The Development of Role Play Learning Model in Management

Accounting Course

Riwayadi

1

, Yulia Hendri Yeni

1

, and Denny Yohana

1

1

Faculty of Economics, Universitas Andalas, Padang, Indonesia

Keywords: Role-Play Learning Model, Student-Centered Learning.

Abstract: This research aims to evaluate the implementation of Role Play Learning Model (RPLM) in achieving the

course’s expected learning outcomes. This is an applied research using primary data collected through survey

and observation. The population consists of 182 management accounting students in the 2nd semester of

2017/2018. This research uses census sampling. Of the total respondents surveyed, 95% returned their

questionnaires. The questionnaire is developed by using five Linkert scales (5 for highly agree). The study

reveals that students agree to implement RPLM on management accounting course. RPLM can improve

students’ grades as none of them got D and E grades. The number of students who got C grade dropped from

17% to 4% while that of those who got A-, B+, B-, and C+ grades increase by 8%, 1%, 5%, and 8%

consecutively. This proves that the implementation of RPLM can (1) build a good teamwork, (2) improve the

understanding of learning materials, (3) increase the motivation of students, (4) build the self-confidence of

students, (5) make students more innovative and creative, and (6) make teaching and learning process more

interesting for the students.

1 INTRODUCTION

Job markets require high competencies that include

hard skills and soft skills. Active, creative, and

innovative learning methods should be developed to

help graduate students’ acquire high competencies.

Teacher-centred learning (TCL) approach is no

longer adequate to make students active, creative, and

innovative. Previous research found that student-

centered learning (SCL) approach is better than

teacher-centered learning (TCL) approach. Hadi

(2007) and Kurdi (2009) argue that SCL allows

students to have high motivation to achieve their

desired competencies. SCL approaches include (i)

Small Group Discussion (SGD), (ii) Role Play,

Games, and Simulation (RPGs), (iii) Case Study

(CS), (iv) Discovery Learning (DL), (v) Self-Directed

Learning (SDL), (vi) Cooperative Learning (CL),

(vii) Collaborative Learning (CbL), (viii) Contextual

Instruction (CI), (vix) Project-Based Learning

(PjBL), and (x) Problem-based learning and Inquiry

(PBL) (LPPPM Unand, 2014). In this research, role

play learning model is developed for management

accounting course. Role play is a learning method

that enables students to understand the concept [3].

The steps of Role Play Learning Model are (1) the

lecturer develops the learning scenario, (2) the

lecturer requests students to learn the scenario, (3) the

lecturer requests students to make a group to discuss

the role of each member, (4) the lecturer requests

students to make a presentation of discussion results,

and (5) The lecturer provides advisory, conclusion,

and refection (Ngalimun, 2012).

Management accounting is a compulsory course

offered in the 4

th

semester. The current learning

methods of this course are lecture and case solution

presentation. At the beginning of the semester, the

student group is established. Each group should

present the solution of the assigned case by using

power point. Student assessments include group

assessment, mid-term exam, final exam, presentation

skills, and class participation. Rubric assessment has

not been used for soft skill assessment. 51% of

management accounting students got E, D, C, C+, and

B- grades. This significant number should be

improved since job markets require the minimum

cumulative GPA of 3 (4 for the highest).

The weaknesses of the current learning method

are (i) lack of team work, since one person might only

do the group tasks, (ii) less communication skills, (iii)

less understanding of the concept between group

members, (iv) less innovation and creativity, and (v)

108

Riwayadi, ., Yeni, Y. and Yohana, D.

The Development of Role Play Learning Model in Management Accounting Course.

DOI: 10.5220/0008680801080110

In Improving Educational Quality Toward International Standard (ICED-QA 2018), pages 108-110

ISBN: 978-989-758-392-6

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

high possibility of plagiarism (only copy paste other

group’s case solution)

Problem definition can be formulated as follows:

is role play learning model more effective in

achieving the both the program’s expected learning

outcomes (PELOs) and management accounting

course’s expected learning outcomes (CELOs)?

The research objective is to evaluate the

effectiveness of role-playing learning model in

achieving PELOs and CELOs. The research benefit is

to provide an input for undergraduate accounting

study program and lecturers in developing the

effective learning methods in order to achieve PELOs

and CELOs.

2 RESEARCH METHOD

This is an applied research that focuses on practical

problem solving directed to answer the specific

questions for policy development, action or particular

performance (Indrianto and Supomo, 1999). This

research is the evaluation research used for the

evaluation of the effectiveness of an action, activity

or program (Indrianto and Supomo, 1999). This

research is a qualitative approach that uses data in the

form of written sentences or verbal, behavioral,

phenomena, events, knowledge, or the object of the

research (Maleong, 2006). Qualitative research is

concerned with developing the explanation of social

phenomena. It aims to help us to understand the world

in which we live and why things are the way they are

(Hancock, 2002).

