The Relationship between Foreign Direct Investment Influx,

Economic Growth, and Financial Institutions in ASEAN-6

Aryani, Made Gitanadya

1

, Pratamasari, Annisa

2

1

Department of Management. Airlangga University

2

Department of International Relations. Airlangga University

Keywords: Foreign direct investment, financial market, ASEAN, economic growth

Abstract: Globalization era has brought about the influx of foreign investment from all over the world, namely foreign

direct investment and international portfolio investment. Those investments are assumed to have positive

impacts on the invested countries, dut to the transfer of technology and knowledge from developed countries

to developing countries. However, previous research stated that it was not always be the case, because FDI

influx differs in each country. One of the causes for the different outcomes on economic growth from FDI

influx is the development of financial market, such as banking system and stock exchange, in invested

countries. The existence of proper financial market in a country marks its readiness to expand FDI even further

to aim for higher economic growth. The object of this research is ASEAN members, because Southeast Asia

is a dynamically growing region in terms of economy; hence, it attracts FDI influx. ASEAN is also a

challenging object in terms of the degree of variability in financial market among its members. Based on

ASEAN Stats data, it is illustrated that the amount of FDI flowing to each ASEAN member differ, especially

between ASEAN members with financial market and without. This quantitative research employs regression

analysis on primary and secondary data related to various macroeconomic variables of ASEAN members to

establish the findings. Hence, this research aims to prove that financial market boosts positive impacts of FDI

to economic growth among ASEAN members.

1 INTRODUCTION

Foreign investment is divided into two forms. Firstly,

it flows directly in the form of fixed asset, like

factory, child-related factory, business vehicle, and

many others; thus, this kind of investment is called

Foreign Direct Investment (FDI). Secondly, it takes

form as security investment, like stocks and

international obligation; hence, this kind of

investment is called international portfolio

investment. Foreign direct investment (FDI) tends to

flow into some countries with low

restrictions/barriers and potentially record high

economic growth; while international portfolio

investment flows into countries with lax tax system,

high interest rate, and strong currency (Madura,

2012).

FDI has some positive impacts, such as increasing

productivity, technology transfer, and introducing

new managerial and operational process and

capability to improve one’s economic growth.

However, based on the findings of previous research

(Alfaro et al., 2005; Tang and Tan, 2016; Carkovic

and Levine, 2002), the impacts may differ between

countries. Some literatures even stated that FDI’s

impacts on economic growth remain inconclusive,

because they frequently provide conflicting results in

different research (Hoang, Wiboonchutikula, and

Tubtimtong, 2015; Wang, 2009). Moreover, not all

countries could maximize the positive impacts of

FDI, and here lies one of the most fascinating

determinants to be investigated: a country’s financial

system development.

World Bank (2016) defined financial system as a

system controlling fund transfer between two parties

with overflowing fund and their respective needs, to

achieve an efficient budget allocation, and to provide

some financial facilities, including payment system

for business activities. Generally, financial system is

divided into two institutions, namely banking and

capital market. These two institutions are financial

intermediaries which are tightly regulated to

minimize risk and strengthen country’s economics.

Meanwhile, ASEAN (Association of Southeast

Asian Nations) is a regional organization with 10

member-states, namely Thailand, Myanmar,

26

Aryani, M. and Pratamasari, A.

The Relationship between Foreign Direct Investment Influx, Economic Growth, and Financial Institutions in ASEAN-6.

DOI: 10.5220/0010272600002309

In Proceedings of Airlangga Conference on International Relations (ACIR 2018) - Politics, Economy, and Security in Changing Indo-Pacific Region, pages 26-33

ISBN: 978-989-758-493-0

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Vietnam, Laos, Malaysia, Cambodia, Singapore,

Philippines, Brunei Darussalam, and Indonesia. It

proposed a further integration in terms of social,

politics, and economics by 2020; however, the

member states decided to push forward ASEAN

Economic Community, in trade and financial system,

to December 31st, 2015. ASEAN Economic

Community is a political project aiming for a further

integration between the members which focuses on

economic development within the region. Some basic

objectives for further economic integration are trade

liberalization, investment enhancement, and opening

of financial markets. In line with that, ASEAN

members also wish to attract more FDI influx to the

region, as well as improving intra-ASEAN

investment level. ASEAN offers huge market of

US$2.6 trillion and over 622 million people

(ASEAN.org, 2018). It also promotes freer movement

of goods, capital, service, investment, and labor

(ASEAN Investment, 2018).

