Inclusive Finance and Enterprise Technological Innovation in the

Context of Big Data: Evidence from Listed Companies

Fangxin Shi

Shaan Xi Normal University, Xi an, Shaan Xi, China

Keywords: Digital Financial Inclusion, Enterprise Technology Innovation, Economic Growth.

Abstract: Computer software engineering development projects involve many fields, and there are many risks and

complex and unknowable factors. In this systematic project, due to the particularity of software products, it is

necessary to pay attention to and apply various digital and modern technologies to make computer software

engineering become a Leading the driving force of innovation and development in various industries and

meeting the needs of modern development. Based on the development and application of digital technology

in computer software engineering, this paper elaborates the methods and technologies commonly used in

engineering development, and proposes corresponding optimization strategies for the application of digital

technology.

1 INTRODUCTION

A lot of convenience has come, and it has played an

irreplaceable key role in the context of the rapid

development of information and modern society.

Computer software engineering is a new thing. After

it entered our country, it has achieved great

development and progress at the technical level. On

the platform of modern and digital technology

application, through the linking and sharing of

information, a new industrial chain and core have

gradually formed. With the extensive development of

digital technology, computer software engineering

has replaced and surpassed traditional technology.

However, in the process of digital technology

development of computer software engineering, there

are still some problems and defects. Considering the

innovation of some application technologies

themselves The lack of performance limits the

application and development of machine software

engineering to a certain extent. To this end, it is

necessary to strengthen the computer digitization

technology independently developed and innovated

in our country. Only on the premise of grasping the

independent and innovative digitization and

modernization technology can we promote the

forward and healthy development of computer

software engineering and safeguard the national

security and defense forces of our country. Escort and

promote the progress and development of my

country's modernization cause.

2 LITERATURE REVIEW

Many scholars have actively explored the causes of

the financing difficulties of enterprises and put

forward corresponding solutions. Due to bank credit

rationing, enterprises can't get access to loan, their

collateral value is the root cause of suffering to bank

credit rationing (Stiglitz, 1981, Weiss, 1981, Wang,

2003, Zhang, 2003). Lack of " hard information"

caused by information asymmetry is also an important

factor restricting its financing (Lin, 2001, Li, 2001).

The banks which use relational loans can ease the

enterprises’ financing dilemma, because the relational

loan depends on the "soft information" of the

enterprise (Berger, 1995, Udell, 1995)

.

During the

epidemic, China's Central Bank also implemented

preferential credit policies such as reserve reduction,

aiming to help enterprises acquire loan and alleviate

their pressure of cash flow, but said most of the

enterprises have not acquired bank loans, its cash flow

pressure has not been eased (Zhu, 2020, Zhang, 2020,

Li, 2020, Wang, 2020).

Inclusive finance provides a new way to solve the

financing problems of enterprises. The concept of

inclusive finance was proposed by the United Nations

194

Shi, F.

Inclusive Finance and Enterprise Technological Innovation in the Context of Big Data: Evidence from Listed Companies.

DOI: 10.5220/0011170600003440

In Proceedings of the International Conference on Big Data Economy and Digital Management (BDEDM 2022), pages 194-198

ISBN: 978-989-758-593-7

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

in 2005, and its essence is to resolve financial

exclusion. In recent years, commercial Banks have

set up inclusive finance institutions, using digital

financial means to provide finance to enterprises

(Zhu, 2020, Zhang, 2020, Li, 2020, Wang, 2020). The

inclusive finance institutions have dedicated risk

management and compensation mechanism, this

mechanism reduce the bank risk bearing level,

improve the credit availability (Yu, 2020, Kang,

2020, Zhou, 2020). Digital financial advantage

continuously emerging, on the one hand, digital

financial in the information gathering has

incomparable advantage over traditional financial,

this advantage allows it to effectively identify risks,

according to the data collected for the credit quality

of the enterprises to provide financing support (Yu,

2020, Dou, 2020). On the other hand, digital finance

with the help of the Internet technology, can reduce

the cost of financing of enterprises, improve the

financing efficiency (Liang, 2018, Zhang, 2018). In

addition, digital financial also broke through the

traditional financial institutions physical network

restrictions on financial services, it is not limited to

offline services model make it possible for financial

services of universal coverage, many scholars believe

that commercial banks use digital inclusion financing

is feasible to resolve enterprise financing difficulties.

