A SERVICE FRAMEWORK FOR LEARNING, QUERYING

AND MONITORING MULTIVARIATE TIME SERIES

Chun-Kit Ngan, Alexander Brodsky and Jessica Lin

Department of Computer Science, George Mason University

4400 University Drive MSN 4A5, Fairfax, Virginia 22030-4422, U.S.A.

Keywords: Service Framework, Multivariate Time Series, Parameter Learning, Decision Support.

Abstract: We propose a service framework for Multivariate Time Series Analytics (MTSA) that supports model

definition, querying, parameter learning, model evaluation, monitoring, and decision recommendation. Our

approach combines the strengths of both domain-knowledge-based and formal-learning-based approaches

for maximizing utility over time series. More specifically, we identify multivariate time series parametric

estimation problems, in which the objective function is dependent on the time points from which the

parameters are learned. We propose an algorithm that guarantees to find the optimal time point(s), and we

show that our approach produces results that are superior to those of the domain-knowledge-based approach

and the logit regression model. We also develop MTSA data model and query language for the services of

parameter learning, querying, and monitoring.

1 INTRODUCTION

Making decisions over multivariate time series is an

important topic which has gained significant interest

in the past decade, as two or more time series are

often observed simultaneously in many fields. In

business and economics, financial analysts and

researchers monitor daily stock prices, weekly

interest rates, and monthly price indices to analyze

different states of stock markets. In medical studies,

physicians and scientists measure patients’ diastolic

and systolic blood pressure over time and

electrocardiogram tracings to evaluate the patients’

health of respiratory systems. In social sciences,

sociologists and demographers study annual birth

rates, mortality rates, accident rates, and various

crime rates to dig out hidden social problems within

a community. The purpose of these measures over

multivariate time series is to assist the specialists in

understanding the same problem in different

perspectives within particular domains. For those

significant events to be identified and detected over

multivariate time series, the events can lead the

professionals to make better decisions and take more

reasonable actions promptly. Those events may

include index bottoms and tops in financial markets,

irregular readings on blood pressure and pulse

anomalies on electrocardiogram, as well as low birth

but high death rates in a population region. To

support such decision-marking and determination

over multivariate time series, we propose a service

framework, Multivariate Time Series Analytics

(MTSA), which consists of services for model

definition, querying, parameter learning, model

evaluation, monitoring, and decision

recommendation. Our technical focus of this work is

on the problem of event detection; namely, the

parameter learning, data monitoring, and decision

recommendation services.

Currently, existing approaches to identifying and

detecting those interesting events can be roughly

divided into two categories: domain-knowledge-

based and formal-learning-based. The former relies

solely on domain expert knowledge. Based on their

knowledge and experiences, domain experts

determine the conditions that trigger the events of

interest. Consider one particular example of the

timely event detection of certain conditions in the

stock market, e.g., the bear market bottom, that can

provide investors a valuable insight into the best

investment opportunity. Such identification and

detection can aid in the task of decision-making and

the determination of action plans. To assist users in

making better decisions and determinations, domain

experts have identified a set of financial indices that

92

Ngan C., Brodsky A. and Lin J..

A SERVICE FRAMEWORK FOR LEARNING, QUERYING AND MONITORING MULTIVARIATE TIME SERIES .

DOI: 10.5220/0003495800920101

In Proceedings of the 13th International Conference on Enterprise Information Systems (ICEIS-2011), pages 92-101

ISBN: 978-989-8425-54-6

Copyright

c

2011 SCITEPRESS (Science and Technology Publications, Lda.)

can be used to determine a bear market bottom or

the “best buy” opportunity. The indices include the

S&P 500 percentage decline (SPD), Coppock Guide

(CG), Consumer Confidence point drop (CCD), ISM

Manufacturing Survey (ISM), and Negative

Leadership Composite “Distribution” (NLCD). If

these indices satisfy the pre-defined, parameterized

conditions, e.g., SPD < -20%, CG < 0, etc., (Stack,

2009), it signals that the best period for the investors

to buy the stocks is approaching. Often these

parameters may reflect some realities since they are

set by the domain experts based on their past

experiences, observations, intuitions, and domain

knowledge. However, they are not always accurate.

In addition, the parameters are static, but the

problem that we deal with is often dynamic in

nature. The market is constantly impacted by many

unknown and uncontrollable factors from the

business surroundings. Thus, this approach lacks a

formal mathematical computation that dynamically

learns the parameters to meet the needs of the

changing environment.

An alternative approach is to utilize formal

learning methods such as non-linear logit regression

models. (Dougherty, 2010) The logit regression

models are used to predict the occurrence of an

event (0 or 1) by learning parametric coefficients of

the logistic distribution function of the explanatory

variables. This is done based on the historical data

by applying nonlinear regression models and

Maximum Likelihood Estimation (MLE). The main

challenge concerning using formal learning methods

to support decision-making is that they do not

always produce satisfactory results, as they do not

consider incorporating domain knowledge into their

formal learning aproaches. Without domain experts’

knoweledge, formal learning methods become

computationally intensive and time consuming. The

whole model building is an iterative and interactive

process, including model formulation, parameter

estimation, and model evaluation. Despite enormous

improvements in computer software in recent years,

fitting such nonlinear quantitative decision model is

not a trival task, especially if the parameter learning

process involves multiple explanatory variables, i.e.,

high dimensionality. Working with high-

dimensional data creates difficult challenges, a

phenomenon known as the “curse of

dimensionality.” Specifically, the amount of

observations required in order to obtain good

estimates increases exponentially with the increase

of dimensionality. In addition, many learning

algorithms do not scale well on high dimensional

data due to the high computational cost. The

parameter computations by formal-learning-based

approaches, e.g., logit regression model, are

complicated and costly, and they lack the

consideration of integrating experts’ domain

knowledge into the learning process – a step that

could potentially reduce the dimensionality. Clearly,

both approaches, domain-knowledge-based and

formal-learning-based, do not take advantage of

each other to learn the optimal decision parameters,

which are then used to monitor the events and make

better recommendations.