True to its objectives, the largest FDI investors are

ASEAN members themselves. ASEAN Stats (2017)

recorded a proportion of FDI from intra-ASEAN at

18.3% in 2015, higher than the inward FDI rate from

China, United States, and European Union. The 10

members respectively have various economic

conditions and financial system’s strength, both in

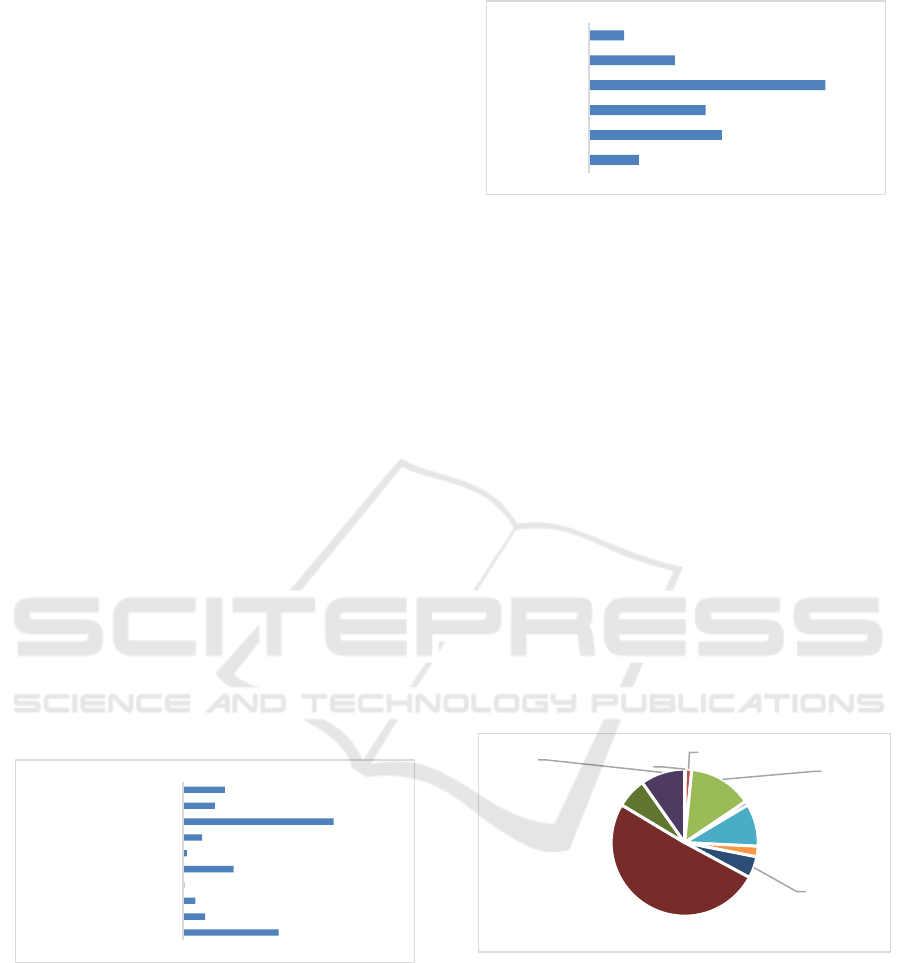

terms of banking system and capital market. Banking

system conditions in each country are illustrated in

Graphic I-1 below, which described the comparison

of banking assets to their Gross Domestic Products

(GDP) in 2015.

Source: South East Asia Network, 2015

Figure 1: Comparison of Banking Assets to GDP of

ASEAN Members in 2015

Comparatively, in terms of capital market, there is

an imbalance because only 6 out of 10 ASEAN

Members have their own stock exchange institution.

Hence, Brunei, Laos, Myanmar, and Cambodia are

taken out of capital market comparison to GDP,

which is depicted on Graphic 1-2 below.

Source: World Bank 2016

Figure 2: Comparison of Capital Market Capitalization to

GDP in 6 ASEAN Members in 2016

UNCTAD (United Nations Conference on Trade

and Development) described that inward FDI to

Southeast Asia region has broken a record by

reaching USD 24 billion in 2016. The record was

achieved by each country’s openness and ASEAN

presence to promote its members’ industries to

prospective foreign investors. ASEAN also facilitates

FDI by establishing ASEAN Investment Area (AIA)

Council.

