Evaluation the Effectiveness of Audit Design and Implementation in

Sub-cycle Procurement Information System: Case Study in PT. X

Rynaldo Jeremy Hamonangan

Magister Akuntansi, Pascasarjana Universitas Indonesia, Jl. Salemba Raya Nomor 4, Jakarta

Keywords: Effectiveness, Audit Design, Audit Implementation, COBIT 5, 3 Lines of Defense

Abstract: This research is based on the problem found in procurement sub-cycle information system that is access

violation, delay and wrong in decision making and lots of goods and services are excluded from cost

recovery calculation by government. This research is aim to evaluate the effectiveness of audit design and

implementation in sub-cycle procurement information system. This research is qualitative research. This

research method is case study. The research subject was PT. X (oil and gas company) and Department

Internal Audit and Compliance as an analysis unit. The sample was audit program in 2017. Research

instrument are interview and documentation. The result showed that audit design is not effective but audit

implementation is effective. The audit design is not effective because the same problem often occurs even

though internal auditor has conducted an audit and provide recommendation that has been implement by

management. Therefore, audit program cannot effect achievement of internal auditor objective that is to add

value and improve organization process to accelerate achievement of company objective (strategic,

operations, reporting and compliance). The main cause of the ineffective audit design is internal auditor not

perform all role according to COBIT 5 framework and doing the wrong role according to 3 lines of defense

framework, so that, internal auditor cannot identify the significant risk and root of problem. Therefore, this

research provides the design of internal auditor role that complied with COBIT 5 and 3 lines of defense

framework and 7 audit program design to eliminate the problem of procurement sub-cycle information

system in PT. X.

1 INTRODUCTION

Oil and gas industry has a lot of risk that is blowout

and oil spill, expensive investment but uncertainty of

existence of oil and gas, and numerous regulations.

Especially in Indonesia, regulations depend on

contract between government and oil and gas

company. Many oil and gas company in Indonesia

hold product sharing contract with type cost

recovery. As consequence, oil and gas company

should make work program and budget and wait

authorization for expenditure documents from

government to begin buy goods and services. If the

oil and gas company not complied with government

regulations, all goods and services that has been buy

will exclude from cost recovery calculation.

The main factor of risk above is procurement

mechanism and human skill and capability who is

part of information system. Many oil and gas

company use information technology and

application (like SAP) in procurement process.

Therefore, auditor should keep up with development

of information system in order to evaluate reliability

of communication networks competently (Weber,

1999:17). But in real, from a lot of instrument

provide by framework, auditor only use maturity

level to audit the information system because

easiness (Zhang and Fever, 2013:395). According to

Gordon (1998:103), one of factor that affected

blowout in oil and gas industry is organization that is

control, planning/ organization, and audit procedure.

PT. X has many problems in procurement sub-

cycle. The problem is KPPU give sanction to PT.X

for jack-up drilling service, empty goods and

services while needed, a lot of goods and services

are excluded from cost recovery calculation, human

error, access violation on AFE Account, WBS

master, budget and recording expense, access AFE

that has been closed, not all of committee member

1108

Hamonangan, R.

Evaluation the Effectiveness of Audit Design and Implementation in Sub-cycle Procurement Information System: Case Study in PT. X.

DOI: 10.5220/0009505411081113

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 1108-1113

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

sign WP&B, access violation in making invoice, and

record asset that there is no physical existence. This

problem has been identified by internal auditor and

audit has been performed. Internal auditor has given

recommendation and management has been doing

the recommendation. But the same problem always

occurs in next interim and next year.

2 METHODOLOGY

This research is qualitative research and the method

applied in this research was case study with mixed

method approached. According to Creswell in

Sugiyono (2017:404) mixed methods research is an

approach to inquiry that combines or associated both

qualitative quantitative forms of research. It involves

philosophical assumptions the use of quantitative

and qualitative approaches, and the mixing of both

approached in a study. Subject in this research was

PT. X (oil and gas company) with Department

Internal Audit and Compliance as an analysis unit.

The sample was audit program in 2017. The research

instrument was interview and documentation.

In this research to analyze the conformity of

internal auditor role with COBIT 5 framework were

use RACI chart from COBIT 5 framework and to

analyze the conformity of internal auditor role with

3 lines of defense framework were use 3 lines of

defense framework. To evaluate the effectivity of

audit design, this research divided the evaluation

into 2 categories effectiveness of audit design that is

effectivity based on criteria and effectivity based on

the effect.

