The Impact of Accounting Information Characteristics on Managerial

Performance in Distance Learning Program Unit of Open University

of Indonesia (UPBJJ-UT)

Zein Ghozali

1

, Bernadette Robiani

2

and Burhanuddin

2

1

Universitas Sjakhyakirti, Indonesia

2

Universitas Sriwijaya, Indonesia

Keywords: Accounting Information Characteristics, Managerial Performance

Abstract: One effort that can be done to improve managerial performance is to increase the important role of

accounting information systems in providing accounting information in the form of financial information

and non-financial information needed by external and internal parties that can provide value added to the

right people in the right way and at the right time. This study uses 5 accounting information characteristics

as the independent variable which is written in the Guidelines for Preparation of Public Service Agency

Financial Statements (BLU) in the Ministry of Education and Culture based on the Government Accounting

System in 2012, and managerial performance as the dependent variable. The aim of paper was to analyze

the effect of the accounting information characteristics on managerial performance in the Distance Learning

Program Unit of Open University (UPBJJ-UT). This research was conducted in 2017 in 37 UPBJJ-UT that

were spread throughout Indonesia by using multiple linear regression analysis. Primary data used in the

form of a questionnaire to 111 respondents as a sample consisting of Head of Unit, Head of Administration,

and Treasurer. The results of the research are partially and simultaneously show the accounting information

characteristics; relevant, reliable, comparable, comprehensible, and the substance over form had a

significant influence on managerial performance. This paper contributes to the accounting information

system literature by providing an understanding of the impact of the accounting information characteristics

on managerial performance.

1 INTRODUCTION

Information is a resource for the organization, so

it is expected that it will be able to help the

organization towards achieving its vision, mission

and goals. Information available and used by

management is very helpful in completing various

economic activities, so it is expected that the

company's performance will increase.(Sayyida,

2013). As described by (Hall and Bennett, 2011) The

application of accounting information systems in an

organization plays an important role in supporting

managerial performance. Accounting information

systems play a role in increasing management's

ability to understand the state of the surrounding

environment and identify relevant activities. And the

theory put forward by (Chenhall and Morris, 1986)

in (Laitinen, 2008) that Information quality is

affected by the information system scope. The scope

refers to the dimensions of the focus, quantification

and time horizon and concentrates on the dimensions

of information produced by information system. The

focus dimension investigates if information is

internal or external, the quantification dimension

on whether information is financial or non-

financial, and the time horizon dimension on

whether information is future or historically

oriented.

Based on (Constitution, 2004) Regarding

concerning Management Check and Responsibility

of State Finance and (Government Regulation, 2006)

concerning Financial Reporting and Performance of

Government Agencies, the status of the Open

University as a State College was established in

1984 (Presidential Decree, 1984) to be Public

Service Agency Financial Management (PK-BLU)

with a present need to improve the quality of

education implementation, improve service

performance for the community, improve financial

Ghozali, Z., Robiani, B. and Burhanuddin, .

The Impact of Accounting Information Characteristics on Managerial Performance in Distance Learning Program Unit of Open University of Indonesia (UPBJJ-UT).

DOI: 10.5220/0008438301890197

In Proceedings of the 4th Sriwijaya Economics, Accounting, and Business Conference (SEABC 2018), pages 189-197

ISBN: 978-989-758-387-2

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

189

performance which is ultimately expected to

increase benefits for the community. Having the

status of the PK-BLU, the Ministry of National

Education which is currently the Ministry of

Research, Technology and Higher Education

(Kemristekdikti) makes the rules outlined

(Regulation of Minister of Education and Culture,

2014) concerning Accounting Guidelines and State

Collage Financial Reporting that Implement

Management Public Service Agency Finance. In the

policy it is stated that the Open University must have

an Accounting Information System that is capable of

presenting financial and non-financial accounting

information in accordance with the standard quality

report characteristics. The Distance Learning

Program Unit (UPBJJ) is a technical implementation

unit of the Open University in the area. The

functions and tasks of UPBJJ-UT are as a place for

students of the Open University to carry out

academic administrative activities and academic

activities. For daily activities, UPBJJ-UT has the

task of implementing distance learning services.

