Users’ Privacy Concerns and Attitudes towards Usage-based Insurance:

An Empirical Approach

Juan Quintero

1 a

and Alexandr Railean

2 b

1

Department of Computer Science, Friedrich-Alexander-Universit

¨

at Erlangen-N

¨

urnberg (FAU), Erlangen, Germany

2

Institute of Computer Science, Georg-August-Universit

¨

at G

¨

ottingen, G

¨

ottingen, Germany

Keywords:

Usage-based Insurance, Pay as You Drive, Telematics Insurance, Acceptance, Privacy Concerns, Driving

Style, Transparency.

Abstract:

Usage-based Insurance (UBI) is a car insurance model in which the insurance payment calculations are based

on driving data such as speed, acceleration, braking, location, etc. Driving data are collected and analysed by

the insurer to provide feedback on driving performance, help drivers improve their skills, and possibly apply

a discount on their next renewal. So far, UBI research has been focused more on its architecture, benefits, or

acceptance, while the users’ perception of such forms of insurance and their privacy concerns received less

attention. To fill this gap, we conducted an online survey with 281 participants and analysed their responses

using qualitative and quantitative methods. We found that data collection and sharing are the main privacy

concerns. Furthermore, we identified potential discounts as the most important feature in favor of adopting

UBI, while data collection and unfair ratings are the main reasons to avoid or quit UBI.

1 INTRODUCTION

Traditional insurance models are based on subsidized

systems, where customers who do not claim insurance

benefits subsidize others who file such claims. Thus,

it is common to find car insurance programs in which

the fees paid by a driver who does not report any ac-

cident do not differ much from others who usually re-

quire the assistance of the insurer. The fees in these

programs are calculated based on historical data av-

eraged across customers grouped by criteria such as

age, gender, or marriage status (Soleymanian et al.,

2019). UBI programs represent a trend, in which

the fee is based on a customer’s personalized driving

style. UBI is also known as Telematics Insurance, Pay

As You Drive (PAYD), or Pay How You Drive (PHYD).

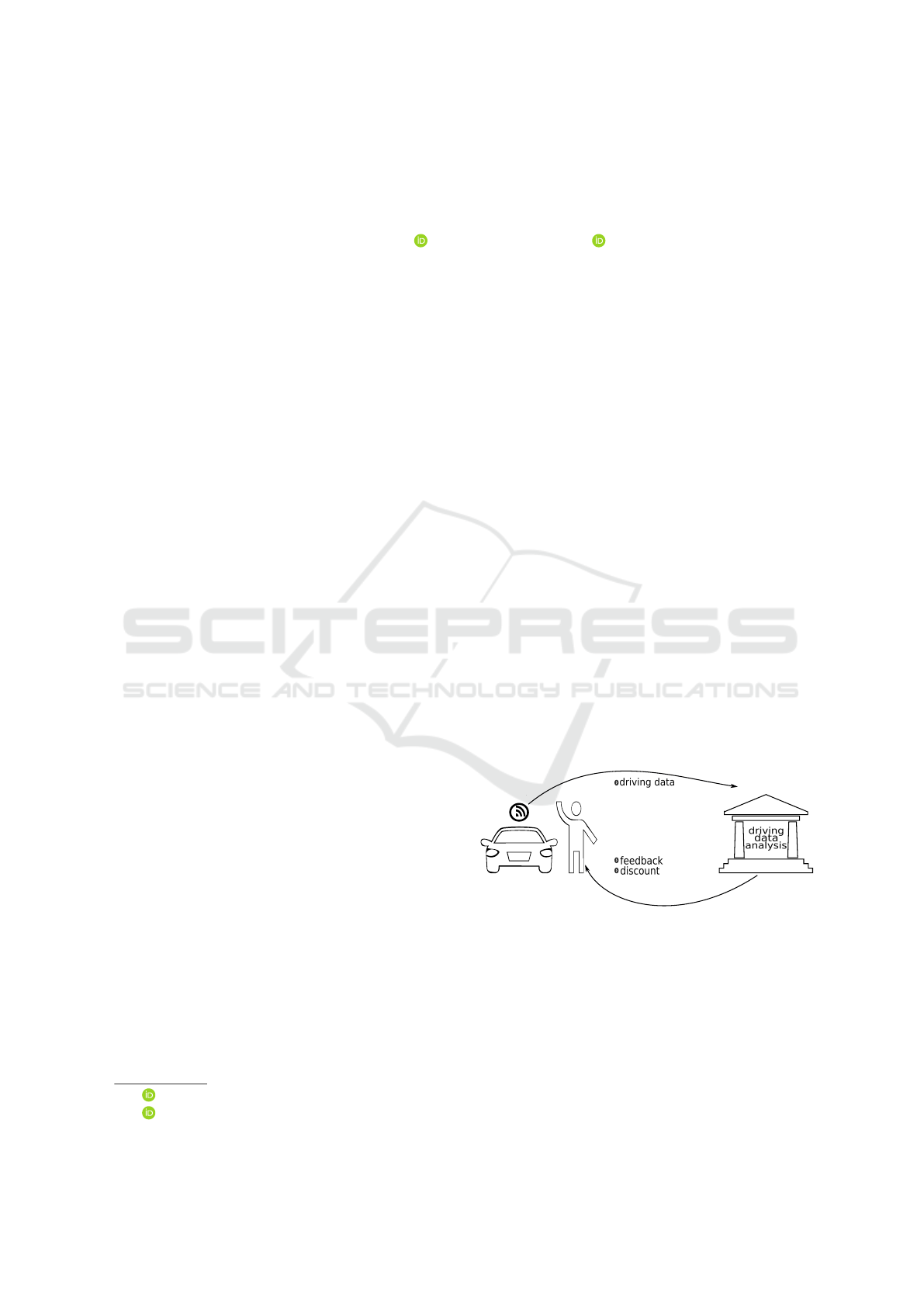

As Figure 1 depicts, driving data are collected through

a telematics device, such as a dongle, a black box, a

smartphone app, or an embedded system, and anal-

ysed by the insurer. The user then gets feedback on

driving performance and a possible discount on the re-

newal payment in case of getting a good driving score.

