The Effect of Machiavellian Characteristics and Auditee Pressure on

Ethical Decision Making of Government Auditors in Palembang

Municipality

Patmawati, Dwirini and Muhammad Hidayat

Faculty of Economics, Universitas Sriwijaya, Palembang, Indonesia

Keywords: Machiavellian Characteristics, Auditee Pressure, Ethical Decision Making

Abstract: This study aims to examine the relationship between the variables of Machiavellian characteristics and

auditee pressure on ethical decision making of government auditors in Palembang Municipality. The

research sample is government auditors of Palembang. Whereas, the data is obtained using Partial Least

Square method. The study results indicate that Machiavellian Characteristics had a significant negative

effect on auditor ethical decision making, while auditor pressure did not inflict any influence on the ethical

decisions making.

1 INTRODUCTION

An auditor is a person who assesses and affirms an

opinion on the fairness in all material respects,

financial balance of business activities and cash

flows that are in accordance with Generally

Accepted Accounting Principles (GAAP) in

Indonesia (Arens, 2003). In Indonesia, government

auditors can be classified into two group, namely

Government External Auditors or Auditors of the

Audit Board (BPK) who are auditors working for the

Audit Board of the Republic of Indonesia (BPK), an

body established under the Indonesian constitution.

Whilst the Government Internal Auditor, better

known as the Government Functional Supervisory

Apparatus (Aparat Pengawasan Fungsional

Pemerintah/APFP) that is carried out by Finance and

Development Supervisory Agency (Badan

Pengawasan Keuangan dan Pembangunan/BPKP),

Department of Inspectorate General/LPND, and the

Regional Supervisory Agency, serves the

government needs.

Based on Law Number 15 Year 2004, decision

making is a part of the principal duties and functions

of the auditors of BPK of the Republic of Indonesia,

especially those related to the assignment of auditors

in examining both the Financial Statements and

other examinations. The success in ethical decision

making of the Audit Board of Republic of Indonesia

(BPK RI) is referred to the Law, whereas the

inspection standard is the benchmark for evaluating

the management and responsibility of state finances.

The inspection standards consist of general

standards, implementation standards, and audit

reporting standards that must be conducted by the

BPK and/or the auditor.

BPK Regulation number 1 Year 2017 is a

regulation stipulated by the BPK as the State

financial audit standard that serves as auditor's main

guideline in carrying out audits. The regulation

becomes a manual on the procedures for auditing the

management of State finances.

Richmon (2001) examined the relationship of a

trait that forms a personality type namely

machivellian characteristics as measured by Mach

IV Score instruments with behavioral tendencies of

accountants in facing ethical dilemmas. The

machiavellian charateristics have an effect on the

tendency of accountants to accept dilemmatic

behaviors that are related to their professional ethics.

It shows that the higher the tendency of

machiavellian characteristics of an accountant, the

higher the tendency to accept ethically dilemmatic

behaviors or actions. Machiavellian charateristics

tend to be selfish, manipulative and aggressive.

Machivellian character is a trait that is likely to exist

in all business professions, especially accountants

and auditors. A person who works as an accountant

or auditor is required to have more ethical

responsibilities, compared to other professions. As

Patmawati, ., Dwirini, . and Hidayat, M.

The Effect of Machiavellian Characteristics and Auditee Pressure on Ethical Decision Making of Government Auditors in Palembang Municipality.

DOI: 10.5220/0008444407150722

In Proceedings of the 4th Sriwijaya Economics, Accounting, and Business Conference (SEABC 2018), pages 715-722

ISBN: 978-989-758-387-2

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

715

an auditor, the profession is highly dependent on

public trust as the users of this professional services.

Machiavellianism as a construct that symbolizes

a series of behaviors, including lack of morality,

negative attitudes and emotional detachment.

Richmond (2001) explains that the higher tendency

of machiavellian charateristic, the more likely a

person to behave unethically. On contrary, if the

tendency of machiavellian is low, then a person will

tend to behave ethically. Murphy (2012) found that

machiavellian accountants are more likely to report

inaccurate financial statements compare to those of

lower machiavellianism. Purnamasari (2006)

explains that individuals with high machiavellianism

tend to take advantage of situations to gain personal

benefits and more willingly to disobey the rules.