Similar with inequality in financial market among

ASEAN members, it also happens to inward FDI.

Graphic 1-3 illustrated that more than half of inward

FDI in ASEAN was flowing into Singapore in 2016.

It is also fascinating that the largest FDI source in this

region is from fellow members of ASEAN, which

was recorded at 18.4% during the same period. It

evidently shows the maturity of ASEAN member-

states in terms of investment and economic

development.

Source: ASEAN Stats, 2016

Figure 3: Inward FDI composition among ASEAN

members in 2016.

Swift flow of FDI in ASEAN is further evidenced

by the rate of growth in this region from 2006 to 2016,

which increased 66%, the third highest growth rate in

Asia Pacific following China and India. However, the

impact of FDI on respective economic growth of each

member differs (World Bank, 2001).

Due to the significance of FDI and its different

impacts on economic growth, as well as the inequality

366%

85%

48%

7%

194%

16%

75%

576%

123%

160%

BruneiDarussalam

Indonesia

Malaysia

Filipina

Thailand

46%

121%

106%

216%

79%

32%

Indonesia

Malaysia

Thailand

Singapura

Filipina

Vietnam

Brunei

Darussalam;

0,14%

Cambodia;

1,41%

Indonesia;

14,00%

LaoPDR;

0,89%

Malaysia;

9,34%

Myanmar;

2,34%

Philippines;

4,74%

Singapore;

50,72%

Thailand;

6,64%

VietNam;

9,77%

The Relationship between Foreign Direct Investment Influx, Economic Growth, and Financial Institutions in ASEAN-6

27

in capital market between ASEAN countries, a

research on the relationship between foreign direct

investment, economic growth, and financial market

among ASEAN members deserves a limelight.

2 LITERATURE REVIEW

Foreign Direct Investment (FDI) is inevitably one of

the driving factors of economic growth in developing

countries. It represents fund inflows to a country,

which also symbolizes international trust toward it. It

is highly related to a country’s reputation and

economic prospect. Related to ASEAN, FDI is also

credited as a prominent variable in re-establishing the

members’ economy post Asian Crisis 1998 and

contributed to their robust economic growth from

then on (Fan and Dickie 2000).

Moreover, FDI influx is often correlated to the

openness of trade and investment within a country or

a region. Tan and Tang (2016) successfully found a

causal relationship between FDI, trade flows, interest

rate, and economic growth in ASEAN between 1970

and 2012. They also concluded that in some countries

(Singapore and Thailand), FDI did not lead to

economic growth, while the findings said otherwise

for Philippines, Malaysia, and Indonesia. Similarly,

Balasubramanyan, Salisu, and Sapsford (1996) also

posited that FDI is significantly related to trade

liberalization, particularly in countries adopting

export-led model.

When a foreign company brings in a new product

or process in a domestic market, then a technology

spillover to domestic companies will happen.

Technology diffusion might happen during a turning

over of workers from local to foreign company.

According to Alfaro et al. (2005), FDI plays a

significant role in modernization and economy

growth, so that government of developing countries

usually support the increasing number of FDI by

providing several incentive schemes for foreign

companies. On the contrary, Carkovic and Levine

(2002), using IMF and World Bank data base of 72

countries between 1960 and 1995, previously

recorded an opposite finding, which stated that FDI

does not robustly influence economic growth.

The theoretical foundation for the link between

FDI and economic growth is derived from

neoclassical model and endogenous model (Hoang,

Wiboonchutikula, and Tubtimtong 2015; Kok and

Ersoy 2009). Neoclassical model considers FDI as the

complimentary of capital stock at the host countries

and affect the host countries’ level of income only

through capital accumulation. However, it did not

guarantee its direct link to long-term economic

growth. While endogenous model posited that FDI

can affect host countries’ growth rate by improving

productivity level through the transfer of technology

and productivity spillovers (Hoang,

Wiboonchutikula, and Tubtimtong, 2015), which is

also the main assumption of this paper.

