Information System Integration, Knowledge Management, and

Management Accounting Adaptibility

Zul Azmi

1*

, Abdillah Arief Nasution

2*

and Iskandar Muda

2

1

Faculty of Economics and Business, Universitas Muhammadiyah Riau

2

Faculty of Economics and Business, Universitas Sumatera Utara

Keywords: Information System Integration, Knowledge Management Enablers, Knowledge Management Process,

Accounting Management.

Abstract:

Management accounting practices are expected to adapt and evolve along with changes in expected

information needs and changes in information technology. The influence of knowledge management and

information system integration on management accounting adaptibility has become an important concern.

Knowledge management enablers (KME) and knowledge management process (KMP) is an important tools

for improving information system utilization. Internal information system intergration (IISI), external

information system integration (EISI) and information system flexibility (FSI) together with knowledge

management roles are expected to improve management accounting adaptibilty (AAM) to change in

information needs and expected adjustments. The questionnaire survey was conducted at the managerial

level for middle and upper level companies in Riau Province Indonesia using the use of information systems

in activities for decision making. 159 respondent were obtained andmet the criteria for use in this study. By

using partial least square SEM (SEM-PLS) obtained FSI, IISI and KMP have significant effect on AAM.

KME is supporting KMP to improve AAM. Increasing KMP level can effect FSI and IISI level. Increased

IISI level can improve EISI utilization level.

1 INTRODUCTION

Contingency theory suggest that management

accounting practices in organization should develop

and change the environment for the better at internal

and external conditions. Management accounting

change related to global competition, changes in

manufacturing technology (Innes et al., 2000),

information technology (Waweru, et al., 2004),

organizational structure (Abernethy & bouwen,

2005) and strategy (Fullerton, 2012). The ability of

management accounting to change over time or its

effectiveness is a critical point to achieve

management accounting conformity (Yigitbasioglu,

2016). Despite the known technological resources as

a facilitator for change (Innes & Mitchell, 1995), but

information system integration can lead on

technological embeddedness, and the stability of

management accounting (Rom dan Rohde, 2007).

Information integration is a present challenge in data

management (Quix & Jarke, 2014). The

development of new technologies and application

will form new conformity criteria that enhance the

information system integration.

Krumwiede & Charles (2014) show that for

firms with low price strategy had a positive impact

on earnings performance, especially when the

activity based costing is used with high quality

information system. Support to improve the quality

of management accounting can be facilitated by

information system integration, such as the

availibility of software budgeting, enterprise

resources planning systems,business intelligence and

analytics (Rom & Rohde, 2009; Yigitbasioglu &

Prasad, 2013). Business intelligence technology can

provide data collection, analysis and information

presentation as a decision making tool that support

the activities of management accountiants

(Rikhardson & Yigitbaisoglu, 2018; Appelbaum et

al., 2017). In addition, the use of business

intelligence and analytics with visualization

techniques in management accounting in big data

becomes an interesting concern because of the

relative lack of knowledge and empirical finding

(Rikhardson & Yigitbaisoglu, 2018). Thus, data

Azmi, Z., Nasution, A. and Muda, I.

Information System Integration, Knowledge Management, and Management Accounting Adaptibility.

DOI: 10.5220/0010070118871894

In Proceedings of the International Conference of Science, Technology, Engineering, Environmental and Ramification Researches (ICOSTEERR 2018) - Research in Industry 4.0, pages

1887-1894

ISBN: 978-989-758-449-7

Copyright

c

2020 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

1887

limitation are not related to manager accountability,

although data problems do not inhibit the

development of measurement systems, but tend to

hamper goverment employees using the resulting

system to evaluate performance (Cavalluzzo &

Ittner, 2004). Thus, the availability of data as

information seems to be inconsistent. Therefore, it

needs to be seen how the integration of information

systems affect managers in providing management

accounting information.

Yigitbasioglu (2016) show that the share

knowledge among managers positively associated

with management accounting adaptibility.

Information system integration can affect the share

knowledge between IT and managers in improving

performance. In relation to organizational

performance, share knowledge is part of knowledge

management. While knowledge management

consist of knowledge management enabler and

knowledge management process that can improve

performance (Lee & Choi, 2003). However, the

influence of knowledge management and

information system integration in improving

management accounting adaptibility is still

uncommon in empirical research.

Accordingly, knowledge become an important

factor in business development. Although some

forms of intellectual capability can be transferred,

but intrinsic knowledge is not easy transferred.

Therefore, the fundamental objective of

management is to improve the process of

acquisition, integration, and utilization of knowledge

known as knowledge management (Kovacic, Bosity

& Loncar, 2006). Knowledge management still has

obstacles. One of the impediment is that

organizations often do not know what they know

(William, John & Peter, 2012). The particular skills

and knowledge possessed by employeses can

sometime be of no value to their colleagues and

superiors, at those who can make use of this

knowledge do not know who is knowledgeable and

unaware of its existence (Nevo et al., 2012).