3 RESEARCH DESIGN

3.1 The Source of Data

In this paper, the annual data of listed companies from

2011 to 2017 are taken as sample data, and the sample

data are screened as follows: First, the listed ST and

delisted as well as the financial, real estate and

insurance categories during 2011-2017 are excluded;

Second, the variables in the data are Winsorized.

Third, for the missing financial information of a large

number of enterprises, this paper will be removed. The

financial and patent application data of enterprises

used in this paper come from Guotai 'an Database, and

the digital Financial Inclusion Index adopts The

Digital Financial Inclusion Index (2011-2018)

compiled by Peking University.

3.2 Model Setting and Variable

Definition

Based on existing studies, this paper constructs the

following model:

01 2

j

tijtjt

innov difi control

ββ β

ε

=+ + +

(1)

Where, i, j, t represent company, region and year.

The explained ariable inov is the innovation capability

of enterprises, and the explained variable difi is digital

inclusive finance. Control is the Control variable,

including enterprise size, profitability roa, Cash flow

cash, fixed asset share fas, corporate leverage lev, and

Capital intensity Capital. In addition, the model

controls the fixed effects of time and industry, and ε is

the error term.

Among them, the explained variable innov

represents the innovation ability of enterprises.

Existing literatures usually measure enterprise

innovation by the innovation input and output of

enterprises, but the data statistics of enterprise

innovation input and output in current databases are

missing. At the same time, patent application can

represent the innovation ability of enterprises.

Therefore, this paper uses the total number of three

types of patent applications of listed companies to

measure enterprise innovation.

The core explanatory variable difi represents the

digital financial inclusion index. Since the digital

financial inclusion index value at the provincial level

is too large compared with other variables, this paper

takes logarithm of the digital financial inclusion

index.

Control is a series of enterprise-level data to

reduce the endogenous problem of the model. The

following variables are selected in this paper:

Profitability (roa), capital intensity (cap), enterprise

age (age), enterprise size (size) and enterprise

leverage (lev), Cash flow (cash), fixed asset share

(fas). In addition, the model controlled for annual and

industry fixed effects.

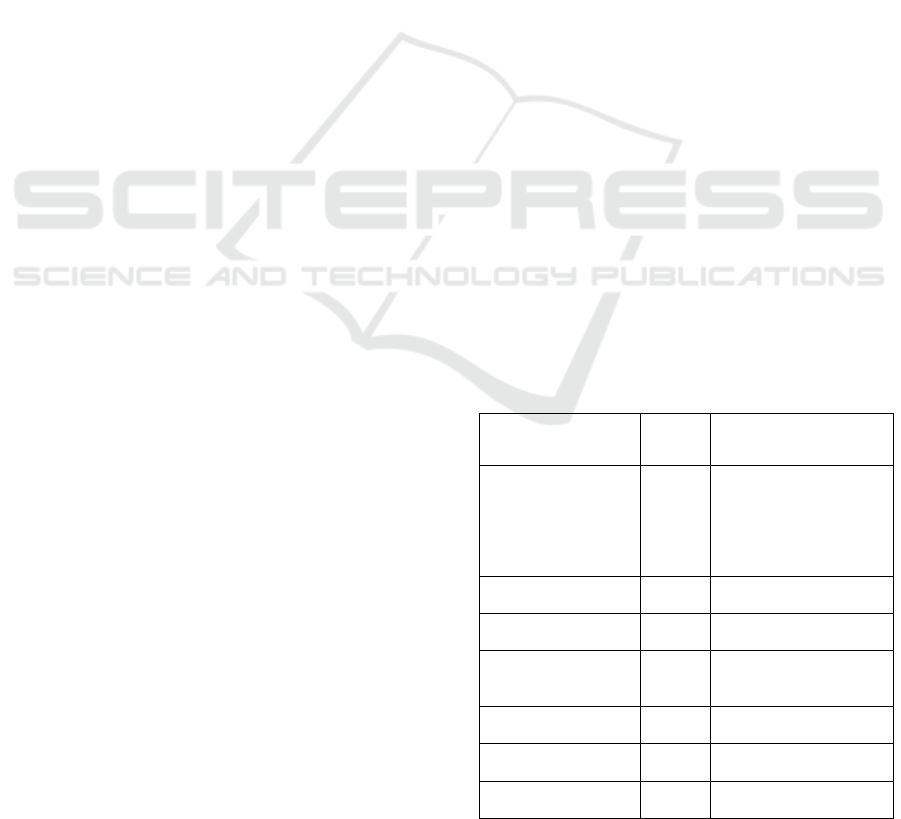

Table 1: Variable Definition.