Madura (2015) stated that there are 2 motives of

Multinational Corporations (MNC) related to FDI,

namely income and cost. FDI brings about income by

creating new demands, gaining an entry to a more

profitable market, and overcoming trade restriction

and diversifications internationally. While cost-

related motives are related to decrease cost per unit to

achieve economies of scale and maximize the usage

of production factors, such as cheap labors and raw

materials. Determinants for the level of FDI influx are

also significantly related to a country’s

macroeconomic conditions, infrastructures, and

labors’ skills (Fan and Dickie, 2000). Hence, it is

probably why Singapore attracted most FDI influx

intra-ASEAN (Chart 1-3).

Furthermore, one of the determinants of FDI

success is absorptive capacities (Esfandyari 2015).

This capacity is determined by the management of

macroeconomy factors, infrastructure, and human

capital. Esfandyari (2015) found that the impact of

FDI on each D8 (eight Islamic developing country)

country can only influence their respective growths if

the level of the countries’ financial development is

good. Levine et al. (2000) preceded her by stating that

financial system plays an important role in economic

growth and productivity development.

Alfaro et al. (2004) also explained that financial

market has an important role to help working capital

from the operation of foreign companies which invest

in a country. FDI is counted as a long-term strategy

of a company, as it needs an investment decision-

making and large funding. FDI encompasses

machinery purchase, factory establishment, and other

production facility. To support factory operation, the

company needs some active capital. Local financial

market plays a role in providing short-term funding in

terms of bank loan or introducing them to some local

investors who readily invest their fund for foreign

companies.

The basic theory of linkage between foreign direct

investment and financial market development stated

that FDI influx increases capital accumulation and

further causes financial intermediaries to boom

(Soumaré and Tchana 2014). Furthermore, they also

attempted to find a causal link between foreign direct

investment and financial market development among

Asian countries (including 6 ASEAN member

ACIR 2018 - Airlangga Conference on International Relations

28

countries used in this research) by focusing on stock

market development.

The arguments of Alfaro et al. (2004) about the

positive impact of financial markets on enhancing

FDI are in line with another finding by Beck, Levince,

and Loayza (2000). They stated that a well-developed

financial system can generate more capital and

accelerate growth, in which FDI provides a stimulate

through capital accumulation. However, research on

the relationship between FDI, financial market

availability, and economic growth in ASEAN

countries still scarce. Hence, this research attempts to

fill the gap in this issue.

Based on the literature reviews, this research

develops several hypotheses. First, FDI positively

impacts on economic growth of ASEAN-6

(Indonesia, Malaysia, Singapore, Thailand,

Philippines, and Vietnam). Second, financial

institutions should strengthen the positive impacts of

inward FDI toward economic growth in ASEAN-6.

The 6-member countries were chosen based on the

consideration that the rest of member countries have

not had any established financial intermediaries.

3 METHODS

This research was conducted to ASEAN-6 between

2000 and 2017. The longer period is chosen to

eliminate irregularities occurred in short-term time

series data. The data were obtained from World Bank

and ASEAN Statistics website. This research

employed 2 models to analyze the effect of foreign

direct investment towards economy growth and the

moderation effect from financial market in each

country chosen as research samples.

Model 1 was formulated as follows (without

moderating variable):

ECO

i,t

= . β

0

+ β

1

FDI

i,j,t

+ β

2

EXC

i,j,t

+ β

3

BNK

i,j,t

+

β

4

INF

i,j,t

+ β

5

POP

i,j,t

+ Ɛ .................................. (1)

ECOi,t = β0 + β1 FDIi,j,t + β2 EXCi,j,t +

β3BNKi,j,t + β4 INFi,j,t + β5 POP i,j,t + Ɛ ....... (2)

While model 2 was formulated as follows (with

financial exchange and bank as moderating variable):

ECOi,t = β0 + β1 FDIi,j,t + β2 (FDI X EXC) i,j,t +

β3 (FDI X BNK) i,j,t + β4 EXC i,j,t + β5 BNK i,j,t +

β6 INF i,j,t + β7 POP I,j,t + Ɛ ............................ (3)

Variable dependent of this research was

economic growth, while the independent variables

were FDI, banking system, and financial market.