The subject of this research comprises Andalas

University’s accounting students enrolled in

management accounting course. The population

consists of all Andalas Univerity’s accounting

students enrolled in management accounting course

for the second semester of 2017/2018. The research

uses census data, that is, all Andalas University’s

accounting students who are taking management

accounting course. 182 accounting students took

management accounting in the second semester of

2017/2018. The research was conducted in the second

semester of 2017/2018 for six months (January – June

2018).

The research uses primary data gathered through

questionnaire and observation. Data were collected

by using two methods: observation and survey.

Observation was conducted when the students were

presenting their video project. The observation aims

to assess the achievement of course’s expected

learning outcomes and lesson’s expected learning

outcomes that include the understanding of concepts,

communication skills, team work, innovation and

creativity, the results will then be compared to the

previous learning method. The questionnaire was

distributed to students on the final exam schedule.

Questionnaire was developed using 5 Linkert scales:

1 (highly agree), 2 (agree), 3 (neutral), 4 (not agree)

and 5 (highly not agree).

2.1 Planning

A learning plan was developed to achieve the

program’s expected learning outcomes (PELOs) that

have been formulated by the Undergraduate

Accounting Study Program. Learning plan includes

program’s expected learning outcomes (PELOs),

course’s expected learning outcomes (CELOs),

lesson’s expected learning outcomes (LELOs).

A learning plan was developed by using role play

learning model. Students will be given the group

project assignment of video creation by using role

play learning model. Each group member acts as a

manager who solves the company problem. She/he

could be a marketing manager, a production manager,

a finance manager or an accounting manager.

2.2 Implementation

The lecturer develops a case based on topics

discussed in management accounting course. The

case reflects the real condition of the companies. Each

group is given the project assignment of video

creation learning. Each group member acts

specifically as a director, division manager,

marketing manager, production manager, finance

manager, accounting manager or another manager

who solve the company’s problems. Each group

should create an interesting video which lasts 10

minutes maximum and submit it to the lecturer at least

one day before the presentation schedule. Students

are free to choose the Spot of video creation. The

Video Project Assignment will be assessed by using

the assessment rubrics.

The steps of data analysis are: (1) tabulating the

questionnaire, (2) calculating the average score of

each question by dividing total score with the total

number of respondents, and (3) drawing the

conclusion.

Besides the questionnaire, the effectiveness of the

learning method will also be assessed by looking at

the grade differences before and after the learning

method development, and also by the observation

results of the video presentation.

The Development of Role Play Learning Model in Management Accounting Course

109

3 RESULTS AND CONCLUSION

Of the 182 questionnaires distributed, 173

questionnaires (95%) were returned and could be

processed. Students agree that role-play learning

method should be used in management accounting

course as indicated by the overall average score of

3,66. Students highly agree that Role Play Learning

Model can build good teamwork and communication

skills as indicated by the above average score of 4

(Appendix 1). After the implementation of Role Play

Learning Model, no student has had D and E grades.

The students who got C grade also dropped from 17%

to 4% or decreased by 13%. The number of students

who got A-, B+, B-, and C+ grades increase by 8%,

1%, 5%, and 8% consecutively (Appendix 2). This

proves that role-play learning model can improve

students’ grades, which will also affect students’

cumulative GPA.

It can be concluded that the implementation of

Role Play Learning Model can (a) build good

teamwork, (b) improve the understanding of the given

materials, (c) encourage student s’ motivation to

learn, (d) build students’ self-confidence, (e) make

students more innovative and creative, and f) make

lecturing activities more interesting to students.

It is suggested that firstly, role play learning

model needs to be implemented for management

accounting course and other courses and secondly,

faculty or study program needs to support the

facilities for the effectiveness of role-playing learning

model implementation.

REFERENCES

Hadi, R 2007. Dari Teacher-Centered Learning ke Student-

Centered Learning: Perubahan Metode Pembelajaran di

Perguruan Tinggi. Insania, Vol. 12, No. 3.

Hancock, Beverley. 2002. An Introduction to Qualitative

Research. Trent Focus Group. University of

Nottingham.

Indriantoro, Nur dan Supomo, Bambang. 1999. Metodologi

Penelitian Bisnis Untuk Akuntansi dan Manajemen,

Edisi Pertama,Yogyakarta: BPFE

Kurdi F.N. 2009. Penerapan Student Centered Learning

dari Teacher Centered Learnng Mata Ajar Ilmu

Kesehatan pada Program Studi Penjaskes. Forum

Kependidikan, Volume 28, Nomor 2.