To mitigate the shortcomings of the existing

approaches, the proposed MTSA service framework

combines the strengths of both the domain-

knowledge-based and the formal-learning-based

approaches. The service framework supports quick

implementation of services towards decision

recommendation over multivariate time series. More

specifically, the MTSA Model Definition Service

takes the template of conditions identified by

domain experts—such template consists of

inequalities of values in the time sequences—and the

Learning Service “parameterizes” it, e.g., SPD < p

1

.

The goal of the learning service is to efficiently learn

parameters that maximize the objective function,

e.g., earnings in our financial example. The

Monitoring and Recommendation Service

continuously monitors the data stream for data that

satisfy the parameterized conditions, in which the

parameters have been instantiated by the learning

service. We also propose an extension of the

relational database model and SQL, with high-level

MTSA constructs to support querying, monitoring,

and parameter learning.

To this end, we identify multivariate time series

parametric estimation problems, in which the

objective function is dependent on the time points

from which the parameters are learned. With the

potentially large data size and multiple variables,

classic branch-and-bound approaches have

exponential complexity in the worst-case scenario.

We develop a new algorithm that guarantees a true

optimal time point, with complexity of O(kNlogN),

where N is the size of the learning data set, and k is

the number of parametric time series. To

demonstrate the effectiveness and the efficiency of

our algorithm, we compare our method with the

domain-knowledge-based approach and the logit

regression model. As a proof of concept, we conduct

an experiment in the financial domain, but note that

our framework is applicable to solve problems in

different domains. We show that our algorithm is

more effective and produces results that are superior

to those of the two approaches mentioned above.

More specifically, in our experiments we show that

our algorithm outperforms the financial experts’

recommendation and the logit regression model,

A SERVICE FRAMEWORK FOR LEARNING, QUERYING AND MONITORING MULTIVARIATE TIME SERIES

93

resulting in higher earnings for our imaginary

investor.

The rest of the paper is organized as follows. In

Section 2 we provide an overview on the MTSA

service framework. We discuss the learning and

monitoring services, by defining the Expert Query

Parametric Estimation (EQPE) model in Section 3.

Section 4 explains the domain-knowledge-inspired

learning algorithm and shows the experimental

evaluation on stock market data. In Section 5, we

describe the MTSA data model and query language.

Section 6 contains the conclusions and future work.

2 A SERVICE FRAMEWORK

FOR MULTIVARIATE TIME

SERIES ANALYTICS (MTSA)

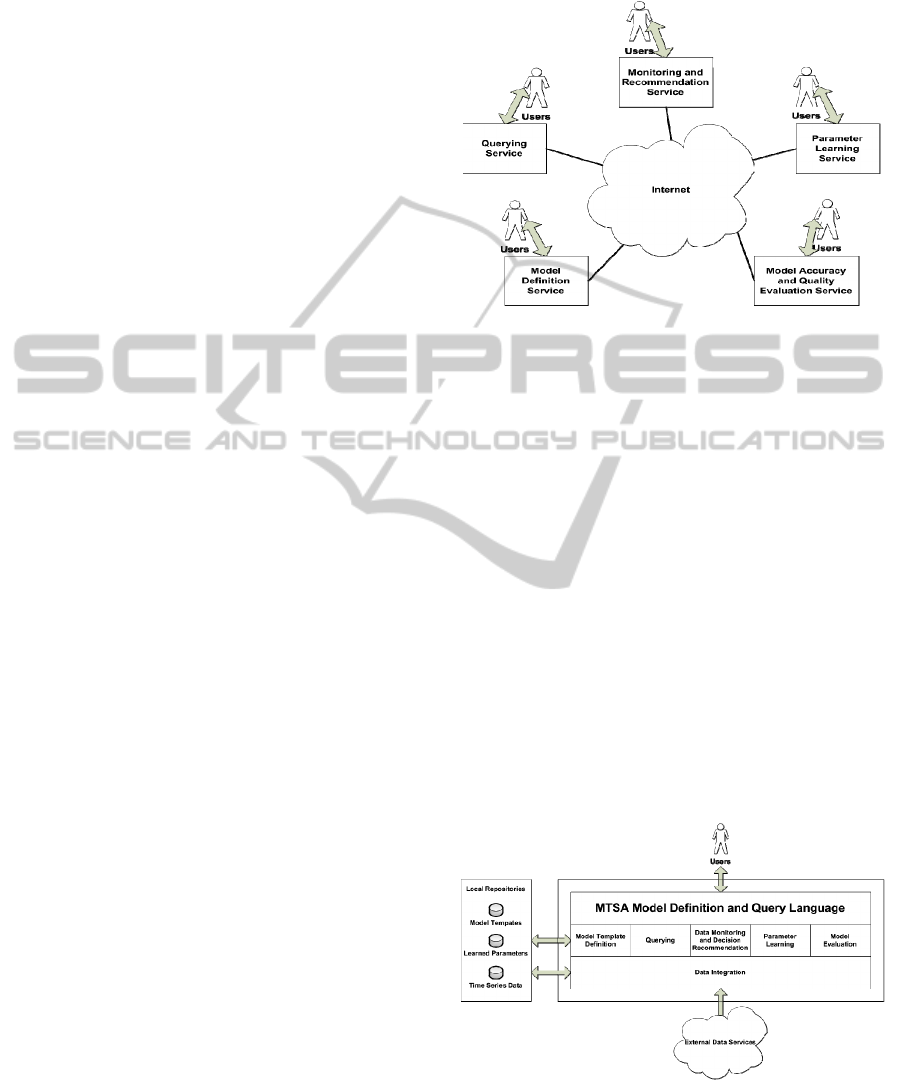

Figure 1 shows a range of common services that is

desirable to be offered over the internet. The MTSA

Model Definition Service provides a parametric

model template identified by the domain experts. In

the financial example that predicts the market

bottom, the model template may consist of indices

such as S&P 500 percentage decline (SPD),

Coppock Guide (CG), etc. These indices are

associated with their respective inequality

constraints, for example, SPD < p

1

, and CG < p

2

.