The results of the preliminary survey with the

Monitoring Team at the UPBJJ-UT’s Palembang

Office and several other UPBJJ-UT offices, obtained

the phenomenon that the quality of accounting

information about financial and non-financial

information produced by Accounting Information in

the UPBJJ-UT’s Palembang Office and several other

UBBJJ-UT offices had not fulfill the five standard

aspects of report quality characteristics as

appropriate. Where, there is still fraud and violation

of standard procedures in presenting information in

it. This can be seen from the report on the

implementation of academic administrative service

activities which include registration and testing

activities as well as reports on the implementation of

learning assistance service activities and teaching

materials services which include the implementation

of tutorials, co-extracurricular activities. The

information presented in these reports is less

relevant because it is not timely and incomplete. In

addition, the report presented is relatively less

reliable because the information submitted is

dishonest and inaccurate, and lacks of substance to

outperform the form because the information is less

reliable. Based on this phenomenon it can be stated

that information that is less relevant, less reliable

and lacking in substance has an impact on

management's decision making in setting a policy

that is often not in accordance with conditions in the

field.Therefore researchers are interested in

analyzing how much influence the characteristics of

accounting information on managerial performance

on UPBJJ-UT.

This paper consists of 5 parts. First, outlines the

literature review. Second, we will discuss how the

methodological framework is built. Third, the

findings of testing hypotheses that show a

fundamental problem in the effect of accounting

information characteristics on managerial

performance. Fourth, a discussion of how much

influence the characteristics of accounting

information on managerial performance partially and

simultaneously. Fifth, the conclusion is to evaluate

the ability of the method in explaining the problem.

2 LITERATURE REVIEW

The grand theory used in this study is The Goal

Setting Theory is part of the motivation theory

proposed by Edwin Locke in 1978. This theory

emphasizes the important relationship between goals

and performance. According to (Locke and Latham,

2002), in (Lunenburg, 2011) goals have a broad

influence on employee behavior and organizational

performance and management practices. Generally,

managers accept goal setting as being very

meaningful to improve and maintain performance

(Dubrin, 2010) in (Lunenburg, 2011). Based on

hundreds of studies that have been conducted, the

main finding of the Goal Setting Theory is that

people who are given specific goals are difficult but

it can be achieved, has better performance than

people who accept goals that are easy and specific or

have no goals at the same time, at the same time

someone must have sufficient ability, accept the

goals set and receive relevant feedback with

performance (Latham, 2003) in (Lunenburg, 2011).

Several previous studies that were relevant to the

researchers made reference in the preparation of this

thesis, including the research conducted by Agbejule

(2005) in (Murtini, 2015), revealing managerial

performance is influenced by interactions between

management accounting information systems and

perceived environmental uncertainty. So, the higher

the level of perceived environmental uncertainty

faced by a company, the higher the usefulness of the

Management Accounting Information System is

expected to improve managerial performance. Then

the (Sayyida, 2013) study of the effect of accounting

information systems focused on Information

Characteristics variables (understandable, relevant,

reliability, and comparable) on company

performance with case studies at PT. BPRS Bhakti

Sumekar Sumenep, shows that the simultaneous

analysis of independent variables does not

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

190

significantly affect the dependent variable. While the

partial analysis of the results is varied, the variables

can be understood and reliability does not

significantly influence the performance of the

company, the reliability variable has a negative

constant coefficient that is contrary to basic

assumptions and theories.

Based on research revealed by (Siamak, 2012)

Accounting Information Systems are all related

components collected to collect information, raw

data or ordinary data and turn it into financial data

for the purpose of reporting it to decision makers

(Mahdi Salehi, vahab rostami and Abdolkarim

Mogadam, 2010). To better understand the term

'Accounting Information Systems' will be described

separately. First, the literature documents that

accounting can be identified into three components,

namely information systems, "business languages"

and financial information sources (Wilkinson, 1993:

6-7). Second, information is valuable data

processing that provides the basis for making

decisions, taking action and fulfilling legal

obligations. Finally, the system is an integrated

entity, where the framework is focused on a set of

goals (Bhatt, 2001; Thomas and Kleiner, 1995) in

(Siamak, 2012).

Benefit is a characteristic that can only be

determined qualitatively in relation to user decisions,

users and beliefs about information. This criterion is

generally called qualitative characteristics or

information quality. Criteria and forming elements

of information quality that make information in a

report have value or benefit (Winidyaningrum,

2010). UPBJJ-UT has implemented Accounting

Information which is expected to be able to present

information guided by (Financial Bureau - General

Secretary of Ministry of Education and Culture,

2012) Guidelines for Preparing Public Service

Agency Financial Statements (BLU) in the Ministry

of Education and Culture Based on Government

Accounting Systems In 2012 (Government

Regulations, 2010), among others: (1) relevant, that

the report produced must have the benefits of

feedback, predictive, timely and complete benefits;

(2) reliable, reports must be presented in an honest,

verifiable, neutral and accurate manner; (3)

comparable, both information comparisons between

periods and comparisons of internal and external

information; (4) comprehensible, that the report

must present information that is easily understood

and can be understood by the user; and (5)

Substance Over Form, that the report must present

information that is reliable, concise and easily

accessible. Characteristics of accounting information

produced by UPBJJ-UT must meet the

characteristics of the report quality standards that

have been set.