Furthermore, moderating variable for FDI was

financial system, which encompasses banking system

and stock exchange. Moreover, the control variables

were inflation and population growth. Operational

definition of each variable was described in following

table:

Table 1: Operational definition of research variable

Dependent variable

ECO

i,

j

,

t

:GDP

g

rowth in

j

countr

y

at t

y

ea

r

Independent variable

FDIv : Proportion of net inward FDI

a

g

ainst

j

countr

y

’s GDP at t

y

ea

r

EXC

i,j,t

: Proportion of stock exchange

capitalization against j country’s

GDP at t

y

ea

r

BNK

i,j,t

: Proportion of domestic loan

a

g

ainst

j

countr

y

’s GDP at t

y

ear

Moderatin

g

Variable

EXC or

BNK

Independent variable: stock

exchan

g

e or bankin

g

Control Variable

INF

i,

j

,

t

: Inflation rate of

j

countr

y

at t

y

ear

POP

i,j,t

: Population growth in j country at t

y

ear

4 RESULTS AND DISCUSSION

The data obtained was analyzed using eViews

software version 5.0 using data panel regression.

More specifically, the first model employed common

effect regression, while the second model used fixed

effect. The regression models has fulfilled all

classical assumption tests for regression in which the

data has been normally distributed, free from any

symptoms of autocorrelation, heteroskedasticity, and

multicollinearity; hence, the data are deemed fit for

further analysis. This study also determines

significance rate of 10% and the result is displayed in

Table 2:

Table 2: Regression result

Independents MODEL 1

Without

moderating

variable

MODEL 2

With

moderating

variable

FDI 0.191*

(0.001)

0.444*

(0.020)

FDI X BNK

-

-0.292 *

(0.028)

FDI X EXC

-

0.0345

(0.571)

BNK -0.046*

(0.000)

-0.024

(0.149)

EXC -0.002

(0.747)

0.0143

(0.193)

The Relationship between Foreign Direct Investment Influx, Economic Growth, and Financial Institutions in ASEAN-6

29

INF -0.064*

(0.003)

-0.0110

(0.085)

POP 2.490*

(0.001)

0.5064

(0.041)

Constanta 0.0433 0.0542

R Square 58.08% 37.37%

Ad

j

usted R

2

56.02% 29.46%

*the number is parentheses are p-value and

determined as significant if it’s below 10%

The result from R-square shows that Model 1

successfully explains economic growth in ASEAN-6

by 56% using 5 independent variables; hence, the

model is considered reliable.

As expected, foreign direct investment affects

economic growth positively. Nunnenkamp (2010)

summarized the advantages of foreign direct

investment as follows:

Foreign direct investment is a long-term project

by building factory or establishment, so the

inflows are less volatile and committed in the

long run;

Foreign direct investment is the most productive

for host country by engaging local people as

worker or harvesting national resource to the

best use;

Foreign direct investment provides more than

just capital, such as technology, management

and skills to be partaken by the local people also.

The less popular result came from financial

institutions that the existence of banks proxied by

domestic loan provided to GDP affected economic

growth inversely. Coccorese (2010) found the same

result from OECD countries by adding the degree of

competition from banking industry. Banking is one of

the highly regulated industry and higher barrier of

entry due to its duty as an intermediary for society’s

funds. Thus, banking represents oligopolistic industry

which is dominated by several major players, like in

this research’s samples. Indonesia’s 4 biggest banks

controlled 54% of its industry asset, while

Singapore’s 3 biggest banks held a staggering 78% of

banking assets (Aryani, 2016). The large banks are

likely to impose high costs on the economy because

of contagion and snowball effects, added with the

‘too-big-to-fail’ status. Big banks tend to take more

risk in their business activity to win the tight

competition by undermining the economy in the

process. Zhao (2017)’s result in China showed the

same effect due to the high level of government’s

interference in banking industry.

Another financial institution, which does not have

significant effect to economy growth, is capital

market. This can be explained by the different levels

of stock market development in each country.

Vietnam opened its stock exchange in Ho Chi Minh

city in 2007, while Singapore’s market capitalization

has doubled its GDP in 2015. (Aryani, 2016). Capital

market takes portfolio investment and mostly in short

term as capital inflow easily moves from one country

to another, hence it cannot bring about significant

effect towards economy growth. Most investors

choose developing countries for its high return to

compensate the risks, but in the event of crisis, the

fund usually flows back to the safe havens or

developed countries. Hermann (2016) also suggested

that capital market valuations are sometimes volatile

and unreliable due to the investor’s sentiment,

emotions and confidence.