Existing studies have consistently found that

machiavellians show low ethical values.

In recent years, many cases involving violations

of law and codes of ethics against government

auditors occurred in 2016, among others, the case

related to big motorbike bribery, the providence of

Senior Auditor at Sub-Auditor VIIB2, Sigit

Yugoharto is now being studied by the Honorary

Council Code of Ethics of the BPK. Cited from

Tempo Newspaper in 2016, in the Panama Papers it

was stated that Harry Azhar Aziz (Chairperson of

the BPK of Republic of Indonesia) is the owner of

one of the offshore companies, Sheng Yue

International Limited. Whilst, Sheng Yue

International Limited is believed to be a company

established in a tax haven with the purpose of

avoiding tax payments in its home countries.

As follow up, an internal examination was

conducted internally on the violations of the ethics

code (in accordance with BPK Regulation No. 3

Year 2016 concerning the Code of Ethics of BPK)

and violations of employee disciplinary rules (in

accordance with Government Regulation No. 3 Year

2010 concerning Civil Servants Discipline). Ethical

considerations is defined as the making of a

deliberation/consideration regarding the exact truth

of an action that is ethically correct to be taken.

Wibowo in Devaluisa (2009) defines ethical

considerations as the contemplation of what must be

done to prevent the occurrence of ethical dilemmas.

Whereas, the auditee pressure felt by each

auditor will also illustrate how far the auditor

influences decision making. With the facilities

provided by the auditee, the auditor may experience

pressure from the auditee. The pressure from the

auditee could be in the form of pressure to provide

an unqualified statement (WTP) on the audit report

of the financial statements as presented by the

management.

2 LITERATURE REVIEW

2.1 Theory of Perception

Perception is one of the important psychological

aspects for humans in responding to the presence of

various aspects and symptoms around us. It contains

a very broad definition, involving internal and

external factors. The term perception is often

referred to as opinions, images, or assumptions,

because in perception there is a person's response to

something, or to an object.

Determination of perceptions is influenced by

internal and external factors, which according to

Robbins (2003) there are three factors that influence

perception. First, the exclusivity, meaning that

someone will have different perceptions on the

behavior of other individuals in different situations.

And if the behavior is considered as something

unusual, then the other individuals who act as the

observer will have a perception that the person is

conducting a behavior generated by external factor.

Contrariwisely, if the behavior is considered as

something that other people usually do, it is

considered as an internal attribution.

Second, the consensus, meaning that people have

the same perception in responding to a person's

behavior in similar setting or condition. If there is a

high consequences, then the attribution is generated

internally. On the other hand, if the consequences

are said to be low, then the attribution is created

externally. The last factor is consistency, meaning

that a person evaluates the behavior of others with

the same reaction or response from time to time. The

more consistent the behavior is, the more likely

people will connect the behavior with internal

factors. Therefore, this perception theory is highly

reassuring for this study

2.2 Theory of Ethics

Ethics is a moral order that has been mutually agreed

upon in a profession and is intended for members of

the said profession. The basic motivation in carrying

out ethical actions is not because of the individual's

aspiration and awareness, but due to legal

regulations (O’Leary and Cotter, 2000).

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

716

Duska and Duska (2003) developed three ethical

theories, whereas these three theories are used to

elaborate this research, that are:

1. Utilitarianism Theory. This theory discusses the

optimization of individual decision making to

maximize benefits and minimize negative

impacts. There are two types of utilirianism,

namely

a. Act utilitarism, for actions that are beneficial to

many people.

b. Rule utilitarism, for moral rules that are accepted

by the wider community.

2. Deontology Theory. This theory discusses the

obligation of individuals to deliver the rights to

others, so that the basis for evaluating whether an

action is good or bad must be based on

obligations, not the consequences of an action.

Deontology emphasizes that actions never turn

out to be good because the results are good, but

because of the obligation that must be made

(Bertens, 2000).

3. Virtue Theory. The theory discusses the character

of a person that allows him/her to behave

morally correct

2.3 Marchevillian Characteristic

Machiavellianism was taught by an Italian political

philosopher named Niccolo Machiavelli (1469-

1527). Machiavellianism, by Christie and Greis

(1970), is defined as a process in which the

manipulators get more rewards compare to the time

when they are not manipulating, while others get

smaller, at least in the short term.