Managerial performance is a measure of how

effectively and efficiently managers have worked to

achieve organizational goals (Stoner 1992).

Evaluation of the performance carried out by

managers varies depending on the culture developed

by each company (Ivancevich 1999: 187). The

following are some of the measures used to evaluate

management performance, based on non-financial

perspectives, among others, First: The ability of

managers to plan (Schermerhorn 1999: 138) Good

planning can increase the focus and flexibility of

managers in handling their work. The issue of focus

and flexibility are two important things in a high and

dynamic competitive environment. The ability of

managers to make plans can be one indicator to

measure manager performance. (Nazaruddin 1998:

149) in (Juniarti and Evelyne, 2003). Second: Ability

to reach targets. Manager's performance can be

measured by their ability to achieve what has been

planned (Mulyadi 2001: 302). Targets must be quite

specific, involve participants, be realistic and

challenging and have a clear time span (Hess 1996:

83) in (Juniarti and Evelyne, 2003), and Third: Gait

managers outside the company. The intensity of

managers in representing companies to deal with

outsiders shows the company's trust in the manager.

This trust can arise due to several things, one of

which is the good performance of the manager.

Wagner (1995: 50) also revealed that the role of

managers in representing companies shows the level

of performance in (Juniarti and Evelyne, 2003).

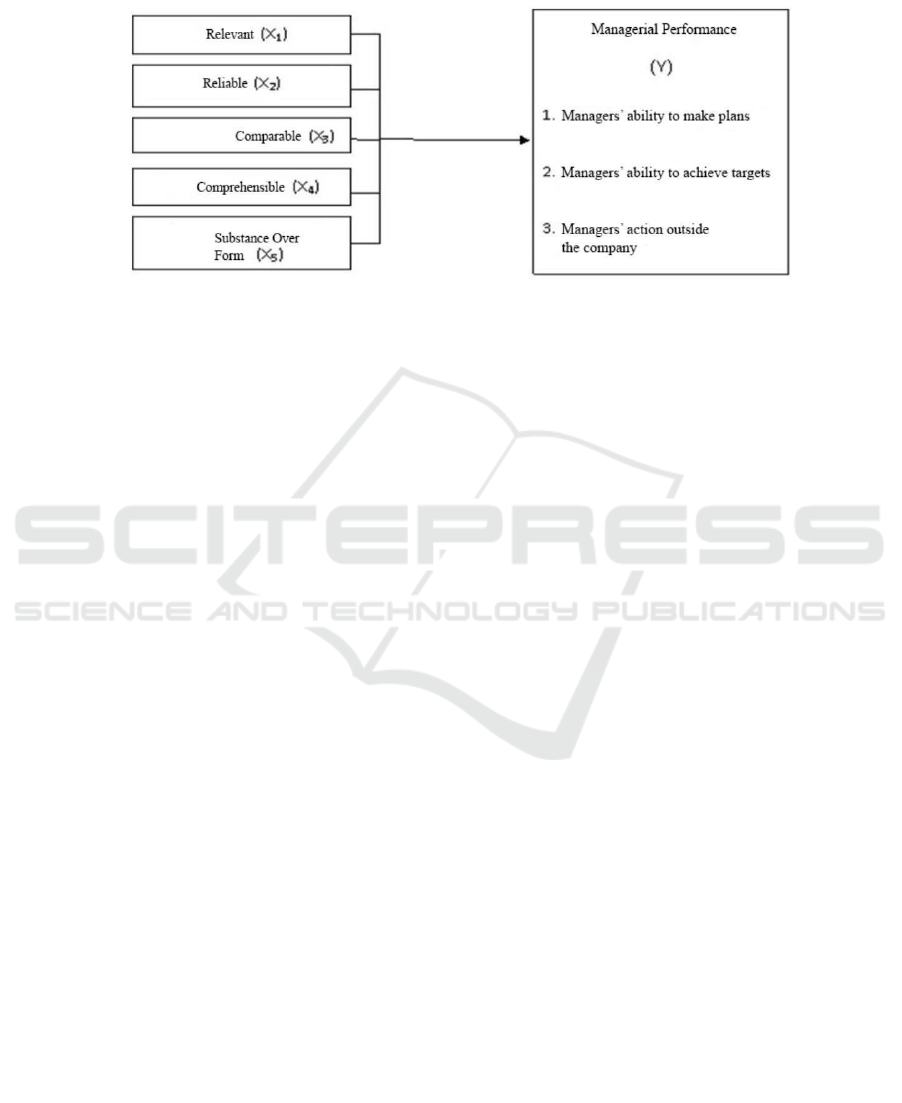

In this paper, there are 5 variables that are used

by researchers as independent variables are written

in (Financial Bureau - General Secretary of Ministry

of Education and Culture, 2012) Guidelines for

Preparation of Public Service Agency Financial

Reports (BLU) in the Ministry of Education and

Culture Based on Accounting Government Standard

of 2012 (Government Regulations, 2010) among

others: (1) relevant, (2) reliable, (3) comparable, (4)

comprehensible, and (5) Substance Over Form.

For the dependent variable, researchers used

previous research conducted by (Juniarti and

Evelyne, 2003) which examined the relationship

between information characteristics and managerial

performance. Managerial performance variables are

measured by how effective and efficient managers

are able to carry out management functions in

achieving organizational goals by mobilizing the

talents and abilities and efforts of several other

people within the authority area of the UPBJJ-UT,

The Impact of Accounting Information Characteristics on Managerial Performance in Distance Learning Program Unit of Open University

of Indonesia (UPBJJ-UT)

191

including; manager’s ability to plan, manager’s

ability to achieve targets and manager’s action

outside the company.

Based on background and problems of this paper,

the researchers describe the research framework as

