Corporate Social Responsibility is Viewed from a Contingency

Perspective

Danri Toni Siboro

1

, Audrey M. Siahaan

1

, Iskandar Muda

2

and Syafruddin Ginting

2

1

Student Postgraduate, Faculty Economic and Business, Universitas Sumatera Utara, Medan Indonesia

2

Lecture Faculty Economic and Business, Universitas Sumatera Utara, Medan Indonesia

Keywords: Stakeholder Theory, Contingency Theory, Corporate Social Responsibility (CSR)

Abstract: Corporate Social Responsibility is a corporate social responsibility to stakeholders where the company is

part of the social environment. Corporate Social Responsibility must achieve balance or must be able to

integrate from the start of environmental economics and social issues at the same time can provide and meet

the expectations of shareholders and stakeholders. So, the company has a responsibility to the corporate

environment. Most companies do only corporate social responsibility voluntarily. Contingency theory is a

theory that adjusts leaders to the right conditions. Contingency theory argues that leader performance is

determined from his understanding of the situation in which they lead. Managers sometimes lack

understanding of the mindset rather than Corporate social responsibility. This study uses a literature study to

see how CSR is viewed from contingency theory. From the analysis, it can be concluded that CSR with

company performance occurs in differences of opinion. There are researchers who claim that the

implementation of CSR is determined by industry partnerships, the role of government, and managerial

incentives. The implementation of corporate social responsibility in the company must be freed from short-

term goals. Corporate social responsibility does not directly have an impact on improving financial

performance.

1 INTRODUCTION

The phenomenon of Corporate Social Responsibility

(CSR) is often a very phenomenon issue; among

companies in Indonesia. In Indonesia corporate

social responsibility is required by law. This is

indicated by the issuance of the Limited Liability

Company Law (UU PT) No. 40 Article 74 of 2007

and entered into force on August 16, 2007. For

companies that go public in Indonesia regulations

regarding social and environmental responsibility

are regulated by the Financial Services

Authorization in OJK Regulation No. 29 / POJK.04 /

2016 concerning annual reports Issuer or public

company. Corporate Social Responsibility Practices

in Indonesia only aim to fulfill the obligations of the

OJK, impose sanctions, a portion of funds and

business interests. The implementation of Corporate

Social Responsibility should have meaning, the

ongoing implementation, the value of the Corporate

Social Responsibility, the goal of sustainable

implementation rather than Corporate Social

Responsibility.

Companies in Indonesia only view Corporate

Social Responsibility as a tool to obtain foreign

funds that are not subject to taxes and other

regulatory obligations. The company has many

objections to the implementation of Corporate Social

Responsibility because the implementation of

Corporate Social Responsibility will impose

company budgets. The implementation of Corporate

Social Responsibility in the company is only limited

to absurd statements or principles that will not be

able to function to solve various social and business

environment problems.

Basically, Corporate Social Responsibility is an

ongoing commitment from the company's business

that acts ethically and contributes to the economic

development of the local community or the wider

community, along with improving the standard of

living of the people around them. Corporate Social

Responsibility must achieve balance or must be able

to integrate from the start of environmental

Siboro, D., Siahaan, A., Muda, I. and Ginting, S.

Corporate Social Responsibility is Viewed from a Contingency Perspective.

DOI: 10.5220/0009499109730977

In Proceedings of the 1st Unimed International Conference on Economics Education and Social Science (UNICEES 2018), pages 973-977

ISBN: 978-989-758-432-9

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

973

economics and social issues at the same time can

provide and meet the expectations of shareholders

and stakeholders.

In Indonesia, a business will be seen as

implementing Corporate Social Responsibility only

for companies engaged in mining or companies

related to Natural Resources, while companies that

do not manage Natural Resources but have an

impact on Natural Resources will never be seen

implementing Corporate Social Responsibility.

Stakeholders always think of how management

in the company is effective and must be able to

understand and implement strategic and tactical

decisions. The purpose of business is to create as

much value as possible for stakeholders.

The corporate environment is part of one of the

desires of stakeholders for the survival of the

company. The theory that can fulfill the desires of

stakeholders for environmental purposes is a

contingency theory. Where this theory will make the

proposition between company activity and company

structure will be formed from the constraints of the

external environment.

Good management oversight of certain activities

and circumstances will be able to encourage the

company to achieve and the company's desires in the

future. Contingency theory can improve the

performance of entities as well as company

management. One contingency factor is the external

environment. The external environment is a source

of information and the need for information, where

information is needed in the stock market to see

whether the situation is stable or not. This

information can be obtained indefinitely. One of the

external environmental information is the corporate

social responsibility.