According to Richmond (2001), Machiavellian is

an aggressive charateristic, and a tendency to

influence and control others to achieve personal

goals. Machiavellian personality, as further

described by Richmond (2001) is a personality that

lacks of affection in personal relationships, ignores

conventional morality, and shows low ideological

commitment.

Machiavellian personality has a tendency to

manipulate others, having a very low appreciation

for others. Shafer and Simmons (2008) identify three

underlying factors of machiavellianism, namely:

1. Advocate for manipulative tactics such as

deception or lies

2. A hostile opinion of humans, that are weak,

weakling, and easily manipulated; and Lack of

consideration for conventional morality

2.4 Auditee Pressure

In carrying out their functions, auditors often have a

conflicts of interest with the company’s

management. The management possibly would like

the company's operations or performance to appear

profitable, that is reflected through higher profits,

with the intention of obtaining awards.

To achieve these objectives, it is not uncommon

for the company management to put pressure on the

auditor so that the audited financial statements

produced are as the requests of the auditee. In this

situation, the auditor encounter dilemmas. On the

one hand, if the auditor respects the auditee’s

request, she/he violates the professional standards.

But if the auditor does not go along with the auditee,

the auditee may terminate the assignment of the

auditor.

Auditee's financial state also influences the

auditor's ability to overcome auditee's pressure

(Knapp, 1985) in (Harhinto, 2004). Auditees having

a strong financial state may provide substantial audit

rewards and valuable facilities for the auditors. In

addition, the probability of bankruptcy on the

auditee that having good financial state is relatively

small. In this situation, auditors become complacent

so they are less careful in conducting audits.

Based on the description above, the auditor is in

a strategic position both in the viewpoint of

company management and the users of financial

statements. Furthermore, the users of financial

statement are maintaining a great trust in the results

of the auditor's work in auditing financial

statements. To be able to fulfill a reliable audit

performance, the auditor as an examiner in carrying

out his/her profession must be guided by the code of

ethics, professional standards and financial

accounting standards that are applied in Indonesia.

Each and every auditor must maintain their integrity

and objectivity in performing their duties by acting

honestly, firmly, without pretension so that they can

act fairly, without being influenced by the pressure

or request from any particular party to fulfill his/her

personal interests.

2.5 Ethical Decision Making

Individual decision making is an important part of

organizational behavior. But how these individuals

in the organization making their final decisions and

the quality of their decisions are mostly influenced

by their perceptions. According to Robbins et al

(2007), decision making occurs as a reaction to

problems. In this case, there are differences between

The Effect of Machiavellian Characteristics and Auditee Pressure on Ethical Decision Making of Government Auditors in Palembang

Municipality

717

the existing and the expected conditions, which then

require other actions as the alternative.

Model Rest (1986) has been widely used in

ethical accounting research. Rest, Moon and Getz

(1986) states that, there are four stages that a person

must do to combine ethical dimensions in decision

making, so called the Four Component Model,

including ethical sensitivity, ethical reasoning,

ethical motivation, and ethical implementation.

The first stage is ethical sensitivity, that

presupposes the need for moral awareness or the

ability to identify moral issues. In this stage, an

interpretation occurs where an individual recognizes

that there is a moral issue in the situation she/he

encounters, or that a moral principle becomes

relevant in it (Wisesa, 2011). This stage ignites the

potential to initiate and to influence an assessment

process, ethical decision making and ethical

behavior of an individual.

After the moral issues were identified, an

individual then makes ethical decisions based on

evaluation of the consequences that suppose to occur

in certain situations together with the alternative

actions that may be taken. Determining alternative

decisions for actions to be taken must be based on

appropriate reasoning that takes into account the

relevant moral principles in the process of ethical

interpretation in the second stage.

In conducting alternative decisions on actions

that have been decided, confidence and

encouragement are required, that is called ethical

motivation in the third stage. Followed by the fourth

stage, that is the ethical implementation in which an

individual performs the chosen alternative action in

reality.