Lembaga Pengembangan Pendidikan dan Penjaminan Mutu

(LP3M) Universitas Andalas. 2014. Panduan Praktis

Pelaksanaan Student Centered Learning (SCL)

Moleong, Lexy J. 2006. Metode Penelitian Kualitatif, Edisi

Revisi, Bandung: Remaja Rosdakarya

Ngalimun. 2012. Strategi dan Model Pembelajaran.

Banjarmasin: Aswaja Pressindo.

APPENDIX

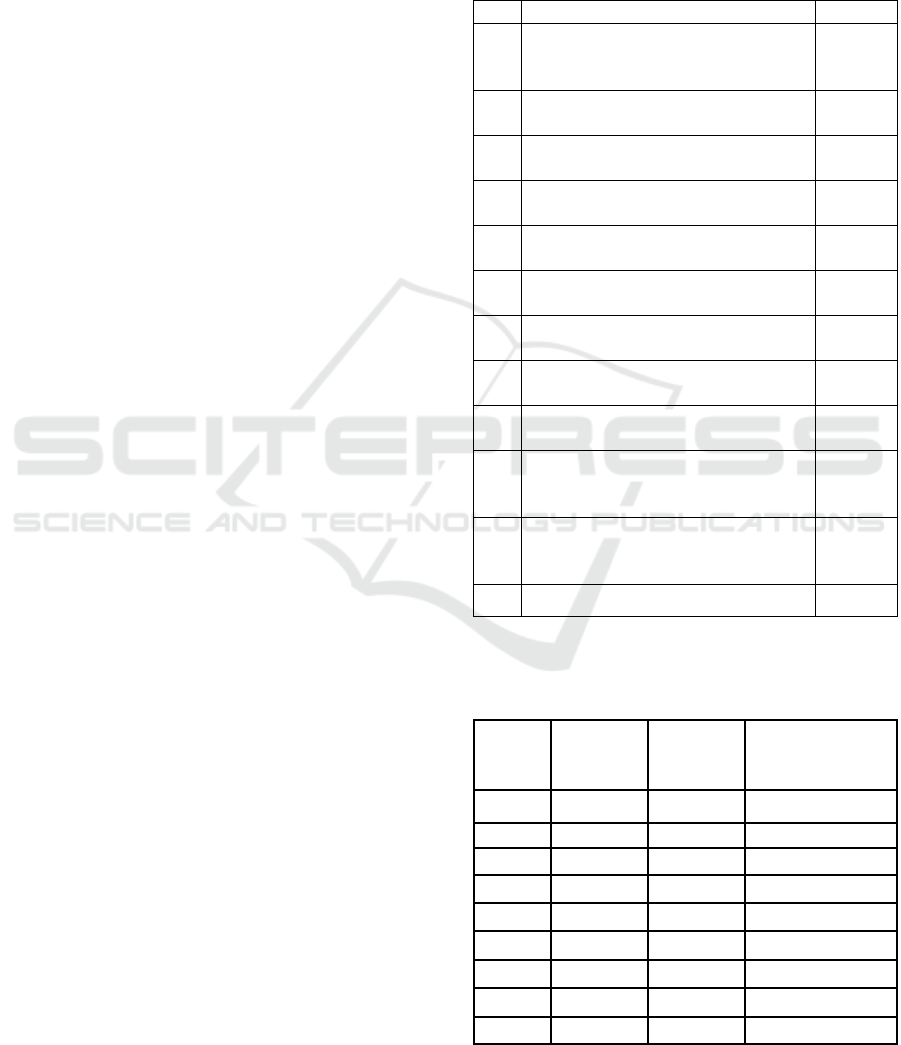

Survey Results

No.

Question

Average

1.

Role play learning model makes it

easier for me to understand

management accounting materials

3,51

2.

Role play learning model boosts my

learning motivation

3,34

3.

Role play learning model makes me

more innovative and creative

3,44

4.

Role play learning model gives me

more self-confidence

3,49

5.

I participate actively in to video

creation

4,13

6.

I have no difficulties in creating the

learning video

3,32

7.

Participate actively in preparing the

scenario

4,11

8.

I participate in getting the

understanding of the case and solution

4,05

9.

I give ideas in the creation of learning

video

3,94

10.

I suggest that this model should be

implemented in management

accounting

3,35

11.

I get many benefits from the

implementation role play learning

method

3,55

Average

3,66

Before and After the Implementation of Role Play Learning

Model.

Grade

2nd Smt.

2016/2017

(Before)

1st Smt.

2017/2018

(After)

Description

A

11%

11%

Unchanged

A-

8%

16%

Increased by 8%

B+

14%

15%

Increased by 1%

B

15%

14%

Decreased by 1%

B-

23%

28%

Increased by 5%

C+

4%

12%

Increased by 8%

C

17%

4%

Decreased by 13%

D

4%

0%

Decreased by 4%

E

3%

0%

Decreased by 3%

ICED-QA 2018 - International Conference On Education Development And Quality Assurance

110