Do Young, Female, and Experienced Characteristics of Risk

Oversight Committee Members Accommodate Bank Risk-Taking?

Evidence from Indonesia

Aulia Natasya Irfani Ampri and Ancella Anitawati Hermawan

Department of Accounting, Universitas Indonesia, Depok, Indonesia

Keywords: Risk Oversight Committee; Risk-Taking; Young; Female; Experienced

Abstract: Although risk oversight committee has been mandatory for Indonesian banking industry since 2006, there has

never been any inquiry trying to understand how the characteristics of risk oversight committee members may

impact their tolerance towards bank management risk-taking. Specifically, this research is aimed to shades

light on how young age, female, and risk management experience characteristics of each members affect their

inclination towards accommodating bank risk-taking. The study uses panel data random effect regression for

unique dataset of 27 banks from 2012-2016 and find that contrary to popular belief, increasing number of

younger members reduce accommodation to bank risk-taking. Moreover, increasing female members

composition is proven to rise bank risk-taking. These results are different with increasing proportion of risk

management experienced committee members as they are proven to have no significant effect towards bank

risk-taking behaviour. Additionally, sensitivity tests conducted using average age as young indicator and

loosening risk management experience criteria by including previous risk oversight committee experience

prove that these characteristics are not impacting bank risk-taking. However, presence of female members in

risk oversight committee have significant impact on improving accommodation to bank risk-taking.

1 INTRODUCTION

The banking industry is a highly volatile industry

in which failure of a bank could destroy the whole

system simultaneously and unexpectedly (Talavera,

Yin, & Zhang, 2018). Moreover, as the nature of

banking is as intermediary institution between those

who have excess money and in need of money

(Undang-Undang No. 10/1998), banks are obliged to

have high-quality governance. The enormous amount

of public funds on its hand and high possibility on

making global crisis due to the high interconnection

makes the banking industry in need of exceptionally

good bank governance (BCBS, 2015).

Banks are facing risks on daily basis (POJK

18/POJK.03/2016). The amount of risk taking,

furthermore, is an important matter. Bank must

manage the risk and reward opportunity cost of the

industry (Haneef, Rana, & Karim, 2012). In order to

ensure executive risk management and risk-taking

decisions, board of commissioner is obliged to create

risk oversight committee (POJK 18/POJK.03/2016).

Although the committee existence is obliged since

2006 (PBI No. 8/4/PBI/2006), there are still very

limited research investigating risk oversight

committee effectiveness and characteristics. Apart

from the fact that most research limits itself to

exclude financial industries (Battaglia & Gallo, 2015;

M. Mayur & Saravanan, 2017). Andarini&Januarti

(2012) expressed that previous research on board of

commissioners' committees are only observing audit

committee as well as nomination and remuneration

committee. Subramaniam et al. (2009) infer that the

phenomenon is due to the lack of empirical

information regarding the characteristics of risk

oversight committee and the fact that the committee

is still relatively new.

Aiming to answer the said question, this research

explores the relationship between gender, age, and

risk management experienced members of banking

risk oversight committee to their tolerance towards

bank risk-taking. It is interesting to deeply explore

this field as the inherent nature of younger age,

female, and experienced characteristics to risk-taking

previous research each contains conflicting views

(Hirshleifer&Thakor, 1992; Serfling, 2014; Harris et

Natasya Irfani Ampri, A. and Anitawati Hermawan, A.

Do Young, Female, and Experienced Characteristics of Risk Oversight Committee Members Accommodate Bank Risk-Taking? Evidence from Indonesia.

DOI: 10.5220/0008436900650074

In Proceedings of the 4th Sriwijaya Economics, Accounting, and Business Conference (SEABC 2018), pages 65-74

ISBN: 978-989-758-387-2

Copyright

c

2019 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

65

al, 2007; Adams & Funk, 2012; Eichner and Lachner,

2017; Garcia-Sanchez, Garcia-Meca & Cudrado

Balles; 2017). Through unique hand-collected data of

Indonesia conventional banks from 2012 to 2016, this

paper is also filling the vacuum of knowledge on

emerging country bank risk-taking behavior as most

risk-taking studies in Asia are conducted in China and

India (Battaglia & Gallo, 2015; Liang et al., 2013;

Talavera et al., 2018). As far as it could be

ascertained, this is the first study showing how young

age, gender, and risk management experienced risk

oversight committee member characteristics is

relevant to bank risk-taking in a way consistent to

bank highly regulated environment. This study would

provide insights to regulators for an ideal composition

of bank board; to investors so they could invest in

banks with similar risk appetite; and to Board of

Commissioner to pick the right candidates suiting

bank risk-appetite.

2 LITERATURE REVIEW AND

HYPOTHESES DEVELOPMENT

2.1 Risk-Taking

Risk-taking is the option on taking unsafe

decision by the company among the pool of other

possible decision. Risk-taking choices are made on

the range of risk appetite or the extent an organization

would like to take risk. Risk-lover organization tends

to make many risky decisions while the risk averse

organizations are less inclined to take risk.

There are various internal and external

motivations underlying risk-taking behavior.

Atkinson (1957) found that there are two chains of

activities related to this: (1) acknowledging

individual reasons for choosing an action compared

to other actions and (2) measuring the implications of

the treatment. He then argues that motives,

expectations, and incentives determine the risk-taking

action of an entity. Fan et al. (2016) add that

competition motives, an external factor, does not

increase the risk-taking behavior by banks. Reducing

regulation in banking activities can increase

competition and make the banking industry more

stable.