Therefore, this research needs to be directed to the

elements those who have a knowledge management

that would support management accounting

adaptibility that will in turn improve performance.

McKeen, Zack & Singh (2009), Nnabuife (2015),

and Wahda (2017) shows the effect of knowledge

management on organizational performance.

Knowledge management (KM) can consist of

different elements, such as on Lee & Choi (2003),

Awan dan Khalid (2015), Hermawan et al. (2015).

To show the effect of enablers on knowledge

management then used KM enablers (KME). KME

will support KM creation process (KMP) consisting

socialization, externalization, internalization, and

combination (SECI) (Lee & Choi, 2002; Hermawan

et al., 2015).

Management accounting adaptibility related to

information systems that support the organization.

The flexibility of information system is an important

element of the organizational information

technology infrastructure (Bird & Turner, 2000).

Information technology resources related to human

resources and organizational skills, knowledge

management, competence, commitment, value,

norms and orgnizational structure. Thus, the

flexibility of information system in information

technology infrastructure can improve management

accounting adaptibility (AAM). AAM associated

with the integration of information system and

information system flexibility. The integration of

information system makes information processing

visible and supports global transparency (McAdam

& Galloway, 2005; Chapman & Kihn, 2009).

Integration and reconfiguration transform the

application of the information system infrastructure

into unique capabilites that provide streaming and

sharing information within the organization and

between the organization (Maiga, 2017). Integratin

of internal and external information system relates to

AAM and operational performance.

Management accounting that can adapt to

changes can improve the effectiveness of

management accounting functions. In other word,

adaptibility is important because the environment in

which the organization operates may change rapidly

(Yigitbasioglu, 2016). Changes in technology,

market conditions, strategies and organizational

style requires a new management accounting

practices. Therefore an adaptable management

accounting system will be more effective than a

relatively static system.

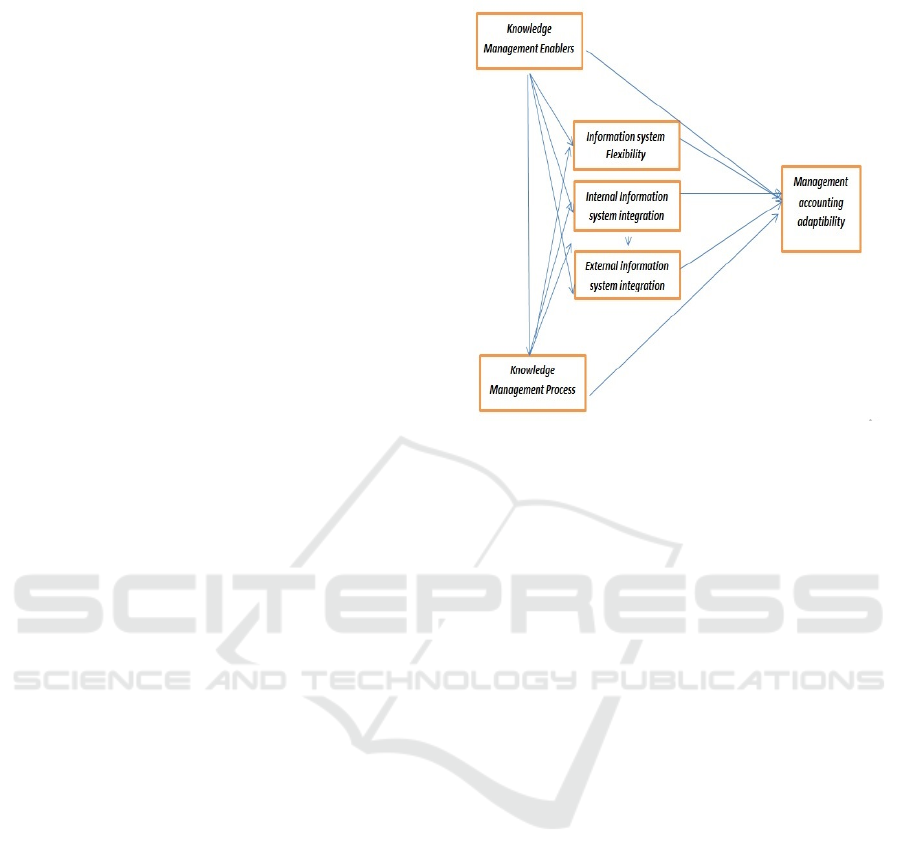

This paper aims to demonstrate knowledge

management enablers and knowledge management

process affect on the integration of internal and

external information system and information system

flexibility on management accounting adaptibility at

the firm. Characteristics of information systems can

be seen in the information system flexibility and

information system integration. Maiga (2017)

demonstrate the operational performance of

manufacturing companies affected by internal

information system integration and external

information system integration. Based on Maiga

(2017) the integration of the internal and external

information system can be describe adaptibility level

of management accounting. The remainder of this

ICOSTEERR 2018 - International Conference of Science, Technology, Engineering, Environmental and Ramification Researches

1888

study is organized as follows. Section 2 provides the

hypothesis development, while section 3 discuss the

research methods. Section 4 presents the result and

discussion, Finally, section 5 presents conclusion.