Meanwhile, most previous researches agreed that

inflation hinders economy growth. Inflation not only

reduces the level of business investment, but also the

efficiency with which productive factors are put to

use. Higher inflation causes decrease in value of

money and purchase power of a society. In terms of

international trade, high inflation will damage the

country with reduced export orders, lower profits and

fewer jobs, and worsen a country’s trade balance. A

fall in exports can trigger negative multiplier and

accelerator effects on national income and

employment. Higher inflation forces the government

to enact tight money policy, resulted in less loans

given for production and/or consumption; thus, it

further deters economy growth in the long run.

Finally, last variable is population growth that

significantly affected economy growth in the same

direction. Historically, it has always been seen that

population increase is detrimental to a nation’s

economy (Malthus, 1978). But that is not the case in

ASEAN-6. According to Thuku, Paul, and Almadi

(2016), in the long run, high population benefits

economy due to technological advancement. Higher

population resulted in larger labor force, which

increases production yet in lower cost. In accordance

with foreign direct investment, the new openings of

factory or business from foreign country will reap the

benefits from the masses of labor force and improve

economic condition. Fox and Dyson (2015) also

stressed the point of quality over quantity where

larger population will be beneficial when it is

supported with better access to education, health care.

and social support.

Meanwhile, the second model gave deviant result

from previous hypothesis. We previously argued that

the existence of financial institution strengthens the

positive impacts of foreign direct investment on

economic growth. The prior result showed that the

existence of bank weakens foreign direct investment,

while capital market renders the significance of

ACIR 2018 - Airlangga Conference on International Relations

30

foreign direct investment. This aberration needs to be

solved by delving deeper in each country to see

significantly different levels of financial institution

development. The result from regressing foreign

direct investment to economy growth moderated by

financial institutions will be detailed in Table 3

Table 3: Regression result for each country

Independents ASEAN INA MAL PHIL SING THAI VIET

FDI 0.444*

(0.020)

4.318*

(0.001)

2.246*

(0.028)

6.129*

(0.048)

1.729*

(0.08)

1.145*

(0.082)

1.783*

(0.015)

FDI X BNK -0.292 *

(0.028)

-6.431*

(0.001)

10.382*

(0.019)

8.359*

(0.059)

1.559

(0.167)

-2.467*

(0.06)

2.129

(0.179)

FDI X EXC 0.0345

(0.571)

-3.237*

(0.007)

7.122*

(0.069)

2.560*

(0.046)

0.364*

(0.08)

4.168

(0.311)

-5.108

(0.104)

BNK -0.024

(0.149)

0.058*

(0.092)

-0.29*

(0.03)

-0.290

(0.493)

-0.440*

(0.08)

0.085*

(0.064)

-0.103

(0.225)

EXC 0.0143

(0.193)

0.064*

(0.016)

-0.181

(0.179)

0.025

(0.66)

-0.025*

(0.51)

-0.031

(0.776)

0.310

(0.126)

Constanta 0.0542 -0.04 0.561 0.11 0.424 -0.14 0.249

R Square 37.37% 85.49% 82.71% 43.73% 79.91% 60.49% 73.55%

Ad

j

usted R

2

29.46% 75.34% 69.27% 41.76% 64.28% 56.77% 62.99%

The result above displays that foreign direct

investment positively affected economic growth with

such significance in all countries, as depicted in the

first model. Indonesia and Philippines are two

countries with the biggest multiplier effects from

foreign direct investment, as confirmed by bigger

coefficient. It is interestingly linked to the average

data from our observations that these two countries

had the lowest foreign direct investment. Indonesia

and Philippines will need to stimulate higher foreign

direct investment to boost their economic growth.

Both are developing countries, unlike Malaysia and

Singapore, so Indonesia and Philippines still have a

lot of room for future growth.

Moreover, the variances clearly show the

moderating effect of different levels of financial

institution development for each country. Indonesia’s

result implies that its financial institutions weaken

positive effects of foreign direct investment. This

could be explained by the fact that Indonesian

banking system charges one of the highest profit

margin in the world; hence, many foreign banks

operate in this country. Indonesian banks merely seek

to maintain their profit, yet it proves to be costly for

the economy, because they charge high interest rate

to its debtors and make the business less thriving. The

stock market also provides the same result.