3 CONCEPTUAL FRAMEWORK

In the scheme of ethical decision making, subjective

attitudes and norms owned by a person are

influencing the process of moral evaluation and the

formation of one's moral intentions, before the

ethical actions were implemented. These subjective

attitudes and norms developed from individual

factors possessed by a person, including the

machivellian characteristics, perceptions of the

importance of ethics and auditee pressure. The

machivellian characteristics partially have a

significant influence on subjective attitudes and

norms, which in turn will affect the person's ethical

decision making process. Based on this theoretical

basis, the the research scheme can be described as in

the following Figure 1:

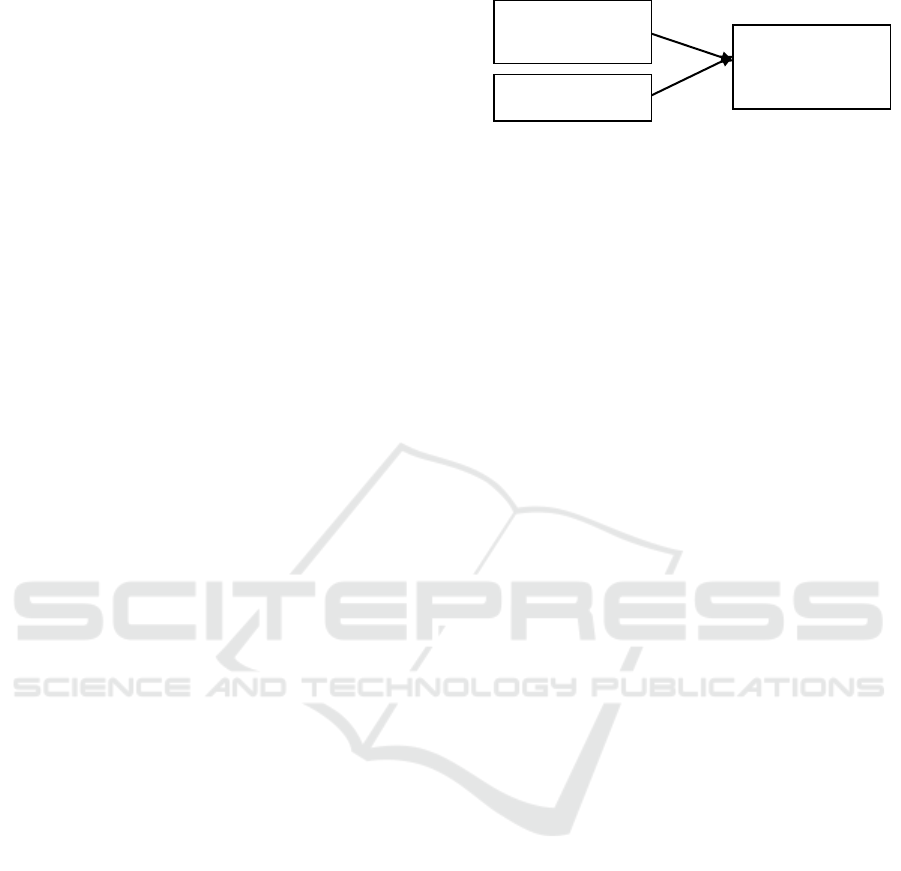

Figure 1: Conceptual Framework

The independent variable consists of

machiavellian charateristics and pressure from the

auditee. While ethical decision making is the

dependent variable which its relationship will be

tested against the independent variables. Each

independent variable causes distinctive influence on

the ethical decision making process, both positive

and negative ones.

This study tries to examine how the machivellian

characteristics and auditee pressure influence ethical

decision making of the government auditors. In line

with previous studies, a person with high tendency

of Machiavellian characteristics is believed to make

less ethical decisions.

4 RESEARCH HYPOTHESIS

Based on theoretical review and previous researches

that have been mentioned above, the hypotheses of

this study are as follows:

H

1

: There is a negative relationship between

Machiavellian characteristics and ethical

decision making of government auditors.

H

2

: There is a negative relationship between

auditee pressure and ethical decision making of

government auditors.

5 RESEARCH METHOD

5.1 Population and Sample

The population to be used in this study are the

Auditors of Audit Board (BPK) and the Auditors of

Finance and Development Supervisory Agency

(BPKP) of South Sumatra Province. The sampling

technique of this study is using purposive sampling

by the following criteria:

1. Government auditors who have conducted audits

at least 2 times.

