The Effect of Environmental Uncertainty and Organizational

Structure to the Quality of Management Accounting Information

Systems and It Implications to the Quality of Management

Accounting Information

Yanuar Ramadhan

1

, Novera Kristianti Maharani

1

, Ahmad Sururi Afif

1

and Rilla Gantino

1

1

Faculty of Economics and Business, Esa Unggul University, West Jakarta

Keywords: Environmental uncertainty, organizational structure, quality of management accounting information

systems, quality of management accounting information.

Abstract: The purpose of this research is to examine and analyze the influence of environmental uncertainty and

organizational structure on the quality of management accounting information system and its implications

on the quality of management accounting information. The phenomenon that occurs in some companies in

Indonesia shows that the management accounting information system at the company has not qualified so

that the impact on the quality of accounting information management. The data of this research were

obtained through a survey by distributing questionnaires to manufacturing companies in the consumer goods

industry sector listed on the Indonesia Stock Exchange. Testing data using Partial Least Square (PLS). The

research method used explanatory research method. The results showed that the environmental uncertainty

affects the quality of the management accounting information system, while the organizational structure

shows the results do not affect the quality of the management accounting information system. The

simultaneous, environmental uncertainty and organizational structure affect the quality of management

accounting information systems and implicate the quality of management accounting information.

1 INTRODUCTION

Wilkinson et al. (2000) explains that "Data are the

raw facts and figures and even the symbols that

together form the inputs to information system".

Gelinas and Dull (2008) and Stair and Reynolds

(2010) argue that the value of information is directly

related to how to help decision makers achieve

organizational goals and that valuable information

can help people and their organizations carry out

more tasks efficient and effective. As for high-

quality management accounting information

according to O'Brien and Marakas (2010), DeLone

and McLean, 1992, Gelinas and Dull (2008) is an

information product whose characteristics, attributes

or quality will help that information become

valuable to users. Related to the system, the quality

of the management accounting information system

according to DeLone and McLean (1992) is

conformity in measuring.

According to Heidmann and Schäffer (2008),

and Belkaoui (2002) states that management

accounting information systems are formal systems

that provide information from the internal and

external environment to management. In line with

the results of Chitmun and Ussahawanitchakit

research (2011) which shows that "timeliness

management accounting system has a significant

positive effect on information quality, integration of

management accounting systems has a positive

impact on information quality".

In reality in Indonesia, there is still a lack of

quality in the application of management accounting

information systems both in government and private

sectors. This was conveyed, among others, by Yudhi

Chrisnandi, Minister of Administrative Reform and

Bureaucratic Reform (2014), Karsani Aulia,

Samudra Energy's Head of Technology (2014),

Surjanto Yasaputera, Corporate Secretary, PT

Wismilak Inti Makmur Tbk. (28/02/2013), and Eka

Suharto, FFI Information and Communication

Technology Manager, PT Frisian Flag Indonesia

(27/09/2007) which stated in essence that as long as

2770

Ramadhan, Y., Kristianti Maharani, N., Sururi Afif, A. and Gantino, R.

The Effect of Environmental Uncertainty and Organizational Structure to the Quality of Management Accounting Information Systems and It Implications to the Quality of Management

Accounting Information.

DOI: 10.5220/0009952527702777

In Proceedings of the 1st International Conference on Recent Innovations (ICRI 2018), pages 2770-2777

ISBN: 978-989-758-458-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

the system not being integrated, it would cause

various problems.

Hansen and Mowen (2007) explain that the core

of management accounting information systems is

the process described by activities to produce

outputs that meet the objectives of the system.The

results study from Strumickas and Valanciene

(2010), and Ajibolade (2013) concludes that

management accounting information systems are

influenced by the external environment

(environmental uncertainty).

Management accounting information systems

also relate to organizational structure.

Organizational structure can affect management

accounting information systems as stated by Stair

and Reynolds (2010), Miyamoto (2008), and

Valanciene (2010) namely that organizational

structure can have a direct impact on organizational

information systems.

Based on the background described above, the

formulation of the problem that can be submitted is

as follows:How much influence is partially

Environmental Uncertainty and Organizational

Structure on the Quality of Management Accounting

Information Systems and how much influence does

the Quality of Management Accounting Information

System have on the Quality of Management

Accounting Information.

