat

marital status

2,310

2.090043

0.378774

1

3

educ

years in school

2,310

7.642857

4.595098

0

18

hhsize

household member

2,310

4.221645

2.046717

1

16

lnpce

log per capita expenditure

2,310

13.48855

0.802055

10.98917

16.10149

pce

per capita expenditure

2,310

999970.9

952227

59229.16

9835334

urban

=1 urban

2,310

0.286147

0.452057

0

1

trrel

religions

2,297

1.836308

0.966885

1

5

tragm

=1 moslem

2,310

0.54329

0.49823

0

1

hos_stat

=1 house ownership

2,310

0.764935

0.424131

0

1

kegiatan

number of community

activities

2,310

3.122078

1.760396

0

9

keg_keu

number of community

activities that related to finance

activities

2,310

0.954978

0.852814

0

4

ca_fin

1 = community activities that

related to finance activities

2,310

0.663204

0.472717

0

1

arpart

=1 join arisan

2,310

0.329437

0.470111

0

1

artype

arisan type

761

1.390276

0.751392

1

8

arattd

arisan in year

760

15.65

16.46007

0

144

aravrg

arisan in month

760

1.630263

1.377929

0

12

arcon1

arisan contribution in year

758

1944914

4.118.290

8000

54,000,000

arcon2

arisan contribution in month

758

162076.2

343.190.9

666.6667

4,500,000

arrec1

arisan recieve in year

761

1769616

4156741

0

50,000,000

arrec2

arisan recieve in month

761

147468

346395.1

0

4,166,667

income

total income

2,310

24.300.000

44,800,000

15000

772,000,000

inc_labor

labor income

2,310

9.680.017

20,800,000

0

173,000,000

inc_other

other income

2,310

194.361.5

2.212.642

0

52,000,000

inc_nfarm

non farm business income

2,310

8.623.800

37,900,000

0

772,000,000

inc_farm

farm business income

2,310

5.836.482

11,100,000

0

86,200,000

own

=1 own business

2,310

0.408225

0.491612

0

1

petani

=1 own land and farmer

2,310

0.634199

0.481758

0

1

7th AICIF 2019 - ASEAN Universities Conference on Islamic Finance

56

Income as dependent variable

(1)

(2)

(3)

pendapatan

inc_farm

inc_nfarm

age

-33995.4621

-60657.6497

***

21436.6841

(63701.1089)

(18240.4239)

(61079.4576)

sex

-1095811.5620

1170550.1974

-2608242.5378

(4314354.6069)

(611220.7596)

(4347781.7993)

educ

68455.0822

-1524.9096

56056.9765

(244881.9196)

(68203.3437)

(235265.9682)

marstat

-1666741.2313

912500.9310

-2921284.5885

(4560501.4111)

(715045.2357)

(4577974.4343)

hhsize

-227124.7812

-131915.5998

-37874.7302

(416756.8085)

(114917.2182)

(406653.1027)

urban

-1151019.7199

490947.5287

-1459708.5419

(2058358.7091)

(524304.6548)

(1969800.6544)

arpart

-2671144.6908

-1183540.3107

*

-1763874.5267

(1493025.7529)

(466807.5912)

(1465285.9700)

lever

952625.9470

-1387749.0339

**

2406430.0891

(2858993.4064)

(500724.0466)

(2833040.9997)

own

17787819.1504

***

20782562.9824

***

(1845396.8136)

(1904093.0392)

petani

-2286921.7622

4047816.1860

***

(1751161.9937)

(449347.0344)

_cons

16049948.7196

4092108.7815

*

7841332.0274

(13376087.3109)

(2044517.1419)

(13108406.2593)

Number of observations

2310.0000

2310.0000

2310.0000

Number of groups

Standard errors in parentheses

*

p < 0.05,

**

p < 0.01,

***

p < 0.001

Ln PCE as dependent variable

(1)

(2)

(3)

lnpce

lnpce

lnpce

age

0.0025

*

0.0024

*

0.0024

*

(0.0011)

(0.0011)

(0.0011)

sex

0.0401

0.0395

0.0371

(0.0418)

(0.0418)

(0.0418)

educ

0.0402

***

0.0402

***

0.0401

***

(0.0035)

(0.0035)

(0.0035)

marstat

-0.0163

-0.0171

-0.0194

(0.0425)

(0.0426)

(0.0425)

hhsize

-0.1761

***

-0.1758

***

-0.1755

***

(0.0077)

(0.0077)

(0.0077)

urban

0.4019

***

0.4051

***

0.4047

***

(0.0318)

(0.0317)

(0.0318)

Social Activities Effect on Household Enterprise: A Descriptive Analysis Form East Indonesia

57

(1)

(2)

(3)

lnpce

lnpce

lnpce

arpart

0.1079

***

0.1082

***

0.1058

***

(0.0301)

(0.0300)

(0.0300)

lever

0.0788

*

0.0786

*

0.0792

*

(0.0382)

(0.0382)

(0.0382)

own

0.0379

0.0461

(0.0278)

(0.0274)

petani

-0.0486

-0.0553

*

(0.0279)

(0.0276)

_cons

13.6689

***

13.6902

***

13.6445

***

(0.1202)

(0.1193)

(0.1192)

Number of observations

2310.0000

2310.0000

2310.0000

Number of groups

Standard errors in parentheses

*

p < 0.05,

**

p < 0.01,

***

p < 0.001

7th AICIF 2019 - ASEAN Universities Conference on Islamic Finance

58