Factors that Influence Auditor’s Professional Skepticism

Evidence from Audit Firms in Surabaya

Lidia Sari Christina and Heru Tjaraka

Department of Accounting, Airlangga University, Surabaya, Indonesia

lidiasarichristina@yahoo.com

Keywords: The auditor’s professional scepticism, experience, expertise, audit situation, ethics, gender.

Abstract: The purpose of this study is to examine the factors that influence auditor’s professional scepticism. The

independent variables used in this study are experience, expertise, audit situation, ethics, and gender

whereas the dependent variable is auditor’s professional scepticism. Data was collected then processed by

Partial Least Square (PLS) from the result of developed questionnaire which were disseminated to the Audit

Firm-KAP in Surabaya. The number of respondent involved in this study were 59 out of 100 respondents or

50 % response rate. The survey questionnaire was delivered directly to the respondents in 15 Audit Firms in

Surabaya by purposive sampling method. After all, the final result shows that expertise, audit situation, and

ethics have positive and significant influence on auditor’s professional scepticism. Whereas experience and

gender do not have a positive influence on auditor’s professional scepticism, because the majority of

respondents' experience is still low, about 10 to 20 assignments and the response answer of both male or

female auditors is the same.

1 INTRODUCTION

Professional scepticism is a vital element in auditing

financial statements. The auditor’s professional

scepticism includes a critical assessment of audit

evidence and is particularly important when

considering the risks of material misstatement due to

fraud. It also means remaining alert for evidence

that contradicts other audit evidence or that brings

into question the reliability of information obtained

from management and those charged with

governance (

AUASB, 2012).

In providing appropriate reports on the

company's financial statements, the auditor must

adhere to professional standards, in which the

auditor is required to apply professional scepticism

(

Glover and Prawitt, 2014). In their assignment, the

auditor should always apply professional scepticism

during the process of collecting and assessing audit

evidence (

AICPA, 2001). A sceptical auditor does

not easily believe in the existing audit evidence,

rather they will always question about the

information they got from the client. Research

conducted based on Accounting and Auditing

Releases (AAERS) stated that one of the causes of

audit failure is an inadequate level of professional

scepticism applied by the auditor (Beasley et al.,

2001). Therefore, it can be said that when the level

of auditor's professional scepticism is low, it can

lead to failure in detecting fraud. Professional

scepticism of an auditor can be influenced by many

factors, including experience, expertise, audit

situation, ethics, and gender (Kushasyandita, 2012).

In this study professional skepticism was measured

through questionnaires given to respondents

regarding (1) auditor's level of doubt on audit

evidence, (2) number of additional assessments, and

(3) direct confirmation.

Both experience and expertise are important

elements for the auditor in performing audit

procedures because the expertise of an auditor also

tends to affect the level of professional scepticism of

an auditor (Kushasyandita, 2012). Experience is

something that needs to be paid attention in the

auditor's sceptic level of judgment, in which

experience allows the auditor to develop knowledge

of patterns that allow them to determine when

evidence does not accumulate (Hurtt, 2013). Auditor

with deeper knowledge of a client’s business is

better in resisting client’s persuasion attempts

(Brewster, 2015). In this case, an experienced

auditor will be more likely to provide a reasonable

explanation for the mistakes in the financial

statements and may classify those errors based on

the audit objectives and structures of the underlying

accounting system. Therefore, it is suspected that

326

Christina, L. and Tjaraka, H.

Factors that Influence Auditor’s Professional Skepticism - Evidence from Audit Firms in Surabaya.

In Proceedings of the 1st International Conference on Islamic Economics, Business, and Philanthropy (ICIEBP 2017) - Transforming Islamic Economy and Societies, pages 326-330

ISBN: 978-989-758-315-5

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

experience has an influence on auditor's professional

scepticism. The experience referred in this study is

the experience of an auditor in doing financial

statements audit in terms of time duration or the

number of assignments that have been done.

Experience variable was measured by questionnaire

on respondents' demographics on the number of

audit assignments completed during the work at the

Audit Firms and how long the auditor had their

experience as an auditor (Kushasyandita, 2012).