Given such a parametric model template in a given

domain, the Monitoring and Recommendation

Service continuously screens the incoming data

stream for indices that satisfy all the constraints

which specify when the event of interest, e.g., the

market bottom, has occurred, and recommends an

action, e.g., buying stock. Note that in the traditional

approach, the decision parameters p

1

and p

2

are

specified by the domain experts, e.g., SPD < -20%,

and CG < 0. However, using hard-set parameters

cannot capture the dynamics of the rapidly changing

market. The Parameter Learning Service

parameterizes the template, e.g., SPD < p

1

and CG <

p

2

, and supports learning of the parameters from the

historic time series. The accuracy of the decision

parameters are ensured through the Model Accuracy

and Quality Evaluation Service, which validates the

prediction, i.e., market bottom, with the observed

real data, and updates the model if necessary. The

Querying Service allows the service developers and

database programmers to express the complex

information services over multivariate time series

mentioned above in a high-level abstraction.

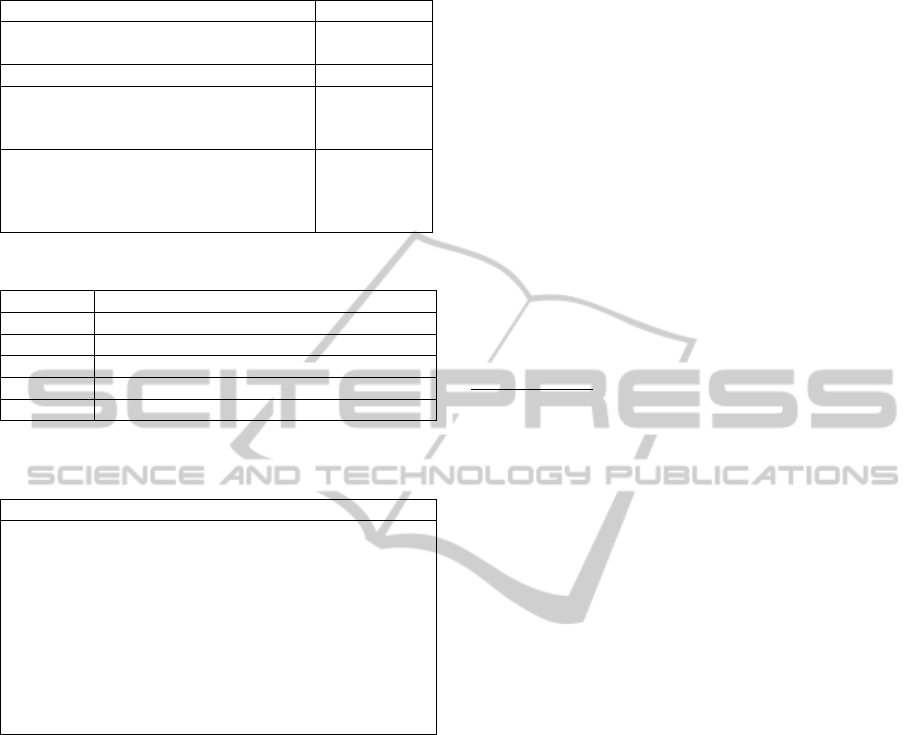

The service framework for multivariate time

series analytics (MTSA) provides a medium that

supports quick implementation of the services

described above. The MTSA service framework is

illustrated in Figure 2.

Figure 1: Services for Multivariate Time Series Over

Internet.

It consists of three layers: data integration,

information processing, and query language. The top

layer is the MTSA Model Definition and Query

Language, which extends the relational model with

time series and SQL with MTSA constructs. The

middle layer supports the MTSA constructs

including MTSA model template definition,

querying, parameter learning, model evaluation, data

monitoring, and decision recommendation. The

bottom, Data Integration Layer, allows service

providers to interact with external data services and

collect time series data from heterogeneous sources,

as well as from local repositories. This integration

layer provides a concentric view of the collected

data. The integration of the model template and the

learned parameters, which may be available both

locally and through external services, is also

supported by the Data Integration Layer.

Figure 2: A Service Framework for Multivariate Time

Series Analytics.

ICEIS 2011 - 13th International Conference on Enterprise Information Systems

94

3 EXPERT QUERY

PARAMETRIC ESTIMATION

(EQPE) MODEL

In this section, we discuss in detail the

methodologies used in the Parameter Learning

Service and the Monitoring and Recommendation

Service in the MTSA framework. More specifically,

we review the mathematical formulations of the

Expert Query Parametric Estimation (EQPE)

problem and solution. We also use the examples to

explain them in detail.

The goal of an EQPE problem is to find optimal

values of decision parameters that maximize an

objective function over historical, multivariate time

series. For an EQPE problem being constructed, we

need to define a set of mathematical notations and a

model for it. We assume that the time domain T is

represented by a set of natural numbers: T = N, and

that we are also given a vector of n real-valued

parameter variables (p

1

, p

2

, …, p

n

).

Definition 1. Time Series: A time series S is a

function S: T → R, where T is the time domain, and

R is the set of real numbers.

Definition 2. Parametric Monitoring Constraint: A

parametric monitoring constraint C(S

1

(t), S

2

(t), …,

S

k

(t), p

1

, p

2

, …, p

n

) is a symbolic expression in terms

of S

1

(t), S

2

(t), …, S

k

(t), p

1

, p

2

, …, p

n

, where S

1

(t),

S

2

(t), …, S

k

(t) are time series, t ∈ T is a time point,

and (p

1

, p

2

, …, p

n

) is a vector of parameters.

We assume a constraint C written in a language

that has the truth-value interpretation I: R

k

x R

n

→

{True, False}, i.e., I(C(S

1

(t), S

2

(t), …, S

k

(t), p

1

, p

2

,

…, p

n

)) = True if and only if the constraint C is

satisfied at the time point t ∈ T and with the

parameters (p

1

, p

2

, …, p

n

) ∈ R

n

. In this paper, we

focus on conjunctions of inequality constraints:

C(S

1

(t), S

2

(t), …, S

k

(t), p

1

, p

2

, …, p

n

) = ∧

i

(S

i

(t) op

p

j

), where op ∈ {<, ≤, =, ≥, >}.

Definition 3. Time Utility Function: A time utility

function U is a function U: T → R.