Risk-taking behavior can have a positive and

negative impact on the company. IFC (2012) explains

that risk-taking can have a positive impact when (1)

the company can perform good operational

management so that cash inflows are higher than

existing assets, (2) firms can manage risk-taking

reinvestment with high profits and support corporate

growth, and (3) company risk-appetite in accordance

with measured risk tolerance. However, excessive

risk-taking behavior can lead companies to make

uninformed decisions and result in large losses to

stakeholders.

Acknowledging that bank main line of

business is as an intermediary between those who

have more money to those who does not, the amount

of lending that banks give to certain type of customers

becomes an area of concern (Dong et al., 2014;

Skała& Weill, 2018). The collapses of banking

industry rise as a result of higher non-performing loan

(NPL) that further contributes to credit risk. Bank

assets are mostly made up of loan while liabilities are

deposit payable so the mismatch between both would

cause greater credit risk (Waemustafa&Sukri, 2015).

In other words, increasing share of non-performing

loan may cause large losses in banks as higher gross

NPL ratio is correlated to higher direct ex-post means

of credit risk (Srairi, 2013). hat different age shows

different tendency of behavior. These differences are

often categorized into two: the older generation and

the younger generation (Berger, Kick, &Schaeck,

2014; Ferrero-Ferrero, Fernández-Izquierdo, &

Muñoz-Torres, 2015; Hertel, I.J.M. Van der Heijden,

H. de Lange, & Deller, 2013; Menkhoff, Schmidt,

&Brozynski, 2006; Talavera et al., 2018). One of the

behavioral impacts of this age differences situations

and become the focus in many researches are how age

impacts someone to make decision.

2.2 Young Age

Aging are associated to neuromodulator changes

for integration of information (Mata, Josef, Samanez-

Larkin, &Hertwig, 2011; Mata, Schooler,

&Rieskamp, 2011; Mata, von Helversen,

&Rieskamp, 2010). Decline on cognitive ability such

as memory may lead to older adult makes simpler

decision and more error if information is combined.

Moreover, motivational theories explain that aging

leads to greater focus on emotional goals which leads

to informational processing bias (Mather

&Carstensen, 2005). These differences in

anticipation are a potential system leading to

differences on risk-taking decisions (Mata et al.,

2011).

The younger generations are stereotyped of

having different characteristics compared to the older

generation. The older generation is found to be

stricter, risk-averse, and less creative. This is due to

the accumulative understanding that they obtain from

longer life (Talavera et al., 2018). The younger

generation, however, are often labelled to have 180

degrees differences from the older generation. They

are viewed to be more adventurous, energetic, and

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

66

loves changes in technology (Mishra &Jhunjhunwala,

2013). These differences are also attributable to both

generation different personal values that sparks

intrageneration conflicts (Talavera et al., 2018).

Popular beliefs evidently find that the older

generation is risk averse and young members have

tendency to take more risk than those older.

MacCrimmon&Wehrung (1990) self-assessed survey

evidence shows that older executive takes lower risk

as they are not into gambling behavior and have more

understanding regarding many experiences in the

past. This is different from younger member who take

more risk as they have less knowledge so they take

the risk anyway (Grable, 2000). Since prior research

deeply considered that younger age has positive effect

on manufacturing firm efficiency level, our first

hypothesis is as followed:

H

1

: Younger member proportion in Risk Oversight

Committee is positively associated with bank

risk-taking.

2.3 Female

Male and female are commonly perceived as

having different traits. This regular perception has

captivated many researchers to discover more

regarding their differences. Male is associated with

masculinity while female is associated with

femininity. Bem (1977) defines masculinity as quality

of being rational, independent, decisive, and

analytical. On the other side, femininity includes

being expressive, intuitive, sensitive, and warm.

Previous research has identified female positive

relationship towards higher monitoring role that

reduces agency costs. This might be caused by

"offspring risk hypothesis" that explains how woman

may see more risks than man as they see it as a way

to keep safe any offspring under their supervision.

Here, the understanding of more risks might cause the

female to be more protective (Sila, Gonzalez,

&Hagendorff, 2015). The finding is supported by

Harris, Jenkins, & Glaser (2006) research which

found that female is generally less risk averse than

male.

Skała& Weill (2018) found that female board

member, specifically CEO, presence is associated

with lower risk. Here, the Swedish women-leaded

banks are obtaining higher capital to asset ratio and

capital adequacy while the credit risk does not

change. As there is no problem on lower asset quality

here as compared to male-led banks, the attributable

different on capital preferences are linked to higher

female risk aversion. The finding on how higher

female proportion leads to lower risk-taking is

supported by various literature (Bucciol&Miniaci,

2011; Dong, Meng, Firth, &Hou, 2014; Sun & Liu,

2014). Higher proportion of female board are found

to significantly reduce risk-taking in China (Dong et

al., 2014)and higher proportion of female audit

committee members lead to increasing oversight of

bank management risk. Through various investment

game, Charness&Gneezy (2012) claims to find strong

evidence regarding gender differences in risk-taking.