Expertise is an important component an auditor

must have in order to work professionally. This is

described in the first general standard of SA Section

210 (SPAP, 2011). In addition, expertise is

described as a progress of individual knowledge

during the development stage from beginner to

expert Harteis and Billett, 2013). The audit

committee needs to have the expertise and

commitment to ask critical questions about

management and external auditors. Moreover, the

audit committee should promote a culture of

professional scepticism by challenging judgments

from both management and auditors and

encouraging all parties to see all the potential

evidence when making a decision (

Glover and Prawitt,

2014)

. Situation factor such as high-risk audit

situation also affects an auditor to improve the

attitude of Auditor’s Professional Scepticism

(Winantyadi and Waluyo, 2014). The situation such

as the difficulty to communicate between past

auditor and new auditor on the information about a

company as an auditee will affect Auditor’s

Professional Scepticism (Arrens, 2007). Therefore, it

is suspected that expertise has an influence on

auditor's professional scepticism. In this study, the

measurement indicators for the expertise are

statements contained in a questionnaire of expertise

in which the questionnaire contained three

statements (Kushasyandita, 2012). They are intended

to determine the ability and knowledge possessed by

an auditor.

Audit situation is a situation in an audit

assignment, in which the auditor is exposed to a

situation with low audit risk (regularities) and a

situation with large audit risk (irregularities)

(Mulyadi, 2011). Irregularities are often defined as a

situation where deliberate or unintentional fraud

occurs. Other study found that the audit situation is

positively affect the auditor’s professional

scepticism (Winantyadi and Waluyo, 2014) (Anisma

and Abidin, 2012). Therefore, it is suspected that

audit situation has an influence on professional

scepticism. In this study, the audit situation variable

was measured using questionnaire questions, there

are five illustrations contained in scenarios one

through five (Kushasyandita, 2012).

Auditor’s ethics has an influence on auditor’s

professional scepticism (Winantyadi and Waluyo,

2014). Professional ethics is required by the auditor

as it is used to maintain public confidence in the

audit. Ethics in this study is a standard or a rule that

guides the act of a person to enhance one's dignity

and honor. The higher the auditor's ethical

awareness in auditing, then it will develop their

professional attitude (Winantyadi and Waluyo,

2014). Therefore, it is suspected that auditor’s ethics

has an influence on auditor's professional scepticism.

In this study, the professional ethics variable was

measured by questioning on the questionnaire for

professional ethics using three illustrations

(Kushasyandita, 2012).

Additionally, gender is also another factor that

affects auditor’s professional scepticism. In general,

gender is a visible difference in terms of behavior

and characteristics that exist in men and women. The

female internal auditors are on average more

sceptical than male ones (Fullerton and Durtschi,

2005). Therefore, in the presence of differences

between male and female characters, it may affect

attitudes and actions performed, so it is suspected to

be one of the reasons gender has an influence on an

auditor's professional scepticism. For the gender

variable, measurements for the variable can be seen

from the demographic of respondents, with

information (1) Male, (2) Female (Kushasyandita,

2012).

Based on the background above, the purpose of

this study is to examine the factors that influence

auditor’s professional scepticism. The method used

is the survey method and the type of data used in this

study is quantitative data in the form of score results

of each scenario in the questionnaire that have been

disseminated. Data analysis techniques in this study

are using Descriptive Statistics Analysis and Partial

Least Square (PLS) with the program SmartPLS.

The result shows that expertise, audit situation, and

ethics have positive and significant influence on

auditor’s professional scepticism. Whereas

experience and gender do not have a positive

influence on auditor’s professional scepticism.

2 METHODS

In this study, the method used is the survey method,

in which the author comes directly to the 15 Audit

Firms (KAP) located in Surabaya. The population in

this study was the auditors working on KAPs in

Surabaya and all the population were used as the

research sample. Sampling was done by purposive

sampling method.

Factors that Influence Auditor’s Professional Skepticism - Evidence from Audit Firms in Surabaya

327

The type of data used in this study is quantitative

data in the form of score results of each scenario in

the 100 questionnaire that have been disseminated.

The research data is the answer of respondent

questionnaires on auditor scepticism, experience,

expertise, audit situation, ethics and gender of the

auditors who work at KAPs in Surabaya. Data

analysis techniques in this study are using

Descriptive Statistics Analysis and Partial Least

Square (PLS) with the program SmartPLS.

3 RESULTS AND DISCUSSION

In this research the result of a questionnaire that can

be processed is 59 out of 100 or 50% rate.

Hypothesis testing was done by looking at the t-

statistic generated structural models (inner models).

The hypothesis can be accepted if t-statistic > 1.96.