2 HYPOTHESIS DEVELOPMENT

The role of management accounting system has

evolved starting form the emphasis of the financial

analysis orientied and budgetary control, then

evolving into management accounting that includes

a more strategic approach with emphasis on

identifying, measuring, and managing key financial

and triggers operation to the value of shareholder

(Ittner & Larker, 2001). The responsibilites of the

management accountants evolve from merely

reporting aggregate historical value to also include

measurement of organization al performance and

providing information for decision making

(Appelbaum, et al., 2017). The ability of accountant

to utilize integrate information system capabilities

can dynamically improve the value. Past research

has shown that management accounting practices

can be effective if suppoerted by integrated

information system (He, 2007; Maiga et al., 2013;

Quix & Jarke, 2014; Chapman & Kihn, 2009;

Yigitbasioglu & Prasad, 2013;Yigitbasioglu, 2016).

Integrated information system can be divided into

two internal information system integration (IISI)

and external information system integration (EISI)

(Fayard et al., 2012; Ward & Zhou, 2006; Maiga,

2017), but few research explains EISI and IISI on

AAM.

IISI capabilities can provide enhanced role to

integrate and coordinate information and diverse

activities within the company’s internal fuctional

areas. Information system can continuously monitor

all corporate activities, updating data can be

reflected in the information system, and facilitate the

sharing information on internal company for

decision making. While on EISI, accountants can

retrieve informationm share information among

members in a value chain whre suppliers and

customer can be invited to join a certain information

areas that can improve their performance (Maiga,

2017; Saxena & Jaiswal, 2013). Inadequate

information in corporate information system

infrastructure, resulting in insufficient enterprise

data input for decision making. With the integration

of information, companies can manage resources to

improve their capabilites in certain field so that the

information needed is available on time and

relevant. In the context of information system, the

effect of internal integration on external integration

can be explained by sharing information, strategic

alliances, and work together (Flynn et al., 2010;

Maiga et al, 2015). If the internal information

system is not integrated, it will be difficult to share

information to supply chain partner and customers.

This is because the information to be shared can be

inaccurate and not timely. Therefore, improvement

at the IISI will impact on EISI. Adequate EISI level

will drive AAM improvement. Therefore,

H1. IISI is positively associated with AAM.

H2. EISI is positively associated with AAM.

H3. IISI is positively associated with AAM.

Environment uncertainty encourage companies

working to improve its capability to take advantage

of their resources in order to collect, combine,

integrate the information needed for decision

making. The formulation and implementation of

strategies on the flexibility of efficient information

systems in an important aspect of risk management

(Palanisamy &Sushil, 2003). Information system

flexibility refers to Gebauer & Schober (2006) who

view the system information from flexible to use and

flexibel to change the system. The integration of

informatin system is claimed to make the form of

analysis more sophisticated and flexible to improve

performance (Chapman & Kihn, 2009). The

characteristics of the integrated data architecture that

underlie the integration of information system affect

the perceived success of the system. This

characteristics include improvements, internal

transparency, global transparncy and flexibility that

refers to Adler & Borys (1996). Flexibility in

information system is an important part of the

enabling approach to control, but does not affect the

performance of information system, this is due to

insufficient conditions of performance (Chapman

&Kihn, 2009). Yigitbasioglu (2016) demonstrate

that the flexibility of information system is

positively and significantly related to AAM. The

flexibility to change hte system is important to

consider because in some cases it require changes to

management accounting that can be done by user

and some other cases should involved technicians

for programming or program modification

(Yigitbaisoglu, 2016). Therefore,

H4. FSI is positively associated with AAM.

Knowledge management deals with the reception

and the storage of knowledge and makes knowledge

accessible to others within the organization (Meso &

Smith, 2000). Reffering to Lee & Choi (2003)

Information System Integration, Knowledge Management, and Management Accounting Adaptibility

1889

knowledge management enablers (KME) consists of

collaboration, trust, learning, centralization,

formalization, t-shape skills, and information

technology support. Some researcher view

knowledge management from a particular

perspective and seldom use integrative perspectives.

Collaboration explains the degree to which

individuals or groups are actively helping each

other. Collaborative culture affect the creation of

knowledge through the exchange of knowedge.

Trust can facilitate openness and influance

knowledge exchange. While centralization refers to

the locus of decision and control authority within the

entity. The more centralized a structure will hinder

communication and reduce the sharing of ideas.

Without communication and discussion of ideas the

creation of knowledge does not occur. The

participatory work envirenment supports knowledge

creation by motivating the involvement of members

of the organization. The same direction also occurs

in formalization. T-shaped skills means the owner

can explore the domain of certain knowledge and its

application to something deeply and broadly. Lastly,

information technology support is an essential

element for knowledge creation. This seven KMEs

as enablers for knowledge creation will become

more useful if the knowledge management process

(KMP) such as socialization, externalization,

combination, and internalization occurs

inorganizational entities (Nonaka & Takeuci, 1995).