Soleymanian et al. (2019) found that the main

benefits of UBI are the incentives to improve one’s

a

https://orcid.org/0000-0002-8205-7072

b

https://orcid.org/0000-0002-7472-2108

driving style through feedback, and the potential dis-

count on their insurance fees. On the other hand, the

main disadvantages are the privacy concerns (Arvids-

son et al., 2011; Derikx et al., 2016; Soleymanian

et al., 2019) and discrimination (most programs are

designed for novice drivers or young people).

Insurer

Telematics

device

User

acceleration, braking

GPS location, speed

time of day

in case of getting a

good driving score

Figure 1: General Usage-Based Insurance model.

Although there is research about the technical as-

pects of UBI (Troncoso et al., 2010; Iqbal and Lim,

2006; H

¨

andel et al., 2013), its benefits (Soleymanian

et al., 2019; Derikx et al., 2016; Litman, 2007), its

user acceptance (Mayer, 2012; Tian et al., 2020), and

usability issues (Quintero et al., 2020), less attention

has been given to the users’ perception of data collec-

tion and sharing, financial benefits, driving feedback,

and driving style. We conducted this online survey

290

Quintero, J. and Railean, A.

Users’ Privacy Concerns and Attitudes towards Usage-based Insurance: An Empirical Approach.

DOI: 10.5220/0011044000003191

In Proceedings of the 8th International Conference on Vehicle Technology and Intelligent Transport Systems (VEHITS 2022), pages 290-299

ISBN: 978-989-758-573-9; ISSN: 2184-495X

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

to know more about these topics, and identify privacy

concerns related to UBI. The following research ques-

tions (RQ) are addressed in this paper:

• RQ-1. What are the privacy concerns identified by

users with UBI?

• RQ-2. What are the most important features of

UBI that influence a person’s decision for or

against UBI?

The contributions of this study are as follows: (1)

we determine that participants are aware of and con-

cerned about the sharing and storage of their driving

data, (2) we identify the discount on the next renewal

in case of getting a good driving score as the most

important factor in favor of UBI and collection of my

driving data (GPS location, acceleration, etc.) and

driving rating is unfair as the most important factors

against deciding to use UBI. (3) Based on our find-

ings, we draw recommendations that can help insur-

ers increase the adoption of UBI. (4) We provide the

source code and data to facilitate the replication of our

analysis.

2 BACKGROUND AND

TERMINOLOGY

Based on prior exploratory research (Derikx et al.,

2016; Quintero et al., 2020), we identified several key

factors as potential candidates for influencing UBI

perception. In what follows, we define and describe

each factor, and formulate hypotheses about the rela-

tionships between these factors.

Intention to Use UBI (IU) is the degree to which a

person has formulated a conscious intention to be or

not to be covered by UBI (adapted from (Warshaw

and Davis, 1985, p. 214)).

Privacy Concerns (PC) follow a scale devised by

Dinev and Hart (2006), and relate to opportunistic be-

havior with respect to the personal information shared

with companies by the respondent in particular.

My Perceived Driving Style (MS) is the degree

to which drivers believe that they drive carefully

and cautiously, obeying traffic rules (adapted from

(Mayer, 2012)).

Others’ Perceived Driving Style (OS) is the percep-

tion of how carefully others drive and follow traffic

rules Quintero et al. (2020).

Discount in UBI (DI) is how much money a driver

can save by participating in UBI.

Driving Feedback (DF) relates to how often feed-

back is given to drivers based on their driving perfor-

mance.

We then formulate the following hypotheses based

on the aforementioned factors:

H1. People with low privacy concerns (PC

↓

) are more

willing to be covered by UBI (IU) than others with

high privacy concerns (PC

↑

).

H2. Magnitude of discount (DI) plays a greater role

than the driving style feedback (DF) in UBI percep-

tion by users with high privacy concerns (PC

↑

).

H3. People with high privacy concerns (PC

↑

) prefer

to avoid using smartphones as a telematics device.

H4. People with high privacy concerns (PC

↑

) pre-

fer to avoid sharing telemetry with entities other than

their insurer.

3 METHOD

In July 2021, we conducted an online survey with UBI

users to determine their: (1) privacy concerns with

UBI; (2) the most important UBI features that influ-

ence a person’s decision for or against UBI; (3) pref-

erences for sharing and storage of driving data. The

selection criteria for our study were (1) to have a driv-

ing license, (2) to have experience being covered by a

car insurance program. Our study got approval from

the data protection officer of our university. The sur-

vey was conducted in English.

3.1 Recruitment

To recruit participants and manage the study we de-

cided to use Prolific, an online platform for research

studies, and hosted the survey on a LimeSurvey server

in our university. Participants were screened asking

about their experience with car insurance and specif-

ically with UBI, as well as when they got their first

driving license. Based on the number of UBI pro-

grams in the market and the participants in Prolific

who met the selection criteria, only participants from

Germany, Ireland, United Kingdom, and the United

States were considered in this study. The screen-

ing survey took approximately 3 minutes to complete.

791 participants out of 807 met the criteria of having

a driving license and car insurance. In UBI, we de-

fined Current users (c) as people covered by a UBI

program. Former users ( f ) are people who had been

covered by UBI and for some reason are no longer

covered by it. Potential users (p) are people with a

driving license who never enrolled in a UBI program.

In this paper, we noted current, former, and potential

users with the subscripts c, f , p respectively. Thus,

we identified 30 current, 77 former, and 684 potential

users of UBI. We invited 30

c

, 77

f

, and 250

p

to take

Users’ Privacy Concerns and Attitudes towards Usage-based Insurance: An Empirical Approach

291

part in our study, from which 15

c

, 41

f

, and 225

p

par-

ticipated. The survey took approximately 10 minutes

to complete. We got a total of 281 completed sur-

veys. Participants were rewarded with 0.30 GBP for

the pre-screen survey and 1 GBP for the final survey.