seen in Figure 1 below.

Figure 1: Frame work

3 HYPOTHESIS

Ha1 : Partially, relevant, reliable, comparable,

comprehensible, and substance over form

accounting information characteristics affect

managerial performance in UPBJJ-UT.

Ha2: Simulataneously, relevant, reliable,

comparable, comprehensible, and substance

over form accounting information

characteristics affect managerial performance

in UPBJJ-UT.

4 RESEARCH METHOD

Based on the literature and previous research,

this study analyzes the characteristics of accounting

information that affect managerial performance in

the Open University Distance Learning Program

Unit (UPBJJ-UT). Variable characteristics of

accounting information (X) are measured through

five variables consisting of relevant (X

1

), reliable

(X

2

), comparable (X

3

), comprehensible (X

4

), and

Substance Over Form (X

5

). While the dependent

variable (Y) is managerial performance, measured

by indicators: the ability of managers to plan, the

ability to achieve targets, and the gait of managers

outside the company. Primary data used for multiple

linear regression analysis by distributing

questionnaires to 111 respondents as samples

consisting of Head of Unit, Head of dministration,

and Treasurer at 37 UT-UPBJJ spread throughout

Indonesia for 2 months, namely from February to

March 2017.

5 HYPOTESIS TESTING

Analysis of Descriptive Statistics Data Variables

(X) Characteristics of accounting information

with Managerial Performance Variables (Y) at

UPBJJ-UT

Statistical test analysis is used to answer the

research objectives, namely knowing the effect of

independent variables (X) Characteristics of

accounting information consisting of relevant (X

1

),

reliable (X

2

), comparable (X

3

), comprehensible (X

4

),

and Substance Over Form (X

5

) on the dependent

variable (Y) managerial performance in UT-UPBJJ

simultaneously or partially is to use the statistical

method of multiple linear regression analysis. Table

1 below is a summary of the results of multiple

linear regression analysis The Effect of Free

Variables (X) Characteristics of accounting

information on Bound Variables (Y) Managerial

Performance as seen in Table 1 below:

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

192

Table 1: Comparison of Variable Performance Score Data Characteristics of accounting information And Managerial

Performance Variables

Independent Variables

Accounting Information

Characteristics

Achievement Score

Dependent Variable

Managerial Performance

Achievement Score

Averag

e

%

Result

Averag

e

%

Result

1.

Relevant (X

1

)

3.56

71.28

High

1.

Manager’s ablity to make

plan

3.59

71.89

High

2.

Reliable (X

2

),

3.66

73.15

High

2.

Manager’s ability to

achieve target

3.30

66.40

Medium

3.

Comparable (X

3

),

3.57

71.49

High

4.

Comprehensible (X

4

),

3.57

71.44

High

3.

Manager’s action outside

the company

3.48

71.14

High

5.