They found that woman is much more financially risk

averse than men. Therefore, in regards with the risk

oversight committee member proportion, this

research proposes the following hypothesis:

H

2

: Female member proportion in Risk Oversight

Committee is negatively associated with bank

risk-taking

2.4 Experience

Experience is a direct contact or observation

regarding a phenomenon.Lejarraga, Hertwig, &

Gonzalez (2012) find proof that people tend to make

decisions based on experience that makes rare events

having less impact than deserved as compared with

their objective probabilities. A direct experience in

one field causes one understand more about the field

compared to those who does not. This also affects the

familiarity regarding the tasks and knowledge on how

to improve it.

Huckman & Upton (2009) stated that the

cumulative production experience, or learning curve,

plays a central role in organizational and individual

learning. They further found that organization and

individual are developing and innovating routines to

decipher todays problem because of their past

experience.

Eichler & Lahner (2017) and Menkhoff,

Schmeling, & Schmidt (2013) has proven that

previous career experience influence one attitude

when seeing certain phenomenon in the present. This

intangible inclination is proven to be similar for

individuals from similar background. While

Menkhoff et al (2013) further expresses that

experienced manager has lower willingness to take

risk as they are less overconfident to the situation as

compared to the inexperienced ones, Koudijs & Voth

(2016) expresses that general personal experiences

may contributes to risk-taking in various way. This is

also due to whether the experience is positive or

negative (Schneider et al., 2016).

This study aims to find out whether direct bank

risk management experience. The bank risk

management related experience can be defined as

those who have worked in bank-related risk

management division (including the compliance

division, director of the bank, vice president of the

bank, vice director of finance, and risk management

committee). This research offers following

hypothesis:

Do Young, Female, and Experienced Characteristics of Risk Oversight Committee Members Accommodate Bank Risk-Taking? Evidence

from Indonesia

67

H

3

: Bank risk management experienced member

proportion in Risk Oversight Committee is

negatively associated to bank risk-taking

3 METHODOLOGY

3.1 Research Models

The research first model, as described in

Equation 3.1, aims to test the research hypothesis of

whether the young age, female, and risk management

experienced members have a significant effect on

bank risk-taking. The control variables for this

equation are bank size, total asset growth, loan to

deposit ratio, and return on asset. is described in

Equation 3.1.

Equation 3.1. Research Main Model

Here, risk-taking is proxied by gross NPL which

is common to be used in bank risk-taking literature

(Skala, 2018; Berger et al., 2009). Meanwhile, the

research obtained proportion for younger members in

the committee by obtaining median from the whole

sample in order to get objective relative younger and

older age of risk oversight committee members,

researcher first collect data of all age for the whole

sample. Once obtained, the research puts '1' for

members with the age equal and lower than median

while puts '0' for those who are older. Meanwhile, the

calculation of gender is straightforward using dummy

and then proportionate it to total committee members.

As this research would like to find the impact of direct

bank risk management expertise to risk-taking, this

study accommodates the definition of experts in Aebi

(2012) and Ghafran& O’Sullivan (2017) to the risk

management context. Specifically, this research

defines bank risk management expertise as those who

have worked in bank-related risk management

division (including the compliance division, director

of the bank, vice president of the bank, vice director

of finance, and risk management committee below

the board of director).

3.2 Population and Sample

Sample selection is done using non-probability

and purposive sampling method. The information

regarding these banks are hand-collectedly obtained

from every bank annual report. The classifications are

general bank listed in the Indonesian Stock Exchange

during the year 2012 - 2016, bank which published

complete annual report, bank that does not undergo

corporate action (eg. merger) during the period of

study, bank that does not undergo extreme trouble

(eg. liquidity shot from government), and bank with

complete data as needed by the research.

4 RESULT AND DISCUSSION

4.1 Descriptive Statistics Analysis

The total observation in the study is 135

observations as the samples are twenty-seven banks

during the period of five years. The panel variable is

bank names and the time variable is year with delta of

one year. Furthermore, the pool of data is strongly

balanced, meaning that there is no empty data point

in the dataset used on this research. The table

detailing descriptive statistics could be seen on

Appendix A.

As for YOUNG, this research approaches the

characteristics by first finding the median age in the

whole risk oversight committee member to know the

comparatively relative older and younger individuals.

The study found that the median of the whole sample

which is 59 years old. This means that those above 59

is considered as 'older' and those below or equal to 59

is considered as 'younger'. The proportion of younger

members compared to the whole committee in each

bank-year is then computed manually. Moreover, the

minimum proportion is zero and the maximum

proportion is one meaning that there are banks which

prefer complete older or younger committee

members. Overall, there are eight bank-year with zero

younger members proportions and ten bank-year

which have all of its members being young.

Here, the mean proportion of FEMALE member

in risk oversight committee is 13.46% with the

median of zero as most banks does not have risk

oversight committee. Female is non-existent in

eighty-one bank-year risk oversight committee.

Risk management experience (EXPER) aims to

explain the proportion of risk oversight committee

members who have directly worked in banking risk

management divisions. The data has shown that the

average proportion of risk oversight committee

members which has directly managed banking risk

management is 22.82%. The minimum proportion of

this trait is zero which consists of eleven banks.

Conversely, the maximum proportion is one in 62

banks which means that some bank-year picks

members with previous experience of direct risk

management exposure in the field.