The purpose of this study is to obtain empirical

evidence in the field that Environmental Uncertainty

and Organizational Structure affect the Quality of

Management Accounting Information Systems and

have implications for the Quality of Management

Accounting Information. The results of this study

are intended to be able to contribute to the

development of science and also can provide

alternative solutions to problems faced by

manufacturing companies in improving the

operational quality of the company, the quality of

production, and the right decision making, and

ultimately can increase the productivity of the

company.

2 LITERATURE REVIEW

2.1 Environmental Uncertainty

Dimensions of external environmental uncertainty

according to Robbins and Coulter (2013),Duncan,

(1972) are the degree of change and the degree of

environmental complexity. While indicators of

external environment uncertainty (Robbins and

Coulter, 2013; Duncan, 1972; Gordon and

Narayanan, 1984; Mejia et al., 2005) are:

Environmental stability (Gordon and Narayanan,

1984); Changes in government regulations (Duncan,

1972); Competitor complexity (Robbins and

Coulter, 2013); Supplier complexity (Robbins and

Coulter, 2013).

2.2 Organizational Structure

The dimensions and indicators of each characteristic

of the organizational structure chosen by the

researcher are as follows: Span of Control: a.)

Communication between superiors and subordinates

(Ivancevich et al., 2014); b.) Level of supervision

(Ivancevich et al., 2014); Centralization: a.) The

level of decision making (Robbins and Coulter,

2013; b.) The level of formal authority (Robbins and

Coulter, 2013); Formalization: a.) Documentation of

procedures (Robbins and Coulter, 2013); b.) Written

regulations (Robbins and Coulter, 2013);

Departmentalization: a.) Coordination between

sections (Robbins and Coulter, 2013); b.) Task

grouping (Robbins and Coulter, 2013)

2.3 The Quality of Management

Accounting Information Systems

Dimensions and indicators of the Quality of

Management Accounting Information Systems are

as follows: Integration, consist of (a) Integration

between system components (Heidmann and

Schäffer, 2008; Azhar, 2013) and (b) Integration

between sub-components system (Azhar, 2013);

Flexibility consists of (a) Being able to adjust user

needs (Heidmann and Schäffer, 2008) and (b) Able

to adapt to changes in the environment (Heidmann

and Schäffer, 2008); Accessibility consists of (a)

Can be accessed easily (Heidmann and Schäffer,

2008; Stair and Reynolds, 2012) and (b) Can be

accessed according to the development of

information technology (Heidmann and Schäffer,

2008; Stair and Reynolds, 2012) ; Formalization:

Following the rules and conditions that apply

(Heidmann and Schäffer, 2008), and Media

Richness consists of (a) Using many channels that

facilitate communication (Heidmann and Schäffer,

2008) and (b) Facilitate interaction between parts

(Heidmann and Schäffer, 2008).

The Effect of Environmental Uncertainty and Organizational Structure to the Quality of Management Accounting Information Systems and

It Implications to the Quality of Management Accounting Information

2771

2.4 The Quality of Management

Accounting Information

The dimensions and indicators that can be used for

each component of the quality of management

accounting information are as follows: Relevance

(Hall, 2011); Accuracy (Laudon and Laudon, 2014);

Completeness (Laudon and Laudon, 2014) and

(Heidmann and Schäffer, 2008); Timeliness

(McLeod and Schell, 2008; Chenhall and Morris,

1986) and (Heidmann and Schäffer, 2008); Scope

(Heidmann and Schäffer, 2008) and Chenhall and

Morris, 1986); Aggregation (Chenhall and Morris,

1986)

2.5 The Influence of Environmental

Uncertainty on the Quality of

Management Accounting

Information Systems

Delivered by among others Laudon and Laudon

(2014); Wilkinson et.al. (2000); Hoque (2003);

Azhar (2013); and research by Gordon and

Narayanan (1984), Duncan (1972); Ajibolade et al.

(2010); and Nita (2008); it can be said that

environmental uncertainty affects the quality of

management accounting information systems.

2.6 The Influence of Organizational

Structure on the Quality of

Management Accounting

Information Systems

Based on opinions between Stair and Reynolds

(2010); Wilkinson et.al. (2000); Laudon and Laudon

(2014) and the results of the study include Salehi

and Abdipour (2011); Indeje and Zheng (2010);

Strumickas and Valanciene (2010) can be said that

organizational structure influences the quality of

management accounting information systems.