Effectivity based on criteria refers criteria from

Sawyer (2006:235) and Information System Audit

and Control Association (ISACA) (2016:7, 13-15) as

an indicator and effectivity based on effect of audit

program is refers to 4 organization objective

(strategic, operations, reporting and compliance)

according to Pickett (2005:13-14) and the 4 effect of

audit information system according to Weber

(1999:11) as an indicator. To evaluate the effectivity

of audit implementation will perform with compare

all working paper with audit design (audit program).

3 RESULT AND DISCUSSION

From research that has been conducted, the result

show that internal auditor has been doing 2 from 4

roles in COBIT 5 framework that is responsible (R)

and accountable (A). But internal auditor not doing

another role that is consulted (C) and informed (I).

Internal auditor never showed his existence as a

place for management get advice and for discuss

about problem that faced by management.

Therefore, internal auditor always faced as

investigator by management. The second result is

internal auditor not complied with 3 lines of defense

framework because internal auditor actively

involved in making internal control system (1st line)

and risk management (2nd line).

For the main objective in this research that is

evaluate the effectiveness design and

implementation of audit in procurement sub-cycle

information system, this research will spread into

evaluate audit design and evaluate audit

implementation. The third result that is audit design

is complied with all criteria in Sawyer and ISACA

(effective in criteria) but not help internal auditor to

fulfil internal audit objective that is to accelerate

achievement of organization objective (strategic,

operations, reporting and compliance) so that audit

design not effective in effect/ result.

However, the effectivity of audit program is

achievement of audit program objective, which audit

program is internal auditor tool to achieve internal

audit objective that is to add value and improve

organization operation to accelerate achievement of

organization objective (strategic, operations,

reporting and compliance) as an indicator to evaluate

audit design effectiveness. Therefore, this research

conclude that audit design is not effective. The

fourth result is audit implementation is effective

because all audit program has been done while audit

is conducted.

After get the result that audit design is not

effective, this research will combine all result from

evaluate internal audit role according to COBIT 5

and 3 lines of defense to know what the root of

problem that cause audit design is not effective. The

result is audit design not effective because internal

auditor not perform all role according to COBIT 5

and wrong doing role according to 3 lines of

defense, internal auditor cannot identify significant

risk, weakness control that should be audited,

determination of audit objective and subject audit for

interview (All of this process is before internal

auditor writes the audit program (designing audit)).

This result is aligned with Sawyer (2006:217)

that said one of the function of audit internal

professional is to show that the program is effective-

only emphasize to significant things and to give

evidence that significant risk and control has been

identified and evaluated.

Furthermore, Sawyer (2006:217) said that

analysis that made with help from operational

manager- can give operational objective, identified

Evaluation the Effectiveness of Audit Design and Implementation in Sub-cycle Procurement Information System: Case Study in PT. X

1109

actual or potential risk, and determine the right

control for this situation. That analysis can produce

thoughtful, relevant, effective and economics audit

program.

Therefore, this research gave 2 output to improve

effectiveness of audit design that is the internal

auditor role that conform with COBIT 5 and 3 lines

of defense framework and 7 audit program to solve

the root of problem that identified in this research.

The role of internal auditor for Department

Internal Audit and Compliance is divided into 2

major that is role in governance and role in

management. The role of internal auditor in

governance is internal auditor should act as place of

management to ask about job allocation,

responsibility and management act in monitoring IT

and internal auditor should act as place of

management to ask about operation of information

system that is use and allocation of resource,

satisfied stakeholder need and risk management on

IT. The role of internal auditor in management is

actively act as consultant in project management,

requirement management and IT operation.