2 LITERATURE STUDY

Stakeholders Theory

This theory is about how management functions to

satisfy the owners and people around the company.

Company management seeks to combine

performance improvement with increased

stakeholder satisfaction. This theory puts forward

the interests of stakeholders first compared to the

interests of company management.

According to Freeman, stakeholder theory can

identify value as the main driver of the company,

and also recognizes that the value must be shared

with a group of stakeholders were not only

shareholders and company managers but also actors

in the community who might have an interest in the

company's operations. (Theodoulidis et al., 2017).

The company is part of several elements that

make up society in the social system. This condition

creates a reciprocal relationship between the

company and the stakeholders. This means that the

company must carry out its role in two directions,

namely to meet the needs of the company itself and

stakeholders.

Contingency Theory

Contingency theory is a theory of leader suitability

which means adjusting the leader to the right

conditions. This theory argues that leader

performance is determined from his understanding

of the situation in which they lead. In simple terms,

contingency theory emphasizes leadership style and

understanding the right situation by the leader.

This theory can be used to answer questions

about someone's leadership with various types of

organizations. This theory can be used to predict

someone who has worked well at one position in an

organization will be equally effective when moved

to a different position. This theory can provide

changes in the good management of top

management with lower management.

According to Donaldson, contingency theory

shows that the results of organizational effectiveness

from the characteristics of the right organization will

reflect the organizational situation. (McAdam,

Miller and McSorley, 2016). The company seeks to

improve performance by increasing conformity and

harmony with the series that has been determined by

contingency theory. Contingency theory will be very

useful when there is a shortage of existing

theoretical frameworks by emphasizing an approach

based on suitable contingencies compared to what is

best done to manage the company.

Corporate Social Responsibility (CSR)

Corporate Social Responsibility is a concept in a

company where the company has responsibility to

stakeholders (such as employees, consumers,

producers, shareholders, a community and

environment) in all company operations that cover

economic, social and environmental aspects. This

Corporate Social Responsibility has a very close

relationship with sustainable development.

Sustainable development in the perspective of

corporate social responsibility must be in the form of

short-term sustainability and long-term

sustainability.

The concept of Corporate Social Responsibility

today is very popular, but uniformity has not been

found in defining the concept of Corporate Social

Responsibility. Corporate social responsibility is

also often seen as a company's business commitment

to sustainable development. To run the company's

operations, based on the point of view of corporate

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

974

social responsibility, the company should not just

look at it from an economic aspect, but also must

look at the social and environmental aspects. For

example, in gaining profits so that dividends can be

distributed, companies must also see the impact of

the emergence of these benefits and for stakeholders

what can be obtained from these benefits.

Corporate social responsibility can also be

business behavior related to business ethics. So,

companies must be responsible for the company's

social environment. In practice, a company must be

more motivated to do more corporate social

responsibility than obligations under a regulation.

There is a relevant relationship between

Corporate social responsibility in the business and

strategies naturally in the company's activities.

Corporate social responsibility and company

performance are considered the most important for

generating wealth and improving company

performancen. (Gallardo-Vázquez and Sanchez-

Hernandez, 2014).

Although many companies have realized the

importance of carrying out CSR, there are also those

who object to implementing it. Even among those

who agree that companies run CSR, there are still

differences in interpreting the level of company

involvement in carrying out CSR. In the end, the

success of CSR and the scope of CSR programs that

are carried out will be determined by the level of

awareness of business people and other relevant

stakeholders.

Corporate Social Responsibility From the

Viewpoint of Contingency Theory

The implementation of Corporate Social

Responsibility carried out by the company as a form

of accountability and concern for the environment

around the company. Many benefits obtained by the

company with the implementation of Corporate

Social Responsibility, among others, products are

increasingly preferred by consumers and companies

are attracted by investors..

Contingency theory says that there is no best

method for managing a company. Management must

be able to balance internal needs and adapt to

environmental conditions. Management must be able

to harmonize and balance internal needs with the

environment.

Most companies do corporate social

responsibility only voluntarily. This mindset guide is

the collection and interpretation of new information.