Socialization transform from the tacit knowledge

through social interaction among members.

Externalization complies tacit knowledge into

explisit concepts. Combination convert explisit

knowledge into a systematic set way to combine it.

And in the internalization of the process of creating

knowledge absorbed by individuals, therefore can

enrich the tacit knowledge. Accordingly, we argue

that KME can improve the management accounting

adaptibility. Yigitbasioglu, (2016) explained that

share knowledge between IT nd managers in

organisations can influence the improvement of

AAM. KME can affect the integration of

information systems. Therefore,

H5. KME is positively associated with AAM

H6. KME is positively associated with KMP

H7a. KME is positively associated with IISI

H7b. KME is positively associated with EISI

H7c. KME is positively associated with FSI

H8a. KMP is positively associated with IISI

H8b. KMP is positively associated with EISI

H8c. KMP is positively associated with FSI

H9. KMP is positively associated with AAM

Figure 1 : Research Model

3 SAMPLE AND MEASURES

3.1 Sample

Sample taken from companies that located in Riau

Province. Questionnaire survey method was

conducted on the respondents. The sample is not

resticted to certain sectors or industries, although the

restrictions are applied to companies of middle and

upper category companies such as in the category of

companies that have SMEs with minimum omzet

Rp. 2,5 billion. Respondent should have an

involvement in the use of information system or

information technology in their work. Respondents

used are managerial level who experience working

more than two years and also have experience of job

involvement with information technology and

information system in management accounting field.

Through the database in the office of UMKM

obtained the list of company and company address.

We send a letter and or email to the respondent to

ask them to fill in the questionnaire. Due to

restrictions, participants with less than 2 years of

experience were excluded from the data, so only 159

responden were used. Survey conducted in

February-May 2018 at hte company in the Riau

Province. This survey is not limited to business

sector of the company. Thus the business services,

trade, manufacturing sectors are included in the

survey.

ICOSTEERR 2018 - International Conference of Science, Technology, Engineering, Environmental and Ramification Researches

1890

3.2 Measures

The size of the flexibility of the information system

is based on Yigitbasioglu (2016) that derived from

Gebauer & Schober (2006). Five point likert-type

scale is used for this questionnaire. For the above

item size the range is used from “1 = strongly

disagree” to “5= strongly agree”. All of the variables

in this study used range 1 to 5. The size of EISI and

IISI refers to Maiga (2017). IISI is measured using

four items and EISI is used four item questions with

a five point likert-type scale. EISI and IISI used to

measure information system integration. KME and

KMP size refer to Lee & Choi (2003). KME

measures include the seven constructs that include

collaboration, trust, learning, centralization,

formalization, T-shape skill, and IT support. Some

items on KME are acually measured on the negative

direction such as in centralization. The size of KMP

include four contructs: socialization, externalization,

combination, and internalization known as SECI. As

for the variable adaptibility management accounting

is based on Yigitbasioglu (2016). Data analysis

technique used is structural equation modelling

(SEM) approach with PLS.

4 RESULT AND DISCUSSION

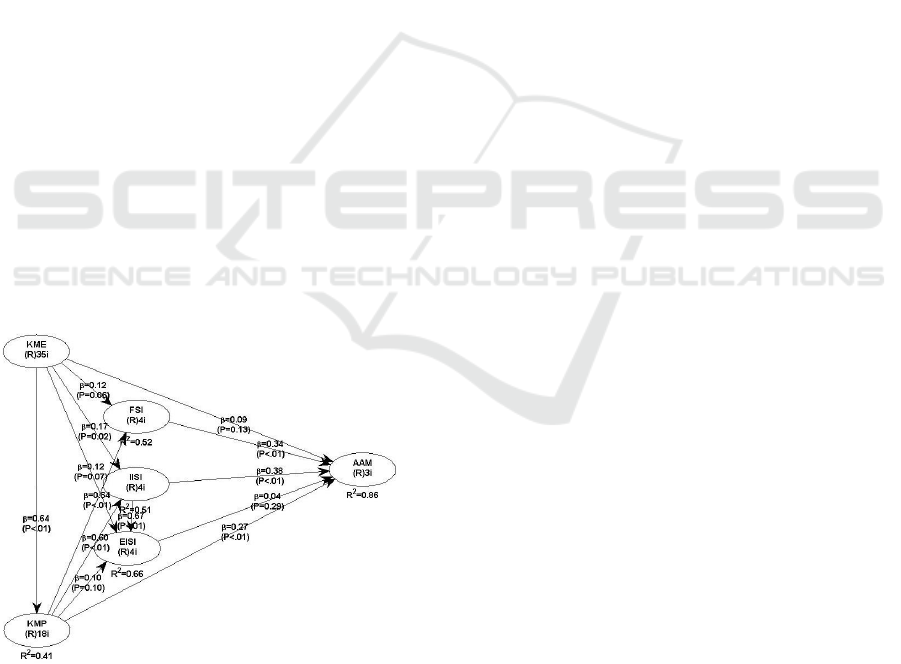

Result for test of influence of contruct presented in

the picture 1.