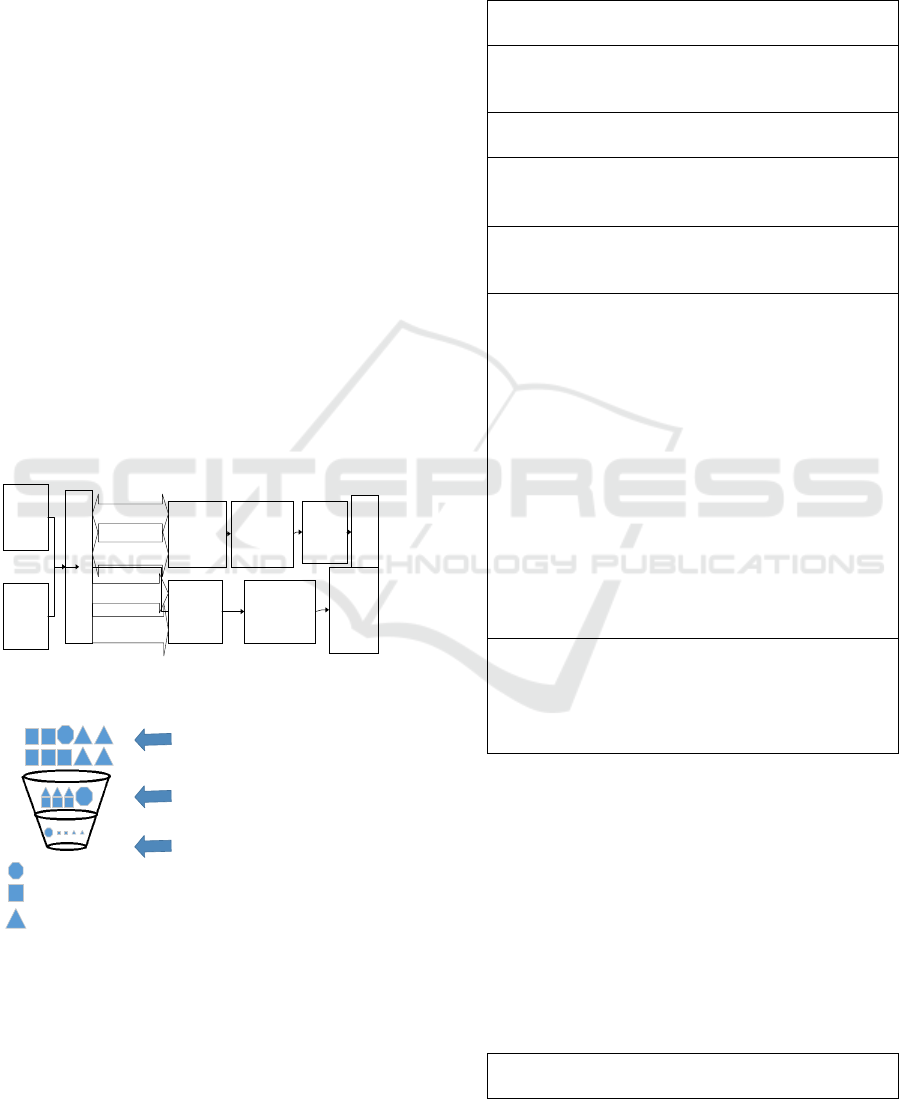

This figure below, describes the suggested

internal auditor’s role (figure 1) and the expected

effect of implementation of the role of internal

auditor that has suggested (figure 2):

COBIT 5

3 LINES OF

DEFENSE

INTERNAL AUDITOR

OPERATIONAL

MANAGEMENT

AND RISK

MANAGEMENT

AUDIT

DESIGN

(AUDIT

PROGRAM)

RISK

REDUCE

REDUCE RISK

BELOW RISK

TOLERANCE

CONSULTED

INFORMED

ACCOUNTABLE

RESPONSIBLE

BUILD INTERNAL

CONTROL AND

RISK

MANAGEMENT

EFFECTIVITY IN

DETERMINE

SIGNIFICANT

RISK

INTERNAL

CONRTOL

Figure 1: Role of Internal Auditor

= Strategic Risk

= Operational Risk

INTERNAL CONTROL THAT

BUILD BY MANAGEMENT AND

RISK MANAGEMENT

AUDIT PROGRAM BUILD BY

INTERNAL AUDITOR THAT

MORE FOCUS ON SPECIFIC

RISK AND STRATEGIC RISK

RISK APETITE DAN RISK

TOLERANCE

= Operational Risk

Figure 2: The Effect which were Expected from

Implementation the Role of Internal Auditor

The audit program in this research contain 7 audit

program that disembogue into 3 part that is:

1) Audit design for data redundancy

To solve wrong and delay in decision making

problem. There is 1 audit design (audit program) for

audit data redundancy, that is:

Table 1: Audit Design (Audit Program) for Data

Redundancy

AUDIT PROGRAM FOR DATA

REDUNDANCY

Audit Ob

j

ective:

To ensure control adequacy to mitigate data

redundanc

y

Time:

Interim 1

Risk:

1) Wrong in decision making

2) Delay in decision making

Control:

Memory capacity is allocate for each

department

Test:

1) Inspect standard operating procedure (SOP)

and compare with how end user using

worksheet

2) Take a sample of data redundancy and

identify who is updating the data redundancy

3) Inspect and compare all data redundancy (see

the data content and what the difference in

content of each data)

4) Compare all data redundancy with data that

has been attached in SAP (see the content

and compare the difference)

5) Discuss, confirm and ask to the user (data

owner and data updater) for the reason of

why data redundancy

Document:

1) Worksheet in Department Supply Chain

Management (procurement sub-cycle)

memory

2) Worksheet that has been attached in SAP

2) Audit design for database goods and services

To solve ordering goods and services that not

needed, ordering to not qualified supplier even

though supplier approved by SKK Migas, goods and

services are exclude from cost recovery calculation

by government and recorded goods that no physical

existence. There is 2 audit design (audit program)

for audit database goods and services, that is:

Table 2: Audit Design (Audit Program) for Goods

and Services Database

AUDIT PROGRAM FOR GOODS AND

SERVICES DATABASE

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1110

Audit Ob

j

ectives:

To ensure control adequacy to mitigate

purchase requisition for goods and services that

not needed.

Time:

Interim 1

Risk:

Purchase requisition for goods and services

that not needed

Control:

Access control

Test:

1) Compare all goods and services catalog with

physic of goods and services

2) Check addition or changes of catalog

parameter or catalog itself

3) Compare changes or addition of catalog

parameter or catalog itself with purchase

requisition (focus on time of occurrence)

4) Check log and see the person who makes

changes or addition on catalog parameter or

catalog itself

5) Re-performance:

a) Make a changes on catalog or catalog

parameter and makes purchase requisition

b) Make an addition on catalog or catalog

parameter and makes purchase requisition

6) Inspect all document of parameter catalog

Document:

1) Record or documentation of changes or

addition on catalog or catalog parameter

2) Record of purchase requisition time

3) Documentation of purchase requisition time

4) Log record of changes or addition on catalog

or catalog parameter

5) Log record of access to goods and services

database

Table 3: Audit Design (Audit Program) for Supplier

Database

AUDIT PROGRAM FOR SUPPLIER

DATABASE

Audit Ob

j

ective:

1) To ensure control adequacy to mitigate

purchasing goods and services that cannot

include in cost recovery calculation

2) To ensure control adequacy to mitigate

purchasing to unqualified supplier even

though the supplier approved by SKK Migas.

Time:

Interim 1

Risk:

1) Purchase goods and services that cannot

include in cost recovery calculation

2) Purchase to unqualified supplier even though

the supplier approved by SKK Migas.

Control:

1) Access

2) Authorization

Test:

1) Obtain purchase requisition (PR) and

purchase order (PO) document.

2) Compare purchase requisition (PR) and

purchase order (PO) document.

3) Check log to know who make purchase order

(PO) document

4) Inspect supplier parameter document and

compare with parameter in supplier database

5) Check log of changing in supplier database

parameter

6) Take a sample (focus on big and small

supplier) and compare supplier qualification

with parameter in database

7) Re-performance:

a) Input supplier name that you want to win

with not changing the parameter

b) Input supplier name that you want to win

with changing the parameter

Document:

1) Supplier parameter

2) List of SKK migas supplier

3) Log list of changing in database supplier

parameter

4) Supplier pra-qualification document

5) Purchase requisition (PR) document

6) Purchase order (PO) document

3) Audit design for administration role in SAP

To solve access violation problem. There is 4 audit

design (audit program) for audit administration role

in SAP, that is:

Table 4: Audit Design (Audit Program) for SAP

Support SOP

AUDIT PROGRAM FOR SAP

SUPPORT SOP

Audit Ob

j

ective:

To know the procedure of giving advice for

updatin

g

role in SAP

Time:

Interim 1

Risk:

There is a person who have 2 or more roles

in SAP

Control:

Segregation of duties

Control:

1) Inspect SOP of SAP Support in a process to

Evaluation the Effectiveness of Audit Design and Implementation in Sub-cycle Procurement Information System: Case Study in PT. X

1111

giving advice for updating role

2) Observe the evaluation mechanism in

determine the suitable role

Document:

SOP of SAP Support in giving advice for

updating role

Table 5: Audit Design (Audit Program) for SAP

Security Admin SOP

AUDIT PROGRAM FOR SAP

SECURITY ADMIN SOP

Audit Ob

j

ective:

To know the role updatin

g

process

Time:

Interim 1

Risk:

SAP Security Admin forget to revoke old

role

Control:

Se

g

re

g

ation of duties

Control:

1) Inspect SOP of SAP Security Admin in

updating role

2) Observe updating role process

Document:

SOP of SAP Security Admin in updating

role

Table 6: Audit Design (Audit Program) for

Information System and SAP Development,

Expansion and Maintenance Documentation

AUDIT PROGRAM FOR

INFORMATION SYSTEM AND SAP

DEVELOPMENT, EXPANSION AND

MAINTENANCE DOCUMENTATION

Audit Ob

j

ective:

1) To know information system access error

2) To know information system fault that can

infiltrated by parties outside the company

3) To detect and prevent the using of double

role because of the faulty of SAP Support

and SAP Security Admin

4) To know the existence of SAP Administrator

Time:

Interim 1

Risk:

Access that not conform with function and

p

osition but authorized by SAP

Control:

Access

Test:

1) Inspect development, expansion and

maintenance documentation

2) Try to access from every information system

network

3) Check the existence of SAP Administrator

function

Document:

1) Information system and SAP development

documentation

2) Information system and SAP expansion

documentation

3) Information system and SAP maintenance

documentation

Table 7: Audit Design (Audit Program) for SAP

Administrator SOP

AUDIT PROGRAM FOR SAP

ADMINISTRATOR SOP

Audit Ob

j

ective:

To ensure that SAP Administrator has gave

the control adequacy for all access in company

information system network (SAP)

Time:

Interim 2

Risk:

Access that not conform with function and

p

osition but authorized b

y

SAP

Control:

Se

g

re

g

ation of duties

Test:

1) Check SOP of SAP Administrator

2) Observe SAP Administrator Activity

3) Compare SOP with observation result of

SAP Administrator activity

Document:

SOP of SAP Administrator

4 CONCLUSIONS

According to research that has been conducted, the

conclusion is audit design is not effective but audit

implementation is effective. The problem that cause

audit design is not effective is internal auditor not

doing all role according to COBIT 5 (only

responsible and accountable but not consulted and

informed) and wrong doing role according to 3 lines

of defense (internal auditor actively involved in

make internal control system and risk management).

This problem make internal auditor cannot identify

significant risk and root of the problem in a process

to design audit (audit program).

REFERENCES

Gordon, Rachael P. (1998). The contribution of human

factors to accidents in the offshore oil industry.

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

1112

Reliability Egineering and System Safety 61 (95-

108)

Information System Audit and Control Association.

(2016). Information System Auditing: Tool and

Techniques Creating Audit Program

___________________________________________.

(2014). Assessment Programme

___________________________________________.

(2012). COBIT 5 Enabling Process

___________________________________________.

(2012). COBIT 5 Implementation

___________________________________________.

(2012). COBIT 5 A Business Framework for the

Governance and Management of Enterprise IT

Pickett, K.H. Spencer. (2005). Auditing the Risk

Management Process. New Jersey: John Willey &

Sons, Inc

Sawyer, Lawrence B. et al. (2006). Sawyer’s Internal

Auditing Audit Internal Sawyer (Desi Adhariani,

Penerjemah) (Edisi 5) (Buku 1). Jakarta: Salemba

Empat

______________________. (2006). Sawyer’s Internal

Auditing Audit Internal Sawyer (Desi Adhariani,

Penerjemah) (Edisi 5) (Buku 2). Jakarta: Salemba

Empat

______________________.(2006). Sawyer’s Internal

Auditing Audit Internal Sawyer (Ali Akbar,

Penerjemah) (Edisi 5) (Buku 3). Jakarta: Salemba

Empat

Sugiyono. (2017). Metode Penelitian Kombinasi (Mixed

Method). Bandung: Alfabeta

Weber, Ron. (1999). Information System Control and

Audit. New Jersey: Prentice Hall

Zhang, Shengnan & Hans Le Fever. (2013) An

Examination of Practicability of COBIT Framework

and the Proposal of a COBIT-BSC Model. Journal

of economics, Business and Management, 1 (4)

Evaluation the Effectiveness of Audit Design and Implementation in Sub-cycle Procurement Information System: Case Study in PT. X

1113