2. The auditor has worked for at least 2 years.

Machevillian

Characteristic

Audit Pressure

Ethical Decision

Making

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

718

3. The auditor has applied his/her knowledge in the

audit domain in practice

Based on the questionnaire that has been distributed,

68 questionnaires are used as research data

5.2 Data Collecting Method

The data to be used in this study are primary data.

Data will be collected using survey method, by

providing questionnaires directly to government

auditors

5.3 Analytical Technique

Based on the explanation of the relationship between

Machiavellian Characteristics and auditee pressure

on ethical decision making, the research model is

formulated as follows:

η = -γ1 - γ2 + ε

whereas

η = Ethical Decision Making

γ1 = Machiavellian characterictics effect

γ2 = Auditee pressure

ε = error

The data analysis technique is using Structured

Equation Modeling (SEM) with Partial Least Square

(PLS) approach.

6 RESULT AND DISCUSSION

6.1 Research Result

The results of the tabulated data were then tested

using Outer Model to get a model that is suitable for

the study. Based on the results of data processing a

fit model was obtained, which is then further

checked for the inner model.

The testing for inner model is conducted to

confirm the research hypotheses that have been

proposed eariler. Table 1 show the results of inner

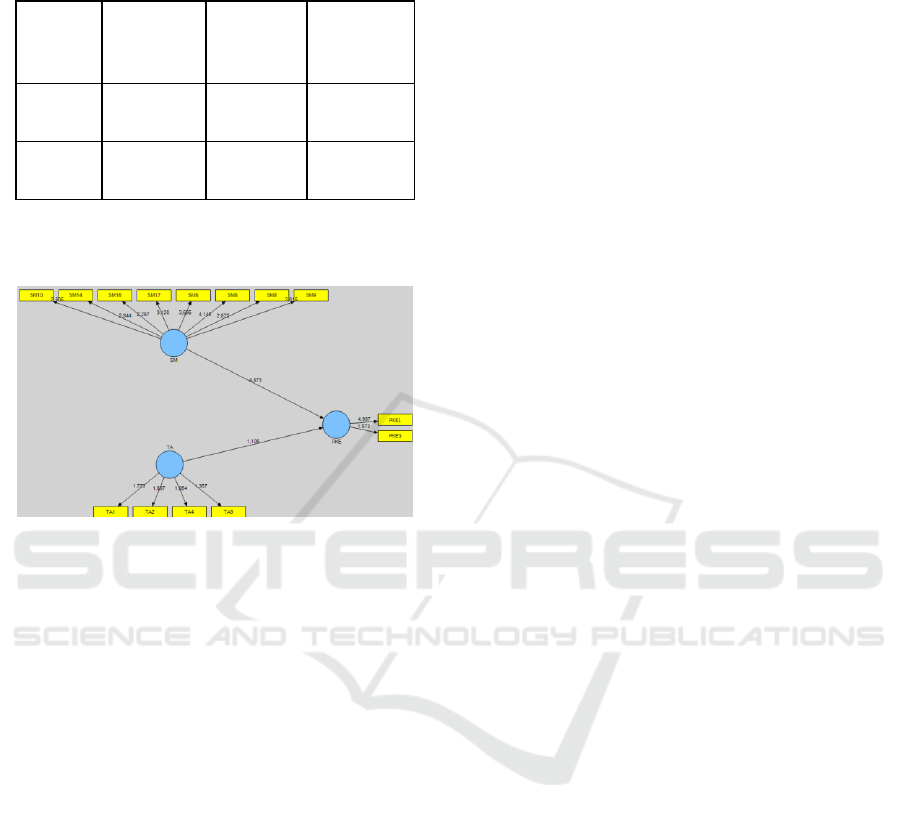

model testing. Based on the Table 1, it can be seen

that the first hypothesis declaring that there is a

significant positive relationship between

Machevilian Characteristics and Auditor Ethical

Decisions is accepted, because arithmetic t is 4.87

greater than t table of 1.96.