3.2 Survey Structure

We developed the online survey questions based on

existing literature and brainstorming sessions. We

conducted a pilot with 5 researchers to identify con-

cerns related to wording, and the connection between

the research and survey questions. After including

their feedback, we conducted another pilot with 6 par-

ticipants (2

c

, 2

f

, 2

p

) to test completion time and the

survey flow. The final version of the survey has a

55s explanatory video and contains 68 questions, of

which 3 are used for checking the understanding of

UBI concepts from the video.

In what follows, we summarize the questionnaire,

while the full text and other materials are available at

zenodo.org/record/6114141:

Part 1: Explanatory video, including 3 quiz questions

to validate the understanding of UBI concepts.

Part 2: Questions of UBI coverage, name of insurer

and UBI program, and how long participants have

been covered by this insurance. For former users, we

asked about the reasons to quit.

Part 3: Questions related to privacy concerns (PC)

and driving style (MS, OS).

Part 4: UBI scenario depending on each user group

(

c

,

f

,

p

). We provided a scenario for each kind of par-

ticipant to contextualize them about using UBI before

starting the questionnaire. For p users we presented

a hypothetical situation in which their insurer is of-

fering a UBI program and they have the option to be

covered by UBI. For c and f users we suggested re-

plying to the survey based on their current and former

experience using UBI, respectively.

Part 5: Intention to use (IU) and preferences on UBI.

We formulated questions related to which information

participants are willing to share for evaluating their

driving score, which telematics device they would

prefer to use, with whom they prefer to share their

driving data, and their preferred frequency and com-

munication channel to get driving feedback. For c and

f users we asked about the discount on their insurance

programs.

Part 6: Demographics, such as age, gender, country

of residence, education level, occupation, and driving

experience (annual distance traveled).

3.3 Data Analysis

After collecting the survey data, we conducted a qual-

itative and quantitative analysis. We used an induc-

tive thematic analysis (Braun and Clarke, 2006) going

from codes to themes to analyse the comments pro-

vided by users in the open-ended questions. For quan-

titative analysis we used Pandas and SciPy, which are

open-source data science tools. The statistical tech-

niques we applied are covered in detail in Section 4.2.

4 RESULTS

160 participants identified as female, 119 as male, and

2 as diverse. The most represented age category was

between 29 and 33 years old. Participants ranged

in age from 21 to 77 years old. Regarding educa-

tion, 118 had a bachelor degree, 74 had completed

a postgraduate degree, 85 had completed professional

or vocational education, and 4 preferred not to dis-

close. Most participants were potential users (225

p

,

41

f

, 15

c

) of UBI. The geographic distribution is as

follows: United Kingdom (255), followed by United

Stated (17), Germany (7), and Ireland (2).

4.1 Qualitative Analysis

Considering that some parts of our survey gave par-

ticipants the option to offer additional comments

about their responses, we performed thematic anal-

ysis (Braun and Clarke, 2006) to reveal common

themes among the 78 collected entries of unstructured

text. Two researchers did so by coding the comments

independently, then comparing notes and refining the

codebook until consensus was reached. The results of

thematic analysis are shown in Table 1. In what fol-

lows, we share the highlights, indicating which par-

ticipant group referred to this idea.

Distracting feedback can cause a decline in user

satisfaction: “It was annoying that they kept sending

me driving alerts, I felt like I was being tracked and

watched too much” (P36

f

). In addition, it can lead

to accidents caused by distracted driving: “On some

local roads that are technically limited to 30, virtually

every motorist drives at 40. When you’re using UBI

you have to stick to 30, and this causes a lot of irrita-

tion to the drivers stuck behind you, and as a driver it

caused me a great deal of stress at times” (P36

f

).

Model deficiency relates to statements about issues

in scoring algorithms, because they are incomplete

and cannot model the complex driving conditions that

occur sometimes. For example, P22

f

stated they got a

lower score for driving in the dark, even though it was

VEHITS 2022 - 8th International Conference on Vehicle Technology and Intelligent Transport Systems

292

Table 1: Summary of thematic analysis. The references indicate how many participants mentioned a theme, they are coded

by participant type: potential, current and former are marked as P, C, and F respectively.

Theme Subtheme

References

Code

P C F

Barriers

Distracting feedback 4 1 Users feel uncomfortable using UBI

UBI not convenient for users 4 3 Financially ineffective

Model deficiency

2 Inaccurate data

1 1 Danger awareness

5 2 4 Scoring process is incomplete or unfair

2 UBI tailored for young, inexperienced drivers

Decision

making

Decision making

3 Difficult to decide

5 Privacy concerns

Adoption

Increasing UBI adoption

1 1 Car sharing

2 Ownership

2 Self-sufficiency

2 Data portability

2 Critical mass

winter, and there are only a few hours of daylight dur-

ing the season. P34

f

summarized that as “conditions

on the road are not taken into account”. In the words

of P42

f

“those systems are not designed for real world

driving ... only the hypothetical driving that is taught

in lessons that doesn’t exist in real life”.

Danger awareness describes situations in which

drivers are forced to make exceptions and act in

ways that would be considered dangerous otherwise:

“sometimes it is necessary to overtake and one has to

speed up fast to do so and it [the system] can’t take

this into account. Also I have had to brake quickly

to avoid an animal/unexpected unindicated moving

across me and got marked down” (P2

c

). “If I have

to brake because a dog runs out in front of me I

shouldn’t have that go against me” (P63

p

). We hence-

forth group this issue, along with model deficiency,

under the term “big picture” problem.

Financially ineffective is how some participants

see UBI, because in their experience it never deliv-

ered the promise of a lower premium. On the contrary,

“[it is] absolutely useless and made my insurance

more expensive by default” (P42

f

), or “I have never

encountered anyone who has had their premium re-

duced” (P22

f

). This skepticism could be rooted in the

belief that insurance companies only seek increased

profits: “insurance companies are in the business of

making money, not making driving safer” (P190

p

).