Substance Over Form (X

5

)

3.57

71.49

High

Variable Average Score

3.59

71.77

High

Variable Average Score

3.42

71.04

Medium

Based on Table 1 the performance score data

from the descriptive statistical analysis on the

independent variable (X) The characteristics of

accounting information consist of relevant (X1),

reliable (X2), comparable (X3), understandable (X4)

and Substance Over Form (Substance Over Form )

(X5) and the dependent variable (Y) of managerial

performance, it was found that the comparison of the

performance score scores for the implementation of

the two variables was not much different, which

were both in the high / good category. This can be

seen from the average score of achievement in each

variable, namely the characteristic variable of

accounting information (X) in general obtained a

score of 3.59 (high / good category) with the

percentage of variable implementation rate of

71.77% of the maximum score . These results are

obtained based on a summary of the score of the

results of each sub-variable consisting of relevant

variables (X1) which is 3.56 with an implementation

level of 71.28% (high / good), reliable variable (X2)

of 3, 66 with an implementation level of 73.15%

(high / good), comparable variable (X3) of 3.57 with

an implementation level of 71.49% (high / good),

variable can be understood (X4) of 3.57 with the

implementation level is 71.44% (high / good) and

variable (X5) the substance outperforms (Substance

Over Form) of 3.57 with an implementation level of

71.49% (high / good). While the performance score

of the implementation of the UPBJJ-UT managerial

performance variable in terms of its three

dimensions which include the ability to plan, the

ability to achieve targets, and the gait of managers

outside the company, the average score of the

variable score is 3.42 with a percentage of 71.04%

which is also in the high / good category.

Table 2: Summary of Results of Double Linear Regression Analysis Effect of Free Variables (X) Characteristics of

accounting information on Bound Variables (Y) Managerial Performance

Variable

Regression

Coefficient

t-count

Sig

Constant

15.239

Relevant (X

1

)

0.494

3.313

0.001

Reliable (X

2

)

0.342

2.915

0.004

Comparable (X

3

)

0.164

2.562

0.012

Comprehensible (X

4

)

0.134

2.205

0.025

Substance over form (X

5

)

0.179

2.365

0.017

Coefficient of Correlation (R)

0.729

Coefficient of determination

(R-square)

0.531

F-Count

12.191

Sig.F

0.000

Based on the results of the multiple linear regression statistical test data in Table 2 above, the

The Impact of Accounting Information Characteristics on Managerial Performance in Distance Learning Program Unit of Open University

of Indonesia (UPBJJ-UT)

193

alues obtained for estimating the regression equation

model for the dependent variable (Y) managerial

performance are:

Y = 15,239 + 0,494

X1

+ 0,342

X2

+ 0,164

X3

+ 0,134

X4

+ 0,179

X5

Based on the data in the regression equation model

above, it can be explained as follows:

a. The constant value is 15,239, so it can be

interpreted that the managerial performance

value at this time is 15,239 (points) with the

assumption that the characteristics of accounting

information consisting of relevant, reliable,

comparable, understandable and substance

outperforms (constant).

b. The relevant variable regression coefficient (X1)

is positive at 0.494 with a probability level (p-

value) of 0.001 (<0.05). Based on this value it

can be assumed that every increase in relevant

factors in the characteristics of accounting

information by 1 point then the managerial

performance value will increase by 0.494 points

higher than the previous value.

c. The reliable variable regression coefficient (X2)

has a positive sign of 0.342 with a probability

level (p-value) of 0.004 (<0.05). Based on this

value it can be assumed that every increase in the

value of reliability in the characteristics of

accounting information by 1 point then the

managerial performance value will increase by

0.342 points higher than the previous value.

d. The regression coefficients of comparable

variables (X3) are positive at 0.164 with a

probability level (p-value) of 0.012 (<0.05).

Based on this value it can be assumed that every

increase in value can be compared in the

characteristics of accounting information by 1

point, the managerial performance value will

also increase by 0.164 points higher than the

previous value.

e. The variable regression coefficient value can be

understood (X4) with a positive sign of 0.134

with a probability level (p-value) of 0.025

(<0.05). Based on this value it can be assumed

that every increase in value can be understood in

the characteristics of accounting information by

1 point, the value of managerial performance will

increase by 0.134 points higher than the previous

value.

f. The substance variable regression coefficient

surpasses form (X5) with a positive sign of 0.179

with a probability level (p-value) of 0.017

(<0.05). Based on this value it can be assumed

that every increase in substance value

outperforms the characteristics of accounting

information by 1 point, the managerial

performance value will increase by 0.179 points

higher than the previous value.

