The Role of Account Representative in Securing the Tax Proceed

Harry Suharman, Evita Puspitasari, and Siti Khaeryyah

Accounting Department, Faculty of Economics And Business, Universitas Padjadjaran

evitapuspitagumilar@gmail.com

Keywords: Account Representative Competency, Account Representative Independency, Tax Proceed, Tax Regulation.

Abstract: The main objective of the research is to study the influence of account representative competency and

independency in stimulating the tax payer in fulfilling their tax obligation so that the tax proceed can be secure

enough. The study takes place at one of the tax office in Bandung. The target population involves 34 account

representatives that work in the tax office as the respondents have become the focus of this research. The data

have been collected by using questionnaires. After having the data being tabulated then it is analyzed by using

multiple regressions. The result indicates that simultaneously both the account representative competency and

independency influence in securing of tax proceed. However partially the account representative

independency itself cannot influence the tax proceed.

1 INTRODUCTION

The Directorate General of Taxation, after having

particular evaluation on tax administration system

implementation, seems there is a need to make

improvement in several aspects due to the tax realm.

Therefore, the first tax reformation has been

conducted in 2002. This tax reformation focus on

three aspects which includes: (a) modernization of tax

administration; (b) Tax policy reformation; (c) both

tax extensification and intensification. Moreover, the

second tax reform have been stated in 2009 which

concentrate on tax system. The objective of this

reform is not only to improve tax compliance by the

tax payer but also triggers good governance in tax

administration. According to the previous head of

Directorate General of Taxation, Mochamad (2009-

2011) in Directorate General of Taxes Ministry of

Finance of the Republic of Indonesia (2010) had

revealed that the second tax reform in line with the

tax strategy as described bellows:

(a) Continue reforming bureaucracy in

Directorate General of Taxation who has

entered the second stage;

(b) Provide incentive in particular group or

sector;

(c) Continue program mapping; and

(d) Implement law enforcement

The tax reforms are in no doubt and enable to

execute continually mapping program. One form of

reform in the field of taxation by the government is to

establish a modern tax office (Kantor Pelayanan

Pajak). The creation of modern tax office make

directorate general taxes always provide excellent

service to the taxpayer. To achieve excellent service,

the directorate general tax provide extra service by

forming Account Representative (AR) in every tax

modern office.

According to Purwono (2010) Account

Representatives serves as a bridge or mediator

between the taxpayer with the tax service office. An

account representative as it has been regulated by the

ministry of finance Republic of Indonesia

No.98/KMK/01/2006 which is then amended by the

regulation of finance minister No.79/PMK.01/2015

about account representative at the tax office. With

this regulation an account representative plays an

important role to cope with the second tax reforms’

strategy and secure the state budget revenue.

According to the above finance minister

regulation, an account representative in tax office are

the tax office employees itself that have been selected

and hired to supervised and provided consultation for

the taxpayer. Account representatives are trained to

be productive staff, to serve and have good tax

knowledge by getting education and training from

various sources. Therefore, the role of account

representative is expected to improve taxpayer

compliance and have implications for increasing state

revenues from the tax sector. This is in line with the

research that has been conducted before. Researchers

such as (Sandi, 2010) and (Wardani, 2011) pointed

out that the results of the survey showed that Account

Representative can improve taxpayer compliance

290

Suharman, H., Puspitasari, E. and Khaeryyah, S.

The Role of Account Representative in Securing the Tax Proceed.

