Real-time Recommendation System for Stock Investment Decisions

Artur Bugaj and Weronika T. Adrian

a

AGH University of Science and Technology, al. A. Mickiewicza 30, 30-059 Krakow, Poland

Keywords:

Recommendation Systems, Decision Making, Collaborative Filtering, Prediction of User Behavior Patterns,

Recommendation Engine, Real-time, Knowledge Graphs, Semantic Processing.

Abstract:

Recommendation systems have become omnipresent, helping people making decisions in various areas. While

most of the systems can give accurate recommendations, their learning procedures can be time-consuming. In

some cases, this is not permissible; for example when the information about the items and users changes

very fast in time. In this paper, we discuss a new recommendation engine, based on labelled property graph

knowledge representation and attributed network embeddings, which calculates real-time recommendations

for stock investment decisions. In particular, we demonstrate an application of the DANE (dynamic attributed

network embedding) framework proposed by Li et al. and show the promising results of the system.

1 INTRODUCTION

Making choices among available options – regardless

if we look for an interesting book or want to make

an investment decision – is significantly determined

by the context in which we operate: the possibilities

we have, our interests, and the previous decisions we

made. Sometimes, our own history of choices may be

limiting, so recommendations based on other people

behaviour and outcomes may be a valuable option that

widens the horizons of our analysis. A particular de-

cision setting is a situation in which we have to make

decisions quicker than usual, and at the same time,

we do not have enough resources to determine what

will be the optimal choice, or if the choice we claim

the best will be optimal in the near future. To obtain

a fast and relatively accurate recommendations, we

need a system that adapts quickly to changing data.

Recommendation systems (Bouraga et al., 2014)

have been around for a few decades, but the rapid

growth of the information stored on the Web, sparked

a renewed interest in their improvements. Ever-

changing data to be analyzed poses a challenge for

real-time systems that must balance the accuracy of

recommendations with the speed of response. In the

field of stock market, prices and forecasts can change

daily and the investors’ activity is dynamic in its na-

ture – they buy or sell stocks or even change fields

of interest. It is thus important to recognize which

and how these factors should be taken into consid-

a

https://orcid.org/0000-0002-1860-6989

eration to deliver fast and accurate recommendation

for a user that wants to make a good investment deci-

sion (Hern

´

andez-Nieves et al., 2020).

In this paper, we propose a recommendation en-

gine for stock market that integrates semantic similar-

ity assessment among investors, to incorporate their

behaviour and areas of interest, with a technical anal-

ysis of the companies considered for investment. By

bringing in the benefits of collaborative filtering and

content-based recommendation, we improve the ac-

curacy of the system’s suggestions. This paper is or-

ganized as follows: in Section 2, we present the ba-

sic concepts and background, Section 3 describes the

proposal and recent results, and we conclude the pa-

per in Section 4.

2 PRELIMINARIES

Recommendation systems can be generally catego-

rized into collaborative filtering (CF)-based (ones that

take into consideration similarities among the sys-

tem’s users), content-based (that rely on considered

items’ attributes) and hybrid that aim to bring in to-

gether the advantages of both approaches and min-

imize their limitations. In recent years, knowledge

graphs have been widely adopted as a side informa-

tion resource for recommendation engines, as they on

the one hand minimize the threat of a “cold start” in

the systems, and on the other – provide a useful mean

for recommendation explanations (for a detailed sur-

490

Bugaj, A. and Adrian, W.

Real-time Recommendation System for Stock Investment Decisions.

DOI: 10.5220/0010714900003058

In Proceedings of the 17th International Conference on Web Information Systems and Technologies (WEBIST 2021), pages 490-493

ISBN: 978-989-758-536-4; ISSN: 2184-3252

Copyright

c

2021 by SCITEPRESS – Science and Technology Publications, Lda. All rights reser ved

vey see (Guo et al., 2020; Liu and Duan, 2021)).

Graph representations, although intuitive, expres-

sive and flexible, do not constitute a good input to

various data mining tasks, such as node classifica-

tion, link prediction or community detection. To this

end, various methods for learning numerical represen-

tations of nodes, edges and subgraphs have been put

forward (Perozzi et al., 2014; Tang et al., 2015). The

assumptions of the underlying graphs differ: some of

these embedding methods are only suitable for ho-

mogeneous networks (i.e., graphs with nodes “of the

same kind”), other allow for various node types, but

only one sort of edges etc. Most of the methods as-

sume a static structure to be learned and only some

of the recent proposals have considered dynamically

changing networks. In particular, Li et al. (Li et al.,

2017) have proposed a framework for dynamic at-

tributed networks embedding that addresses both the

rich set of attributes being associated with nodes in a

graph and a dynamic nature of it (addition deletion of

nodes and edges).