Indonesia’s stock exchange still relies on foreign

capital in which 60% of its fund is invested by foreign

investors. The investors usually seek short-term profit

and the stock’s return will be flown back to their

home country. Financial market in Indonesia is still

heavily regulated by the government and it is hard for

foreign firms to fund its project locally. Most banks

refuse to lend money to joint ventures, particularly to

foreign firms, even though such investment is also a

form of foreign direct investment. Currently none of

foreign firms go public in Jakarta Stock Exchange,

due to the high level of red tapes. These factors

further weaken the positive effect of foreign direct

investment in Indonesia.

Different result came from Malaysia and

Philippines in which their financial institution indeed

strengthened the efficacy of foreign direct

investment. Malaysia showed equal growth in banks

and stock exchange by 130% of its GDP, as displayed

in Table 4. Philippines recorded similar result, albeit

in lower number by 56% of its GDP. The similarity

here proves the importance of balanced financial

institution in which both plays complementary roles

in supporting Malaysian economy. This finding is in

line with Beck, Levince, and Loayza’s (2000) which

stated that proper financial system turn more capital

into profits and stimulate the economy even further.

They stated that a well-developed financial system

can generate more capital and accelerate growth, in

which FDI provides a stimulate through capital

accumulation. Both banks and stock exchange act as

financial intermediaries and together shall ensure that

the fund flows to the right creditor or firms, hence

boosting the economy

The Relationship between Foreign Direct Investment Influx, Economic Growth, and Financial Institutions in ASEAN-6

31

Table 4: Data average for all samples and variables

Moreover, Singapore is considered as the most

developed country among other ASEAN members;

thus, it has the highest level of FDI influx. However,

it lacks equal development of financial institutions,

unlike Malaysia and Philippines. Thus, Singaporean

banks may render FDI insignificant due to extremely

high level of competition among 3 largest financial

institutions. When there are only 3 banks holding

76% of country’s banking assets, the competition will

become unhealthy. Like other developed countries,

Singaporean banks no longer focus in lending, but

shifting towards investment services and supporting

stock exchange. The stock exchange has a bigger

effect towards its economy, as confirmed by its size

which is doubled the country’s GDP during research

period. It is expected to boost the positive effect from

FDI on economy growth. Unlike Indonesia, there are

many foreign firms listed in Singapore stock

exchange, so it is easier for FDI-invested firms to

fund its operations through capital market.

On the other hand, Thailand displays an opposite

result to Singapore, in which stock exchange reduces

the significance of FDI due to the smaller size of its

banking system. Most Thai business is still funded by

banks, so it is confirmed that FDI may enhance its

positive effects by strengthening banking regulation

in Thailand.

The last country observed is Vietnam.

Unfortunately, the effects from both financial

institution diminished the positive influence of FDI.

Wang (2016) stated that Vietnamese banks currently

focus in retail and consumer loans. Vietnam

government also controls financial industry

rigorously and its stock market just opened in 2007.

Therefore, it shows insignificant moderated results.

5 CONCLUSIONS

This research explains positive impacts of FDI

on economy growth among ASEAN-6 countries.

The most illuminating result is the importance of

balanced financial institution in each country to

support economy growth. Both bank and stock

exchange market are financial intermediaries

and should have complemented each other,

instead of acting like competitors.

For future researches, it is advised to add

more observed variables, due to the limit of

sampling procedures in this study. Also, the

rising trend of non-bank financial institution

(NBFI) can be included as funding alternative

from banks and stock exchange.

REFERENCES

Alfaro, Laura., Chanda, Areendam., Kalemli-Ozcan,

Sebnem., and Sayek Selin. (2004). FDI and economic

growth: the role of local financial markets. Journal of

International Economics. 64.

Aryani, Made Gitanadya. (2016). Determinants of Bank’s

Net Interest Margin in 5 South East Asian Countries.

(Master Thesis. Universitas Airlangga, Surabaya)

ASEAN. (2018). ASEAN Economic Community.

Retrieved from asean.org/asean-economic-community/

ASEAN Investment. (2018). About AEC. Retrieved from

http://investasean.asean.org/index.php/page/view/a

sean‐economic‐

community/view/670/newsid/755/about‐aec.html

ASEAN Stats. (2017). Retrieved from

http://www.aseanstats.org/

Balasubramanyam, N.V., Salisu, M., and Sapsford, D.

(1996). Foreign Direct Investment and Growth in EP

and IS Countries. The Economic Journal, 106(43).