6 DISCUSSION

6.1 The Impact of Relevant on Managerial

Performance in UPBJJ-UT

Based on the results of the first partial hypothesis

testing H

a1.1

, partially, the relevant characteristics of

accounting information have a significant impact on

managerial performance in UPBJJ-UT. This finding

supports (Sayyida, 2013) research which stated that

the Characteristics of relevant quality accounting

information have a significant impact on company

performance.

6.2 The Impact of Reliable on Managerial

Performance in UPBJJ-UT

Based on the results of the second partial

hypothesis testing H

a1.2

, partially, the reliable

characteristics of accounting information have a

significant impact on managerial performance in

UPBJJ-UT. This finding is not in line with research,

that the Characteristics of reliable quality accounting

information do not have a significant impact and

contribute negatively to company performance.

6.3 The Impact of Comparable on Managerial

Performance in UPBJJ-UT

Based on the results of the third partial

hypothesis testing H

a1.3

, partially, the comparable

characteristics of accounting information have a

significant impact on managerial performance in

UPBJJ-UT. This finding is not in line with (Sayyida,

2013) research, that the Characteristics of

comparable quality accounting information do not

have a significant impact on company performance.

6.3 The Impact of Comprehensible on

Managerial Performance in UPBJJ-UT

Based on the results of the fourth partial

hypothesis testing H

a1.4

, partially, the

comprehensible characteristics of accounting

information have a significant impact on managerial

performance in UPBJJ-UT. This finding is not in

line with (Sayyida, 2013) research, that the

Characteristics of comprehensible quality

accounting information do not have a significant

impact on company performance.

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

194

6.4 The Impact of Substance Over Form on

Managerial Performance in UPBJJ-UT

Based on the results of the fifth partial

hypothesis testing H

a1.5

, partially, the substance over

form characteristics of accounting information have

a significant impact on managerial performance in

UPBJJ-UT. Thus, the results of this study indicate

that substance over form factor as one of the

requirements that must be met in the qualitative

characteristics of the financial statements of

accounting information in UPBJJ-UT has a

significant (real) influence on managerial

performance. That is, substance over form

characteristics measured from trustworthiness,

concision and accessibility are factors that

significantly influence the high and low of

managerial performance.

6.5 The Impact of Accounting Information

Characteristics on Managerial Performance in

UPBJJ-UT

Based on the results of H

a2

simultaneous

hypothesis testing, the characteristics of accounting

information consisting of relevancy, reliability,

comparability, comprehensibility and substance over

form simultaneously have a significant (real)

influence on UPBJJ-UT managerial performance (F-

count 12.191> F-table 2.301 and p-value 0.000 < α

0.05, H

a2

is accepted). That is, the high and low of

managerial performance in UPBJJ-UT is

significantly influenced by the quality of the

implementation of the existing Characteristics of

accounting information. This provides evidence that

managerial performance achievement in terms of the

level of effectiveness and work efficiency of

managers in mobilizing their talents and abilities and

the efforts of several other people who are under

their authority to make plans, to achieve work

targets, and to establish relationships with outside

parties to achieve the purpose of the UPBJJ-UT

organization which is in the good enough category is

due to the quality of the implementation in realizing

the relevant, reliable, comparable, comprehensible

and substance over form characteristics.

Therefore, in the future, it is necessary to

improve and refine the implementation of the

relevant, reliable, comparable, comprehensible, and

substance over form characteristics in order to create

better accounting information Characteristics

quality. This must be done because it can contribute

significantly to improving managerial performance,

where the better the quality of the characteristics of

accounting information, the higher the managerial

performance in UPBJJ-UT.

7 CONCLUSION

1. The results in this study indicate that the

relevance factor as one of the requirements that

must be met in the qualitative characteristics of

the financial statements of accounting

information in UPBJJ-UT has a significant (real)

impact on managerial performance. That is, the

relevant characteristics of accounting

information consisting of having the feedback

value, having predictive value, timely, and

complete value are one of the factors that

significantly influence managerial performance.

The higher the quality of the embodiment of

relevant characteristics in accounting

information, the higher the managerial

performance in UPBJJ-UT will be.

Therefore, in the future, there is a need for

improvements and refinements to improve the

implementation of the characteristics of

accounting information with a better level of

relevant quality, for it will make a real

contribution in improving managerial

performance.