Definition 4. Objective Function: Given a time

utility function U: T → R and a parametric

constraint C, an objective function O is a function O:

R

n

→ R, which maps a vector of n parameters on R

n

to a real value R, defined as follows. For (p

1

, p

2

, …,

p

n

) ∈ R

n

, O(p

1

, p

2

, …, p

n

) ≝ U(t), where U is the

utility function, and t ∈ T is the earliest time point

that satisfies C, i.e.,

(1) S

1

(t) op

1

p

1

∧ S

2

(t) op

2

p

2

∧ … ∧ S

n

(t) op

n

p

n

is satisfied, and

(2) There does not exist 0 ≤ t' < t, such that S

1

(t')

op

1

p

1

∧ S

2

(t') op

2

p

2

∧ … ∧ S

n

(t') op

n

p

n

is satisfied.

Definition 5. Expert Query Parametric Estimation

(EQPE) Problem: An EQPE problem is a tuple <S,

P, C, U>, where S = {S

1

, S

2

, …, S

k

} is a set of k time

series, P = {p

1

, p

2

, …, p

n

} is a set of n real-value

parameter variables, C is a parametric constraint in S

and P, and U is a time utility function.

Intuitively, a solution to an EQPE problem is an

instantiation of values into the vector P of n real-

value parameters that maximizes the objective O.

Definition 6. Expert Query Parametric Estimation

(EQPE) Solution: A solution to the EQPE problem

<S, P, C, U> is argmax O(p

1

, p

2

, …, p

n

), i.e., the

(estimated) values of parameters, p

1

, p

2

, …, p

n

, that

maximize O, where O is the objective function

corresponding to U.

The base time series in our financial example are

shown in Table 1. We suppose that the first starting

date in any time-series data set is t = 0. Note that

some base time series are the direct inputs, whereas

some are used to derive another set of time series.

For instance, the derived time series in our case

study are shown in Table 2. The decision parameters

used in the case study are defined in Table 3. Let us

consider the following constraint C as an

illustration:

C(SPD(t), CG(t), CCD(t), ISM(t), NLCD(t), p

1

,

p

2

, p

3

, p

4

, p

5

) = SPD(t) < p

1

∧ CG(t) < p

2

∧

CCD(t) < p

3

∧ ISM(t) < p

4

∧ NLCD(t) > p

5

It means that the parametric monitoring

constraint C is satisfied, i.e., its interpretation is

True, if the above inequalities with the decision

parameters are satisfied at the time point t. The

interpretation also indicates that the monitoring

event occurs. We assume that the investor buys the

S&P 500 index fund at the decision variable time t

and sell it at the given t

S

, which is the last day of the

given training data set. The earning function SP(t

S

)/

SP(t) – 1 ∈ R is the utility, which is maximized by

choosing the optimal value t ∈ T, where SP(t

S

) and

SP(t) are the sell and buy value of the S&P 500

index fund at the time t

S

and t respectively. The

EQPE problem and solution for our example can be

constructed by putting the considered time series,

parameters, constraints, and functions to the

definitions shown in Table 4.

Table 1: Base Time-Series Data.

Base Time Series S Abbreviation

S&P 500 SP500(t)

Coppock Guide CG(t)

Consumer Confidence CC(t)

ISM Manufacturing Survey ISM(t)

Negative Leadership Composite NLC(t)

A SERVICE FRAMEWORK FOR LEARNING, QUERYING AND MONITORING MULTIVARIATE TIME SERIES

95

Table 2: Derived Time-Series Data.

Derived Time Series S Abbreviation

Percentage decline in SP(t) at the time

point t

SPD(t)

Points drop in CC(t) at the time point t CCD(t)

Number of consecutive days in Bear

Market “DISTRIBUTIOIN” of NLC(t)

at and before the time point t

NLCD(t)

Time Utility Earning at the time point t,

i.e., the index fund is bought at t and

sold at t

s

, where t

s

is the last day of the

learning data set

Earning(t)

Table 3: Decision Parameters.

Parameter Interpretation

p

1

Test if SPD(t) is less than p

1

at t.

p

2

Test if CG(t) is less than p

2

at t.

p

3

Test if CCD(t) is less than p

3

at t.

p

4

Test if ISM(t) is less than p

4

at t.

p

5

Test if NLCD(t) is greater than p

5

at t.

Table 4: EQPE Problem and Solution Formulation for

S&P 500 Index Fund.

Problem and Solution

Problem:

<S, P, C, U>, where

S = {SPD, CG, CCD, ISM, NLCD}

P = {p

1

, p

2

, p

3

, p

4

, p

5

}

C = SPD(t) < p

1

∧ CG(t) < p

2

∧ CCD(t) < p

3

∧

ISM(t) < p

4

∧ NLCD(t) > p

5

U = SP(t

s

)/SP(t) - 1

Solution:

argmax O(p

1

, p

2

, p

3

, p

4

, p

5

) ≝ U(t)

The values of the optimal decision parameters

can be determined by using the learning algorithm,

Checkpoint. Before explaining the Checkpoint

algorithm in detail, we first review the concept of

Dominance.

Definition 7. Dominance ≻: Given an EQPE

problem <S, P, C, U> and any two time points t, t' ∈

T, we say that t' dominates t, denoted by t' ≻ t, if the

following conditions are satisfied:

(1) 0 ≤ t' < t, and

(2) ∀(p

1

, p

2

, …, p

n

) ∈ R

n

, C(S

1

(t), S

2

(t), …, S

k

(t),

p

1

, p

2

, …, p

n

) → C(S

1

(t'), S

2

(t'), …, S

k

(t'), p

1

, p

2

, …,

p

n

).

Intuitively, t' dominates t if for any selection of

parametric values, the query constraint satisfaction

at t implies the satisfaction at t'. Clearly, the

dominated time points should be discarded when the

optimal time point is being determined. We formally

claim that:

Claim 1 - Given the conjunctions of inequality

constraints, S

1

(t) op

1

p

1

∧ S

2

(t) op

2

p

2

∧ … ∧ S

k

(t) op

k

p

k

and the two time points t', t such that 0 ≤ t' < t, t'

≻ t if and only if S

1

(t') op

1

S

1

(t) ∧ S

2

(t') op

2

S

2

(t) ∧ …

∧ S

k

(t') op

k

S

k

(t). The proof is shown in Appendix.

For example, suppose there are three time series

S

1

, S

2

, S

3

and three decision parameters p

1

, p

2

, p

3

.