2.7 The Influence of Quality of

Management Accounting

Information Systems on the Quality

of Management Accounting

Information

Hall (2011), Stair and Reynolds (2012), Hansen and

Mowen (2007), Bagranoff et al. (2010), Atkinson

(2012), Xu (2003), Heidmann and Schäffer (2008),

Richardson et al. (2014) and also the results of

research from Shoommuangpak (2011), Valanciene

and Gimzauskiene (2007) can be said that the

quality of management accounting information

systems will be able to influence the quality of

management accounting information so that

decisions are made be right.

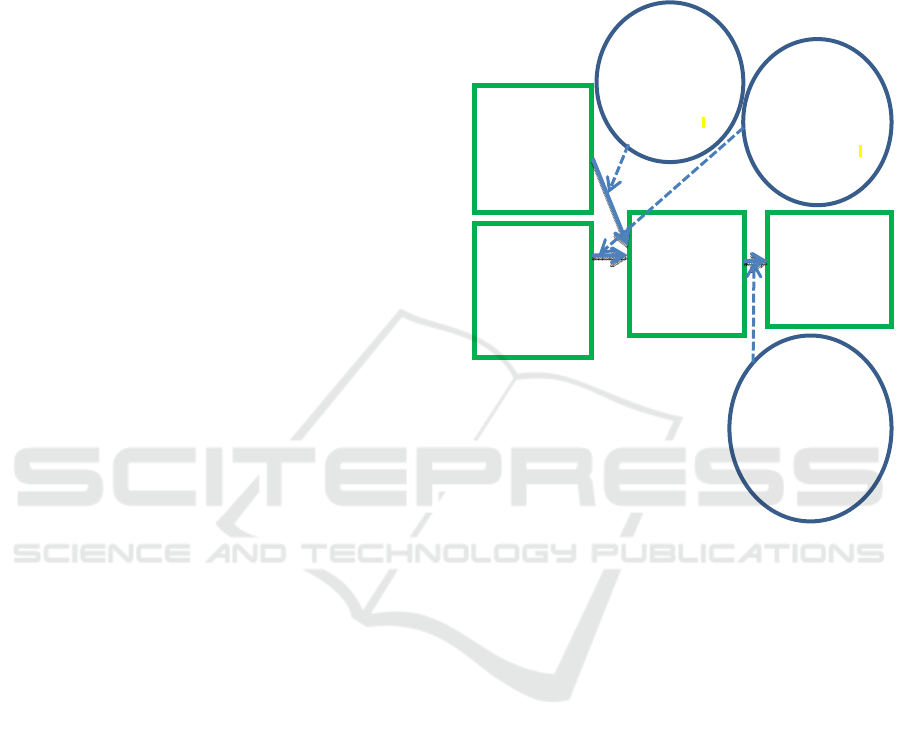

Figure 1 shows the thought framework as a basis

for submitting hypotheses.

Figure 1: Conceptual Framework

3 RESEARCH METHOD

In this study, the method used is descriptive and

explanatory research (Sekaran and Bougie, 2013).

Researchers want to get a basic answer about the

cause and effect by analyzing the causes of

phenomena in the concepts raised in the study

(Cooper and Schindler, 2014). While the indicators

in this study use an ordinal scale which is measured

based on the attitude scale using a Likert approach.

3.1 Population and Sample

Based on data from the Indonesia Stock Exchange,

in 2015 there were 511 companies including 147

manufacturing companies. Whereas those included

in the category of consumer goods industry sector

amounted to 40 companies. To test the hypothesis of

this study researchers used Structural Equation

KETIDAKPASTIAN

LINGKUNGAN (X1)

(Robbins&Coulter,

2013:77; Miles&Snow,

2003; Mejia et al., 2005;

GordonAnd Narayanan,

1984; Duncan, 1972;

Hoque, 2003)

STRUKTUR

ORGANISASI (X2)

(Mejia et al., 2005;

Robbin &Coulter, 2013;

Robbins, 2013;

McShane&Glinow, 2010;

Gibson, 2012:399;

Ivancevich, 2011)

KUALITAS SISTEM

INFORMASI

AKUNTANSI

MANAJEMEN (Y)