The following is the Figure. 1 of the t-statistic

generated structural models (inner models) and the

coefficient of influence (original sample) :

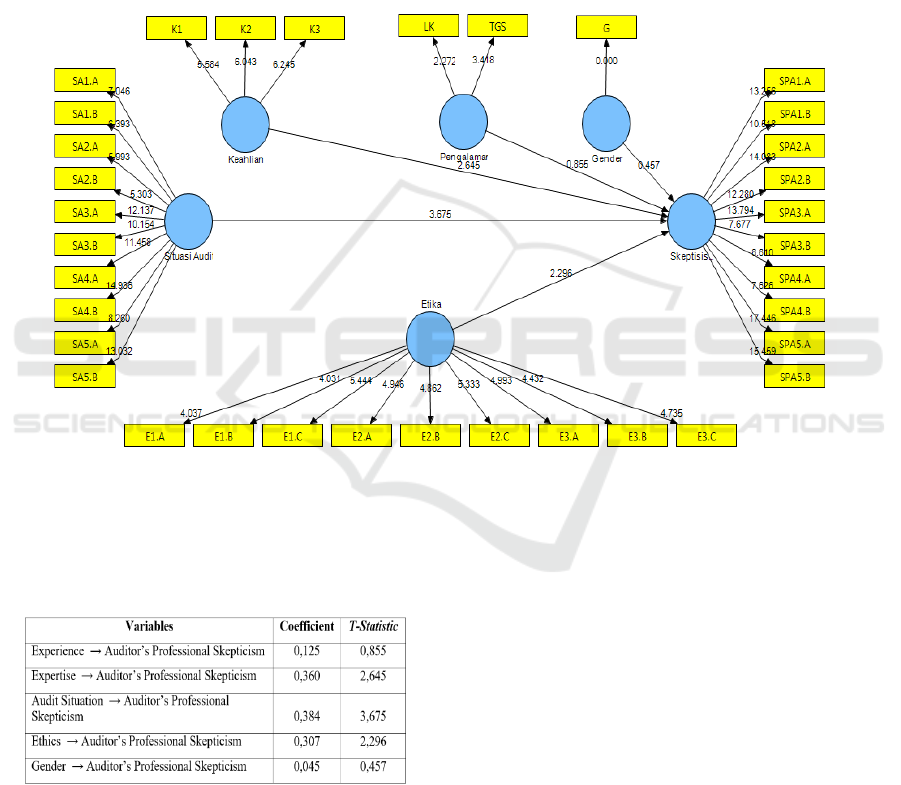

Figure 1: The t-statistic of the influence of experience, expertise, audit situation, ethics, and gender on auditor’s

professional skepticism.

Table 1: The test result.

Table 1 are the coefficient and t-statistic of the

influence of experience, expertise, audit situation,

ethics, and gender on auditor’s professional

skepticism.

From the table 1, the coefficient of the influence

of experience on auditor’s professional skepticism is

0.125 with t-statistic of 0.855 <1.96 showed in

Figure. 1. These results conclude that there is no

significant positive influence between experience

and auditor’s professional skepticism. Basically, an

auditor with longer term has generally performed

more audit assignments, thus having more

experience in detecting potential mistakes and frauds

during audits (Larimbi et al., 2017). In addition,

experienced senior auditors exhibited more

consistency between the selected relevant

information and the control risk assessment

response, selected fewer cues, and made judgments

in less time (Cahan and Sun, 2015). Other research

showed that the experience positively affected the

Auditor’s Professional Scepticism (Winantyadi and

Waluyo, 2014) (Anugerah, 2014). The study also

found that more experience reviewers more

accurately assess fraud risk (Agoglia et al., 2009).

However, in this study there is no significant

positive influence between experience and auditor’s

professional skepticism. The reason for that is

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

328

suspected because the majority of respondents'

experience is still low, about 10 to 20 assignments.

Thus, it can be said that when the level of auditor's

experience is low, then auditor's professional

scepticism is low and it can lead to failure in

detecting fraud.

For expertise variable, the coefficient of the

influence of expertise on auditor’s professional

skepticism is 0.360 showed in Table 1 with t-statistic

of 2.645 > 1.96 showed in Figure. 1. These results

conclude that there is a significant positive influence

between the expertise and auditor’s professional

skepticism. The first general standard of SA section

210 explains that an audit should be carried out by a

person with sufficient technical skills and training as

an auditor (Institut Akuntan Publik Indonesia, 2012).

The assumption of auditing expertise is that the

more knowledge auditors have, the more likely it is

that they hold a higher position, and also being

better at knowledge transfer due to experience will

mean that they make different (better) decisions than

someone with less knowledge (Rodgers et al., 2017).