Inaccurate data leads to erroneous scoring. Some

of our participants encountered loss of a GPS sig-

nal or had their telematics devices stop working for

a while: “I doubt its accuracy at times. We were told

that sometimes the link goes [down] and it can disrupt

the reading” (P63

f

).

Car sharing and ownership references were also

mentioned when pointing out limitations of UBI.

When a car is shared by multiple people, it is not al-

ways possible to attribute a score to a specific person:

“If you share a car with another person, how does UBI

know who to rate or do they just average it out. A lot

of people do share after all” (P82

p

). This can also

occur in families where the car is owned by a parent,

but driven by a child: “needs to be a system divorced

from driver ownership” (P249

p

).

Critical mass must be achieved for UBI to be ef-

fective, according to some of our participants. The

rationale is related to context, like in the case of dan-

ger awareness: “Data does not relate your driving to

that of others and how it impacts you. If all cars are

covered then UBI may be more conclusive” (P229

p

).

It can be difficult to decide whether to join UBI:

“Having never tried it or having had any experience

of it, I don’t know which I would prefer” (P114

p

).

Data portability is another potential acceptance

barrier, as tech-savvy users like P184

p

want to avoid

vendor lock-in: “portability of that data across multi-

ple UBI suppliers could also be an issue”.

Privacy concerns where explicitly named by some

participants, for example: “feels very big brother to

me, so not a fan” (P112

p

), or “do not know if my data

will be shared or mis-used, very off putting” (P88

p

).

Young drivers are seen as the group to benefit most

by some participants, because UBI can help them im-

prove their driving skills: “this is for the younger per-

son starting out on their driving life” (P143

p

).

Self-sufficiency can reduce the potential for pri-

vacy abuse, e.g.,: “a unit that can work to generate

scores without communicating” (P254

p

).

4.2 Quantitative Analysis

To test the hypotheses and answer the research ques-

tions, we applied statistical analysis. We first cleaned

the data set by discarding responses from participants

that did not provide consent, did not have a driving li-

cense at the time of participation, or have never been

Users’ Privacy Concerns and Attitudes towards Usage-based Insurance: An Empirical Approach

293

covered by car insurance. We then computed the cor-

relations between the following factors: privacy con-

cerns (PC), intention to use (IU), one’s driving style

(MS), the driving style of others (OS), the discount

in UBI (DI), the frequency with which one receives

feedback about their driving (DF), and preferences

related to collecting (CD) and sharing (SD) driving

data. Spearman and Pearson correlation was used for

ordinal and continuous factors respectively.

We set the significance level to p <= 0.05 and use

the following thresholds to define the correlations as

weak <= 0.35, moderate <= 0.67, high <= 0.89,

very high <= 0.99, or perfect 1 (Taylor, 1990). Note

that correlations can be positive or negative, thus a

correlation of -0.67 is “negative moderate”.

4.2.1 Hypotheses Testing

Prior to running our questionnaire, we formulated

several hypotheses about the participants’ attitudes to-

wards UBI. In what follows, we list these hypotheses

and explain how they were tested. Note that due to

space constraints, we do not include the detailed cal-

culations of how the latent variables below were com-

puted. However, all of the calculations are available

in the supplementary materials (see Section 3.2).

We considered several latent variables, which we

computed via 5-point Likert-scale questions. The

variables are: Intention to use (marked as IU, mea-

sured through 3 questions), Privacy concern (PC, 5

questions), preferences of sharing driving data (SD,

6 questions), preference of telematics device for col-

lecting driving data (CD, 1 question).

We then conducted an exploratory factor anal-

ysis to determine how many factors are needed to

represent each latent variable. Thus, we used the

Kaiser-Meyer-Olkin (KMO) test with a threshold of

KMO >= 0.6 (Kaiser and Rice, 1974).

Next, we computed the Pearson or Spearman cor-

relation for continuous and ordinal variables respec-

tively. Note that we treat a latent variable as continu-

ous if it can be represented by a single factor that was

computed as the mean of ordinal variables.

We now present the results for each hypothesis.

H1: Following the methodology above, we find that

the Pearson correlation between PC and IU is corr =

−0.129, p = 0.046. This indicates a weak negative re-

lationship, which suggests that participants with low

privacy concerns are more willing to be covered by

UBI. Therefore, our findings support H1.

H2: We considered the Discount, Driving feedback,

and Privacy concerns only for current and former

users, because only they have experience getting dis-

counts and driving feedback in UBI programs. Given

that these are ordinal variables, we calculated the

Spearman correlation between PC and DI (corr =

0.317, p = 0.044), and PC and DF (corr = 0.141, p =

0.379). We found a weak positive correlation between

PC and DI, while the correlation between PC and DF

is not significant. That means, people with high PC

expect to get a high discount in their UBI program.

Therefore, H2 is supported.

H3: We analyzed the users’ preference to collect their

driving data using a black box, dongle, embedded sys-

tem, or smartphone app as telematics device, as well

as the option to not collect any driving data at all. Fol-

lowing our methodology, we calculated the Spearman

correlation, resulting in the coefficients between vari-

ables depicted in Table 2

Table 2: Preference of collecting driving data using telemat-

ics device. Corr is the correlation between privacy concerns

(PC) and the preference of collecting driving data using a

particular telematics device. Note that entries in gray are

not statistically significant.

Data collection preference corr p

Do not collect data 0.283 1.407e-06

Embedded system 0.022 0.713

Dongle -0.025 0.682

Black box -0.030 0.611

Smartphone app -0.164 0.006

We found a weak positive correlation between PC

and the preference to avoid data collection, as well as

a weak negative correlation between PC and the usage

of a smartphone app as a telematics device. There-

fore, H3 is supported. Note that our results do not

show whether other types of telematics devices are

preferred, as other correlations were not significant.

Moreover, the data shows clearly that avoiding data

collection is preferred, if the option is available.

H4: We considered the users’ preference to share

their driving data with academia, a government

agency, a marketing agency, their insurer, other in-

surer, and traffic authorities. We computed the Pear-

son correlation between PC and the preference to

share driving data with the entities above, getting the

coefficients depicted in Table 3.