(Heidmann, 2008;

Hansen&Mowen, 2007;

Azhar, 2013;

Stair&Reynold, 2012;

Horngren et al. 2002)

KUALITAS INFORMASI

AKUNTANSI

MANAJEMEN (Z)

(Heidmann, 2008;

Stair&Reynold, 2012;

Atkinson, 2012;

Turban&Volonino, 2011;

McLeod and Schell, 2008)

Y terhadap Z (H3):

(Hansen&Mowen, 2007;

Stair&Reynolds, 2012;

Hall, 2011; Xu, 2003;

Atkinson, 2012;

Bagranoff et al., 2010;

Laudon&Laudon, 2014;

Shoommuangpak, 2011;

Heidmann, 2008)

X1 terhadap Y (H1):

(Wilkinson et al, 2000;

Laudon dan Laudon,

2014;

Azhar, 2013; Hoque,

2003; Haldma andLaats,,2

0

Nita, 2008;

Ajibolade et al., 2010)

X2 terhadap Y (H2):

(Stair dan Reynolds,

2010; Laudon & Laudon,

2014; Wilkinson, 2000;

Strumickas, 2010;

Salehi&Abdipour, 2011)

ICRI 2018 - International Conference Recent Innovation

2772

Modeling (SEM) with Partial Least Square (PLS)

estimation.

3.2 Method of Collecting Data

Data collection method used in this study is to use a

questionnaire method, provide direct questionnaires

or postal self-administered questions or via e-mail

(internet survey).

3.3 Data Testing Method

Data collection is done using a questionnaire.

Therefore, to test the sincerity of the respondent's

answer, two types of tests are needed: a test of

validity and test of reliability. Testing is done in data

analysis using SEM.

3.4 Analysis Design and Hypothesis

Test

3.4.1 Analysis Design

Two types of analysis were carried out to obtain

results that were consistent with the objectives of the

study, namely descriptive analysis and analysis

through Structural Equation Model (SEM).

3.4.2 Model Evaluation

The model in structural equation modelling through

the partial least square (PLS) approach consists of

two types, namely the measurement model

suitability test (outer model) and the structural

model suitability test (inner model).

4 RESULTS AND DISCUSSION

4.1 Descriptive Analysis

Based on the calculation of the outer loadings value,

all indicators of each construct have Loading Factor

above 0.5 said to be valid. The value of composite

reliability (CR) of each construct is reliable because

its value is above 0.7. All constructs have good

convergent validity because they have AVE values

above 0.5.

The discriminant validity evaluation results

which are seen from the cross loading value

concluded that the construct of Environmental

Uncertainty (EU) and Quality of Management

Accounting Information System (MAIS)

discriminates its good validity. The construct of

Organizational Structure (ORGSTR) and Quality of

Management Accounting Information (MAI)

discriminates its validity less well.

Subsequent evaluation of discriminant validity

shows the construct AVE root value Environmental

Uncertainty, Organizational Structure, and Quality

of Management Accounting Information System is

greater than the maximum correlation with other

constructs so that it can be said discriminant validity

is good because AVE root value must be higher than

the correlation between constructs.