Variable name

Variabl

e

symbol

Variable definition

The innovation

ability

innov

The total number of

patents filed by

enterprises (including

inventions, practical

shapes and designs) is

logarithmic

Profitability roa

Net profit margin on

total assets

Capital intensity cap

Ratio of total assets to

total operating income

Enterprise age age

Year of observation

minus year of

establishmen

t

The enterprise scale size

Take the logarithm of

total enterprise assets

Corporate leverage

ratio

lev

Corporate asset-liability

ratio

Cash flow cash

Net cash flows from

operating activities

Inclusive Finance and Enterprise Technological Innovation in the Context of Big Data: Evidence from Listed Companies

195

Variable name

Variabl

e

symbol

Variable definition

Share of fixed assets fas

Fixed assets account for

the proportion of total

assets

4 RESULTS AND ANALYSIS

Table 1 shows the empirical test results of the impact

of digital financial inclusion on enterprise

technological innovation. In Model (1), the fixed

effect of "time-industry" is controlled. The results

show that the regression coefficient of digital

inclusive finance (difi) on enterprise patent

application is positive, and passes the significance

test of 1%, which indicates that the development of

digital inclusive finance helps promote enterprises to

improve their independent innovation ability.

From the perspective of control variables, some

factors of enterprises themselves will also affect the

local technology innovation of enterprises. The

regression coefficient of capital intensity, leverage

ratio and cash flow of an enterprise is significantly

positive, which indicates that the more capital

intensity, the higher the share of fixed assets and the

more cash flow of an enterprise, the more beneficial

it is to technological innovation.

Table 2: Results of Regression.

(1)(2)

innov innov

difi 30.43

***

17.69

***

(6.54) (4.33)

roa 62.19

(1.35)

cap 2.34e-08

***

(32.63)

age -0.193

(-0.52)

size 59.72

(0.22)

lev 97.90

***

(7.95)

cash 4.26e-08

***

(7.72)

fas 48.35

(0.15)

cons -49.79

*

-95.85

Industry, Yea

r

(-1.99)

control

(-0.29)

control

N

adj.R

2

8287

0.005

8287

0.266

Note: The brackets are t values, where *, ** and *** represent significance levels of

10%, 5% and 1% respectively

5 RSULTS AND ANALYSIS

Table 2 shows the empirical test results of the impact

of digital financial inclusion on enterprise

technological innovation. In Model (1), the fixed

effect of "time-industry" is controlled. The results

show that the regression coefficient of digital

inclusive finance (difi) on enterprise patent

application is positive, and passes the significance

test of 1%, which indicates that the development of

digital inclusive finance helps promote enterprises to

improve their independent innovation ability.

From the perspective of control variables, some

factors of enterprises themselves will also affect the

local technology innovation of enterprises. The

regression coefficient of capital intensity, leverage

ratio and cash flow of an enterprise is significantly

positive, which indicates that the more capital

intensity, the higher the share of fixed assets and the

more cash flow of an enterprise, the more beneficial

it is to technological innovation.