In Proceedings of the 1st International Conference on Islamic Economics, Business, and Philanthropy (ICIEBP 2017) - Transforming Islamic Economy and Societies, pages 290-294

ISBN: 978-989-758-315-5

Copyright © 2018 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

Similarly, with quantitative approach from the results

of their studies argued that the competence factor

service, service credibility and compliance control

material significantly influence taxpayer compliance

in KPP Pratama. Further Boihaqi, Kumadji and

Suhari (2015) reinforce the role of AR. The findings

of his research states that counseling, consultation

and supervision significantly influence corporate

taxpayers. Even supervisory variable is the dominant

variable in influencing taxpayer compliance in KPP

Madya Malang. Recently, (Farikha & Praptoyo,

2016) conducted a case study with a qualitative

approach. The findings also strengthen the opinion of

the researchers above by stating that the reporting rate

of tax returns increases each year which proves that

the awareness of taxpayers is increasing so that the

role of account representative as counseling,

consultation and supervisor in providing socialization

taxation more effective.

Despite several studies relating to the role of an

account representative claimed to have contributed to

the taxpayer's compliance rate both in calculating tax

liabilities and reporting in the form of tax returns and

then paying the tax payable to the state treasury. The

author is interested to study more about several

factors related to the competence and independence

of account representative.

2 LITERATURE REVIEW

2.1 Accounts Representatives

Account representative has the duty to perform the

function of counseling, consultation and supervision.

Based on the regulation of the Minister of Finance

No. 79 / PMK / .01 / 2015 on Account Representative

at the Tax Office, It function has been separated into

two functions. The two functions include:

(a) Account Representative that performs tax

service and consulting functions.

(b) Account Representative that performs

supervisory function and excavates taxpayer

potential.

According to Purnomo (2015) Account

Representative who is in the Section of Supervision

and Consultation globally has a task and work that

can generally be divided into three types,namely:

(a) As an authorized consultant appointed by

DGT which is free of charge (free) is

provided to the Taxpayer in order to obtain

information and simultaneously consultation

related tax issues.

(b) Administration / Clerical Work related to

formal service to Taxpayers' application,

detailed in the Standard Operation and

Procedure of Settlement of Application

(SOP-AR). (c) Security of Tax Receipts,

either, through supervision and potential

excavation.

(c) Such strategic and tasks mandated by the

DGT to Account Representative show that

the DGT gives such great trust to Account

Representative in carrying out the vision and

mission of the DGT. But the reality in the

Community Account Representative itself,

not all of one voice related belief given the

DGT. Trust given DGT to Account

Representative in the form of tasks and such

a strategic job for the achievement of

organizational goals should be able to give

positive contribution in the form of pride of

the trust. The pride derived from such

positive thoughts will generate positive

attitudes as well and eventually any work

that is mandated can be accomplished very

well.

2.2 Account Representative Competency

As has been known that the competence of a person

will be influenced and determined by the level of

knowledge and skill level. Both factors can be

realized through the achievement of formal and

informal education level. In addition, relevant work

experience will also contribute to the improvement of

skills and knowledge in a more professional direction.

According to (Meija, Balkin, & Caldi, 2010)

competence is a characteristic inherent in someone

who is associated with success.

Fulfillment of the requirements imposed on an

account representative results in a competent account

representative officer. Competence will give hope for

improvement of service function and consultation of

taxpayer. Mastery of good tax regulation will provide

convenience to study the objective conditions of

taxpayer business activities in order to obtain

information or provide consultative tax-related

issues. This consultative activity is expected to

stimulate the taxpayer compliance level in relation to

its obligation to perform the payment of tax payable

to the state.

Based on the above explanation, competence will

give hope for improvement of service function and

consultation of taxpayer. Mastery of good tax

regulation will provide convenience to study the

objective conditions of taxpayer business activities in

order to obtain information or provide consultative

tax-related issues.

The Role of Account Representative in Securing the Tax Proceed

291

Furthermore, the safeguarding of tax revenue can

even be increased through the supervision and

exploration of potential taxes. Based on the above

explanation, then the hypothesis that requires

verification is as follows:

H1: Account Representative Competence affects the

security of tax revenue proceed.