Table 1: Inner model and Path Coefficient Testing

Original

Sample

(O)

Standard

Error

(STERR)

T-Statistic

(O/STERR)

SM -> PKE

-0,392024

0,080441

4,873429

TA -> PKE

-0,203261

0,183863

1,105498

Whereas, the second hypothesis stating that there

is a significant negative correlation between Auditee

Pressure and Auditor Ethical Decision Making is

rejected, because the arithmetic t of 1.10 is smaller

than t table of 1.96.

Based on the above data, a research equation to

describe the research model used in this study is then

formulated. The research model produced is as

follows:

AED = -0,39SM – 0,20TA + e

By the equation above, it can be explained that

every change in one additional macheavilian

character will reduce Ethical Decision Making by

0.39 and an addition of one Auditee Pressure will

reduce Ethical Decision Making by 0.20.

6.2 Discussion

6.2.1 The Effect of Macheavilian

Characteristics on Auditor’s Ethical

Decision Making

Based on the results of research data processing,

Macheavillian Characteristics are found to have

significant negative effect on auditor ethical

decisions. This indicates that government auditors

who are the sample of the study are having a low

Machevilian characteristics. Where based on these

results, government auditors respond negatively to

the possibility of fraud that they can do during the

audit. Thus, they are capable of making ethical

decisions that do not oppose to the applicable

regulations.

The low macheavillian charateristics of

government auditors is inseparable from the code of

ethics that is always maintained by government

auditors. Strict sanctions contained in the code of

ethics for government employees, particularly the

auditors, are contributing to the integrities held by

government auditors to avoid acts that are against

the regulations (machevilian characteristics) even

The Effect of Machiavellian Characteristics and Auditee Pressure on Ethical Decision Making of Government Auditors in Palembang

Municipality

719

though the decision may provide individual and

financial benefits to the relevant auditor.

The macheavillian character of every

government auditor could be repressed through

continuous training for the auditors. The training

should not only related to the auditor's technical

abilities but also to instill an attitude that maintain

the ethical code of government auditors.

To prevent the growing of machevillian

characters in government auditors, Peer Review by

superiors or by a team formed by the government is

conducted as well, that is based on the results of

audits performed by government auditors. Review

on the audit results becomes a detection control

carried out by the government to ensure that the

implementation of the audits that have been carried

out are free from the possibility of code of ethics

violations that might be conducted by the auditor

during the auditing process.

The prevention should not only organized by the

internal government, but also by the community.

The audit results that are accessible by the public are

factors that are accounted for by government

auditors. The audit results, that are not in line with

the facts, will lead to negative opinion in the

community so that public may submit complaints to

request a review on the results of the audit been

conducted

6.2.2 The Effect of Auditee Pressure on

Auditor Ethical Decisions

Based on the results of this study, it can be

confirmed that the pressure imposed by the auditee

during and after the audit did not significantly

influence the Ethical Decision of the Auditor. The

pressure made by the auditee was responded

negatively by government auditors. This indicates

that government auditors are free from auditee

pressure in making their decisions, or in other

words, the auditors are independent in their decision

making.

The self-determination in decision making is

made possible by the incentives obtained by

government auditors has fulfilled the auditors needs.

The amount of incentives gained by the auditors has

made them invulnerable to be affected by the

facilities offered by the auditee during the audit.

A strict code of ethics also influences

government auditors to be free from the pressure

imposed by the auditee. The civil servants’ code of

ethics regulates the relationship between the auditor

and the auditee during the audit, where the auditor is

prohibited from having any relationship that may

disrupt the auditor's objectivity and is prohibited

from receiving any facility provided by the auditee.

The pressure made by the auditee to manipulate

the audit is also becoming an indicator for the

auditor that the auditee being evaluated has the

possibility of committing serious violations. By this

assumption, the auditor will respond negatively to

the pressure, because if the auditors adhere to the

auditee's request, the audit results will not be

independent and the opinion produced is not

objective, in addition, there might be a possibility of

ethical violations by the auditor that will lead to

sanctions for the auditor’s actions.

7 CONCLUSION

Based on the data that has been collected and the

testing that has been conducted by model testing

using PLS analysis, the conclusions taken are as

follows:

1. Machevillian Characreristics has a significant

negative effect on Ethical Decision Making of

government auditors in Palembang.