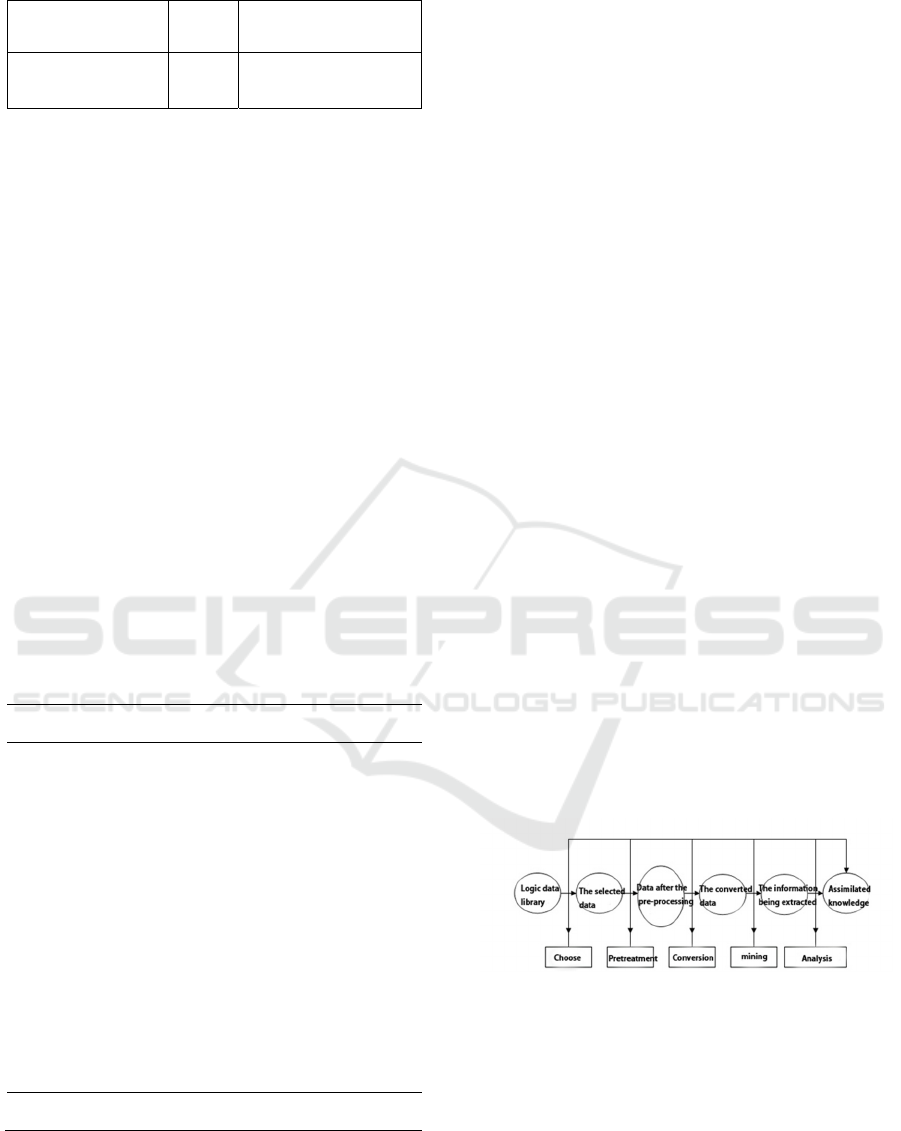

6 THE APPLICATION PROCESS

OF DATA MINING

1) Data mining environment. Data mining refers to a

complete process that mines previously unknown,

effective, and practical information from a large

database, and uses this information to make decisions

or enrich knowledge.

2) Data mining process diagram. The figure below

describes the basic process and main steps of data

mining.

Figure 1. The basic process and main steps of data mining.