3 SYSTEM PROPOSAL AND

IMPLEMENTATION

Our proposal utilizes the attributed network embed-

ding concept described in (Li et al., 2017). We model

the domain of investors and their stock decision with

a labelled property graph that is later appropriately

queried for a given user, and the obtained subgraph is

embedded onto a low-dimensional vector space with

the so-called consensus embedding. Once we obtain

the suggestions for potential companies to invest in,

we incorporate the technical analysis of the candidate

stocks to produce the final recommendations in near

real-time. The system consist of two modules:

• recommendation-engine: a module that calcu-

lates recommendations based on users similarity

(common relationships and attributes), and

• data-provider: a module that calculates current

stock movement score (i.e., if a price is predicted

to grow, to fall, or to stay the same).

Investors and their data, gathered from Investor

Hunt

1

and Nasdaq

2

services, are stored in a graph

database (see Fig. 1). The model contains four types

of nodes:

1. Investors,

2. Categories,

1

See https://investorhunt.co/.

2

See https://www.nasdaq.com/.

3. Industries,

4. Stocks,

linked with the following relationships:

1. (Investor)-[:POSSESS]-(Stock),

2. (Investor)-[:INTERESTED]-(Category),

3. (Category)-[:INCLUDES]-(Industry),

4. (Industry)-[:COMPANY]-(Companies),

The recommendation system works in three consecu-

tive phases that are:

1. Candidate Selection, in which the system fetches

a subgraph related to the target user from the

database. It ensures that further processing is

done on most similar investors.

2. Scoring: similarity matrices for nodes in the

fetched subgraph are created, in order to create

their embeddings and to find correlations between

them (here goes the actual implementation of con-

sensus embedding)

3. Re-ranking: after computing the recommenda-

tions, we add scores dependent on other factors,

which are important, but could not be retrieved

with previous steps.

In the following subsection, we discuss the details of

the process.

3.1 Candidate Selection

The first phase of the process is finding the most sim-

ilar investors according to the graph database struc-

ture. Consequently, we reduce the number of similar

investors and stocks significantly, using only a single

query that reduces searching to subgraph of related

nodes. Such a subgraph is shown on Figure 1. It is a

result of a parametrized query, where the parameter is

a target investor ID. We expect most similar investors

as those, which we can find as having some common

companies as well as some common interests.

We fetch only the necessary data, which optimizes

the performance of the database; the common cat-

egories with the target investor and the stocks they

have. To simplify a whole process, graph data is

“mapped” into set of records, which are sorted by

amount of common companies. We can fetch all in-

vestors, or limit a number of retrieved record to some

constant number. It can potentially reduce some valu-

able data, but taking into account further calculations,

we get much more speed by sacrificing only a little

of data (in Subsec. 3.2, we describe a part of the rec-

ommendation engine algorithm, where we create sim-

ilarity matrices, calculation of which is O(n

2

)).

Real-time Recommendation System for Stock Investment Decisions

491

Figure 1: Subgraph selected in Candidate selection phase.

3.2 Scoring

After selecting a subset of the most similar investors,

we prepare the data to be used in further recommen-

dations, which are done according to the method pro-

posed in (Li et al., 2017). We take into account the

data that we have fetched in the previous step, that

is, common categories of the stocks that investors are

interested in and the companies they currently have.

We create similarity matrices for them. Since data we

have are actually collections, we can calculate simi-

larity of collections (sets) with Jaccobi similarity met-

ric. In our case, where stocks and categories are rep-

resented as nodes, this is the best way to map them

into matrices. Let us denote similarity matrices for

categories and stocks as C

n×n

and S

n×n

. Let us also

denote D

C

, D

S

and L

C

, L

S

as diagonal and Laplacian

matrices created from C and S, respectively. We cal-

culate D

C

(and D

S

) as

D

C

=

∑

n

i=1

M

C

(1,i) ··· 0

.

.

.

.

.

.

.

.

.

0 ···

∑

n

i=1

M

C

(n,i)

0

and L

C

(and L

S

) as

L

C

= D

C

− M

C

Then, we normalize Laplacian matrix, from which

we will calculate eigen decomposition problem.

L

Anorm

=

∑

n

i=1

A(1,i)−A(1,1)

∑

n

i=1

A(1,i)

···

A(1,n)

∑

n

i=1

A(1,i)

.

.

.

.

.

.

.

.

.