And the constraints are C(S

1

(t), S

2

(t), S

3

(t), p

1,

p

2

, p

3

)

= S

1

(t) ≥ p

1

∧ S

2

(t) ≥ p

2

∧ S

3

(t) ≤ p

3

. Also assume the

values for S

1

, S

2

, and S

3

at the time point t

1

, t

2

, and t

3

respectively in Table 5 shown in the next page.

In this case, the time point t

3

is dominated

because there is a time point t

1

that make the

inequality, S

1

(t

1

) ≥ S

1

(t

3

)

∧ S

2

(t

1

) ≥ S

2

(t

3

)

∧ S

3

(t

1

) ≤

S

3

(t

3

), equal to true.

On the contrary, for all t' < t, if S

1

(t') ¬op

1

S

1

(t)

∨

S

2

(t') ¬op

2

S

2

(t)

∨…∨ S

n

(t') ¬op

n

S

n

(t) is satisfied, t is

not dominated

by t' denoted by t' ⊁ t. Let us

consider the same example above. Because S

1

(t

1

) <

S

1

(t

2

) ∨ S

3

(t

1

) > S

3

(t

2

), t

2

is not dominated.

4 CHECKPOINT ALGORITHM

AND EXPERIMENTAL

EVALUATION

Conceptually, we can search a particular set of

parameters {p

1

, p

2

, …, p

n

} which is at the earliest

time point t that is not dominated by any t' such that

the value of the objective function O is maximal

among all the instantiations of values into

parameters. However, the problem of this approach

is that for every single parameter set at t in a

learning data set, the parameter set at t has to be

examined with all the previous sets of parameters at

t' for checking the non-dominance before the

optimal solution can be found. In fact, due to the

quadratic nature, the conceptual approach is time

consuming and expensive particularly if the size of

the learning data set is significantly large. Instead,

the Checkpoint algorithm uses the KD-tree data

structure and searching algorithm to evaluate

whether a time point t is dominated based on the

Claim 1 for checking the non-dominance. The

pseudo code of the algorithm is:

Input: <S, P, C, U>

Output: p[1…k] is an array of the

optimal parameters that maximize

the objective.

Data Structures:

1. N is the size of the learning data

set.

ICEIS 2011 - 13th International Conference on Enterprise Information Systems

96

2. T

kd

is a KD tree that stores the

parameter vectors that are not

dominated so far.

3. MaxT is the time point that gives

the maximal U so far, denoted by MaxU.

Processing:

STEP 1: T

kd

:= <S

1

(0), S

2

(0), …,

S

k

(0)>;

MaxT := 0;

MaxU := U(0);

STEP 2: FOR t := 1 TO N - 1 DO {

Non-Dominance Test: Query the T

kd

to find if there exists a point

(

1

,

2

, …,

k

) in the T

kd

, which

is in the range [S

1

(t), ∞) x

[S

2

(t), ∞) x … x [S

k

(t), ∞).

IF (NOT AND t is not dominated

AND U(t) > MaxU) THEN Add

<S

1

(t), S

2

(t), …, S

k

(t)> to T

kd

;

MaxT := t;

MaxU := U(t);}

STEP 3: FOR i := 1 TO k DO {

p[i] := S

i

(MaxT);}

STEP 4: RETURN p[1…k];

Clearly, the first time point is not dominated

because there is no time point preceding it.

Therefore, <S

1

(0), S

2

(0), …, S

k

(0)> can be added to

T

kd

. 0 and U(0) can be assigned to MaxT and MaxU

respectively.

Using the Checkpoint algorithm step by step for

the problem shown in Table 5, we can search

through a particular set of parameters {p

1

, p

2

, p

3

}

which is at the earliest time point t that is not

dominated by any t' such that the value of the utility

function U is maximal. In STEP 1, the <S

1

(t

1

),

S

2

(t

1

), S

3

(t

1

)> is added to the T

kd

since it is the first

time point. Then t

1

and U(t

1

) are assigned to MaxT

and MaxU respectively. In STEP 2, t

2

is not

dominated because S

1

(t

1

) < S

1

(t

2

) ∧ S

2

(t

1

) > S

2

(t

2

) ∧

S

3

(t

1

) > S

3

(t

2

) does not satisfy the Claim 1. However,

t

3

is dominated because S

1

(t

1

) > S

1

(t

3

) ∧ S

2

(t

1

) > S

2

(t

3

)

∧ S

3

(t

1

) < S

3

(t

3

) does satisfy the Claim 1. <S

1

(t

2

),

S

2

(t

2

), S

3

(t

2

)> is added to the T

kd

because t

2

is not

dominated and U(t

2

) > U(t

1

). Thus t

2

and U(t

2

) are

assigned to MaxT and MaxU respectively. In STEP

3, p[1] := S

1

(MaxT), p[2] := S

2

(MaxT), and p[3] :=

S

3

(MaxT) in the for-loop statement. In STEP 4, the

algorithm returns 25, 15, and 2.

The time complexity for the range search and

insertion of a parameter vector in the T

kd

tree is

O(klogN) respectively.

Theorem 1: For N parameter vectors in the data set,

the Checkpoint algorithm correctly computes an

EQPE solution, i.e., argmax O(p

1

, p

2

, p

3

, p

4

, p

5

),

where O is the objective function of the EQPE

problem, with the complexity O(kNlogN). The proof

of the theorem is shown in Appendix.

Using the Checkpoint algorithm, we can obtain

the optimal decision parameters and the maximal

earning from the training data set for the financial

problem shown in Table 6. The time complexity of

the MLE for the logit regression model is O(k

2

N),

where k is the number of decision parameters, and N

is the size of the learning data set. For the

Checkpoint algorithm, the complexity is O(kNlogN).

Using the decision parameters from the financial

expert (i.e., -20%, 0, -30, 45, 180 days), the logit

regression model, and the Checkpoint algorithm, the

“Best Buy” opportunities in stock and their earnings

are shown in Table 7. Note that the Checkpoint

algorithm considerably outperforms both the

financial expert’s criteria and the logit regression

model.

Table 5: Values of S

1

, S

2

, S

3

, and U at the time point t

1

, t

2

,

and t

3

.

Time S

1

S

2

S

3

U

t

1

13 27 3 10

t

2

25 15 2 200

t

3

10 20 5 150

Table 6: Optimal Decision Parameters and Maximum

Earning (%) from the Learning Data Set

1

.

p

1

p

2

p

3

p

4

p

5

O(p

1

,p

2

,p

3

,p

4

,p

5

)

-29.02

-

20.01

-

26.61

49 70 53.37

Table 7: Investors’ Earning of the S&P 500 Index Fund

from the Test Data Set

2

.