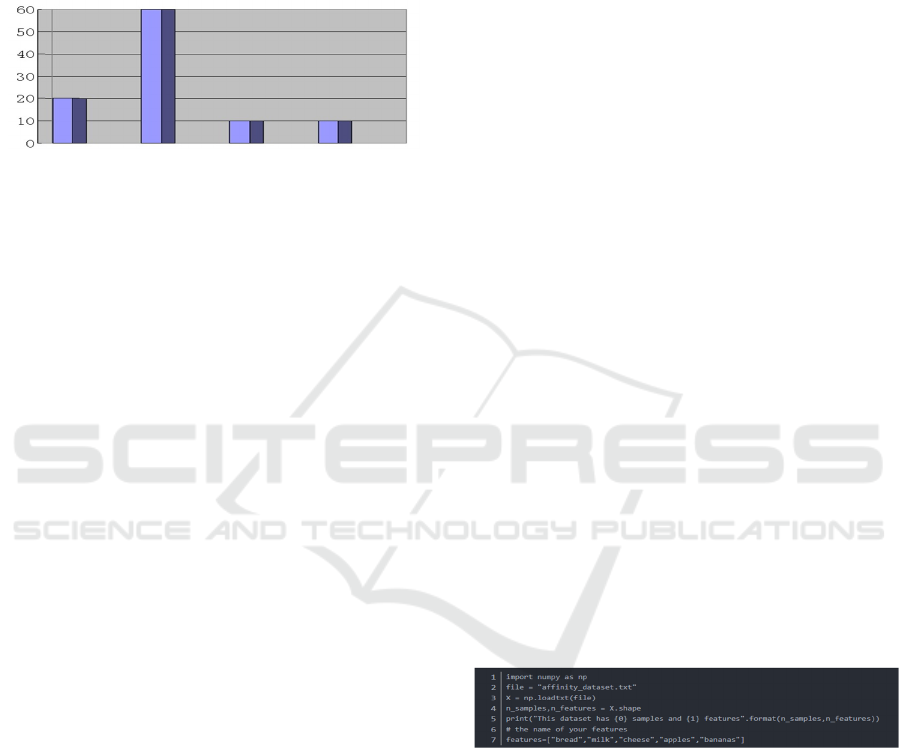

3) Workload of data mining process

The business object being studied in data mining

is the foundation of the entire process. It drives the

entire data mining process. It is also the basis for

testing the final results and guiding the analysts to

complete the data mining and consultants. The steps

in Figure 2 are completed in a certain order, of course.

There will also be feedback between steps in the

whole process. The process of data mining is not

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

196

automatic, and most of the work needs to be done

manually. Figure 3 shows the ratio of the workload of

each step in the whole process, which can be seen as

60% Time is spent on data preparation, which shows

that data mining has strict requirements for data, and

subsequent mining work only accounts for 10% of the

total workload.

Figure 2. Proportion of workload in the data mining

process.

4) The general content of each step in the data

mining process is as follows:

(1) Determine the business object

Clearly define business problems. Recognizing

the purpose of data mining is an important step in data

mining. The final structure of mining is

unpredictable, but the problems to be explored should

be foreseeable. For data mining, data mining is blind.

(2). Data preparation

1) Data selection. Search all internal and external

data information related to business objects, and

select data suitable for data mining applications.

2) Data preprocessing. The quality of the research

data is prepared for further analysis, and the type of

mining operation to be carried out is determined.

3) Data conversion. The data is converted into an

analysis model. This analysis model is established for

the mining algorithm. The establishment of an

analysis model that is really suitable for the mining

algorithm is the key to the success of data mining.

(3). Data mining

Except for the selection of the appropriate mining

algorithm for mining the obtained converted data, all

other tasks can be completed automatically.

(4). Result analysis

The analysis method used to interpret and

evaluate the results should generally be determined

by data mining operations, and visualization

techniques are usually used.

(5). Assimilation of knowledge

Integrate the knowledge obtained from the

analysis into the organizational structure of the

business information system. The step-by-step

implementation of the data mining process requires

personnel with different expertise in different steps.

They can be roughly divided into three categories.

Business analysts: required to be proficient in

business, able to explain business objects, and

determine the business requirements for data

definition and mining algorithms based on each

business object.

Data analysis personnel: proficient in data

analysis technology, have a relatively proficient grasp

of statistics, and have the ability to transform business

requirements into various steps of data mining, and

select the appropriate technology for each operation.

Data management personnel: proficient in data

management techniques, and collect data from

databases or data warehouses. It can be seen from the

above that data mining is a process of cooperation

between a variety of experts, and it is also a process

of high investment in capital and technology. This

process must be repeated in the repeated process,

constantly approaching the essence of things, and

constantly prioritizing problems. Data reorganization

and subdivision, adding and splitting records,

selecting data samples, visualization, data

exploration, clustering analysis, neural network,

decision tree mathematical statistics, comprehensive

interpretation and evaluation of time series

conclusions, data knowledge, data sampling, data

exploration, data adjustment, modeling evaluation.

For example: Relevance Analysis. Relevance

analysis is to give the similarity of items or objects.

There are mainly the following application scenarios.

Providing different services or advertisements to the

target audience. Movie recommendation or Taobao

product recommendation. Genetic analysis to

discover common ancestors. To simplify the code, we

only consider two items at the same time. Let's say

that user A buys milk and bread. We want to follow

the principle that if user A buys X, then he is likely to

buy Y as well.

Figure 3. Code set.

7 CONCLUSIONS AND

RECOMMENDATIONS

In recent years, the development of digital inclusive

finance has attracted high attention from all walks of

life, it also has a profound influence on China's

economic development. This paper studies the impact

of digital inclusive finance on enterprises' innovation

ability, empirically tests the impact of digital

inclusive finance on enterprises' technological

Inclusive Finance and Enterprise Technological Innovation in the Context of Big Data: Evidence from Listed Companies

197

innovation with the help of the data of Chinese listed

companies from 2011 to 2017, and draws the

following conclusions. The development of digital

inclusive finance plays a significant role in promoting

the technological innovation of enterprises. The

possible mechanism of digital inclusive finance to

promote technological innovation of enterprises is

that it alleviates the financing constraints of

enterprises and enables enterprises to increase

investment in R&D activities. It is worth mentioning

that there are still some shortcomings in this paper.