A(n,1)

∑

n

i=1

A(n,i)

···

∑

n

i=1

A(n,i)−A(n,n)

∑

n

i=1

A(n,i)

(1)

Then, we make other calculations of Offline

Model of DANE (Li et al., 2017), which is the eigen

decomposition problem mentioned earlier, and inter-

mediate embeddings, which we denote as Y

C

(for cat-

egories) and Y

S

(for stocks):

L

Anorm

v = λv

Y

C

,Y

S

= [c

2

,...,c

k

,c

k+1

],[s

2

,...,s

k

,s

k+1

]

(2)

Result of Y

C

and Y

S

is a [c

2

,...,c

k

] and [s

2

,...,s

k

],

where c

k

and s

k

is a vector representing similarity

between target investor, and k

th

investor according

to companies, and categories, repectively. As those

vectors have been obtained with eigen decomposi-

tion, they are eigenvectors of normalized Laplacian

matrix. After eigen decomposition and getting top-

k eigen vectors we maximize correlation between in-

termediate embeddings Y

C

and Y

S

, and therefore we

solve eigen decomposition problem for:

Y

C

Y

0

C

Y

C

Y

0

S

Y

S

Y

0

C

Y

S

Y

0

S

p

C

p

S

= γ

Y

C

Y

0

C

Y

C

Y

0

S

Y

S

Y

0

C

Y

S

Y

0

S

p

C

p

S

(3)

We obtain the final result with

Y =

Y

C

,Y

S

× P (4)

where P = [p

C

; p

S

] is a top l eigenvectors from Eq. 3.

Once we have calculated the most similar investors,

we can check which companies could be potentially

most interesting for target investor. Let us denote the

similarity of investor i as s

i

and investor i’s stocks set

as I

i

= {s

1

,s

2

,...,s

l

}. Then:

r

investor

=

n

∑

i=1

(

0 s /∈ I

i

s

i

s ∈ I

i

(5)

where r

investor

is a similarity result for stock basing on

investors’ similarity.

3.3 Re-ranking

After calculation of the most similar stocks accord-

ing to similarity of investors (r

investors

), we re-rank

those stocks, according to the price forecasts. The

price forecasts are calculated in another module, in

which we predict the price movements with technical

analysis. Let us denote this as r

f orecast

. We calcu-

late r

f orecast

based on several technical analysis algo-

rithms of current stock movement, such as: Detection

of support/resistance of price, RSI, and OBV. Such a

calculation allows us to estimate (with some proba-

bility) future movement of specified stock price. We

want to recommend stocks which can grow in near

future, and advice against those, whose price can fall.

Therefore, the final recommendation is calculated as:

r

stock

= r

investors

+ r

f orecast

(6)

In this way, target user can get recommendations not

necessarily from their target of interest, but they can

see more stocks, which can lead to profits.

WEBIST 2021 - 17th International Conference on Web Information Systems and Technologies

492

3.4 Update

In (Li et al., 2017), only eigenvalues and correspond-

ing eigenvectors are updated, which increases the ef-

ficiency of the solution. This is possible, when we

take into account whole knowledge graph. We are

guaranteed, that indexes of columns on intermediate

and consensus embedding will not change. However,

with such an approach, the first step will be incredibly

slow, as creation of similarity matrix, and eigen deco-

mopsition are computationally complex calculations.

As we mentioned in Sect. 3.1, we fetch a sub-

graph. If we assume, that relations between nodes

changes in time, we can get different set of investors,

in different order (a record mentioned in 3.1 refers to

one investor’s data), what implies the fact, that the

similarity matrices can have different sizes, and the

calculated properties can be related to different nodes

in consecutive iterations. Therefore, we cannot make

any updates, as it is proposed in (Li et al., 2017). Due

to this setting, we have to repeat the whole procedure

of calculation of eigendecomposition per each itera-

tion, however, it is still a fast computation.

3.5 Results and Discussion

We have evaluated our proposal on the data scrapped

from Investor Hunt and Nasdaq services: in total,

1368 investors with their business categories interests,

amount of investments and average transaction value,

and 545 companies. As an evaluation criterion, we

state that a recommended stock have to occur mini-

mum 6 times in top 40% most similar investors. Low-

ering the relevancy criterion would decrease this ac-

cordingly. We compared our results to ones obtained

with alternative embedding algorithms, such as Deep-

Walk (Perozzi et al., 2014) and LINE (Tang et al.,

2015). The results are shown in Tables 1 and 2. They

could be better, if we consider whole graph in cal-

culations instead of subgraph, but it would affect the

response speed simultaneously.