Table 3: Preference of sharing driving data. Corr is the

correlation between privacy concerns and the preference of

sharing driving data with a given entity.

Entity to share data with corr p

Road traffic authorities -0.197 0.001

My insurer -0.248 2.819e-05

Academic researchers -0.253 1.934e-05

Marketing companies -0.299 3.593e-07

Government agencies -0.305 2.116e-07

Other insurers -0.311 1.132e-07

We found a weak negative correlation between PC

and the willingness to share driving data with all en-

VEHITS 2022 - 8th International Conference on Vehicle Technology and Intelligent Transport Systems

294

tities above. Note that the strength of the correlation

varies, e.g., participants with high privacy concerns

are less reluctant to share data with road traffic au-

thorities, and more so when it comes to sharing with

other insurers or government agencies. For that rea-

son, H4 is not supported, because in retrospect it

is clear that the hypothesis was too optimistic. The

results show that participants with high privacy con-

cerns would rather not share data with anyone, even

their insurer.

4.2.2 Analysis of Research Questions

In this section we present our analysis for each re-

search question.

RQ-1: We considered the PC and questions related

to the preference of storage and sharing of driving

data, as well as the preference of telematics device

type. We calculated the Pearson correlation between

PC and each storage option for driving data, the re-

sults are shown in Table 4.

Table 4: Preference of driving data storage. Corr is the

correlation between privacy concerns and the preference of

storing driving data in a specific device or place. Entries in

gray are not statistically significant.

Data storage preference corr p

Dev. installed by me -0.026 0.663

Dev. installed by certified staff -0.092 0.122

Insurer -0.155 0.009

Other insurer -0.176 0.003

My phone -0.217 0.0002

The negative correlation shows that participants

with high PC are reluctant to accept the collection of

driving data regardless of storage method.

We also found that the Pearson correlation be-

tween PC and the option to participate in UBI without

storing driving data is corr = 0.215, p = 0.0003, thus

confirming the previous finding.

We also asked our participants about their pref-

erence to share driving data (e.g., speed, location,

mileage, dashcam footage, etc., see materials refer-

enced in Section 3.2 for a complete list). We found

that participants are more open to sharing their speed,

mileage, and braking behavior. Participants with high

privacy concerns are not willing to share their loca-

tion and dashcam recordings. More participants with

high privacy concerns prefer not to share their driv-

ing data (14.95%) than those with low (1.42%) and

neutral (3.56%) privacy concerns.

In addition, we computed the Pearson correlation

between PC and the preference of sharing driving data

with various entities. We found a weak negative cor-

relation between PC and all previously mentioned en-

tities (see Section 4.2.1), which suggests that partic-

ipants with low privacy concerns are more willing to

share their driving data.

We also asked our participants about their prefer-

ence to use UBI with a black box, dongle, embedded

system, or a smartphone app. We found that more

participants with high privacy concerns like to get the

benefits of UBI without any data collection.

If data collection is mandatory, participants with

low and neutral privacy concerns would prefer to use

a smartphone app as telematics device.

We conclude that participants identified as privacy

concerns the sharing and storage of their driving data,

especially when it comes to their position and dash-

cam recordings.

RQ-2: We asked participants about the most impor-

tant features of UBI in favor and against UBI. Based

on previous research and forums of UBI, we collected

features of UBI, elaborating two lists, one with the

arguments in favor (e.g., potential discount, driving

feedback, etc.), and another with arguments against

UBI (e.g., unfair ratings, age constraints, privacy con-

cerns, etc.).

We found that a discount on the next renewal in

case of getting a good driving score is the most im-

portant factor that influences a person’s decision in

favor of UBI. On the other hand, collection of my

driving data (GPS location, acceleration, etc.) and

driving rating is unfair are the most important factors

against deciding to use UBI.

Other Findings: In addition, we found a weak

positive correlation between PC and DI (corr =

0.334, p = 0.012), which suggests that participants

with high privacy concerns expect a high discount.

For driving feedback, we found that most participants

do not want to get any feedback. However, if it were

mandatory, they would like to receive it through email

or a smartphone app.

We found a weak positive correlation between the

MS-IU (corr = 0.181, p = 0.002), which suggests

that people who consider themselves good drivers are

willing to use UBI. We also found that only 8 partici-

pants out of 281 consider themselves bad drivers.

We found that participants aged between 29 and

38 have the highest privacy concerns. Also, partici-

pants under 33 are more willing to be covered by UBI.

Participants with a Master or Bachelor’s degree have

the highest privacy concerns in our sample. In terms

of occupations - employees, workers, and civil ser-

vants have the highest privacy concerns.

We did not find significant correlations between

the intention to use and the participants’ gender, the

mileage driven, the discount in UBI, the residence

country of our participants, or OS.

Users’ Privacy Concerns and Attitudes towards Usage-based Insurance: An Empirical Approach

295

5 DISCUSSION

Our findings indicate that participants with high PC

prefer not to use smartphone apps as telematics de-

vices. This could be because participants are in-

formed about potential vulnerabilities and tracking is-

sues associated with smartphones, therefore they do

not regard them as secure or private. However, this

question remains to be explored in future research.

The correlation between privacy concerns and the

expectation of a higher discount could be caused by

the fact that privacy conscious users want a fair com-

pensation for the data they share. In contrast, users

with low privacy awareness may not fully realize the

value of what they give up, hence they accept less fa-

vorable terms and have lower expectations.

Overall, our participants referred to the sharing

and collection of data as the main factors that make

them hesitate to join to UBI. The results show that

participants would be more open towards UBI if they

could take advantage of it without data collection and

sharing. It is thus possible, that a self-sufficient sys-

tem that relies on the resources of the car itself, and

does not involve third parties, could have a higher

acceptance. To the best of our knowledge, no such

solutions are available to customers at the moment.