Because mindset acts as an information filter, it is

dynamic and continues to develop in response to

new information. At this time new information

appears and is not consistent with this mindset that

will make the mindset change. The following in

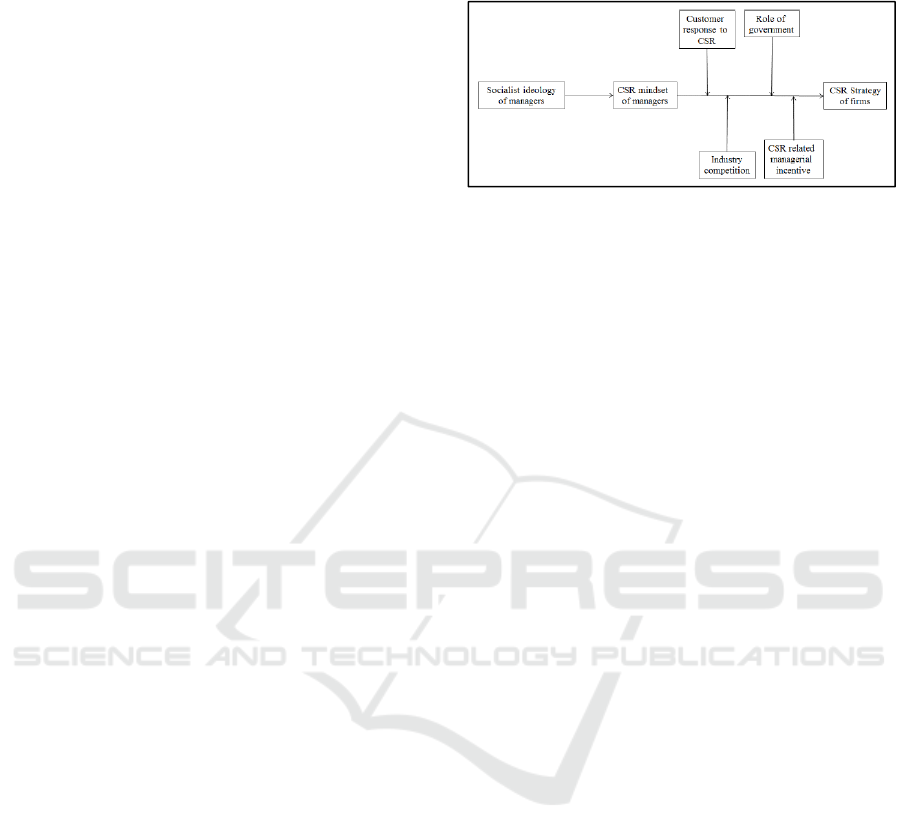

Figure 1 we can see the contingent framework

according to Jiang et al.

Figure 1: A contingent Framework of Political

Ideology, CSR mindset and CSR Stategy

Managers sometimes lack understanding of the

mindset rather than Corporate social responsibility,

so they do not consider Corporate social

responsibility less. A manager's mindset can be in

the form of the desire to maximize profits, or the

manager is considered as the representative of the

owner of the company or, more concerned with

improving the manager's personal life. Corporate

social responsibility often focuses on fulfilling

employee rights, social justice, and environmental

preservation. This is what makes the mindset of

Corporate Social Responsibility for each manager

different so that he is unable to understand the

purpose of overall corporate social responsibility.

3 METHODOLOGY

The researcher conducted a literature study to find

out how the implementation of corporate social

resposibility is seen from the perspective of a

contingency perspective. Researchers examine from

several journals related to corporate social

resposibility and contingency theory. The researcher

wants to find out whether how corporate social

resposibility is carried out by companies for the

interests of stakeholders so that a contingency

perspective is needed.

4 RESULT AND ANALYSIS

Contingency theory explains that the higher the fit

between management control predictions and other

contingent factors, the higher the level of

achievement of entity performance or vice versa.

The results of research on corporate social

responsibility with the company's performance are

very much and there are differences of opinion, there

is research that there is a positive relationship

between corporate social responsibility and company

Corporate Social Responsibility is Viewed from a Contingency Perspective

975

performance. And there are also results of research

saying that there is a negative relationship between

corporate social responsibility and company

performance. But there are also studies that say there

is no relationship between corporate social

responsibility and company performance.

Corporate social responsibility has a positive

relationship with company performance. (Wang et

al., 2015). The benefits of corporate social

responsibility will be greater in value than the costs

incurred. The commitment of a company to

implement Corporate Social Responsibility will

increase economic value.

Corporate social responsibility has a negative

relationship with company performance. (Mallin,

Farag and Ow-Yong, 2014; Chen, Feldmann and

Tang, 2015). This is because the company believes

that the social environmental costs are avoidable

costs.

Corporate social responsibility has no

relationship with company performance. (Lu et al.,

2014).