4.2 Statistical Tests

Testing panel data regression models through

Chow Test, Breusch Pagan, Langrange Multiplier and

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

68

Haussman test concludes that the best regression

model for this research is the random effect model.

Meanwhile, the classic assumption tests results show

that the research model is free from the problem of

normality, autocorrelation and heteroscedasticity.

Centering for variable LDR and BANK SIZE treats

the multicollinearity problem. The results of the

random effect regression testing in this research are

described in Appendix B. Additionally, the research

also includes sensitivity testing towards bank risk-

taking using committee average age as alternative

proxy of young, loosening definition of experience by

including of overseeing committee experience, and

existence of woman in the committee which is not

attached in the paper due to page limitation.

4.3 Main Model Analysis

4.3.1 Impact of Increasing Young Age

Proportion to Risk-Taking

As for the relationship between the proportion of

younger risk oversight committee members

(YOUNG) and bank risk-taking, Appendix B shows

that the relationship is inverse. The relationship is

negative and significant at α = 5%. This association

rejects the research second hypothesis which is

regarding how increasing younger risk oversight

committee member proportion is expected to increase

bank risk-taking. The relationship could be due to the

fact that the median and mode age of the whole risk

oversight committee is 59 while the mean age is 58.4.

The definition of relatively 'younger' risk oversight

committee could not be directly attributed to the

definition of young by previous researches as the

previous studies considered 'young' at the year much

younger than 59 years old. This is confirmed by Mata

et al. (2011) which conducts literature review on

impact of aging to risky choice. Mata et al. found that

literatures are justifying 'young' at the age range of 18

to 35 years old while considering 'old' at 65 to 85

years old. In other words, the median of 59 years old

clearly shows that the risk oversight committee

members are skewed to the 'old' criteria. The research

has shed light on how Indonesian risk oversight

committee is coming from people from overall the

same generation.

Moreover, the fact that increasing number of

young members are inversely related to risk-taking is

also attributable to the reputational and career

concerns (Serfling, 2014; Holstrom, 1999;

Hirshleifer&Thankor, 1992). The young members

can be replaced more easily and received less

tolerance from the labor market for faultiness

(Hirshleifer&Thankor, 1992). The harsh truth deters

initial inclination towards risk and make the younger

members more inclined to the consensus to avoid

market punishment.

A sensitivity test conducted to know whether

relative age proportion is the right measure by

calculating the mean age of a board which is a

common way to measure 'young' find that using

average age has no significant result to risk-taking. In

other words, the main model (Appendix B) is proven

to be robust.

4.3.2 Impact of Increasing Female

Proportion to Risk-Taking

According to Appendix B regression with panel

data, increasing number of female members in the

risk oversight committee (FEMALE) is found to

increase bank risk-taking asproxied by Non-

Performing Loan over Total Loan. The relationship is

positive and significant at 1% significancy point. The

discovery of this relationship rejects the research

second hypothesis which is how increasing

proportion of female in the risk oversight committee

is expected to decrease bank risk-taking and is

contrary to many various previous literature (Bucciol

& Miniaci, 2011; Dong et al., 2014; Harris et al.,

2006; Skała & Weill, 2018; Sun & Liu, 2014). As this

negative result is significant at α = 1%, it is worth

exploring why the result differs with common

believes. The prominent role of female is also shown

in additional test which shows that the mere existence

of woman supports committee accommodation to

bank risk-taking.

There are various possible reasons on why higher

proportion of female leads to more risk-taking.

Berger et al., (2014) found that increasing number of

women in the board leads to higher portfolio risk.

Berger argues that most of the previous research that

claims women are risk averse investigate woman in

lower-position. Berger argues that the higher-

positioned women are different and they are risk-

takers. The findings are further supported by Adams,

Funk, Barber, Ho, &Odean (2012). They found that

woman is carelessly more risk-loving than man

although they are still having higher benevolence

trait. Woman are, moreover, found to be more risk-

taking as they care less about power perception from

other people compared to the male counterpart.

Women have to understand the context of

decisions they make and comfortable to the

environment in order to pursue higher risk-taking

behavior. When women are familiar to the context of

decision, various evidence shows that they are more

risk-loving (Miller &Ubeda, 2011; Johnson and

Powell, 1994; Levin et al., 1988). The environmental

context fit into this decision as woman have to be in

a condition where there are no excessive stereotypical

perceptions on what woman risk-taking should be.

Do Young, Female, and Experienced Characteristics of Risk Oversight Committee Members Accommodate Bank Risk-Taking? Evidence

from Indonesia

69

This is due to the fact that woman underlying risk-

taking behavior is found to be greatly influenced by

the general view from the society (Ball et al., 2011).

4.3.3 Impact of Increasing Experienced

Proportion to Risk-Taking

This research expects to find the positive or

negative relationship between increasing proportion

of risk-management experienced (EXPER) member

in risk oversight committee to bank risk-taking. As

can be seen on Appendix B, the negative association

strengthens Menkhoff et al. (2013) argument that

existence of direct experience in related field results

on lower risk-taking behavior. This means that the

members are less overconfident towards the

surrounding situations and take more precaution as

they are already familiar regarding the field volatility

(Huckman& Upton, 2009). This condition might

result on higher skepticism on risk management

experienced members that allow them to not be easily

convinced by optimist high-risk action that bank

management may propose.