2.3 Account Representative

Independency

From the audit point of view, Arrens et al. (2012) as

an experts argues that independence is an unbiased

view of performing in auditing, evaluation of the

results of the examination or testing, and report the

results of audit findings. This impartial attitude can be

shaped in two perspectives:

(a) Independence in the mental attitude

(independence in fact) which means the

accountant can maintain an impartial attitude

in carrying out the examination of the

financial statements;

(b) Independence in appearance (independent in

appearance) which means the accountant to

be impartial according to the perceptions of

users of financial statements.

This is also reinforced by the second common

standard of SA Section 220 (SPAP 2011) which

suggests that in all respects related to engagement,

independence in the mental attitude must be

maintained by the auditor. Likewise, the standard of

tax audit which has been regulated by the Director

General of Tax Regulation No. PER-23 / PJ / 2013

dated June 11, 2013 provides guidance that the

examiner should be independent, that is not easily

influenced by the circumstances, conditions, deeds

and / or taxpayers examined. Therefore, based on

these requirements then the propose hypothesis:

H2: The independency of account representative may

affect the security of tax revenue proceed.

2.4 Securing the Tax Proceed

As has been pointed out that the reform of the

structure and organization of the Directorate General

of Taxes solely is to be able to increase tax revenue.

Therefore, the existence of competent and

independent account representative Who are

competent and independent have the duty to carry out

supervision of taxpayer compliance obligations,

guidance / appeal to taxpayer and technical

consultation taxation, compilation of taxpayer

profile, reconciliation of taxpayer data in the

framework of intensification and evaluate the result

of appeal based on applicable provisions (Purnomo,

2015). Furthermore, the challenge of tax revenue can

basically be divided into 2 (two) sectors, which are:

(a) Routine acceptance challenges and;

(b) Challenges of extra-effort acceptance.

The Challenges of routine acceptance can be

made with supervision over:

(a) Comparison of tax payments per tax period

(apple to apple comparison);

(b) Business plan and project data from

taxpayer;

(c) DIPA Data (List of Budget Usage) of central

and regional treasurer.

2.5 The Challenge extra effort

This challenge occurs in the light of there is a gap

between tax revenue estimation and the target set by

the tax office. Therefore, the challenge of exploring

the potential for increasing tax revenues through extra

effort can be grouped as follows:

(a) Challenge taxpayers of certain entrepreneurs

(WP OPPT) and WP PP 46 of 2012.

(b) Taxpayer Challenges with IDLP

(Information, Data, Reports and

Complaints).

(c) The Taxpayer Challenge does not report SPP

Tahunan PPh Badan.

(d) Non-PKP Taxpayer Challenge.