According to Jiang et al., (2015) that managerial

decision making in terms of strategy Corporate

social responsibility is influenced by political

ideology. The manager's mindset will influence the

strategy of Corporate social responsibility. The

strength of the relationship between the mindset of

Corporate social responsibility and the choice of

strategy Corporate social responsibility is moderated

by customer responses to Corporate social

responsibility, industry competition, the role of

government, and managerial incentives related to

corporate social responsibility. (Jiang et al., 2018).

In the economy in transition, manufacturing

companies are encouraged to invest more in

corporate social responsibility. According to the

managers of a company that implements corporate

social responsibility, it will create better customers

and increase the value of a company. Xie (2017)

stated that efforts to improve corporate social

responsibility can improve customer satisfaction and

recognition so that financial performance is better.

(Xie et al., 2017).

During the implementation of Corporate Social

Responsibility, all parties in the company must be

freed from short-term goals. Corporate social

responsibility does not directly have an impact on

improving financial performance.(Lu et al., 2018).

The owner and top management of the company

must consider the employee to be a tool to connect

the success of Corporate social responsibility.

Because, the company invests its money in

Corporate Social Responsibility, and the company

receives great benefits for the implementation of

Corporate Social Responsibility.. (De Roeck and

Maon, 2018).

5 CONCLUSIONS

Many company management, in allocating company

resources to improve the performance of Corporate

social responsibility. The resources owned and used

by the company do not fully translate into

productive efficiency and economic values. Every

company that moves and operates competitively will

present heterogeneity in terms of time availability.

REFERENCES

Chen, L., Feldmann, A. and Tang, O. (2015)

‘Therelationship between disclosures of

corporate social

016/J.IJPE.2015.04.004.Gallardo-Vázquez, D.

and Sanchez-Hernandez, M. I. (2014)

‘Measuring Corporate Social Responsibility

for competitive success at a regional level’,

Journal of Cleaner Production. Elsevier, 72,

pp. 14–22. doi:

10.1016/J.JCLEPRO.2014.02.051.

Jiang, F. et al. (2018) ‘Mapping the relationship

among political ideology, CSR mindset, and

CSR strategy: A contingency perspective

applied to Chinese managers’, Journal of

Business Ethics, 147(2), pp. 419–444. doi:

10.1007/s10551-015-2992-7.

Lu, W. et al. (2014) ‘A decade’s debate on the nexus

between corporate social and corporate

financial performance: a critical review of

empirical studies 2002–2011’, Journal of

Cleaner Production. Elsevier, 79, pp. 195–206.

doi: 10.1016/J.JCLEPRO.2014.04.072.

Lu, W. et al. (2018) ‘The paradoxical nexus between

corporate social responsibility and sustainable

financial performance: Evidence from the

international construction business’, Corporate

Social Responsibility and Environmental

Management, 25(5), pp. 844–852. doi:

10.1002/csr.1501.

Mallin, C., Farag, H. and Ow-Yong, K. (2014)

‘Corporate social responsibility and financial

performance in Islamic banks’, Journal of

Economic Behavior & Organization. North-

Holland, 103, pp. S21–S38. doi:

10.1016/J.JEBO.2014.03.001.

McAdam, R., Miller, K. and McSorley, C. (2016)

‘Towards a contingency theory perspective of

UNICEES 2018 - Unimed International Conference on Economics Education and Social Science

976

quality management in enabling strategic

alignment’, International Journal of Production

Economics. Elsevier. doi:

10.1016/J.IJPE.2016.07.003.

De Roeck, K. and Maon, F. (2018) ‘Building the

Theoretical Puzzle of Employees’ Reactions to

Corporate Social Responsibility: An

Integrative Conceptual Framework and

Research Agenda’, Journal of Business Ethics,

149(3), pp. 609–625. doi: 10.1007/s10551-

016-3081-2.

Theodoulidis, B. et al. (2017) ‘Exploring corporate

social responsibility and financial performance

through stakeholder theory in the tourism

industries’, Tourism Management. Pergamon,

62, pp. 173–188. doi:

10.1016/J.TOURMAN.2017.03.018.

Wang, D. H.-M. et al. (2015) ‘The effects of

corporate social responsibility on brand equity

and firm performance’, Journal of Business

Research. Elsevier, 68(11), pp. 2232–2236.

doi: 10.1016/J.JBUSRES.2015.06.003.

Xie, X. et al. (2017) ‘Corporate social responsibility,

customer satisfaction, and financial

performance: The moderating effect of the

institutional environment in two transition

economies’, Journal of Cleaner Production.

Elsevier Ltd, 150, pp. 26–39. doi:

10.1016/j.jclepro.2017.02.192.

Corporate Social Responsibility is Viewed from a Contingency Perspective

977