It is inferred that the insignificant relationship

might be due to the fact that this research handcollect

data for members who have direct banking risk

management experience. Meaning that the ones

counted as having risk management experience got to

obtain experience in the banking industry risk

management division. This means that those

indirectly learn about risk management but never

practice risk management or risk management

practitioners that is not originated from banking

industry does not count as risk management

experienced members in this research. In other words,

this may mean that board of commissioner select

other factors, such age and gender, as more important

thing of consideration than direct bank risk

management experience as risk management

expertise could also be obtained in other industries or

through certification. The finding suggests that even

though the existence of member with risk

management expertise in the bank risk oversight

committee is compulsory, banking sector specific risk

management experience is not significant in affecting

risk-taking. The finding is further strengthened by

sensitivity test 2 (Table 4.4.) which loosen the

definition of bank risk management to include

previous risk oversight committee experience also

found the same result.

4.3.4 Other Factors Impacting the

Relationship between Risk Oversight

Committee Characteristics and Bank

Risk-Taking

The other factors impacting the relationship

between the committee characteristics and bank risk-

taking are the control variables, consisting of bank

size, total asset growth, loan to deposit ratio, and

return on asset. The relationship between bank size

and bank risk-taking is positive and significant

consistent with Bhagat, Bolton, & Lu (2015). The

larger the bank size, as proxied by total asset, the

more leverage it could bear and the more trustworthy

it gets from the stakeholders. As the bank would like

to keep their position as one of the largest in the

industry, these banks may take to be able to earn

more.

Total asset growth shows the result of bank

strategy year by year. Here, asset growth has an

inverse relationship with bank risk-taking and this is

significant at α = 1%. The condition infers that lower

asset growth results in higher risk-taking. When bank

strategy results in lower asset growth, bank would

then prefer to take more risk to try to obtain more

growth.

The correlation between loan to deposit ratio is

not significant. This is contrary to Skala (2018) which

found that the correlation of LDR to risk-taking is

positive and significant. This means that the risk-

taking decisions bank conducts and overseen by the

risk oversight committee does not look at the amount

of loan to deposit ratio and rather look at other factors.

Return on asset relationship to bank risk-taking is

negative and significant at α = 5%. This result is

consistent with Srairi (2013) and Affan (2014)

finding on return on asset also display a strong

negative association to credit risk. This shows that

banks with lower profitability is aiming to take more

risk to save and improve its position.

5 CONCLUSIONS

5.1 Conclusions

This research is aimed to understand the

unexplored realm of risk oversight committee

characteristics and its tendency to tolerate bank

management risk-taking behavior. The characteristics

that are specifically explored here are young, female,

and risk-management experience. This research uses

random effect panel data estimator and use novel

dataset on 27 banks from 2012 - 2016. The model has

a F-test significance at 1% implying that the model is

highly reliable in explaining bank risk-taking.

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

70

This study has found that increasing proportion of

young risk oversight committee members decreases

committee accommodation towards bank risk-taking.

This is due to the fact that risk oversight committee

members are relatively old and not suitable to risk-

taking literature's definition of young. The median

age of the risk oversight committee member is 59 and

the average age is 58.3 which could be defined as old

age. Although the findings are contrary to the

hypothesis, previous study suggests that the

difference might also be dued to the reputation and

bargaining power of members inside the committee.

Younger manager is proven to deter on making

mistakes as they face less career safety as they have

less reputation and face higher pressure from the

labor market. Sensitivity test conducted shows that

average age which is believed as measurement of

young committee, as opposed to proportion of young

age members, is not significant to impact bank risk-

taking.

On the other hand, increasing proportion of

female risk oversight committee members increases

the committee accommodation towards bank risk-

taking behavior. The result is contrary to the

hypothesis as well as the popular belief that women

are risk-averse and that they are less inclined to make

change. Woman in the higher position, like risk

oversight committee members, are expected to take

different decision than most woman and these

decisions are very likely to be accommodating risky

behavior. Moreover, it is understood that in woman's

nature that if a woman is familiar with the context of

a decision and the environment support woman to do,

woman is more inclined to take on risks. Sensitivity

test conducted shows that the existence of at least one

woman in the risk oversight committee impacts bank

risk-taking behavior accommodation positively. This

means that female existence in the committee plays a

strong role in Indonesia's bank risk-taking tolerance.

Moreover, risk management experienced risk

oversight committee members have negative impact

to bank risk-taking behavior. However, the

relationship is not significant. The result is negative

as more experienced members have more work

experience which make them more aware of risk

consequence. Moreover, they are also more scseptical

and less overconfident when presented by bank

management opportunistic plan. Reasoning for

insignificant result could be from the data limitation

which depends on each bank annual report that might

not report the risk management experience.

Furthermore, the result could also be influenced by

the fact that board of commissioner select other

factors, such age and gender, as more important thing

of consideration than direct bank risk management

experience as risk management expertise could also

be obtained in other industries or through

certification. Sensitivity test conducted when loosen

the risk management experience criteria to include

members who have been risk oversight committee in

the previous years have shown the result of not

significant. The finding enhances understanding that

characteristics other than experience are considered

more important to impact bank risk-taking in

Indonesia.