In addition, the third general standard of SA section

230 states that in performing audit of the statement

preparations, the auditor has to use their professional

proficiency meticulously and thoroughly (Institut

Akuntan Publik Indonesia, 2012). Therefore, each

auditor is required to have professional skill and

expertise in performing their duties as an auditor.

The result in this study shows that the expertise

positively affects auditor’s professional scepticism.

This means that the higher the auditor's expertise,

will increase significantly (real) auditor professional

skepticism.

For audit situation variable, the coefficient of the

influence of audit situation on auditor’s professional

skepticism is 0.384 showed in Table 1 with t-statistic

of 3.675 > 1.96 showed in Figure. 1. These results

conclude that there is a significant positive influence

between audit situation and auditor’s professional

skepticism. In this case, an audit situation with high

risk (irregularities situation) will affect the auditor to

improve the attitude of Auditor’s Professional

Scepticism (Winantyadi and Waluyo, 2014). This

means that the higher the audit situation, will

increase significantly (real) auditor professional

skepticism.

For ethics variable, the coefficient of the

influence of ethics on auditor’s professional

skepticism is 0.307 showed in Table 1 with t-statistic

of 2.296 > 1.96 showed in Figure. 1. These results

conclude that there is a significant positive influence

between ethics and auditor’s professional

skepticism. In this case, the characteristics that can

describe professional scepticism possessed by an

auditor includes a questioning mind. A questioning

mind indicates that an auditor is sceptical in terms of

finding excuses, evidences, justifications, or proofs

(Hurtt, 2010). Professional ethics is required by the

auditor to maintain Auditor’s Professional

Scepticism attitude (Winantyadi and Waluyo, 2014).

This study shows that the auditor ethics affects

Auditor’s Professional Scepticism. This means that

the higher ethics, will increase significantly (real)

auditor professional skepticism.

For gender variable, the coefficient of the

influence of gender on auditor’s professional

skepticism is 0.045 showed in Table 1 with t-statistic

of 0.457 < 1.96 showed in Figure. 1. These results

conclude that there is no significant positive

influence between gender and auditor’s professional

skepticism. Generally, gender is the effect of social

definitions and internalizations of the meaning of

being a man or a woman (Haynes, 2013). In essence,

men and women have equal positions, both of which

are created in the same degree, self-worth, and

dignity. Characteristics of men and women can

influence how they deal with something (Larimbi et

al., 2017). Other study showed that the professional

scepticism of female management accountant is

higher than that of a male management accountant

(Charron and Lowe, 2008). In addition, study found

that the female auditors are more accurate in

performing complex assignments than the male ones

(Chung and Monroe, 2001). However, in this study

shows that there is no significant positive influence

between gender and auditor’s professional

skepticism. The reason for that is suspected because

the response answer of the respondents in Surabaya

both male or female auditors are the same. This

means that male and female auditors have the same

view on professional skepticism.

4 CONCLUSIONS

This study examined the factors that influence

auditor’s professional scepticism. The independent

variables used in this study are experience, expertise,

audit situation, ethics and gender whereas the

dependent variable is auditor’s professional

scepticism. In this study, the results showed that

expertise, audit situation, and ethics have positive

and significant influence on auditor’s professional

scepticism. While experience and gender do not

have a positive influence on auditor’s professional

scepticism. This study provide an explanation that in

order to improve the quality of audit, each auditor

should always improve the audit experience, audit

expertise, consider audit risks in certain audit

situations, ethical awareness, as well as improve

Factors that Influence Auditor’s Professional Skepticism - Evidence from Audit Firms in Surabaya

329

auditor’s professional scepticism for both male and

female auditors, in order to provide the right

opinion, because they will be useful to improve the

integrity and credibility of the public accountant

profession. This study has a number of limitations.

In this study, the method used is only the survey

method (i.g. spreading the questionnaire), without

conducting interviews. Therefore, the results

obtained only based on data collected through

written questionnaires. Further research is expected

to add data collection methods, such as interviews or

observations, to understand more about the actual

state of respondents. In addition, future research is

expected to not spread the research questionnaire at

the time the auditor is performing many audit tasks

that are usually done at the end of the year. It is

necessary to note in order to get more research

samples.

REFERENCES

Agoglia, C. P., Beaudoin, C., Tsakumis, G. T., 2009. The

effect of documentation structure and task-specific

experience on auditors' ability to identify control

weaknesses. Behavioral Research in Accounting,

21(1): p. 1-17.