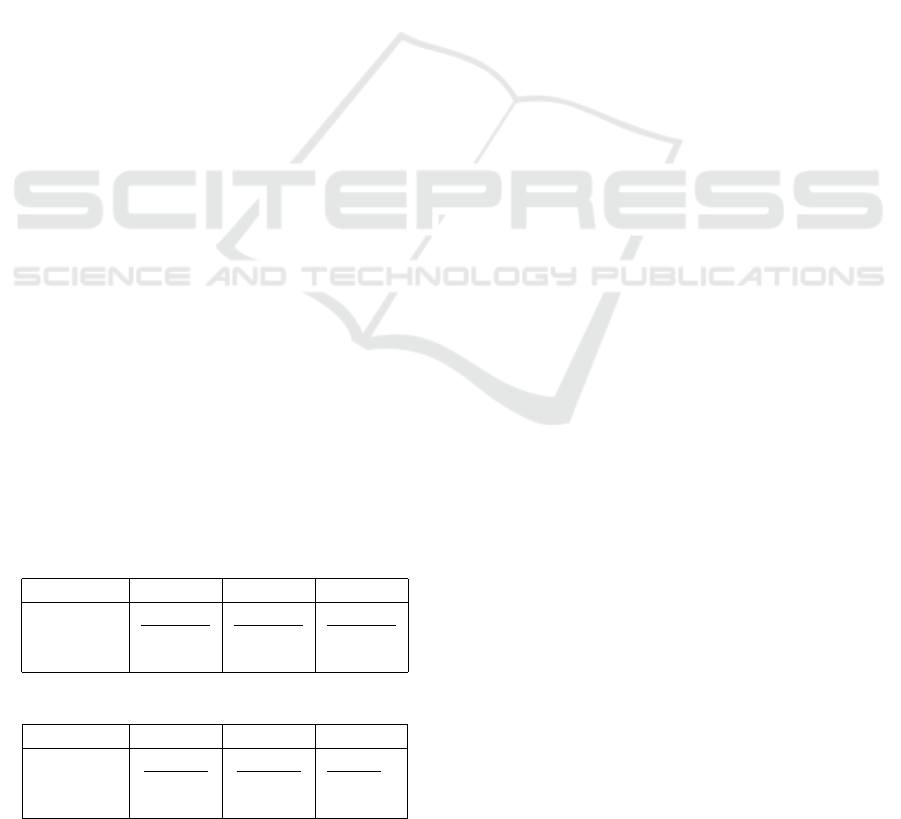

Table 1: Comparison of precision@k.

Top@10 Top@25 Top@50

DANE 63,33% 52,67% 31,67%

DeepWalk 25% 24% 21%

LINE 30% 32% 19%

Table 2: Comparison of recall@k.

Top@10 Top@25 Top@50

DANE 63,33% 85,47% 97,9%

DeepWalk 25% 27,67% 49, 17%

LINE 30% 58,88% 71,67%

4 CONCLUSION

In this paper, we addressed the challenge of real-time

recommendation for stock market. We discussed a

new system for investment recommendation based on

attributed network embeddings and technical analy-

sis of stocks. Our recommendation engine provides

fast and robust computation of recommendations for

the investment decisions, based on joint analysis of

similarity of investors and stock predictions. The re-

sults obtained so far are promising and motivating for

further exploration and a broader evaluation of the ap-

proach, covering also the technical analysis.

REFERENCES

Bouraga, S., Jureta, I., Faulkner, S., and Herssens, C.

(2014). Knowledge-based recommendation systems:

A survey. International Journal of Intelligent Infor-

mation Technologies (IJIIT), 10(2):1–19.

Guo, Q., Zhuang, F., Qin, C., Zhu, H., Xie, X., Xiong, H.,

and He, Q. (2020). A survey on knowledge graph-

based recommender systems. IEEE Transactions on

Knowledge and Data Engineering.

Hern

´

andez-Nieves, E., del Canto,

´

A. B., Chamoso-Santos,

P., de la Prieta-Pintado, F., and Corchado-Rodr

´

ıguez,

J. M. (2020). A machine learning platform for stock

investment recommendation systems. In International

Symposium on Distributed Computing and Artificial

Intelligence, pages 303–313. Springer.

Li, J., Dani, H., Hu, X., Tang, J., Chang, Y., and Liu, H.

(2017). Attributed network embedding for learning in

a dynamic environment. In Proceedings of the 2017

ACM on Conference on Information and Knowledge

Management, pages 387–396.

Liu, J. and Duan, L. (2021). A survey on knowledge

graph-based recommender systems. In 2021 IEEE

5th Advanced Information Technology, Electronic and

Automation Control Conference (IAEAC), volume 5,

pages 2450–2453.

Perozzi, B., Al-Rfou, R., and Skiena, S. (2014). Deepwalk:

Online learning of social representations. In Proceed-

ings of the 20th ACM SIGKDD international confer-

ence on Knowledge discovery and data mining, pages

701–710.

Tang, J., Qu, M., Wang, M., Zhang, M., Yan, J., and Mei,

Q. (2015). Line: Large-scale information network em-

bedding. In Proceedings of the 24th international con-

ference on world wide web, pages 1067–1077.

Real-time Recommendation System for Stock Investment Decisions

493