Decision

Approach

Best

Buy

S&P

500 Index

Earning

%

Financial Expert’s

Criteria

10/09/08 909.92 1.03

Logit Regression

Model

11/26/08 887.68 3.56

Checkpoint

Algorithm with

Financial Expert’s

Template

03/10/09 719.6 27.8

1. The learning data set is from 06/01/1997 to 06/30/2005.

2. The test data set is from 07/01/2005 to 06/30/2009 that is the

sell date of the fund with the value of 919.32.

A SERVICE FRAMEWORK FOR LEARNING, QUERYING AND MONITORING MULTIVARIATE TIME SERIES

97

5 MTSA DATA MODEL

AND QUERY LANGUAGE

5.1 Data Model

The time-series (TS) data model is an extension of

the relational model with specialized schemas. A

time-series schema is of the form TSname(T:Time,

Vname:Vtype), where Time and Vtype are data

types, Vtype is either Real or Integer, and TSname

and Vname are names chosen by users.

A time-event (TE) schema is of the form

TEname(T:Time, Ename:Binary), where Binary is

the binary type corresponding to the domain {0,1},

and TEname and Ename are names chosen by users.

A TS database schema is a set of relational

schemas which may include (specific) TS and/or TE

schemas.

A TS tuple over a schema TSname(T:Time,

Vname:Vtype) is a relational tuple over that schema,

i.e., a mapping m: {T, Vname} → Dom(Time) x

Dom(Vtype), such that m(T) ∈ Dom(Time) and

m(Vname) ∈ Dom(Vtype).

A TE tuple over a similar schema

TEname(T:Time, Ename:Binary) is a mapping m:

{T, Ename} → Dom(Time) x Dom(Binary), such

that m(T) ∈ Dom(Time) and m(Ename) ∈

Dom(Binary).

Let us consider our financial example. In the

market-bottom scenario, the service provider can use

the querying service to create the base, derived, and

related time-series tables as inputs and store them in

the database. The base time-series tables are

SP500(T, Index), CG(T, Index), CC(T, Index),

ISM(T, Index), and NLC(T, Index).

5.2 Querying Service

Using the base time series tables, we can generate

derived time series tables (if any) by the traditional

SQLs. In our case study, some derived time series

tables, e.g., SPD(t), CCD(t), etc., are:

CREATE VIEW SPD AS (

SELECT After.T, After.Average /

Before.Average – 1 AS Value

FROM (SELECT SP1.T,AVG(SP2.Index)

AS Average

FROM SP500 SP1, SP500 SP2

WHERE SP2.T <= SP1.T

AND SP2.T >= SP1.T – 6

AND SP1.T – 6 >= 0

GROUP BY SP1.T) After,

(SELECT SP1.T, AVG(SP2.Index) AS

Average

FROM SP500 SP1, SP500 SP2

WHERE SP2.T <= SP1.T – 150

AND SP2.T >= SP1.T – 156

AND SP1.T – 156 >= 0

GROUP BY SP1.T) Before

WHERE After.T = Before.T);

CREATE VIEW CCD AS (

SELECT After.T, (After.Average –

Before.Average) AS Value

FROM (SELECT CC1.T,AVG(CC2.Index)

AS Average

FROM CC CC1, CC CC2

WHERE CC2.T <= CC1.T

AND CC2.T >= CC1.T – 6

AND CC1.T – 6 >= 0

GROUP BY CC1.T) After,

(SELECT CC1.T,AVG(CC2.Index)

AS Average

FROM CC CC1, CC CC2

WHERE CC2.T <= CC1.T – 150

AND CC2.T >= CC1.T – 156

AND CC1.T – 156 >= 0

GROUP BY CC1.T) Before

WHERE After.T = Before.T);

5.3 Monitoring and Recommendation

Service

Using the monitoring and recommendation service

over the new incoming data, the financial analyst

can recommend the investors whether or not they

should buy the stock. In our example, the input

parametric time series tables for monitoring are

SPD(T, Value), CG(T, Index), CCD(T, Value),

ISM(T, Index), and NLCD(T, Value). The

monitoring and recommendation service can be

expressed by a monitoring view and executed by the

MONITOR command.

CREATE VIEW MarketBottomTable AS (

SELECT SPD.T,(CASE WHEN SPD.Value <

PR.p

1

AND CG.Index < PR.p

2

AND CCD.Value < PR.p

3

AND

ISM.Index < PR.p

4

AND

NLCD.Value > PR.p

5

THEN ‘1’

ELSE ‘0’ END) AS MB

FROM SPD, CG, CCD, ISM, NLCD,

Para PR

WHERE SPD.T = CG.T AND CG.T =

CCD.T AND CCD.T = ISM.T AND ISM.T =

NLCD.T);

CREATE VIEW

MB_Monitoring_Recommendation

AS (SELECT MBT.T, (CASE WHEN MBT.MB

= ‘1’ THEN ‘Market

Bottom Is Detected.

Buy Stock Is

Recommended.’

END) AS Action

FROM MarketBottomTable MBT);

MONITOR MB_Monitoring_Recommendation;

ICEIS 2011 - 13th International Conference on Enterprise Information Systems

98

where Para is a table to store the decision

parameters, e.g., p

1

= -20, p

2

= 0, p

3

= -30, p

4

= 45,

and p

5

= 180. If the parametric monitoring constraint

in the CASE WHEN clause is satisfied at the current

time point t, the value of the attribute “MB”

dedicates “1”. The service then recommends the

financial analysts to buy the index fund for the

investors since the market bottom is predicted.

5.4 Parameter Learning Service

As we discussed, the expert’s suggested parameters

(-20. 0, -30, 45, 180) are not accurate enough to

monitor the dynamic financial market at all time;

thus, the parameter learning service should be

adopted by expressing as follows:

Step 1: Store base TS tables, e.g.,

SP500, CG, CC, ISM, and NLC, in

the database.

Step 2: Define SQL views for derived

TS tables, e.g, SPD, CCD,

etc., shown in Section 5.2.