Figure 2 : path diagram and hipothesis test results

Based on the calculation of PLS can be seen that

coefficient path of 0,637 and p<0,001 for KME

effect on KMP. Thus H6 is supported. This mean

that socialization, externalization, combination,

internalization (SECI) in KMP run well because it is

supported by KME which become enablers.

Collaboration, trust, learning, centralization,

formalization, t-shaped skills and IT support as part

of KME have an effect on socialization,

externalization, combination, internalization. The

essence of SECI is the alteration to tacit knowledge

to exsplicit knowledge or vice versa, or as well as

from tacit knowledge to tacit knowledge and from

exsplicit knowledge to explicit knowledge

(Hermawan et al, 2015; Yeleneva et al., 2017;

Nonaka & Takeuchi, 1995). To improve the

capability of the management accounting

adaptibility that has to move change to adjust the

analysis needs for management, it needs to be

managed by KME and KMP.

For calculation of KME on FSI, path coefficient

=0,121 and p=0,06 which mean bigger than p<0,05.

KME has no significant effect on FSI. Thus, H7c is

rejected. While the calculation of KMP on FSI, path

coefficient = 0,636, p<0,001. H8c is therefore

supported. This explained that the creation process,

knowledge lead to the success of SECI than KME

toward FSI. H8c is therefore supported. For

calculation KME to IISI known path coefficient

equal to 0,166 and p=0,016. This means H7a is

supported. While the result of calculation of KMP

on IISI obtained path coefficient equal to 0,599,

p<0.001 meaning significant effect. Thus, H8a is

supported. Information integration can make visible

processing and support cognitve processes so that

the presentation of information become responsives.

The ability of IISI to provide information can enable

user to obtain detailed internal information regarding

their work. KME and KMP are very useful to

support the integration of information system on

internal activites of the company.

The effect of KME on EISI is shown bt hte path

coefficient of 0,116 and p=0,068. Therefore H7b is

rejected. The effect of KMP on EISI is described by

path coefficient equal to 0,101 and p=0,098. Thus

H8b is rejected. This indicate that the effect of KME

and KMP to EISI are not significant. The integration

of information system is sourced from both internal

dan external. This insignificant influence is probably

because manager feel quite satisfied with existing

information system and are reluctant to spend time

and knowledge for the new system (Cavalluzzo &

Ittner, 2004). In addition, the supply chain

information system refers to conformity between

firms so that the design of outgoing information

system is not the main focus of attention.

Information System Integration, Knowledge Management, and Management Accounting Adaptibility

1891

The effect of KME on AAM is shown by the

path coefficient of 0,087 and p=0,132. Thus, H5 is

rejected. The effect of KMP on AAM is equal to

0,273 and p<0,001, so that H9 is supported. This

mean that KMP with SECI elements can improve

AAM. The result of FSI calculation on AAM

obtained the path coefficient equal to 0,337 and

p<0,001, so H4 is supported. This indicate that FSI

related to changes or modification to the interface or

features required can be tailored to the individual

needs of the user. In the context of capturing the

user’s reaction to the financial statements, AAM can

be facilitated because of FSI support.

For the calculation of the effect of IISI on EISI,

path coefficient equal to 0,668, p<0,001. Hence, H3

is supported. Because EISI is related to standardize

information exchange, digitizing sharing between

organizational business activities, integration will

make information available on time and relevant to

information exchange with supply chain partnersfor

business decision making (Zou & Benton, 2007).

The higher the IISI level the higher the level of EISI,

in other words IISI inline with EISI. If you want to

build EISI capability, IISI capability will built first

(Maiga et al., 2015). For the calculation of IISI on

AAM, path coefficient equal to 0,382 and p<0,001

which mean IISI have significat effect on AAM.

Hence, H1 is supported. Because IISI deal with the

application of enterprise information technology to

systematic data acquisition, data processing, and

data storage, that support accurately and timely

information, its useful for AAM’s adaptation

capabilities.

To calculate effect of EISI on AAM, the result

show path coefficient equal to 0,04 and p=0,290.

This mean EISI has no significant effect on AAM,

so H2 is rejected. Although the EISI level increases,

it does not contribute significantly to AAM. This

indicates that EISI is still important to AAM but not

sufficient to support AAM performance.