2. The results in this study indicate that the

reliability factor as one of the requirements that

must be met in the qualitative characteristics of

the financial statements of accounting

information in UPBJJ-UT has a significant (real)

impact on managerial performance. That is, the

reliable characteristics of accounting information

measured from transparent presentation,

verifiability, neutrality, and accuracy are one of

the factors that significantly influence

managerial performance. The better the

embodiment of reliable characteristics in

accounting information, the higher the

managerial performance in UPBJJ-UT will be.

Therefore, in the future, improvements and

refinements are needed to create characteristics

of accounting information with better quality

level of reliability, for it will contribute

significantly to improve managerial

performance.

3. The results in this study indicate that the

comparability factor as one of the requirements

that must be met in the qualitative characteristics

of the financial statements of accounting

information in UPBJJ-UT has a significant (real)

impact on managerial performance. That is, the

comparable characteristics of accounting

information measured from information

comparison between periods and internal and

external information comparison are one of the

The Impact of Accounting Information Characteristics on Managerial Performance in Distance Learning Program Unit of Open University

of Indonesia (UPBJJ-UT)

195

factors that significantly influence the high and

low of performance produced by UPBJJ-UT

managerial. In this study, the conditions

generating comparable characteristics of

accounting information have a significant impact

on the managerial performance of UPBJJ-UT

because the samples that researchers obtained

such as the Head of Unit, Head of Administration

and Treasurer are staff in the finance and

accounting department.

4. Referring to the opinion of (Romney and

Steinbart, 2015) that the qualitative

characteristics of financial report information

with high comparable quality will be useful for

users in decision making, thus, in the future it is

expected that improvements will be made to

create better comparable quality of accounting

information. This will make a positive

contribution to improving managerial

performance, because the better the quality of

comparable characteristics in accounting

information, the greater the managerial

performance of UPBJJ-UT will increase.

5. The results in this study indicate that the

comprehensibility factor as one of the

requirements that must be met in the qualitative

characteristics of the financial statements of

accounting information in UPBJJ-UT has a

significant (real) impact on managerial

performance. That is, comprehensible

characteristics of accounting information

measured from information that is easily

understood and perceived by users are one of the

factors that significantly influence the high and

low of managerial performance. the conditions

generating comprehensible characteristics of

accounting information have a significant impact

on the managerial performance of UPBJJ-UT

because the samples that researchers obtained

such as the Head of Unit, Head of Administration

and Treasurer are staff in the finance and

accounting department.

According to (Hall and Bennett, 2011),

qualitative characteristics of financial statement

information must be easy to be understood and

perceived by users because it will be useful in

decision making. Referring to the theory, it is

expected that in the future there will be

improvements and refinements to create

characteristics of accounting information with

better comprehensible quality. This will make a

positive contribution to improving managerial

performance, because the better the quality of

comparable characteristics in accounting

information, the greater the managerial

performance of UPBJJ-UT will increase.

6. The better the embodiment of substance over

form characteristics in accounting information,

the higher the managerial performance in UPBJJ-

UT will be. Therefore, in the future,

improvements and refinements are needed to

create characteristics of accounting information

with better quality of substance over form, for it

will contribute significantly to improve

managerial performance.

Based on the description of the results of partial

hypothesis testing above, the quality of relevant,

reliable and substance over form characteristics

in accounting information is the factor that

significantly influences managerial performance,

while comparable and comprehensible

characteristics have no significant influence on

managerial performance in UPBJJ-UT.

8 SUGGESTION

Further studies are needed and should add other

variables since there are still other variables that

may affect the managerial performance. The second

suggestion is that future researchers should conduct

an interview with the respondents so that the results

of the research can be more assured and in

accordance with the object of purpose intended by

the researchers. The third suggestion is that future

researchers should use performance measurement

instruments that are not measured based on the

institution to prevent performance measurement or

performance measurement facilities errors provided

by the institution.

ACKNOWLEDGMENTS

The researchers would like to thank the Rector of

Open University of Indonesia that give me

permission for research in his institution, Rector of

Universitas Sjakhyakirti Palembang for the

motivation and financial support for the

implementation of this research. Researchers are

also grateful to the parties involved in the process of

data collection and data analyzing, and the

completion of this article.

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

196

REFERENCES

Chenhall, R. H. and Morris, D. (1986) ‘The Impact of

Structure, Environment, and Interdependence on the

Perceived Usefulness of Management Accounting

Systems’, Source: The Accounting Review. doi:

10.2307/247520.