Some researchers proposed systems that collect and

share aggregated data (H

¨

andel et al., 2013; Iqbal and

Lim, 2006; Troncoso et al., 2010), however they are

susceptible to the “big picture” problem discussed in

Section 4.1. Therefore, the design of an accurate

and auditable self-sufficient solution remains an open

question. We hypothesize that this can be achieved

by re-purposing self-driving car technology. Accord-

ing to the requirements defined by the Society of Au-

tomotive Engineers (SAE) in (SAE J3016, 2018), a

level-2 autonomous vehicle must be able to control

steering, braking and acceleration independently (i.e.,

without receiving instructions from a remote server).

Therefore, it must be aware of the environment, which

includes other cars, road markings, weather and road

conditions, etc. A re-purposed system could leverage

the same technology, but with the goal of evaluating

the driving style like an examination officer would,

rather than with the goal of driving the car. Such an

“examiner AI” could not only alleviate privacy con-

cerns, but also address the “big picture” problem.

This would be of a great benefit, because our re-

sults show that a common limitation perceived by par-

ticipants is the inability of UBI to understand the big

picture of the road conditions, thus leading to inac-

curate scores. Moreover, some users consider the

scores to be unfair, this can happen if they deviate

from the rules to prevent an accident. Such maneuvers

are penalized by the algorithm, because it is unaware

of what other agents (e.g, drivers, vehicles, pedestri-

ans, animals) were doing in the given circumstances.

Some of our participants express skepticism regarding

UBI, stating that it will be inefficient unless a critical

mass is achieved: either all vehicles must participate

in such insurance, or the algorithms must be sophis-

ticated enough to consider all relevant external fac-

tors. Since this is not feasible at the moment, a so-

lution would be to make the algorithms more tolerant

to such outlier behaviour. For example, they could

penalize drivers only if they consistently deviate from

the rules. Another possibility would be to provide an

option to dispute scores. However, this feature must

be implemented by taking into account the burden of

proof. A driver may not always have a video record-

ing to prove their innocence (e.g., in some countries

such cameras may be illegal), so it would be unfair to

penalize them if they failed to provide evidence dur-

ing the dispute. We believe that insurers are in a bet-

ter position to collect such evidence (e.g., by contact-

ing traffic safety authorities, retrieving public camera

footage, etc.), and thus the presumption of innocence

principle must be guaranteed.

The feedback collected from our participants in-

dicates that insurers are yet to make a compelling ar-

gument about why their service is unique and worth

the investment. This could make some potential users

hesitate to sign up, because UBI requires too much

commitment up-front (e.g., acquiring new hardware,

possibly modifying something in the car, etc.), with-

out the certainty that good driving will lead to a dis-

count. This is especially relevant when potential users

learn from others through word of mouth that they

have never met anyone who actually got a discount.

Therefore, we posit that there could be an entry bar-

rier that insurance companies have to bring down,

e.g., by offering the hardware for free or by leveraging

the hardware that modern cars are equipped with from

the factory, or by improving transparency and making

it easy to make accurate estimations of the discount

amount. Such transparent estimation tools could as-

sist potential users in making informed decisions.

Disagreement with the calculated driving scores

is a major concern raised by the participants. Al-

though none of them has explicitly stated they want

more transparency in this calculation, we believe that

the lack of such information could make users less

likely to perceive the scoring results as objective. Our

data show that most participants consider themselves

good drivers, so they could attribute errors to the algo-

rithm rather than to their own behaviour, thus reduc-

ing the level of satisfaction with the service. There-

fore insurers might remediate this by increasing the

VEHITS 2022 - 8th International Conference on Vehicle Technology and Intelligent Transport Systems

296

transparency of all processes, including data collec-

tion, data sharing and driving score calculation.

Data portability is another concern mentioned by

the participants. While Art. 20 of the General Data

Protection Regulation (GDPR) guarantees the right to

obtain one’s data in a “structured, commonly used and

machine-readable format and [..] to transmit those

data to another controller without hindrance”, cus-

tomers in some parts of the world do not necessarily

enjoy the same level of protection. It is therefore pos-

sible that adoption of UBI could be lower in regions

where such protections are not available.

Regarding the most important feature in favor of

UBI, the brochures of some UBI companies highlight

improving driving style and paying based on one’s

own driving style as key advantages. However, our

participants prioritized the discount on the next re-

newal, which can indicate that some users are focused

on saving money, rather than on improving their driv-

ing style. This raises a question: what is the users’

rationale for joining UBI? If the motivation is sav-

ing money, as participants remarked, this is included

in the traditional car insurance, where drivers pay

based on their historical claims. That means, even

though in traditional car insurance novice drivers have

a high insurance premium, they could pay less in the

next years if they report no incidents to the insurer.

Thus, good drivers can pay less even in traditional

insurance, hence UBI should attract users with argu-

ments other than reduced premiums. It is also possi-

ble that one’s cultural background determines the ex-

tent to which the calculated discount influences adop-

tion, however our sample is not diverse enough geo-

graphically to verify this hypothesis.

Regarding telematics devices, participants who do

not have high privacy concerns prefer to use a smart-

phone app as a telematics device if data collection

is unavoidable. This is despite usability issues that

Quintero et al. (2020) identified earlier, e.g., high bat-

tery consumption or inaccurate GPS location. This

suggests that users find smartphones appealing due to

some benefits that outweigh these issues. For exam-

ple, it could be due to (1) familiarity - they under-

stand the user interface and there is no need to learn

anything new, (2) privacy - they can turn it off when

they want (e.g., when driving to certain addresses),

(3) convenience - the smartphone is already used for

maps and navigating, (4) cost savings - there is no

need to purchase additional hardware, nor spend time

setting it up, (5) perceived trust - users are used to

storing sensitive data on their smartphones (e.g., pho-

tographs, correspondence), therefore they could also

entrust them with their driving data. However, the us-

age of smartphones can lead to security issues that

non-expert users are unaware of. Specifically, if a

device runs outdated software (e.g., no updates are

released by the manufacturer), then it could be an

easier target for attackers. Considering that only a

small portion of smartphones are running the latest

software (Quintero et al., 2020), insurers should care-

fully consider the implications of using smartphones

as telematics devices. This is especially important be-

cause driving data logs can be remotely manipulated

on a compromised smartphone, which could lead to

a higher rate of disputes. Moreover, malicious cus-

tomers could manipulate the logs themselves (e.g.,

delete data for the period when they drove aggres-

sively) in order to improve their score.