4.2 Model Evaluation Structural

The complete relationship between variables in this

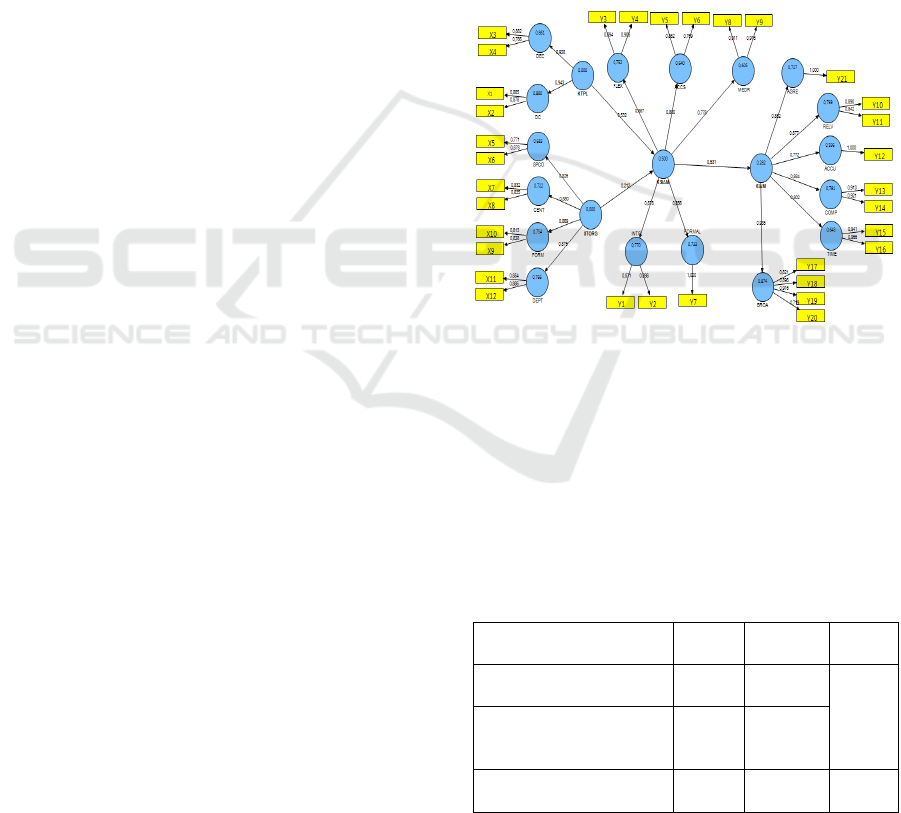

study can be explained as shown in Figure 2.

Figure 2:Model of the influence of Environmental

Uncertainty and Organizational Structure on Quality of

Management Accounting Information through Quality

Management Accounting Information Systems

Testing of the structural model is done by testing the

significance of each parameter by comparing the t-

statistic value with t table (at 5% significance level),

then looking at the R-square value which is a

goodness-fit test model.

Table 1: Parameter Coefficient

λ

T-

Statistic

R-

square

Organizational Structure

->MAIS Quality

0.212 1.334

0.500

Environmental

Uncertainty ->MAIS

Quality

0.532 3.473

MAIS Quality ->MA

Information Quality

0.531 4.566 0.282

**significant at the level 0.05, t

table

= 1.96

The Effect of Environmental Uncertainty and Organizational Structure to the Quality of Management Accounting Information Systems and

It Implications to the Quality of Management Accounting Information

2773

Based on Table1, MAISQ = 0.212 ORGST + 0.532

EU + 0.500 and MAIQ = 0.531 MAISQ + 0.718

The parameter coefficient of Organizational

Structure and Environmental Uncertainty on the

Quality of Management Accounting Information

System is positive. This means that the

Organizational Structure and Environmental

Uncertainty can improve the Quality of Management

Accounting Information Systems. If the

Organizational Structure increases by 1 unit, it will

improve the Quality of Management Accounting

Information System by 0.212 and if the

Environmental Uncertainty increases by 1 unit, it

will improve the Quality of Management

Accounting Information System by 0.532. R square

value of 0.532 indicates that the Organizational

Structure and Environmental Uncertainty can

explain the Quality of Management Accounting

Information System constructs by 50.0%, the

remaining 50.0% is explained by other constructs in

addition to Organizational Structure and

Environmental Uncertainty. Parameter coefficient of

Management Accounting Information System

Quality variable on Management Accounting

Information Quality variable is positive. This means

that the Quality of the Management Accounting

Information System can improve the Quality of

Management Accounting Information. If the Quality

of the Management Accounting Information System

increases by 1 unit, it will improve the Quality of

Management Accounting Information by 0.531. R

square value of 0.282 indicates that the Quality of

Management Accounting Information System can

explain Management Accounting Information

Quality variables of 28.2%, the remaining 71.8% is

explained by other constructs other than Quality of

Management Accounting Information Systems. Next

to see the effect of each variable partially and

simultaneously obtained the following results:

Table 2: Partial Test of Environmental Uncertainty on

MAIS Quality

λ T-Statistic

Environmental Uncertainty

->MAI Systems Quality

0.532 3.473

Based on Table 2, it is obtained a statistical t

value of 3.473. Because the value of t statistic is

greater than t table (t table with a significance of 5%

at 1.96), then it gives a significant conclusion that

there is a significant influence of Environmental

Uncertainty on the Quality of Management

Accounting Information Systems.