This paper does not test the influence mechanism of

digital inclusive finance on enterprise technological

innovation, which is also the next research of the

author.

Combined with the test results of digital inclusive

finance on enterprise technological innovation, This

paper puts forward the following policy suggestions.

First, we should actively promote the development of

big data technology, encourage financial institutions

to provide financing services to enterprises by means

of digital inclusive finance, and provide full financial

support for technological innovation activities of

enterprises. According to the Plan for Promoting The

Development of Inclusive Finance (2016-2020)

issued by The State Council, inclusive finance refers

to providing appropriate and effective financial

services at an affordable cost to all social strata and

groups in need of financial services based on equal

opportunities and the principle of business

sustainability. Small and micro enterprises, farmers,

urban low-income groups, poor people, the disabled,

the elderly and other special groups are the key

service objects of inclusive finance in China. It is of

great significance to develop inclusive finance to help

those who have long been outside the formal financial

system to obtain effective financial support.

Second, the characteristics of digital inclusive

finance, such as low threshold and high convenience,

make it have a positive impact on many aspects of the

economy. However, the distorted development of

Internet companies blindly pursuing profits not only

has a huge impact on traditional commercial banks,

but also endangers the stability of the entire financial

system. From the liability side of banks, various

financial products launched by digital inclusive

finance make the deposit competition faced by

commercial banks increasingly fierce. Financial

products represented by Yu'ebao have been highly

sought after by investors since their issuance. They

not only promise flexible access to investors' funds,

but also bring investors returns higher than bank

deposits, leading to continuous loss of savings

deposits in commercial banks. From the asset side of

the bank, the bank may choose the assets with high

risk and high return to make up for the loss of its

liability side. From the point of view of payment end,

Alipay, wechat Pay and other third-party payment

platforms have formed a situation of competing with

banks. Banks' fee income has been slashed by the fact

that most payments are bypassing the banking

system, with no fees charged and money transferred

immediately to their accounts. The digitalization of

finance makes high-risk behaviors more hidden.

Regulators should be alert to non-performing asset

securitization and financial products of commercial

banks. Although these financial products are covered

with the cloak of inclusive finance, they are

essentially Ponzi Financing, which undermines the

stability of commercial banks and even the entire

financial system. Therefore, the management's

supervision of the financial field should follow

closely the financial innovation and prevent financial

risks.

REFERENCES

Berger A. N., Udell G. F., "Relationship Lending and Lines

of Credit in Small Firm Finance". Journal of Business,

1995.

Liang Bang, Zhang Jianhua." The Impact of China's

Inclusive Financial Innovation on Smes' Financing

Constraints ", Journal of China Science and

Technology Forum, Vol.11, pp.94-105, 2018.

Lin Yifu, Li Yongjun.” Development of small and medium-

sized Financial institutions and financing of small and

medium-sized enterprises”. Journal of Economic

Research, Vol.1, pp.10-18+53-93, 2001.

Stiglitz J. and Weiss A., “Credit Rationing in Market with

Imperfect Information. The American Economic

Review”, 1981.

Wang xiao, Zhang Jie. “The relationship between bank

credit rationing and sme lending: a Theoretical model

of Endogenous Collateral and firm size”, Journal of

Economic Research, Vol.3, pp.68-75+92, 2003.

Wuxiang Zhu, Ping Zhang, Pengfei Li, Ziyang Wang. "The

impact of COVID-19 on smes' dilemma and policy

efficiency: an analysis based on two national

questionnaire surveys ", Management World, Vol.4,

pp.13~26, 2020.

Yu P, Dou J X. Digital inclusive finance, “firm

heterogeneity and innovation of msmes”,

Contemporary Economic Management, Vol. (12),

pp79~87,2020.

Yu Weifeng, Kang Qi, Zhou Yongfeng." Can the

Establishment of Inclusive Finance Division in

Commercial banks improve the credit availability of

small and micro enterprises? -- Empirical Test based on

PSM-DID model ", International Journal of Finance,

Vol.11, pp.77-86, 2020.

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

198