5.1 Recommendations

Based on the qualitative analysis of the feedback from

our participants (see Sec. 4.1), we recommend insur-

ers to work on improvements related to:

Car Sharing. If several family members use the same

car, or if drivers change during a road trip, UBI should

provide a way to indicate who is currently driving

the vehicle. The data from our participants shows

that such use cases are currently not handled well by

their insurers. Note that the user experience must take

into consideration the different types of telematics de-

vices. While it is possible to link several smartphones

to a car, or add a “user profiles” feature to a program

that runs on a single smartphone, this is not an option

when an embedded device is used for logging data,

unless each person can somehow “check in” before

they start driving.

Self-contained Systems that can evaluate the driving

style without sharing data with third parties or send-

ing it over a network would be a major step forward

in addressing users’ privacy concerns. Such systems

would also address the “big picture” issue, because

they provide fair scores even if not all vehicles on

the road participate in UBI. This also applies to cases

when no other vehicles are involved, e.g., a sudden

braking maneuver to avoid a collision with an animal

that crosses a street in a remote location. In such

circumstances there is no nearby infrastructure that

could provide recordings of the incident, nor are there

other cars that could have caught it on their dashcam.

A “discard trip” feature could be an alternative stop-

gap measure until self-contained systems are avail-

able. A driver could remove a trip from their history

if it involved an incident like the previously described

maneuver to avoid an animal on the road. Insurance

providers should also consider how this functionality

could be abused by drivers who use it to hide their vi-

olations. This can be addressed in different ways, e.g.,

Users’ Privacy Concerns and Attitudes towards Usage-based Insurance: An Empirical Approach

297

to limit the number of trips that can be discarded per

month, or to incur a progressively larger penalty for

each discarded trip, such that the accumulated penalty

would exceed the penalty of an incident one attempts

to conceal.

Participants’ Culture should be taken into account

at the moment of implementing UBI in a specific

country. Our findings indicate that most participants

are focused on saving money, which could be influ-

enced by the cost of living in the country of residence,

which might also influence acceptance of UBI.

Transparency. Providing users information about the

different stages in UBI (e.g., data collection, storage,

processing, etc.) could increase the transparency of

driving data handling and score calculation (Quintero

et al., 2020). Following the participants’ preference

about driving feedback, the insurers could provide

this information by Email or smartphone app. UBI

should provide clear information about how driving

data are transformed into one’s driving score.

5.2 Limitations

Our sample has a limited geographical distribution,

as 91% of the participants come from the UK and 6%

are from the USA, whereas the rest of the world adds

up to less than 3%. We are therefore unable to ob-

serve variations in attitudes towards UBI that might

be rooted in culture, or the way in which transport

infrastructure is managed in specific countries. Con-

sidering that road design influences driving behaviour

and leads to significant differences between countries

in terms of traffic safety and the severity of accidents

(Buehler and Pucher, 2017), we have reasons to be-

lieve that similar effects could apply to UBI and are

worthy of examining in future work.

In addition, we had few participants experienced

in UBI, most of them being potential users, rather

than current or former ones. This is because the rela-

tive novelty of UBI makes it difficult to recruit partic-

ipants with past experience.

6 RELATED WORKS

Aspects of UBI, such as acceptance, privacy, trans-

parency and disadvantages have been discussed by

researchers. In what follows, we summarize the find-

ings of related literature.

After comparing several distance-based insurance

programs, Litman (2007) concludes that these pro-

grams can be more beneficial for drivers and society

than for insurers. He argues that drivers could get

a lower premium by reducing the distance traveled,

thus benefiting society (e.g., less pollution, fewer ac-

cidents, etc.).

However, others did not find significant effects on

the mileage driven after using UBI for six months (So-

leymanian et al., 2019). They also found that drivers

improved their driving style during the observed pe-

riod, but it is not clear whether this is a long-lasting

effect.

Quintero et al. (2020) analyzed discussions in on-

line communities of current and former users of UBI,

and interviewed potential users. They found that

drivers may identify their mistakes based on feed-

back, and thus drive more cautiously, hence reduce

the frequency of accidents. In addition, insurers may

have a more accurate risk estimation by analysing col-

lected driving data.

The disadvantages of UBI discussed in literature

are usually related to privacy concerns, discrimina-

tion, dangerous driving, lack of transparency (e.g.,

data usage, unclear evaluation criteria), and the in-

vestment costs for the insurer (Arvidsson et al., 2011;

Derikx et al., 2016; Soleymanian et al., 2019; Quin-

tero et al., 2020). For example, drivers could pro-

voke dangerous situations while attempting to guess

how the scoring works, due to lack of algorithmic

transparency (Quintero et al., 2020). Discrimination

can occur because most UBI programs to date target

young drivers or people with little driving experience.

Privacy concerns in UBI are related to the collec-

tion of drivers’ location via GPS (Soleymanian et al.,

2019; Quintero et al., 2020). Although some UBI

programs do not use location to determine the driv-

ing score, several authors argued that privacy could

be compromised by inferring locations through com-

binations of factors like: distance traveled, speed and

time of driving, speed limits, start location or previ-

ous destinations (Dewri et al., 2013; Gao et al., 2014;

Wahlstr

¨

om et al., 2016; Bellatti et al., 2017).

Some academic solutions have been designed to

mitigate these privacy concerns, though at the time

of this writing they are not yet implemented in prac-

tice. In particular, they attempt to solve the problem

by performing all the calculations locally, and only

sending aggregated data to the insurer (H

¨

andel et al.,

2013; Iqbal and Lim, 2006; Troncoso et al., 2010).