Table 3: Partial Test of Organizational Structure on MAI

Systems Quality

λ T-Statistic

Organizational Structure ->

MAI Systems Quality

0.212 1.334

Based on Table 3, the statistical t value is 1.334.

Because the t value of statistics is smaller than t

table (t table with a significance of 5% at 1.96), then

it gives a non-significant conclusion, meaning there

is no significant influence from the Organizational

Structure on the Quality of Management Accounting

Information Systems.

Table 4: Partial Test of MAI Systems Quality on MAI

Quality

λ T-Statistic

MAI Systems Quality -

>MAI Quality

0.531 4.566

Based on Table 4, the statistical t value is 4.566.

Because the value of t statistic is greater than t table

(t table with a significance of 5% at 1.96), then it

gives a significant conclusion which means that

there is a significant influence of the Quality of

Management Accounting Information System on the

Quality of Management Accounting Information.

Table 5: Simultaneous Test, Environmental Uncertainty

and Organizational Structure on the Quality of

Management Accounting Information Systems

R

2

F

Environmental Uncertainty and

Organizational Structure -

>Quality of Management

Accounting Information Systems

0.500 31.000

Through test statistics with = 5% and df1 = k = 3,

df2 = n-k-1 = 65-2-1 = 62 obtained F table value of

± 3,145.

Based on the following test criteria: Accept Ho if

F counts <F table and Reject Ho if F counts> F

table. Based on the data in Table 5, it can be

obtained the Fcount value of 31,000. Because the F

value is calculated (31,000)> F table (3,145), then

Ho is rejected. That is, the Organizational Structure,

and Environmental Uncertainty have a significant

effect jointly on the Quality of Management

Accounting Information Systems.

ICRI 2018 - International Conference Recent Innovation

2774

Table 6: Direct Influences

Path

Coefficient

Direct

Influences

Total

Influences

Environmental

Uncertainty–

MAIS Quality

0.532 0.283 28.35%

Organizational

Structure–MAIS

Quality

0.212 0.045 4.5%

MAIS Quality –

Management

Accounting

Information

Quality

0.531 0.282 28.2%

From Table 6 can be seen that the total effect of

Environmental Uncertainty on the Quality of the

Management Accounting Information Systems is

28.35%, and the total influence of the Organizational

Structure on the Quality of Management Accounting

Information Systems is 4.5%; and the total effect of

the total influence of the Quality of the Management

Accounting Information System on the Quality of

Management Accounting Information at 28.2%.

5 CONCLUSIONS

Based on the discussion and analysis related to the

phenomenon, the formulation of the problem,

hypothesis, and the results of the study concluded, as

follows:

a. Environmental uncertainty affects the quality of

management accounting information systems.

Thus the company's ability to anticipate/follow

up on any changes related to the level of

environmental change, such as environmental

stability and changes in government regulations.

The company has also been able to anticipate the

complexity of the environment, for example

against competitors and suppliers.

b. Organizational Structure does not affect the

quality of management accounting information

systems. The quality of the management

accounting information system in the company is

not yet high due to the high span of control, the

low communication between superiors and

subordinates, and the low coordination between

sections.

c. The quality of the management accounting

information system affects the quality of

management accounting information. Thus the

consumer goods industry sector manufacturing

companies listed on the IDX have implemented a

quality management accounting information

system, so as to meet the needs of stakeholders.

Based on the results of the research and discussion

and conclusions in this study, it is recommended:

a. Submission of information to management on

environmental changes that occur, for example,

changes made by competitors, suppliers,

customers, government regulations.

b. Improvement in the organization so that the

company has a structure that can facilitate

supervision, direct communication or through

technological devices, and coordination between

parts in processing data becomes information so

that the decision making the process by

management can be made appropriately.

c. Increase flexibility in management accounting

information systems, such as the ability to adjust

to user needs so as to produce quality

information and also improve the ability of the

system to adapt to changing situations and

conditions

d. Increase the accuracy of management accounting

information which will ultimately be taken into

consideration in management decisions.

e. Perform replicability and generalibility, it is

recommended for other researchers to conduct

research again based on the results of this study

using the same research method, in different

units of analysis and samples.

f. Other researchers are expected to examine other

variables such as company strategy, manager

competence, organizational culture, management

changes, ethics, and others.