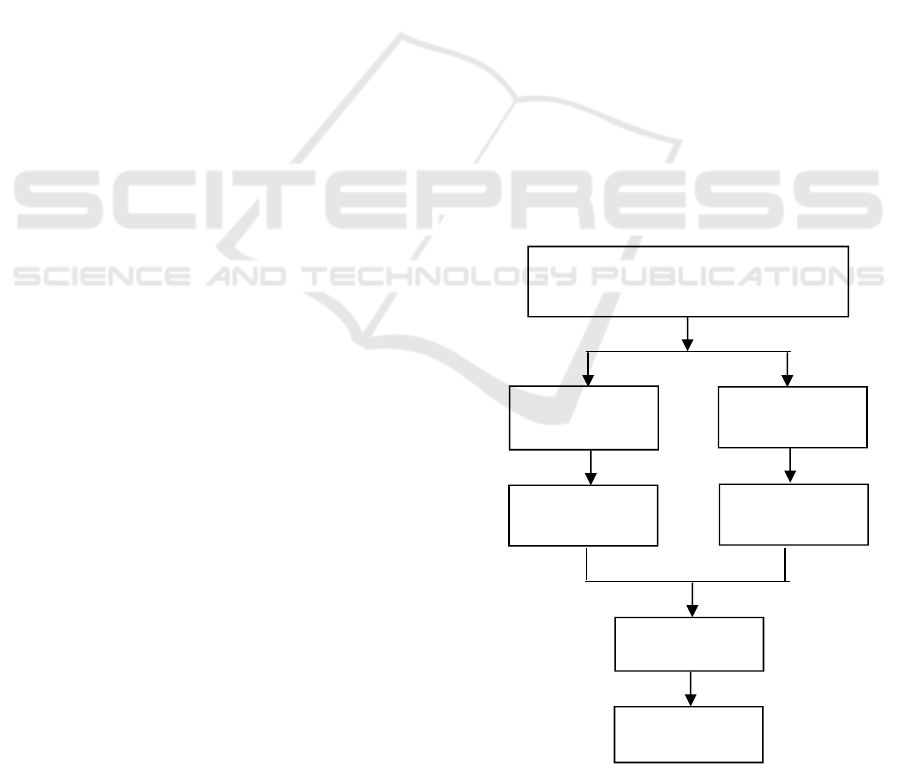

Figure 1: Caption of research model.

Account

Reprensentative

Competency

Account Representative Competency and

Independency Affect Securing of Tax

Proceed

Account

Representative

Independency

Creative, Innovative

Mastering Tax

regulation

Integrity, Fairness,

Commitment, and

Synergize

Improve Tax

Potential

Securing Tax

Proceed

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

292

3 METHODS

3.1 Empirical Design

This research seeks to obtain empirical data that

provides an overview and can explain the

presuppositions that require answers and have been

specified in the form of hypotheses. These

respondents include Account Representative in

Kantor Pelayanan Pajak (KPP) Madya Bandung.

There are 34 people account representative who are

in the working area of KPP Madya Bandung. Thus the

samples used by the researchers fall into the census

category.

Data collection techniques were conducted by

field research (Field Research). Besides that also

made an instrument which hopefully will give answer

to primary data needed. Instruments used to obtain

empirical data in form of questionnaire. The design of

questionnaires consisting of questions that indicate

the variables studied have been arranged

systematically that will facilitate for researchers in the

tabulation and processing of empirical data.

4 RESULTS AND DISCUSSION

Before testing the classical assumption and

hypothesis testing, first it requires to test the validity

of data and reliability data. This test is necessary

because the type of research data is the primary data.

4.1 Simultaneously Hypothesis Test

Summary of hypothesis testing results show that from

Table 1 ANOVA can be known research model on the

variables studied can be accepted. This can be seen

from the value of F arithmetic 7.045 with a

significance level of 0.03 is smaller than 0.05. The

value of F arithmetic shows the goodness of fit for the

propose research model.

Table 1: F-Test result.

Model

F

Sig.

1

Regression

7.045

.003

b

Therefore, according to the F test results it can be

stated that the result of the regression model shows

that there is significant influence of Representative

Account Competence, Independence of Account

Representative simultaneously on Security of Tax

Proceed at KPP Madya Bandung. However if the

study focus on the extent of independent variable

(Representative Account Competence, Independence

of Account Representative) that influence on Security

of Tax Proceed is 31% (see Table 2). . The value of R

2

is between zero and one. The value of R

2

is between

zero and one. A small R

2

value means the ability of

independent variables to explain the variation of a

dependent variable is very limited. A value close to

one means the independent variables provide almost

all the information needed to predict the variation of

the dependent variable.

The two independent variables are not good

enough to predict and explain in order to improve the

security of tax proceed. It requires further study and

analysis of certain variables which may give rise to fit

the study, especially in trying to increase potential tax

income.

Table 2: Determinant Coefficient

Model

R

R Square

Adjusted R Square

1

.559a

.312

.268

If independent variable more than one, then it are

better to see the ability of variable predict the

dependent variable, the value used is adjusted value

R

2

that is 32%. In other words 32% change in tax

revenue can be explain by variable Account

Representative competence, Independence Account

Representative of 68% explained by other factors not

included in this study model.