2. Auditee pressure does not significantly influence

Ethical Decision Making of government auditors

in Palembang municipality.

8 LIMITATION AND FUTURE

RESEARCH

1. The sample of this study is covering only

government auditors in the BPK and BPKP in

Palembang so that the results of the study cannot

be generalized.

2. The number of variables used in this study is

very limited so that it greatly affects the

suitability of the model being used.

3. It is recommended to expand the research

population and sample to cover external auditors

from the Public Accounting Office (KAP) who

have examined government financial reports.

REFERENCES

Arens, Alvin., Elder, Randal J., Beasley, Mark S. 2003.

“Auditing and Insurance Service: An Integrated

Approach, Ninth Edition”. Prentice Hall, New Jesey.

Bertens, K. 2000. “Pengantar Etika Bisnis”. Penerbit

Kanisius: Yogyakarta.

Christie, Richard and Geis, Florence L. 1970. Studies in

Machiavellianism. Academic Press

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

720

Devaluisa, Titanny and Handayani, Sri. 2009. Hubungan

Pertimbangan Etis, Perilaku Machiavellian dan

Gender dalam Pengambilan Keputusan Etis: (Studi

pada mahasiswa S1 Akuntansi dan Mahasiswa PPA di

Universitas Diponegoro dan Auditor di Semarang.

Skipsi. Undip

Duska, Ronald F and Duska, Brenda Shay. 2003.

Accounting Ethics. Blackwell Publishing

Harhinto, Teguh. 2004. “Pengaruh Keahlian dan

Independensi Terhadap Kualitas

Audit Studi Empiris”. Universitas Diponegoro, Semarang.

Murphy, P. R. 2012. “Attitude, Machiavellianism and the

rationalization of misreporting”. Accounting,

Organizations and Society, 37 (4), 242-259.

O’Leary, C., & Cotter D. 2000. “The Ethics of Final Year

Accountancy Students:an International Comparison”.

Managerial Auditing Journal.

Purnamasari, S. V. 2006. “Sifat Machiavellian dan

Pertimbangan Etis”. Paper Dipresentasikan pada

Acara Simposium Nasional Akuntansi IX, Padang.

Rest, J. R. 1986. “Issues and Methodology in Moral

Judgment”. Dalam S. Modgil dan C. Modgil (Ed.).

Lawrence Kohlberg: Consensus and Controversy.

Philadelphia, PA: Falmer Press.

Rest, J., S. J. Thoma, Y. L. Moon, dan I. Getz. 1986.

“Different Cultures, Sexes, and Religions”. Dalam J.

Rest (ed.). Moral Development: Advances in Research

and Theory. NY: Praeger.

Richmond, K. A. 2001. “Ethical Reasoning, Machiavellian

Behavior, dan Gender: The Impact on Accounting

Students’ Ethical Decision Making”. Phd Dissertation,

Virginia Polytechnic Institute dan State University.

Robbins, R. W., & Wallace, W. A. (2007). “Decision

support for ethical problem solving: A multi-agent

approach”. Decision Support Systems, 43(4), 1571-

1587.

Robbins, Stephen P. 2003. “Perilaku Organisasi Jilid 1”.

Edisi 9. Penerjemah Tim Indeks. Jakarta : PT. Indeks,

Gramedia Grup

Shafer, William E dan Richard S. Simmons. 2008. “Social

Responsibility, Machiavellianism, and Tax

Avoidance: A Study of HongKong Tax Professionals”.