Step 3: Create a parameter table

which stores the optimal

decision parameters.

CREATE VIEW Para (

p

1

REAL,

p

2

REAL,

p

3

REAL,

p

4

REAL,

p

5

REAL);

Step 4: Create a TS view for the

time utility.

CREATE VIEW Earning AS (SELECT

SP1.T,

((Last.Index/SP1.Index –

1) * 100) AS Percent FROM SP500

SP1,

(SELECT SP2.Index

FROM SP500 SP2

WHERE SP2.T >= ALL

(SELECT SP3.T

FROM SP500 SP3)) Last);

Step 5: Create a learning event and

then execute the event

construct to learn the

parameters.

CREATE EVENT

LearnMarketBottomParameter (

LEARN Para PR

FOR MAXIMIZE E.Percent

WITH SPD.Value < PR.p

1

AND

CG.Index < PR.p

2

AND

CCD.Value < PR.p

3

AND

ISM.Index < PR.p

4

AND

NLCD.Value > PR.p

5

FROM SPD, CG, CCD, ISM,

NLCD, Earning E

WHERE SPD.T = CG.T AND

CG.T = CCD.T AND CCD.T =

ISM.T AND ISM.T = NLCD.T

AND NLCD.T = E.T;)

EXECUTE

LearnMarketBottomParameter;

When the event “LearnMarketBottomParameter”

is executed, the command “LEARN” will call for the

Checkpoint algorithm to solve the corresponding

EQPE problem and will put its solution in the Para

table, where all parameters, e.g., p

1

, p

2

, p

3

, p

4

, and p

5

are instantiated with optimal values.

6 CONCLUSIONS AND FUTURE

WORK

To the best of our knowledge, this is the first paper

to propose a service framework for multivariate time

series analytics that provides model definition,

querying, parameter learning, model evaluation,

monitoring, and decision recommendation over

multivariate time series data. The parameter learning

services combine the strengths of both domain-

knowledge-based and formal-learning-based

approaches for maximizing utility over multivariate

time series. It includes a mathematical model and a

learning algorithm for solving Expert Query

Parametric Estimation problems. Using the

framework, we conduct a preliminary experiment in

the financial domain to demonstrate that our model

and algorithm are more effective and produce results

that are superior to the two approaches mentioned

above. We also develop MTSA data model and

query language for the services of querying,

monitoring, and parameter learning. There are still

many open research questions, for example, what

models can capture different types of events and

how those events impact the services that the

framework provides.

REFERENCES

Bellman, R., 1961. Adaptive Control Processes: A Guided

Tour. Princeton, University Press.

Bentley, J. L., 1975. Multidimensional Binary Search

Trees Used for Associative Searching.

Communications of the ACM, Vol 18 Issue 09, p.

509-517, 1975.

A SERVICE FRAMEWORK FOR LEARNING, QUERYING AND MONITORING MULTIVARIATE TIME SERIES

99

Bentley, J. L., 1979. Multidimensional Binary Search

Trees in Database Applications, Vol 5 Issue 04, p.

333-340. IEEE Transactions on Software Engineering.

Brodsky, A., Henshaw, S.M., and Whittle, J., 2008.

CARD: A Decision-Guidance Framework and

Application for Recommending Composite

Alternatives. 2

nd

ACM International Conference on

Recommender Systems.

Brodsky, A. and Wang. X. S., 2008. Decision-Guidance

Management Systems (DGMS): Seamless Integration

of Data Acquisition, Learning, Prediction, and

Optimization. Proceedings of the 41st Hawaii

International Conference on System Sciences.

Brodsky, A., Bhot, M. M., Chandrashekar, M., Egge, N.E.,

and Wang, X.S., 2009. A Decisions Query Language

(DQL): High-Level Abstraction for Mathematical

Programming over Databases. Proceedings of the

35th SIGMOD International Conference on

Management of Data.

Dougherty, C., 2007. Introduction to Econometrics (Third

Edition). Oxford University Press.

Dumas, M., O’Sullivan, J., Heravizadeh, M., Edmond, D.,

and Hofstede, A., 2001. Towards a Semantic

Framework for Service Description. Proceedings of

the IFIP TC2/WG2.6 Ninth Working Conference on

Database Semantics: Semantic Issues in E-Commerce

Systems.

Erl, T., 2005. Service-Oriented Architecture (SOA):

Concepts, Technology, and Design. Prentice Hall.

Erradi, A., Anand, S., and Kulkarni, N., 2006. SOAF: An

Architectural Framework for Service Definition and

Realization. IEEE International Conference on

Services Computing (SCC'06).

Hansen, B. E., 2010. Econometrics. University of

Wisconsin. http://www.ssc.wisc.edu/~bhansen/

econometrics/Econometrics.pdf.

Harrington, J., 2009. Relational Database Design and

Implementation (Third Edition). Morgan Kaufmann.

Heij, D., De Boer, P., Franses, P. H., Kloek, T., and Van

Dijk, H. K., 2004. Econometric Methods with

Applications in Business and Economics. Oxford

University Press.

Holyfield, S., 2005. Non-technical Guide to Technical

Frameworks. JISC CETIS.

http://www.elearning.ac.uk/features/nontechguide1.

Josuttis, N., 2007. SOA in Practice: The Art of Distributed

System Design. O'Reilly Media.

Ngan, C. K., Brodsky, A., and Lin, J., 2010. Decisions on

Multivariate Time Series: Combining Domain

Knowledge with Utility Maximization. The 15th IFIP

WG8.3 International Conference on Decision Support

Systems.

Nicholls, P., 2009. Enterprise Architectures and the

International e-Framework. e-framework

Organization. http://www.e-

framework.org/Portals/9/docs/EAPaper_2009-07.pdf

Olivier, B., Roberts, T., and Blinco, K., 2005. The e-

Framework for Education and Research: An

Overview. e-framework Organization. http://www.e-

framework.org/Portals/9/Resources/eframeworkrV1.p

df.

Ort, Ed. Service-Oriented Architecture and Web Services:

Concepts, Technologies, and Tools. Sun Developer

Network Technical Articles and Tips.

http://java.sun.com/developer/technicalArticles/WebS

ervices/soa2/

Papazoglou, M., and Heuvel, W., 2005. Service Oriented

Architectures: Approaches, Technologies, and

Research Issues. The VLDB Journal, June.