AICPA, 2001. Analytical procedures. American Institute

of Certified Public Accountants.

Anisma, Y., Abidin, Z., 2012. Faktor Yang Mempengaruhi

Sikap Skeptisme Profesional Seorang Auditor Pada

Kantor Akuntan Publik di Sumatera. Pekbis (Jurnal

Pendidikan Ekonomi Dan Bisnis), 3(02).

Anugerah, R., Sari, R. N., Frostiana, R. M., 2014. The

Relationship Between Ethics, Expertise, Audit

Experience, Fraud Risk Assessment and Audit

Situational Factors On Auditor Professional

Scepticism Audit Experienxe.

Arrens, A., 2007. Auditing dan Pelayanan Verifikasi :

Pendekatan Terpadu, Tim Dejacarta. Jakarta.

AUASB, 2012. Professional Scepticism in an Audit of a

Financial Report. Australian Government AUASB

Bulletin, Australia.

Beasley, M. S., J. V. Carcello and D. R. Hermanson, 2001.

Top 10 audit deficiencies. Journal of Accountancy,

191(4): p. 63.

Brewster, B., 2015. An experimental examination of

delayed persuasion during analytical procedures: Are

auditors susceptible to the sleeper effect, Working

paper.

Cahan, S. F., Sun, J., 2015. The effect of audit experience

on audit fees and audit quality. Journal of Accounting,

Auditing & Finance, 30(1): p. 78-100.

Charron, K. F., Lowe, D. J., 2008. Skepticism and the

Management Accountant: Insights for Fraud

Detection, Management Accounting Quarterly, 9(2).

Chung, J., Monroe, G. S., 2001. A research note on the

effects of gender and task complexity on an audit

judgment. Behavioral Research in Accounting, 13(1):

p. 111-125.

Fullerton, R., Durtschi, C., 2005. The effect of professional

skepticism on the fraud detection skills of internal

auditors, Working Paper.

Glover, S. M., D. F. Prawitt, 2014. Enhancing auditor

professional skepticism: The professional skepticism

continuum. Current Issues in Auditing, 8(2): p. P1-

P10.

Harteis, C., Billett, S., 2013. Intuitive expertise: Theories

and empirical evidence. Educational Research Review

9 p. 145-157.

Haynes, K., 2013. Sexuality and sexual symbolism as

processes of gendered identity formation: An

autoethnography of an accounting firm. Accounting,

Auditing & Accountability Journal, 26(3): p. 374-398.

Hurtt, R. K., 2010. Development of a scale to measure

professional skepticism. Auditing: A Journal of

Practice & Theory, 29(1): p. 149-171.

Hurtt, R. K., 2013. Research on auditor professional

skepticism: Literature synthesis and opportunities for

future research. Auditing: A Journal of Practice &

Theory, 32 p. 45-97.

Institut Akuntan Publik Indonesia, 2012. Standar

Profesional Akuntan Publik, Salemba Empat. Jakarta.

Kushasyandita, R., Sabrina, S., Januarti, I., 2012.

Pengaruh Pengalaman, Keahlian, Situasi Audit, Etika

dan Gender Terhadap Ketepatan Pemberian Opini

Auditor Melalui Skeptisisme Profesional Auditor

(Studi Kasus Pada KAP Big Four di Jakarta).

Simposium Nasional Akuntansi, 15.

Larimbi, D., Subroto, B., Rosidi, R., 2017. Pengaruh

Faktor-Faktor Personal Terhadap Skeptisisme

Profesional Auditor. Ekuitas (Jurnal Ekonomi dan

Keuangan), 17(1): p. 89-107.

Mulyadi, M., 2011. Auditing, Salemba Empat. Jakarta,

Edisi Enam.

Rodgers, W., Mubako, G. N., Hall, L., 2017. Knowledge

management: The effect of knowledge transfer on

professional skepticism in audit engagement planning.

Computers in Human Behavior, 70: p. 564-574.

SPAP, 2011. Standar Profesional Akuntan Publik,

Salemba Empat. Jakarta.

Winantyadi, N., Waluyo, I., 2014. Pengaruh Pengalaman,

Keahlian, Situasi Audit, dan Etika terhadap

Skeptisisme Profesional Auditor (Studi Kasus pada

KAP di Provinsi Daerah Istimewa Yogyakarta),

Nominal: Barometer Riset Akuntansi dan Manajemen

3(1).

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

330