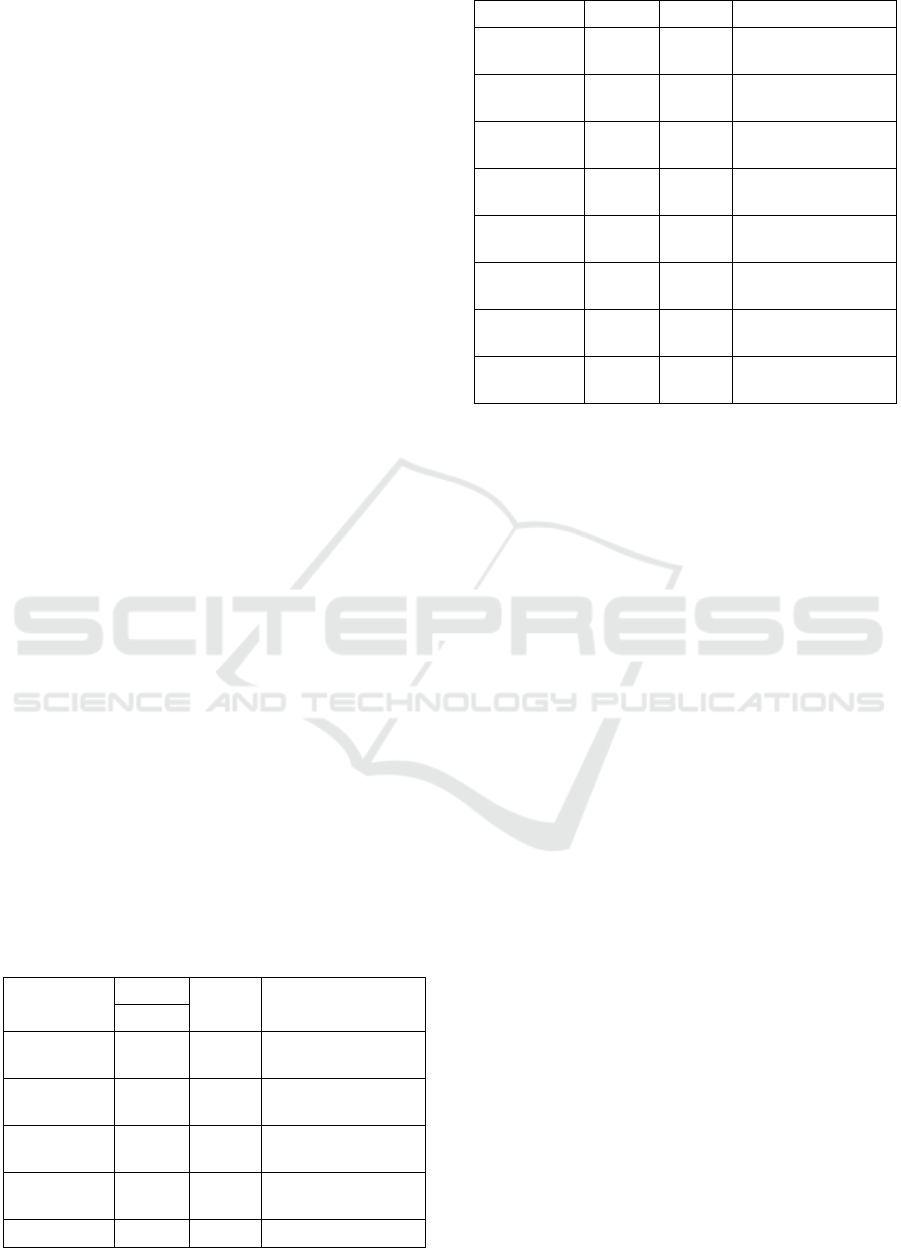

Table 1 : Summary of the results

Effect Coeff. p Description

Path

KME on

KMP

0,64 <0,01 Significant

KME on

A

AM

0,09 <0,13 Insignificant

KME on

FSI

0,12 <0,06 Insignificant

KME on

IISI

0,17 <0,02 Significant

KME on 0,12 <0,07 Insignificant

EISI

KMP on

FSI

0,64 <0,01 Significant

KMP on

IISI

0,60 <0,01 Significant

KMP on

EISI

0,10 <0,10 Insignificant

KMP on

A

AM

0,27 <0,01 Significant

FSI on

A

AM

0.34 <0,01 Significant

IISI on

A

AM

0,38 <0,01 Significant

EISI on

A

AM

0,04 <0,29 Insignificant

IISI on

EISI

0,67 <0,01 Significant

The indirect effect model can be statistically

identified through the path. To know the indirect

influence or influence of mediation can be seen

through the path diagram. The indirect effect of

KME to AAM can be though five liner; (1) KME-

FSI-AAM; (2) KME-IISI-AAM; (3) KME- EISI-

AAM; (4) KME-KMP-AAM; (5) KME-IISI-EISI-

AAM. If one or more of these indirect effect are

significant than the indicate partial mediation

(Solihin, 2013). Thus there can be a significant

direct influence as well as significant indirect

influence. On line 1 is not significant because KME-

FSI is not significant. In liner 2 significant because

KME-IISI and FSI-AAM are both significant. On

line 3 and 5 are not significant. While in line 4

significant.

The indirect effect model of KMP-AAM can

be explained through four line: (1) KMP-FSI-AAM;

(2) KMP-IISI-AAM; (3) KMP-EISI-AAM; (4)

KMP-IISI-EISI-AAM. In path 1 of KMP-FSI-AAM

is significant and so in path 2. While in path 3

and 4

are no significant. Thus FSI and IISI mediate partial

effects of KMP-AAM. In other words, KME

positively affects AAM through KMP and IISI as

mediating variables. KMP positively affect AAM

with FSI and IISI as mediation variables.