Quartel, D., Steen, M., Pokraev S., and Sinderen, M.,

2007. COSMO: A Conceptual Framework for Service

Modelling and Refinement, Volume 9, Numbers 2-3,

225-244, July. Journal of Information Systems

Frontiers.

Ralph H. Sprague, Jr., 1980.

A Framework for the

Development of Decision Support Systems, Volume 4,

Number 4, 1-26, December. MIS Quarterly.

Samet, H., 2006. Foundations of Multidimensional and

Metric Data Structures. Morgan Kaufmann.

Stack, J. B., 2009. Technical and Monetary Investment

Analysis, Vol 9 Issue 3 & 5. InvesTech Research.

Stephen, B., et al., 2008. Database Design: Know It All.

Morgan Kaufmann.

Wilson, S., Blinco, K., and Rehak, D., 2004. Service-

Oriented Frameworks: Modelling the Infrastructure

for the Next Generation of e-Learning Systems. JISC

CETIS. http://www.jisc.ac.uk/uploaded_documents/

AltilabServiceOrientedFrameworks.pdf.

Zhang, T., Ying, S., and Cao, S., and Jia, S., 2006. A

Modeling Framework for Service-Oriented

Architecture. Proceedings of the Sixth International

Conference on Quality Software (QSIC'06).

ICEIS 2011 - 13th International Conference on Enterprise Information Systems

100

APPENDIX

Claim 1 - Given the conjunctions of inequality

constraints, S

1

(t) op

1

p

1

∧ S

2

(t) op

2

p

2

∧ … ∧ S

k

(t) op

k

p

k

and the two time points t', t such that 0 ≤ t' < t, t'

≻ t if and only if S

1

(t') op

1

S

1

(t) ∧ S

2

(t') op

2

S

2

(t) ∧ …

∧ S

k

(t') op

k

S

k

(t).

Proof:

Without loss of generality, we assume that op

i

=

“≤”, for all 1 ≤ i ≤ k. It is because “≥” can be

replaced with ≤ by changing a corresponding time

series S

i

(t) to - S

i

(t). For op

i

= “=”, we can use the

conjunction with both ≥ and ≤.

If Direction:

Assume that S

1

(t') ≤ S

1

(t) ∧ S

2

(t') ≤ S

2

(t) ∧ … ∧

S

k

(t') ≤ S

k

(t). For any (p

1

, p

2

,

…, p

k

) ∈ R

k

and every i

= 1, 2, …, k, if S

1

(t) ≤ p

1

, then S

1

(t') ≤ p

1

because

S

1

(t') ≤ S

1

(t). Therefore, S

1

(t) ≤ p

1

∧ S

2

(t) ≤ p

2

∧ … ∧

S

k

(t) ≤ p

k

→ S

1

(t') ≤ p

1

∧ S

2

(t') ≤ p

2

∧ … ∧ S

k

(t') ≤ p

k

and then t' ≻ t.

Only If Direction:

Assume that t' ≻ t. Then S

1

(t) ≤ p

1

∧ S

2

(t) ≤ p

2

∧

… ∧ S

k

(t) ≤ p

k

→ S

1

(t') ≤ p

1

∧ S

2

(t') ≤ p

2

∧ … ∧ S

k

(t')

≤ p

k

. Therefore, for any (p

1

, p

2

,

…, p

k

) ∈ R

k

and

every i = 1, 2, …, k, we have S

i

(t) ≤ p

i

→ S

i

(t') ≤ p

i

.

Proof of Theorem 1: The Checkpoint algorithm

correctly solves the EQPE problem, i.e., if argmax

O(p

1

, p

2

, p

3

, p

4

, p

5

), where O is the objective

function of the EQPE problem.

The time complexity is O(kNlogN), where k is

the number of time series and N is the size of the

learning data set.

Proof: To prove the correctness of the algorithm

if it is sufficient to show Claim 2: The Non-

Dominance test in STEP 2 of the Checkpoint

Algorithm is satisfied for the time point t if and only

if there does not exist t' that dominates t, where 0 ≤ t'

< t.

We prove it by induction on t, where 1 ≤ t ≤ N.

For t = 1, T

kd

= ∅ and t = 1 is not dominated;

therefore, the “if and only if” condition holds.

Assuming the correctness for 1, 2, …, t-1; it follows

the STEP 2 of the algorithm that T

kd

at point t

contains all non-dominated time points t', where t' ≤

t - 1.

If Direction:

The IF part of Claim 2 is straightforward since if

t is not dominated by an earlier time point t', such

point cannot appear on the T

kd

tree; therefore, the

Non-Dominance Test must be satisfied by Claim 1.

Only If Direction:

For the ONLY IF part of the Claim 2, assume

that the Non-Dominance test in STEP 2 of the

algorithm is satisfied. Then there does not exist the

time point t' on T

kd

for which (S

1

(t'), S

2

(t'), …, S

k

(t'))

∈ [S

1

(t), ∞) x [S

2

(t), ∞) x … x [S

k

(t), ∞), where 0 ≤ t'

< t. Assume that T

kd

at time t contains the time

points

<

<⋯<

and assume, by

contradiction, that there exists t' that dominates t, t'

≻ t, where 0 ≤ t' < t. Clearly, t' is not one of

<

<⋯<

because they do not dominate t

by the induction hypothesis. Because t' was not

added to the T

kd

tree and the induction hypothesis,

≻

′

for some j = 1, 2, …, m. From the

contradiction assumption t' ≻ t and the transitivity of

≻, it follows that

≻. Thus, by Claim 1,

(

)≤

() ∧

(

)≤

() ∧ ⋯ ∧

(

)≤

() which contradicts the fact that the Non-

dominance test in STEP 2 was satisfied for t. This

completes the proof of Claim 2 and of the

correctness of the algorithm.

Time Complexity: The algorithm performs N

iterations in STEP 2, spending time O(klogN) using

the T

kd

algorithm (Bentley, 1975 & 1979) for the T

kd

range query in Non-Dominance Test. Thus the

overall complexity is O(kNlogN).

A SERVICE FRAMEWORK FOR LEARNING, QUERYING AND MONITORING MULTIVARIATE TIME SERIES

101