Others examined the problem of UBI acceptance.

Mayer finds that privacy concerns do not play a

role, whereas the expected discount and hedonic

motivation on driving are important acceptance fac-

tors (Mayer, 2012). Derikx et al. (2016) find that

small financial rewards could motivate customers to

share their driving data. Tian et al. (2020) conclude

that perceived enjoyment and trust play an important

role for some age groups.

VEHITS 2022 - 8th International Conference on Vehicle Technology and Intelligent Transport Systems

298

7 CONCLUSIONS

We conducted an online survey with current, former,

and potential users of UBI, analysing their responses

through a qualitative and quantitative analysis.

The results indicate that privacy concerns arise if

driving data are stored and shared. Given the choice,

our participants would rather use self-sufficient UBI

implementations that perform all the analysis locally

and avoid sending data to the insurer or other parties.

We find that participants prioritize saving money

over improving their driving style, when it comes to

one’s perception of UBI utility. It should be noted that

no participants reported any actual savings they have

made via UBI, nor do they know anyone who has.

The issue is exacerbated by the lack of transparency of

the scoring algorithms, which made some participants

conclude that UBI is only meant to benefit insurers.

Therefore, we consider that improving transparency

should be a top priority, otherwise a growing share of

users might be disappointed, thus reducing adoption.

Based on the results, we propose several recom-

mendations for insurers, aimed at increasing UBI ac-

ceptance (see Section 5.1).

ACKNOWLEDGEMENTS

We thank Zinaida Benenson and Freya Gassmann

for their valuable comments on earlier versions of

this paper. This research has received funding from

the H2020 Marie Skłodowska-Curie EU project “Pri-

vacy&Us” under the grant agreement No 675730.

REFERENCES

Arvidsson, S. et al. (2011). Reducing asymmetric informa-

tion with usage-based automobile insurance. Swedish

National Road & Transport Research Institute (VTI),

(2010):2.

Bellatti, J., Brunner, A., Lewis, J., Annadata, P., Eltarjaman,

W., Dewri, R., and Thurimella, R. (2017). Driving

habits data: Location privacy implications and solu-

tions. IEEE Security & Privacy, 15(01):12–20.

Braun, V. and Clarke, V. (2006). Using thematic analysis in

psychology. 3(2):77–101.

Buehler, R. and Pucher, J. (2017). Trends in walking and cy-

cling safety: Recent evidence from high-income coun-

tries, with a focus on the united states and germany.

107(2):281–287.

Derikx, S., De Reuver, M., and Kroesen, M. (2016). Can

privacy concerns for insurance of connected cars be

compensated? Electronic markets, 26(1):73–81.

Dewri, R., Annadata, P., Eltarjaman, W., and Thurimella, R.

(2013). Inferring trip destinations from driving habits

data. In Proceedings of the 12th ACM workshop on

Workshop on privacy in the electronic society, pages

267–272.

Dinev, T. and Hart, P. (2006). An extended privacy calcu-

lus model for e-commerce transactions. Information

systems research, 17(1):61–80.

Gao, X., Firner, B., Sugrim, S., Kaiser-Pendergrast, V.,

Yang, Y., and Lindqvist, J. (2014). Elastic pathing:

Your speed is enough to track you. In Proceedings of

the 2014 ACM International Joint Conference on Per-

vasive and Ubiquitous Computing, pages 975–986.

H

¨

andel, P., Ohlsson, J., Ohlsson, M., Skog, I., and Nygren,

E. (2013). Smartphone-based measurement systems

for road vehicle traffic monitoring and usage-based in-

surance. IEEE systems journal, 8(4):1238–1248.

Iqbal, M. U. and Lim, S. (2006). A privacy preserving gps-

based pay-as-you-drive insurance scheme. In Sympo-

sium on GPS/GNSS (IGNSS2006), pages 17–21.

Kaiser, H. F. and Rice, J. (1974). Little jiffy, mark iv. Edu-

cational and psychological measurement, 34(1):111–

117.

Litman, T. (2007). Distance-based vehicle insurance feasi-

bility, costs and benefits. Victoria, 11.

Mayer, P. (2012). Empirical Investigations on User Percep-

tion and the Effectiveness of Persuasive Technologies.

PhD thesis, University of St. Gallen.

Quintero, J., Railean, A., and Benenson, Z. (2020). Accep-

tance factors of car insurance innovations: The case of

usage-based insurance. Journal of Traffic and Logis-

tics Engineering Vol, 8(2).

SAE J3016 (2018). Taxonomy and Definitions for Terms

Related to Driving Automation Systems for On-Road

Motor Vehicles. Standard, Society of Automotive En-

gineers (SAE).

Soleymanian, M., Weinberg, C. B., and Zhu, T. (2019). Sen-

sor data and behavioral tracking: Does usage-based

auto insurance benefit drivers? Marketing Science,

38(1):21–43.

Taylor, R. (1990). Interpretation of the correlation coeffi-

cient: a basic review. Journal of diagnostic medical

sonography, 6(1):35–39.

Tian, X., Prybutok, V. R., Mirzaei, F. H., and Dinulescu,

C. C. (2020). Millennials acceptance of insurance

telematics: An integrative empirical study. Tian, Xi-

aoguang, pages 156–181.

Troncoso, C., Danezis, G., Kosta, E., Balasch, J., and Pre-

neel, B. (2010). Pripayd: Privacy-friendly pay-as-

you-drive insurance. IEEE Transactions on Depend-

able and Secure Computing, 8(5):742–755.

Wahlstr

¨

om, J., Skog, I., Rodrigues, J. G., H

¨

andel, P., and

Aguiar, A. (2016). Map-aided dead-reckoning—a

study on locational privacy in insurance telematics.

arXiv preprint arXiv:1611.07910.

Warshaw, P. R. and Davis, F. D. (1985). Disentangling be-

havioral intention and behavioral expectation. Journal

of experimental social psychology, 21(3):213–228.

Users’ Privacy Concerns and Attitudes towards Usage-based Insurance: An Empirical Approach

299