5 CONCLUSION

AAM can work well if the integratio of internal

information system improved. The agility to adapt is

determined by how flexible the information system

is. Flexible means flexible to use and flexible to

change. Thus, flexibility of information system can

ICOSTEERR 2018 - International Conference of Science, Technology, Engineering, Environmental and Ramification Researches

1892

improve AAM. Improvement of IISI quality depend

on KME and KMP. Knowledge management in this

case is important for IISI readiness providing

information to accountant. All KME enablers needed

to improve KMP quality. The proces of knowledge

management can improve the fungtinality of IISI in

providing information for the need of management

accounting adaptibility in responding to change

quickly. It seems that flexibility in the FSI has no

significant effect on KME. However, KMP has a

significat effect on FSI.

The readiness of information system integration

in the context of accounting is associated with big

data. The general concensus is that big data can lead

to disruptive conditions in accounting. Therefore

some management accounting techniques will

become obsolate and unused, so that management

accounting changes and the role of management

accounting can shift. Significant change can occur

that require adaptibility of management accounting.

However, we did not examine the effect of big data

in IT readiness providing information for business

organizations.

REFERENCES

Abernethy, M.A., Bouwen, J. (2005). Determinants of

Accounting innovation implementation, Abacus, Vol.

41, No. 3, pp. 217-240

Adler, P., & Borys, B. (1996). Two type of bureucracy:

enabling and coercive, Administrative science

quarterly, 41 (1), 61-90.

Anderson, S.W. & Young, S.M. (1999). The impact of

contextual and process factor on the evaluation of

activity based costing system, Accounting

organization and society, 24, 525-559.

Appelbaum, D., Kogan, A., Vasarhelyi, M.,& Yan, Z.

(2017). Impact of business analytics and enterprise

systems on managerial accounting, International

journal of accounting information systems, vol. 25, pp.

29-44.

Awan, A.G., & Khalid, M. I., (2015). Impact of

Knowledge Management on Organizational

Performance: A Case of Selected Universities in

Southern Punjab-Pakistan. Information And

Knowledge Management, Vol. 5 (6), Hal. 59-67.

Byrd, T.A. & Turner, D.E. (2000). Measuring the

flexibility of information technology infrastructure:

exploratory analysis of a construct, Journal of

management information system, 17: 167-208.

Cavalluzzo, K.S. & Ittner, C.D. (2004). Implementing

performance measurement innovations: evidence from

government, Accounting, organization and society, 29,

pp.243-267.

Chapman, C.S. & Kihn, L-A. (2009). Information system

integration, enabling control and performance,

Accounting, organization, and society, 34: 151-169.

Fayard, D., Lee, L.S., Leitch, R.A. & Kettinger, W.J.

(2012), effect of internal cost management,

information system integration, and absorbtive

capacity on interorganisasional cost management in

supply chains, Accounting, organization and society,

37, 168-187.

Flynn, B.B., Huo, B., & Zhao, X. (2010). The impact of

supply chain integration on performance: a

contingency and configuration approarch, Journal of

operation management, 28(1), 58-71.

Fullerton, R.R., Kennedy, F.A., & Widener, S.K., (2012),

Management accounting and control practice in a lean

manufacturing environment, Accounting,

organization, and society, Vol. 38, No. 1, pp. 50-71.

Gebauer, J. & Schober, F. (2006). Information system

flexibility and the cost efficiency of business

processes, journal of the association for information

system, vol.7 no.3, pp.122-147.

He, Y. (2007). A research of integration between ERP

system and ABCM, in Proceeding of the 2nd

international confrence of and practical issues of

enterprise information system, pp. 781-786. Beijing.

Hermawan, S., Hariyanto, W. & Sumartik, (2015).

Integrasi InteLLectual Capital dan Knowledge

Management Serta Dampaknya Pada Kinerja Bisnis

Perusahaan Farmasi, Jurnal Akuntansi

Multiparadigma, Vol 6(3), Hal. 341-511.

Innes, J. & Mitchell, F. (1990). The process change in

management accounting: some field study evidence,

Management accounting research, 1 (1):3-19.

Innes, J., Mitchell, F. & Sinclair, D., (2000). Activity

based costing in the UK’s largest companies: a

comparison of 1994 and 1999 survey result,

Management Accounting Research, Vol.11 (3), pp.

349-362.

Ittner, C.D., & Larker, D.F. (2001). Assessing empirical

research in management accounting: a vaue based

management perspective, Journal of Accounting and

economics, 32 (1), pp. 349-410.

Kovacic, A. Bosiji, V., & Loncar V., (2006). A Process-

Based Approach to Knowledge Management,

Economic Research, Vol 19 (2), Hal 53-66.

Krumwiede, K.R., & Charles, S.L. (2014). The use of

activity based costing with competitive strategies:

impact on firm performance, Advances in management

accounting, vol. 23, 113-148.