4.2 Test partial hypothesis

Based on the data in Table 3 above can be assessed

that t arithmetic for Account Representative

Competence is equal to 3.688 with significance of

0.001 count and for Independence Account

Representative of -0.312 with significance 0.757,

respectively. Thus from these results of data testing,

it can be stated that the independent variable has no

significant effect on the Security of Tax Proceed,

while the competence variable has a significant

influence on Tax Proceed Security.

Table 3. T-test Hypothesis.

Unstandardized Coefficients

Standardized Coefficients

t

Sig.

B

Std. Error

Beta

(Constant)

12.531

2.386

1.328

0.194

independency

-.0.15

0.115

-0.048

-0.312

0.757

competency

0.111

0.098

0.57

3.688

0.001

The Role of Account Representative in Securing the Tax Proceed

293

The results of this study show that partially

Representative Account Competence significantly

influences the Security of Tax Proceed. Based on

these results note that the competence in this expertise

obtained from education and training can encourage

tax revenue through Account Representative

Expertise in conducting tax audits professionally. The

success of Account Representative in performing its

function is done through competence; the competence

of an Account Representative is measured by its

ability to execute and mastery of good tax regulation.

It is expected that one may provide convenience to

study the objective conditions of taxpayer business

activities.

The main objective of these activities is to obtain

information or provide consultative tax-related

issues. By doing this it may stimulate the taxpayer

compliance level in relation to its obligation to

perform the payment of tax payable to the state.

5 CONCLUSION

Simultaneously the competency of account

representative and account representative

independence can influence the increase of security

of tax proceed although relatively low. The security

of tax proceed can be increased in terms of revenues

when examining beyond the two variables that have

been studied in this matter. Similarly, if viewed

partially the variable independency account

representative is not sufficient enough to be able to

stimulate the taxpayer in carrying out its tax

obligations.

Considering that this research involves only the

tax authorities, it is necessary to include the taxpayer

in the study of the variables that have been studied.

To be able to obtain a sound review of the results

related to the factors that can increase the potential

improvement in tax revenue following the security it

is advisable to add other variables beyond the

competence and independency account

representative. With the studying addition of

variables are expected to explain securing of tax

proceed better.

REFERENCES

Arens et. al. 2012. Auditing and Assurance Services: An

Intregrated Approach. Fourteen Edition : Prentice Hall.

Boihaqi, I., Kumadji, S., Suhari, M. 2015. Pengaruh Fungsi

Account Representative Terhadap Kepatuhan. Jurnal

Administrasi Bisnis=Perpajakan (JAB) Vol.5 No.2.

Directorate General of Taxes Ministry of Finance of the

Republic of Indonesia. 2010. Annual Report

Farikha, I., Praptoyo, I. 2016. Sosialisasi Peraturan

Perpajakan dan Kinerja Account Representative Kaitan

Dengan Kepatuhan Wajib Pajak. Jurnal Ilmu dan Riset

Akuntansi. Vol.5, No.3, Maret.

Meija, K. G., Balkin, D. B., Caldi, R. L. 2010. Managing

Human Resources. Sixth Edition. Canada: Pearson

Education.

Purnomo, J. 2015, May Tuesday. Retrieved June Sunday,

2017, from www.bppk.kemenkeu.go.id.

Purwono, H. 2010. Dasar-Dasar Perpajakan dan

Akuntansi Pajak. Jakarta: Erlangga.

Sandi, B. N. 2010. Analisis Pengaruh Pelayanan,

Pengawasan, dan Konsultasi Account Representative

terhadap Kepatuhan Wajib Pajak. Jakarta: Fakultas

Ekonomi dan Bisnis Universitas Negeri Sysrif

Hidayatullah.

Wardani, E. S. 2011. Pengaruh Kualitas Pelayanan dan

Efektivitas Pengawasan Account Representative

terhadap Kepatuhan Formal Wajib Pajak. Surabaya:

Fakultas Ekonomi dan Bisnis Universitas Airlangga.

ICIEBP 2017 - 1st International Conference on Islamic Economics, Business and Philanthropy

294