5.2 Suggestions for Future Research

The research is limited to the usage of sample on

national conventional banks from 2012 to 2016. The

data obtained, moreover, are solely due to each bank

annual report. There might have been information,

such as risk management experience that the

members experience but not written in the annual

report, that might have not been captured in this

research. The research also limits its risk-taking

proxy to the non-performing loan ratio which

specifically measures bank credit risk. Lastly,

demographic data regarding gender is limited to

whether the person is male or female

Based on the limitations of the study, we can

conclude some suggestions for further research

including increasing the scope of the research,

conduct more exploratory research in the field of risk

oversight committee, employ other risk-taking, and

conduct more rigorous research on demographic data

such as specific educational backgrounds or previous

experiences.

REFERENCES

Adams, R. B., & Mehran, H. (2012). Bank board structure

and performance: Evidence for large bank holding

companies. Journal of Financial Intermediation, 21(2),

243–267. https://doi.org/10.1016/j.jfi.2011.09.002

Aebi, V., Sabato, G., & Schmid, M. (2012). Risk

management, corporate governance, and bank

performance in the financial crisis. Journal of Banking

and Finance.

https://doi.org/10.1016/j.jbankfin.2011.10.020

Affan, M. (2014). Pengaruh Tingkat Suku Bunga terhaadp

Pengambilan Risiko pada Bank Umum di Indonesia

Periode 2004-2012. Universitas Indonesiaa.

Andarini, P., & Januarti, I. (2012). Hubungan Karakteristik

Dewan Komisaris dan Perusahaan terhadap keberadaan

Komite Manajemen Risiko. Jurnal Akuntansi Dan

Keuangan Indonesia.

https://doi.org/10.21002/jaki.2012.06

Atkinson, J. W. (1957). Motivational determinants of risk

taking behavior. Psychological Review, 64(6), 359–

372. https://doi.org/10.1037/h0043445

Do Young, Female, and Experienced Characteristics of Risk Oversight Committee Members Accommodate Bank Risk-Taking? Evidence

from Indonesia

71

Bank Indonesia. (2006). Peraturan Bank Indonesia Nomor

8/4/PBI 2006 tentang Pelaksanaan Good Corporate

Governance

Basel Committee on Banking Supervision. (2015).

Corporate governance principles for banks. Bank for

International Settlements.

Battaglia, F., & Gallo, A. (2015). Risk governance and

Asian bank performance: An empirical investigation

over the financial crisis. Emerging Markets Review, 25,

53–68. https://doi.org/10.1016/j.ememar.2015.04.004

Bem, S. (1977). The measurement of psychological

androgyny: An extended replication. Journal of

Clinical Psychology. https://doi.org/10.1002/1097-

4679(197710)33:4<1009::AID-

JCLP2270330417>3.0.CO;2-5

Berger, A. N., Kick, T., & Schaeck, K. (2014). Executive

board composition and bank risk taking. Journal of

Corporate Finance, 28, 48–65.

https://doi.org/10.1016/j.jcorpfin.2013.11.006

Bhagat, S., Bolton, B., & Lu, J. (2015). Size, leverage, and

risk-taking of financial institutions. Journal of Banking

& Finance, 59, 520–537.

https://doi.org/10.1016/j.jbankfin.2015.06.018

Bucciol, A., & Miniaci, R. (2011). Household Portfolios

and Implicit Risk Preference. Review of Economics and

Statistics, 93(4), 1235–1250.

https://doi.org/10.1162/REST_a_00138

Charness, G., & Gneezy, U. (2012). Strong Evidence for

Gender Differences in Risk Taking. Journal of

Economic Behavior and Organization.

https://doi.org/10.1016/j.jebo.2011.06.007

Dong, Y., Meng, C., Firth, M., & Hou, W. (2014).

Ownership structure and risk-taking: Comparative

evidence from private and state-controlled banks in

China. International Review of Financial Analysis, 36,

120–130. https://doi.org/10.1016/j.irfa.2014.03.009

Eichler, S., & Lahner, T. (2017). Career experience,

political effects, and voting behavior in the Riksbank’s

Monetary Policy Committee. Economics Letters, 155,

55–58. https://doi.org/10.1016/j.econlet.2017.03.015

Fan, J. P. H., Wong, T. J., Dulewicz, V., Herbert, P., Dalton,

D. R., Daily, C. M., … Kassim, S. I. (2016). Does board

structure in banks really affect their performance ?

Does board structure in banks really affect their

performance ? Journal of Financial Economics, 32(1),

1–25. https://doi.org/10.1108/S1479-

3563(2012)000012B005

Ferrero-Ferrero, I., Fernández-Izquierdo, M. Á., & Muñoz-

Torres, M. J. (2015). Age diversity: An empirical study

in the board of directors. Cybernetics and Systems,

46(3–4), 249–270.

https://doi.org/10.1080/01969722.2015.1012894

Ghafran, C., & O’Sullivan, N. (2017). The impact of audit

committee expertise on audit quality: Evidence from

UK audit fees. British Accounting Review.

https://doi.org/10.1016/j.bar.2017.09.008

Grable, J. E. (2000). Financial Risk Tolerance and

Additional Factors That Affect Risk Taking in

Everyday Money Matters. Journal of Business and

Psychology, 14(4), 625–630.

https://doi.org/10.1023/A:1022994314982

Haneef, S., Rana, M. A., & Karim, Y. (2012). Impact of

Risk Management on Non-Performing Loans and

Profitability of Banking Sector of Pakistan Hailey

College of Commerce University of the Punjab Hafiz

Muhammad Ishaq Federal Urdu University of Arts ,

Science and Technology. International Journal of

Business and Social Science, 3(7), 307–315.