Lee, H., & Choi, B., (2003). Knowledge Management

Enablers, Processes, and Organizational Performance:

an Investigative View and Empirical Examination.,

Journal of Management Information System, Vol 20

(1), Hal. 179-228.

Maiga, A.S., (2017). Assessing the main and interaction

effects of activity based costing and internal and

external information system integration on

manufacturing plant operational performance,

Advances in Management Accounting, Vol. 29, pp.55-

90.

Information System Integration, Knowledge Management, and Management Accounting Adaptibility

1893

Maiga, A.S., Nilsson, A. & Jacob, F.J. (2013). Extent of

managerial IT use, learning routines and firm

performance: a tructural equation modelling of their

relationship, International journal of accounting

information system, 14 (4), pp.297-320.

Maiga, A.S., Nilsson, A., & Ax, C. (2015). Relationship

between internal and external system integration, cost

and quality performance , and firm profitability,

International journal of production economics,

http://dx.doi.org/10.1016/j.ijpe.2015.08.030

McAdam, R. & Galloway, A. (2005). Enterprise resources

planning and organisasional innovation: a

management perspective, Industrial management and

data system, vol. 105, no. 3, pp. 280-290.

McKeen, J.D., Zack, MH., Singh, S., (2009). Knowledge

Management and Organizational Performance: An

Exploratory Survey, Journal of Knowledge

Management, Vo. 13 Issue 6, Hal. 392-409.

Meso, P., & Smith, R. (2000). A resource based views of

organisational knowledge management system,

journal of knowledge management, 4(3), 224-234.

Nevo, D., Benbasat, I. Dan Wand, Y., (2012). The

Knowledge Demands of Expertise Seekers In Two

Different Context: Knowledge Allocation Versus

Knowledge Retrieval, Decision Support Systems, Vol

53, Hal.482-489.

Nnabaufe, K.E., Onwuka, E.M, dan Ojukwu, H.S., (2015).

Knowledge Management and Organizational

Performance In Selected Commercial Bank in Awka,

Anambra State, Nigeria. IOSR Journal of Business

And Management, Vo. 17, Issue 8, Hal.25-32

Nonaka, I. & Takeuchi, H. (1995). The knowledge

creating company, New york, Oxford university press.

Palasinamy, R. & Sushil, (2003). Achieving organizational

flexibility and competitive advantage through

information system, journal of information and

knowledge management, 2(3).

Quix, C., & Jarke, M., (2014). Information integrastion in

research information system, Procedia Computer

Science, 33, pp. 18-22.

Rikhardsson,P. & Yigitbasioglu, O. (2018). Business

intelligence & analytics in management accounting

research: status and future focus, International journal

of accounting information system, vol.29, pp.37-58.

Rom, A. & Rohde,C. (2007). Management accounting and

integrated information system: a literature review,

International journal of accounting information

system, vol 8 (1), pp. 40-68.

Saxena, A. & Jaiswal, M.P. (2013). Impact of enterprise

system on firm performance: a busines integration

capabilites perspective, IUP Journal of Operation

management, 12 (3), 29.

Solihin, M. & D. Ratmono, (2013). Analisis SEM-PLS

dengan warppls 3.0, Ed. 1, penerbit Andi offset,

Yogyakarta.

Wahda, (2017). Mediating effect of knowledge

management on organizational learning culture in the

context of organizational performance, Journal of

Management Development, Vol. 36 Issue: 7, pp.846-

858

Ward, P. & Zhou, H. (2006). Impact of information

technology integration and lean/just in time practice

on lead time performance, Decision science, 37, 177-

203.

Waweru, N.M., Hoque, Z., and Uliana, E., (2004).

Management accounting change in South Africa: case

study from retail services, Accounting, auditing, and

Accountability journal, Vol. 17, No.5, pp. 675-704.

William, N., John, V., & Peter, D., (2012). How

Organization Know What They Know: A Survey of

Knowledge Identification Method Among Australian

Organization. 23rd Australian Conference on

Information Systems, Geelong.

Yeleneva, J.Y., Kharin, A.A., Yelenev, K.S., & Andreev,

V.N. (2017). Corporate knowledge management in

rump up conditions: the stakeholder interests account,

the responsibility center allocation, CIRP Journal of

manufacturing science and technology, available at

https://doi.org/10.1016/j.cirpj.2017.12.002 .

Yigitbasioglu, O., (2016). Firm’s information system

characteristics and management accounting

adaptibility, International Journal of Accounting and

Information Management, Vol. 24 No.1, pp. 20-37

Yigitbasioglu, O. & Prasad, A. (2013). Management

accounting adaptibility in an integrated information

system environment, in 10th international confrence

on enterprice system accounting and logistic 2013

proceeding, utrecht, pp.93-101.

Zhou, H., & W.C. Benton, (2007). Suplly chain practice

and information sharing, Journal of operation

management, 25 (6), 1348-1365.

ICOSTEERR 2018 - International Conference of Science, Technology, Engineering, Environmental and Ramification Researches

1894