Constitution (2004) Constitution of Republik Indonesia

No. 15 year 2004 Concerning Management Check and

Responsibility of State Finance,

https://www.ut.ac.id/en/node/515. doi:

10.1017/CBO9781107415324.004.

Financial Bureau - General Secretary of Ministry of

Education and Culture (2012) ‘Guidelines for

Preparing Public Service Agency Financial Reports

(BLU) in the Ministry of Education and Culture Based

on Government Accounting Standards (SAP)’, pp.

2010–2014. Available at:

http://simkeu.kemdikbud.go.id.

Government Regulation (2006) ‘Government Regulation

No. 8 year 2006 Concerning Financial Reporting and

Performance of Government Agencies’,

https://www.ut.ac.id/en/node/515. Available at:

https://www.ut.ac.id/en/node/515.

Government Regulations (2010) ‘Government Regulation

No. 71 year 2010 Concerning Government Accounting

Standards’, https://www.ut.ac.id/en/node/515, p. 413.

Available at: https://www.ut.ac.id/en/node/515.

Hall, J. A. and Bennett, P. E. (2011) Accounting

information systems. 7th edn, South-Western. 7th edn.

Edited by C. Jack W. South-Western Cengage

Learning. Available at:

http://site.iugaza.edu.ps/hmadi/files/2014/11/JAMES-

AIS_unprotected.pdf.

Juniarti and Evelyne (2003) ‘The Relationship of

Information Characteristics Produced by Management

Accounting Information Systems to Managerial

Performance in Manufacturing Companies in East

Java’, Jurnal Akuntansi dan Keuangan. doi:

10.1093/acprof.

Laitinen, E. K. (2008) ‘Extracting appropriate scope for

information systems: A case study’, Industrial

Management & Data Systems, 109(3), pp. 305–321.

doi: 10.1108/02635570910939353.

Lunenburg, F. C. (2011) ‘Goal-setting theory of

motivation’, International Journal of Management,

Business, and Administration, 15(1), pp. 1–6. doi:

10.1111/j.1551-2916.2010.04191.x.

Murtini (2015) ‘Pengaruh Sistem Informasi Akuntansi

Terhadap Kinerja Manajerial Dengan Variabel

Moderasi Strategi Bisnis dan Persepsi Ketidakpastian

Lingkungan’, 8, pp. 75–84. Available at:

http://jurnal.pekalongankota.go.id/index.php/litbang/ar

ticle/view/37/35.

Presidential Decree (1984) ‘Presidential Decree No. 41

year 1984 Concerning The establishment of the Open

University’, 13(1), pp. 7–34. Available at:

http://ditjenpp.kemenkumham.go.id.

Regulation of Minister of Education and Culture (2014)

‘Regulation of Minister of Education and Culture

No.77 Tahun 2014 Concerning Guidelines for

Proposal and Provision of Remuneration for

Management Officers, Supervisory Boards, and

Employees at State Universities that Implement Public

Service Agency Financi’,

https://www.ut.ac.id/en/node/515, 11(3), pp. 287–301.

Available at: https://www.ut.ac.id/en/node/515.

Romney, M. B. and Steinbart, P. J. (2015) ‘Accounting

Information System’, in Pearson. 13 Global. Harlow,

Essex Pearson, p. 734 pages : colour illustrations ; 28

cm. Available at:

http://www.worldcat.org/title/accounting-information-

systems/oclc/921672240.

Sayyida (2013) ‘Pengaruh Karakteristik Sistem Informasi

Akuntansi Terhadap Kinerja Perusahaan’,

PERFORMANCE Bisnis dan Akuntansi, III(2), pp. 17–

30. Available at:

https://www.researchgate.net/publication/316314656_

PENGARUH_KARAKTERISTIK_SISTEM_INFOR

MASI_AKUNTANSI_TERHADAP_KINERJA_PER

USAHAAN.

Siamak, N. S. (2012) ‘The Usefulness of an Accounting

Information System for Effective Organizational

Performance’, International Journal of Economics and

Finance. doi: 10.5539/ijef.v4n5p136.

Winidyaningrum, R. C. (2010) ‘Effect of Human

Resources and Utilization of Information Technology

on Reliability and Timeliness of Local Government

Financial Reporting with Intervening Variables in

Accounting Internal Control (Empirical Study in

Subosukawonosraten Local Government)’, National

Accounting Symposium XIII, Purwokerto. Available at:

www.sna13purwokerto.com.

The Impact of Accounting Information Characteristics on Managerial Performance in Distance Learning Program Unit of Open University

of Indonesia (UPBJJ-UT)

197