Harris, C. R., Jenkins, M., & Glaser, D. (2006). Gender

Differences in Risk Assessment : Why do Women Take

Fewer Risks than Men ?, 1(1), 48–63.

Hertel, G., I.J.M. Van der Heijden, B., H. de Lange, A., &

Deller, J. (2013). Facilitating age diversity in

organizations – part II: managing perceptions and

interactions. Journal of Managerial Psychology,

28(7/8), 857–866. https://doi.org/10.1108/JMP-07-

2013-0234

International Finance Corporation. (2012). Risk Taking: A

Corporate Governance Perspective. Retrieved from

https://www.academia.edu/12679420/Risk_Taking_A

_Corporate_Governance_Perspective%5Cnhttps://ww

w.academia.edu/12679420/Risk_Taking_A_Corporate

_Governance_Perspective?auto=download&campaign

=weekly_digest

Lejarraga, T., Hertwig, R., & Gonzalez, C. (2012). How

choice ecology influences search in decisions from

experience. Cognition.

https://doi.org/10.1016/j.cognition.2012.06.002

Liang, Q., Xu, P., & Jiraporn, P. (2013). Board

characteristics and Chinese bank performance. Journal

of Banking and Finance, 37(8), 2953–2968.

https://doi.org/10.1016/j.jbankfin.2013.04.018

MacCrimmon, K. R., & Wehrung, D. A. (1990).

Characteristics of Risk Taking Executives.

Management Science, 36(4), 422–435.

https://doi.org/10.1287/mnsc.36.4.422

Mata, R., Josef, A. K., Samanez-Larkin, G. R., & Hertwig,

R. (2011). Age differences in risky choice: A meta-

analysis. Annals of the New York Academy of Sciences.

https://doi.org/10.1111/j.1749-6632.2011.06200.x

Mata, R., Schooler, L. J., & Rieskamp, J. (2011). The Aging

Decision Maker: Cognitive Aging and the Adaptive

Selection of Decision Strategies. In Heuristics: The

Foundations of Adaptive Behavior.

https://doi.org/10.1093/acprof:oso/9780199744282.00

3.0022

Mata, R., von Helversen, B., & Rieskamp, J. (2010).

Learning to choose: Cognitive aging and strategy

selection learning in decision making. Psychology and

Aging. https://doi.org/10.1037/a0018923

Mather, M., & Carstensen, L. L. (2005). Aging and

motivated cognition: The positivity effect in attention

and memory. Trends in Cognitive Sciences.

https://doi.org/10.1016/j.tics.2005.08.005

Mayur, M., & Saravanan, P. (2017). Performance

implications of board size, composition and activity:

empirical evidence from the Indian banking sector.

https://doi.org/10.1108/CG-03-2016-0058

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

72

Menkhoff, L., Schmeling, M., & Schmidt, U. (2013).

Overconfidence, experience, and professionalism: An

experimental study. Journal of Economic Behavior and

Organization, 86, 92–101.

https://doi.org/10.1016/j.jebo.2012.12.022

Menkhoff, L., Schmidt, U., & Brozynski, T. (2006). The

impact of experience on risk taking, overconfidence,

and herding of fund managers: Complementary survey

evidence. European Economic Review, 50(7), 1753–

1766.

https://doi.org/10.1016/j.euroecorev.2005.08.001

Mishra, R., & Jhunjhunwala, S. (2013). Diversity and the

Effective Corporate Board. Academic Press.

OJK. (2016). Peraturan Otoritas Jasa Keuangan Nomor 55

/POJK.03/2016 tentang Penerapan Tata Kelola Bagi

Bank Umum

OJK. (2016). Peraturan Otoritas Jasa Keuangan Nomor

18/POJK.03/2016 tentang Penerapan Manajemen

Risiko bagi Bank Umum

Republik Indonesia. (1998). Undang-Undang Nomor 10

Tahun 1998 tentang Perbankan

Sila, V., Gonzalez, A., & Hagendorff, J. (2015). Women on

board: Does boardroom gender diversity affect firm

risk? Journal of Corporate Finance.

https://doi.org/10.1016/j.jcorpfin.2015.10.003

Skała, D., & Weill, L. (2018). Does CEO gender matter for

bank risk? Economic Systems.

https://doi.org/10.1016/j.ecosys.2017.08.005

Srairi, S. (2013). Ownership structure and risk-taking

behaviour in conventional and Islamic banks: Evidence

for MENA countries. Borsa Istanbul Review, 13(4),

115–127. https://doi.org/10.1016/j.bir.2013.10.010

Subramaniam, N., Mcmanus, L., Zhang, J., Mcnutt, P. A.,

Demidenko, E., Mcnutt, P., … Christopher, J. (2009).

The association between corporate governance

guidelines and risk management and internal control

practices: Evidence from a comparative study.

Managerial Auditing Journal Iss International Journal

of Social Economics Iss Managerial Auditing Journal,

24(4), 316–339. Retrieved from

http://dx.doi.org/10.1108/02686900910948170

Sun, J., & Liu, G. (2014). Audit committees’ oversight of

bank risk-taking. Journal of Banking and Finance,

40(1), 376–387.

https://doi.org/10.1016/j.jbankfin.2013.12.015

Talavera, O., Yin, S., & Zhang, M. (2018). Age diversity,

directors′ personal values, and bank performance.