Average ECO FDI BNK EXC

IND 5.3% 1.20% 44.92% 35.22%

MAL 5.1% 3.30% 131.8% 136.5%

PHIL 5.3% 1.55% 53.69% 58.59%

SING 5.3% 18.67% 90.60% 210.7%

THAI 4.0% 2.85% 137.3% 71.56%

VIET 6.4% 5.46% 90.43% 14.27%

ALL 5.2% 5.50% 91.46% 87.80%

ACIR 2018 - Airlangga Conference on International Relations

32

Beck, T., Levine, R., and Loayza, N. (2000). Finance and

sources of growth. Journal of Financial Economics,

58(1-2).

Coccorese, Paolo. (2010). Banking competition and

economic growth. Proceedings from the 58th Annual

Conference of the Italian Economic Association.

Università degli Studi di Salerno vol 58, Fisciano, Italy.

Carkovic, M. and Levine, R. (2002). Does foreign direct

investment accelerate economic growth? Department of

Finance Working Paper, University of Minnesota.

Esfandyari, Marzieh. (2015). The Role of Financial

Markets Development in the Foreign Direct Investment

Effect on Economic Growth (The case of D8 with

Emphasizing on Iran). International Journal of

Academic Research in Business and Social Sciences,

5(10).

Fan, Xiaoqin, and Dickie, Paul M. 2000. The Contribution

of Foreign Direct Investment to Growth and Stability:

A Post-CrisisASEAN-5 Review. ASEAN Economic

Bulletin. 17(3).

Fox, Sean and Dyson, Tim. (2015). Is population growth

good or bad for economic development? Retrieved

from https://www.theigc.org/

Hermann, Simon. (2016). Is there a correlation between

GDP growth and stock market returns? Retrieved from

http://investopedia.com

Hoang, Thu Thi, Wiboonchutikula, Paitoon, and

Tubtimtong, Bangorn. (2010). Does Foreign Direct

Investment Promote Economic Growth in Vietnam?

ASEAN Economic Bulletin, 27(3).

Kok, Recep, and Ersoy, Bernur A. (2009). Analyses of FDI

determinants in developing countries. International

Journal of Social Economics, 36(1/2).

Levine, R., Loayza, N., Beck, T., (2000). Financial

intermediation and growth: causality and growth.

Journal of Monetary Economics. 46(1).

Liang, Hsin-Yu. Reichert, Alan K. (2010). The impact of

banks and non-bank financial institutions on economic

growth. The Service Industries Journal. 32(5).

Madura, Jeff. (2012). International Financial Management

(11th edition). New York: Cengage Learning.

Nunnenkamp, Peter. (2001). Foreign direct investment in

developing countries: What policymakers should not do

and what economists don't know, Kieler

Diskussionsbeiträge, 380. Retrieved from

http://hdl.handle.net/10419/2616

Soumaré, Issouf and Tchana, Fulbert T. (2014). Causality

between FDI and Financial Market Development:

Evidence from Emerging Markets. World Bank

Economic Review.

South East Asia Network for Development. (2015). AFAS

on Financial Services. Retrieved from

http://www.seanet.com/

Tan, Bee Wah, and Tang, Chor Foon. (2016). Examining

the Causal Linkages among Domestic Investment, FDI,

Trade, Interest Rate and Economic Growth in ASEAN-

5 Countries. International Journal of Economics and

Financial Issues, 6(1).

Thuku, Gideon, Paul, Gachania and Almadi, Oebere.

(2016). The impact of population change on economic

growth in Kenya. International Journal of Economics

and Management Sciences. 19(25).

UNCTAD. (2016). The World Investment Report. United

Nations Conference on Trade and Development,

Geneva, Switzerland.

Wang, Miao. (2009). Manufacturing FDI and economic

growth: evidence from Asian economies. Applied

Economics. 41(8).

Wang, Shenming. (2016). Vietnam banks: putting their

money in retail banking and technology. Retrieved

from http://www.theasianbanker.com/

World Bank. (2001). Investment Flows through the Decade.

The World Bank, Washington, DC.

World Bank. (2016). Global Development Financial

Report. The World Bank, Washington, DC.

Zhao, Shiyong. (2016). Does financial development

necessarily lead to economic growth? Evidence from

China. Macau University of Science and Technology,

Macau, China.

The Relationship between Foreign Direct Investment Influx, Economic Growth, and Financial Institutions in ASEAN-6

33