Accounting, Auditing, and Accountability Journal,

Vol.21, No. 5, pp. 695-720

Wisesa, Anggara. 2011. Integritas Moral dalam Konteks

Pengambilan Keputusan Etis. Jurnal Manajemen

Teknologi. Vol.10 No.1

APPENDIX

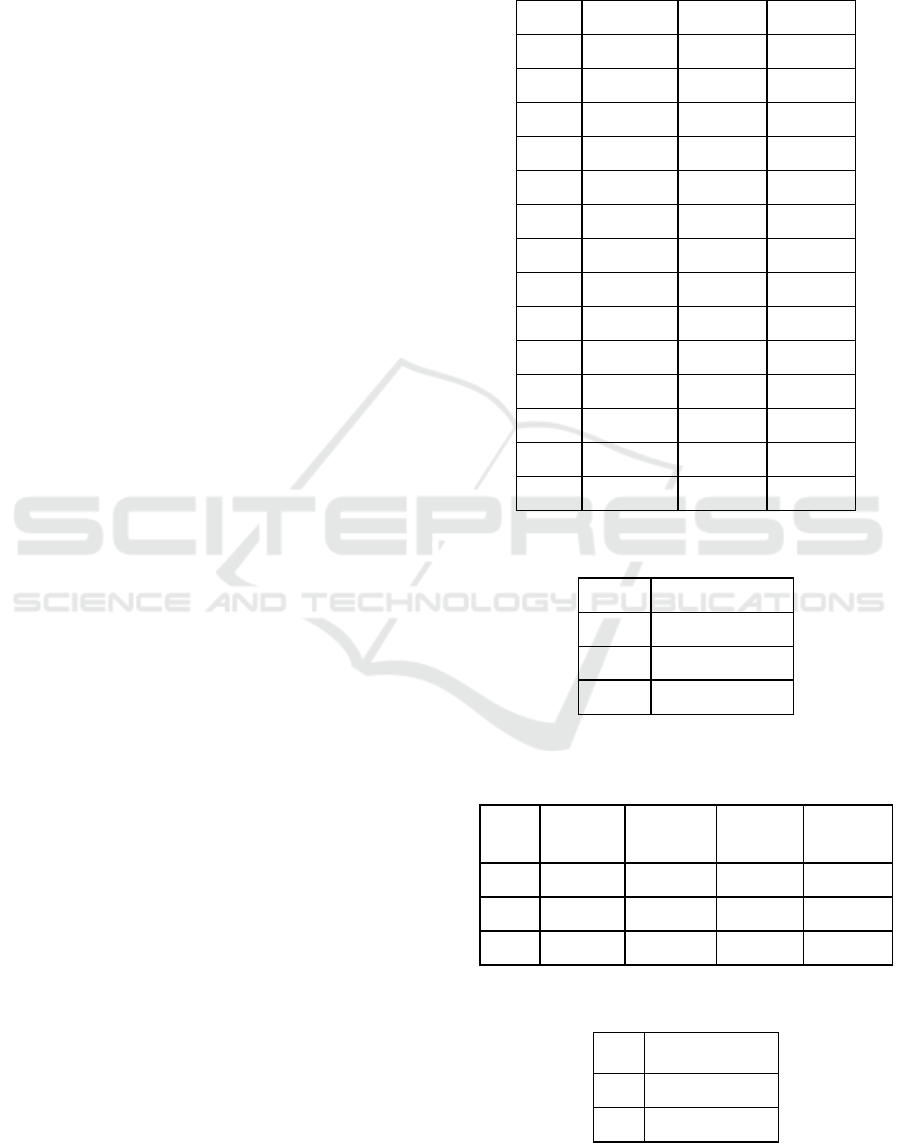

AP-1 Outer Loading

PKE

SM

TA

PKE1

0,934650

PKE3

0,702175

SM10

0,595644

SM14

0,562902

SM15

0,585038

SM17

0,693328

SM5

0,562477

SM6

0,640265

SM8

0,561457

SM9

0,625661

TA1

0,747037

TA2

0,697947

TA4

0,727148

TA8

-0,615385

AP-2 AVE

AVE

PKE

0,683310

SM

0,552578

TA

0,588160

AP-3 Composite Reability, R-Square, Cronbach

Alpha, Communality

CR

R

Square

CA

C

PKE

0,808795

0,608023

0,574605

0,683309

SM

0,811808

0,756002

0,552578

TA

0,542062

0,596453

0,588159

AP-4 Inner Model

PKE

SM

4,873429

TA

1,105498

The Effect of Machiavellian Characteristics and Auditee Pressure on Ethical Decision Making of Government Auditors in Palembang

Municipality

721

AP-5 Path C

Original

Sample (O)

Standard

Error

(STERR)

T-Statistic

(O/STERR)

SM ->

PKE

-0,392024

0,080441

4,873429

TA ->

PKE

-0,203261

0,183863

1,105498

Coefficient

AP-6 Path Diagram

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

722