International Review of Financial Analysis, 55(October

2017), 60–79.

https://doi.org/10.1016/j.irfa.2017.10.007

APPENDIX

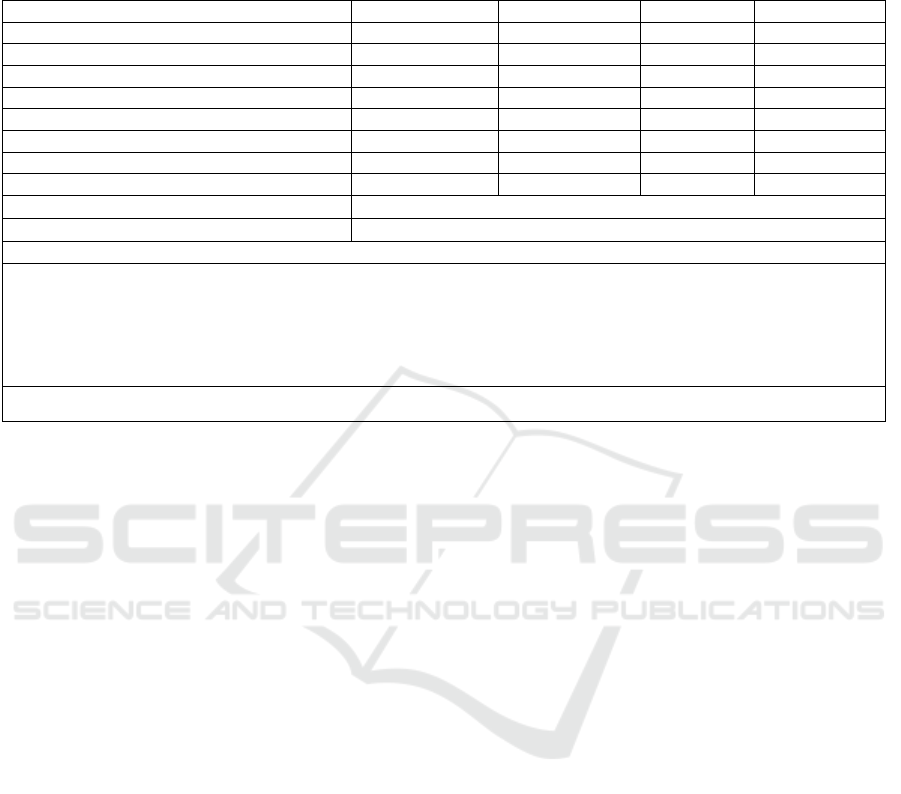

Appendix A: Descriptive Statistics

Variable

Mean

Std. Dev.

Min

Max

Median

RISK-TAKING

0.0245

0.0156

0.0014

0.0824

0.0233

YOUNG

0.5164

0.2463

0.0000

1.0000

0.5000

FEMALE

0.1347

0.1747

0.0000

0.6667

0.0000

EXPER

0.2282

0.2706

0.0000

1.0000

0.2000

BANK SIZE (in

billion Rupiah)

158,233

0.2300

2,541

1,038.706

69,703

ASSETGROWTH

0.1538

0.1355

-0.2926

0.675678

0.1470

LDR

0.8485

0.1144

0.5239

1.133

0.8639

ROA

0.0178

0.0181

-0.1115

0.0515

0.0176

Number of observation: 135

RISK-TAKING = Ratio of non-performing loan to total loan, YOUNG = Proportion of younger members in risk

oversight committee, FEMALE = Proportion of female members in risk oversight committee, EXPER = Proportion of

risk management experienced members in risk oversight committee, BANK SIZE = natural logarithm of total asset at

book value, ASSET GROWTH = (

)/

, LDR = Ratio of total loan to

total deposit, ROA = Ratio of net income to average total asset

Do Young, Female, and Experienced Characteristics of Risk Oversight Committee Members Accommodate Bank Risk-Taking? Evidence

from Indonesia

73

Appendix B: Regression Result of Research Main Model

Variables

Exp. Sign

Coef.

z

P>|z|

CONS

0.0451***

13.61

0.0000

YOUNG

+

-0.0062**

-1.69

0.0438

FEMALE

-

0.0161***

2.86

0.0020

EXPER

-

-0.0008

-0.18

0.4375

ASSET GROWTH

-

-0.0338***

-4.55

0.0000

BANK SIZE

-

0.0026**

2.20

0.0140

ROA

-

-0.7690***

-8.77

0.0000

LDR

-

-0.0001

-0.78

0.1595

within

0.7193

Prob>

0.0000

Number of observation: 135

RISK-TAKING = Ratio of non-performing loan to total loan, YOUNG = Proportion of younger members in risk

oversight committee, FEMALE = Proportion of female members in risk oversight committee, EXPER = Proportion of

risk management experienced members in risk oversight committee, BANK SIZE = natural logarithm of total asset at

book value, ASSET GROWTH = (

)/

, LDR = Ratio of total loan to

total deposit, ROA = Ratio of net income to average total asset

*** significant at = 1%; ** significant at = 5%; * significant at = 10%

SEABC 2018 - 4th Sriwijaya Economics, Accounting, and Business Conference

74