REFERENCES

Ajibolade, S. O. (2013). Management accounting systems

design and company performance in Nigerian

manufacturing companies: A contingency theory

perspective. British Journal of Arts and Social

Sciences, 14(2): 228-244.

Ajibolade, S. O., Arowomole, S. S. A., & Ojikutu, R. K.

(2010). Management Accounting Systems, Perceived

Environmental Uncertainty And

Companies'Performance In Nigeria. International

Journal of Academic Research, 2(1).

Atkinson, A.A., Kaplan, R.S., Matsumura, E.M., and

Young S.M. (2012). Akuntansi Manajemen. 5

th

edition. Indeks Publisher.

Azhar,S. (2013).Sistem Informasi Akuntansi, Struktur-

Pengendalian-Resiko-Pengembangan. Bandung:

Lingga Jaya Publisher.

The Effect of Environmental Uncertainty and Organizational Structure to the Quality of Management Accounting Information Systems and

It Implications to the Quality of Management Accounting Information

2775

Bagranoff, N.A., Simkin, M.G., and Norman, CS. (2010).

Core concepts of: Accounting Information Systems.

Eleventh Edition. John Wiley & Sons, Inc.

Belkaoui, A. (2002). Behavioral management accounting.

Greenwood Publishing Group.

Chenhall, R. H., and Morris, D. (1986). The impact of

structure, environment, and interdependence on the

perceived usefulness of management accounting

systems. Accounting Review, pp. 16-35.

Chitmun, S., and Ussahawanitchakit, P. (2011).

Management Accounting Systems Sophistication and

Decision Making Performance. Journal of Academy of

Business and Economics, 11(3).

Cooper, D.R., and Schindler, P.S. (2014). Business

Research Methods, Twelfth edition. The McGraw-Hill

Companies, Inc.

DeLone, W. H., and McLean, E. R. (1992). Information

systems success: The quest for the dependent variable.

Information systems research, 3(1): 60-95.

Duncan, R.B. (1972). The Effects of Perceived

Environmental Uncertainty on Organizational

Decision Unit Structure: A Cybernetic Approach,

Unpublished Ph.D. dissertation, Yale University, New

Haven, Connecticut.

Eka, S. (2007). Kecanggihan Di Balik Manisnya Susu

Bendera. Available at:http://swa.co.id/listed-

articles/kecanggihan-di-balik-manisnya-susu-bendera.

27/09/2007

Gelinas, U.J., and Dull, RB. (2008). Accounting

Information Systems, 7th Edition. Thomson South-

Western.

Gordon, L. A., and Narayanan, V. K. (1984). Management

accounting systems, perceived environmental

uncertainty and organization structure: an empirical

investigation. Accounting, organizations and society,

9(1): 33-47.

Haldma, T., and Lääts, K. (2002). Influencing

Contingencies On Management Accounting Practices

In Estonian Manufacturing Companies–University of

Tartu, Faculty of Economics and Business

Administration, 13: 41.

Hall, J.A. (2011). Accounting Information Systems, 7th

Edition, South-Western, Cengage Learning.

Hansen, D.R., and Mowen, M.M. (2007). Managerial

Accounting, 8th Edition. Cengage Learning.

Heidmann, M. (2008). The role of management

accounting systems in strategic sensemaking.

Wiesbaden: Deutscher Universitäts-Verlag.

Hoque, Z. (2003). Strategic Management Accounting–

Concepts, Processes, and Issues, Second Edition.

Horngren, C. T., Sundem, G. L., Stratton, W. O.,

Burgstahler, D., and Schatzberg, J. (2002).

Introduction to Management Accounting: Chapters 1-

19. Prentice Hall.

Indeje, W. G., and Zheng, Q. (2010, September).

Organizational culture and information systems

implementation: A structuration theory perspective. In

InIEEE International Conference on Information and

Financial Engineering Chongqing-China, pp.17-19.

Ivancevich, J.M., Konopaske, R., and Matteson, MT.

(2011). Organizational Behavior and Management.

Nineth Edition.

Ivancevich, J.M., Konopaske, R., and Matteson, MT.

(2014). Organizational Behavior and Management.

Tenth Edition.

Karsani, A. (2014). Penemuan Migas di Indonesia Timur

Terganjal Data. Available

at:http://www.tempo.co/read/news/2013/06/19/090489

623/ Penemuan-Migas-di-Indonesia-Timur-Terganjal-

Data.

Laudon, K. C., and Laudon, J. P. (2009). Essentials of

management information systems. Upper Saddle

River: Pearson.

Laudon, K. C., and Laudon, J. P.(2014). Management

Information Systems (Managing the Digital Firm).

Thirteenth Edition.

McLeod, R.Jr., and Schell, GP. (2008). Sistem Informasi

Manajemen, 10th edition. Salemba Empat.

McShane and Glinow, V. (2010). Organizational

Behavior. Emerging Knowledge and Practice for the

Real World, Fifth Edition. McGraw-Hill.

Mejia, L.R.G., Balkin, D.B., and Cardy, R.L.(2005).

Management,Second Edition. McGraw-Hill.

Miles, R.E., and Snow, CC.(2003). Organization Strategy,

Structure and Process. Stanford Business Books

California.

Miyamoto, K. (2008). International Management

Accounting in Japan: Current Status of Electronics

Companies, 4. World Scientific.

Nita, B. (2008). Transformation of Management

Accounting: From Management Control to

Performance Management. Transformations in

Business & Economics, 7(3):53.

O’Brien, J.A., and Marakas G. M. (2010). Introduction to

Information Systems,Fifteenth Edition. The McGraw-

Hill Companies, Inc.

Richardson, V., Chang, J., and Smith, R. (2014).

Accounting Information System. McGraw-Hill

International Edition.

Robbins, S.P. and Coulter, M.(2013). Management,

Eleventh Edition. Pearson Education Limited.

Salehi, M., and Abdipour, A. (2011). A study of the

barriers of implementation of accounting information

system: Case of listed companies in Tehran Stock

Exchange. Journal of Economics and Behavioral

Studies, 2(2): 76-85.

Sekaran, U. and Bougie, R. (2013). Research Methods for

Business. A Skill-Building Approach., Sixth Edition.

John Wiley & Sons Ltd.

Shoommuangpak, P. (2011). Effectiveness of management

accounting implementation, decision making quality

and performance: an empirical study of thai-listed

firms. International Journal of Business Strategy,

11(1): 197-209.

Stair, R.M., and Reynolds, G.W. (2010). Principles of

Information Systems,Ninth Edition. Course

Technology, Cengage Learning.

ICRI 2018 - International Conference Recent Innovation

2776

Stair, R.M., and Reynolds, G.W. (2012). Fundamentals of

Information Systems,Sixth Edition. Course

Technology, Cengage Learning.

Strumickas, M., and Valanciene, L. (2010). Development

of Modern Management Accounting System.

Engineering Economics, 21(4): 377-386.

Surjanto, Y. (2013). Sistem ERP SAP Tingkatkan

Performa PT Wismilak Inti Makmur, Tbk. Available

at:http://www.metrodata.co.id/read-press-

release/sistem-erp-sap-tingkatkan-performa-pt-

wismilak-inti-makmur--tbk/200. 28/02/2013

Turban, E., and Volonino, L. (2011). Information

Technology for Management -Improving Strategic and

Operational Performance, 8th Edition. John Wiley &

Sons, Inc.

Valančienė, L., & Gimžauskienė, E. (2007). Changing role

of management accounting: Lithuanian Experience

case studies. Engineering Economics, 55(5).

Wilkinson, J.W., Cerullo, M.J., Raval, V., and Wong, B.

(2000). Accounting Information Systems: Essential

Concepts and Application, Fourth Edition. John &

Sons. Inc.

Xu, H. (2003). Critical success factors for accounting

information systems data quality (Doctoral

dissertation, University of Southern Queensland).

Yudhi, C. (2014). Uang Sebesar Rp 14 Triliun Habis di

Sektor IT Tanpa Ada Integrasi. Available

at:http://wartaekonomi.co.id /news/get_news_by_id/

38420/ menteri-yudhi-uang-sebesar-rp-14-triliun-

habis-di-sektor-it-tanpa-ada-integrasi. 23 November

2014.

The Effect of Environmental Uncertainty and Organizational Structure to the Quality of Management Accounting Information Systems and

It Implications to the Quality of Management Accounting Information

2777